1 Applied Business Statistics Case studies Basel II - Introduction Mauro Bufano Risk Management –...

23

1 Applied Business Applied Business Statistics Statistics Case studies Case studies Basel II - Introduction Basel II - Introduction Mauro Bufano Mauro Bufano Risk Management – Risk Management – Banca Banca Mediolanum Spa Mediolanum Spa

-

Upload

margery-harrison -

Category

Documents

-

view

219 -

download

1

Transcript of 1 Applied Business Statistics Case studies Basel II - Introduction Mauro Bufano Risk Management –...

11

Applied Business StatisticsApplied Business StatisticsCase studiesCase studies

Basel II - IntroductionBasel II - Introduction

Mauro BufanoMauro Bufano

Risk Management – Risk Management – BancaBanca Mediolanum Spa Mediolanum Spa

22

Basel II – motivationsBasel II – motivations In a market economy, every company is free to In a market economy, every company is free to

determine its own capital, basing on shareholders’ determine its own capital, basing on shareholders’ preferencespreferences

This is not true for banks! Financial institutions have This is not true for banks! Financial institutions have minimum capital requirements imposed by regulators. minimum capital requirements imposed by regulators.

Why?Why?

a)a) Centrality of banks in the overall economyCentrality of banks in the overall economyb)b) Contagion effect: a bank’s default can affect the entire Contagion effect: a bank’s default can affect the entire

economic system (see Lehman Brothers 2008)economic system (see Lehman Brothers 2008)c)c) In banks’ liabilities we have families’ savings (in many In banks’ liabilities we have families’ savings (in many

cases, with a State guarantee within a limit)cases, with a State guarantee within a limit)d)d) How much does it cost to save banks from default?How much does it cost to save banks from default?

33

Basel I agreement-1988Basel I agreement-1988

The first international agreement on banks’ capital was The first international agreement on banks’ capital was made in 1988 by the “Basel committee” it’s an made in 1988 by the “Basel committee” it’s an international institution established in 1974 by the G10 international institution established in 1974 by the G10 countries. It reports directly to the Central Banks of G10countries. It reports directly to the Central Banks of G10

The main reasons of this agreement were:The main reasons of this agreement were: To prevent banks’ crisis, avoiding excessive risk takingTo prevent banks’ crisis, avoiding excessive risk taking To harmonize different capital requirements in developed To harmonize different capital requirements in developed

countries, that could have caused distortions in the marketcountries, that could have caused distortions in the market To ensure financial stability of the banks, impacting directly on To ensure financial stability of the banks, impacting directly on

consolidated balance sheetconsolidated balance sheet

44

Basel I agreement-1988Basel I agreement-1988 The first agreement regulated only capital requirements on The first agreement regulated only capital requirements on credit credit

riskrisk, by applying the rule of “8%”, by applying the rule of “8%” The regulatory capital had to be at least 8% of the risk weighted The regulatory capital had to be at least 8% of the risk weighted

assetsassets

Regulatory capital Regulatory capital constituted by:constituted by: Tier I capital: share capital, disclosed reserves, general provisions, Tier I capital: share capital, disclosed reserves, general provisions,

innovative capital instrumentsinnovative capital instruments Tier II capital: undisclosed and revaluation reserves, hybrid capital Tier II capital: undisclosed and revaluation reserves, hybrid capital

instruments and subordinated debtinstruments and subordinated debt Tier III capital (from 1996): short term subordinated debt covers Tier III capital (from 1996): short term subordinated debt covers

only market risk, was not present in the first agreementonly market risk, was not present in the first agreement

%8capital Regulatory

ratio Capital i

iiwA

55

The 1988 agreement had some “weights” in order to determine “risk The 1988 agreement had some “weights” in order to determine “risk weighted assets”weighted assets”

a)a) wwii =0% for cash and exposure vs central governments, central =0% for cash and exposure vs central governments, central

banks and EUbanks and EU

b)b) wwii =20% for exposures vs banks and public sector =20% for exposures vs banks and public sector

c)c) wwii =50% for mortgage loans =50% for mortgage loans

d)d) wwii =100% for private sector exposures, equities, subordinated =100% for private sector exposures, equities, subordinated

loans, hybrid instrumentsloans, hybrid instruments Problems:Problems:

• There was few or no differentiation of exposures at allThere was few or no differentiation of exposures at all

