1-1 Brokers Awareness program (5) Dr. Mounther Barakat Securities and Commodities Authority.

150

1-1 Brokers Awareness program (5) Dr. Mounther Barakat Securities and Commodities Authority

-

Upload

dustin-alexander -

Category

Documents

-

view

218 -

download

5

Transcript of 1-1 Brokers Awareness program (5) Dr. Mounther Barakat Securities and Commodities Authority.

1-1

Brokers Awareness program

(5)

Dr. Mounther Barakat

Securities and Commodities Authority

1-2

برنامج توعية الوسطاء اللقاء الخامس

د. منذر بركات العمري

هيئة االوراق المالية والسلع

1-3

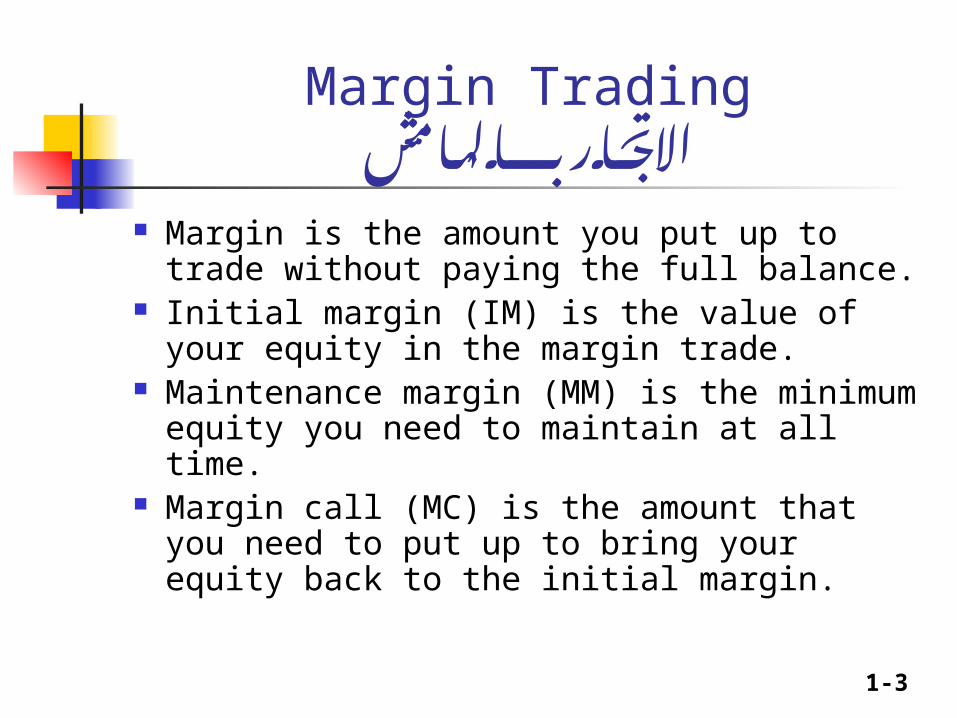

Margin is the amount you put up to trade without paying the full balance.

Initial margin (IM) is the value of your equity in the margin trade.

Maintenance margin (MM) is the minimum equity you need to maintain at all time.

Margin call (MC) is the amount that you need to put up to bring your equity back to the initial margin.

Margin Tradingبالهامش االتجار

1-4

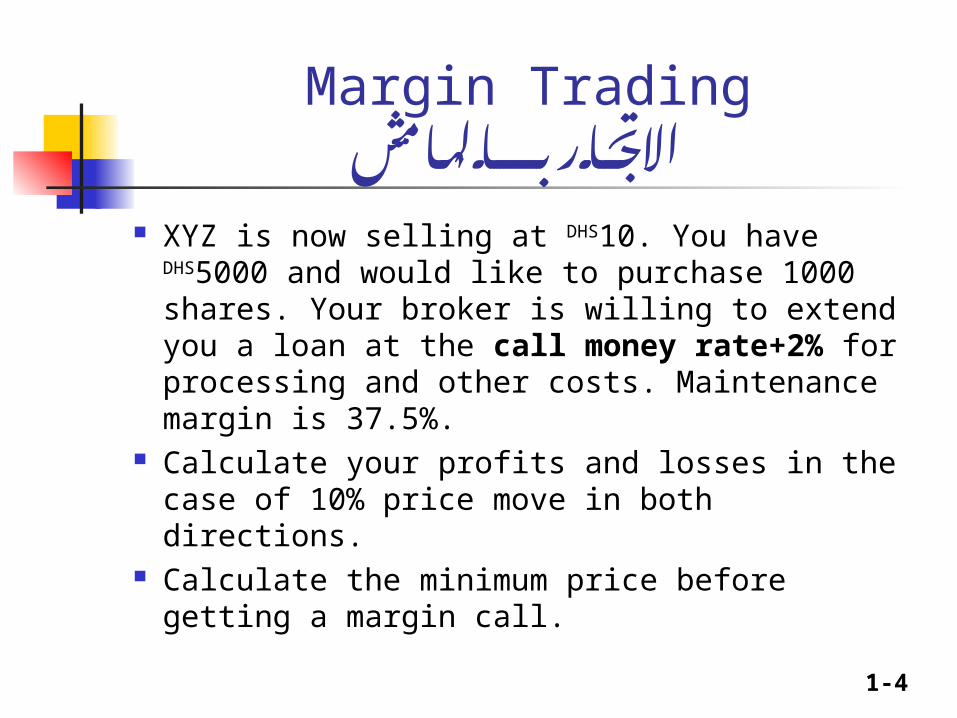

Margin Tradingاالتجار بالهامش

XYZ is now selling at DHS10. You have DHS5000 and would like to purchase 1000 shares. Your broker is willing to extend you a loan at the call money rate+2% for processing and other costs. Maintenance margin is 37.5%.

Calculate your profits and losses in the case of 10% price move in both directions.

Calculate the minimum price before getting a margin call.

1-5

Margin Tradingبالهامش االتجار

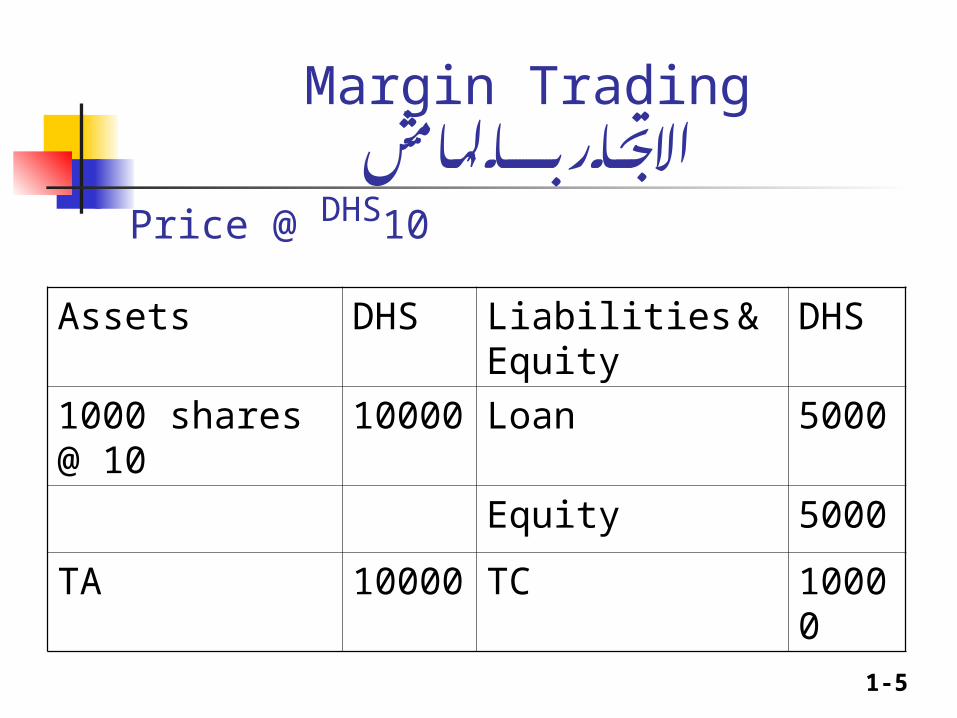

Assets DHS Liabilities & Equity

DHS

1000 shares @ 10

10000

Loan 5000

Equity 5000

TA 10000

TC 10000

Price @ DHS10

1-6

Margin Tradingبالهامش االتجار

Assets DHS Liabilities & Equity

DHS

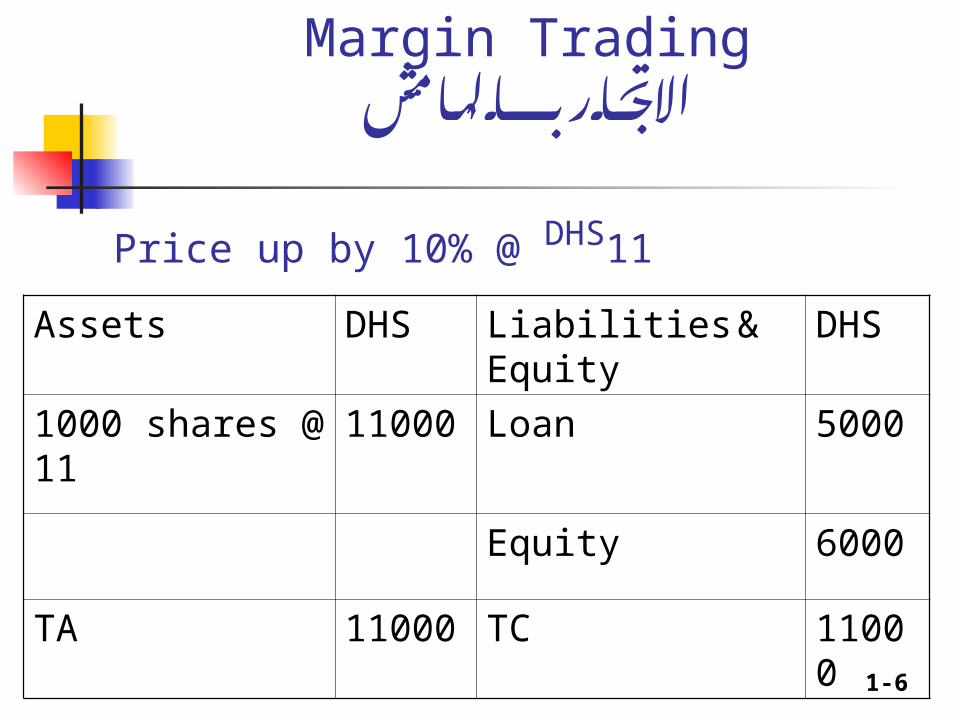

1000 shares @ 11

11000 Loan 5000

Equity 6000

TA 11000 TC 11000

Price up by 10% @ DHS11

1-7

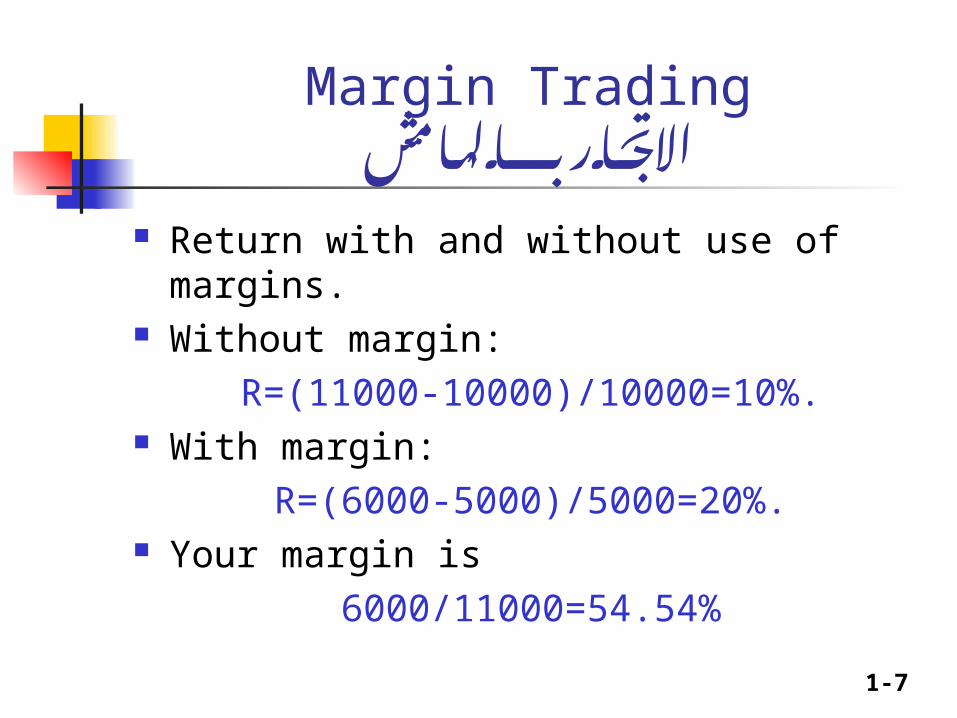

Return with and without use of margins. Without margin:

R=(11000-10000)/10000=10%. With margin:

R=(6000-5000)/5000=20%. Your margin is

6000/11000=54.54%

Margin Tradingبالهامش االتجار

1-8

Margin Tradingبالهامش االتجار

Assets DHS Liabilities & Equity

DHS

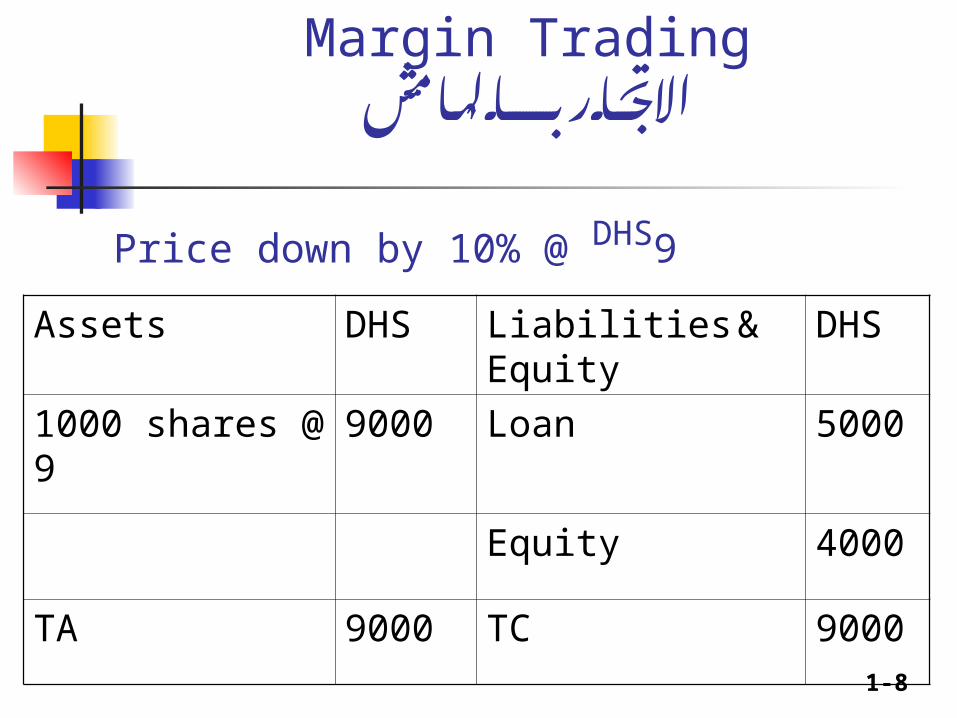

1000 shares @ 9

9000 Loan 5000

Equity 4000

TA 9000 TC 9000

Price down by 10% @ DHS9

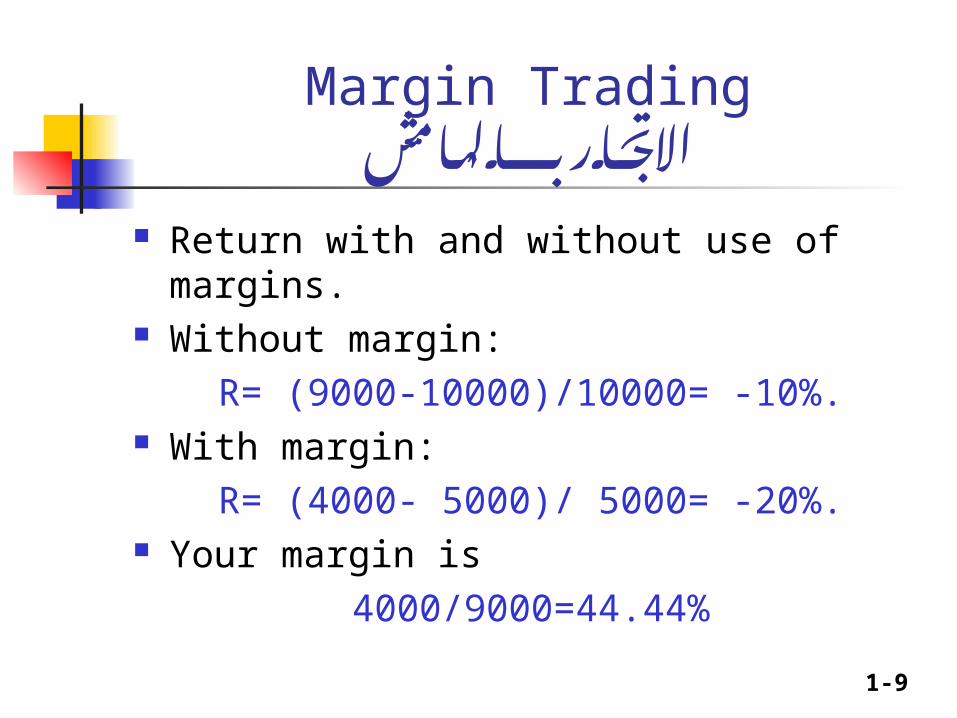

1-9

Return with and without use of margins. Without margin:

R= (9000-10000)/10000= -10%. With margin:

R= (4000- 5000)/ 5000= -20%. Your margin is

4000/9000=44.44%

Margin Tradingبالهامش االتجار

1-10

Margin Tradingبالهامش االتجار

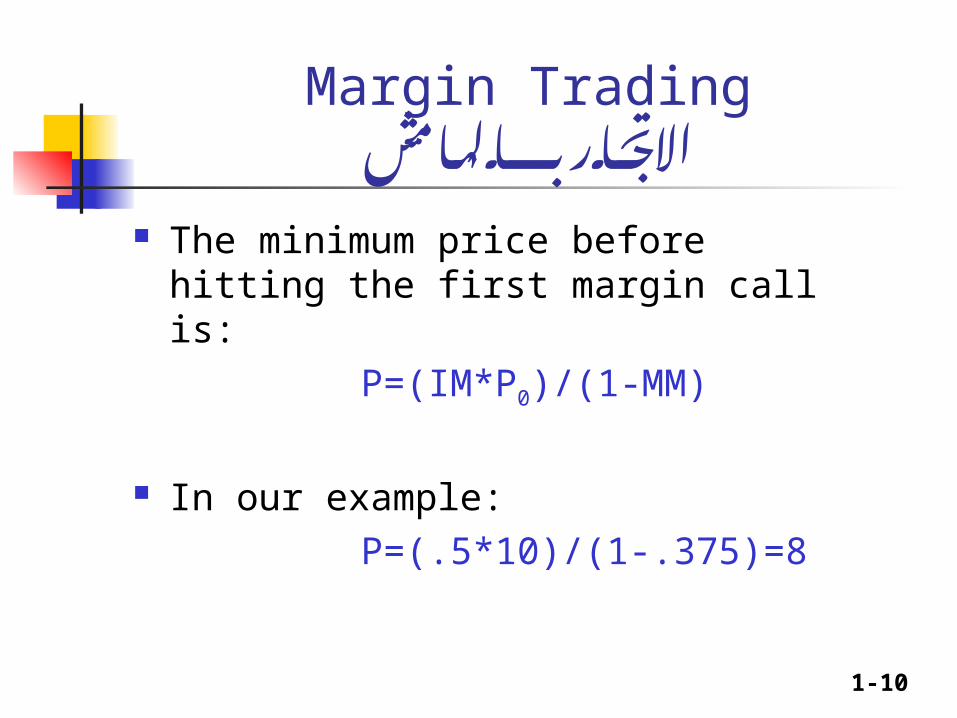

The minimum price before hitting the first margin call is:

P=(IM*P0)/(1-MM)

In our example:P=(.5*10)/(1-.375)=8

1-11

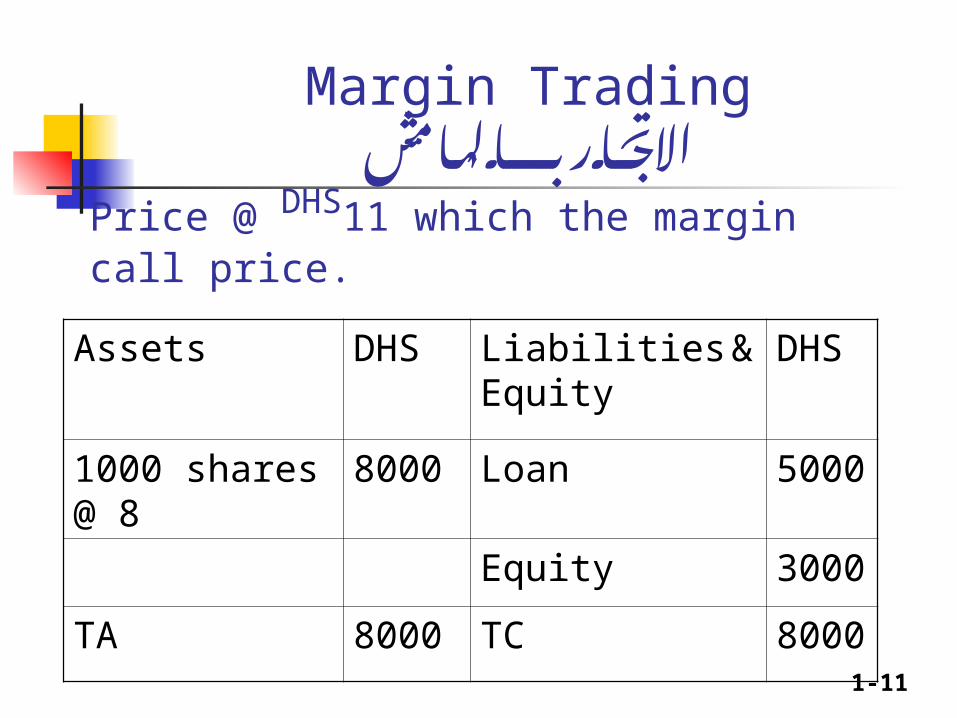

Margin Tradingبالهامش االتجار

Assets DHS Liabilities & Equity

DHS

1000 shares @ 8

8000 Loan 5000

Equity 3000

TA 8000 TC 8000

Price @ DHS11 which the margin call price.

1-12

Margin Tradingبالهامش االتجار

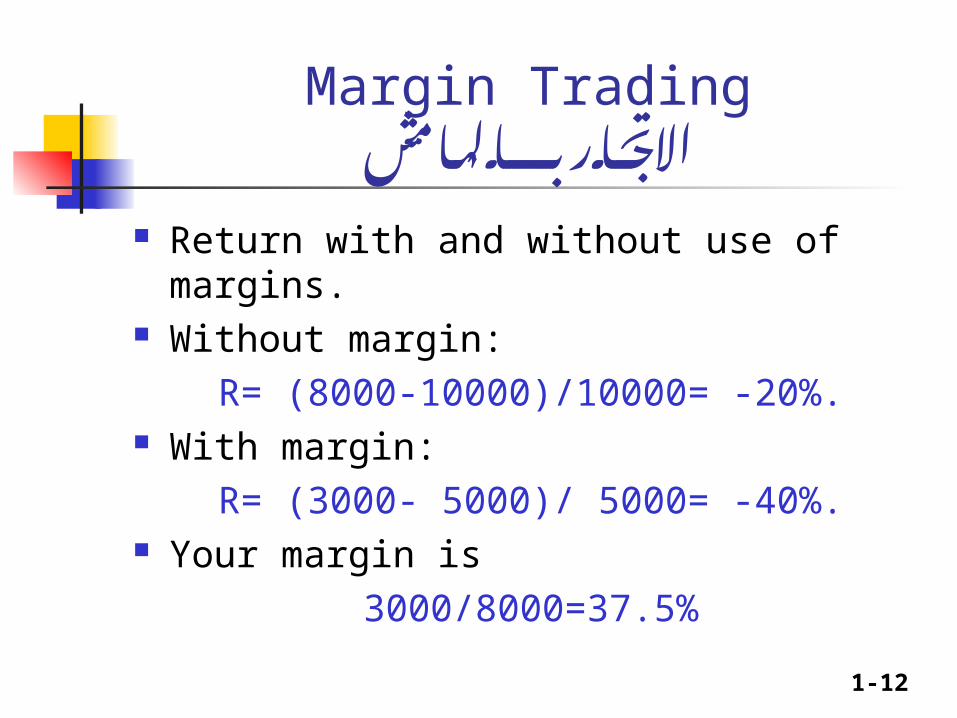

Return with and without use of margins. Without margin:

R= (8000-10000)/10000= -20%. With margin:

R= (3000- 5000)/ 5000= -40%. Your margin is

3000/8000=37.5%

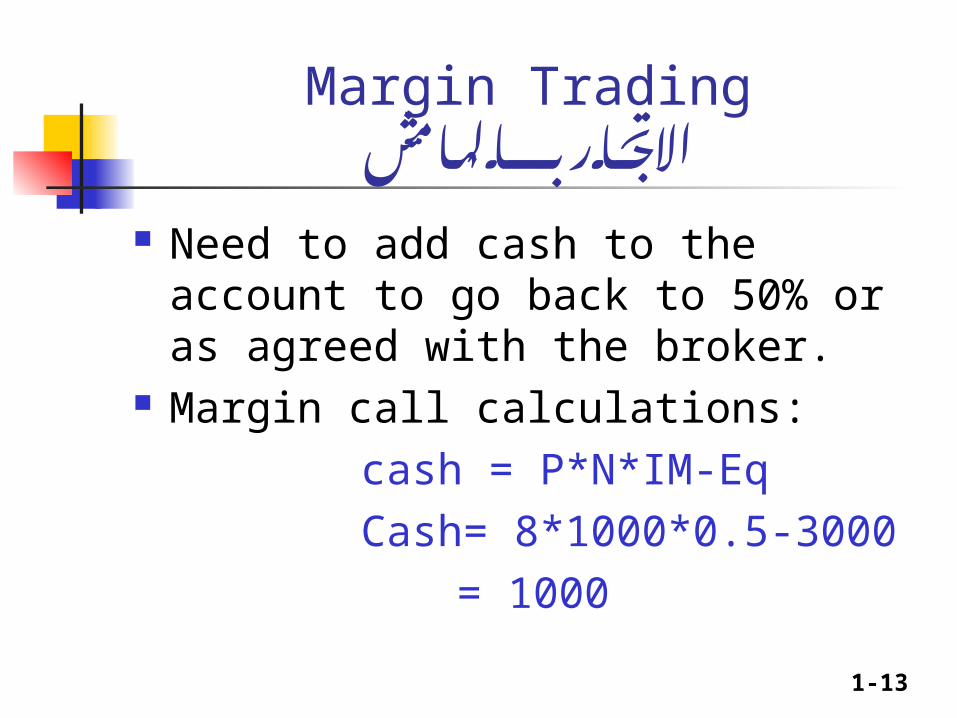

1-13

Margin Tradingبالهامش االتجار

Need to add cash to the account to go back to 50% or as agreed with the broker.

Margin call calculations:cash = P*N*IM-EqCash= 8*1000*0.5-3000

= 1000

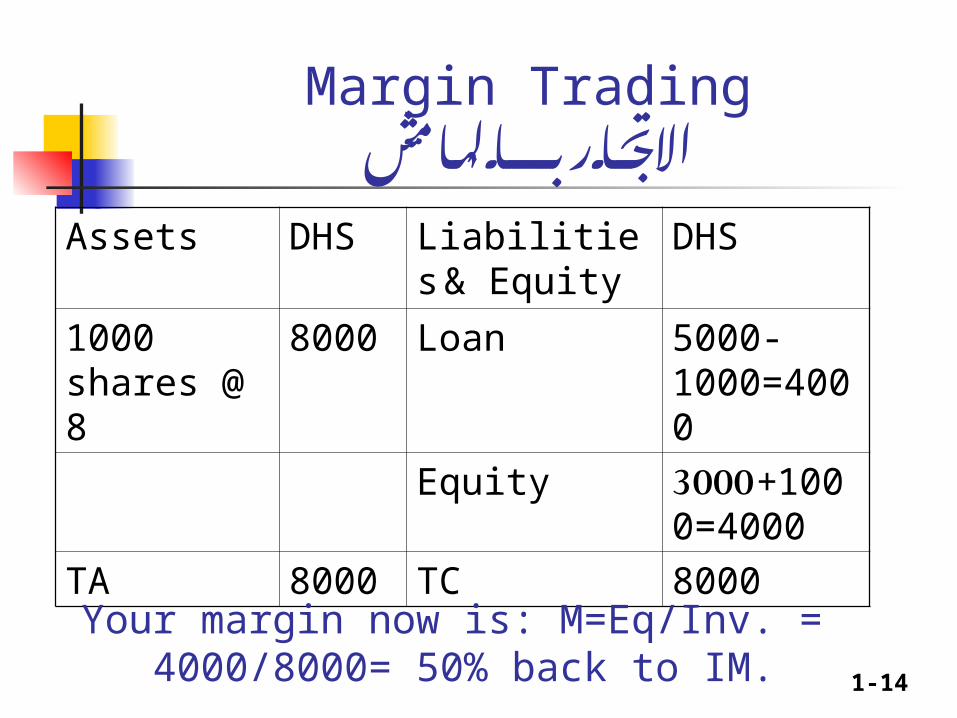

1-14

Margin Tradingبالهامش االتجار

Assets DHS Liabilities & Equity

DHS

1000 shares @ 8

8000 Loan 5000-1000=4000

Equity 3000+1000=4000

TA 8000 TC 8000Your margin now is: M=Eq/Inv. =

4000/8000= 50% back to IM.

