0121006891 - NE Sturdevant Road

97

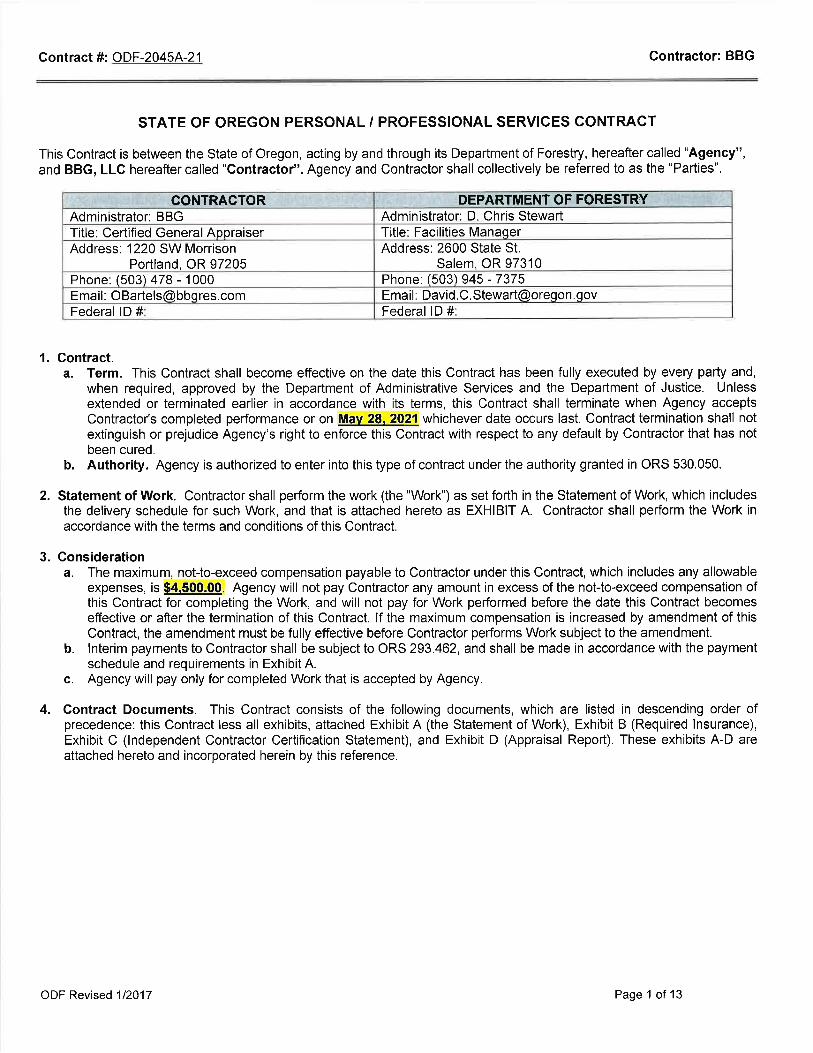

Foley Land Northeast Sturdevant Road Toledo, Oregon 97391 BBG File #0121006891 Contract #ODF-2045A-21 Prepared For Mr. D. Chris Stewart Oregon Department of Forestry 2600 State St. Salem, OR 97310 Report Date June 16, 2021 Prepared By BBG, Inc., Portland Office 1220 SW Morrison Portland, OR 97205 503-478-1000 Client Manager: Owen Bartels, MAI [email protected]

Transcript of 0121006891 - NE Sturdevant Road

Foley Land Northeast Sturdevant Road

Toledo, Oregon 97391

BBG File #0121006891 Contract #ODF-2045A-21

Prepared For Mr. D. Chris Stewart

Oregon Department of Forestry 2600 State St.

Salem, OR 97310

Report Date June 16, 2021

Prepared By BBG, Inc., Portland Office

1220 SW Morrison Portland, OR 97205

503-478-1000

Client Manager: Owen Bartels, MAI [email protected]

FOLEY LAND APPRAISAL

June 16, 2021

Mr. D. Chris Stewart Oregon Department of Forestry 2600 State St. Salem, OR 97310

Re: Appraisal of Real Property

Foley LandNortheast Sturdevant Road Toledo, Oregon 97391

BBG File #0121006891 Contract #ODF-2045A-21

Dear Mr. Stewart:

In accordance with your authorization (per the engagement letter found in the addenda of this report), we have prepared an Appraisal of the above-referenced property.

The subject property consists of 5.54 acres of unimproved land comprised of two tax lots which are in the Urban Growth Boundary for the City of Toledo. The property owner is in the process annexing them into the City (with a change in residential zoning) and filing a lot line adjustment. Per the client's request, we consider that both the annexation (with related zoning change) and lot line adjustment have been completed.

Key to understanding the subject property is the recognition that it is not currently improved. There is no home, no septic or sewer to a building site, no well or public water installed, no driveway. The owner has expressed an intention to subdivide the property and sell individual lots, but there is not a plat map drawn or approved, nor an application for subdivision submitted, nor engineering drawings or approvals. As of the writing of this report, the property is raw land with some future development potential.

As of the valuation date of this report, Kelly and Lorraine Foley own the subject property. The client is considering the purchase of the property in order to develop an office on it (via a conditional use permit). A purchase price has not been established.

This appraisal report was prepared to conform with the requirements of the Uniform Standards of Professional Appraisal Practice (USPAP), and has been written in accordance with the Code of Ethics and the Standards of Professional Practice of the Appraisal Institute. In addition, this report is intended to be in compliance with additional requirements of Oregon Department of Forestry (client). The report is intended to be used by the client. No other party may rely upon the findings in this report.

The global outbreak of a "novel coronavirus" known as COVID-19 was officially declared a pandemic by the World Health Organization (WHO) on March 11, 2020, with the President of the United States declaring the COVID-19 outbreak a national emergency on March 13.

The goal is to encourage "social distancing," which health experts have stressed can slow the spread of the disease and keep health systems from being overwhelmed. The order will almost certainly help in

Mr. Stewart June 16, 2021 Page 2

FOLEY LAND APPRAISAL

mitigating the impact of the virus, particularly for the most vulnerable populations. However, while the economic effects of this order are currently unclear, the impact on the regional and state economy could be considerable.

During the initial stage of the response it was ordered that businesses that do not provide “essential” services must send workers home. Among those remaining open are grocery stores, pharmacies, restaurants for delivery only and hardware stores. Most workers are ordered to stay home, with exceptions including health care workers; police, fire and other emergency responders; and utility providers such as electricians, plumbers and sanitation workers. Public transportation will run for essential travel, and airports are not closing.

The impact of the virus has created near-term instability in the capital and real estate markets. It is currently unknown what direct, or indirect, effect, this event may have on the national economy, the local economy and the market in which the subject property is located for some time. The reader should note the data and comparables used in this report are data points that occurred in the past and there is projection risk associated with using lagging indicators. While every attempt has been made to determine the impact on value of the subject property, the associated risk may not yet be priced into the real estate market. Our conclusions have been based on best available market evidence including interviews with market participants and analysis of all relevant current market data.

Please reference the COVID-19 Disease overview section of this appraisal report for further discussion.

Note: Our opinion of market value is subject to the following Extraordinary Assumptions and/or Hypothetical Conditions:

Based on our inspection of the property and the investigation and the analysis undertaken, we have concluded the following value opinion(s).

This letter must remain attached to the report, which should be transmitted in its entirety, in order for the value opinion set forth to be considered valid.

Extraordinary Assumption(s) This apprai sa l empl oys no extraordinary ass umptions .

Hypothetical Condition(s) This apprai sa l is based on the hypothetical condi tion that the propos ed lot l ine is

complete, as indicated on the provi ded map for thi s appra is al .

This appra isa l is bas ed on the hypothetica l condition that the subject has been

incorporated into the Ci ty of Tol edo, a t the sel l er's expens e.

The val ues pres ented wi thin this apprai sa l report are s ubject to the extraordinary as sumpti ons and hypothetical

condi tions l i s ted below. Purs uant to the requi rement within Uniform Standards of Profess iona l Appra is al Practi ce

Standards , i t i s stated here that the us e of any extraordinary as sumpti ons might have affected the ass ignment

res ul ts .

EXTRAORDINARY ASSUMPTION(S) AND HYPOTHETICAL CONDITION(S)

Appraisal Premise Interest Appraised Date of Value Value Conclusion

Market Va lue - As Is Fee Simple May 13, 2021 $240,000

MARKET VALUE CONCLUSION(S)

Mr. Stewart June 16, 2021 Page 3

FOLEY LAND APPRAISAL

Our firm appreciates the opportunity to have performed this appraisal assignment on your behalf. If we may be of further service, please contact us.

Sincerely, BBG, Inc.

Owen Bartels , MAI Sydni A. Nicol ici

OR Certi fied Genera l Apprais er OR Certi fied Genera l Apprais er

License #: C000870 License #: C001356

503-478-1016 503-478-1011

FOLEY LAND APPRAISAL

TABLE OF CONTENTS

Subject Property ................................................................................................................................1

Summary of Salient Facts ...................................................................................................................2

Property History ................................................................................................................................3

Scope of Work ...................................................................................................................................4

Market Concerns................................................................................................................................8

Regional Analysis ............................................................................................................................. 19

Surrounding Area Analysis ............................................................................................................... 26

Market Analysis ............................................................................................................................... 30

Site Description................................................................................................................................ 32

Property Tax Analysis ....................................................................................................................... 44

Highest and Best Use ....................................................................................................................... 45

Valuation Process ............................................................................................................................ 48

Land Valuation ................................................................................................................................. 49

Certification ..................................................................................................................................... 61

Standard Assumptions and Limiting Conditions ................................................................................ 62

Addenda .......................................................................................................................................... 66

SUBJECT PROPERTY 1

FOLEY LAND APPRAISAL

SUBJECT PROPERTY

AERIAL PH OTOGRAPH

SUMMARY OF SALIENT FACTS 2

FOLEY LAND APPRAISAL

SUMMARY OF SALIENT FACTS

PROPERTY DATA

Property Name

Address

Location

County

Parcel Number

Census Tract No.

Legal Description

Site Area

Primary Site 241,322 s quare feet (5.5400 acres )

Zoning

Flood Status Zone AE is a Specia l Flood Hazard Area (SFHA) where base flood elevations are

provided. AE Zones are now used on new format Flood Insurance Rate Maps (FIRM)

instead of A1-A30 Zones . In communities that parti cipate in the Nationa l Flood

Insurance Program (NFIP), mandatory flood insurance purchase requi rements apply to

this zone.

