050914 Hartmann final - Commerzbank AG€¦ · Basel II Corporate-Retail (max. loans €1m) 2,766.1...

50

Investors‘ Day Risk Management: Minimizing risks – Optimizing profits? Wolfgang Hartmann Member of the Board of Managing Directors Frankfurt, 14.09.2005

Transcript of 050914 Hartmann final - Commerzbank AG€¦ · Basel II Corporate-Retail (max. loans €1m) 2,766.1...

Investors‘ DayRisk Management: Minimizing risks – Optimizing profits?

Wolfgang HartmannMember of the Board of Managing Directors

Frankfurt, 14.09.2005

2/48

Agenda

Market Regulator

Customers Bank

Commerzbank

Risk Management

Risk Controlling

I.

Risk Management and Control at Commerzbank

I. II. III.Dynamics in the financial industry

What are the drivers of change?• Globalisation• Trading orientation• Regulations• Technology / IT• Market Focus / CompetitionIs minimizing risk a good measure to optimising profits?

II.

III.Risk Management as a major value driver in overall bank management: Current trends

Dynamics in the Financial Industry

3/48

Regulation

• MaH• MaK• MaRisk• Basel II• IAS

Globalisation

Dynamic changes in the financial industry are being caused by the following drivers:

Increasing pressure for change with higher complexity and volatility in banking businessleads to higher demands for Risk Management and Control in the monitoring of

• Closer integration of financial markets

• Concentration process in banking sector

• EU-enlargement• Corporate clients:

winners and losers(insolvencies, relocation of business abroad)

Trading orientation

• ABS• Credit Trading• Structured

products• Credit Default

Swaps (CDS)• Hedge funds/

Private equity

Competition

• Change management

• Cost pressure• Risk-taking

capability• Management of

complex processes• Market shares for

target groups/products

Technicalfeatures

• Value creation,sequence chain

• Vertical integration, outsourcing

• IT infrastructure• Technological

advance (communication systems, IT)

1. Credit Risk 2. Market Risk 3. Operational Risk

I. II. III.Dynamics in the financial industry

4/48

Trend since 2001in $ bn

Source: ISDA Market Survey

• Modern trading products (e.g CDS, CDO, ABS, (distressed) loan trading) make risks tradeable and enable banks to optimise theirportfolios (e.g. bulk risk limitation, diversification).

• Trading-oriented business makes possible timely valuation of market prices for risk positions instead of internal valuation.

• Hedge funds and private-equity funds have established themselves as important partners for portfolio diversification.

More trading-oriented business: notional amount of credit default swaps grew from $3,800bn to $8,400bn in `04 (annual growth rate of 123%)

919

2,192

3,779

8,422

5,442

2,688

632

1,563

06/01 12/01 06/02 12/02 06/03 12/03 06/04 12/04

I. II. III.Dynamics in the financial industry

5/48

Risk-adjusted pricing in the financial industry is supported by relevant risk parameters (e.g. PD, LGD) for banks which are using the Advanced Approaches.

• The capital requirements under the new Basel II regulatory framework are more risk-sensitive than the current Grundsatz I.

• Main capital drivers are the asset classes Corporates, Trading Book and Operational Risk (new under Basel II).

• Rationale for specific asset classes:

• Banks/sovereigns: real PD’s instead of low risk weights, due to OECD status

• Trading book: no 50% cap anymore

• Equity and ABS: new rules are very negative

• Retail/SME as retail: low risk weights compared to current Grundsatz I

+ = higher capital requirements- = lower capital requirements

Quite different development of minimum capital requirement afterimplementation of Basel IIAsset classes Changes MRC AIRB

Corporates +Banks +Sovereigns +SME treated as Corporate -SME treated as Retail -Other Retail +Residential Mortgages -Qualifying Revolving Retail -Specialised Lending +Trading Book +Equity +Securitisation +Market Risk 0Operational Risk +

I. II. III.Dynamics in the financial industry

6/48

Almost 40% of all IT costs are internal and external personnel costs

- illustrative -

IT Organisation/IT Processes

Development tools

Staff know-how in IT and business units

Application environment (isolated applications vs.data warehouse)

IT Infrastructure

Governance/User involvement

Standards/Documentation

Insourcing / Outsourcing/Offshoring

• According to a Boston Consulting survey, 15% of all bank costs are IT costs• No clear indication that higher IT spending pays off in terms of higher efficiency and of higher effectiveness• A flexible and efficient IT environment is essential for an advanced risk architecture

Other materialsNetworkSoftwareHardwareOutsourcingExternal employeesPersonnel

A future-oriented IT system is essential for efficient bank processes

Structure and dynamics of the IT environment is determined by …

25%

15%

6% 18%

17%

9%

10%

I. II. III.Dynamics in the financial industry

Source: BCG

7/48

CB estimate, ZKV

28

41

15

26 2832 33

3027

3238 39

27.8332.39

8.4510.92

15.1518.82

22.3425.53

27.47 26.6227.93

37.6239.47 39.60 38.00-

40.002

`91 `92 `93 `94 `95 `96 `97 `98 `99 `00 `01 `02 `03 `04 `05

2.89 2.98 3.01 3.04 3.15 3.41

0.92 0.94 1.08 1.24 1.25 1.16

?

1 2 Creditreform estimate 3 Gross Domestic Product (real), change on previous year in %

2.2 -1.1 2.3 1.7 0.8 1.4 2.0 2.0 2.9 0.8 -0.15.1 0.1GDP3 1.6 0.81

Corporate insolvency losses, in € bn

Source: Creditreform

Germany is a risky environment under reconstruction with 400,000–600,000 job losses p.a.

Number in `000

Number of corporates in bn

Insolvencies in %≥ 1.5

< 1.5

≥ 3.0

Main reasons: globalisation, weak economy, low capital base and insufficient management skills

86

I. II. III.Dynamics in the financial industry

8/48

Turnover 2002in € m

Number of corporates (in `000)

33

29

4

2.4

1.6

91

< 2

< 5

< 10

< 50

< 100

< 250

> 250 ←←←← Large caps, multinationals

mid-caps

Basel II SMEs

Basel II normal corporates

SMEs are essential for the growth and the necessary reorganizationof Germany as a service-orientedeconomy with:• more than 2/3 of all employees• 4/5 of all trainees• 50% Gross value added• 50% Turnover subject to tax• 50% Gross investments

2,766.1Basel II Corporate-Retail (max. loans €1m)

• Repositioning of banks within the SME sector in context of Basel II is under way

• Commerzbank’s strategic target is to play the major role in mid-cap, SME and corporate retail business

• Good risk management is essential for being on top in segments with high insolvency and restructuring rates

But restructuring of mid-caps and SMEs could be a good basis for professional financial advice

99.7% of all corporates have nodirect capital market access

I. II. III.Dynamics in the financial industry

9/48

in %

Source: Annual Reports

CitigroupDresdner Bank

HSBCBank of America

HVBDeutsche BankCommerzbank

JP Morgan ChaseLloyds TSB

San Paolo-IMIBarclays

Société GénéraleABN Amro

BNP ParibasING Groep

Credit SuisseUBS

Does minimizing risk mean that the net LLP ratio2 is reduced as much as possible?