• It encouraged “regulatory arbitrages”It encouraged “regulatory arbitrages”

• It didn’t take into account many other risks present in banks’ It didn’t take into account many other risks present in banks’ business (market risk, operational risk and so on)business (market risk, operational risk and so on)

Basel I agreement-1988Basel I agreement-1988

66

Basel II agreement - 2004Basel II agreement - 2004 Basel II agreements in 2004 is a more complex one than its “parent” in Basel II agreements in 2004 is a more complex one than its “parent” in

19881988 It’s based on 3 pillars:It’s based on 3 pillars:

1.1. Pillar I: Minimum capital requirementsPillar I: Minimum capital requirements

2.2. Pillar II: Internal Capital Adequacy Assessment Process (ICAAP) Pillar II: Internal Capital Adequacy Assessment Process (ICAAP) + Supervisory Review Process (SREP)+ Supervisory Review Process (SREP)

3.3. Pillar III: Market disciplinePillar III: Market discipline Its aims are:Its aims are:

New rules for capital requirements (+ differentiations, + risk factors)New rules for capital requirements (+ differentiations, + risk factors) Supervision of banks by regulators (e.g. Bank of Italy)Supervision of banks by regulators (e.g. Bank of Italy) + information to the market on the capital adequacy (and risk + information to the market on the capital adequacy (and risk

bearing) of a bankbearing) of a bank Possibility to use (after validation by the regulator) internal capital Possibility to use (after validation by the regulator) internal capital

modelsmodels From “single exposure” approachFrom “single exposure” approach “portfolio” approach“portfolio” approach

towards

77

Basel II – Pillar IBasel II – Pillar I The first pillar of Basel II is also the most important, because it states The first pillar of Basel II is also the most important, because it states

minimum minimum mandatorymandatory capital requirements for banks capital requirements for banks In Pillar I three types of risks are consideredIn Pillar I three types of risks are considered

Credit riskCredit risk Market riskMarket risk Operational riskOperational risk

Minimum capital requirements can either be determined by:Minimum capital requirements can either be determined by: Standardized risk weightsStandardized risk weights Internal modelsInternal models they have to be validated by the regulator: they they have to be validated by the regulator: they

need an internal complex process and IT sourcesneed an internal complex process and IT sources

For this reason only major banks can use internal models for capital For this reason only major banks can use internal models for capital requirements’ purposes. Smaller banks can use for Pillar I the requirements’ purposes. Smaller banks can use for Pillar I the standardized approachstandardized approach

88

Pillar I – Credit riskPillar I – Credit risk

Even in the standardized approach, credit risk estimation has Even in the standardized approach, credit risk estimation has advanced a lot from 1988 agreementadvanced a lot from 1988 agreement

Risk weights are no more based only on the nature of exposure, Risk weights are no more based only on the nature of exposure, but also on the credit worthiness, stated by the but also on the credit worthiness, stated by the agency ratingsagency ratings (Moody’s, S&P, Fitch etc.)(Moody’s, S&P, Fitch etc.)