Foley Land

Northeast Sturdevant Road

Toledo, Oregon 97391

The subject fronts the east s ide of SE Sturdevant Rd. and extends east to SE Chedester

Rd. in the UGB for the Ci ty of Toledo.

Lincoln

A portion of R273276, R508704

951400

A portion of Lot 1100 and al l of Lot 1000 in the Northeast 1/4 of Section 17, Township 11S,

Range 10W, WM, Lincoln County, Oregon. A more deta i led legal description was not

ava i lable and the subject i s currently subject to a lot l ine adjustment.

R-1; Medium Dens i ty Res identia l

Zone X (unshaded) i s a Non-Special Flood Hazard Area (NSFHA) of minimal flood hazard,

usual ly depicted on Flood Insurance Rate Maps (FIRM) as above the 500-year flood level .

Thi s is an area in a low to moderate risk flood zone that i s not in any immediate danger

from flooding caused by overflowing rivers or hard ra ins . In communities that parti cipate

in the National Flood Insurance Program (NFIP), flood insurance is avai lable to a l l

property owners and renters in thi s zone.

Advantages The subject wi l l be annexed into the City which market parti cipants indicate

increas es val ue.

The property i s fronted by a paved, publ i c roadway.

Electrici ty i s ava i lable to the s i te.

Challenges Publ ic sewer i s 500-600' away and the cost to extend would be s i gni fi cant.

The property i s heavi ly treed and wi l l need to be cl eared i n order to be developed.

RISK SUMMARY

As Is as of May 13, 2021

Approach Reliance

Value Conclusion - As Is $240,000 $0.99 Per Square Foot

Exposure Time (Months) 1-3 months

Marketing Time (Months) 1-3 months

VALUE INDICATIONS

Sales Comparison Approach

PROPERTY HISTORY 3

FOLEY LAND APPRAISAL

PROPERTY H ISTORY

The subject is owned by Kelly and Lorraine Foley. The client is considering the purchase of the property, although a purchase price has not been established as of yet. The subject owner purchased the property more than 10 years ago and has retained it as an investment. Due to the increased home values in the area, they decided it would be a good time to sell the property.

As part of the sale negotiations, the seller will manage and pay for the annexation of the subject into the City. Also, they will complete a lot line adjustment which provides a buffer to the home they own adjacent to the subject.

We interviewed the City and County regarding the subject. The representatives for each planning department stated the annexation process is typical of similar properties in the UGB. Steps for approval have been taken and the soonest annexation could occur was reported to be July. However, the City planner stated it may take longer and depends on the availability of committees for approvals.

Electricity is available to the site. However, the City of Toledo planner stated water and sewer are about 50—to 600’ away (to the south, near the school).

We are not aware of any other sale or listing activity of the subject in the past three years.

SCOPE OF WORK 4

FOLEY LAND APPRAISAL

SCOPE OF WORK

SCOPE OF THE INVESTIGATION

General and Market Data Analyzed

Regional economic data and trends

Market analysis data specific to the subject property type

Published survey data

Neighborhood demographic data

Comparable sale data

Floodplain status

Zoning information

Assessor’s information

Interviewed professionals knowledgeable about the subject’s property type and market

Inspection Details Owen Bartels, MAP, conducted an interior and exterior inspection on May 13, 2021.The comparables were not personally inspected by the appraisers signing this report.

Property Specific Data Requested and Received

Data Requested, but not Provided

APPRAISAL INFORMATION

Client

Intended User(s)

Intended Use

Property Rights Appraised / Premise

Date of Inspection

Marketing Time

Exposure Time

Owner of Record

Property Contact(s)

Most Probable Purchaser

Highest and Best Use

If Vacant

This appraisa l i s to be used for potential property acquis ition purposes .

Oregon Department of Forestry

2600 State St.

Sa lem, OR 97310

This appraisa l report may only be rel ied upon by the cl ient and intended user(s ) named

herein Oregon Department of Forestry.

•Market Value of the Fee Simple interest in the subject property, As Is as of May 13, 2021

May 13, 2021

1-3 months

1-3 months

Kel ly K. and Lorra ine J. Foley

Justin Peterson, Community and Economic Development Planner, provided information

regarding annexation a long with a representative from the Ci ty of Toledo Planning

Department. Kel ly Foley, sel ler, was a lso interviewed for this appra isal .

Investor or owner-user

Hold for development to uses al lowed by zoning

PROPERTY DATA RECEIVEDLot l ine adjustment map

Broker Opinion of Va lue

DATA REQUESTED, BUT NOT PROVIDED

Ti tle report

SCOPE OF WORK 5

FOLEY LAND APPRAISAL

Data Sources

VALUATION METHODOLOGY

Most Probable Purchaser To apply the most relevant valuation methods and data, the appraiser must first determine the most probable purchaser of the subject property.

The most probable purchaser of the subject is an investor looking to hold the property as an investment (until public utilities are pulled to the site) or an owner-user who will develop the property to uses allowed by zoning, which do not require public utilities.

Valuation Methods Utilized This appraisal employs only the Sales Comparison Approach. Based on our analysis and knowledge of the subject property type and relevant investor and buyer profiles, it is our opinion that this approach would be considered necessary and applicable for market participants. Since no improvements exist on site, the Cost Approach is not relevant. The property generates no income and is not typically marketed, purchased or sold on the basis of anticipated lease income; thus, the Income Capitalization Approach was precluded.

Si te SizeAs ses s or's Records & Propos ed Lot Line

Adjustment Map

Tax Data As ses s or's Records

Zoning InformationPlanning Dept (Ci ty of Toledo a nd Lincoln

County)

Flood Status FEMA

Demographics Reports Spotl ight

Comparable Land Sa lesMLS, Brokers , Phone Veri fi cations,

Appra is er's Fi les

DATA SOURCES

Extraordinary Assumption(s) This apprai sa l empl oys no extraordinary ass umptions .

Hypothetical Condition(s) This apprai sa l is based on the hypothetical condi tion that the propos ed lot l ine is

complete, as indicated on the provi ded map for thi s appra is al .

This appra isa l is bas ed on the hypothetica l condition that the subject has been

incorporated into the Ci ty of Tol edo, a t the sel l er's expens e.

The val ues pres ented wi thin this apprai sa l report are s ubject to the extraordinary as sumpti ons and hypothetical

condi tions l i s ted below. Purs uant to the requi rement within Uniform Standards of Profess iona l Appra is al Practi ce

Standards , i t i s stated here that the us e of any extraordinary as sumpti ons might have affected the ass ignment

res ul ts .

EXTRAORDINARY ASSUMPTION(S) AND HYPOTHETICAL CONDITION(S)

SCOPE OF WORK 6

FOLEY LAND APPRAISAL

DEFINITIONS

Market Value “The most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby:

Buyer and seller are typically motivated;

Both parties are well informed or well advised, and acting in what they consider their own best interests;

A reasonable time is allowed for exposure in the open market;

Payment is made in terms of cash in U.S. dollars or in terms of financial arrangements comparable thereto; and

The price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions granted by anyone associated with the sale.”

(Source: Code of Federal Regulations, Title 12, Chapter I, Part 34.42[g]; also Interagency Appraisal and Evaluation Guidelines, Federal Register, 75 FR 77449, December 10, 2010, page 77472

As Is Market Value As is market value is defined as, “The estimate of the market value of real property in its current physical condition, use, and zoning as of the appraisal date.”

(Source: Appraisal Institute, The Dictionary of Real Estate Appraisal, 6th ed. (Chicago: Appraisal Institute, 2015); also Interagency Appraisal and Evaluation Guidelines, Federal Register, 75 FR 77449, December 10, 2010, page 77471

Definition of Property Rights Appraised

Fee simple estate is defined as, “Absolute ownership unencumbered by any other interest or estate, subject only to the limitations imposed by the governmental powers of taxation, eminent domain, police power, and escheat.”

Source: Appraisal Institute, The Dictionary of Real Estate Appraisal, 6th ed. (Chicago: Appraisal Institute, 2015)

SCOPE OF WORK 7

FOLEY LAND APPRAISAL

Applicable Requirements

This appraisal is intended to conform to the requirements of the following:

Uniform Standards of Professional Appraisal Practice (USPAP);

Code of Professional Ethics and Standards of Professional Appraisal Practice of the Appraisal Institute;

Applicable state appraisal regulations.

LEVEL OF REPORTING DETAIL

Standards Rule 2-2 (Real Property Appraisal, Reporting) contained in USPAP requires each written real property appraisal report to be prepared as either an Appraisal Report or a Restricted Appraisal Report.

This report is prepared as an Appraisal Report. An Appraisal Report must at a minimum summarize the appraiser’s analysis and the rationale for the conclusions. This format is considered most similar to what was formerly known as a Summary Appraisal Report in prior versions of USPAP.

MARKET CONCERNS 8

FOLEY LAND APPRAISAL

MARKET CONCERNS

COVID-19 D ISEASE; SARS-COV-2 V IRUS

CDC

On January 30, 2020, the International Health Regulations Emergency Committee of the World Health Organization (WHO) declared the outbreak a “public health emergency of international concern” (PHEIC). On January 31, Health and Human Services Secretary Alex M. Azar II declared a public health emergency (PHE) for the United States to aid the nation’s healthcare community in responding to COVID-19. On March 11, WHO publicly characterized COVID-19 as a pandemic. On March 13, the President of the United States declared the COVID-19 outbreak a national emergency.

COSTAR | MARCH 1, 2021

The process for writing this column every week generally starts with updating a set of charts tracking high-frequency data on the economy and then discussing what they mean. The narrative direction for the week is born out of your authors’ ongoing Microsoft Teams chat, trading charts back and forth, sending quotes from Federal Reserve speeches, talking markets.

That process last week led to something of a landmark event for CoStar Economy: We’re feeling quite optimistic on the economy for the first time in a long time. Let’s explain why.

First, let’s check in on the most important graph for the economy: COVID-19 infection rates. This has been the graph to watch for nearly a full year as we are approaching the anniversary of the quarantine. As fast and furious as the rise in coronavirus infection rates was to close out 2020, they have come down just as quick. For the West and Midwest in particular, positive test rates are as low as they have been since the pandemic began.

MARKET CONCERNS 9

FOLEY LAND APPRAISAL

This is great news as the third wave of cases clearly affected economic and job growth, with net negative job growth over the months of December 2020 and January 2021. It appears that activity picked up quickly as the spread began to subside, almost concurrently. Some of our favorite high-frequency indicators are showing very strong signs that things are starting to get better. And quickly. Data from the reservation service OpenTable on restaurant traffic, below in red, is already back to its highest levels since the summer of 2020, when massive rehiring of leisure, hospitality and entertainment workers was driving monthly jobs gains into the millions. Credit and debit card spending, as measured by Affinity Solutions in blue, is also clearly rising in 2021 and currently stands at pandemic highs — even though the trend is pretty volatile.

