09.10.2011 Infrastructure building the mining supply chain, Jim Dwyer

Upload

the-business-council-of-mongoliaCategory

view

226download

0

CENTRAL BANK POLICY

Enkhjargal Danzanbaljir

Mongolia Investment Summit-2011

London

OUTLINE

I. State Monetary Policy Guideline for 2012

II. Economic core indicators

III. Policy measures of the Bank of Mongolia: 2011

IV. Inflation projection

V. BOP, exchange rate indicators

VI. Banking sector indicators

Objective of the Central Bank

According to the Central Bank law, …

… the main objective of the Bank of Mongolia is ensuring stability of Togrog.

… within this, main objective the Bank of Mongolia shall also promote balanced and sustained development of the national economy, through maintaining the stability the national economy, through maintaining the stability of money, financial markets and the banking system.

The Bank of Mongolia formulates monetary policy guidelines and submits it to the Parliament every year.

I. State Monetary Policy Guideline for 2012

Monetary policy will aim at maintaining macroeconomic andfinancial stability and enhancing sustained economic growth overthe medium and long term.

Under the monetary policy framework:

• Monetary policy will aim at maintaining CPI-inflation at a single-digit level for 2012 and below 8 % for 2013-2014.digit level for 2012 and below 8 % for 2013-2014.

• Will establish macro prudential policy framework for (Fiscalprudential policy):� Ensuring sustainable economic growth

� Strengthening financial stability and soundness

• To increase capacity framework to manage inflation expectations.

• To continue open transparent policy on its monetary policy and itsinstruments to the public.

.

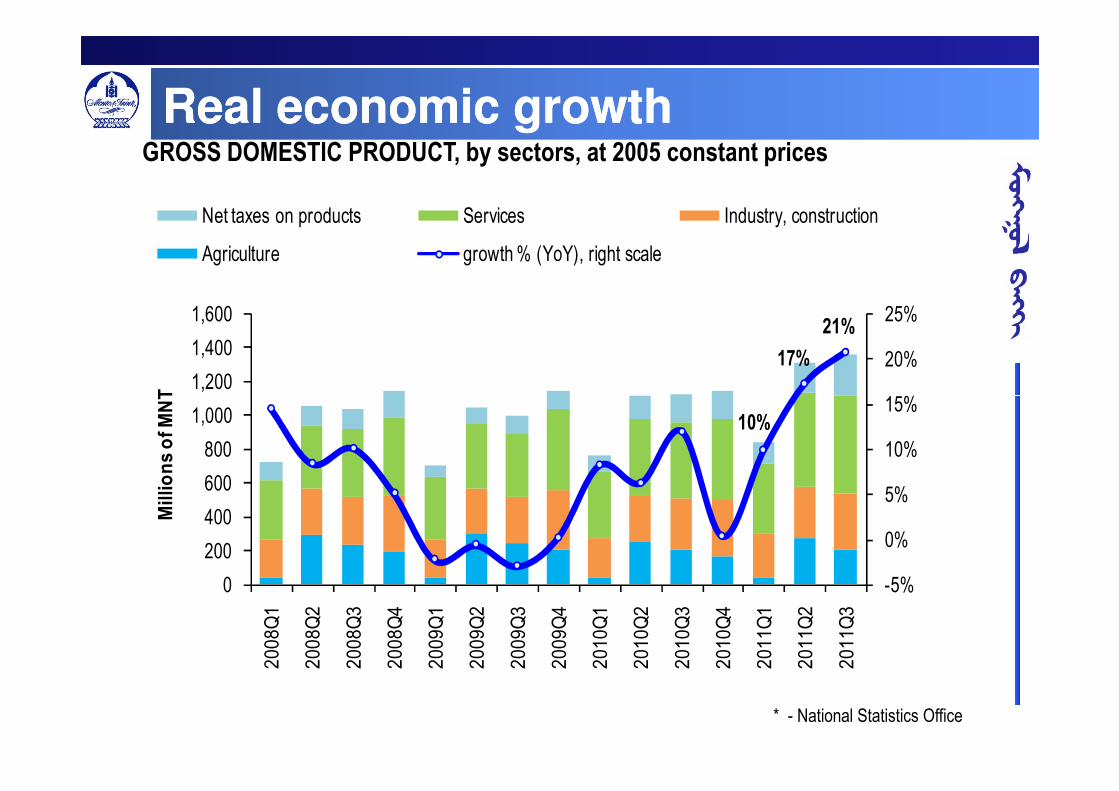

Real economic growthReal economic growthGROSS DOMESTIC PRODUCT, by sectors, at 2005 constant prices

