Academy of Economic Studies Doctoral School of Finance - DOFIN Exchange Rate Risk: Heads or Tails?

Upload

silvia-hortonCategory

view

217download

0

1

Academy of Economic StudiesDoctoral School of Finance - DOFIN

Evidence of the Unspanned Stochastic Volatility in crude-oil market

Student: Răzvan Daniel TudorSupervisor Professor: PhD. Moisă Altăr

Bucharest, July 2008

2

Paper Topics

Literature Review

Overview of the data

The Model

The Model Estimation and Analysis

Conclusions

Bibliography

3

Paper Goals

To characterize the crude-oil market

To determine if commodity equilibrium models which assume that futures

contracts by construction embed market volatility are correct

To see if the classical hedging strategies based on entering a rolling futures

contract offers enough protection against volatility risk

To determine if options on futures are redundant securities

To sum up - the main purpose is to provide an empirical evidence of

unspanned stochastic volatility in crude-oil market

4

Literature Review First equilibrium models from commodity markets are based on Kaldor’s Theory

of Storage (1939)

Deaton and Laroque (1992), Chambers and Bailey (1996), Routledge, Seppi and Spatt (2000) models link the term structure of futures prices with the level of inventories of commodities.

Litzenberger and Rabinowitz (1995) showed for crude oil, and Ng and Pirrong (1994), for metals, that the degree of futures prices backwardation is positively related to volatility, indicating that most of volatility risk is spanned by the futures contracts.

Gordon, Hayashi and Rouwenhorst (2005), analyzed the fundamentals of commodity futures returns, and showed that the convenience yield is a decreasing, non-linear relationship of inventories and also linked the current spot commodity price and the current (nearest to maturity) futures price to the level of inventories.

5

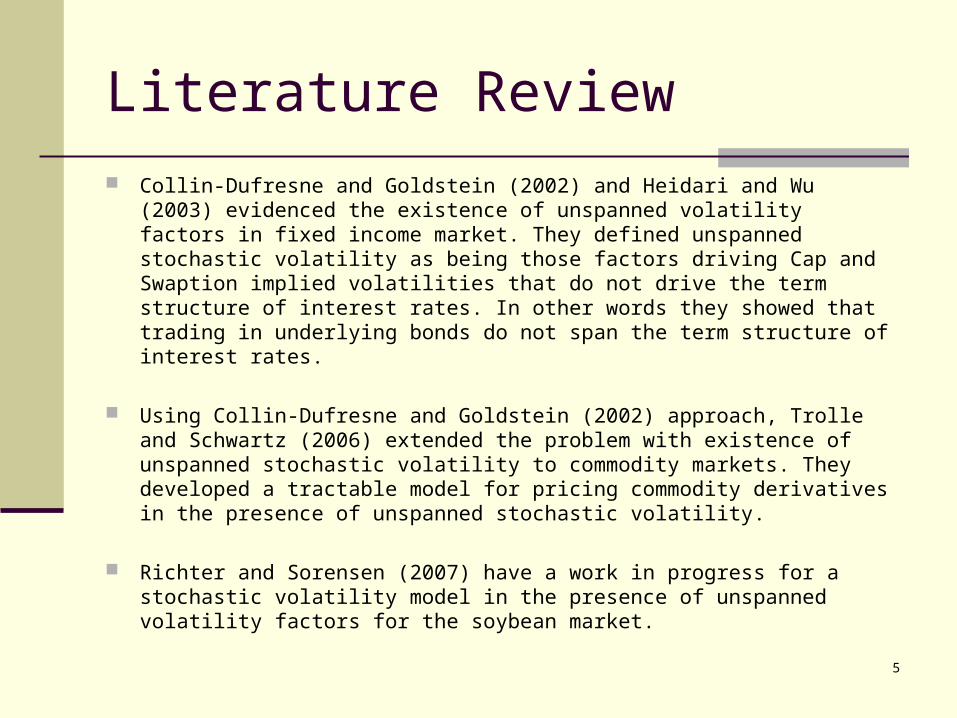

Literature Review

Collin-Dufresne and Goldstein (2002) and Heidari and Wu (2003) evidenced the existence of unspanned volatility factors in fixed income market. They defined unspanned stochastic volatility as being those factors driving Cap and Swaption implied volatilities that do not drive the term structure of interest rates. In other words they showed that trading in underlying bonds do not span the term structure of interest rates.