Exposure/Rating AAA to AA-

A+ to A-

BBB+ to BBB-

BB+ to BB-

B+ to B-

Unrated Past-due

Corporates 20% 50% 100% 100% 150% 100% 150% Sovereign 0% 20% 50% 100% 150% 100%

Banks 20% 50% 50% 100% 150% 50% Retail 75% 100%-

150% Residential mortgages

35% 100%-150%

Non residential mortgages

100%-150% 150%

99

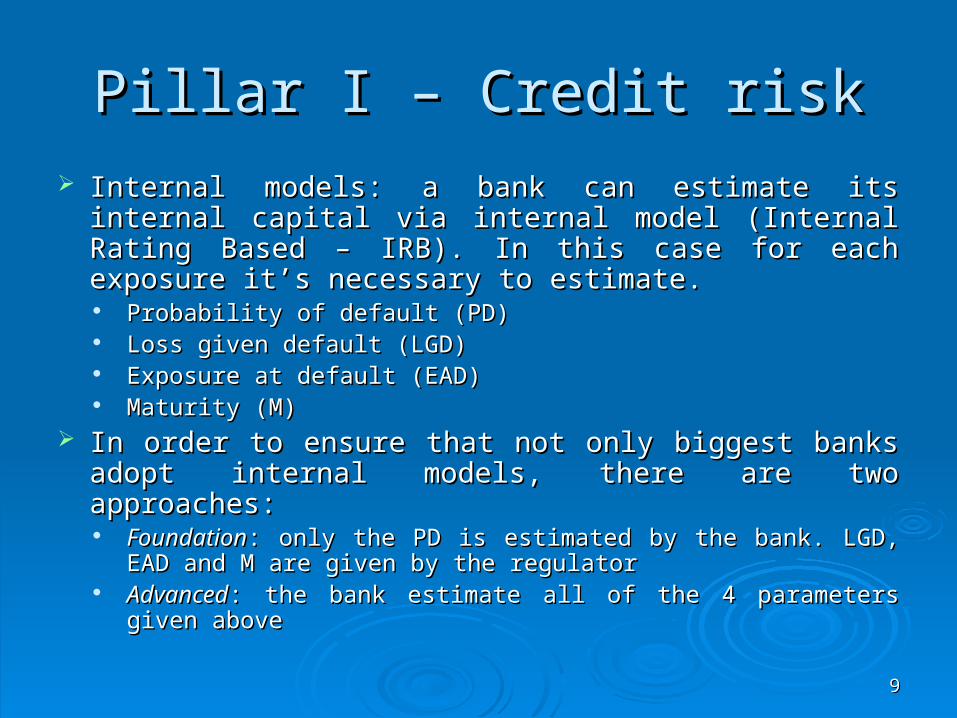

Pillar I – Credit riskPillar I – Credit risk Internal models: a bank can estimate its internal capital Internal models: a bank can estimate its internal capital

via internal model (Internal Rating Based – IRB). In this via internal model (Internal Rating Based – IRB). In this case for each exposure it’s necessary to estimate.case for each exposure it’s necessary to estimate.

Probability of default (PD)Probability of default (PD) Loss given default (LGD)Loss given default (LGD) Exposure at default (EAD)Exposure at default (EAD) Maturity (M)Maturity (M)

In order to ensure that not only biggest banks adopt In order to ensure that not only biggest banks adopt internal models, there are two approaches:internal models, there are two approaches:

FoundationFoundation: only the PD is estimated by the bank. LGD, EAD : only the PD is estimated by the bank. LGD, EAD and M are given by the regulatorand M are given by the regulator

AdvancedAdvanced: the bank estimate all of the 4 parameters given : the bank estimate all of the 4 parameters given aboveabove

1010

Pillar I – Credit riskPillar I – Credit risk Once the “single exposure” parameters are estimated, we can Once the “single exposure” parameters are estimated, we can

determine expected losses and unexpected losses.determine expected losses and unexpected losses. Expected losses: EL = EAD*PD*LGD Expected losses: EL = EAD*PD*LGD Expected losses have to be Expected losses have to be

budgeted in the profit and loss accountbudgeted in the profit and loss account Unexpected losses: Unexpected losses: these losses represent a “tail event” in the loss these losses represent a “tail event” in the loss

distribution. Given a confidence level of 99.9 % (as stated by Basel II for distribution. Given a confidence level of 99.9 % (as stated by Basel II for Credit risk), we have that minimum capital requirement (for exposure Credit risk), we have that minimum capital requirement (for exposure ii) ) isis

ii

i

iiiii LGDPD

PDLGDEADk *

1

)()(**06.1*

11

1111

The IRB formula represent the unexpected loss (i.e. the The IRB formula represent the unexpected loss (i.e. the 99.9% loss quantile), calculated under the Vasicek-99.9% loss quantile), calculated under the Vasicek-Gordy model (2000)Gordy model (2000)

Its assumptions are:Its assumptions are: An infinitely granular portfolioAn infinitely granular portfolio One common risk factorOne common risk factor Normal distribution of the unique risk factorNormal distribution of the unique risk factor The correlation with the risk factor is modelled via a Gaussian The correlation with the risk factor is modelled via a Gaussian

copula functioncopula function The correlation factor The correlation factor ρ ρ is not estimated by the bank, but given is not estimated by the bank, but given

by the regulator (it’s generally a decreasing function of the PD)by the regulator (it’s generally a decreasing function of the PD)