17%

21%

15%

20%

25%

1,200

1,400

1,600

Millions of MNT

Net taxes on products Services Industry, construction

Agriculture growth % (YoY), right scale

* - National Statistics Office

10%

-5%

0%

5%

10%

15%

0

200

400

600

800

1,000

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

2011Q3

Millions of MNT

H1 H2 H1 H2 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Total GDP 1782.4 2181.6 1759.4 2154.3 764.5 1119.0 1126.2 1153.2 840.3 1312.3 1360.5

growth % (YoY) 10.8% 7.4% -1.3% -1.3% 8.2% 6.3% 12.0% 0.4% 9.9% 17.3% 20.8%

Agriculture 338.5 429.9 351.0 445.4 35.9 257.4 204.7 166.1 38.0 272.8 204.7

growth % (YoY) 4.7% 4.6% 3.7% 3.6% -15.6% -16.5% -15.2% -18.5% 5.7% 6.0% 0.0%

2008 2009 2010 2011

Real economic growthReal economic growthGROSS DOMESTIC PRODUCT, by sectors, at 2005 constant prices

Industry, construction 493.8 621.6 482.5 628.3 240.8 275.7 305.7 336.2 263.3 305.5 338.4

growth % (YoY) 0.2% -1.6% -2.3% 1.1% 10.1% 4.5% 11.0% -4.7% 9.3% 10.8% 10.7%

Services 732.2 867.7 750.7 861.8 391.4 448.1 451.2 479.6 417.2 558.2 574.3

growth % (YoY) 17.4% 15.9% 2.5% -0.7% 4.7% 18.9% 19.4% -0.9% 6.6% 24.6% 27.3%

Net taxes on products 217.9 262.3 175.2 218.7 96.3 137.8 164.5 171.3 121.8 175.7 243.0

28.7% 9.2% -19.6% -16.6% 34.8% 32.9% 48.5% 58.6% 26.4% 27.5% 47.7%

* - National Statistics Office

II. Economic outlook: Core indicators

Indicators2007

X

2008

X

2009

X

2010

X

2011

X

2012

Forecast

Inflation (National)

(annual change)14.7 27.9 0.9 11.3 10.9% 18.4%

Meat price

(annual change)17.9 21.3 -16.5 27.5 30.3% na

Core inflation

(annual change)12.9 24.9 2.9 8.5 10.3% na

• At the beginning of 2011,

meat price increased

sharply due to foot and

mouth disease but in

March to May meat price

went down therefore,

inflation decreased.

• Core inflation continued to

increase from February

2011 until July 2011.

However, in August it had Broad money

(annual change)46.4% 4.1% 13.3% 45.0% 57.2% 30.4%

Reserve money

(annual change)17.7% 8.3% 53.4% 10.5% 83.8% 33.4%

Loan

(annual change)70.9% 39.5% -2.7% 18.0% 69.0% 32.6%

Loan nominal rate

(domestic currency) 21.3% 21.0% 21.9% 19.5% 15.9% na

Loan nominal rate

(foreign currency)13.8% 16.7% 15.8% 13.8% 13.3% na

GDP growth 12.8% 9.8% 0.1% 6.3% 12.2%* 18.4%

However, in August it had

decline due to high growth

in same period of the last

year. In September it went

up again.

• Inflation pressure would be

increased result from lower

lending rate and high

growth of money supply

and loan.

* GDP annual growth as calculating sum

of four quarters, as of the second quarter

of 2011

II. Economic outlook: Inflation ...2011:

• In first 2 months meat price

increased /foot and mouth

disease/, Since March meat

price went down /supply

increased/. But from July it

has been a slight increase.

• Core inflation continued to • Core inflation continued to

increase in last six months

due to cash distributions,

large capital inflows, money

supply growth, and price

increases in Government

regulated goods and fuel.

II. Inflation...

Due to excess demand, core inflation is increasing continuously...

Core inflation is calculated as excluding prices of meat, diary products, and vegetables.

HOUSING PRICE INDEX

7.5

6.7

4.0

6.0

8.0Quaterly Housing Price Index Changes in Ulaanbaatar

-2.1

-1.3

-0.6

0.2

-0.3 -0.2

1.4 1.6 1.6

-4.0

-2.0

0.0

2.0

2009.I 2009.II 2009.III 2009.IV 2010.I 2010.II 2010.III 2010.IV 2011.I 2011.II 2011.III

II. GDP, MONEY, LOAN GROWTH...

II. Credit growth

Individual loan is increasing more rapidly...

III. Policy measures of the Bank of Mongolia: 2011

2011:

� Large capital inflows,

� Rapid growth of loan,

� Cash distribution welfare policy,

� Fuel price increase

� Expectation of price increase in other goods,

� Price increase in Government regulated goods

The BoM took following measures against inflation pressure due to

above mentioned demand and supply factors:

• In February: Raised reserve requirement by 4 % points

• In April: Raised policy rate by 0.5% points.