1-15

Margin Tradingبالهامش االتجار

See XLS file for further training

1-16

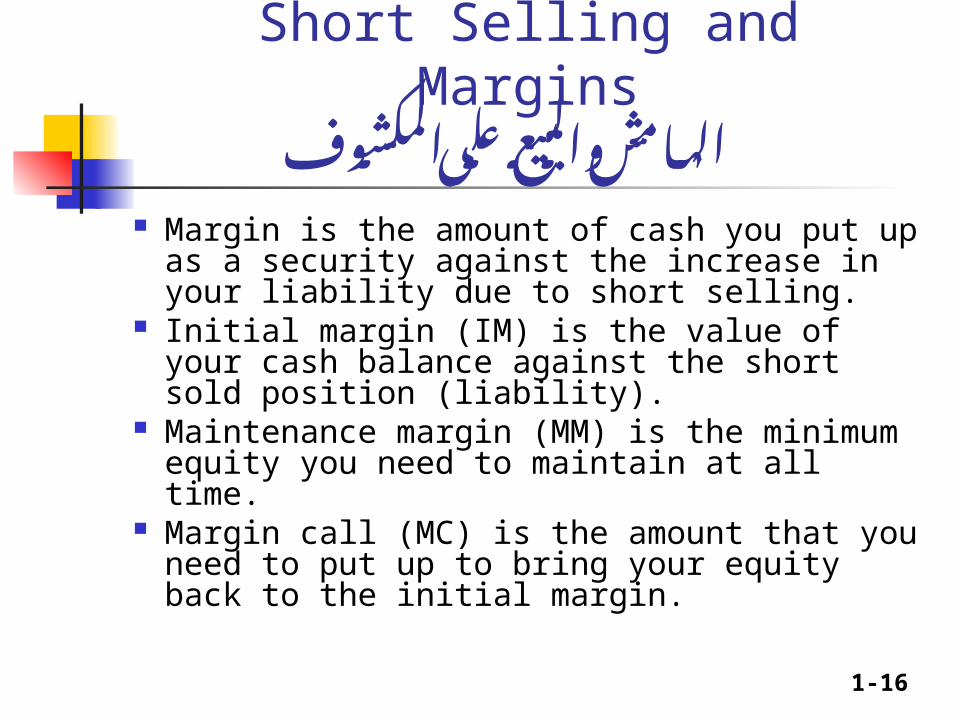

Short Selling and Marginsالهامش والبيع على المكشوف

Margin is the amount of cash you put up as a security against the increase in your liability due to short selling.

Initial margin (IM) is the value of your cash balance against the short sold position (liability).

Maintenance margin (MM) is the minimum equity you need to maintain at all time.

Margin call (MC) is the amount that you need to put up to bring your equity back to the initial margin.

1-17

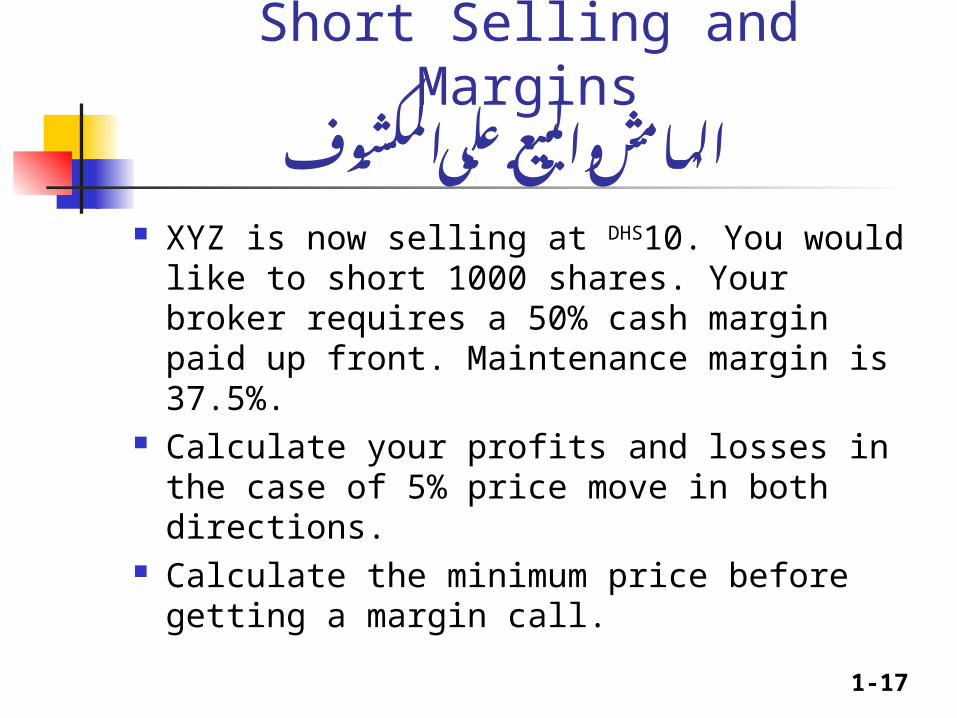

Short Selling and Marginsالهامش والبيع على المكشوف

XYZ is now selling at DHS10. You would like to short 1000 shares. Your broker requires a 50% cash margin paid up front. Maintenance margin is 37.5%.

Calculate your profits and losses in the case of 5% price move in both directions.

Calculate the minimum price before getting a margin call.

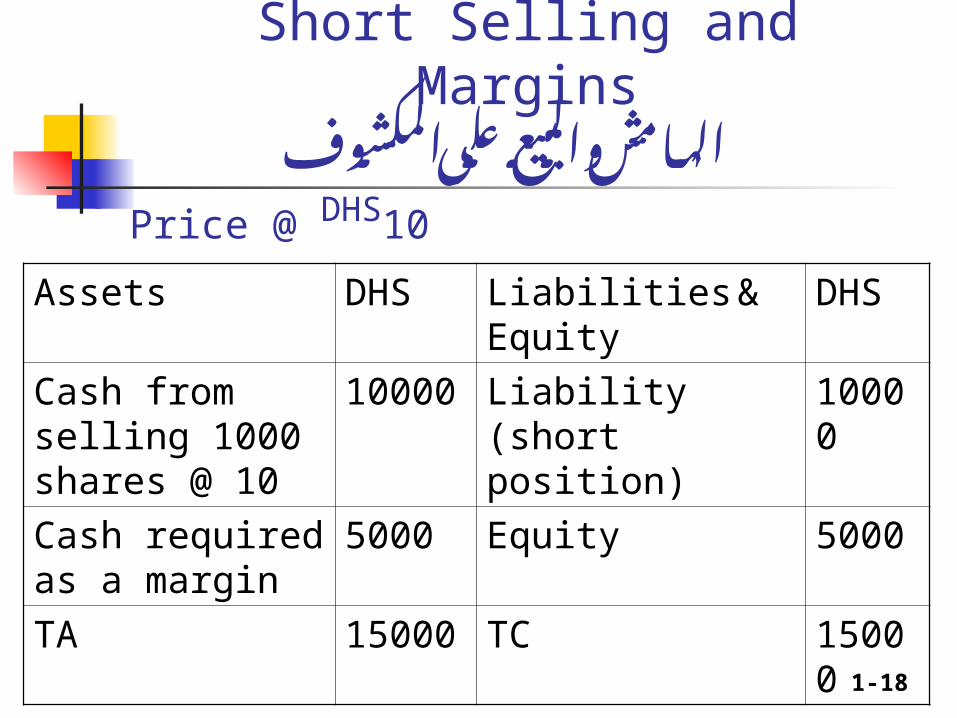

1-18

Short Selling and Marginsالهامش والبيع على المكشوف

Assets DHS Liabilities & Equity

DHS

Cash from selling 1000 shares @ 10

10000 Liability (short position)

10000

Cash required as a margin

5000 Equity 5000

TA 15000 TC 15000

Price @ DHS10

1-19

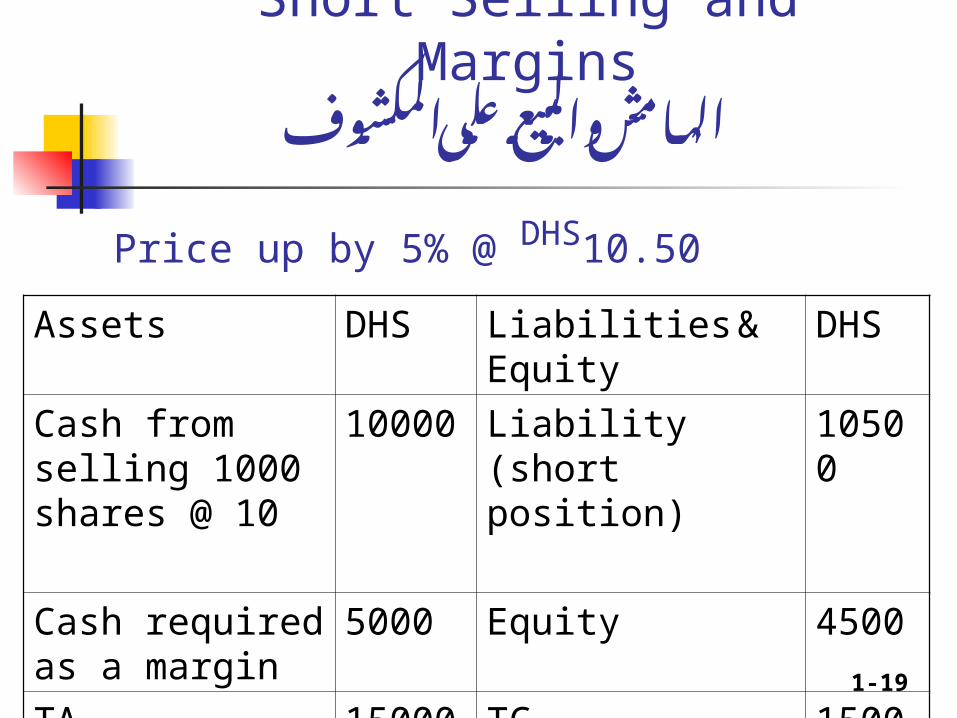

Short Selling and Marginsالهامش والبيع على المكشوف

Assets DHS Liabilities & Equity

DHS

Cash from selling 1000 shares @ 10

10000 Liability (short position)

10500

Cash required as a margin

5000 Equity 4500

TA 15000 TC 15000

Price up by 5% @ DHS10.50

1-20

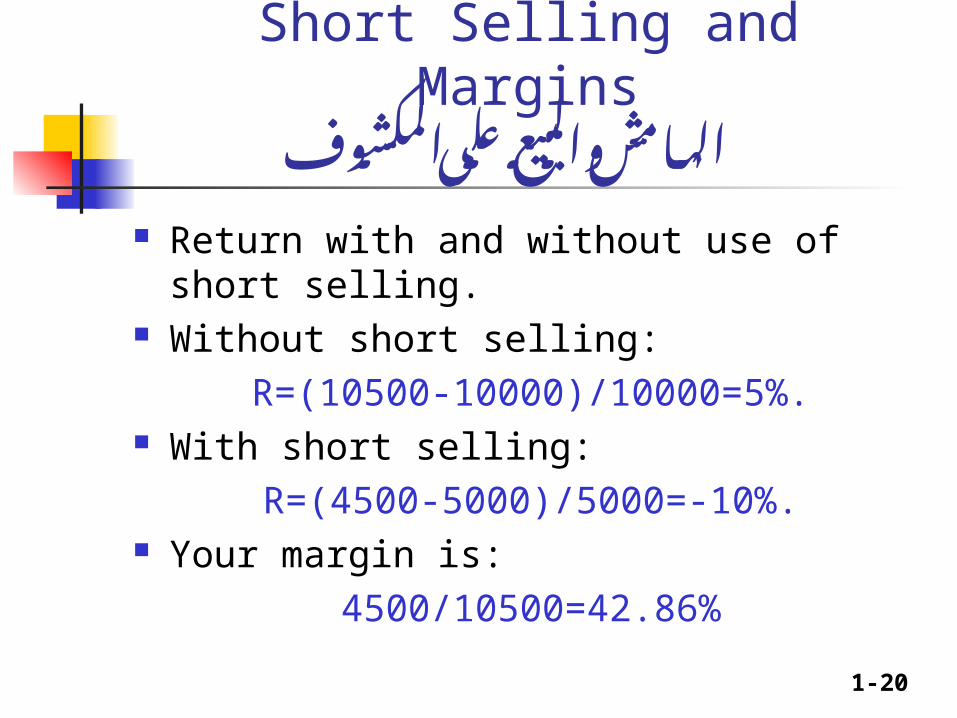

Return with and without use of short selling.

Without short selling: R=(10500-10000)/10000=5%.

With short selling: R=(4500-5000)/5000=-10%.

