1 Blending Grants and Loans Getting the Most out of the Global Financing Architecture Amar...

15

1 Blending Grants and Blending Grants and Loans Loans Getting the Most out of the Global Financing Getting the Most out of the Global Financing Architecture Architecture Amar Bhattacharya Amar Bhattacharya Conference on Marketplace on Innovative Financial Conference on Marketplace on Innovative Financial Solutions for Development Solutions for Development Blending Grants and Loans Session Blending Grants and Loans Session Thursday, March 4 Thursday, March 4 Paris, France Paris, France

-

Upload

bertha-randall -

Category

Documents

-

view

215 -

download

2

Transcript of 1 Blending Grants and Loans Getting the Most out of the Global Financing Architecture Amar...

1

Blending Grants and Blending Grants and LoansLoans

Getting the Most out of the Global Getting the Most out of the Global Financing ArchitectureFinancing Architecture

Amar BhattacharyaAmar BhattacharyaConference on Marketplace on Innovative Financial Conference on Marketplace on Innovative Financial

Solutions for DevelopmentSolutions for DevelopmentBlending Grants and Loans Session Blending Grants and Loans Session

Thursday, March 4 Thursday, March 4 Paris, FranceParis, France

2

ContextContext

Improved growth performance and Improved growth performance and debt sustainability across both debt sustainability across both middle and low-income countriesmiddle and low-income countries

Persistence of development gaps Persistence of development gaps some warranting concessional some warranting concessional financingfinancing

Unmet global public goods linked Unmet global public goods linked often to domestic public goodsoften to domestic public goods

3

Strong Growth Across the Strong Growth Across the Developing WorldDeveloping World

Average Growth Number of Countries

2003-2008 >6 4-6 <4

MICs 5.7 28 39 19

LICs 5.1 20 15 13

4

Average Annual GDP Growth in sub-Average Annual GDP Growth in sub-Saharan, 1996-2005Saharan, 1996-2005

(Percent)(Percent)

-5 0 5 10 15 20 25

Zimbabwe

Guinea-Bissau

Central African Republic

Cote d'Ivoire

Eritrea

Kenya

South Africa

Madagascar

Malawi

Zambia

Guinea

Gambia, The

Ghana

Mauritania

Mauritius

Tanzania

Mali

Uganda

Mozambique

Congo, Rep

Cameroon

Angola

Equatorial Guinea

Source:: WDI, WB

5

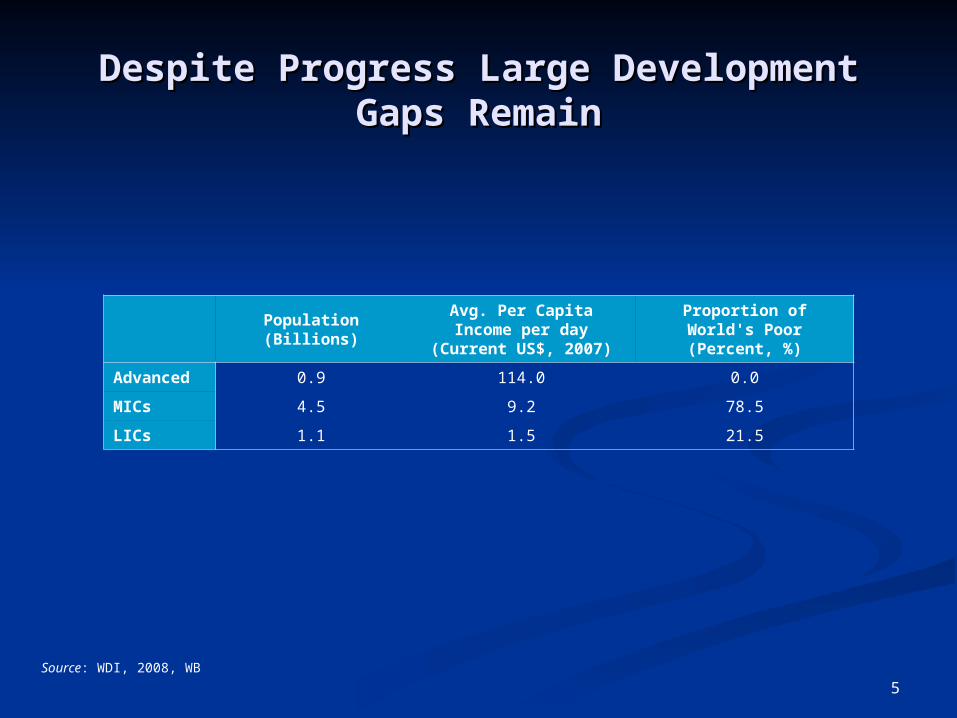

Despite Progress Large Development Despite Progress Large Development Gaps RemainGaps Remain