• In August: Raised policy rate and reserve requirement by 0.25

and 2 % points to 11%

• In October: Raised policy rate by 0,5% points to 12,75%

IV. Monetary policy stance: Increased Reserve Requirement

rate…

IV. Monetary policy stance: Growth of money supply is

weakened due to increased RR…

IV. Monetary policy stance: Increased policy rate…

IV. Monetary policy stance:

Ex-post real interest rate:

• Calculated as using CBB

rate for overall inflation.

• During last three quarters

of 2010 inflation was

higher than CBB rate so higher than CBB rate so

that ex-post real interest

rate was negative.

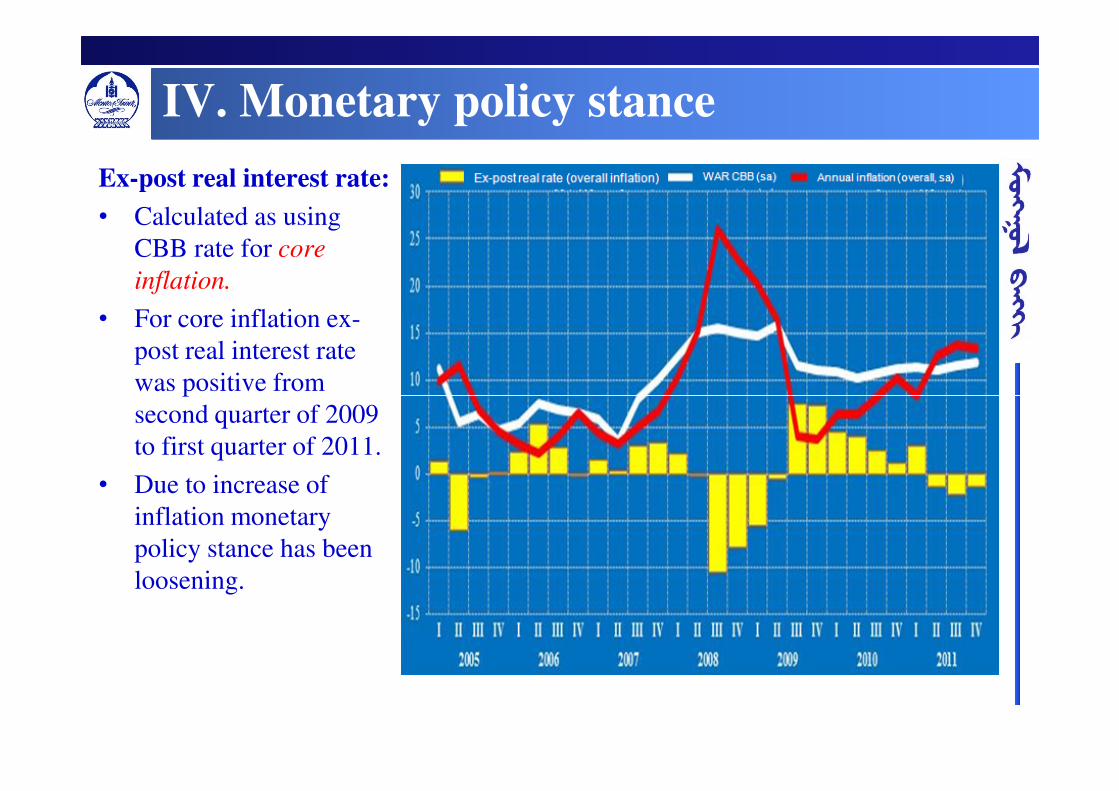

IV. Monetary policy stance

Ex-post real interest rate:

• Calculated as using

CBB rate for core

inflation.

• For core inflation ex-

post real interest rate

was positive from was positive from

second quarter of 2009

to first quarter of 2011.

• Due to increase of

inflation monetary

policy stance has been

loosening.

IV. Monetary policy stance...

Ex-ante real interest rate:

• Calculated as using CCB

rate for expected inflation.

• For expected inflation ex-

ante real interest rate has

been positive since second been positive since second

quarter of 2008.

• From 2010 monetary policy

stance has been tightening.

INTEREST RATE STRUCTURE

V. Inflation projection

Following demand factors result in increase of core inflation near future.

� Increase of budget expenditure and cash distribution,

� Capital inflows,

� Rapid growth of loan, particularly, individual loan growth shows � Rapid growth of loan, particularly, individual loan growth shows

economic overheating.

Following supply side factors can increase Inflation.

� Increase in fuel price in global market,

� Uncertainity of fuel price in domestic market,

� Increase in other goods price due to increased food and fuel price,

� Increase in food price in global market,

V. Inflation projection

� Increase in food price in global market,

� Inflation in neighbour countries,

� Meat price may increase in last six months of the year due to

seasonal effect, export, and herdsmen who have more cash.