High LLP ratios could be...... an indication of weak points in some banks,

banking groups or economies OR

... the result of a successful banking strategy� targeted (risk-return oriented)steering of portfolio into attractive portfoliosegments (e.g. consumer lending, mid-capand emerging markets financing)

1 Average lending ² net provisioning relative to total lending

0.98 (1.80)

1.59 (2.00)

0.05 (0.08)

0.24 (0.92)

0.31 (0.43)

0.35 (0.40)

0.43 (0.55)

0.94 (0.31)

0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

0.47 (0.54)

0.64

0.49 (0.36)

0.67

2003

0.68 (0.88)

0.76 (0.91)

2002

0.63 (0.65)

1 (0.911)

(1.64)

0.66 (0.77)

0.45 (0.53)

Ø 0.61 Ø 0.80

I. II. III.Dynamics in the financial industry

10/48

Low LLPs don’t automatically mean high profitability:Germany is bottom of the class

Source: Moody‘s, January 2003

Net interest income (without risk costs) of average interest-bearing assetsin %

Risk costs

I. II. III.Dynamics in the financial industry

HVB

0 0,5 1 1,5 2 2,5 3 3,5 4 4,5 5

West LBCommerzbank

Dresdner Bank

Intesa

HSBC

BBVASantander

Bank of AmericaBank One

HVB

0 0,5 1 1,5 2 2,5 3 3,5 4 4,5 5

West LBCommerzbank

Dresdner Bank

Intesa

HSBC

BBVASantanderCH

Bank of AmericaBank One

HVB

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

HelabaBayerische LB

West LBCommerzbank

Dresdner Bank

Deutsche Bank

Societe GeneraleCredit LyonnaisCredit Agricole

Bank AustriaErste Bank

ABN Amro

IntesaUnicredito

HSBCLloyds TSB

BBVASantander

Banco Popular

Bank of AmericaBank One

Citigroup

Conclusion: Major German banks might have weaknesses in …• … credit risk management• … risk-adjusted pricing• … business focus

Essential for the assessment of business success is the net margin of interest (interest income minus risk costs/risk-weighted assets)

11/48

Critical factors for success in risk management, e.g.:• Clear risk strategy• Timely monitoring, reporting and good corporate governance• Limiting bulk risk• Good knowledge of own portfolio in all risk and return dimensions• Efficient instruments/infrastructure for identifying, assessing and monitoring risks and returns,

advanced risk-adjusted pricing systems • Clear focus on markets/sectors with a high return • A keen sense of the market • Highly qualified staff• Shared risk culture

“Great deeds are usually wrought at great risks.”

Does minimizing risk really lead to an optimisation of profits?

Herodotus, The Histories of Herodotus, Greek historian & traveller (484 BC - 430 BC)

NO: Minimizing risk can mean the loss of shares in highly profitable markets and possibly failure to achieve high earnings in these markets (e.g. mid-caps, SME’s, retail business)

NO: Risky market segments usually generate a higher returnBUT: Sound risk management and control (based on advanced techniques) is essential for realising this

potential, otherwise failure is inevitable

Risk Management is the key to sustainable future income

I. II. III.Dynamics in the financial industry

12/48

Agenda

Market Regulator

Customers Bank

Commerzbank

Risk Management

Risk Controlling

I.

Risk Management and Control at Commerzbank

Mission statement “being the benchmark“Responsibilities/OrganisationRisk reportingEconomic capital conceptBasel II projectExamples credit:• Rating/Scoring • Pricing• LLP• Bulk risks

II.

III.Risk Management as a major value driver in overall bank management: Current trends

Dynamics in the Financial Industry

I. II. III.Risk Management and Control at Commerzbank

• Master scale• Credit process• Problem loans• Credit risk strategy

13/48

“Stages of Excellence” risk/capital management

Shar

ehol

der v

alue

Risk management sophistication

Riskidentification

Consistent riskquantification

Stage 1:Risk controlprevention

Linking riskand return

Stage 2:Continuous and

integrated improvement

Capitalallocation

Portfoliomanagement

Strategic valueenhancement

Stage 3:Group-widecapital mgt.

The Bank believes that substantial value leverage still exists for boosting the Bank’s earnings performance on a sustained basis in the claim to “being the benchmark in risk control and management”.(see Annual Report 2004, page 87)

Evolution in risk management

RoRaC

Economic capital

I. II. III.Risk Management and Control at Commerzbank

14/48

ReputationalRisk

StrategicRisk

CreditRisk

MarketRisk

LiquidityRisk

ComplianceRisk

OperationalRisk

Quantification

BusinessRisk

…while other non-quantifiable risks like Reputational Risk, Sustainability and Compliance Risk are not covered by the risk departments ZRC (Global Risk Control), ZCO (Global Credit Operations) and ZCP (Credit Operations Private Customers).

The Chief Risk Officer is responsible for all quantifiable risks…

I. II. III.Risk Management and Control at Commerzbank

quantifiable

Risk

quantifiable

Risk

Non-quantifiable Risk

Quantifiable Risk

15/48

As a result of the end-to-end implementation of new systems and processes, the organisation of credit line functions will significantly change within the next few years.

Head of Risk Control

Market RiskControl

Credit RiskControl

Functions• DevelopmentRating methods

• DevelopmentScoring methods

• Validation methods

• Implementationmethods

• SecuringData quality

Section 1

Rating- /Scoring-Methods

Block

Functions• DevelopmentRating methods

• DevelopmentScoring methods

• Validation methods

• Implementationmethods

• SecuringData quality

Section 1

Rating- /ScoringMethods

Section 2

QuantitativeCredit Risk

Dr. Giese

Functions• LGD / EADestimation

• EL (SRK) /UL (CVaR)

• Risk adjust.Pricing

• Validation SRK,CVaR, Pricing

Section 2

QuantitativeCredit Risk

Functions• LGD / EADestimation

• EL (SRK) /UL (CVaR)

• Risk adjust.Pricing

• Validation SRK,CVaR, Pricing

Section 3

CreditRisk Strategy /

Portfolio

Functions• Credit Riskstrategy

• Portfolio - / CreditRisk Control

• Group wide loan loss provision plan

• worldwide group exposures/Foreign Country Liabilities

• KWG registration

Section 3

CreditRisk Strategy

/PortfolioControlling

Functions• Credit Riskstrategy

• Portfolio - / CreditRisk Control

• Group wide loan loss provision plan

• worldwide group exposures/Foreign Country Liabilities

• KWG registration

Section 4

Market RiskControl

Treasury/Methods

Dr. Schwarz

Functions• Market riskmonitoring/analysis ZGT/Others

• Liquidity Risk

• Internal Model

• Model Validation

• Market Conformity Check / Client Valuation

• Market data

Section 4

Market RiskControl

Treasury/Methods

Functions• Market riskmonitoring/analysis ZGT/Others

• Liquidity Risk

• Internal Model

• Model Validation

• Market Conformity Check / Client Valuation

• Market data

Market riskcontrol

Credit riskcontrol

Section 6

OperationalRisk Control /

BusinessManagement

Functions• Project Basel II

• Internal /externalloss data

• Self Assessment

• Key RiskIndicators

• OpRisk Value -atRisk (EL and UL)

• Project HOC –Processes

Section 6

OperationalRisk Control

/ BusinessManagement

Functions• Project Basel II

• Internal /externalloss data

• Self Assessment

• Key RiskIndicators

• OpRisk Value -atRisk (EL and UL)

• Project HOC –Processes

Section 7

IntegratedRisk

Functions

TBA

Functions• Overall risk monitoring /Economic Capital

• New Products(Coordination

Of the processes /Overall risk

assessment)

• Complexaktivities

Integrated Functions

Section 7

IntegratedRisk

Functions

Functions• Overall risk monitoring /Economic Capital

• New Products(Coordination

Of the processes /Overall risk

assessment)