Pillar I – Credit riskPillar I – Credit risk

1212

Pillar I - Market riskPillar I - Market risk Also for market risk we have a standardized and an advanced Also for market risk we have a standardized and an advanced

approachapproach Standardized approachStandardized approach: it consists in weights and haircuts based : it consists in weights and haircuts based

on:on: The maturity of the securityThe maturity of the security Its duration Its duration The credit worthiness of the issuerThe credit worthiness of the issuer Compensation for netting long/short positionsCompensation for netting long/short positions

Internal modelInternal model: it’s based on the concept of Value at Risk (VaR): it’s based on the concept of Value at Risk (VaR)

RiskDefault 60

*,max

60

11

1

i

t

ti

VaRFVaRk

1313

The VaR must have the following characteristics:The VaR must have the following characteristics:• A confidence level of (at least) 99%A confidence level of (at least) 99%• A time horizon of (at least) 10 working daysA time horizon of (at least) 10 working days• Historical sample for volatility at least 1 yearHistorical sample for volatility at least 1 year• Update of volatility and correlation at least quarterlyUpdate of volatility and correlation at least quarterly• Total VaR obtained by summing VaR of different risk factors Total VaR obtained by summing VaR of different risk factors

(correlations equal to 1 among risk factors)(correlations equal to 1 among risk factors)• Reflect non-linear risk profile of option contractsReflect non-linear risk profile of option contracts• Calculated on a daily basisCalculated on a daily basis

The factor The factor FF is a number between 3 and 4, it reflects the quality of internal is a number between 3 and 4, it reflects the quality of internal modelmodel

Default risk must be calculated with the model adopted for credit risk (IRB)Default risk must be calculated with the model adopted for credit risk (IRB)

Pillar I - Market riskPillar I - Market risk

1414

Pillar IIPillar IIPillar II consists in two different aspectsPillar II consists in two different aspects

ICAAP: it’s a process internal in the bank itself. Its aim is to ICAAP: it’s a process internal in the bank itself. Its aim is to determine the capital adequacy for unexpected lossesdetermine the capital adequacy for unexpected losses

SREP: it’s a review of the risk measurement process carried SREP: it’s a review of the risk measurement process carried out by the individual banks, requiring, if necessary, a further out by the individual banks, requiring, if necessary, a further capital buffer in addition to the one of ICAAPcapital buffer in addition to the one of ICAAP

The final goal of Pillar II is to determine an internal capital to The final goal of Pillar II is to determine an internal capital to tackle different risks. There is no regulatory requirement, but tackle different risks. There is no regulatory requirement, but the banks are free to choose the models to adopt in order to the banks are free to choose the models to adopt in order to correctly estimate riskscorrectly estimate risks

The capital amount necessary to cover all risks is named The capital amount necessary to cover all risks is named economic capitaleconomic capital

1515

Pillar IIPillar II

Pillar II requires the quantification of several risks not embedded Pillar II requires the quantification of several risks not embedded in Pillar I or too much simplified. Among these:in Pillar I or too much simplified. Among these:

a)a) Concentration risk:Concentration risk: it’s part of the credit risk. It derives from it’s part of the credit risk. It derives from the fact that loan portfolios are not perfectly granular but the fact that loan portfolios are not perfectly granular but some exposures are particularly heavy (therefore their some exposures are particularly heavy (therefore their defaults could result in a huge loss for the bank): The IRB defaults could result in a huge loss for the bank): The IRB formula needs to be augmented of a buffer (Granularity formula needs to be augmented of a buffer (Granularity adjustment, GA), calculated with the Herfindahl Index (H)adjustment, GA), calculated with the Herfindahl Index (H)

cHEADGA

wHn

ii

**1

2

1616

b)b) Interest rate risk on banking book:Interest rate risk on banking book: it’s the risk of a it’s the risk of a mismatch between asset and liabilities in a bank. Like mismatch between asset and liabilities in a bank. Like concentration risk, it has a capital requirementconcentration risk, it has a capital requirement

Among other risks, not having a capital requirement, we Among other risks, not having a capital requirement, we find:find:

c)c) Liquidity riskLiquidity risk

d)d) Residual riskResidual risk

e)e) Reputation riskReputation risk

f)f) Compliance riskCompliance risk

Pillar IIPillar II

1717

Pillar II – stress testsPillar II – stress tests

A fundamental requirement of Pillar II is the A fundamental requirement of Pillar II is the stress stress testing testing of all Basel II risks (included Pillar I risks): it of all Basel II risks (included Pillar I risks): it consists in conditioning the risk factors to particularly bad consists in conditioning the risk factors to particularly bad events (stress test scenarios) and working out the capital events (stress test scenarios) and working out the capital adequacy that the bank would need in those scenariosadequacy that the bank would need in those scenarios