V. Inflation forecast

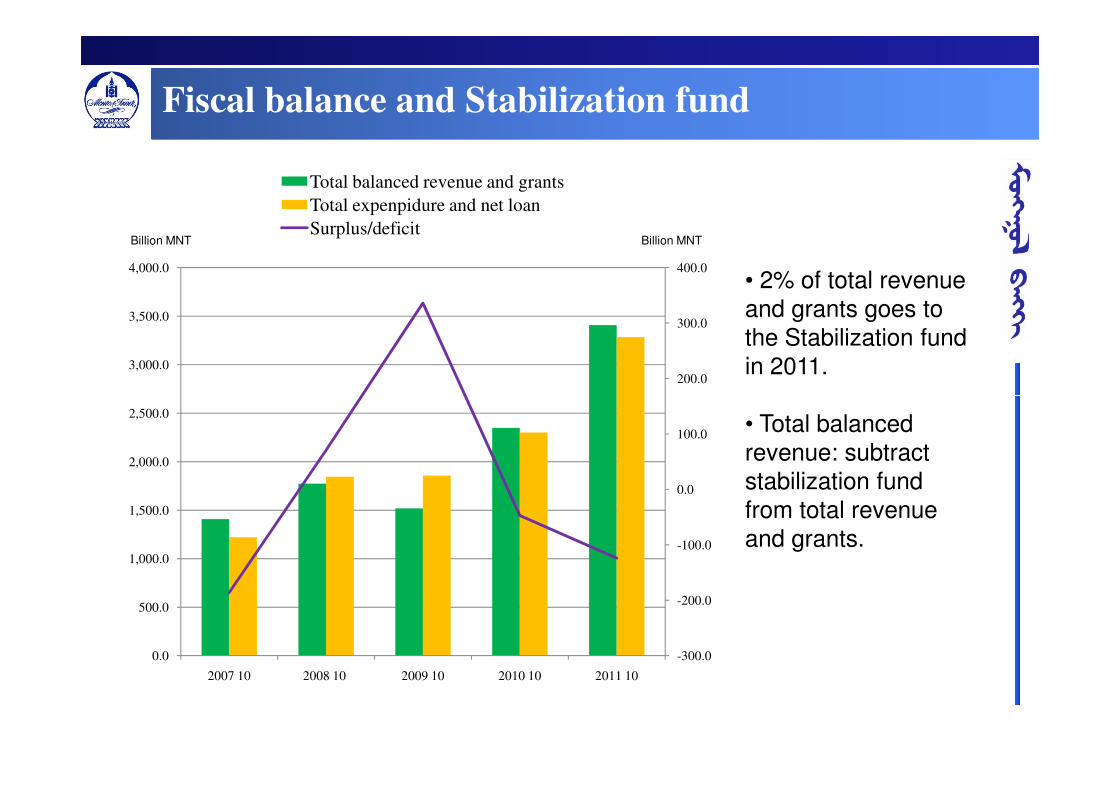

Fiscal balance and Stabilization fund

200.0

300.0

400.0

3,000.0

3,500.0

4,000.0

Total balanced revenue and grants

Total expenpidure and net loan

Surplus/deficitBillion MNT Billion MNT

• 2% of total revenue and grants goes to the Stabilization fund in 2011.

-300.0

-200.0

-100.0

0.0

100.0

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

2007 10 2008 10 2009 10 2010 10 2011 10

• Total balanced revenue: subtract stabilization fund from total revenue and grants.

VI. Banking sector’s indicators: Growth of liabilities...

Net capital flow and credit multiplier are compounding bank’s

liability growth.

Asset side....

Policy challenges

• Economic growth is more faster

• Potential GDP increase?

• Inflation pressure still remained high

• Financial market stability issue becomes more

importantimportant

• Increase in salary can make a pressure to private

sector

• Pro-cyclical policy should not be repeated

State Monetary Policy Guideline for 2012

The flexible exchange rate regime will be continued consistent withmacroeconomic fundamentals.

Policy continues on:

• No capital control• No capital control

• No exchange control

. The Central Bank of Mongolia signed the three-year currency swap,worth almost 1 trillion Mongolian togrog or 5,0 billion-yuan ($769million) with People’s Bank of China. This deal is aimed atpromoting bilateral trade, cross border trade settlements andoffering short-term liquidity to the two countries' financialinstitutions to reduce its reliance on the U.S. dollar in the wake ofthe global financial crisis.

Policy action in the FX market

Policy continues on:

• The flexible exchange rate regime consistent withmacroeconomic fundamentals.

• No capital control

• No exchange control

Signed the 3 year currency swap, worth ₮1 trillion= CNYSigned the 3 year currency swap, worth ₮1 trillion= CNY5,0 billion ($769 million) with People’s Bank of China.This deal is aimed at promoting bilateral trade, crossborder trade settlements and offering short-termliquidity to the two countries' financial institutions toreduce its reliance on the U.S. dollar in the wake of theglobal financial crisis.