Population (Billions)

Avg. Per Capita Income per day

(Current US$, 2007)

Proportion of World's Poor (Percent, %)

Advanced 0.9 114.0 0.0

MICs 4.5 9.2 78.5

LICs 1.1 1.5 21.5

Source: WDI, 2008, WB

6

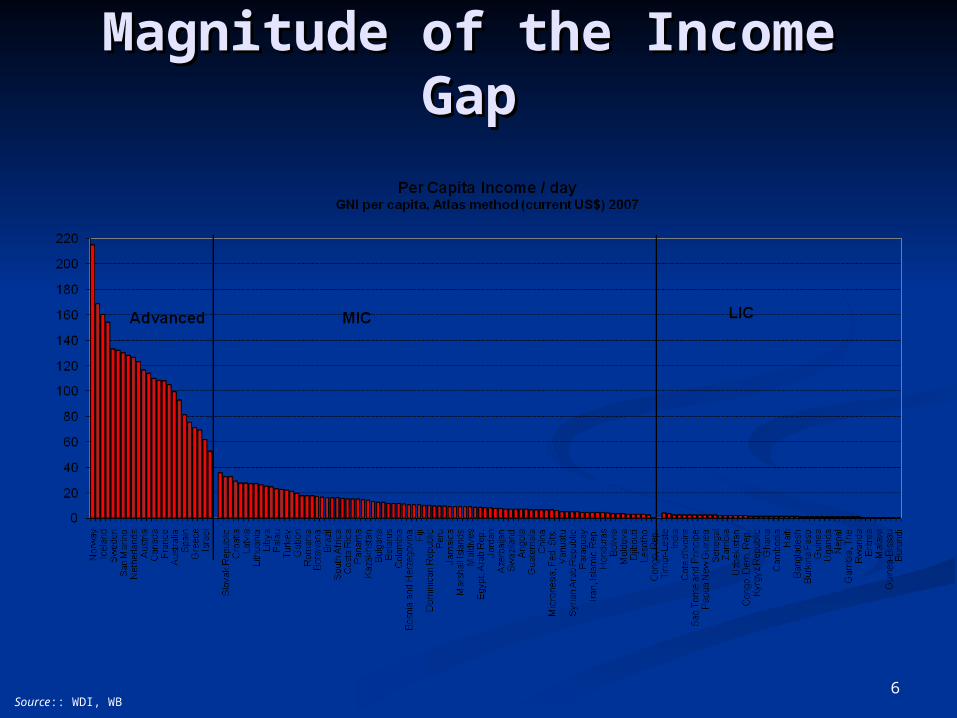

Magnitude of the Income Magnitude of the Income GapGap

Source:: WDI, WB

7

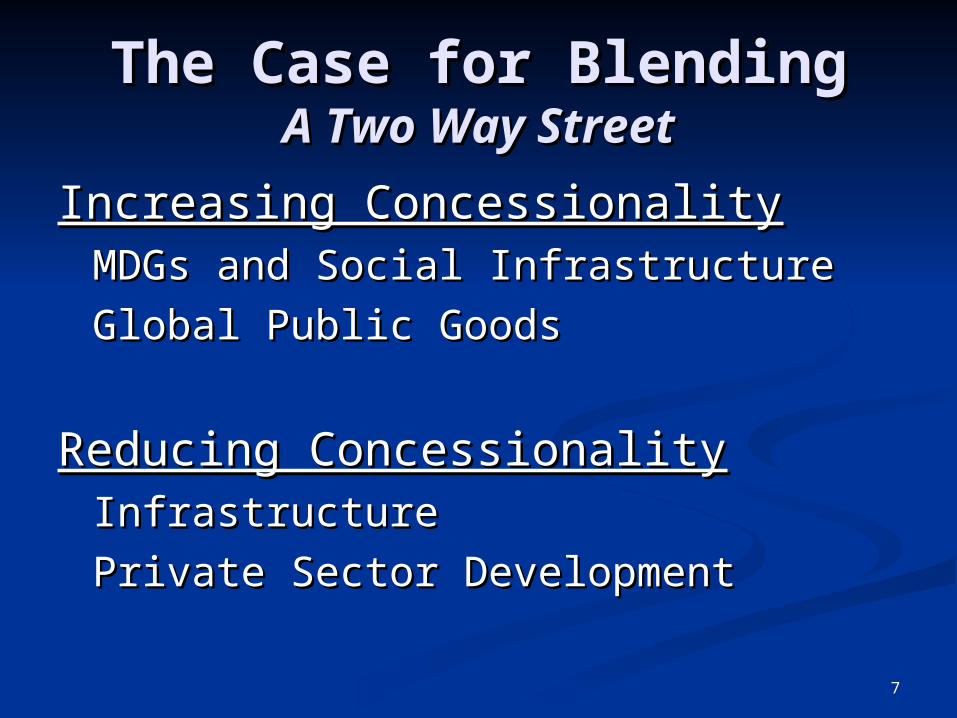

The Case for BlendingThe Case for BlendingA Two Way StreetA Two Way Street

Increasing ConcessionalityIncreasing ConcessionalityMDGs and Social InfrastructureMDGs and Social Infrastructure