Also for stress tests, the final goal is to determine a Also for stress tests, the final goal is to determine a stressed economic capitalstressed economic capital and take actions (when and take actions (when needed) in order to manage those risksneeded) in order to manage those risks

1818

Example of stress testsExample of stress testsMarket risk: Market risk: an example of a stress test could consists in a parallel shift an example of a stress test could consists in a parallel shift

of the yield curve of of the yield curve of ± ± 200 bps200 bps

For every shift, we must calculate the theoretical value of the portfolio For every shift, we must calculate the theoretical value of the portfolio and the eventual loss associated to each scenarioand the eventual loss associated to each scenario

Parallel shifts of the yield curve

0

1

2

3

4

5

6

7

1y 2y 3y 4y 5y 6y 7y

Maturity

Inte

res

t ra

te (

%)

04/12/2007

+ 200 bp

- 200 bp

1919

Credit risk: Credit risk: considering the time series of default of Italian families (last 20 considering the time series of default of Italian families (last 20 years), we could take as an extreme event the worst rate registered (source, years), we could take as an extreme event the worst rate registered (source, Bank of Italy)Bank of Italy)

Conditioned on the highest default rate, we could work out the additional Conditioned on the highest default rate, we could work out the additional capital requirement basing on the IRB formulacapital requirement basing on the IRB formula

Example of stress testsExample of stress tests

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

< 125.000 €

>= 125.000 € e < 500.000 €

>= 500.000 €

Totale

Tassidi ingresso a sofferenza 1990-2008

2020

Pillar III - market disciplinePillar III - market discipline

The third pillar of Basel II consists in the “transparency” of banks’ The third pillar of Basel II consists in the “transparency” of banks’ risks and its reporting to the market (included customers). risks and its reporting to the market (included customers). Information provided include:Information provided include:

Size and composition of capital and risky assetsSize and composition of capital and risky assets Distribution of credit exposure and default ratesDistribution of credit exposure and default rates Risk measurement and control systemsRisk measurement and control systems Accounting practices in useAccounting practices in use Capital allocation criteria within the banksCapital allocation criteria within the banks

2121

Advantages and limitations of Basel Advantages and limitations of Basel IIII

Advantages:Advantages:• More flexibility of capital ratiosMore flexibility of capital ratios• Takes into account portfolio diversificationTakes into account portfolio diversification• Extends the rules of the supervisors and of the marketExtends the rules of the supervisors and of the market• + space for risk management techniques+ space for risk management techniques• Internal models as source of competitive advantageInternal models as source of competitive advantage

Limitations:Limitations: ProcyclicalityProcyclicality: the regulatory requirements could decrease : the regulatory requirements could decrease

capital in booms and increase capital in recessions the capital in booms and increase capital in recessions the parameters should be calibrated on a long time horizonparameters should be calibrated on a long time horizon

Excessive dependency on agency ratingsExcessive dependency on agency ratings Complexity?Complexity?

2222

What next?What next?

2008-09 global recession has shown many limitations of 2008-09 global recession has shown many limitations of Basel II agreements Basel II agreements

Moving towards Basel III?Moving towards Basel III?

Anyway, capital adequacy agreements are developing Anyway, capital adequacy agreements are developing

also in other industries, basing on Basel II risk factors also in other industries, basing on Basel II risk factors (e.g. Solvency II for insurance companies)(e.g. Solvency II for insurance companies)

2323

ReferencesReferences

1. Resti, A. and Sironi, A., “Risk Management and Shareholders’ Value in Banking”

2. Basel II: International Convergence of Capital Measurement and Capital Standards – www.bis.org

3. Circolare 263/2006 Banca d’Italia – www.bancaditalia.it/vigilanza/banche/normativa/disposizioni/vigprud

4. Vasicek, O. A., “Credit Valuation”, KMV Corporation

5. Gordy, M. B., (2000b), “A comparative analysis of credit risk models”, Journal of Financial and Quantitative Analysis,12, 541-522