Terms of trade (TOT): stable and highTerms of trade (TOT): stable and high

1.5

2.0

2.5

4.0

5.0

6.0

7.0

8.0

Terms of trade (R.scale) Export price index Import price index

Source: Bank of Mongolia

0.0

0.5

1.0

0.0

1.0

2.0

3.0

4.0

20

00

m1

20

00

m7

20

01

m1

20

01

m7

20

02

m1

20

02

m7

20

03

m1

20

03

m7

20

04

m1

20

04

m7

20

05

m1

20

05

m7

20

06

m1

20

06

m7

20

07

m1

20

07

m7

20

08

m1

20

08

m7

20

09

m1

20

09

m7

20

10

m1

20

10

m7

20

11

m1

20

11

m7

200

300

400

500

Net foreign exchange inflowsNet foreign exchange inflows

$US 0.3 bln. $US 1.6 bln.$US 416

mln.

-200

-100

0

100

2009-01

2009-02

2009-03

2009-04

2009-05

2009-06

2009-07

2009-08

2009-09

2009-10

2009-11

2009-12

2010-01

2010-02

2010-03

2010-04

2010-05

2010-06

2010-07

2010-08

2010-09

2010-10

2010-11

2010-12

2011-01

2011-02

2011-03

2011-04

2011-05

2011-06

2011-07

2011-08

2011-09

2011-10

2011-11

Source: Bank of Mongolia

FX inflow compositionFX inflow composition

Export

Loan9%

Currency and deposit10% Others

2%

(Jan - Sep 2010)

Export34%

Currency and deposit24%

Others2%

(Jan - Sep 2011)

Source: Bank of Mongolia

Export47%

Services4%

Income1%

Current transfer8%

FDI19%

Services4%

Income0%

Current transfer4%

FDI26%

Loan6%

Balance of PaymentsBalance of Payments

0

500

1000

1500Million USD

Current account

Capital and Financial account

Overall BOP

Source: Bank of Mongolia

-1000

-500

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

2004 2005 2006 2007 2008 2009 2010 2011

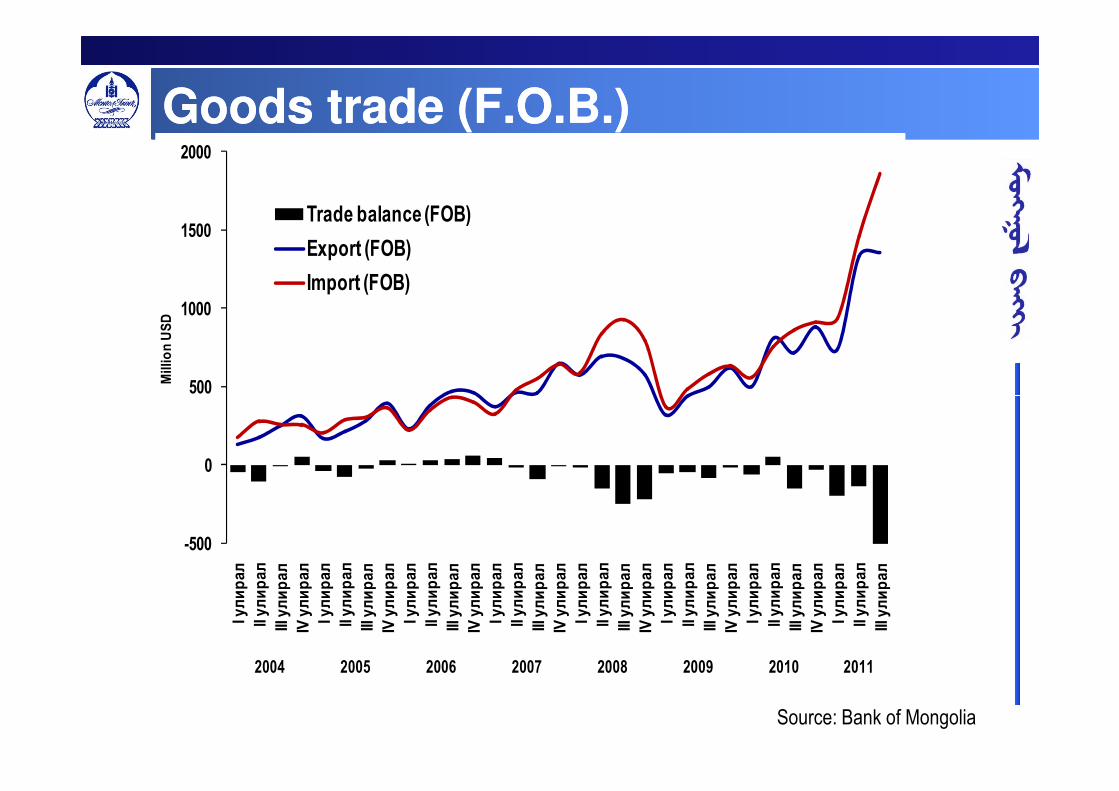

Goods trade (F.O.B.)Goods trade (F.O.B.)