• Regulationsactivities

Integrated functions

• Complex

“Brains trust” Risk Control department is driving the development

Section 5

MarketRisk Control

Functions• Market risk monitoring/analysis ZGS

• Intensive Support ZGS / providing reports on portfolio level

• Illiquid markets

• New Products(Analysis)

Section 5

MarketRisk Control

Functions• Market risk monitoring/analysis ZCM

• Intensive Support ZCM / providing reports on portfolio level

• Illiquid markets

• New Products(Analysis)

ZCM

I. II. III.Risk Management and Control at Commerzbank

Operational risk control

16/48

ZENTRALER STAB RISIKOCONTROLLINGZENTRALER STAB RISIKOCONTROLLINGRISK REPORT AS OF 06/2005RISK REPORT AS OF 06/2005

Strictly ConfidentialStrictly Confidential

0. ExecutiveSummary

I. Risk Taking Capability (Economic and Regulatory Capital)

II. Credit Risk (incl. Credit Risk StrategyDeviation Analysis)

III. Market andLiquidityRisk (Trading/Banking BookandParticipations)

IV. Operational Risk (incl. Legal Risk)

V. Regulations and Other Risks

Table of Contents

Quarterly Risk ReportCommerzbank Group

ZENTRALER STAB RISIKOCONTROLLINGZENTRALER STAB RISIKOCONTROLLINGReportingReporting period Juneperiod June 20052005

Strictly ConfidentialStrictly Confidential

2

Reporting period June 2005

4.1 Interest Rates4.1 Interest Rates4.1 Interest Rates

ContentContent

4.1.1 ZCM IR Trading4.1.2 ZGT4.1.3 Essen Hyp4.1.4 EEPK4.1.5 BRE Bank S.A.

4.4 Credit Markets4.4 Credit Markets4.4 Credit Markets

4.2 Equities4.2 Equities4.2 Equities

4.3 Foreign Exchange – ZCM FX Trading 4.3 Foreign Exchange 4.3 Foreign Exchange –– ZCM FX Trading ZCM FX Trading

4.2.1 ZCM Special Situations4.2.2 ZCM Risk Management4.2.3 ZCM Equity Derivatives

4.4.1 ZCM Credit Trading4.4.2 Credit Derivatives Investment Book

3. Stresstest and Scenario Analysis - CB Group3. Stresstest and Scenario Analysis 3. Stresstest and Scenario Analysis -- CB GroupCB Group

3.1 Global Stress3.2 Scenario Analysis

5 Liquidity Risk5 Liquidity Risk5 Liquidity Risk

1. Executive Summary – Market Risk and P&L1. Executive Summary 1. Executive Summary –– Market Risk and P&LMarket Risk and P&L

2. Market Overview – Interest Rates, Credit Spreads, Foreign Exchange, Equities2. Market Overview 2. Market Overview –– Interest Rates, Credit Spreads, Foreign Exchange, EquitiesInterest Rates, Credit Spreads, Foreign Exchange, Equities

4. Key Portfolios4. Key Portfolios4. Key Portfolios

1.1 Profit and Loss1.2 Market Risk1.3 Risk Limit Approvals and Decisions1.4 Historical Overview of P&L and Risk

2.1 Market Overview 2.2 Market Views of Business Units and ZKV

6 Clean-P&L Backtesting6 Clean6 Clean--P&L BacktestingP&L Backtesting

Monthly presentation for Board ofDirectors and Risk Committee• Economic Capital Report• Risk-taking capability

Monthly presentation for Boardof Directors and Risk/Credit Committee• Bulk risks• Largest problem loans• Largest substandard loans

ZENTRALER STAB RISIKOCONTROLLINGZENTRALER STAB RISIKOCONTROLLINGOperational RISK REPORT Q2 2005Operational RISK REPORT Q2 2005

2

OpRiskOpRisk Report Report CommerzbankCommerzbank GroupGroup

2. OpRisk Losses 2. 2. OpRiskOpRisk Losses Losses

1. OpRisk Capital1. 1. OpRiskOpRisk CapitalCapital

0.1. OpRisk Highlights Q2 2005

1.1. Group Capital Requirement

0. Executive Summary0. Executive Summary0. Executive Summary

2.1. Internal Losses2.2. External Losses

3. OpRisk Process Analysis3. 3. OpRiskOpRisk Process AnalysisProcess Analysis

3.1. Quality-Self-Assessment (QSA) –Results and Key Risk Drivers3.2. Business ContinuityManagement (BCM) –Assessment Results3.3. Key Risk Indicators (KRI)3.4. Risk & Control Inventory(RCI) / Scenarios: Fat-Tail Potential

4. Significant OpRisk Audit Findings And Mitigation Actions4. Significant 4. Significant OpRiskOpRisk Audit Findings And Mitigation ActionsAudit Findings And Mitigation Actions

5. OpRisk Provisions And Insurance5. 5. OpRiskOpRisk Provisions And InsuranceProvisions And Insurance

5.1. Provisions for pending legal risk5.2. Insurance

1.2. OpRisk Capital by business unit

AttachmentsAttachmentsAttachments

I. Significant internal loss dataII. a) QSA b) BCM Analysis

III. Significant Audit Findings

Quarterly Operational Risk Report for Board of Directors and OpRiskCommittee

in addition

Quarterly presentation for Board of Directors and Risk Committee of

the Supervisory Board

The quarterly Risk Report is CB’s central risk information medium

Monthly Market and Liquidity Risk Report for Board of Directors and Risk Committee

in additionin addition

in addition

I. II. III.Risk Management and Control at Commerzbank

17/48

Economic Capital(Unexpected loss)

approx. €10bn

CreditRisk55%

MarketRisk27%

OperationalRisk13%

BusinessRisk

5%

• All components of economic capital are calculated using the same time horizon (1 year) and confidence level (99.95%, corresponding to the Commerzbank target rating of A1).

• Main objective is the optimisation of the RoRaC on the total economic capital, limited by the available capital for risk coverage ( = equity capital + budgeted operating profit + revaluation reserves).

Commerzbank’s economic capital and risk-taking capability

RoRaC=

Operating pre-tax profitEcon. capital

Capital for risk coverage

Actual risk buffer35%

(minimumbuffer = 20%)

Economic capital incl.

diversificationof approx. 25%

Available capital for risk coverage

(incl. Trading/bankingbook and participations)

I. II. III.Risk Management and Control at Commerzbank

18/48

Risk Type Basel I Basel II Best Practice Commerzbank

Commerzbank came first in an economic capital benchmarking study of German BdB banks which showed that its approach is on best practice level

Differences between regulatory and internal calculation of risk capital requirements

Yes, but not risk-sensitive

Integrated modelling of Credit VaR

Significant improvements

Transfer risk

Interest rate risk

Trading book

Correlation matrix/ factor model

Earnings volatility (EaR) /

Scenario-approach

Internal model

Business risk

Operational risk

Integrated modelling of VaR

Total risk= MR + CR + OR

No

allowed

Significant improvements

No

Internal VaR model

No

Cre

dit R

isk

No

Internal VaR model

No

Yes, but risk underestimated

No

No

Total risk= MR + CRRisk aggregation

Settlement risk Yes, but risk underestimated

Liquidity risk Internal monitoringMonitoring acc. 2

Pillar II

Yes, but not risk-sensitive

Internal modelReal estate risk No No

Yes, but not risk-sensitive

Counterparty Risk,Concentration/Bulk risks

Integrated modelling of Credit VaR

Significant improvements

Transfer risk

Interest rate riskin the banking book

Trading book

Correlation matrix/ factor model

Earnings volatility (EaR)/Scenario-approach

Internal model

Business risk

Operational risk

Integrated modelling Of VaR

Participations in bankingbook

Total risk= MR + CR + OR

No

Yes, internal models allowed

Significant improvements

No

Internal VaR model

No

Cre

dit R

isk

No

Internal VaR model

No

Yes, but risk underestimated

No

No

Total risk= MR + CRRisk aggregation

Ris

k

Settlement risk Yes, but risk underestimated

Liquidity risk Internal monitoringMonitoring acc.