Global Public GoodsGlobal Public Goods

Reducing ConcessionalityReducing ConcessionalityInfrastructureInfrastructure

Private Sector DevelopmentPrivate Sector Development

8

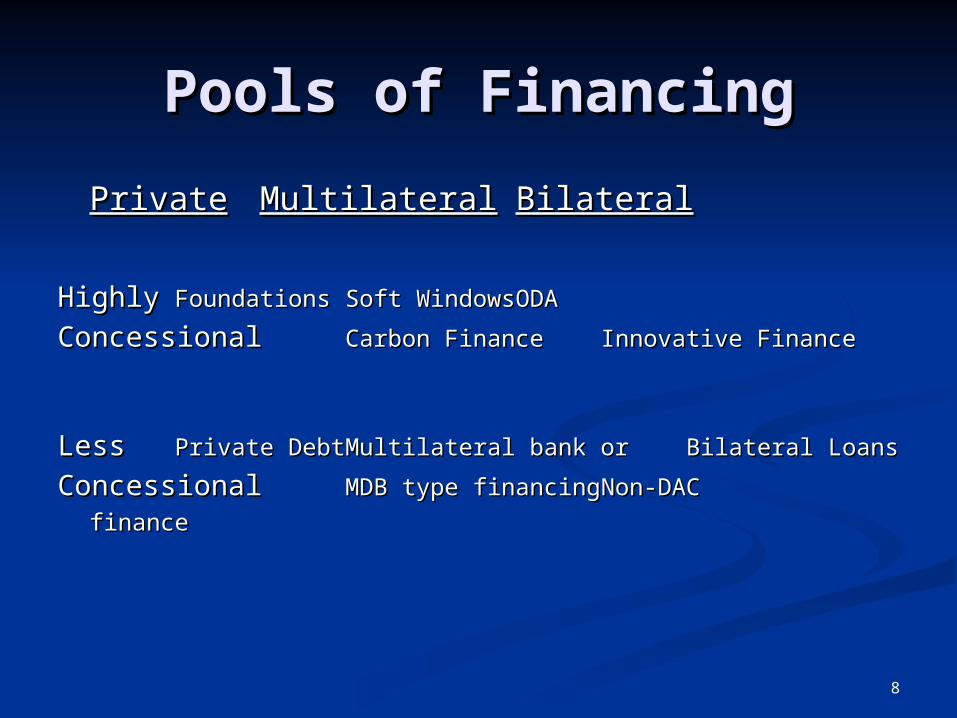

Pools of FinancingPools of Financing

PrivatePrivate MultilateralMultilateralBilateralBilateral

HighlyHighly FoundationsFoundations Soft WindowsSoft Windows ODAODA

ConcessionalConcessional Carbon FinanceCarbon Finance Innovative FinanceInnovative Finance

LessLess Private DebtPrivate Debt Multilateral bank orMultilateral bank or Bilateral Bilateral LoansLoans