500

1000

1500

2000Million USD

Trade balance (FOB)

Export (FOB)

Import (FOB)

Source: Bank of Mongolia

-500

0

500

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

IV улирал

I улирал

II улирал

III улирал

2004 2005 2006 2007 2008 2009 2010 2011

2000

2500

3000

3500

4000million USD

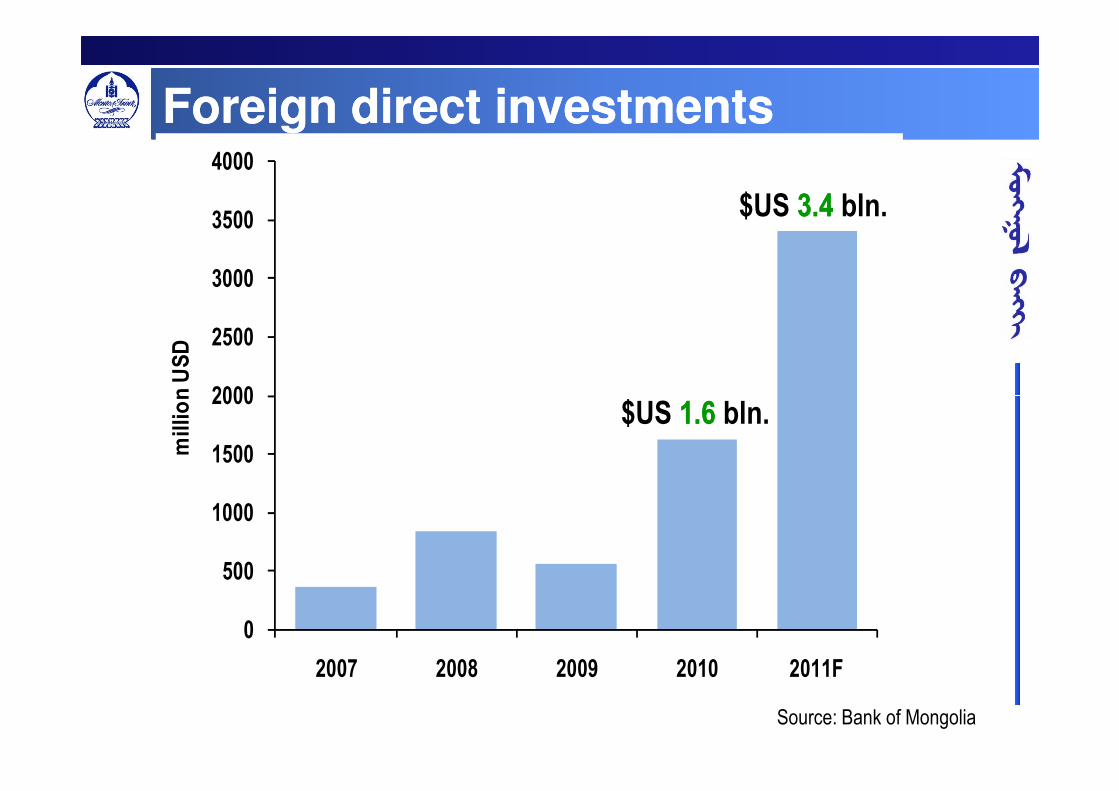

Foreign direct investments Foreign direct investments

$US 1.61.6 bln.

$US 3.43.4 bln.

0

500

1000

1500

2000

2007 2008 2009 2010 2011F

million USD

Source: Bank of Mongolia

$US 1.61.6 bln.

1,700

2,200

2,700

3,200m

illi

on

usd

Gross international reserves, $US Gross international reserves, $US mlnmln..

End-2006:

718End-2007:

1001End-2008:

657End-2009:

13271327End-2010:

22882288(39% ↑) (34% ↓) (102% ↑) (72% ↑)

Oct 2010:

26282628

200

700

1,200

20

06…

04

07

10

20

07…

04

07

10

20

08…

04

07

10

20

09…

04

07

10

20

10…

04

07

10

2011

…

04

07

10

mil

lio

n u

sd

Source: Bank of Mongolia

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1,400

1,500

1,600

1,700 Reference rate

Daily volatility (R.Scale)

Reference rate: Stability Reference rate: Stability �������� since Aprsince Apr--0909

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

1/1

/08

3/1

/08

5/1

/08

7/1

/08

9/1

/08

11/1

/08

1/1

/09

3/1

/09

5/1

/09

7/1

/09

9/1

/09

11/1

/09

1/1

/10

3/1

/10

5/1

/10

7/1

/10

9/1

/10

11/1

/10

1/1

/11

3/1

/11

5/1

/11

7/1

/11

9/1

/11

11/1

/11

1,100

1,200

1,300

1,400

Source: Bank of Mongolia

Crisis

BANKING SECTOR

MONGOLIAN FINANCIAL SECTOR CONSISTS OF:

14 domestic commercial banks;

177 non-banking financial institutions;

212 credit and savings unions;

48 security companies;

18 insurance companies;

353 listed companies.