Grundsatz IIPillar II

internal monitoring

Yes, but not risk-sensitive

Internal modelReal estate risk No

Improved CreditRisk+ model

Internal model based on correlation matrix

Fee income and cost forecast model

Internal model

Internal market risk model

Historical simulation

Internal monitoring/ scenario analysis

Not relevant

Improved CreditRisk + model

Internal model based on correlation matrix

Fee income and cost forecast model

Internal model

Internal market risk model

Historical simulation

Internal monitoring/ scenario analysis

Not relevantNo

I. II. III.Risk Management and Control at CommerzbankM

arke

t

19/48

Private andBusiness Customers

AssetManagement Mittelstand

InternationalCorporateBanking

Corporates & Markets

MortgageBanks

Others andConsolidation

Jun- 05 Credit Risk

Jun- 05 Other Risks

ECAP Credit risk

ECAP Other risks

RegCap Credit risk

RegCap Market risk

There is almost no difference between overall regulatory and economic capitalbut the risk structure differs significantly for activities and risk types

Regulatory and economic capital for Commerzbank’s various segments

I. II. III.Risk Management and Control at Commerzbank

20/48

-I = Current Grundsatz I SA = Standardized approachFIRB = Basic IRB Approach AIRB = Advanced IRB approach

GS-I

100%

SA

124%* AIRB(QIS 4)

103%*

Econ

omic

alEq

uity

cha

rge

* Compared with Grundsatz I (Basis: QIS 4 figures, Dec `04)

FIRB

105%*

90% floor in 2008 �

80% floor in 2009 �

Withconservativeassumptionsfor LGD, EaD

AssumingAIRB

as from1/2008

approx. 95%

with own futureLGD and EaDvalues

AIRB advantages Depending on:• internal LGD• internal EaD• necessaryrecalibration by the regulator

GS

There are additional significant value drivers in the Advanced IRB Approach: • Higher discriminatory power -> improved risk selection• Avoidance of defaults• Provision of PD and LGD figures for internal controlling • Greater efficiency -> further optimisation• Adequate allocation of economic capital• Higher reputation

I. II. III.Risk Management and Control at Commerzbank

Significant advantages for AIRB Approach

21/48

CBK is in close and regular/continuous contact with the regulators with regard to home/host issues and AIRB/AMA application process...

Home/Host issues• Commerzbank has been chosen as the national, case study bank by German regulators

• During 2004 several meetings/presentations with the regulators took place in this context as well as meeting with the ad-hoc working group of the IIF

• The case study initiative was followed by the college of supervisors in March 2005 where CB presented the state of Basel II implementation to 17 international banking supervisory authorities from countries where CB has business units

AIRB/AMA application• Following the meeting in March, the process of AIRB application has been started on the basis of

the BaFin circular of December 2004

• 19.7.05 the formal AIRB application was sent to BaFin/Bundesbank

• Beginning of August, a first working meeting with BaFin/Bundesbank took place to evaluate the further deliverables

• The formal AMA application process will start once BaFin/Bundesbank has published the relevant paper

I. II. III.Risk Management and Control at Commerzbank

22/48

2.

4.

5.

% o

f tot

al G

roup

cre

dit e

xpos

ure

(EAD

)

1.1.05 1.1.06 1.1.08 1.1.10 1.1.12

100

50

1.1.07 1.1.09 1.1.11 1.1.13

Beginningof AIRB

Regulatory reference point Permanent partial use

92%

80%

50%

Core non-retail segments (banks, corporates)

Core Germanretail segments

Material subsidiaries using Group-wide ratings

Other subsidiaries, remainingratings

Permanent partial use (e.g. small retail portfolios, immaterial subsidiaries)

Focus of each proposed audit “wave”:

Commerzbankcumulative AIRBcoverage (EAD)

Ratings inthe “1st wave”:

RC-GERRC-LACRC-INT

Banks (incl. EssenHyp)Specialized Finance

Commerzbank is well positioned with respect to portfolio coverage in AIRB Approach

1. 3.2. 4. 5.

Status:• AIRB application sent to BaFin on 19.7.05• Expected begin of on-site AIRB examination

end of Q2 `06

1.

3.

Proposed audit “waves”

I. II. III.Risk Management and Control at Commerzbank

Minimum requirement

23/48

Basel II project overview

I. II. III.Risk Management and Control at Commerzbank

Proj

ect m

aste

rpla

n (IT

and

Spe

cial

ised

Dep

artm

ent)

Rating

non-retailRatingretail

LGD projects

Basel II calculation engine

EL/UL

Ongoing coordination with the regulators / AIRB/AMA application/certification

Futu

re B

II re

gist

ratio

n/

Impl

emen

tatio

nSA

MB

A

Trading book (new Project;Basel II paper 18.07.)

Stress test/Backtesting

Proj

ect e

nd a

nd tr

ansf

er t

o lin

e fu

nctio

ns

Risk mitigation

ORS: OpRiskimplementation

Reporting/KRS(depends on DWH Rel 1)

Calculation engine / EC calculator - Simulation -/ QIS 5

Calculation engine /Capital calculator - Production -

• AIRB approach• (Standardized approach)• (FIRB approach)

ORE: OpRisk• AMA approach• (Standardized approach)• (Basis indicator approach)

Pricing(methodology)

ABS

Impl

emen

tatio

nPi

llar

III

qual

itativ

e re

quire

men

ts

PII +

MaR

isk

Dat

aw

areh

ouse

Subs

idia

ries

inte

rfac

e

Balance-sheetanalysis,new

Data quality

Inte

rest

rate

ris

kin

ban

k bo

okEC

ap

Decision machine (etec)

BRE

CCR

Essen-hyp

Rel 1

Rel 2

Balancesheetintegr.

Stra

tegi

cim

pact

sLi

quid

ityris

k

Proj

ect m

aste

rpla

n (IT

and

Spe

cial

ised

Dep

artm

ent)

Ratingnon-retail

Ratingretail

LGD projects

Basel II calculation engine

EL/UL

Futu

re B

II re

gist

ratio

n/

Impl

emen

tatio

nSA

MB

A

Trading book (New Project; Basel II paper 18.07.)

Stress test/ Backtesting

Proj

ect e

nd a

nd tr

ansf

er t

o lin

e fu

nctio

ns

Risk mitigation

ORS: OpRiskimplementation

Reporting/KRS(depends on DWH Rel1)

Calculation engine / EC calculator - Simulation -/ QIS 5

Calculation engine /Capital calculator - Production -

• AIRB approach• (Standardized approach)• (FIRB approach)

ORE: OpRisk• AMA approach• (Standardized approach)• (Basis indicator approach)

Pricing(methodology)

ABS

Impl

emen

tatio

nPi

llar

III

Qua

litat

ive

requ

irem

ents

PI

I + M

aRis

k

Dat

aw

areh

ouse

Subs

idia

ries

inte

rfac

e

Balance sheetanalysis news

Data quality

Inte

rest

rate

ris

kin

ban

k-in

gbo

okEC

ap

Decision machine (etec)

BRE

CCR

Essen-hyp

Rel 1

Rel 2

Balancesheetintegr.