Your margin is:4500/10500=42.86%

Short Selling and Marginsالهامش والبيع على المكشوف

1-21

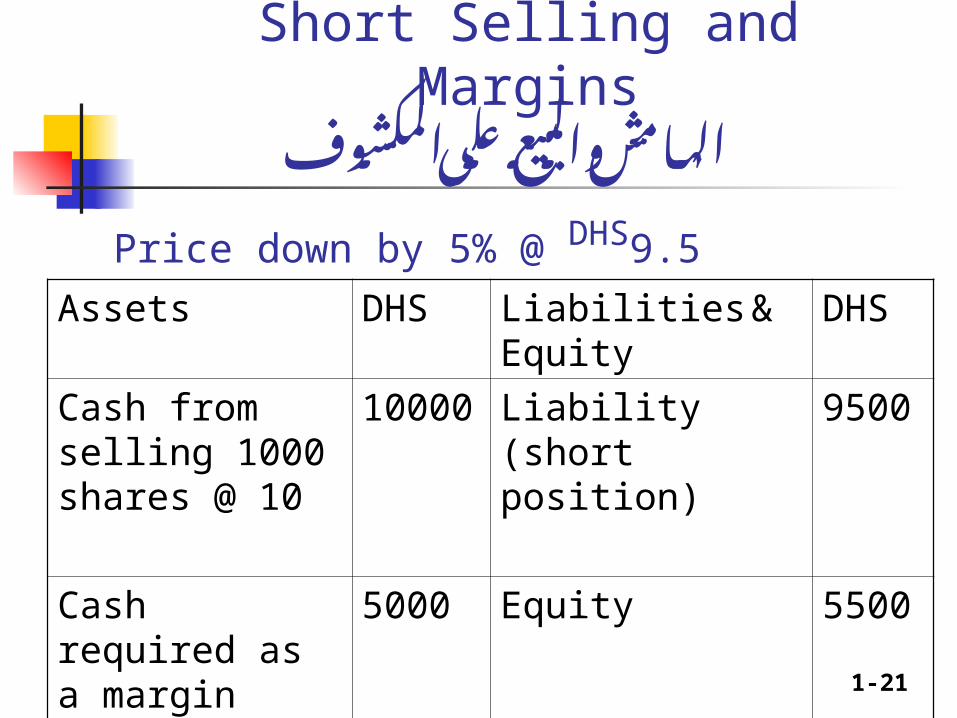

Short Selling and Marginsالهامش والبيع على المكشوف

Price down by 5% @ DHS9.5

Assets DHS Liabilities & Equity

DHS

Cash from selling 1000 shares @ 10

10000 Liability (short position)

9500

Cash required as a margin

5000 Equity 5500

TA 15000 TC 15000

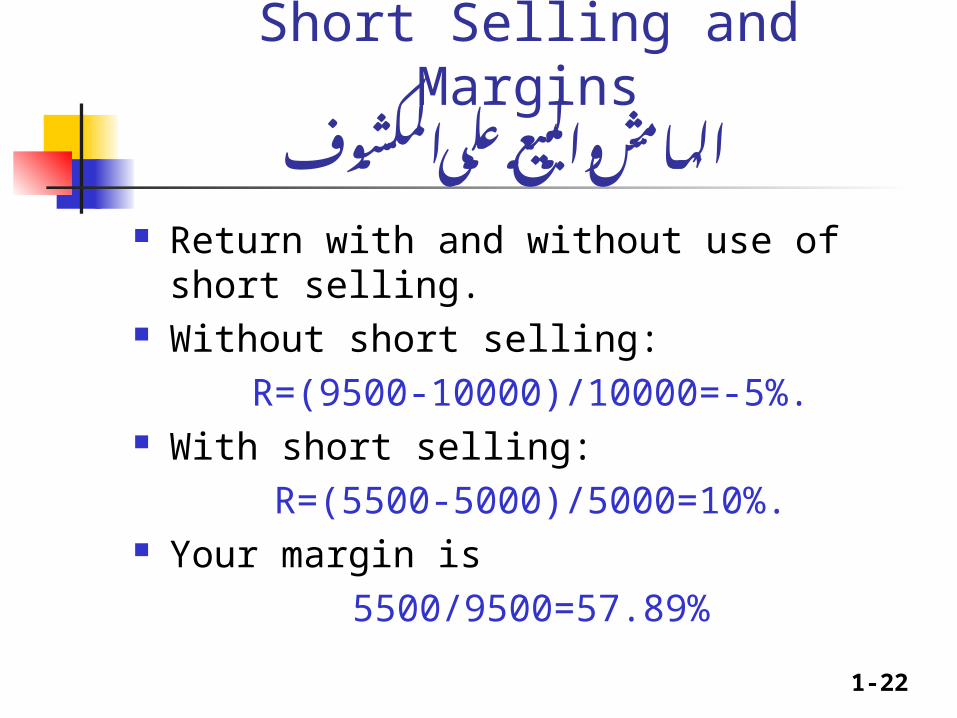

1-22

Return with and without use of short selling.

Without short selling: R=(9500-10000)/10000=-5%.

With short selling: R=(5500-5000)/5000=10%.

Your margin is 5500/9500=57.89%

Short Selling and Marginsالهامش والبيع على المكشوف

1-23

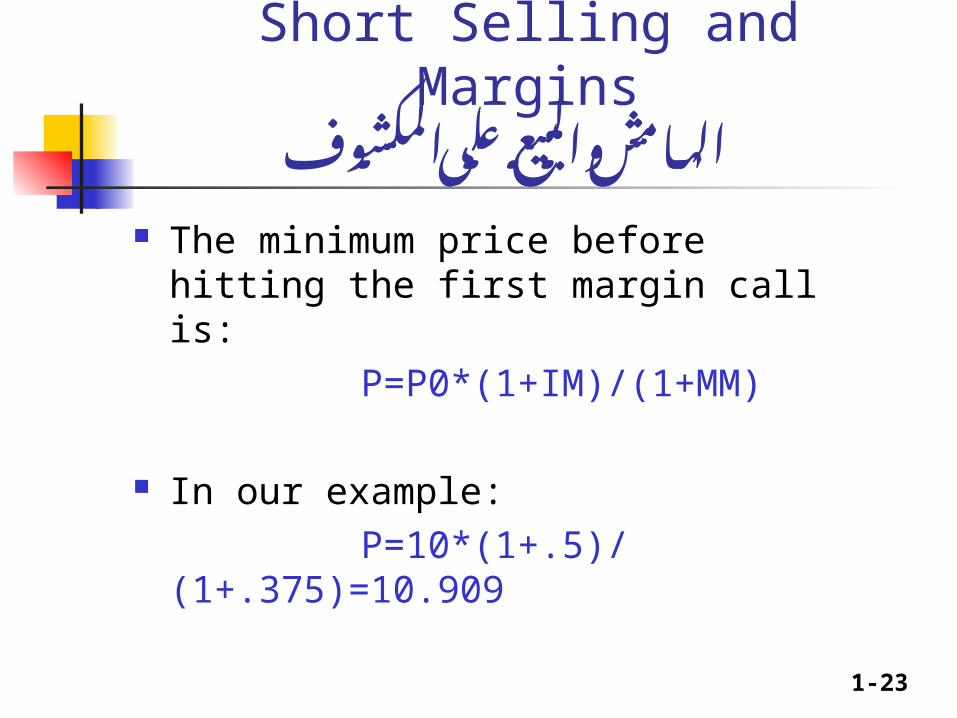

Short Selling and Marginsالهامش والبيع على المكشوف

The minimum price before hitting the first margin call is:

P=P0*(1+IM)/(1+MM)

In our example:P=10*(1+.5)/

(1+.375)=10.909

1-24

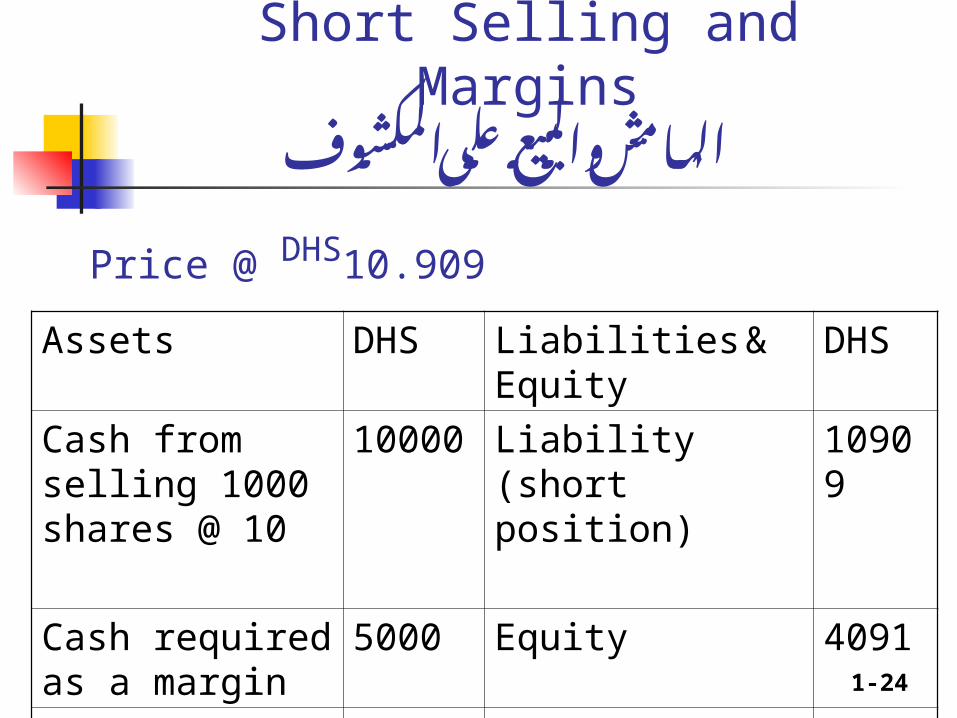

Short Selling and Marginsالهامش والبيع على المكشوف

Price @ DHS10.909

Assets DHS Liabilities & Equity

DHS

Cash from selling 1000 shares @ 10

10000 Liability (short position)

10909

Cash required as a margin

5000 Equity 4091

TA 15000 TC 15000

1-25

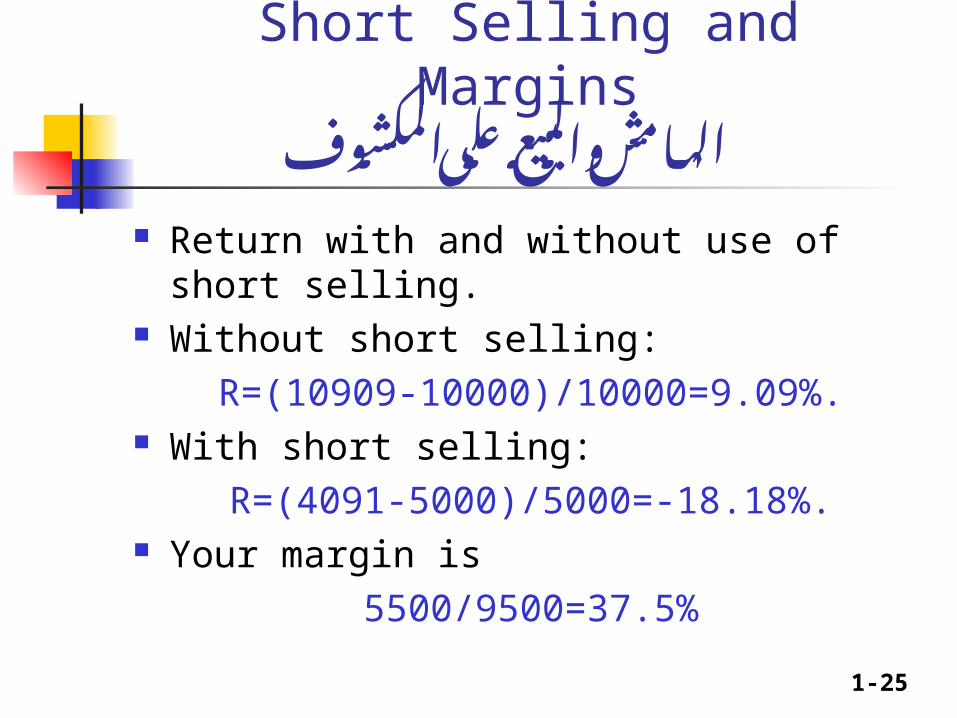

Short Selling and Marginsالهامش والبيع على المكشوف

Return with and without use of short selling.

Without short selling: R=(10909-10000)/10000=9.09%.

With short selling: R=(4091-5000)/5000=-18.18%.