Using Collin-Dufresne and Goldstein (2002) approach, Trolle and Schwartz (2006) extended the problem with existence of unspanned stochastic volatility to commodity markets. They developed a tractable model for pricing commodity derivatives in the presence of unspanned stochastic volatility.

Richter and Sorensen (2007) have a work in progress for a stochastic volatility model in the presence of unspanned volatility factors for the soybean market.

6

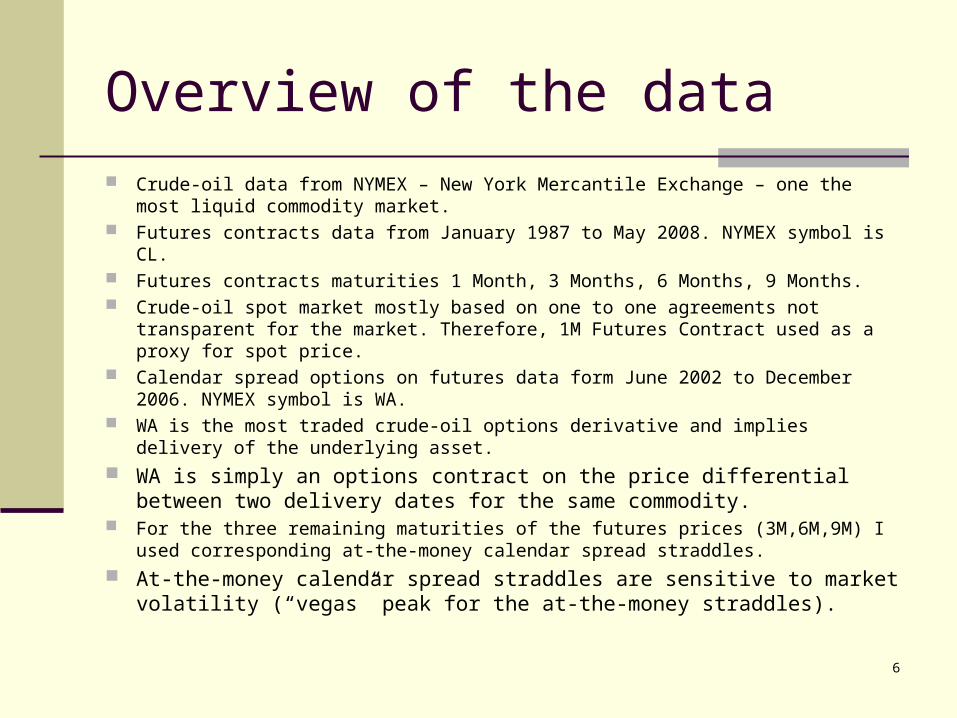

Overview of the data

Crude-oil data from NYMEX – New York Mercantile Exchange – one the most liquid commodity market.

Futures contracts data from January 1987 to May 2008. NYMEX symbol is CL. Futures contracts maturities 1 Month, 3 Months, 6 Months, 9 Months. Crude-oil spot market mostly based on one to one agreements not transparent

for the market. Therefore, 1M Futures Contract used as a proxy for spot price. Calendar spread options on futures data form June 2002 to December 2006.

NYMEX symbol is WA. WA is the most traded crude-oil options derivative and implies delivery of the

underlying asset.

WA is simply an options contract on the price differential between two delivery dates for the same commodity.

For the three remaining maturities of the futures prices (3M,6M,9M) I used corresponding at-the-money calendar spread straddles.