Stra

tegi

c im

pact

sLi

quid

ity

risk

24/48

Development of market default rate (probability of default, PD)Mid-cap corporates with turnover between €2.5m and €750min %

On average, German Mittelstand firms fall into the “non-investment grade” category,i.e. into the risk segment (<<<< BBB- according to S&P) – similar to the United States!

B+

BB-

BB

BB+

ComparableS&P ratings

CB’s German Mittelstand target group: Market default rates in Germany, by turnover class

1.96

2.42 2.47

2.29

1.54 1,46

2.03

1.711.65

1.12

1.451.34

1.01

0.62

0.920.68

0.60

1.22

1.50

1.22

1.05

1.29

1.711.55

1.39

1.751.56

1.87

2.072.13

1.86

1.511.75

1.64

1.151.26

1.34

1.01

0.770.81

1.11.02

0.49

0.78

0.54

0.39 0.410.37

0.98

1.32

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Non-weighted average€50m - €750m€25m - €50m€7.5m - €25m€2.5m - €7.5m

I. II. III.Risk Management and Control at Commerzbank

25/48

AAA

AA

A

BBB

BB

B

CCC

C, D - I, D- II

1.01.21.41.61.82.02.22.42.62.83.03.23.43.63.84.04.24.44.64.85.05.25.45.65.8

6.1 - 6.5

Rating levels

0,010,020,040,070,11

0,260,390,570,811,141.562,102,743,504,355,426,748,3910,4312,9816,1520,09

S&P

- IIDefault

0

0.17

25.00< 100

Average probability of default, in %

AAA

AA+, AA, AA-

A+, A, A-

BB

B

CCC+

BBB+

BBB-

BB+

BB-

B+

B-

CCC to CC

DEFAULT

IFD

I

II

III

IV

V

VI

by way of comparison:

Typical Mittelstand customer(SMEs/mid-caps)

BBB

Little significance for Mittelstand,significance for large caps andcapital market-using multinationalsas well as banks and sovereigns

Weaker SMEs and mid-capswith the need to reposition orrestructure

Larger mid-caps with above-averagequality

Mittelstand customers in crisis:turnaround by management orneed for recapitalisation

Rating Master Scale and PD/EL values compared with S&P and IFD classes, structured by relevant target groups for detailed migration analysis

I. II. III.Risk Management and Control at Commerzbank

26/48

*) KfW direct loans only

Commerzbank has the most detailed rating differentiation for mid-caps

IFD rating scale – Mapping of top German banks

PDs

0.7 – 1.5%

1.5 - 3%

3 - 8%

> 8%

IFDrating

III

IV

V

VI

3.0 – 3.4

3.6 – 3.8

4.0 – 4.8

5.0

8

9 (or 10)

(10)11

12 -14

III

IV

V

VI

3.0 – 3.4

3.6 – 3.8

4.0 – 4.8

> 5.0

M10 – M11

M12 – M13

M14 – M15

M16 – M20

*)

4 – 5

5 – 6

6 – 7

> 7

< 0.3% - 5I 1.0 – 2.4 1 I 1.0 – 2.4 M1 – M71+ –3 -

0.3 – 0.7%II 2.6 – 2.8 6, 7II 2.6 – 2.8 M8 – M93 – 4- -

- -

-

iAAA – iBBB

iBBB – iBB+

iBB

iBB- – iB+

iB – iB-

> iCCC

Num

berof rating

levels

43 665

Rating levelsrelevant

for mid-cap

financing

Relevant

for mid-cap

financing

10

146 20212330

PDs

0.7 – 1.5%

1.5 - 3%

3 - 8%

> 8%

IFDrating

III

IV

V

VI

3.0 – 3.4

3.6 – 3.8

4.0 – 4.8

5.0

8

9 (or 10)

(10)11

12 -14

III

IV

V

VI

3.0 – 3.4

3.6 – 3.8

4.0 – 4.8

> 5.0

M10 – M11

M12 – M13

M14 – M15

M16 – M20

*)

4 – 5

5 – 6

6 – 7

> 7

< 0.3% - 5I 1.0 – 2.4 1 I 1.0 – 2.4 M1 – M71+ –3 -< 0.3% - 5I 1.0 – 2.4 1 I 1.0 – 2.4 M1 – M71+ –3 -

0.3 – 0.7%II 2.6 – 2.8 6, 7II 2.6 – 2.8 M8 – M93 – 4- -0.3 – 0.7%II 2.6 – 2.8 6, 7II 2.6 – 2.8 M8 – M93 – 4- -

- -

-

iAAA – iBBB

iBBB – iBB+

iBB

iBB- – iB+

iB – iB-

> iCCC

Num

berof rating

levels

43 665

Rating levelsrelevant

for mid-cap

financing

Relevant

for mid-cap

financing

10

146 20212330

I. II. III.Risk Management and Control at Commerzbank

27/48

What distinguishes good from bad rating systems – αααα−−−− and ββββ−−−−errors

Rating classes Bad

Measure: GINI coefficient (increase from 70% to 75%) means sustainable reduction of loan loss provisions by approx. 1/6

Business which was unfortunately done

Business, which weshould have done

Borderline score/rating categorywhere no more business is carried out

Rating methods with high discriminatory power are characterized by a small overlapping sector of “good” and “bad” companies and provide clear guidelines for business.

Intensive competition between the banks for state-of-the-art rating systems strengthens the economy and provides significant competitive advantages for the leading banks.

Good

“Bad”companies

“Good”companies

�-error =

β-error =

Error types

Frequency

I. II. III.Risk Management and Control at Commerzbank

28/48

Annual turnover in € m

Commerzbank’s new PD rating systems for different types of corporate clients with high discriminatory power (GINI coefficient)

Commerzbank is on state-of-the-art level in banking sector

Head office in

0.0

750.0

Germany Other countries

Rating CorporatesLarge Companies (RC-LAC)For multinationals and larger companiesbank-wide, annualturnover > €750m

Rating corporatesGermany (RC-GER)For German medium-sizedbusinesses, annual turnover€2.5m to 750m

Rating CorporatesInternational (RC-INT)For international medium-sized businesses, annualturnover up to €750m

GINI = 75%

GINI = 70%

GINI = 75%

0.0

750.0

Germany Other countries

Rating CorporatesLarge Companies (RC-LAC)For multinationals and larger companiesbank-wide, annualturnover > €750m

Rating corporatesGermany (RC-GER)For German medium-sizedbusinesses, annual turnover€2.5m to 750m

Rating CorporatesInternational (RC-INT)For international medium-sized businesses, annualturnover up to €750m

Segment private Customers

GINI = 75%

GINI = 70%

GINI = 75%

Head office in

0.0

750.0

Germany Other countries

Rating CorporatesLarge Companies (RC-LAC)For multinationals and larger companiesbank-wide, annualturnover > €750m

Rating corporatesGermany (RC-GER)For German medium-sizedbusinesses, annual turnover€2.5m to 750m

Rating CorporatesInternational (RC-INT)For international medium-sized businesses, annualturnover up to €750m

GINI = 75%

GINI = 70%

GINI = 75%

0.0

2.5

750.0

Germany Other countries

Rating CorporatesLarge Companies (RC-LAC)For multinationals and larger companies bank-wide, annualturnover > €750m

Rating corporatesGermany (RC-GER)For German medium-sizedbusinesses, annual turnover€2.5m to 750m