ConcessionalConcessional MDB type financingMDB type financing Non-DAC Non-DAC

financefinance

99

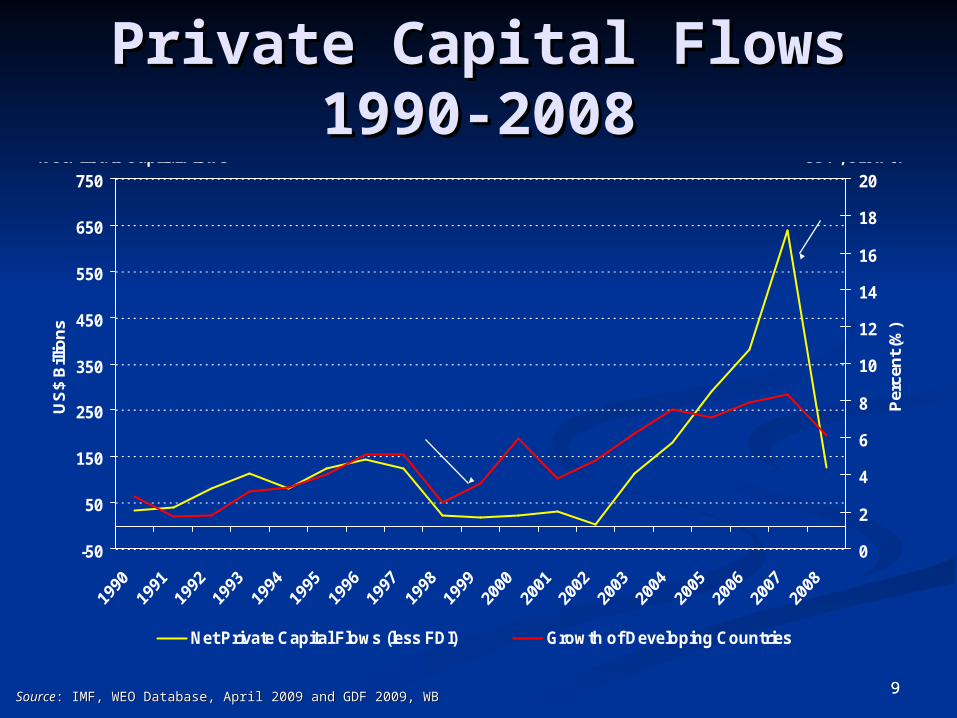

Private Capital FlowsPrivate Capital Flows1990-20081990-2008

-50

50

150

250

350

450

550

650

750

US

$ B

illio

ns

0

2

4

6

8

10

12

14

16

18

20

Per

cen

t (%

)

Net Private Capital Flows (less FDI) Growth of Developing Countries

Net Private Capital Flows GDP, Growth

2008 Financial Crisis

Asian/DotCom Crisis

SourceSource: IMF, WEO Database, April 2009 and GDF 2009, WB: IMF, WEO Database, April 2009 and GDF 2009, WB