At-the-money calendar spread straddles are sensitive to market volatility (“vegas” peak for the at-the-money straddles).

7

The Model – general approach

There are four alternatives to evidence the presence of unspanned stochastic volatility in crude oil market:

- Investigate how much of the variation in the prices of derivatives highly exposed to stochastic volatility (ATM straddles) can be explained by variation in the underlying futures prices;

- Investigate how much of the variation in implied volatilities (which is related to expectations under the risk-neutral measure of future volatility) can be explained by variation in the underlying futures prices;

- Investigate how much of the variation in realized volatility, estimated from high frequency data, can be explained by variation in the underlying futures prices.

- Investigate how much of the volatility of the variance swaps can be explained by variation in the underlying futures prices.

Due to lack of high futures contracts frequency data and illiquid market for variance

swaps the model will focus on first two approaches.

8

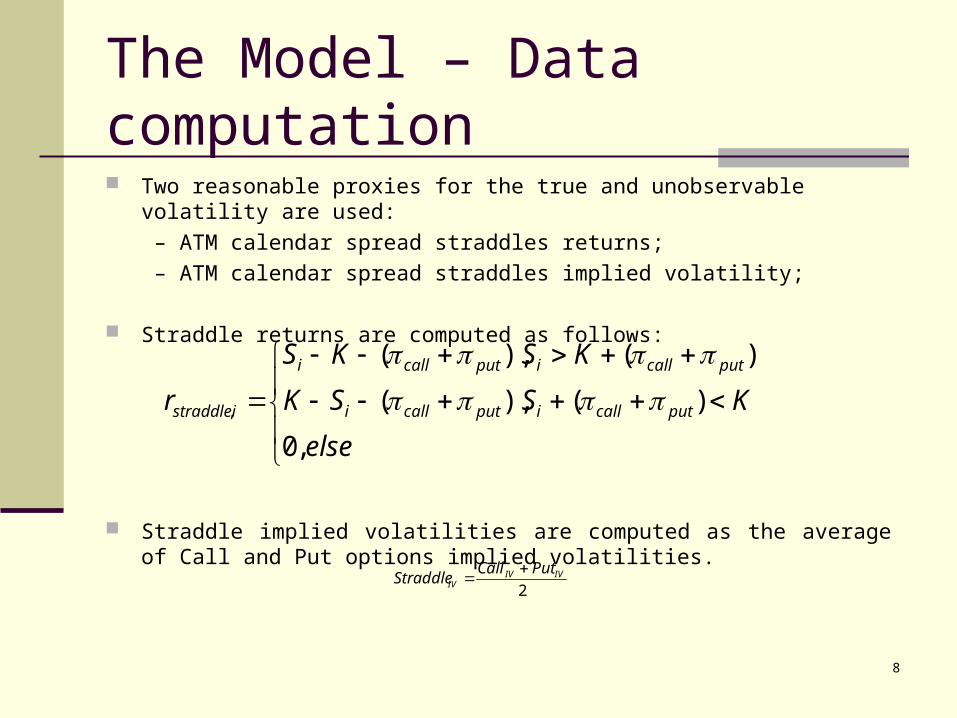

The Model – Data computation

Two reasonable proxies for the true and unobservable volatility are used:

– ATM calendar spread straddles returns;

– ATM calendar spread straddles implied volatility;

Straddle returns are computed as follows:

Straddle implied volatilities are computed as the average of Call and Put options implied volatilities.

else

KSSK

KSKS

r putcalliputcalli

putcalliputcalli

istraddle

,0

)(),(

)(),(

,

2IVIV

IV

PutCallStraddle

9

The Model –Data computation

Call and Put options implied volatilities are derived from Black-Scholes option pricing model.

All the parameters needed to extract the implied volatilities are NYMEX observed values, except the risk free rate which is the risk free rate of the US T-Bills with corresponding maturities.