Rating CorporatesInternational (RC-INT)For international medium-sized businesses, annualturnover up to €750m

Segment private Customers

GINI = 75%

GINI = 70%

GINI = 75%

I. II. III.Risk Management and Control at Commerzbank

29/48

Financial analysis of annual fin. statemtents

Statistical evaluation of annualfinancial statement data

Financial analysis of current results

Trend evaluation by user PD is set higher for older data, on moving scale

Qualitativerisk analysis

70 -120 questions, depending on case

Warning indicators

Group integration

Override/manual change

Override is transparent, possible only as final step of rating, by max. of one notch, i.e. +/ -0.2

Analysis New rating methodsEvaluation of annual fin. statementscompared with benchmark data

34 questions

Evaluation of customer’s (credit)account behaviour and ext.payments

Simple substitution of rating classes

Overrides possible in individual partsof rating process

previously

Specific evaluation of 24 factors

Substitution of PDs weighting depends on relationship between PDs of parent and subsidiary

PD/borrower rating Borrower rating class mapped to PDPD mapped to rating class

Evaluation of current resultscompared with benchmark data

The new rating methods for German SME’s differ from the existing rating system

Rating Corporates Germany (RC-GER)Rating migration

Intensive treatment

51%

52%

5%

10%

5%

7%

39%

31%

Intensive treatment

New ratings (RC-GER)

Old ratings (CODEX/RB-

1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0 5,5 6,0

1,0 1,4 1,8 2,2 2,6 3,0 3,4 3,8 4,2 4,6 5,0 5,4 5,8

Intensive treatment

51%

52%

5%

10%

5%

7%

39%

31%

Intensive treatment

New ratings (RC-GER)

- FK)

1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0 5,5 6,0

1,0 1,4 1,8 2,2 2,6 3,0 3,4 3,8 4,2 4,6 5,0 5,4 5,8

I. II. III.Risk Management and Control at Commerzbank

30/48

Credit margin

Cross-subsidisation due to standard margin

Standardmargin

Offers to good customers are too expensive ���� good new business is lost to banks with risk-oriented pricing

Offers to bad customers are too cheap ���� risk in portfolio increases via inflow of customers with weak solvency from banks with risk-sensitive pricing.

rating classes

In case of lower creditworthiness and in weaker economies, the willingness to grant loans ends much earlier if standard margins are used.

Too expensive

Too cheapfor risk

coverage

• Standard margins and weakly calibrated spread curve: Bank grows in sectors with weaker ratings and would be well advised to stop the granting of loans at an early stage.

• Only banks with good rating systems and risk-adjusted pricing do not suffer from this effect.

I. II. III.Risk Management and Control at Commerzbank

31/48

“From customer solvency to actual credit risk”= from PD (probability of default) to EL (expected loss)

Einflussfaktoren

InanspruchnahmeLimit

KreditartSicherheitenetc.

PD (in %)Expected defaultof transactions ortotal exposureof a customer

• Recovery rates foruncollateralized part and physical collateral

• Reason for default e.g. restructuring, formal insolvency

• Customer group• Legal framework

(country)• etc.

EaD (in €)X LGD (in %)

EL in relation to EaD= risk premium

in % or = standard

risk costs

X = EL (in €)

EL / EaD

Quantitativefactors

FaktorenQualitativefactors

• credit volume(drawings)

• financial collateral

• Limit credit type• etc.

Influencing factors

EaD = Exposure at defaultLGD = Loss given default

Rating

Commitment rating

Influencing factors

A good knowledge of all relevant Basel II parameters is essential for risk-adjusted pricing. Within Commerzbank’s Basel II project, we evaluate all the necessary parameters for all target groups.

I. II. III.Risk Management and Control at Commerzbank

32/48

EL

Low ECB prime rate (substantially lower inflation), good fundingbasis of the bank (a favourable external bank rating is essential)

Good rating ���� less effort required for creditworthiness check large portfolio ���� economies of scale,standardised products/processes ���� lower costs for individual cases,large single loans, less and simplified collateral processing

Good rating ���� less documents/information for creditworthiness check ���� focus on sales

Internet bank ���� no personal support, standardised/ target-oriented support and advice, many customers per relationship manager

Good solvency ���� good rating ���� low PD,high degree of collateral ���� low EL

Refinancing/purchase costs

Costs for relationship management

Costs for credit process

Standard risk costs

Reg. equity capital costs according to Basel II

(IRB Advanced Approach)

Good rating ���� low PD ���� low equity charge High collateral ���� low EaD/LGD, lower equity costsfavourable portfolio class (e.g. Retail-SME) ���� low capital costsAllocation of business with no equity charges = cross selling (e.g. payment services, international banking, asset management)

Proc

ess

man

agem

ent

Reasons for a bank’s favourable interest rates

Efficient banking systems are able to offer a stable credit supply for all customer segments with differentiated but competitiveconditions. Customer and bank contribute jointly to favourable lending rates.The rating is an essential factor for the margin in all price components.

I. II. III.Risk Management and Control at Commerzbank

33/48

Commerzbank’s etec project (end-to-end credit) for corporate customers has redesigned the whole credit process for mid-cap business using modern instruments

Mitt

elst

and

Externally and internally committed facilities

individual “light”process

up to €0.75m

Special processes in centres of competence (e.g. Commercial Real Estate, Public Finance, Specialised Lending, Renewable Energy)

I. II. III.Risk Management and Control at Commerzbank

Large customers,

MNCs

>€0.75m - €5m > €5m

Mid-caps(=€750m)

SME’s(=€50m)

individual process

standard process

individual“light”

process

34/48

Decision process

Standard process for German SMEs up to €50m

Green: Decision by account managerYellow: Escalation processRed: No credit

Pricing decision4.2

Additional initialtests with regard to• Maximum

amount of credits with given enterprise size

• Portfolio limits

Risk decision0

Collateral quota (in %)

34

7

5

2

0 10 20 30 40 50 60 70 80 90 100*

1

6

PD(in

%)

98

10

100Gross margin (in bp)

1.0

Com

mitm

ent r

atin

g

600300200100 400 500

1.41.82.22.63.03.43.8

0

Green: Decision by account managerYellow: Decision in one single credit centreRed: No credit

Yes/no decision by machine based on EL and additional pricing requirements for improved decisions

I. II. III.Risk Management and Control at Commerzbank

35/48

Coverage ratio for non-performing loansin €m

Loan-loss provisions in bpsLoan-loss provisions in €m

1,498

1,683

1,158

1,322

1,614

1,822

1,629

792

1.084

1,358

589

873

537

724

555 545 522

909

810 621

598

822

1.267

836688

1997 1998 1999 2000 2001 2002 2003 2004 2005

Non-performing loans

Loan-loss provision

CountryLLP+General provision

Collateral

110

90

106

44

6774

66

52

111

99

85

7074

57

33

4044

32 33 33

4453 38

33

46

1997 1998 1999 2000 2001 2002 2003 2004 2005

Releases

Net LLP

Gross LLP

Averagenet LLP 1997-2004

CB - Gross/net loan-loss provisions and releases 1997–2005 (August top-down forecast)

I. II. III.Risk Management and Control at Commerzbank

Dec `04

6,924326

1,831

5,352

119.3%

7,509

Mar `05

116.0%

6,393

334

1,723

5,402

7,459

Jun `05

117.5%

6,202

341

1,539

5,407

7,2871,066 1,215 1,085In excess:

36/48

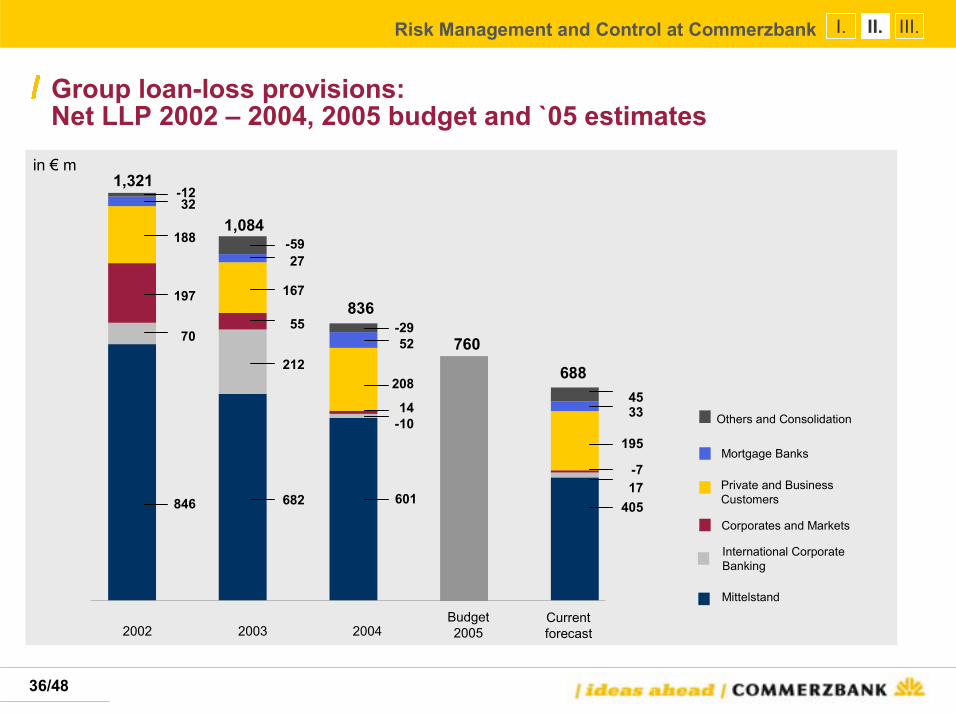

in € m

40517-7

195

3345

Currentforecast

Mittelstand

International Corporate Banking

Corporates and Markets

Mortgage Banks

Others and Consolidation

601

14-10

208

52-29

2004

682

212

55

167

27-59

2003

1,084

846

70

197

188

32-12

2002

1,321

688

Private and Business Customers

Group loan-loss provisions: Net LLP 2002 – 2004, 2005 budget and `05 estimates

I. II. III.Risk Management and Control at Commerzbank

Budget2005

760

836

37/48

69.062.160.4

55.954.0

66.762.4

48.4

92.790.282.783.3

Total lending

non-performing loans 6.8 7.1 6.3 6.2total LLPs 5.7 5.9 5.7 5.7npl in % total lending 4.0% 4.3% 3.9% 3.9%

8.9 5.3 3.5 3.34.3 3.3 2.3 2.3

0.4% 0.3% 2.4% 2.3%

n.a. 10,7 7,3 4,7n.a. 5,6 4,4 2,9n.a. 10,4% 7,7% 4,6%

2002 2003 2004 2002 20032002 2003 2004200406/05

171 165 161 158

06/05

229 166 144 145

06/05

123 102 95 102

Total loan-loss provisions as percentage of total non-performing loans (incl. collateral)

…while coverage ratios of other top German banks are still at a significantly lower level

in €

bn

CB’s strong ratio of loan-loss provisions to non-performing loans – already at a high level – increased again in the first half of 2005 …

I. II. III.Risk Management and Control at Commerzbank

38/48

Development of uncovered risk for the top 20 problem loans (performing/non-performing)in € bn

Domestic corporates and foreign units (defined by CR 6.0-6.5/ER 6.1-6.5)

Overall coverage ratiofor top 20 problem loans:

12/03: 48%12/04: 48%

3/05: 56%6/05: 62%

12/03 3/05 6/0512/04

1.5

2.0

0.5

1.0

20 biggest problem loans have been significantly reduced since 2003

I. II. III.Risk Management and Control at Commerzbank

39/48

• Target for single bulk risk limitation according to the Credit Risk Strategy is to keep the economic capital for single customers below €20m for all ratings of less than 4.5 and below €5m for ratings worse than 4.5.

• Monitoring of compliance with the target is based on a traffic-lights system and regular monthly reporting to Risk/Credit Committee and Board of Directors.

• The traffic-light colour is determined according to the economic capital (Credit VaR) of the single customer. For customers above the limit of €20m, risk reduction (not the same as exposure reduction) is required.

• Within Commerzbank’s Credit Risk Strategy, an overall reduction target for economic capital for credit has been set for 2005/2006

• As of today, only a few customers of the Commerzbank Group are over the limit.

The ECap traffic light derives from the amount of economic capital

which is assigned to the bulk.

since 03/05

1

10

1

€20m

€20m

€20m

3.5€326m

2.0

2.0€1,170m

ECap (CVaR)

year

years€334m

year

MaturityRatingRisk volumeImportant factors influencing economic capital (CVaR) are rating and maturity. The example to the left shows different constellations, all of which lead to the same ECap (CVaR) of €20m.

Bulk risk limitation by economic capital

I. II. III.Risk Management and Control at Commerzbank

Economic capital traffic lights systemTrafficlight Economic capital Measures

> € 20m All R > 4.4: > €5m

Risk reduction required

Monitoring on single-customer

basis

Bulk-risk entry zone

All R < 4.4: > €10m and< €20m

All R < 4.4: > €5m and< €10m

40/48

Volatility

EC / CVaR (Economic capital / Credit value-at-risk)

PD (Probability of default)

LGD (Loss given default)

EaD(Exposure at default)

Totalrevenues Total cost

RoRaC1)

(Return on risk-adjusted capital)

Contributionmargin III

EL/RP (Expected loss / risk provisioning)

Basel II projects:• Master Scale • Rating/scoring• methods (validated

with high GINI)

Bulk risk managementReduction of bulk risk

Internal CB Credit Riskmodel (external bench marked):• Maturity-adjusted CVaR• Element of risk-taking

capability calculation(according to MaRisk)

Projects:• Move to the Top(i.e. “value-driven management”) • Grow to Win

Basel II: LGD Loss collection/estimates• Collateral valuation• Work-out policy

- -

:

Efficiency projects Commerzbank Group

• Risk-adjusted pricing• Performance measurement• Risk management

• Collateral management

• Reduction/ limitation of large free credit lines

• etec project

• Determination of hurdle rate• Alternative: m-t-m evaluation of risk

assets and management as trading position

1) RoRaC is defined as the ratio of operating profit to economic capital (Credit, Operational, Market and Business Risk)

Commerzbank’s hierarchy of targets – Value levers of credit risk strategy

I. II. III.Risk Management and Control at Commerzbank

41/48

Retail

Essenhyp

Corporates Germany

Corporates E. Europe

Corporates USA

Financial institutions

Corporates & Markets (incl. trading book)

BRE

Participations

Workout/ intensive treatment

Bulks

Corporates W. Europe

Corporates Asia

Focus growth Focus risk limitationOverall strategyPortfolio

Clear credit risk strategy

for single portfolios

growth no/low growth reduction

Clear credit risk strategy for segments with potential for growth and risk limitation

I. II. III.Risk Management and Control at Commerzbank

42/48

Agenda

Market Regulator

Customers Bank

Commerzbank

Risk Management

Risk Controlling

I.