MARKET CONCERNS 10

FOLEY LAND APPRAISAL

While restaurant traffic is still down a hefty 40% from a year ago, a combination of vaccinations, healthier restaurant practices and possibly herd immunity effects are pushing activity higher much faster. With Johnson & Johnson’s single-shot vaccine getting very positive news last week, this dynamic of increasing in-person activity should accelerate through the spring.

Consumer spending has been on an absolute tear as well, for all the reasons mentioned above but more importantly because of the fiscal stimulus enacted at the close of 2020. The chart below measures total personal income growth against personal income without emergency fiscal stimulus. Personal income in January 2021 skyrocketed to levels not seen since $1,200 checks were sent out in April 2020. While this time around the checks were only $600, these government benefits completely overshadowed the income growth weakness that began in December as hiring slowed to a standstill.

MARKET CONCERNS 11

FOLEY LAND APPRAISAL

With incomes boosted once again, and more freedom for individuals to move around and spend money, we can say with confidence this is the most optimistic backdrop we’ve had since the start of the crisis. The bond market has noticed this too, with 10-year U.S. Treasury rates hitting 1.6% briefly before falling back to close the week just below 1.5%. These are levels not seen since February 2020. Federal Reserve Chairman Jerome Powell stuck to his dovish script in front of Congress this past week, indicating “monetary policy is accommodative and it continues to need to be accommodative. ... Expect us to move carefully, patiently, and with a lot of advance warning.”

We feel compelled to offer a few reminders. First, rising long-term bond yields aren’t necessarily a bad thing! It’s less important to know that yields are rising than it is to know why they are rising. In this case, they are rising because economic growth is picking up. As of this writing, the Atlanta Fed’s GDPNow forecast for gross domestic product growth for the first quarter of 2021 is near 9%. That’s a good thing and will help make up the shortfall in GDP from pre-pandemic levels as well as assist in putting the roughly 10 million people without jobs back to work.

Second, the level of interest rates matters, not just the direction. The worry is that fast-rising interest rates will choke off economic growth. Does anyone here think 1.5% or even 2% interest rates are restrictive, hovering around zero when adjusted for inflation? As we wrote last week, housing market tailwinds will occur even at higher mortgage rates. Both mortgage and Treasury yields remain lower than at any level ever prior to 2020.

Lastly, the Fed has held strong in its conviction to keep short-term interest rates low until a rebound in the economy and labor market is well underway. The two-year Treasury rate agrees with them. While rates at points further out the curve have risen sharply, the two-year has barely budged and remains at

MARKET CONCERNS 12

FOLEY LAND APPRAISAL

only 0.14% as of this writing. That tells us that the Fed won’t be raising rates anytime soon to slow down the economy. That means the yield curve has been steepening quickly. Bizarrely, this has been pointed out as a bad sign for growth, or at least a reason to worry that growth will be crimped by higher interest rates. In fact, a steepening yield curve has been a clear leading indicator for an improving economy coming out of a recession. The move steeper over the last few weeks has been fairly sharp, but it’s actually just catching levels typically seen when coming out of a recession.

The yield curve tracks consumer and business sentiment indices quite closely. If this is an indication of anything, it’s of more strength to come.

We don’t want to miss the forest through the trees here: there is still a long, long way to go before cumulative conditions return to where we were a year ago, and millions upon millions are still out of work. But if these trends keep up, and especially if new stimulus passes, that could happen quite quickly. As our opening quote suggests, many households and industries were broken in 2020. The world itself broke, in a way. But it appears that we are healing, and becoming stronger in those broken places.

The Week Ahead …

Next week is all about jobs, with an update on employment in February to be released on Friday. As activity remained depressed as of early February, the report is unlikely to capture the optimism we discussed above. But we will continue to keep a close eye on hiring of employment service employees, a reliable leading indicator for broader hiring, as well as the working conditions for long-term unemployed and disaffected workers.

Secondary to the jobs report, but still important and perhaps more forward-looking, are the Institute for Supply Management surveys. Business confidence has been strong in light of improved vaccine news, and look to continue that way as the ISM manufacturing index is released on Monday and ISM services index on Wednesday.

MORT GA GE BAN KER S ASSOCIA TION: HOME PUR CHA SES | FE BRUARY 5, 2021

Mortgage applications to purchase a home have accelerated in the second half and the housing market remains healthy and active. Home purchases spur economic activity.

MARKET CONCERNS 13

FOLEY LAND APPRAISAL

INIT IA L JOBLE SS CLA IM S|FEBRUARY 25, 2021

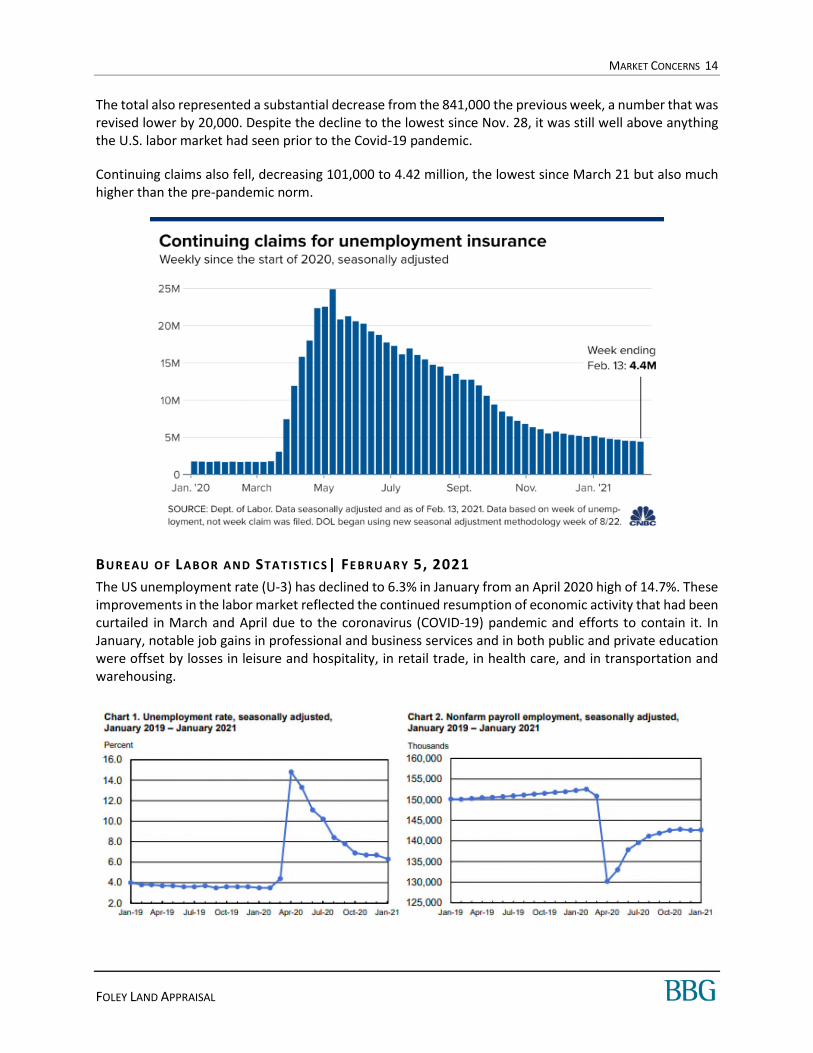

On March 26th initial jobless claims showed an increase in unemployment by 3.1 million persons for the week of March 16th-20th, setting a record that would be broken the following week at 6.9 million. All weekly claims reported since March 26th are higher than any historical figure prior to COVID-19. The following chart illustrates the weekly initial jobless claims in 2020 and into 2021.

Jobless claims fell sharply last week despite severe winter storms that swept across Texas and other parts of the South, the Labor Department reported Thursday. First-time filings for unemployment insurance totaled 730,000 for the week ended Feb. 20, well below the Dow Jones estimate of 845,000.

MARKET CONCERNS 14

FOLEY LAND APPRAISAL

The total also represented a substantial decrease from the 841,000 the previous week, a number that was revised lower by 20,000. Despite the decline to the lowest since Nov. 28, it was still well above anything the U.S. labor market had seen prior to the Covid-19 pandemic.

Continuing claims also fell, decreasing 101,000 to 4.42 million, the lowest since March 21 but also much higher than the pre-pandemic norm.

BUREAU OF LABOR AND STA TISTIC S| FE BRUAR Y 5, 2021

The US unemployment rate (U-3) has declined to 6.3% in January from an April 2020 high of 14.7%. These improvements in the labor market reflected the continued resumption of economic activity that had been curtailed in March and April due to the coronavirus (COVID-19) pandemic and efforts to contain it. In January, notable job gains in professional and business services and in both public and private education were offset by losses in leisure and hospitality, in retail trade, in health care, and in transportation and warehousing.

MARKET CONCERNS 15

FOLEY LAND APPRAISAL

GDP FOREC A ST S

The following chart summarizes GDP forecasts from various economists and institutions. Please note the annualized figures are the quarterly change multiplied by four.

While Q2 was beyond painful, the worst is behind us and Q3 was outstanding. The fourth quarter was strong and the outlook for 2021 is much improved. High growth rates are expected into 2022.

NAREIT/TREPP: CMBS DEL IN QUENC Y| MARCH 2021

In February, the Trepp CMBS Delinquency Rate generated its largest improvement since the beginning of the pandemic. After two huge jumps in the reading in May and June of last year, the rate has now declined for eight consecutive months. The Trepp CMBS Delinquency Rate in February was 6.80%, a decline of 78 basis points from the January number, which is the biggest drop over the last eight months. The percentage of loans in the 30 days delinquent bucket is 0.58% – down 16 basis points for the month.