NBFIs

2.1%

Credit &

savings

unions

1.0%

Insurance

0.9%

Security

0.5%

Foreign Banks:

ING (Rep. office)

Standard Chartered Bank ( Rep. office)

Development agencies:

Mongolian Development Bank

SME fund

Banks

95.6%

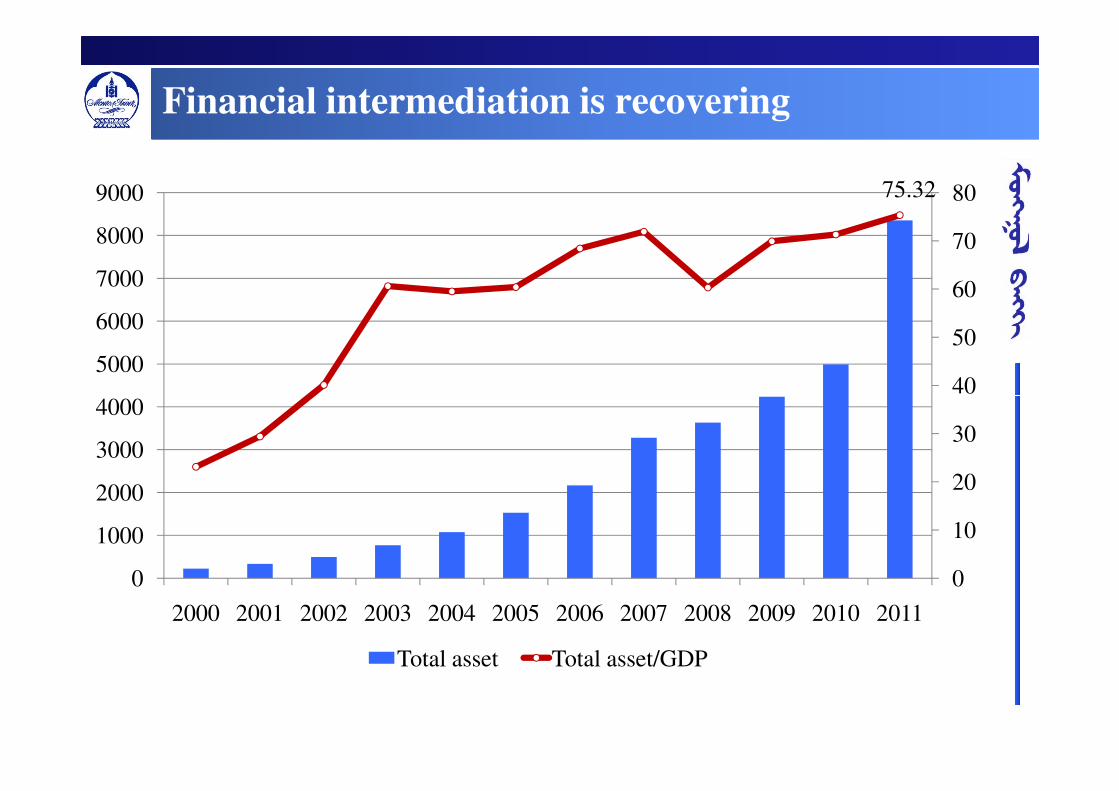

Financial intermediation is recovering

75.32

40

50

60

70

80

4000

5000

6000

7000

8000

9000

0

10

20

30

40

0

1000

2000

3000

4000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Total asset Total asset/GDP

Liquidity Indicators

LOAN OUTSTANDING BY SECTORS

Loan quality of banking sector

Domestic credit to GDP, by countries

293.0%

200.0%

250.0%

300.0%

350.0%

126.2% 126.1%112.6%

34.4%25.9%

0.0%

50.0%

100.0%

150.0%

200.0%

Japan China France Korea Mongolia Russia

Loan to Deposit Ratio

Deposits are stable

Billion.MNT

54.4

30

40

50

60

4000

5000

6000

7000

0

10

20

30

0

1000

2000

3000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Deposit Deposit/GDP

Capital Adequacy Ratio

Policy activity

• Liquidity ratio was reached by Bank of Mongolia from 18 percent to 25

percent

• The central bank of Mongolia are planning to implement countercyclical

Macroprudential policy tools .