Risk Management and Control at Commerzbank

Risk management as a bank’s core competencyGerman Banking InitiativeActivities and outlook

II.

III.Risk Management as a major value driver in overall bank management: Current trends

Dynamics in the Financial Industry

I. II. III.Risk Management as a major value driver in overall bank management

43/48

Risk management is our core competenceRisk management brings benefits for…

…ourcustomers

…ourshareholders

…ourexternal ratings

…ourstaff

• Low beta-errors and the readiness to give loans also to weaker customers • Risk-adjusted, fair market conditions by modern pricing tools and efficient processes• Steady supply with innovative credit and capital-market products• Intensive treatment based on early warning systems focused on restructuring

• Stable earnings through low volatility and professional early warning systems based on an advanced RoRaC concept increase profitability

• Risk transparency and forecasting capability with regard to portfolioquality are essential for external rating agencies

• Clear and consistent steering concepts for asset allocation

• To work for a top risk management institution creates confidenceand higher motivation

Our strategic goal: ‘Being the benchmark’ in risk management and risk control

CB seeks distinction through professional risk management!

I. II. III.Risk Management as a major value driver in overall bank management

44/48

Commerzbank’s CRO is sitting in the driver’s seat in the German Banking Initiative (IFD) as lead Sherpa for mid-cap financing

Direct capital-market access

Financing of SMEs and mid-caps in normal and growth

periods

Medium-sized corporates in crisis and measures of the

banks

Financing of start-ups and young companies

Rating as an added value for medium-sized corporates

Equity capital provision and mezzanine financing

Efficient collateral management

Sound knowledge of risk management helps to find market solutions in a more volatile environment: e.g. IFD mid-cap financing activities

I. II. III.Risk Management as a major value driver in overall bank management

45/48

����

Internal rating in accordance with Basel II strengthens Germany as a financial centre and therefore “Standort Deutschland”

Rating functions

Banks will be distinguished in future by the quality of their rating and scoring systems, as well as by their use in production, sales and communication.

Instrument of communication

Diagnosis:early detection of adverse trends at

the company

Ensures SME financing

Basis for alternative forms of financing

(e.g. mezzanine)

Enhance banks’ willingness to

grant loans

Risk-adjustedpricing

I. II. III.Risk Management as a major value driver in overall bank management

46/48

Besides front office and back office (operative credit functions), an active portfolio management unit has been set up, which takes loans at market-oriented calculative prices and steers these portfolios for own account. Loans shifted from banking book to trading book.

A2 Development ofcredit portfolio-managementfunction

More rigid framework within Basel II: differences between EL calculation and loan-loss provisions (LLP) will be reduced. Stronger market focus on adequate LLP for disclosure-relevant portfolios within the context of Basel II. Implementation of LLP requirements according to IAS.

A3 Loan-loss provisions (LLP)

Reorganisation based on the results of the end-to-end credit project. Increasing use of risk engines for standardized, granular portfolios. Achieving a leaner credit administration using all possibilities, incl. outsourcing.

A5 Credit linefunctions

Enhanced use of secondary markets in line with proactive management (e.g. syndication, securitisation, hedging by CDSs). Limitation through allocated economic capital. At single-deal and portfolio levels, development and establishment of active credit trading.

A1 Active trading on secondarycredit markets

A Credit Risk

In the course of Basel II, banks are focusing on core portfolios in keeping with clear credit-risk strategies. Market-entry barriers for smaller institutions, as certain deals cannot be adequately handled (e.g. specialized lending).

A4 Credit portfoliostructure

Market outlook and Commerzbank activities

I. II. III.Risk Management as a major value driver in overall bank management

47/48

Risk control is well positioned for further enhancements with three sections responsible for credit risk. Build-up of a solid data history, definition of a salary framework for employees, scaling of the parameters PD, LGD, EaD according to Basel II for all relevant market portfolios; evidence of a consistent use-test, establishment of a standard “default” definition via Basel II (substantial liabilities of a debtor more than 90 days overdue).

A7 Credit risk control

Enhancement of the job description of a bank risk manager for single customers in difficult financial conditions (= intensive treatment) with knowledge of secondary markets and credit-administrator expertise. Clear measurement of the success of theportfolios. Optimisation of work-out, using all available modern instruments. Clear orientation to transfer prices for the optimisation of the portfolio. Enhancement of early-warning capability in “white area” [higher rating brackets]. Creation of centres of competence for renewable energy and shipping, Service Centre Inkasso and CORECD.

A8 Intensivetreatment

Credit risk strategy refined to reflect MaK in coordination with the Bank’s supervisory authorities. Strategic limitation based on unexpected loss and steering of all relevant portfolios via RoRaC. Concentration on mid-caps, private-customer lending andliquid trading-oriented products for large caps.

A6 Credit risk strategy

Enhancement of rating- and scoring-systems (analysis of discriminance, concentration measures, rating migrations, Gini coefficient, etc.). Advanced use of secondary-market databases (KMV, credit spreads).

A9 Credit riskanalysis

Market outlook and Commerzbank activities

I. II. III.Risk Management as a major value driver in overall bank management

48/48

Stronger cash-flow orientation through use of forward-looking scenario analyses. Limit-setting for base and stress scenarios.

D LiquidityRisk

Regulatory support for “New Product Processes”. Development of product- and target-group analysis (risk-)cost/revenue calculations and enhanced integration of economic capital concepts into all sub-areas of overall bank management. Implementation of MaRisk at Commerzbank and relevant Group entities. Ensure full MaRisk compliance within the external deadline (Dec. 2006).

E Overall bankmanagement/regulations

More scenario analysis (focusing on event risk, stress testing and economic cycles). Shorter holding period for participations (reduced long positions). Enhanced liquidity valuation of trading positions. Inclusion of hedge fund investments.

B Market Risk

Build-up of data histories, alternative modelling in line with Basel II. Great and increasing significance of outsourcing projects and enhanced risk mitigation (e.g. via insurance).

C Operational Risk

Market outlook and Commerzbank activities

I. II. III.Risk Management as a major value driver in overall bank management

For more information, please contact:Commerzbank Investor Relations

Jürgen Ackermann Head of Investor RelationsP: +49 69 136 22338M: [email protected]

Sandra BüschkenP: +49 69 136 23617M: [email protected]

Ute Heiserer-JäckelP: +49 69 136 41874M: [email protected]

Simone NuxollP: +49 69 136 45660M: [email protected]/ir

Disclaimer

/ investor relations /

This presentation has been prepared and issued by Commerzbank AG. This publication is intended for professional and institutional customers./Any information in this presentation is based on data obtained from sources considered to be reliable, but no representations or guarantees are made by Commerzbank Group with regard to the accuracy of the data. The opinions and estimates contained herein constitute our best judgement at this date and time, and are subject to change without notice. This presentation is for information purposes, it is not intended to be and should not be construed as an offer or solicitation to acquire, or dispose of any of the securities or issues mentioned in this report./Commerzbank AG and/or its subsidiaries and/or affiliates (herein described as Commerzbank Group) may use the information in this presentation prior to its publication to its customers. Commerzbank Group or its employees may also own or build positions or trade in any such securities, issues, and derivatives thereon and may also sell them whenever considered appropriate. Commerzbank Group may also provide banking or other advisory services to interested parties./Commerzbank Group accepts no responsibility or liability whatsoever for any expense, loss or damages arising out of, or in any way connected with, the use of all or any part of this presentation./Copies of this document are available upon request or can be downloaded from www.commerzbank.com/aktionaere/index.html