Source Date Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full Year

CNBC/Moody's Consensus 3/1 -- -- -- -- -- 5.0% 8.5% 7.0% -- 6.0%

Mortgage Bankers Association 2/19 -- -- -- -- -- 4.8% 5.1% 7.2% 6.4% 5.9%

Goldman Sachs 2/9 -- -- -- -- -- -- -- -- -- 6.8%

Atlanta Fed GDP Now 3/1 -- -- -- -- -- 10.0% -- -- -- --

Actual -5.0% -32.8% 33.4% 4.0% -3.5% -- -- -- --

CNBC/Moody's Consensus -- -- -- -- -- 1.3% 2.1% 1.8% --

Mortgage Bankers Association -- -- -- -- -- 1.2% 1.3% 1.8% 1.6%

Goldman Sachs -- -- -- -- -- -- -- -- --

Atlanta Fed GDP Now -- -- -- -- -- 2.5% -- -- --

Actual -1.3% -8.2% 8.4% 1.0% -- -- -- --

2020 GDP Forecasts

Annualized

2021 GDP Forecasts

Annualized

Change from Previous Quarter

MARKET CONCERNS 16

FOLEY LAND APPRAISAL

URBAN LA ND INSTITUTE : REA L ESTATE EC ON OMIC FORECA ST| OC TOBER 2020

ULI compiled forecasts from 43 economist/analysts at 37 real estate organizations. The key findings are noted as follows.

Transaction Volume

Commercial real estate transaction volume reached $593 billion in 2019, a post-Great Financial Crisis peak. Volume is expected to be about 50% lower in 2020 with a forecast of $300 billion. Forecasts for ‘21 and ’22 show growth to $400 billion and $500 billion, respectively.

CRE Pricing

The RCA Commercial Property Price Index (CPPI) has experienced strong growth over the last nine years, staying consistently above 6 percent annually. Prices are expected to drop by 2% in 2020, remaining at that level with no change in ‘21 and then resuming growth in ‘22 with a 4% growth rate.

MARKET CONCERNS 17

FOLEY LAND APPRAISAL

MCK IN SEY & COM PAN Y | OCT OBER 30, 2020

The following from McKinsey & Company illustrates the many possible scenarios for the economic impact of the COVID-19 crisis. With a strong public health response and the stimulus package the most likely scenarios are A1 through A4. Other, more extreme scenarios can also be conceived, and some of them are already being discussed (B1–B5 in Exhibit 3). One can’t exclude the possibility of a “black swan of black swans”: structural damage to the economy, caused by a yearlong spread of the virus until a vaccine is widely available, combined with the lack of policy response to prevent widescale bankruptcies, unemployment, and a financial crisis.

If Scenario A1 occurs, McKinsey & Company projects US GDP will return to pre-crisis levels in the third quarter of 2022. If Scenario A3 occurs, McKinsey & Company projects US GDP will return to pre-crisis levels in the first quarter of 2021.

OTHER FEDERA L, STA TE AND LOCA L CON SIDER AT ION S

The federal government, states and municipalities are enacting legislation to lessen the economic impact of COVID-19. Landlords’, owners’ and tenants’ rights may be affected by such legislation. Many states and cities issued shelter-in-place orders forcing most residents to remain indoors except for essential needs like groceries and essential businesses. Several states have proposed legislation that would forgive rent and/or would allow termination of contracts. These issues should be closely monitored as they could place downward pressure on value.

FORCE MA JEURE

Force majeure clauses are contract provisions that excuse a party’s inability to perform its obligations under the contract if an unforeseeable event prevents such performance. Most leases have similar clauses. We are not experts with regard to force majeure contacts and laws. Should COVID-19 become accepted in the US as a force majeure event there may be additional risk for landlords.

MARKET CONCERNS 18

FOLEY LAND APPRAISAL

CONC LUSI ON

COVID-19 infections and overall economic implications are the primary concern of US and international investors; however, as vaccines are becoming more available and GDP growth rates have rebounded the worry among investors has been greatly reduced. Strong economic growth is expected throughout 2021 and into 2022 as rates are expected to remain near historical lows. Given recent bond yield increases, investors have expressed worries over upward pressure on interest rates; however, rates remain well below historical norms.

Medium and long-term outlooks are favorable and interest rates are expected to remain low into 2023, which could bode well for commercial real estate. Over the short-term hotels, restaurants and non-credit retail have taken the brunt of the declines while industrial, self-storage and multi-family have been the least affected. Office demand has faced downward pressures due to remote working trends and elevated levels of unemployment, which are declining. We will continue to interview market participants regarding changes in market conditions.

REGIONAL ANALYSIS 19

FOLEY LAND APPRAISAL

REGIONAL ANALYSIS

L INCOLN COUNTY AREA ANALYSIS

The subject of this appraisal is in the UGB of the City of Toledo, in Lincoln County, Oregon. Lincoln County is in coastal Oregon approximately 130 miles southwest of Portland. It is 980 square miles in size and has a population density of 49 persons per square mile.

Lincoln County extends some 60 miles north and south, but just 15 to 25 miles in width, and is bordered by the Pacific Ocean and the Coast Range. Lincoln County is part of the Central Oregon Coast region, and its northern border is about 80 miles south of the Columbia River. The county is bounded by the Pacific Ocean in the west, by Tillamook County in the north, by Polk and Benton counties in the east, and by Lane County in the south.

TOPOGRA PHY

Principal features of Lincoln County’s topography are rounded hills, and narrow, winding coastal valleys, with the coastal plains being broken at many points by rugged headlands rising abruptly from the ocean. Small, scattered areas of level bottom land border the rivers and streams. Some of the valleys lie only a few feet above sea level; others are as high as 400 feet. Ridge tops vary from 1,000 feet to 1,500 feet in elevation. Many peaks of the Coast Range rise more than 2,000 feet and Saddleback Mountain east of Otis in Clatsop County reaches 3,350 feet.

Lincoln County has five major rivers that run into the Pacific Ocean: the Alsea, Salmon, Siletz, Yachats, and the Yaquina. All have their principal headwaters near the crest of the Coast Range, winding west to the Pacific. Each has formed a small shallow bay at its mouth, the largest of which is the Yaquina, at Newport.

The climate of Lincoln County is greatly influenced by the prevailing westerly winds from the Pacific Ocean. Characteristic features are moderate temperatures, a long frost-free season, and abundant rainfall. Prevailing winds are usually southwest during the winter, and northwest during the summer. Other parts of Oregon at the same latitude are much colder in winter and hotter in the summer. Snow in Lincoln County is rare, except for light falls on the peaks of the Coast Range. The growing season averages 248 days in Newport, 195 days in the Toledo area inland. The last frost of winter can be as late as March 23rd, and the first fall frost as late as November 26th. Lincoln County's mild climate, long growing season, and generous amounts of precipitation are extremely favorable to the growth of vegetation, trees, shrubs, and flowers.

Lincoln County is classified as an entirely rural county by the Oregon Economic Development Department. Thirty-five percent of the county's total land mass is publicly owned--some 217,000 acres, while 65%, or 417,880 acres, is privately owned.

TRANSPORTA TI ON NE TW ORK

The transportation system has a profound impact on Oregon’s coastal counties.

REGIONAL ANALYSIS 20

FOLEY LAND APPRAISAL

H I GHWA YS

Two federal highways serve the county: Highway 101 runs along the Pacific Coast from the Mexican to the Canadian borders. Highway 20 follows a winding route through the Coast Range, connecting with Highway 191 at Newport and with Interstate-5 at Albany. All are winding two-lane highways.

State Routes 18 and 34 connect Lincoln County to the Willamette Valley and Interstate-5, the major West Coast north-south interstate. State Route 18 follows a northeast to southwest route to Lincoln City through McMinnville before connecting with Highway 99W in Newberg. State Route 34, the Alsea Highway, winds through the Coast Range between Waldport and Corvallis before continuing to Lebanon near the eastern edge of the Willamette Valley.

RAI L SERVI CE

The Portland & Western Railroad’s branch line from Albany through Corvallis to Toledo near the eastern end of Yaquina Bay exclusively serves Georgia Pacific’s Toledo pulp and paper mill.

A IRPORTS

Newport Municipal Airport is a city-owned, public use airport located three miles south of Newport’s CBD. It formerly supported commercial passenger service with connections to Portland International Airport, but SeaPort Airlines discontinued service to Newport in July 2011.

POPU LA TION

Lincoln County has an estimated 2021 population of 50,087, which represents an average annual 0.8% increase over the 2010 census of 46,034. Lincoln County added an average of 676 residents per year over the 2010-2021 period, but its annual growth rate lagged the State of Oregon rate of 1.0%.

Looking forward, Lincoln County's population is projected to increase at a 1.0% annual rate from 2021-2026, equivalent to the addition of an average of 432 residents per year. Lincoln County's growth rate is expected to equal that of Oregon, which is projected to be 1.0%.

EMP LOYMEN T

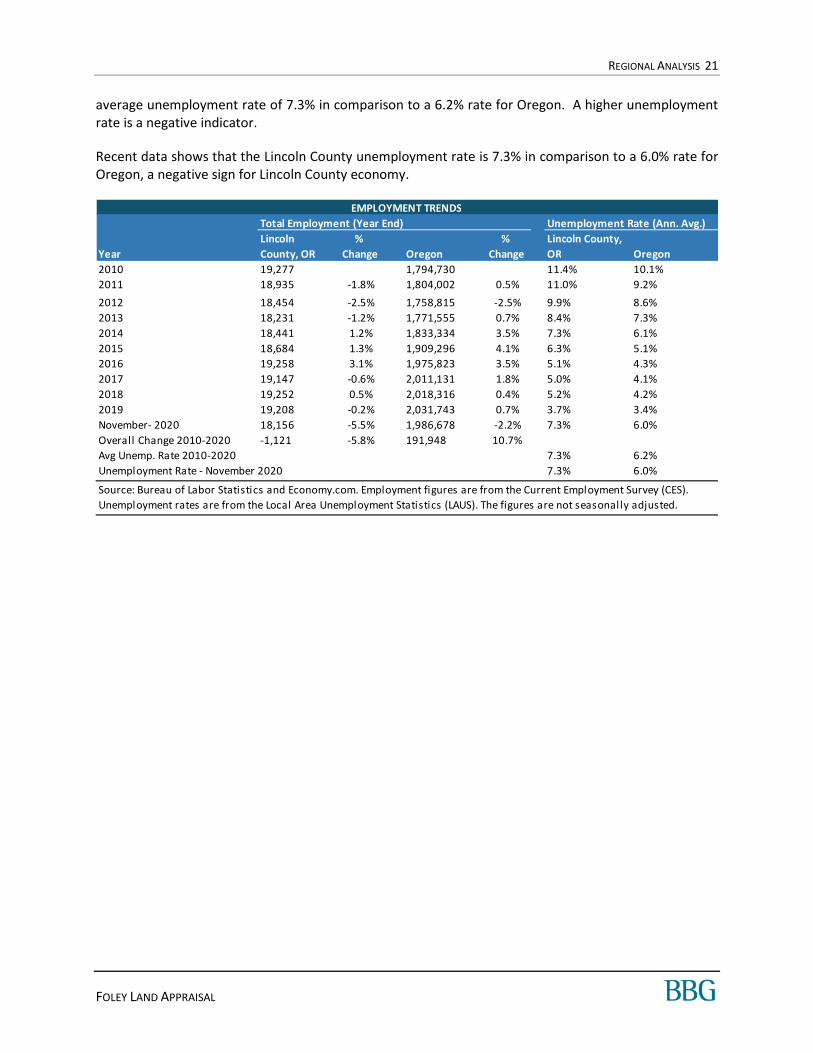

Total employment in Lincoln County is currently estimated at 18,156 jobs. Between year-end 2010 and the present, employment fell by 1,121 jobs, equivalent to a 5.8% decrease over the entire period. There were gains in employment in four out of the past ten years despite the national economic downturn and slow recovery. Along with Lincoln County's employment decreasing over the last decade, it also underperformed Oregon, which experienced an increase in employment of 10.7% or 191,948 jobs over this period.