1010

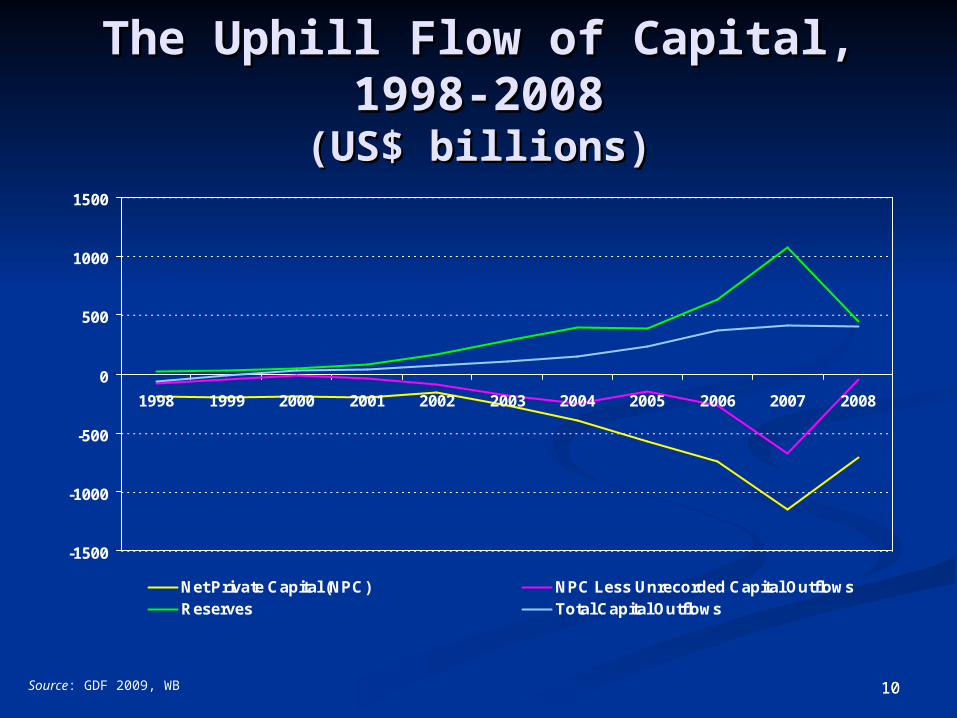

The Uphill Flow of Capital, The Uphill Flow of Capital, 1998-20081998-2008

(US$ billions)(US$ billions)

-1500

-1000

-500

0

500

1000

1500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Net Private Capital (NPC) NPC Less Unrecorded Capital OutflowsReserves Total Capital Outflows

Source: GDF 2009, WB

11

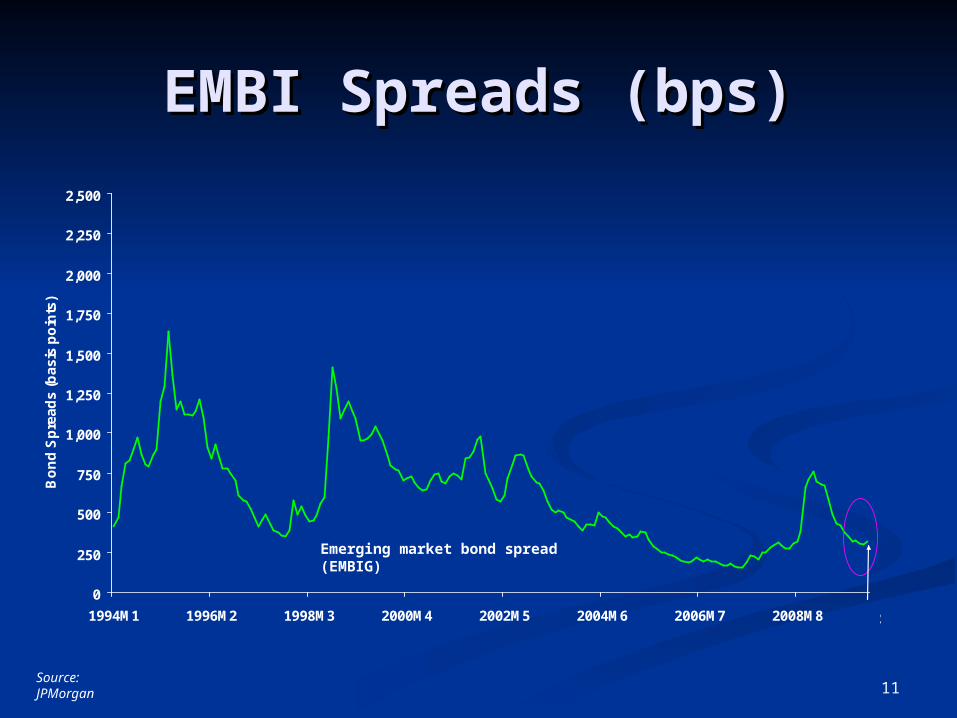

EMBI Spreads (bps)EMBI Spreads (bps)

Source: JPMorgan

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2,250

2,500

1994M1 1996M2 1998M3 2000M4 2002M5 2004M6 2006M7 2008M8

Bo

nd

Sp

rea

ds

(b

as

is p

oin

ts)

2010M2

Emerging market bond spread (EMBIG)