Your margin is 5500/9500=37.5%

1-26

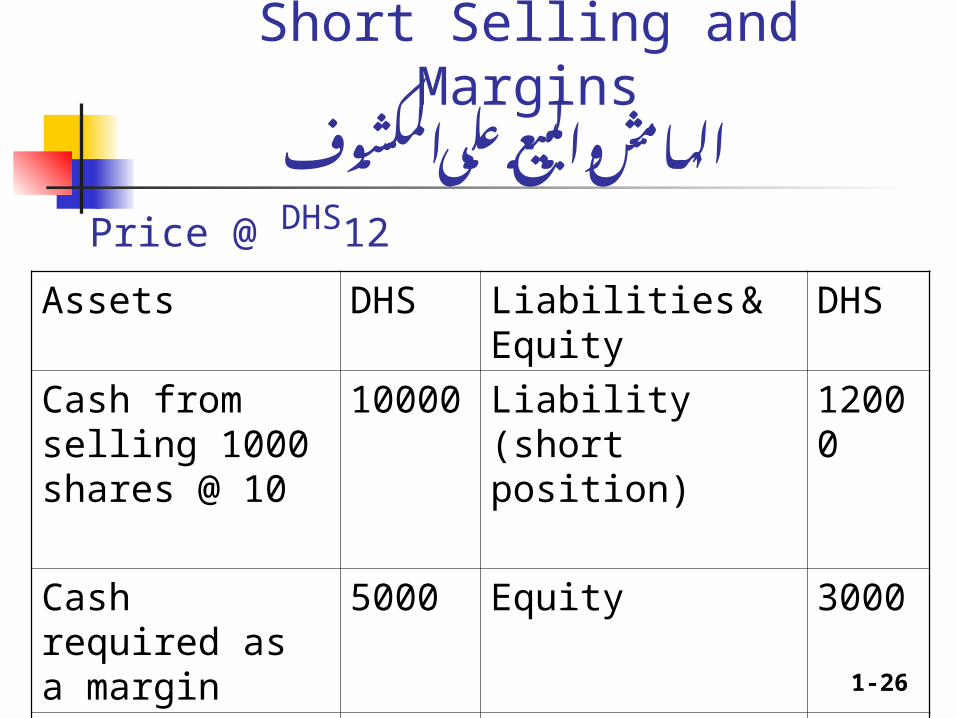

Short Selling and Marginsالهامش والبيع على المكشوف

Price @ DHS12

Assets DHS Liabilities & Equity

DHS

Cash from selling 1000 shares @ 10

10000 Liability (short position)

12000

Cash required as a margin

5000 Equity 3000

TA 15000 TC 15000

1-27

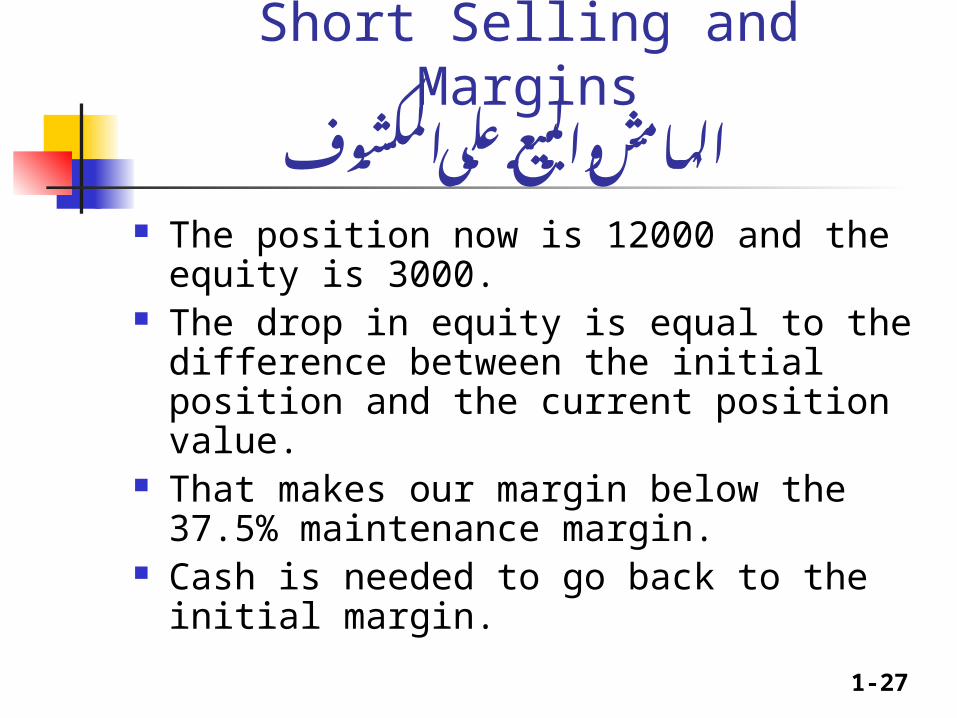

Short Selling and Marginsالهامش والبيع على المكشوف

The position now is 12000 and the equity is 3000.

The drop in equity is equal to the difference between the initial position and the current position value.

That makes our margin below the 37.5% maintenance margin.

Cash is needed to go back to the initial margin.

1-28

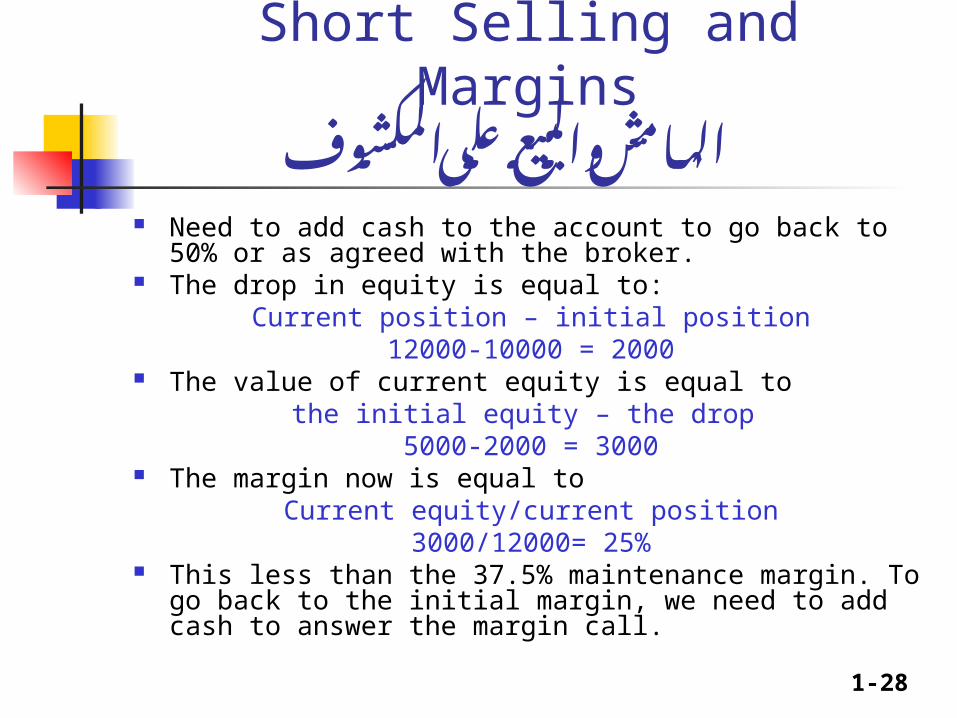

Short Selling and Marginsالهامش والبيع على المكشوف

Need to add cash to the account to go back to 50% or as agreed with the broker.

The drop in equity is equal to:Current position – initial position

12000-10000 = 2000 The value of current equity is equal to

the initial equity – the drop 5000-2000 = 3000

The margin now is equal toCurrent equity/current position

3000/12000= 25% This less than the 37.5% maintenance margin. To go

back to the initial margin, we need to add cash to answer the margin call.

1-29

Short Selling and Marginsالهامش والبيع على المكشوف

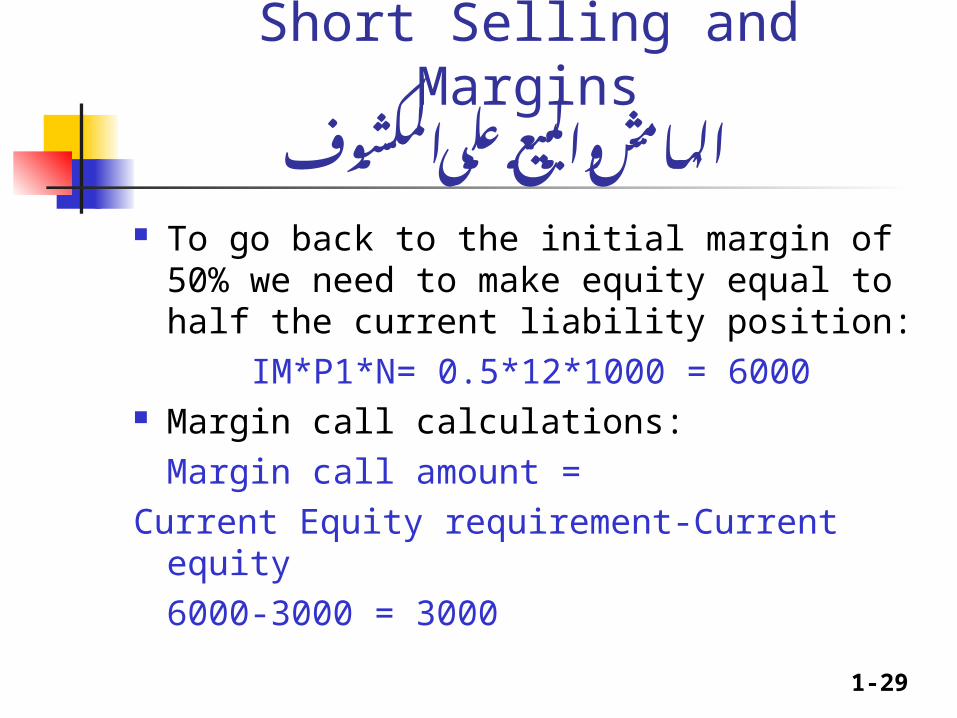

To go back to the initial margin of 50% we need to make equity equal to half the current liability position:

IM*P1*N= 0.5*12*1000 = 6000 Margin call calculations:

Margin call amount = Current Equity requirement-Current equity

6000-3000 = 3000

1-30

Short Selling and Marginsالهامش والبيع على المكشوف

See XLS file for further training

1-31

Advanced Margin Calculations

حسابات هامش اكثر تعقيدا Margin Accounts can become very complex

especially if there are multiple diverse transactions.

An example would be to calculate the margin requirements for buying a stock on margin and short selling another.

Or, you may want to add to that some other securities purchased without the use of margin.

Or, add to all of the above margin calculations for futures contracts and options premiums.

Will revisit later on.

1-32

Segregation of Clients Accounts

فصل الحسابات Client Money is separated from brokers

money. Brokers can no longer use one client

money (free of charge) to lend to other clients for stock purchases.

Benefits: Lower risk. Enhance the availability of cash for clients

withdrawals.

1-33

Segregation of Clients Accounts

فصل الحسابات

Where does the cash go? To banks. Why then move the cash from

brokers to banks? Two reasons: Banks enjoy higher liquidity and

greater readiness to answer cash demand.

Bank capital is structured to have a component that accounts for these deposits, brokers do not.

1-34

Segregation of Clients Accounts

فصل الحسابات What are the problems with brokers

practice of using clients cash to finance other clients stock purchases? Risk of illiquidity Strains on leveraged brokers accounts No brokers capital rules to protect loans

made to clients using other clients money Brokers are not allowed to make such loans

by legal definition of brokering There are no regulations for margin trading

in place.

1-35

Segregation of Clients Accounts

فصل الحسابات

What are the problems of account segregation? - Lower liquidity for trading.

Well this liquidity is not allowed in the first place and markets should have never used this extra liquidity.

1-36

Segregation of Clients Accounts

فصل الحسابات If brokers are so concerned about this

lack of liquidity and they think it is not healthy to stay without it – then why not bear the cost of borrowing from banks to create this claimed extra liquidity?

In no way does the SCA condone or encourage brokers to do so, not until the regulations that deal with that are ready.

These regulations are being worked on and will be ready very soon.

1-37

Segregation of Clients Accounts

فصل الحسابات

So, to avoid this lack of liquidity, why didn’t SCA delay account segregation until after it had such regulations in place?

Well, SCA never allowed lending by brokers and such lending should not be happening.

1-38

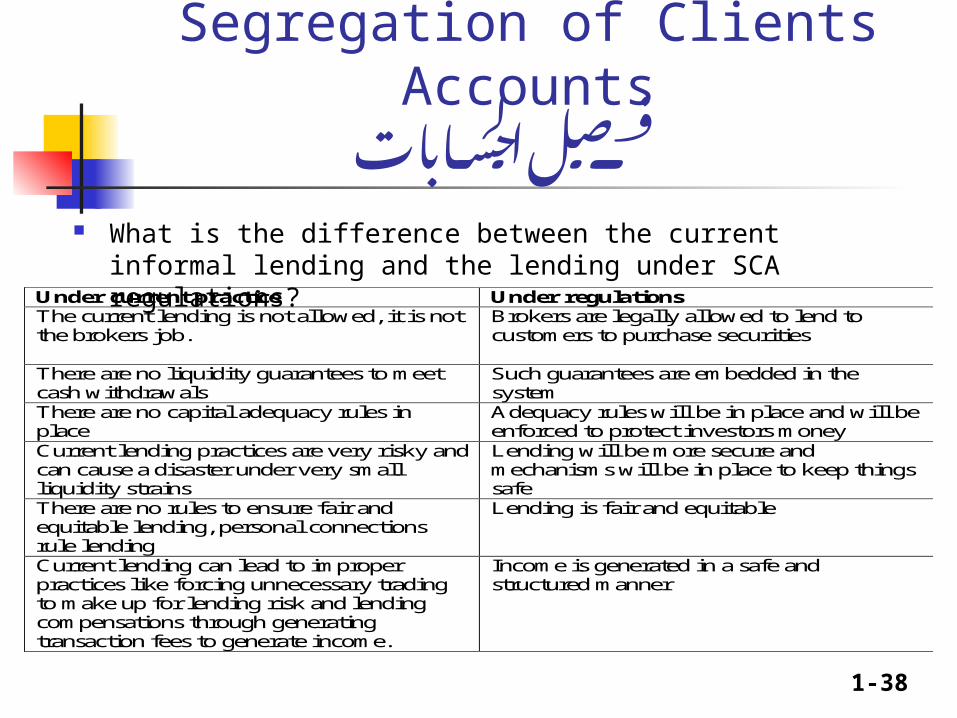

Segregation of Clients Accounts

فصل الحسابات What is the difference between the current informal

lending and the lending under SCA regulations?Under current practice Under regulations The current lending is not allowed, it is not the brokers job.

Brokers are legally allowed to lend to customers to purchase securities

There are no liquidity guarantees to meet cash withdrawals

Such guarantees are embedded in the system

There are no capital adequacy rules in place

Adequacy rules will be in place and will be enforced to protect investors money

Current lending practices are very risky and can cause a disaster under very small liquidity strains

Lending will be more secure and mechanisms will be in place to keep things safe

There are no rules to ensure fair and equitable lending, personal connections rule lending

Lending is fair and equitable

Current lending can lead to improper practices like forcing unnecessary trading to make up for lending risk and lending compensations through generating transaction fees to generate income.

Income is generated in a safe and structured manner

1-39

Segregation of Clients Accounts

الحسابات فصل

Under the regulations things will be:

Organized Safe Fair And controllable

1-40

Market Makingصانع السوق

Evidence shows that two of the main problems that emerging markets face are: Capital supply shortage and low liquidity

Market making is thought to be a good tool to remedy these problems.

1-41

Market Makingصانع السوق

The tools other than market making that are used to by emerging markets to remedy the above problems are: market segmentation (trading hours, main and

parallel markets), different trading phases (continuous and auction

trading), introduction of special incentives for submission

of limit orders (hidden reserve orders, standing orders, etc).

1-42

Market Makingصانع السوق

The implementation of the market making system contributes the following: promotes liquidity, lowers transaction costs, reduces volatility and improves daily turnover of the listed

securities

1-43

Market Makingصانع السوق

Four types of market making systems which are applied in modern stock markets: The quote-driven market making system, The centralized market making system in an

order-driven market – electronic The centralized market making system in an

order-driven market – Floor The noncentralized market making system

in an order-driven market.