A comparison of unemployment rates is another way of gauging an area’s economic health. Over the past decade, the Lincoln County unemployment rate has been generally higher than that of Oregon, with an

Population Compound Ann. % Chng

2010 Census 2021 Estimate 2026 Projection 2010 - 2021 2021 - 2026

Lincoln County, OR 46,034 50,087 52,249 0.8% 0.8%

Oregon 3,831,074 4,281,747 4,491,795 1.0% 1.0%

Source: Environics Analytics

POPULATION TRENDS

REGIONAL ANALYSIS 21

FOLEY LAND APPRAISAL

average unemployment rate of 7.3% in comparison to a 6.2% rate for Oregon. A higher unemployment rate is a negative indicator.

Recent data shows that the Lincoln County unemployment rate is 7.3% in comparison to a 6.0% rate for Oregon, a negative sign for Lincoln County economy.

Total Employment (Year End) Unemployment Rate (Ann. Avg.)

Year

Lincoln

County, OR

%

Change Oregon

%

Change

Lincoln County,

OR Oregon

2010 19,277 1,794,730 11.4% 10.1%

2011 18,935 -1.8% 1,804,002 0.5% 11.0% 9.2%

2012 18,454 -2.5% 1,758,815 -2.5% 9.9% 8.6%

2013 18,231 -1.2% 1,771,555 0.7% 8.4% 7.3%

2014 18,441 1.2% 1,833,334 3.5% 7.3% 6.1%

2015 18,684 1.3% 1,909,296 4.1% 6.3% 5.1%

2016 19,258 3.1% 1,975,823 3.5% 5.1% 4.3%

2017 19,147 -0.6% 2,011,131 1.8% 5.0% 4.1%

2018 19,252 0.5% 2,018,316 0.4% 5.2% 4.2%

2019 19,208 -0.2% 2,031,743 0.7% 3.7% 3.4%

November- 2020 18,156 -5.5% 1,986,678 -2.2% 7.3% 6.0%

Overall Change 2010-2020 -1,121 -5.8% 191,948 10.7%

Avg Unemp. Rate 2010-2020 7.3% 6.2%

Unemployment Rate - November 2020 7.3% 6.0%

EMPLOYMENT TRENDS

Source: Bureau of Labor Statistics and Economy.com. Employment figures are from the Current Employment Survey (CES).

Unemployment rates are from the Local Area Unemployment Statistics (LAUS). The figures are not seasonally adjusted.

REGIONAL ANALYSIS 22

FOLEY LAND APPRAISAL

MA JOR EM PLOYER S

Major employers in Lincoln County are shown in the following table.

HOU SEH OLD INC OME

Lincoln County has a considerably lower level of household income than Oregon. Median household income for Lincoln County is $51,631, which is 25.3% less than the corresponding figure for Oregon.

Name

1 Confederated Tribes of Siletz Indians

2 Samaritan Health Services

3 Lincoln County School District

4 Lincoln County

5 OSU Hatfield Marine Science Center

6 Georgia-Pacific - Toledo

7 Rogue Ales and Spirits

8 Fred Meyer

9 Wal-Mart Stores Inc.

10 Mo's Restaurants

11 City of Newport

12 Salishan Spa and Golf Resort

13 Safeway - Newport and Lincoln City

14 City of Lincoln City

15 NOAA - Land and at sea

16 Oksenholt Companies/Meredith

17 Central Lincoln PUD

18 Inn at Spanish Head

19 Oregon Coast Aquarium

20 Mid-Columbia Bus Company

MAJOR EMPLOYERS - LINCOLN COUNTY, OR

Source: Economic Development All iance of Lincoln County

Average Median

Lincoln County, OR $69,318 $51,631

Oregon $95,518 $69,151

Comparison of Lincoln County, OR to Oregon - 27.4% - 25.3%

Source: Environics Analytics

MEDIAN HOUSEHOLD INCOME - 2021

REGIONAL ANALYSIS 23

FOLEY LAND APPRAISAL

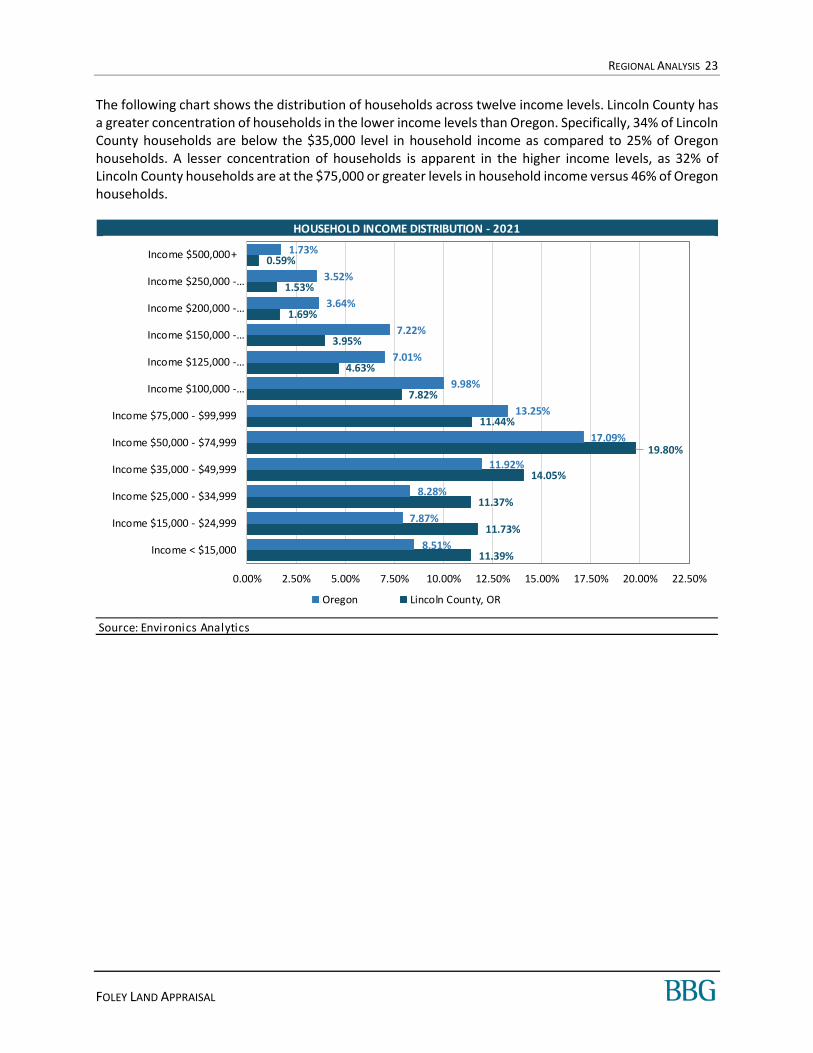

The following chart shows the distribution of households across twelve income levels. Lincoln County has a greater concentration of households in the lower income levels than Oregon. Specifically, 34% of Lincoln County households are below the $35,000 level in household income as compared to 25% of Oregon households. A lesser concentration of households is apparent in the higher income levels, as 32% of Lincoln County households are at the $75,000 or greater levels in household income versus 46% of Oregon households.

HOUSEHOLD INCOME DISTRIBUTION - 2021

Source: Environics Analytics

11.39%

11.73%

11.37%

14.05%

19.80%

11.44%

7.82%

4.63%

3.95%

1.69%

1.53%

0.59%

8.51%

7.87%

8.28%

11.92%

17.09%

13.25%

9.98%

7.01%

7.22%

3.64%

3.52%

1.73%

0.00% 2.50% 5.00% 7.50% 10.00% 12.50% 15.00% 17.50% 20.00% 22.50%

Income < $15,000

Income $15,000 - $24,999

Income $25,000 - $34,999

Income $35,000 - $49,999

Income $50,000 - $74,999

Income $75,000 - $99,999

Income $100,000 -…

Income $125,000 -…

Income $150,000 -…

Income $200,000 -…

Income $250,000 -…

Income $500,000+

Oregon Lincoln County, OR

REGIONAL ANALYSIS 24

FOLEY LAND APPRAISAL

EDUCAT ION AN D AGE

Residents of Lincoln County have a lower level of educational attainment than those of Oregon. An estimated 24% of Lincoln County residents are college graduates with four-year degrees, versus 32% of Oregon residents. People in Lincoln County are older than their Oregon counterparts. The median age for Lincoln County is 52 years, while the median age for Oregon is 40 years.

CONC LUSI ON

The Lincoln County economy will be affected by a growing population base and lower income and education levels. Lincoln County experienced growth in the number of jobs over the past decade, and it is reasonable to assume that employment growth will occur in the future. We anticipate that the Lincoln County economy will improve and employment will grow, strengthening the demand for real estate.