Use of principal components analysis (PCA) to extract futures returns variance factors and to avoid near multicollinarity. In crude-oil market, futures prices (returns) are highly correlated.

)()(),( 21 dKedSTSC rT

)()(),( 12)( dSdKeTSP tTr

10

The Model - PCA Principal component analysis is based on eigenvalues and eigenvector analysis of V

=X’XT, the k x k symmetric matrix of correlations between the variables in X. Each principal component is a linear combination of the X columns, where the weights are chosen in such way that:- the first principal component explains the greatest amount of the total variation in X, the second component explains the greatest amount of the remaining variation, and so on;- the principal components are uncorrelated to each other;

Denoting by W the k x k matrix of eigenvectors of V. Thus: VW=WΛ.Where Λ is the k x k diagonal matrix of eigenvalues of V. Then we order the columns of W according to the size of corresponding eigenvalue. Thus if for i,j=1,…,k then the m-th column of W, denoted is the k x 1 eigenvector corresponding to the eigenvalue and the column labeling has been chosen so thatTherefore the m-th principal component of the system is defined by:

Where denotes the i-th column of X. The sum of the eigenvalues is k, the number of variables in the system. Therefore, the

proportion of variation explained by the first n principal components together is:

)( ijwW

),...,( 1 kmmm www m k ...21

kkmmmm XwXwXwP ...2211

iX

kn

ii /

1

11

The Model – Evidence Procedure The evidence procedure consists of three steps:

a) The first step is principal components analysis of the correlation matrix of daily futures returns.

b) For each futures contract “i” regress the daily closest to the at-the-money straddle returns on the futures returns principal components. Also, for each futures contract “i” regress the daily straddle implied volatilities on futures returns principal components. The values of and will indicate the extent to which volatility is spanned by the futures contracts.

Regression Equation (Straddle Returns):

Regression Equation (Implied Volatility):

Where:

- - The principal components of the futures return data. They are numbered according to they variation explanatory power from principal component with highest eigenvalue to the principal component with smallest eigenvalue.

- - The straddle returns at “i” maturity. In my case i = 3, 6, 9 Months.

- - The implied volatility of the straddles at “i” maturity.

tiiiiiiiiiiii xxxxxxxxxxxxy 329318217

236

225

214332211

tiiiiiiiiiiii xxxxxxxxxxxxz 329318217

236

225

214332211

3,2,1, ixi

iyiz

2R2R

12

The Model – Evidence Procedure

c) Analyze the principal components of the time series of residuals from the straddle return

regressions and the implied volatility regressions.

There are two possible outcomes:

- If there is unspanned stochastic volatility in the data, there should be at least one significant explanatory principal component for the variation due to unspanned factors;

- If the residuals are simply due to noisy data, there should not be one principal component with high explanatory power among residuals.

Finally:

- repeat the evidence procedure using sample rolling windows and see if the new results are consistent with previously illustrated unspanned stochastic volatility evidence.

13

The Model Estimation and Analysis - Crude-oil market characterization -

Commodity futures prices are characterized by some important properties:

- Commodity futures prices are often “backwardated" in that they decline with time to delivery,

- Spot and futures prices are mean reverting;

- Commodity prices are strongly non-stationary and price volatility is correlated with the degree of backwardation;

- Unlike financial assets, many commodities have pronounced seasonality in both price levels and volatilities.

Backwardation property:

Given S(t) the time-t crude-oil spot price and F(t, T ) [P(t, T )] the time-t price of a crude-oil futures contract [zero

Coupon bond] with maturity T - t. The futures contract is backwardated if S(t) - P(t, T )F(t, T ) > 0 and strongly

backwardated if S(t) - F(t, T ) > 0.

14

The Model Estimation and Analysis - Crude-oil market characterization - Backwardation property

Even if the crude-oil market proved to be in contango – during June 2002 – December 2006 period – the market expectations derived from futures prices were bearish.

Strongly non-stationary property makes the crude-oil prices (spot and futures) to be non-usable for further research. Therefore, instead of prices series I will work with returns series.