1-44

Market Makingصانع السوق

1-45

Market Makingصانع السوق

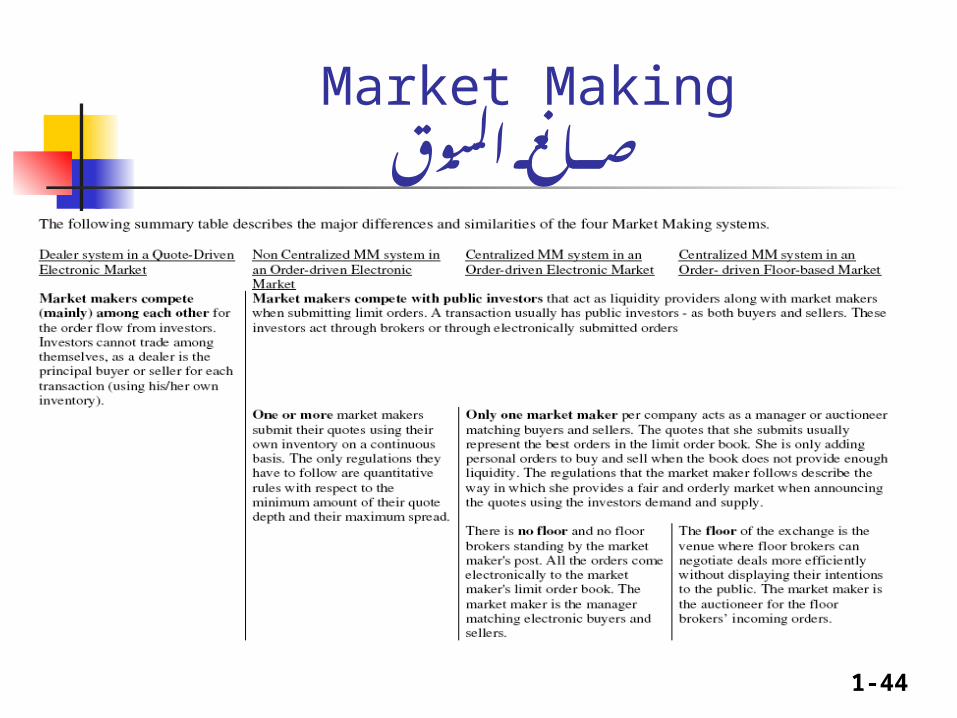

Market making (dealer) system in a quote-driven, electronic market

public investors generally cannot trade directly among themselves.

In order for buyers (sellers) to execute an order they have to contact a market maker (dealer) who uses his/her own inventory in the transaction.

There is more than one market maker per company who announces on a continuous basis quotes to buy and sell a number of shares at a particular price.

Dealers compete among themselves for more competitive bid and/or ask prices that will attract the order flow from public

Certain exchanges prohibit the use of market makers for their high liquidity stocks. In LSE, the 100 stocks that belong to the SETS system are traded electronically.

Stock markets that apply this system are the NASDAQ and the London Stock Exchange (LSE).

1-46

Market Makingصانع السوق

Centralized market making system in an order-driven, floor-based market

All potential buyers or sellers can directly trade among themselves Requires the use of a single market maker that has monopolistic

information on both the market orders and the limit order book. There exist a floor, which is a physical location where market makers

reside and interact with orders that come electronically to their terminal and with orders that come from floor brokers.

Market makers are required to announce quotes on a continuous basis that reflect both the limit order book interest and floor brokers intentions

As a result, market makers only provide the necessary liquidity from their own account when there is a lack of either a buy or a sell interest.

Typically this scenario occurs when there is a temporary disparity between supply and demand that asks for the market maker’s intervention in order to come up with an equilibrium price.

Floor-based markets where a centralized market making system is applied are the NYSE and the eight stock markets in Germany (Deutsche Börse).

1-47

Market Makingصانع السوق

Centralized market making system in an order-driven electronic market

Same as the floor-based market with a single market maker in the centralized dual role of matching buyers and sellers and providing the necessary liquidity when needed.

The only major difference is that in an order driven market there is neither a floor nor floor brokers to interact with the limit order book for providing extra liquidity.

Such a system was applied in the Amsterdam Stock Exchange (prior to its inclusion in Euronext).

1-48

Market Makingصانع السوق

Non-Centralized market making system in an order-driven electronic market.

There can be more than one per company required to announce limit orders to buy and sell

on a continuous basis They do not possess any monopolistic

information on the incoming orders or the limit order book.

They compete with investors for order flow. This system is applied in Euronext, in the Italian

Stock Exchange (ISE) and in the Athens Stock Exchange (ASE), among others.

1-49

Market Makingصانع السوق

1-50

Market Makingصانع السوق

1-51

Market Makingصانع السوق

Costs and Challenges of Applying a Market Making System to Emerging Markets: Factors for Consideration

1. current exchange design and the costs of restructuring

2. current investors’ sentiment towards the exchange both domestically and internationally

3. the market design in countries hosting the target foreign capital

4. size of the emerging market.

1-52

Market Makingصانع السوق

1- current exchange design and the costs of restructuring

The least costly to implement in terms of both machinery and technical personnel and supplies, is the noncentralized market making system.

The quote-driven market making system is much more costly as it requires more capital for the system to be fully functional.

The centralized (especially floor systems) are extremely costly.

This should not be a major problem in the UAE.

1-53

Market Makingصانع السوق

2- Current Investors’ Sentiment Towards the Exchange - Domestically and Internationally

Market making has many requirements that are not currently available in the UAE, som of which are:

Experienced financial researchers Short selling, security borrowing, high liquidity,

derivative securities to hedge MM portfolios. Do we think of a centralized MM to be trust

worthy. Collusion is possible in Quote or non centralized

1-54

Market Makingصانع السوق

3- Market Designs in Countries Hosting the Target Foreign Capital

Are foreigners used to our system Do they trust our regulations and

market participants The answer is yes, due to

the increasing international interest in the UAE

the UAE’s ability to adapt to new systems, methodologies and technologies.

1-55

Market Makingصانع السوق

4- Size of the Emerging Market Looking at the capitalization of the

markets that employ either the centralized market making system or the quote-driven market making system, we observe that these are much larger on average than other markets that follow the non-centralized market making system.

The UAE markets are small once compares to quote and centralized markets

1-56

Market Makingصانع السوق

Conclusion: Noncentralized is the closest fit to

the UAE.

1-57

What Are Conflicts of Interest and Why Are They Important?

وأهميته المصالح تعارض تعريف

Financial intermediaries engage in a variety of activities to collect, produce, and distribute information. By providing large volume of each service the realize economies of scale and by providing multiple services, they realize economies of scope.

However, these services may be competing with one another, and this creates the potential for a conflict of interest (e.g. IBF and BF)

1-58

What Are Conflicts of Interest and Why Are They Important?

وأهميته المصالح تعارض تعريف

The conflicts of interest may arise as the concealment of information or the dissemination of misleading information.

We care about these conflicts of interest because a reduction in the quality of information increases the presence of asymmetric information.

This will lead to adverse selection and moral hazard

1-59

Ethics and Conflicts of Interestالمصالح تضارب و المهنة آداب

Conflicts of interest generate incentives to provide false or misleading information. This behavior is considered unethical.

One way to limit these conflicts is to make workers aware of the ethics issues at stake, so that they are less likely to engage in unethical behavior.

1-60

Types of Conflicts of Interestالمصالح تضارب أنواع

Four areas of financial service activities that harbor the greatest potential for generating conflicts of interest. These are: Underwriting and research in investment

banking

Auditing and consulting in accounting firms

Credit assessment and consulting in credit-rating agencies

Universal banking

1-61

Underwriting and Research in Investment Banking

ودائرة االستثمار بنكير دائرة لدى المصالح تعارضالمالية االوراق شركات في المالي والتحليل الوساطة

Some investment banks both underwrite new securities sold to the public as well as provide research (recommendations) to the investing public

When revenues from underwriting exceed brokerage commissions, favorable research will attract more business, at the expense of unbiased recommendations to the investing public.

1-62

Underwriting and Research in Investment Banking

ودائرة االستثمار بنكير دائرة لدى المصالح تعارضالمالية االوراق شركات في المالي والتحليل الوساطة

In initial public offerings of equity, underwriters direct the new shares as they wish, typically to their best clients or potential new clients.

Since most IPOs are underpriced, many of these shares are immediately sold for a profit (called spinning). This immediate “profit” may appear as nothing more than payment for future business.

1-63

Auditing and Consulting in Accounting Firms

شركات لدى االستشارات وتقديم المالي التدقيقالمحاسبة

The role of auditors in public firms is to provide an unbiased view of the financial reports to reduce asymmetric information between the firm’s management and the investing public.

By also providing management advisory services (such as systems support), the auditor has an incentive to fudge the audit if the fees from other services are substantial.

1-64

Auditing and Consulting in Accounting Firms

شركات لدى االستشارات وتقديم المالي التدقيقالمحاسبة

Auditors also have a conflict of interest since they are paid by the firm they audit. If the auditor gives an unfavorable audit report, the auditor may lose the auditing business as well.

A well known case of the failure of auditors to provide unbiased reports was Arthur Andersen’s audit of Enron.

1-65

Credit Assessment and Consulting in Credit-Rating Agencies

السندات تقييم مؤسسات لدى المصالح في تضارب

Bond investors rely on credit-rating agency assessment of firm’s debt (debt ratings).

However, ratings are only provided when the firm pays the agency. Agencies, then, have an incentive provide “better” ratings to attract business.

1-66

Credit Assessment and Consulting in Credit-Rating Agencies

السندات تقييم مؤسسات لدى المصالح في تضارب

Rating agencies have also started providing firms with other services, and have the same conflicts as auditors in this regard.

1-67

Universal Bankingمالية خدمة من اكثر مقدمي لدى المصالح تضارب

واحد آن في

Universal banking refers to institutions that provide some combination of commercial banking, investment banking, and insurance services.

1-68

Universal Bankingمالية خدمة من اكثر مقدمي لدى المصالح تضارب

واحد آن في

Issuers that use the underwriting services of a bank will also benefit from sale of its products to the banks other (retail) customers. Customers should expect unbiased advice, but may not get it.

Bank managers may push investing products of its affiliates, even if they aren’t in customer’s best interest.

1-69

Universal Bankingمالية خدمة من اكثر مقدمي لدى المصالح تضارب

واحد آن في

Lenders with private (bad) information have an incentive to withhold the information during security issuances in order to get paid themselves, at the expenses of the investing public.

Lenders may offer favorable terms to secure future underwriting business.

1-70

Universal Bankingمالية خدمة من اكثر مقدمي لدى المصالح تضارب

واحد آن في

Banks may use strong-arm tactics to sell its affiliate insurance products.

1-71

When Are Conflicts of Interest a Serious Problem?

خطرة مشكلة المصالح في التضارب يصبح متى

Conflicts of interest are a problem when they lead to a decreased flow of reliable information (increased asymmetric information).

However, even with potential conflicts, the incentives (financial gain) may not be present to actually act on them.

1-72

Conflicts of Interest: Empirical Evidence.

: عملية دراسات المصالح تضارب

Empirical evidence suggests that rating agency debt ratings are unbiased, despite being paid by the firms.

Underwriting and commercial banking also appeared to be free from exploitations. Many banks spun-off their investment banking activities to separate the functions.

1-73

Conflicts of Interest: Empirical Evidence.

: عملية دراسات المصالح تضارب

Empirical evidence also suggests that the investing public recommendations are made by the underwriter’s analysts.

However, when temporary rewards to highly trusted firms may extract reputational rents from the investing public by seeking short-term gains at the expense of their future reputation.

1-74

Suggested actions to minimize conflict of interest and fraudulent practices.

الغير والممارسات المصالح تضارب لتقليل توصياتأخالقية

Beside

A- the known laws (SCA law, Company law, fraud laws, fin markets law, banking laws, exchangers law)

B- and the monitoring and examining of the SCA, Government agencies, internal and external auditing

1. Establish a Public Company Accounting Oversight Board to supervise accounting firms.

2. Prohibit public accounting firms from engaging in nonaudit services to a client it is also auditing.

3. Members of the board’s audit committee must be independent.

1-75

Suggested actions to minimize conflict of interest and fraudulent practices.

الغير والممارسات المصالح تضارب لتقليل توصياتأخالقية

4. Require the reporting of off-balance sheet activities.

5. Increase the charges for white-collar crimes and obstruction.

1-76

Suggested actions to minimize conflict of interest and fraudulent practices.

الغير والممارسات المصالح تضارب لتقليل توصياتأخالقية

1. Firms must severe the link between underwriting and research activities.

2. Firms must make public analyst recommendations and target prices.

1-77

Suggested actions to minimize conflict of interest and fraudulent practices.

الغير والممارسات المصالح تضارب لتقليل توصياتأخالقية

4. Brokerage firms required to obtain third-party, independent research for their clients.

5. Massive fines and very harsh penalties even for the smallest of violations.

1-78

Policies to Remedy Conflicts of Interest

لتضارب السيئة اآلثار من للتخلص سياساتالمصالح

A trade-off between potential conflicts of interest and economies of scale exists. Simply eliminating any potential conflict may not be the best solution:

1. The existence of a conflict of interest does not mean that the conflict will have severe consequences.

2. Even if incentives to exploit conflicts are high, eliminating the conflict may be worse if it reduces the flow of reliable information.

1-79

Policies to Remedy Conflicts of Interest

لتضارب السيئة اآلثار من للتخلص سياساتالمصالح

Leave It to the Market: an appealing approach that relies on market forces, but has the problem that the market has a “short” memory for past problems.

Regulate for Transparency: regulate mandatory disclosure, even if it is more costly than the information provided.

1-80

Policies to Remedy Conflicts of Interest

لتضارب السيئة اآلثار من للتخلص سياساتالمصالح

Supervisory Oversight: force firms to provide private information to a supervisor, who can act on it as deemed necessary.

Separation of Functions: separate those functions that create conflicts, either within firms or (in extreme cases) by not allowing those functions within the same firm.

1-81

Policies to Remedy Conflicts of Interest

لتضارب السيئة اآلثار من للتخلص سياساتالمصالح

Socialization of Information Production: look to public funding for information providers, such as credit agencies.

Non government societies, peer pressure and the code of ethics.