REGIONAL ANALYSIS 25

FOLEY LAND APPRAISAL

REGI ONA L MAP

SURROUNDING AREA ANALYSIS 26

FOLEY LAND APPRAISAL

SURROUNDING AREA ANALYSIS

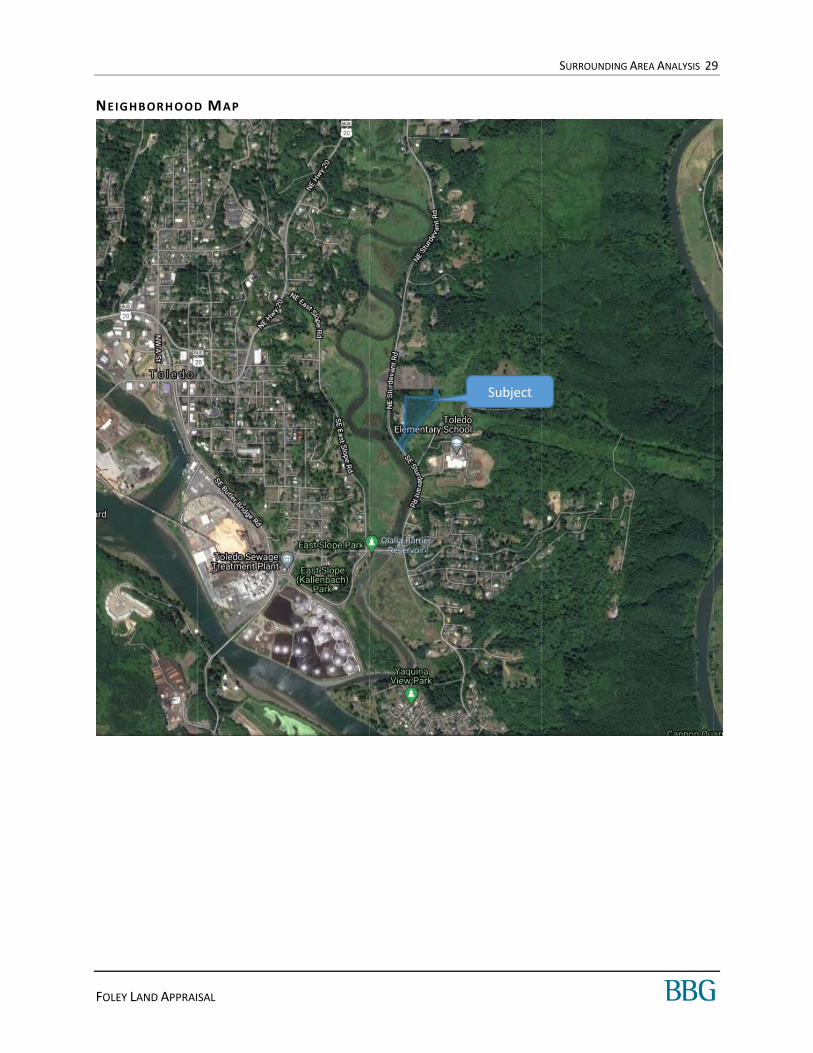

BOU NDAR IES

The subject is located in unincorporated Lincoln County, just outside of the City of Toledo, and within the UGB. This area is part of the Newport, OR MSA.

A map identifying the location of the property follows this section.

ACCESS A ND L I N KA GES

Primary access to the area is provided by Hwy 20, a major arterial that crosses the Lincoln County area in an east/west direction. Access to the subject from Hwy 20 is provided by Sturdevant Rd and travel time from the major arterial to the subject is about two minutes. Overall, vehicular access is good.

Public transportation is provided by Transit Intercity and provides access to major areas of Lincoln County. The nearest bus station is located at SE Sturdevant Rd & 10th, about one mile south of the subject. However, the primary mode of transportation in this area is the automobile.

The nearest municipal airport is located in Newport, 14.5 miles southwest from the property; travel time is about 22 minutes, depending on traffic conditions. A smaller, public airport, Toledo State Airport, is located just 5 minutes driving time from the subject in Toledo.

DEMA ND GE NERAT OR S

Major employers include Confederated Tribes of Siletz Indians, Samaritan Health Services, Lincoln County School District, Lincoln County, and OSU Hatfield Marine Science Center. These are located within 20 miles of the property, except for Samaritan Health Services, which is located in Corvallis about 47 miles away. These employers represent significant concentrations in the education, health, and government industries.

Coastal Oregon is a well-known tourist destination and is an additional significant demand generator for the county.

SURROUNDING AREA ANALYSIS 27

FOLEY LAND APPRAISAL

DEMOGRAPH IC S

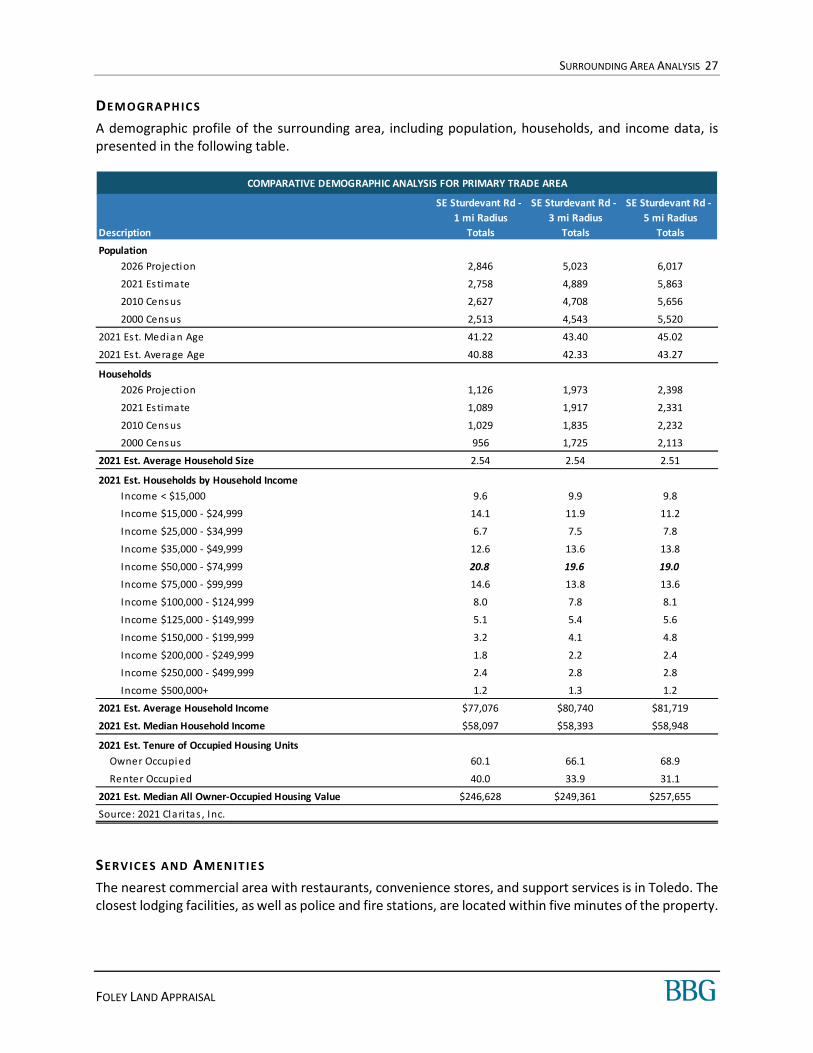

A demographic profile of the surrounding area, including population, households, and income data, is presented in the following table.

SERVICE S AND AMEN IT IE S

The nearest commercial area with restaurants, convenience stores, and support services is in Toledo. The closest lodging facilities, as well as police and fire stations, are located within five minutes of the property.

COMPARATIVE DEMOGRAPHIC ANALYSIS FOR PRIMARY TRADE AREA

SE Sturdevant Rd -

1 mi Radius

SE Sturdevant Rd -

3 mi Radius

SE Sturdevant Rd -

5 mi Radius

Description Totals Totals Totals

Population

2026 Projection 2,846 5,023 6,017

2021 Estimate 2,758 4,889 5,863

2010 Census 2,627 4,708 5,656

2000 Census 2,513 4,543 5,520

2021 Est. Median Age 41.22 43.40 45.02

2021 Est. Average Age 40.88 42.33 43.27

Households

2026 Projection 1,126 1,973 2,398

2021 Estimate 1,089 1,917 2,331

2010 Census 1,029 1,835 2,232

2000 Census 956 1,725 2,113

2021 Est. Average Household Size 2.54 2.54 2.51

2021 Est. Households by Household Income

Income < $15,000 9.6 9.9 9.8

Income $15,000 - $24,999 14.1 11.9 11.2

Income $25,000 - $34,999 6.7 7.5 7.8

Income $35,000 - $49,999 12.6 13.6 13.8

Income $50,000 - $74,999 20.8 19.6 19.0

Income $75,000 - $99,999 14.6 13.8 13.6

Income $100,000 - $124,999 8.0 7.8 8.1

Income $125,000 - $149,999 5.1 5.4 5.6

Income $150,000 - $199,999 3.2 4.1 4.8

Income $200,000 - $249,999 1.8 2.2 2.4

Income $250,000 - $499,999 2.4 2.8 2.8

Income $500,000+ 1.2 1.3 1.2

2021 Est. Average Household Income $77,076 $80,740 $81,719

2021 Est. Median Household Income $58,097 $58,393 $58,948

2021 Est. Tenure of Occupied Housing Units

Owner Occupi ed 60.1 66.1 68.9

Renter Occupi ed 40.0 33.9 31.1

2021 Est. Median All Owner-Occupied Housing Value $246,628 $249,361 $257,655

Source: 2021 Clari tas , Inc.

SURROUNDING AREA ANALYSIS 28

FOLEY LAND APPRAISAL

LAN D USE

In the immediate vicinity of the subject, land uses are mixed. There are residential, commercial, light industrial, and agricultural properties surrounding the subject. Other land use characteristics are summarized in the following table.

SURROUNDING AREA LAND USES

Character of Area Suburban to Semi-Rural

Predominant Age of Improvements 10-100 years

Predominant Quality and Condition Average

Approximate Percent Developed 25%

Infrastructure/Planning Average

SUBJECT’S IMMEDIATE SURROUNDINGS

North BPA Toledo Substation

South Toledo Elementary School

East Single-Family Residences

West Single-Family Residences

DEVELOPME NT ACTI VITY AND TREND S

During the last five years, development in Lincoln County has been predominantly of retail and multi-family uses and has included two Dollar General stores and three Class A apartment buildings. Most of these buildings are located along the coast, and none were built in or near Toledo. The pace of development has generally been intermittent over this time.

OUTLOOK A ND CONC LU SION S

The area is in the growth stage of its life cycle. Given the history of the area and the growth trends, it is anticipated that property values will increase in the near future.