12

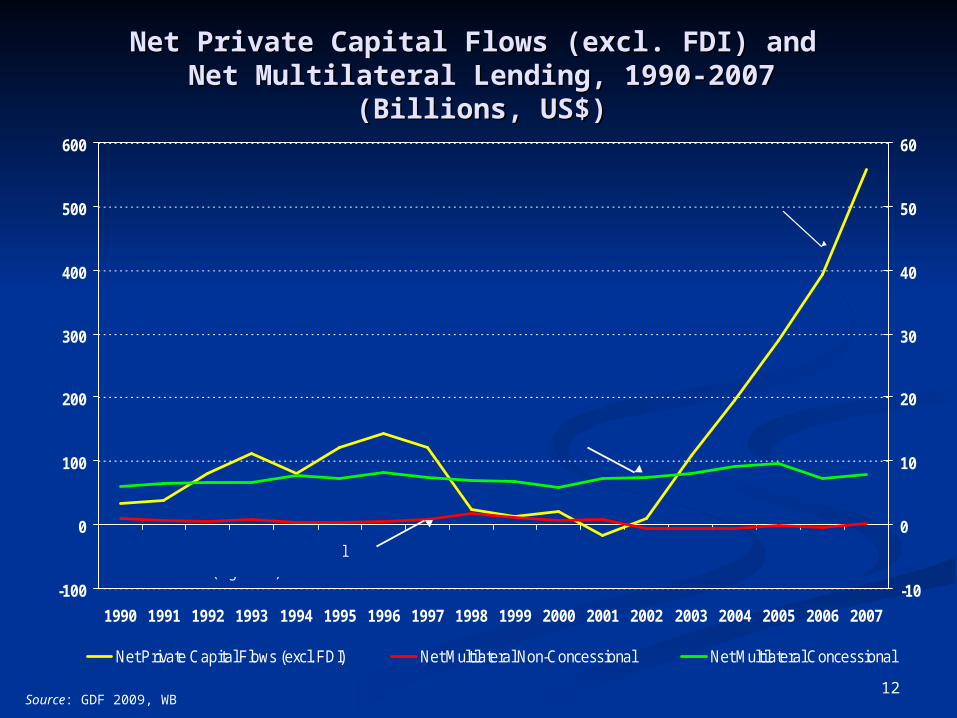

Net Private Capital Flows (excl. FDI) and Net Private Capital Flows (excl. FDI) and Net Multilateral Lending, 1990-2007Net Multilateral Lending, 1990-2007

(Billions, US$)(Billions, US$)

-100

0

100

200

300

400

500

600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

-10

0

10

20

30

40

50

60

Net Private Capital Flows (excl. FDI) Net Multilateral Non-Concessional Net Multilateral Concessional

Net private Capital Flows(Left axis)

Net Multilateral Concessional(Right axis)

Net Multilateral Non-Concessional (Right axis)

Source: GDF 2009, WB

13

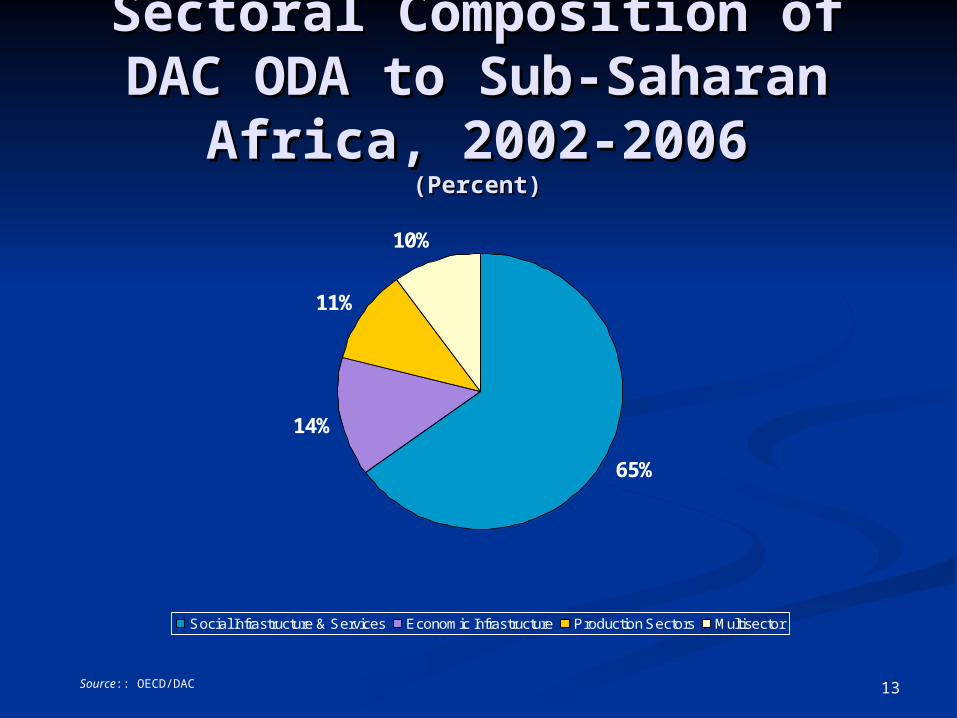

Sectoral Composition of Sectoral Composition of DAC ODA to Sub-Saharan DAC ODA to Sub-Saharan