15

The Model Estimation and Analysis - Futures returns characterization - Futures returns are highly correlated

Principal components analysis (PCA) to extract futures returns variance factors and to avoid near multicollinarity issue.

16

The Model Estimation and Analysis - Futures returns principal components significance -

The first principal component, which will be further denoted as , has the highest eigenvalue, which is responsible for explaining 98.76% ( , where k is the matrix dimension, in my case 3) of the variation of the future returns. If we look at corresponding eigenvector weights they are quite similar due to strong correlation between futures returns.

The significance of the first principal component corresponding eigenvector weights is that an upward shift in the first principal component induces a downward parallel shift of the futures returns curve. For this reason first principal component is called the trend component.

The second principal component, which will be further denoted as , explains only 1.18% of futures returns variation. The weights turn positive. Thus an upward movement of the second principal component induces a change in slope of the futures returns, where short maturities move down and long maturities move up. The second principal component significance is that 1.18% of the total futures return variation is attributed to changes in slope.

The third principal component, which will be further denoted as , explains only 0.03% of the futures returns variation. The weights are positive for the short term returns, negative for the medium term returns and positive for the long term returns. Therefore we can say that the third component influences the convexity of the returns curve. The significance of the third principal component is that 0.03% of the total variation is due to changes in convexity.

1PC

k/1

2PC

3PC

17

The Model Estimation and Analysis - Straddle returns and Straddle implied volatilities -

3M Straddle returns – overview and unit root test

3M Straddle implied volatilities – overview and unit root test

18

The Model Estimation and Analysis - 3M Straddle returns regression -

Output:- Low values for and ;- Coefficients are significant;- Straddle returns dependency

on trend component takes the

shape of an increasing convex

function;- Also the marginal influence of

the components is significant

– trend component change on

slope component change and

trend component change on

convexity component change).

- Regression both and values - 0.61 and 0.60 - indicates that trading in futures contracts do not span much of crude-oil prices volatility embedded in our volatility proxy – straddle returns. The values are low for commodity and financial markets where high and (meaning good explanatory power for the regressors) should exceed 0.85, whereas and bellow 0.7 indicate that volatility risk cannot be hedged using only futures contracts.

2R 2R

2R 2R

2R2R

2R 2R

19

The Model Estimation and Analysis - 3M Straddle returns regression issue - The regression Durbin-Watson test suggest there is autocorrelation among residuals.

Modeling the residuals with an

order MA(2) process shows that

coefficients are significant; Residuals from original regression

are kept for further analysis;

20

The Model Estimation and Analysis - Straddle returns regression and Straddle implied volatility regression overview -

Straddle returns regression

Straddle implied volatility regression

- Futures explanatory power decreases with maturity;- (actual versus fitted of straddle returns) increases while time-to-maturity