1-82

1-83

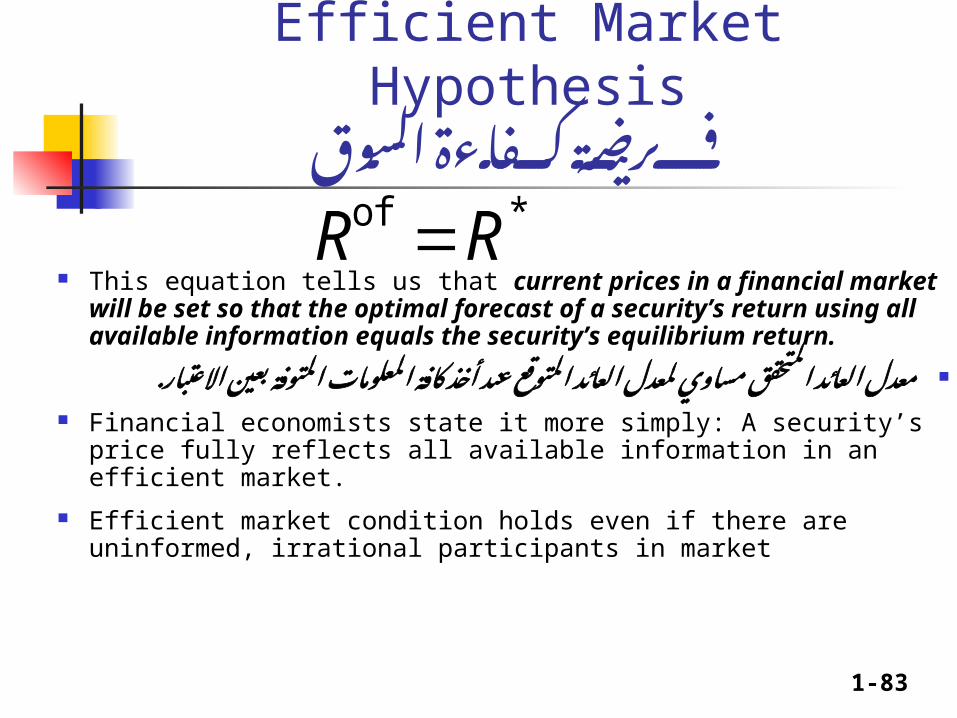

Efficient Market Hypothesisالسوق كفاءة فرضية

This equation tells us that current prices in a financial market will be set so that the optimal forecast of a security’s return using all available information equals the security’s equilibrium return.

. الاعتبار بعين المتوفة المعلومات كافة أخذ عند المتوقع العائد لمعدل مساوي المتحقق العائد معدل Financial economists state it more simply: A security’s price

fully reflects all available information in an efficient market.

Efficient market condition holds even if there are uninformed, irrational participants in market

Rof R*

1-84

Rationale Behind the Hypothesisالمراجحة عدم حالة هو الفرضية سبب

When an unexploited profit opportunity arises on a security (so-called because, on average, people would be earning more than they should, given the characteristics of that security), investors will rush to buy until the price rises to the point that the returns are normal again.

1-85

Rationale Behind the Hypothesis (cont.)المراجحة عدم حالة هو الفرضية سبب

In an efficient market, all unexploited profit opportunities will be eliminated.

Not every investor need be aware of every security and situation, as long as a few keep their eyes open for unexploited profit opportunities, they will eliminate the profit opportunities that appear because in so doing, they make a profit.

1-86

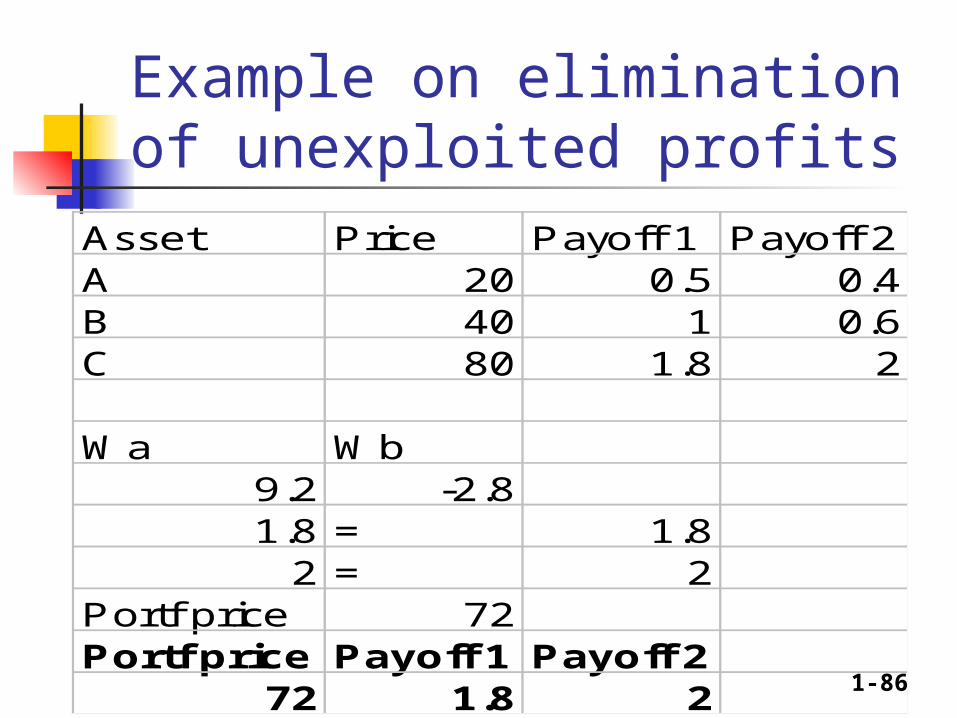

Example on elimination of unexploited profits

Asset Price Payoff 1 Payoff 2A 20 0.5 0.4B 40 1 0.6C 80 1.8 2

Wa Wb9.2 -2.81.8 = 1.8

2 = 2Portf price 72Portf price Payoff 1 Payoff 2

72 1.8 2

1-87

Stronger Version of the Efficient Market Hypothesis

السوق كفاءة لفرضية اقوى صيغة Many financial economists take the EMH one

step further in their analysis of financial markets. Not only do they define an efficient market as one in which expectations are optimal forecasts using all available information, but they also add the condition that an efficient market is one in which prices are always correct and reflect market fundamentals (items that have a direct impact on future income streams of the securities)

. على مبنية واألسعار ¬ مسبقا بها المتنبأ تلك تساوي أألسعار. تكلفة وبدون للجميع ¬ أصال المتوفرة المعلومات

1-88

Stronger Version of the Efficient Market Hypothesis (2) This stronger view of market efficiency has

several important implications in the academic field of finance:

1. It implies that in an efficient capital market, one investment is as good as any other because the securities’ prices are correct. كافة

الخطورة بمستوى المعدل العائد نفس تنتج االستثمارات2. It implies that a security’s price reflects all

available information about the intrinsic value of the security.

والمتعلقة المتوفرة المعلومات كافة تعكس االصول أسعارتسعيره المراد باألصل

1-89

Stronger Version of the Efficient Market Hypothesis (2)

3. It implies that security prices can be used by managers of both financial and nonfinancial firms to assess their cost of capital (cost of financing their investments) accurately and hence that security prices can be used to help them make the correct decisions about whether a specific investment is worth making or not.

بدقة المال رأس تكلفة تحديد في المدراء تساعدالمشاريع تقييم في وتساعدهم

1-90

Evidence on Efficient Market Hypothesis الفرضيةوالواقع Favorable Evidence للفرضية المؤيد الواقع

1. Investment analysts and mutual funds don't beat the market

2. Stock prices reflect publicly available info: anticipated announcements don't affect stock price

3. Stock prices and exchange rates close to random walk; if predictions of ∆P big, Rof > R* predictions of ∆P small

4. Technical analysis does not outperform market

1-91

Evidence in Favor of Market Efficiency Performance of Investment Analysts and

Mutual Funds should not be able to consistently beat the market

اداء من افضل محفظته اداء يكون ان الحد يمكن ال T دائمًا الكلية السوق محفظة

The “Investment Dartboard” often beats investment managers.

Mutual funds not only do not outperform the market on average, but when they are separated into groups according to whether they had the highest or lowest profits in a chosen period, the mutual funds that did well in the first period do not beat the market in the second period.

1-92

Evidence in Favor of Market Efficiency Performance of Investment Analysts

and Mutual Funds should not be able to consistently beat the market Investment strategies using inside information is

the only “proven method” to beat the market. It is illegal to trade on such information, but that is not true in all countries.

على الحصول هو السوق اداء من افضل ألداء الوحيدة الطريقةالمعتادة بالطرق السوق عليها يحصل ان قبل داخلية معلومات

1-93

Evidence in Favor of Market Efficiency Do Stock Prices Reflect Publicly

Available Information as the EMH predicts they will? Thus if information is already publicly

available, a positive announcement about a company will not, on average, raise the price of its stock because this information is already reflected in the stock price.

لن االسعار فان المعلومات كافة تعكس االسعار كانت اذامتضمن االعالن هذا مثل الن الشركة من اعالن بأي تتغير

الحالي بالسعر اصال

1-94

Evidence in Favor of Market Efficiency Do Stock Prices Reflect Publicly

Available Information as the EMH predicts they will? Early empirical evidence confirms: favorable

earnings announcements or announcements of stock splits (a division of a share of stock into multiple shares, which is usually followed by higher earnings) do not, on average, cause stock prices to rise.

الشركة ياعالن تتأثر ال االسعار ان اثبتت العملية الدراساتشابه ما او السهم انقسام او االيرادات في زيادة أي عن

ذلك

1-95

Evidence in Favor of Market Efficiency Random-Walk Behavior of Stock Prices that is,

future changes in stock prices should, for all practical purposes, be unpredictable

أألسهم ألسعًار العشوائية والحركة االرتبًاط عدم ظًاهرة If stock is predicted to rise, people will buy to

equilibrium level, if stock is predicted to fall, people will sell to equilibrium level (both in concert with EMH)

Thus, if stock prices were predictable, thereby causing the above behavior, price changes would be near zero, which has not been the case historically

1-96

Evidence in Favor of Market Efficiency Technical Analysis means to study past stock

price data and search for patterns such as trends and regular cycles, suggesting rules for when to buy and sell stocks

الفعًال السوق فرضية حسب للوقت مضيعة التقني التحليل The EMH suggests that technical analysis is a waste

of time The simplest way to understand why is to use the

random-walk result that holds that past stock price data cannot help predict changes. Therefore, technical analysis, which relies on such data to produce its forecasts, cannot successfully predict changes in stock prices

1-97

Evidence on Efficient Market Hypothesis Unfavorable Evidence صحة تنفي دالئل

الفرضية1. Small-firm effect: small firms have

abnormally high returns

2. January effect: high returns in January3. Market overreaction4. Excessive volatility5. Mean reversion6. New information is not always

immediately incorporated into stock prices

1-98

THE PRACTICING MANAGER: Implications for Investing

المالية بالوساطة الفرضية عالقةواالستثمار

1. How valuable are published reports by investment advisors?

2. Should you be skeptical of hot tips?

3. Do stock prices always rise when there is good news?

4. Efficient Markets prescription for investor

1-99

Implications for Investing How valuable are published reports

by investment advisors? تحديد في المالية التقارير قيمة هي ما

االسعار؟

1-100

Implications for Investing1. Should you be skeptical of hot tips?

الى تؤدي التي السرية االخبار مصداقية في نشك هلالسريع؟ الغنى

YES. The EMH indicates that you should be skeptical of hot tips since, if the stock market is efficient, it has already priced the hot tip stock so that its expected return will equal the equilibrium return.

Thus, the hot tip is not particularly valuable and will not enable you to earn an abnormally high return.

1-101

Implications for Investing

1. Should you be skeptical of hot tips? As soon as the information hits the

street, the unexploited profit opportunity it creates will be quickly eliminated.

The stock’s price will already reflect the information, and you should expect to realize only the equilibrium return.

1-102

Implications for Investing Do stock prices always rise when there is

good news?

؟¬ دائما جيدة اخبار توفر مع ايجابيا االسعار تتفاعل هل NO. In an efficient market, stock prices will

respond to announcements only when the information being announced is new and unexpected.

So, if good news was expected (or as good as expected), there will be no stock price response.

And, if good news was unexpected (or not as good as expected), there will be a stock price response.

1-103

Implications for Investing Efficient Markets prescription

for investor

تكاليف في توفر الكفؤة السوق فرضيةالتحويالت

Investors should not try to outguess the market by constantly buying and selling securities. This process does nothing but incur commissions costs on each trade.

1-104

Implications for Investing Efficient Markets prescription

for investor المستمر االتجار من افضل واالحتفاظ الشراء

سريعة ارباح عن بحثا Instead, the investor should pursue a “buy

and hold” strategy—purchase stocks and hold them for long periods of time. This will lead to the same returns, on average, but the investor’s net profits will be higher because fewer brokerage commissions will have to be paid.

1-105

Implications for Investing Efficient Markets prescription for investor

صغار تنصح الكفؤة السوق فرضية فان التحويل تكاليف من وللتخلصالمتعددة لفوائدها االستثمار صناديق في باالستثمار المستثمرين

It is frequently a sensible strategy for a small investor, whose costs of managing a portfolio may be high relative to its size, to buy into a mutual fund rather than individual stocks. Because the EMH indicates that no mutual fund can consistently outperform the market, an investor should not buy into one that has high management fees or that pays sales commissions to brokers but rather should purchase a no-load (commission-free) mutual fund that has low management fees.

1-106

Behavioral Finance التمويلالسلوكي Dissatisfaction with using the EMH to explain events

like 1987’s Black Monday gave rise to the new field of behavioral finance, in which concepts from psychology, sociology, and other social sciences are applied to understand the behavior of securities prices

االفراد سلوك باستخدام االسعار في التغير تفسير تحاول النظرية هذهوالمجتمعات

EMH suggests that “smart money” would engage in short sales to combat overpriced securities, yet short sale volume is low, leading to behavior theories about “loss aversion”

Other behavior analysis points to investor overconfidence as perpetuating stock price bubbles

1-107

Why Should Capital MarketsBe Efficient?