Africa, 2002-2006Africa, 2002-2006(Percent)(Percent)

65%

14%

11%

10%

Social Infrastructure & Services Economic Infrastructure Production Sectors Multisector

Source:: OECD/DAC

14

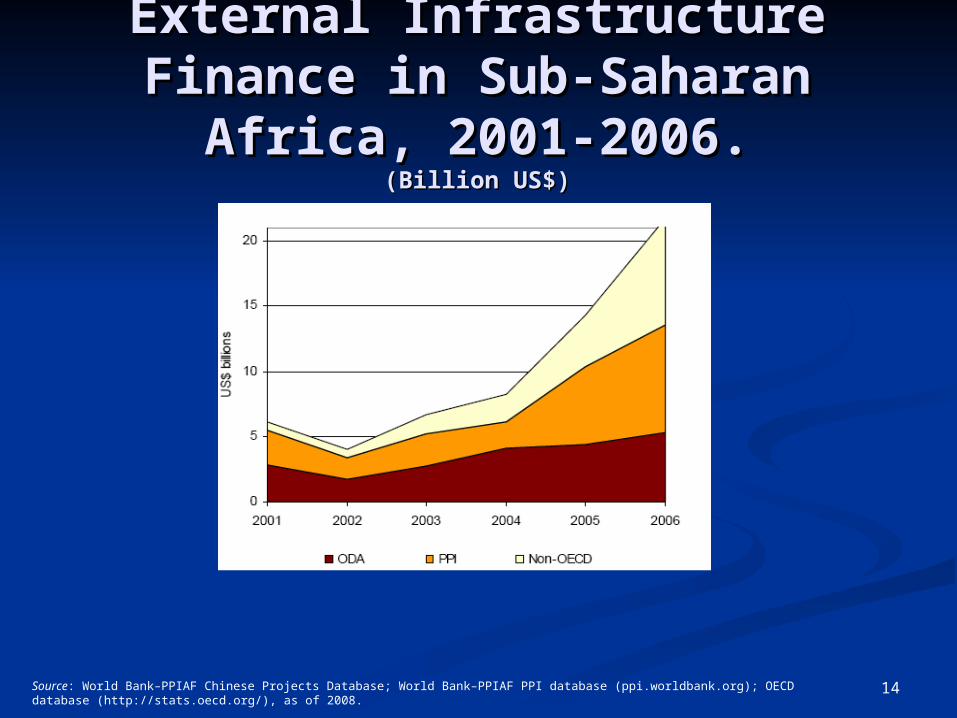

ExternalExternal Infrastructure Infrastructure Finance in Finance in SubSub--SaharanSaharan

AfricaAfrica, 2001-2006., 2001-2006.(Billion US$)(Billion US$)

Source: World Bank–PPIAF Chinese Projects Database; World Bank–PPIAF PPI database (ppi.worldbank.org); OECD database (http://stats.oecd.org/), as of 2008.

15

Concluding ThoughtsConcluding Thoughts Private debt flows can make important development Private debt flows can make important development

contribution but tend to be concentrated, volatile and contribution but tend to be concentrated, volatile and subject to high risk premiasubject to high risk premia

MDB model provides arguably the most important MDB model provides arguably the most important means for harnessing stable market based finance for means for harnessing stable market based finance for development but has been greatly under-utlized in development but has been greatly under-utlized in recent yearsrecent years

Lessons from Climate Investment FundsLessons from Climate Investment Funds Complementarities between DAC and non-DAC Complementarities between DAC and non-DAC

financingfinancing Time to resuccitate bilateral loans?Time to resuccitate bilateral loans? Synergies extend beyond leverage and concessionalitySynergies extend beyond leverage and concessionality