increases. yy ˆ

21

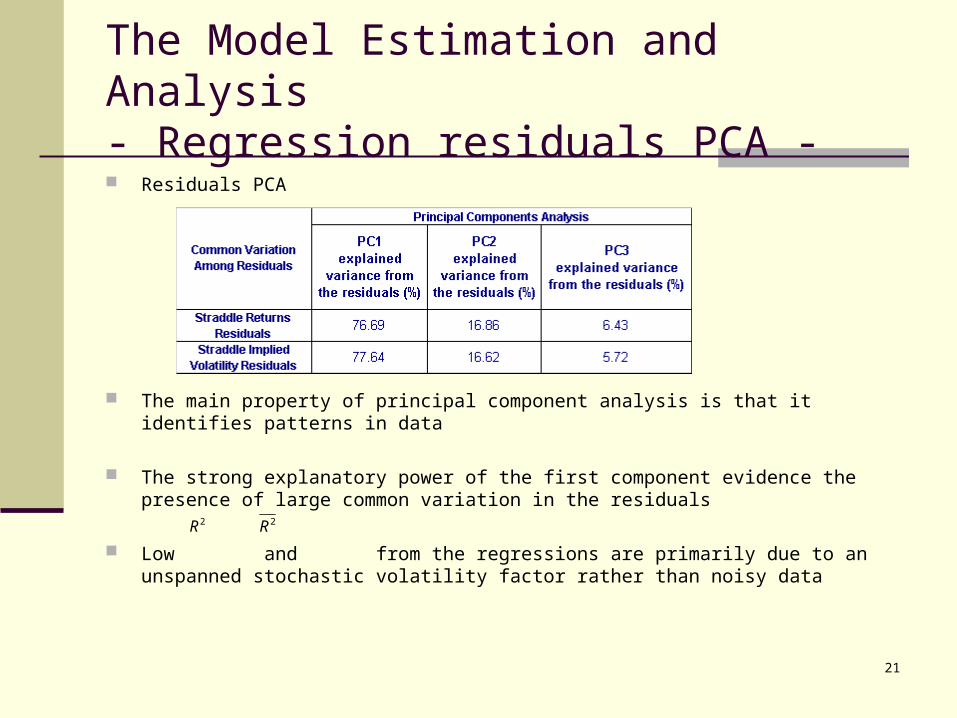

The Model Estimation and Analysis - Regression residuals PCA - Residuals PCA

The main property of principal component analysis is that it identifies patterns in data

The strong explanatory power of the first component evidence the presence of large common variation in the residuals

Low and from the regressions are primarily due to an unspanned stochastic volatility factor rather than noisy data

2R 2R

22

The Model Estimation and Analysis - Straddle returns regression - Rolling Window -

23

The Model Estimation and Analysis - Straddle returns residuals PCA –Rolling Window - Residuals PCA – Rolling Window

The first component explanatory power ranges from 49.5% to 92%.

This suggest as well the presence of large common variation in the residuals, the signal that low and are due to an unspanned stochastic volatility factor rather than noisy data.

2R 2R

24

The Model Estimation and Analysis - Evidence approaches Pros and Cons - Straddle returns:

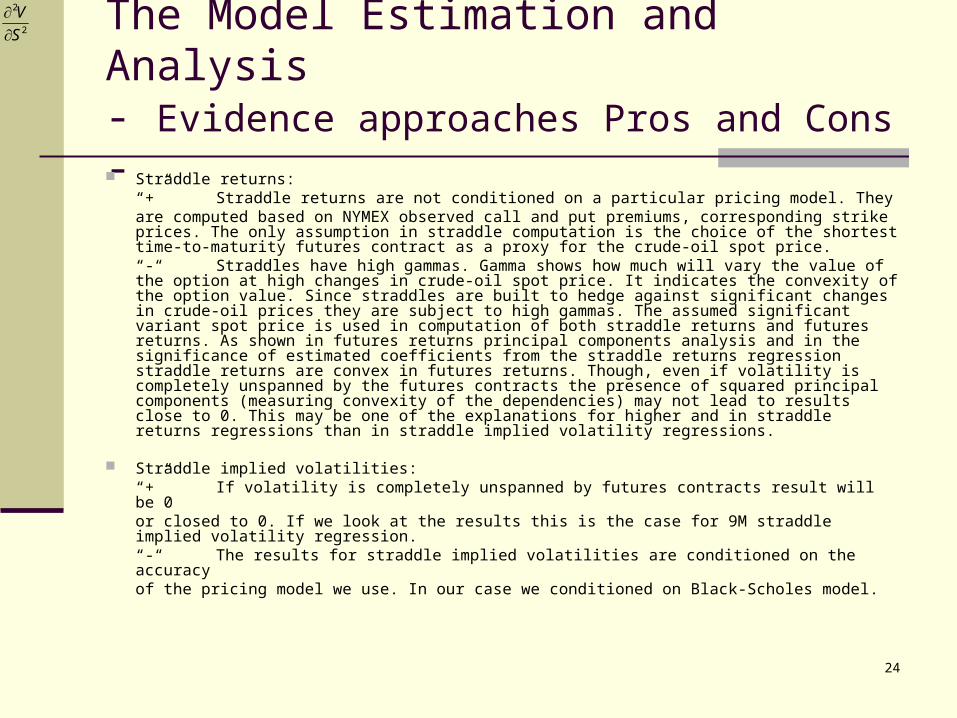

“+” Straddle returns are not conditioned on a particular pricing model. They are computed based on NYMEX observed call and put premiums, corresponding strike prices. The only assumption in straddle computation is the choice of the shortest time-to-maturity futures contract as a proxy for the crude-oil spot price.“-“ Straddles have high gammas. Gamma shows how much will vary the value of the option at high changes in crude-oil spot price. It indicates the convexity of the option value. Since straddles are built to hedge against significant changes in crude-oil prices they are subject to high gammas. The assumed significant variant spot price is used in computation of both straddle returns and futures returns. As shown in futures returns principal components analysis and in the significance of estimated coefficients from the straddle returns regression straddle returns are convex in futures returns. Though, even if volatility is completely unspanned by the futures contracts the presence of squared principal components (measuring convexity of the dependencies) may not lead to results close to 0. This may be one of the explanations for higher and in straddle returns regressions than in straddle implied volatility regressions.

Straddle implied volatilities:“+” If volatility is completely unspanned by futures contracts result will be 0 or closed to 0. If we look at the results this is the case for 9M straddle implied volatility regression. “-“ The results for straddle implied volatilities are conditioned on the accuracy of the pricing model we use. In our case we conditioned on Black-Scholes model.

2

2

S

V

25

Conclusions

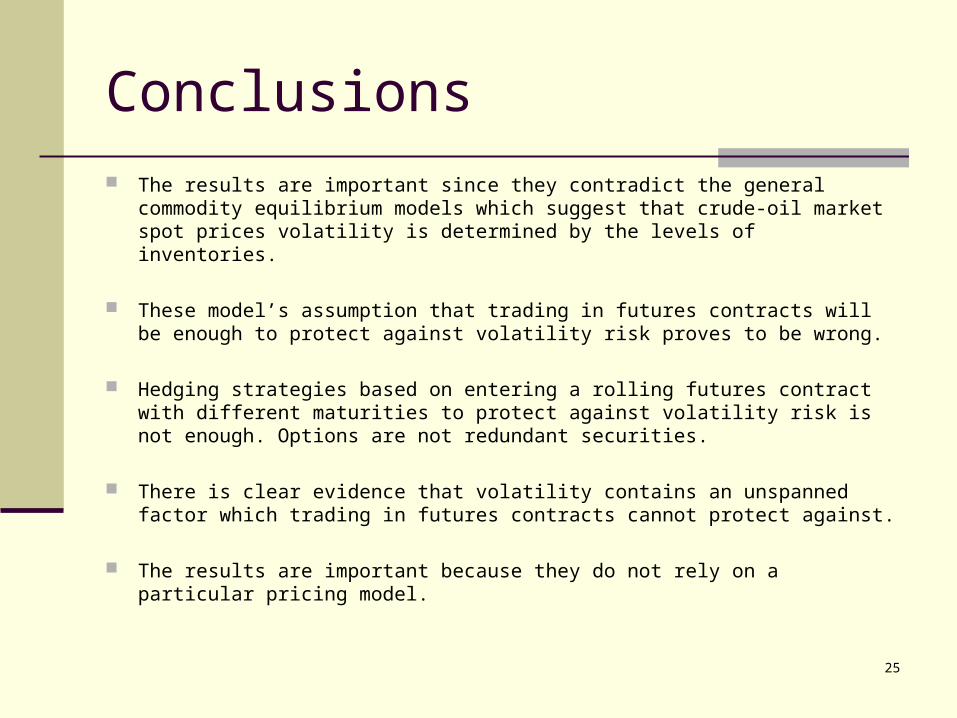

The results are important since they contradict the general commodity equilibrium models which suggest that crude-oil market spot prices volatility is determined by the levels of inventories.