كقؤة؟ االسواق تكون ان يجب لماذا

The premises of an efficient market A large number of competing profit-

maximizing participants analyze and value securities, each independently of the others

New information regarding securities comes to the market in a random fashion

Profit-maximizing investors adjust security prices rapidly to reflect the effect of new information

Conclusion: the expected returns implicit in the current price of a security should reflect its risk

1-108

AlternativeEfficient Market Hypotheses (EMH)

الكفؤة السوق فرضية مشتقات من

Random Walk Hypothesis – changes in security prices occur randomly

العشوائي التحرك Fair Game Model – current market price

reflect all available information about a security and the expected return based upon this price is consistent with its risk

العادلة اللعبة Efficient Market Hypothesis (EMH) - divided

into three sub-hypotheses depending on the information set involved

الكفؤة 3 السوق لفرضية مستويات

1-109

Efficient Market Hypotheses (EMH)

Weak-Form EMH - prices reflect all security-market information

الضعيفة الصيغة Semistrong-form EMH - prices reflect all

public information المتوسطة الصيغة

Strong-form EMH - prices reflect all public and private information

القوية الصيغة

1-110

Weak-Form EMHال التداول وحجوم االسعار عن التاريخية المعلومات معرفة

المعدل الربح معدل فوق ارباح أي كسب في تفيدبالمخاطر

Current prices reflect all security-market information, including the historical sequence of prices, rates of return, trading volume data, and other market-generated information

This implies that past rates of return and other market data should have no relationship with future rates of return

1-111

Semistrong-Form EMHال ومعرفتها االسعار في اصال متضمنة العامة المعلومات

المعدل الربح معدل فوق ارباح أي كسب في تفيدبالمخاطر

Current security prices reflect all public information, including market and non-market information

This implies that decisions made on new information after it is public should not lead to above-average risk-adjusted profits from those transactions

1-112

Strong-Form EMHفي تفيد ال والخاصة والعامة السابقة المعلومات معرفة

بالمخاطر المعدل الربح معدل فوق ارباح أي كسب

Stock prices fully reflect all information from public and private sources

This implies that no group of investors should be able to consistently derive above-average risk-adjusted rates of return

This assumes perfect markets in which all information is cost-free and available to everyone at the same time

1-113

Tests and Results of Weak-Form EMHالضعيفة للصيغة العملية الفحوص

Statistical tests of independence between rates of return Autocorrelation tests have mixed

results Active Vs. Buy and Hold show

varying results

1-114

Tests and Results of Weak-Form EMHلها مؤيد وبعضها الضعيفة الصيغة فشل يري بعضها

Comparison of trading rules to a buy-and-hold policy is difficult because trading rules can be complex and there are too many to test them all

Filter rules yield above-average profits, but only before taking into account transactions costs

Trading rule results have been mixed, and most have not been able to beat a buy-and-hold policy

Results generally support the weak-form EMH, but results are not unanimous

1-115

Tests of the Semistrong Form of Market Efficiency

المتوسطة للصيغة العملية الفحوص

These tests involve a joint hypothesis and are dependent both on market efficiency and the asset pricing model used

المزدوجة الفرضية مشكلةThey use:1- Event studies الحدث دراسات2- Trading volumes and price عالقة دراسات

التداول بحجم السعر3- Multipliers المضاعفات

1-116

Tests and Results of Semistrong-Form EMH

The January Anomaly التوقيت ظاهرة Stocks with negative returns

during the prior year had higher returns right after the first of the year

Tax selling toward the end of the year has been mentioned as the reason for this phenomenon

Such a seasonal pattern is inconsistent with the EMH

1-117

Tests and Results of Semistrong-Form EMH

Other calendar effects All the market’s cumulative

advance occurs during the first half of trading months

Monday/weekend returns were significantly negative

1-118

Tests and Results of Semistrong-Form EMH

The size effect (total market value) ظاهرةالصغيرة الشركات

The studies indicate that risk-adjusted returns for extended periods indicate that the small firms consistently experienced significantly larger risk-adjusted returns than large firms

The small-firm effect is not stable from year to year

Firm size is a major efficient market anomaly

1-119

Tests and Results of Semistrong-Form EMH

Neglected Firms المهملة الشركات ظاهرة Firms divided by number of

analysts following a stock Neglected firm effect caused by

lack of information and limited institutional interest

Neglected firm concept applied across size classes

1-120

Tests and Results of Semistrong-form EMH

Trading volume التداول حجم ظاهرة Studied relationship between returns,

market value, and trading activity. No significant difference was found

between the mean returns of the highest and lowest trading activity portfolios

1-121

Tests and Results of Semistrong-Form EMH

Ratio of Book Value of a firm’s Equity to Market Value of its equity مضاعف ظاهرةالملكية Significant positive relationship found

between current values for this ratio and future stock returns

Results inconsistent with the EMH Size and BV/MV dominate other ratios such

as E/P ratio or leverage الربحية مضاعف ظاهرة

1-122

Evidence Against Market Efficiency Market Overreaction: recent research

suggests that stock prices may overreact to news announcements and that the pricing errors are corrected only slowly

الجديدة للمعلومًات الفعل ردة مبًالغة ظًاهرة When corporations announce a major change in

earnings, say, a large decline, the stock price may overshoot, and after an initial large decline, it may rise back to more normal levels over a period of several weeks.

This violates the EMH because an investor could earn abnormally high returns, on average, by buying a stock immediately after a poor earnings announcement and then selling it after a couple of weeks when it has risen back to normal levels.

1-123

Evidence Against Market Efficiency Excessive Volatility: the stock market

appears to display excessive volatility; that is, fluctuations in stock prices may be much greater than is warranted by fluctuations in their fundamental value.

المفرط التباين ظاهرة Researchers have found that fluctuations in the S&P

500 stock index could not be justified by the subsequent fluctuations in the dividends of the stocks making up this index.

Other research finds that there are smaller fluctuations in stock prices when stock markets are closed, has produced a consensus that stock market prices appear to be driven by factors other than fundamentals.

1-124

Evidence Against Market Efficiency Mean Reversion: Some researchers have

found that stocks with low returns today tend to have high returns in the future, and vice versa.

الربح معدل الى الرجوع ظاهرة Hence stocks that have done poorly in the

past are more likely to do well in the future because mean reversion indicates that there will be a predictable positive change in the future price, suggesting that stock prices are not a random walk.

Newer data is less conclusive; nevertheless, mean reversion remains controversial.

1-125

Evidence Against Market Efficiency New Information Is Not Always

Immediately Incorporated into Stock Prices

المعلومًات مع التجًاوب في السوق تأخر ظًاهرةالجديدة

Although generally true, recent evidence suggests that, inconsistent with the efficient market hypothesis, stock prices do not instantaneously adjust to profit announcements.

Instead, on average stock prices continue to rise for some time after the announcement of unexpectedly high profits, and they continue to fall after surprisingly low profit announcements.

1-126

Tests and Results of Semistrong-Form EMH

الوسطية السوق كفاءة اختبار في الحدث دراسات استخدام Event studies examine how fast stock prices

adjust to specific significant economic events Stock split studies show that splits do not

result in abnormal gains after the split announcement, but before

Initial public offerings seems to be underpriced by almost 18%, but that varies over time, and the price is adjusted within one day after the offering

Listing of a stock on an national exchange may offer some short term profit opportunities for investors

1-127

Tests and Results of Semistrong-Form EMH

Event studies (continued) Stock prices quickly adjust to

unexpected world events and economic news and hence do not provide opportunities for abnormal profits

Announcements of accounting changes are quickly adjusted for and do not seem to provide opportunities

Stock prices rapidly adjust to corporate events such as mergers and offerings

The above studies provide support for the semistrong-form EMH

1-128

Summary on the Semistrong-Form EMH

Evidence is mixed: بالصيغة كفؤ السوق ان تثبت الحدث دراسات معظم

الوسطية strong support from numerous event

studies Studies on predicting rates of return for a

cross-section of stocks indicates markets are not semistrong efficient (e.g. use of multipliers like PE, or calendar effects

1-129

Tests and Results of Strong-Form EMHالقوية للصيغة العملية الفحوص

Strong-form EMH contends that stock prices fully reflect all information, both public and private

This implies that no group of investors has access to private information that will allow them to consistently earn above-average profits

1-130

Testing Groups of Investors

Corporate insiders Stock exchange specialists Security analysts Professional money managers (e.g.

investment funds managers)

1-131

Corporate Insider Trading اتجار فحصت دراساتالداخليين

Corporate insiders include major corporate officers, directors, and owners of 10% or more of any equity class of securities

Insiders must report to the SEC each month on their transactions in the stock of the firm for which they are insiders

These insider trades are made public about six weeks later and allowed to be studied

1-132

Corporate Insider Tradingاعلى عائد معدل يحصلون الداخليين ان وجدت الدراسات

الخارجيين منالقوية بالصيغة كفؤ غير السوق ان أي

Corporate insiders generally experience above-average profits especially on purchase transaction

This implies that many insiders had private information from which they derived above-average returns on their company stock

1-133

Corporate Insider Trading

Studies showed that public investors who traded with the insiders based on announced transactions would have enjoyed excess risk-adjusted returns (after commissions), but the markets now seem to have eliminated this inefficiency (soon after it was discovered)

1-134

Stock Exchange Specialists على يحصلون الذين المختصين ان وجدت الدراسات

اعلى عائد معدل يحصلون العامة عليها يحصل ال معلوماتالعامة من

القوية بالصيغة كفؤ غير السوق ان أي

Specialists have monopolistic access to information about unfilled limit orders

You would expect specialists to derive above-average returns from this information

The data generally supports this expectation

1-135

Security Analystsيحصلون الذين الماليين المحللين ان وجدت الدراسات

عائد معدل يحصلون العامة عليها يحصل ال معلومات علىالعامة من اعلى

القوية بالصيغة كفؤ غير السوق ان أي

Tests have considered whether it is possible to identify a set of analysts who have the ability to select undervalued stocks

This looks at whether, after a stock selection by an analyst is made known, a significant abnormal return is available to those who follow their recommendations

1-136

The Value Line Enigma (PSE is considering similar system) في االكاديميين ان وجدت الدراسات

VL غيرهم من اعلى عائد معدل يحصلونالقوية بالصيغة كفؤ غير السوق ان أي

Value Line (VL) publishes financial information on about 1,700 stocks

The report includes a timing rank from 1 down to 5

Firms ranked 1 substantially outperform the market

Firms ranked 5 substantially underperform the market

Changes in rankings result in a fast price adjustment

1-137

Professional Money Managersعلى يحصلون الذين االستثمار مدراء ان وجدت الدراساتاعلى عائد معدل يحصلون العامة عليها يحصل ال معلومات

العامة منالقوية بالصيغة كفؤ غير السوق ان أي

Trained professionals, working full time at investment management

If any investor can achieve above-average returns, it should be this group

If any non-insider can obtain inside information, it would be this group due to the extensive management interviews that they conduct and due to high stakes in owned firms

1-138

Performance of Professional Money Managers

Most tests examine mutual funds New tests also examine trust

departments, insurance companies, and investment advisors

Risk-adjusted, after expenses, returns of mutual funds generally show that most funds did not match aggregate market performance

1-139

Conclusions Regarding the Strong-Form EMH

القوية بالصيغة كفؤ غير السوق ان وجدت الدراساتاالحيان معظم في

Mixed results, but not much support Tests for corporate insiders and stock

exchange specialists do not support the hypothesis (Both groups seem to have monopolistic access to important information and use it to derive above-average returns)

1-140

Conclusions Regarding the Strong-Form EMH

Tests results for analysts are concentrated on Value Line rankings

Results have changed over time. Currently tend to support EMH

Individual analyst recommendations seem to contain significant information

Performance of professional money managers seem to provide support for strong-form EMH

1-141

Efficient Markets and Technical Analysisالفني والتحليل الكفؤة السوق نظرية

Assumptions of technical analysis directly oppose the notion of efficient markets

الن السوق بكفاءة يعترف ال الفني التحليلللجميع متوفرة غير المعلومات

Technicians believe that new information is not immediately available to everyone, but disseminated from the informed professional first to the aggressive investing public and then to the masses

1-142

Efficient Markets and Technical Analysisالفني والتحليل الكفؤة السوق نظرية

Technicians also believe that investors do not analyze information and act immediately - it takes time

ال المستثمرين ان يقولون الفنيين المحللين ان كماالسعار في نمطية يخلق مما بسرعة المعلومات يللون

منها واالستفادة تحديدها يمكن Therefore, stock prices move to a new

equilibrium after the release of new information in a gradual manner, causing trends in stock price movements that persist for periods

1-143

Efficient Markets and Technical Analysisالفني والتحليل الكفؤة السوق نظرية

تثبت لم التي الفنية االستراتيتجيات من الكثير يوجدعادية الغير االرباح جني على معظمها قدرة

Technical analysts develop systems to detect movement to a new equilibrium (breakout) and trade based on that

Contradicts rapid price adjustments indicated by the EMH

If the capital market is weak-form efficient, a trading system that depends on past trading data can have no value

1-144

Efficient Markets and Fundamental Analysisاألساسي والتحليل الكفؤة السوق نظرية

لالصول حقيقية قيمة بوجود يؤمن االساسي التحليلللعامة المتوفرة المعلومات من حسابها ويمكن

Fundamental analysts believe that there is a basic intrinsic value for the aggregate stock market, various industries, or individual securities and these values depend on underlying economic factors

Investors should determine the intrinsic value of an investment at a point in time and compare it to the market price

1-145

Efficient Markets and Fundamental Analysisاألساسي والتحليل الكفؤة السوق نظرية

االرباح جني على قدرتك تحدد التحليل على قدرتك If you can do a superior job of

estimating intrinsic value you can make superior market timing decisions and generate above-average returns

This involves aggregate market analysis, industry analysis, company analysis, and portfolio management

Intrinsic value analysis should start with aggregate market analysis

1-146

Efficient Markets and Investment Fund Management

االستثمارية المحافظ وادارة الكفؤة السوق نظرية

من اكثر مكاسب يجنوا ان يستطيعوا الجيدين المدراءقدراتهم بسبب المعدل

Investment Fund Managers with Superior Analysts

concentrate efforts in stocks that do not receive the attention given by institutional Investment Fund managers to the top-tier stocks

the market for these neglected stocks may be less efficient than the market for large well-known stocks

1-147

Efficient Markets and Investment Fund Management

االستثمارية المحافظ وادارة الكفؤة السوق نظرية

ادارة خطوات باتباع عادي عائد على يحصلوا العاديين المدراءعليها المتعارف المحافظ

Investment Fund Managers without Superior Analysts Determine and quantify your client's risk

preferences Construct the appropriate portfolio Diversify completely on a global basis to

eliminate all unsystematic risk Maintain the desired risk level by rebalancing

the portfolio whenever necessary Minimize total transaction costs

1-148

The Rationale and Use of Index Fundsالحصول ثم ومن السوق لمحفظة مطابقة محافظ بناءهو مخاطرته وبمستوى السوق لعائد مساوي عائد على

¬ كفؤا السوق يكون عندما المثلى االستثمار طريقة

Efficient capital markets and a lack of superior analysts imply that many Investment Funds should be managed passively (so their performance matches the aggregate market, minimizes the costs of research and trading)

Institutions created market (index) funds which duplicate the composition and performance of a selected index series

1-149

Behavioral Financeالسلوكي التمويل علم

It is concerned with the analysis of various psychological traits of individuals and how these traits affect the manner in which they act as investors, analysts, and portfolio managers

1-150

Insights from Behavioral Finance

Growth companies will usually not be growth stocks due to the overconfidence of analysts regarding future growth rates and valuations

ال قد التي النمو شركات في للمحللين الزائدة الثقةخسائر الى تؤدي يعتقدون كما تنمو

Notion of “herd mentality” of analysts in stock recommendations or quarterly earnings estimates is confirmed

كالقطيع يتصرفون الناس