In comparison to other areas in the region, the area is rated as follows:

SURROUNDING AREA ATTRIBUTE RATINGS

Highway Access Above Average

Demand Generators Average

Convenience to Support Services Average

Convenience to Public Transportation Average

Employment Stability Average

Police and Fire Protection Average

Property Compatibility Average

General Appearance of Properties Average

Appeal to Market Average

Price/Value Trend Average

SURROUNDING AREA ANALYSIS 29

FOLEY LAND APPRAISAL

NEIGHBORH OOD MAP

Subject

MARKET ANALYSIS 30

FOLEY LAND APPRAISAL

MARKET ANALYSIS

RESIDENTIAL ANALYSIS

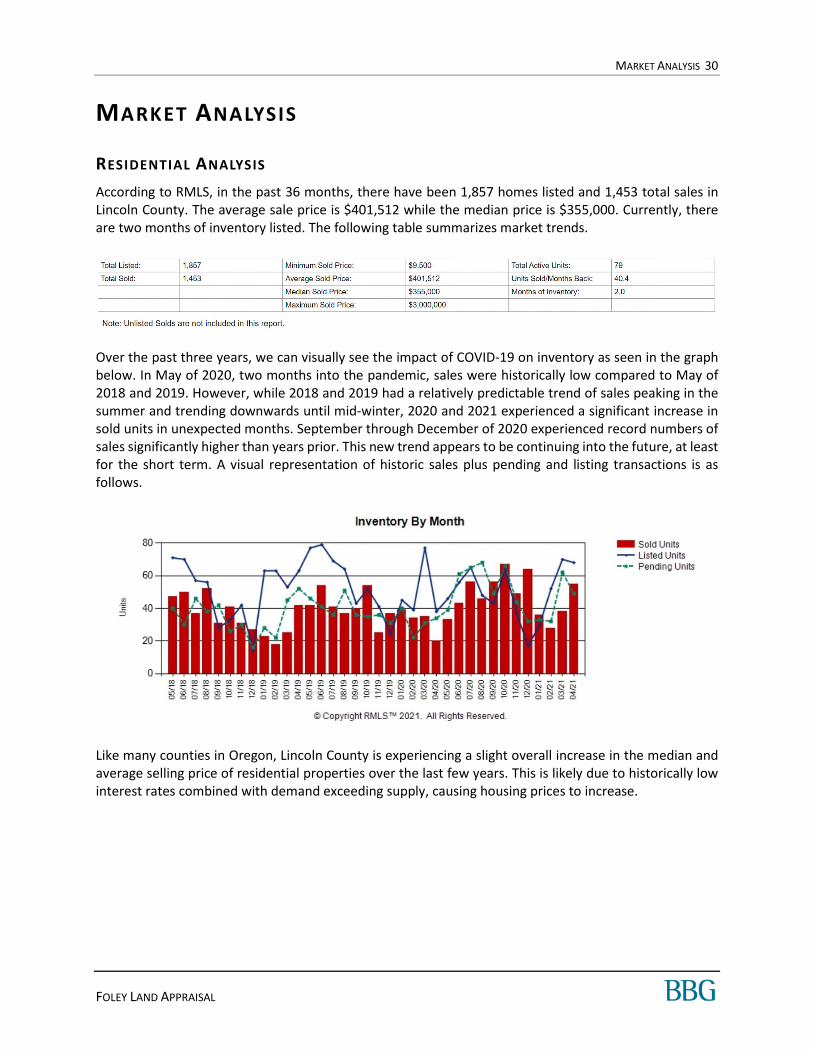

According to RMLS, in the past 36 months, there have been 1,857 homes listed and 1,453 total sales in Lincoln County. The average sale price is $401,512 while the median price is $355,000. Currently, there are two months of inventory listed. The following table summarizes market trends.

Over the past three years, we can visually see the impact of COVID-19 on inventory as seen in the graph below. In May of 2020, two months into the pandemic, sales were historically low compared to May of 2018 and 2019. However, while 2018 and 2019 had a relatively predictable trend of sales peaking in the summer and trending downwards until mid-winter, 2020 and 2021 experienced a significant increase in sold units in unexpected months. September through December of 2020 experienced record numbers of sales significantly higher than years prior. This new trend appears to be continuing into the future, at least for the short term. A visual representation of historic sales plus pending and listing transactions is as follows.

Like many counties in Oregon, Lincoln County is experiencing a slight overall increase in the median and average selling price of residential properties over the last few years. This is likely due to historically low interest rates combined with demand exceeding supply, causing housing prices to increase.

MARKET ANALYSIS 31

FOLEY LAND APPRAISAL

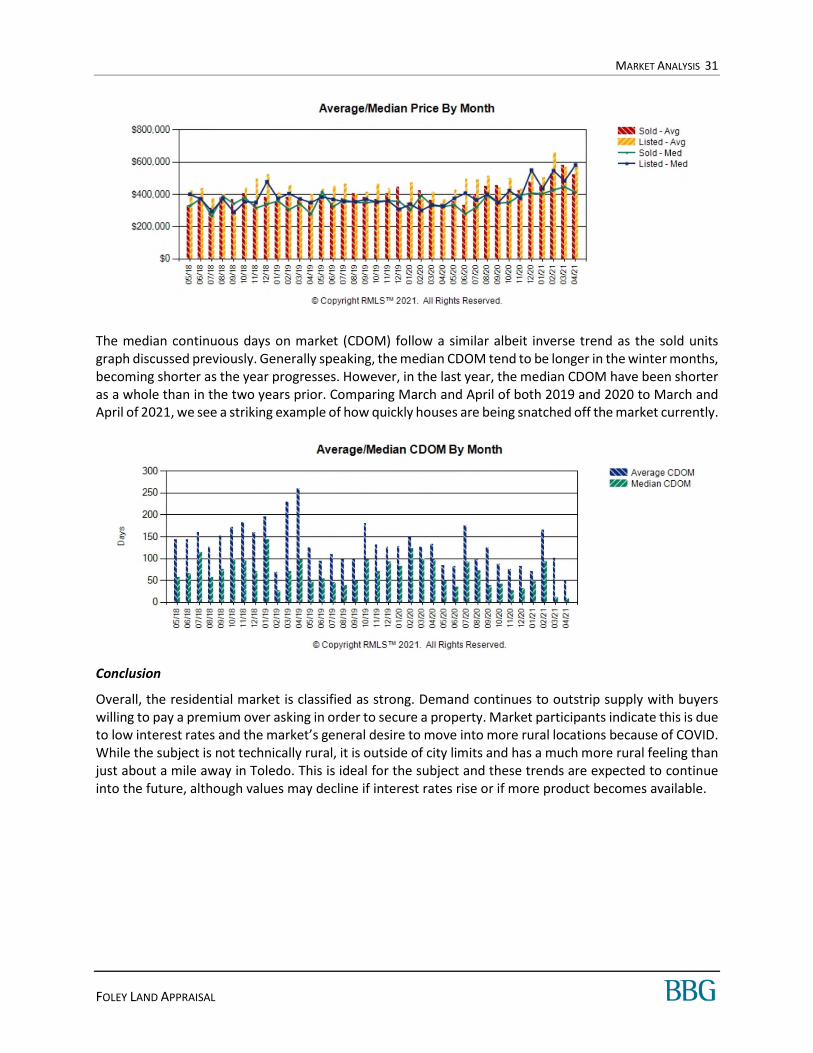

The median continuous days on market (CDOM) follow a similar albeit inverse trend as the sold units graph discussed previously. Generally speaking, the median CDOM tend to be longer in the winter months, becoming shorter as the year progresses. However, in the last year, the median CDOM have been shorter as a whole than in the two years prior. Comparing March and April of both 2019 and 2020 to March and April of 2021, we see a striking example of how quickly houses are being snatched off the market currently.

Conclusion

Overall, the residential market is classified as strong. Demand continues to outstrip supply with buyers willing to pay a premium over asking in order to secure a property. Market participants indicate this is due to low interest rates and the market’s general desire to move into more rural locations because of COVID. While the subject is not technically rural, it is outside of city limits and has a much more rural feeling than just about a mile away in Toledo. This is ideal for the subject and these trends are expected to continue into the future, although values may decline if interest rates rise or if more product becomes available.

SITE DESCRIPTION 32

FOLEY LAND APPRAISAL

S ITE DESCRIPTION

AERIAL MAP

INTRODUCTION

The description of the site is based upon our physical inspection of the property, information available from the client, and public sources. See the Data Sources Used Within This Appraisal table in the Scope of Work section for more detail.

SITE DESCRIPTION 33

FOLEY LAND APPRAISAL

GENERAL DESCRIPTION OVERVIEW

Location

Parcel Number A portion of R273276,

R508704

Legal Description

Site Area

Primary Site 241,322 s quare feet (5.5400 acres)

Configuration

Topography

Drainage

Utilities/Municipal Services

Floodplain Zone Map Date

Zone AE, X 41041C0531E October 18, 2019

Census Tract No.

Soil/Subsoil Conditions

Environmental Concerns

Land Use Restrictions

Hazards Nuisances

Enterprise Zone The s ubject i s not located within an opportuni ty zone.

We were not provided a current ti tle report to review. We are not aware of a ny

easements , encroachments , or res trictions that would adversely affect va lue. Our

valuation assumes no adverse impacts from easements , encroachments , or restrictions ,

a nd further a ssumes that the s ubject has clear and marketable ti tle.

No hazards or nuisances were obs erved.

An environmenta l as sess ment report was not provided for review, and during our

inspection, we did not obs erve any obvious s igns of contamination on or nea r the

s ubject. However, envi ronmenta l i ss ues are beyond our s cope of experti se. It i s

a ssumed tha t the property i s not advers ely affected by envi ronmenta l hazards .

The subject fronts the eas t s ide of SE Sturdeva nt Rd. and extends east to SE Chedes ter

Rd. in the UGB for the Ci ty of Toledo.

A portion of Lot 1100 a nd al l of Lot 1000 in the Northeast 1/4 of Section 17, Township 11S,

Range 10W, WM, Lincoln County, Oregon. A more deta i led legal des cription was not

a vai lable and the subject i s currently subject to a lot l ine adjustment.

Irregular

Sloping

Above street grade

Electrci ty i s avai lable to the s i te. Sewer and water a re approximately 500-600' to the

s outh of the s ubject (per Ci ty of Toledo).

Zone AE is a Specia l Flood Hazard Area (SFHA) where bas e flood eleva tions are

provided. AE Zones are now us ed on new format Flood Ins urance Rate Ma ps (FIRM)

instead of A1-A30 Zones . In communities tha t participate in the National Flood

Insurance Program (NFIP), ma ndatory flood ins urance purchase requirements apply to

this zone.

951400

We did not receive nor review a soi l report. However, we a ssume that the soi l 's load-

bearing capaci ty i s sufficient to support exis ting and/or proposed structure(s ). We did

not obs erve any evidence to the contra ry during our phys ica l inspection of the property.

Zone X (uns haded) is a Non-Specia l Flood Hazard Area (NSFHA) of minimal flood ha zard,

usual ly depicted on Flood Insura nce Rate Maps (FIRM) as above the 500-year flood level .

This is an area in a low to moderate risk flood zone that i s not in any immediate danger

from flooding caused by overflowing rivers or hard ra ins . In communities that participa te

in the Na tional Flood Ins urance Program (NFIP), flood insura nce is avai lable to al l

property owners and renters in this zone.