These model’s assumption that trading in futures contracts will be enough to protect against volatility risk proves to be wrong.

Hedging strategies based on entering a rolling futures contract with different maturities to protect against volatility risk is not enough. Options are not redundant securities.

There is clear evidence that volatility contains an unspanned factor which trading in futures contracts cannot protect against.

The results are important because they do not rely on a particular pricing model.

26

Conclusions – Further Directions

Extend the evidence procedure taking into account high frequency data as Andersen and Benzoni (2005) did for fixed income market or taking into account the variance swaps.

Develop and test if an option pricing model which takes into account the unspanned stochastic volatility is reliable in hedging against volatility risk.

Investigate the unspanned stochastic volatility in other commodity markets less liquid where the futures contracts trading covers the most part of the transactions. (e.g. metals commodities markets).

27

Bibliography (selective) Alexander, C. (2001): “Market Models. A Guide to Financial Analysis”, John Wiley & Sons Ltd.

Andersen, T. G. and L. Benzoni (2005): “Can bonds hedge volatility risk in the U.S. treasury market? A specification test for affine term structure models,” Working paper, Kellogg School of Management, Northwestern University

Brooks, C. (2002): “Introductory Econometric for Finance”, Cambridge University Press

Carlson, M. , Khoker, Z. , Titman, S. (2006): “Equilibrium Exhaustible Resource Price Dynamics”, NBER Working Paper 12000.

Cassassus, J. and P. Collin-Dufresne (2005): “Stochastic convenience yield implied from commodity futures and interest rates,” Journal of Finance, 60:2283–2331.

Deaton, A. and G. Laroque (1992): “On the behaviour of commodity prices,” Review of Economic Studies, 59:1–23.

Deaton, A. and G. Laroque (1996): “Competitive storage and commodity price dynamics,” Journal of Political Economy, 104:896–923.

Elekdag, S., Lalonde, R., Laxton, D., Muir, D. and Pesenti, P. (2008): “Oil prices movements and the global economy: A model-based assessment”, NBER Working Paper 13792.

Gibson, R. and E. S. Schwartz (1990): “Stochastic convenience yield and the pricing ofoil contingent claims,” Journal of Finance, 45:959–976.

28

Bibliography (selective) Heidari, M. and L. Wu (2003): “Are interest rate derivatives spanned by the term structure of interest

rates?,” Journal of Fixed Income, 13:75–86.

Kogan, L., D. Livdan, and A. Yaron (2005): “Futures prices in a production economy with investment constraints,” Working paper, NBER # 11509.

Litzenberger, R. H. and N. Rabinowitz (1995): “Backwardation in oil futures markets: Theory and empirical evidence,” Journal of Finance, 50:1517–1545.

Miltersen, K. (2003): “Commodity price modeling that matches current observables: Anew approach,” Quantitative Finance, 3:51–58.

Nielsen, M. J. and E. S. Schwartz (2004): “Theory of Storage and the Pricing of Commodity Claims,” Review of Derivatives Research, 7:5–24.

Richter, M. and C. Sørensen (2002): “Stochastic volatility and seasonality in commodity futures and options: The case of soybeans,” Working paper, Copenhagen Business School.

Routledge, B. R., D. J. Seppi, and C. S. Spatt (2000): “Equilibrium forward curves forcommodities,” Journal of Finance, 55:1297–1338.

Schwartz, E. S. (1997): “The stochastic behavior of commodity prices: Implications forvaluation and hedging,” Journal of Finance, 52:923–973.

Trolle, A. and E. Schwartz (2006): “A general stochastic volatility model for the pricingand forecasting of interest rate derivatives,” Working paper, UCLA and NBER # 12337.

29

Thank you for the attention!

Q&A?