• Increasing Tier 1 ratio

Money supply: Gradual expansionMoney supply: Gradual expansion

YoYYoY 57% 57% increasedincreased

10%

15%

20%

4,000

5,000

6,000

7,000

billion togrog

M2

M2, monthly changes (right scale)

Sep 2011

6,063.9 bill tog

Source: Bank of Mongolia

-10%

-5%

0%

5%

0

1,000

2,000

3,000

4,000

2004/01

05

09

2005/01

05

09

2006/01

05

09

2007/01

05

09

2008/01

05

09

2009/01

05

09

2010/01

05

09

2011/01

05

09

billion togrog

4,000

5,000

6,000

7,000

8,000

9,000

Banking sector total assetsBanking sector total assets

8.2 8.2 trillion togrog as of end Sep 2011:* 31% 31% increase since Jan 1, 2011* 47% 47% increase y-o-y

0

1,000

2,000

3,000

4,000

III VI IX XII III VI IX XII III VI IX XII III VI IX XII III VI IX XII III VI IX XII III VI IX XII III VI IX

2004 2005 2006 2007 2008 2009 2010 2011

Source: Bank of Mongolia

5%

6%

7%

8%

9%

2,500

3,000

3,500

4,000

4,500

5,000

In billions of MNT

Total loans outstanding (million MNT)

NPL/Loan ratio (R.Scale)

NPL / Loan ratio has rapidly been NPL / Loan ratio has rapidly been declining…declining…

0%

1%

2%

3%

4%

5%

0

500

1,000

1,500

2,000

2,500

2006 01040710

2007 01040710

2008 01040710

2009 01040710

2010 01040710

2011 010406

In billions of MNT

Source: Bank of Mongolia

LOAN OUTSTANDING BY SECTORS

3 large banks

LOAN TO DEPOSIT RATIO

110

120

130

140

150

4,000

5,000

6,000

per centbillion MNT

Loan Deposit LTD ratio

132%

50

60

70

80

90

100

-

1,000

2,000

3,000

LOAN TO DEPOSIT RATIO

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

0.20

0.40

0.60

0.80

1.00

1.20

0.61

Loan/Liability ratio

� Large banks – 0.61

� Medium banks – 0.63

� Small banks – 0.72

• Loan/Deposit ratio

• Large banks– 1.24

• Medium banks – 2.07

• Small banks – 2.00

--

Policy actions

• Minimum capital requirement increased from ₮8 bln to ₮16 bln.

• Deadline for existing banks to implement this requirement by May 2013.

• Capital adequacy ratio is 10%, with intention to increase to 14%

• Liquidity ratio was introduced at 18 %, with intention to increase to 25 %

• Supervisory measures will use countercyclical macro prudential policy

tools .

Policy support to banking sector

• Blanket deposit guarantee

• No tax on interest income earned by private people’s deposit

• No limit or restrictions on FX transactions

• Government comprehensive medium term • Government comprehensive medium term master plan to reduce loan interest rates and expenses:

Credit guarantee scheme

Credit information system ( private & public)

Transfer of Banking Training institute to MBA

Payment clearing centre privatization

I. State Monetary Policy Guideline for 2012

Under the framework of ensuring financial sector stability:

• The BOM will ensure the strengthening of financial capacity ofbanks and improving supervisory standards and regulationmethods in line with international best practices.

• The BOM will ensure disclosure and transparency of operations ofthe banking sector, enforce good governance principles at banks,the banking sector, enforce good governance principles at banks,maintain fair-competitiveness and tighten financial discipline in thesector.

• To prepare to introduce the limited deposit insurance scheme.

• To expand favorable conditions for investment banking andenhance supervision of the financial conglomerates.

• To establish legal frameworks for regulations and supervision offoreign bank branch and units.

I. State Monetary Policy Guideline for 2012

• To increase usage of non-cash payment instruments,such as debit- credit cards, mobile-internet banking, toensure uninterrupted and secure functioning of thepayment and settlement system.

• To implement recommendations and principles issuedby FATF for combating and preventing moneyby FATF for combating and preventing moneylaundering and financing of terrorism.

THANK YOU FOR YOUR

ATTENTIONATTENTION

Ms.Enke Enkhjargal Danzanbaljir

Chief Representative ( Director)

London Office, Bank of Mongolia

in UK Address:

3d Floor-D. 17 Lancaster Gate. London W2 3LH,

UK Tel/Fax +44 (0) 20-77063773

Mobile +44 (0) 7799641868Mobile +44 (0) 7799641868

in Mongolia Address:

Baga toiruu-9, Ulaanbaatar-46, Mongolia

Mobile +976-99115972

Fax +976(11)311471