SITE DESCRIPTION 34

FOLEY LAND APPRAISAL

TOPOGRAPHY

The following graph indicates the general topography of the subject from north to south. The subject’s topography is gently sloping, from the highest elevation of 76 ft in the north to the lowest elevation of 19 ft in the south, towards SE Chedester Rd.

A topographic map of the property is below. The subject property line is estimated.

SITE DESCRIPTION 35

FOLEY LAND APPRAISAL

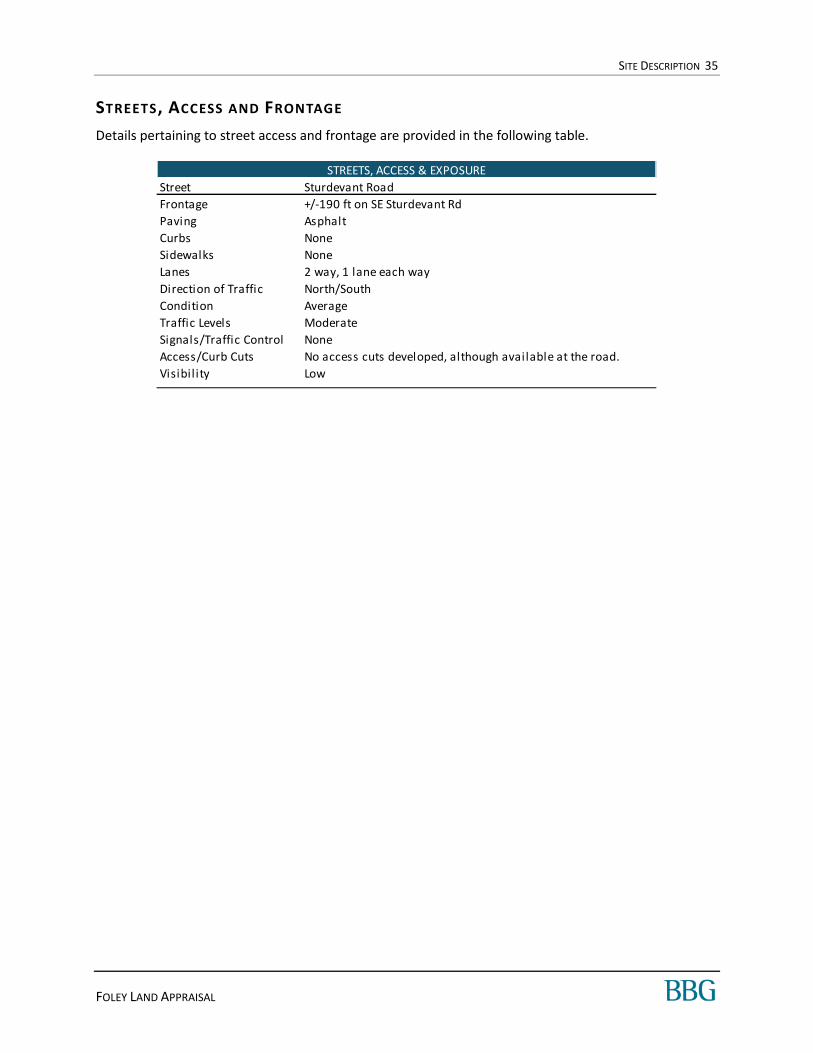

STREETS, ACCESS AND FRONTAGE

Details pertaining to street access and frontage are provided in the following table.

Street Sturdevant Road

Frontage +/-190 ft on SE Sturdevant Rd

Paving Asphalt

Curbs None

Sidewalks None

Lanes 2 way‚ 1 lane each way

Direction of Traffic North/South

Condition Average

Traffic Levels Moderate

Signals/Traffic Control None

Access/Curb Cuts No access cuts developed, although available at the road.

Visibil ity Low

STREETS, ACCESS & EXPOSURE

SITE DESCRIPTION 36

FOLEY LAND APPRAISAL

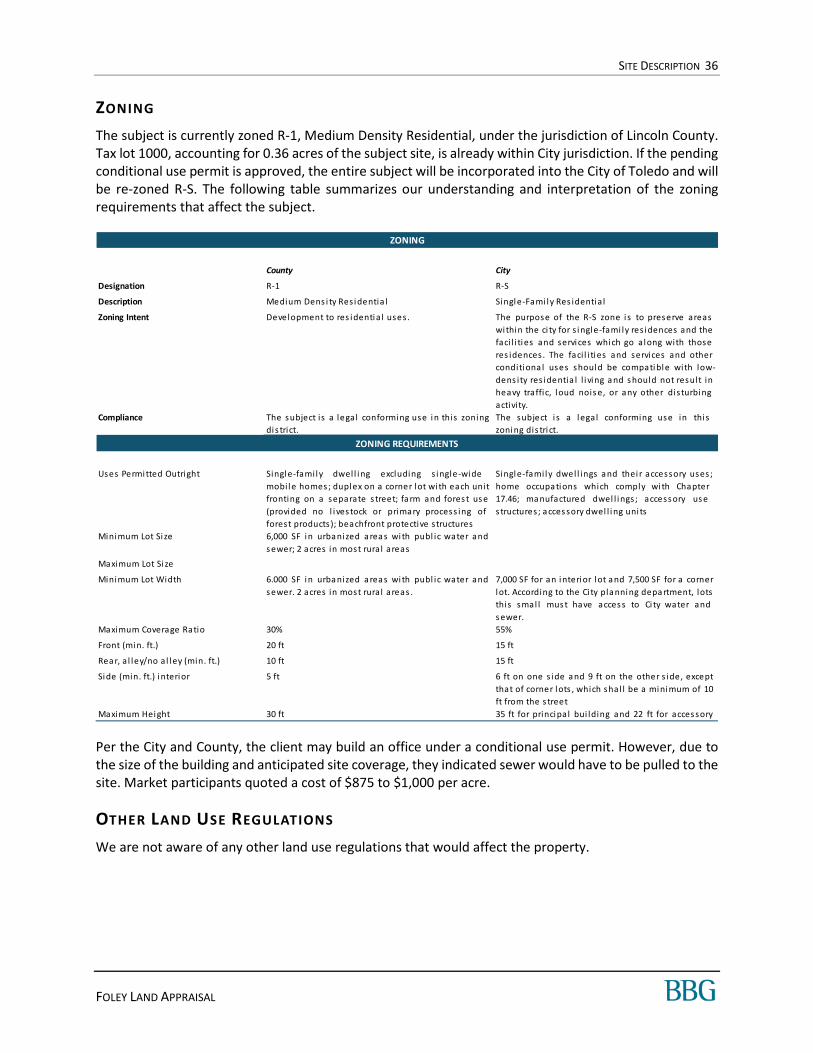

ZONING

The subject is currently zoned R-1, Medium Density Residential, under the jurisdiction of Lincoln County. Tax lot 1000, accounting for 0.36 acres of the subject site, is already within City jurisdiction. If the pending conditional use permit is approved, the entire subject will be incorporated into the City of Toledo and will be re-zoned R-S. The following table summarizes our understanding and interpretation of the zoning requirements that affect the subject.

Per the City and County, the client may build an office under a conditional use permit. However, due to the size of the building and anticipated site coverage, they indicated sewer would have to be pulled to the site. Market participants quoted a cost of $875 to $1,000 per acre.

OTHER LAND USE REGULATIONS

We are not aware of any other land use regulations that would affect the property.

County City

Designation R-1 R-S

Description Medium Dens i ty Res identia l Single-Fami ly Res identia l

Zoning Intent Development to res identia l uses. The purpose of the R-S zone is to preserve areas

within the ci ty for s ingle-fami ly res idences and the

faci l i ties and services which go along with those

res idences . The faci l i ties and services and other

conditiona l uses should be compatible with low-

dens ity res identia l l i ving a nd s hould not result in

heavy traffic, loud nois e, or any other disturbing

activity.

Compliance The subject is a legal conforming use in this zoning

dis trict.

The subject i s a legal conforming use in this

zoning dis tri ct.

Uses Permitted Outright Single-family dwel l ing excluding s ingle-wide

mobile homes ; duplex on a corner lot wi th each unit

fronting on a separate s treet; fa rm and fores t us e

(provided no l ives tock or primary process ing of

forest products); beachfront protective structures

Single-family dwel l ings a nd thei r accessory uses ;

home occupa tions which comply with Chapter

17.46; ma nufactured dwel l ings; access ory us e

s tructures; a cces sory dwel l ing uni ts

Minimum Lot Si ze 6,000 SF in urba nized a rea s wi th publ ic water and

s ewer; 2 acres in most rural areas

Maximum Lot Si ze

Minimum Lot Width 6.000 SF in urba nized a rea s wi th publ ic water and

s ewer. 2 acres in most rural areas .

7,000 SF for an interior lot a nd 7,500 SF for a corner

lot. According to the Ci ty pla nning depa rtment, lots

thi s smal l mus t have acces s to Ci ty water and

s ewer.

Maximum Coverage Ratio 30% 55%

Front (min. ft.) 20 ft 15 ft

Rea r, a l ley/no a l ley (min. ft.) 10 ft 15 ft

Side (min. ft.) interior 5 ft 6 ft on one s ide a nd 9 ft on the other s ide, except

that of corner lots , which shal l be a minimum of 10

ft from the s treet

Maximum Height 30 ft 35 ft for principal bui lding and 22 ft for acces sory

ZONING REQUIREMENTS

ZONING

SITE DESCRIPTION 37

FOLEY LAND APPRAISAL

CONCLUSION OF S ITE ANALYSIS

The subject site contains 241,322 square feet or 5.54 acres of Medium Density Residential zoned land. It is currently being incorporated in the City of Toledo and will be zoned R-S, Single Family Residential. The site is irregularly shaped and has sloping topography. The shape is not ideal but would not impact the development of the site. Topography is not steep and also would not impact development.

The south portion of the property is in a flood zone. However, this area would be developed to an access drive and/or would be in the required setbacks. The remainder of the property is outside of the flood hazard area.

The site size and zoning requirements would permit subdivision and the development of multiple residences. However, according to the associated planning departments, the size of the lots would be determined by zoning and the availability of sewer and water. Larger lots would only be approved if sewer was not brought to the site. Sewer is reported to be 500-600’ feet away.

Overall, the physical characteristics of the site and the availability of utilities result in functional utility suitable for a variety of uses including those permitted by zoning. We are not aware of any other restrictions on development.

SITE DESCRIPTION 38

FOLEY LAND APPRAISAL

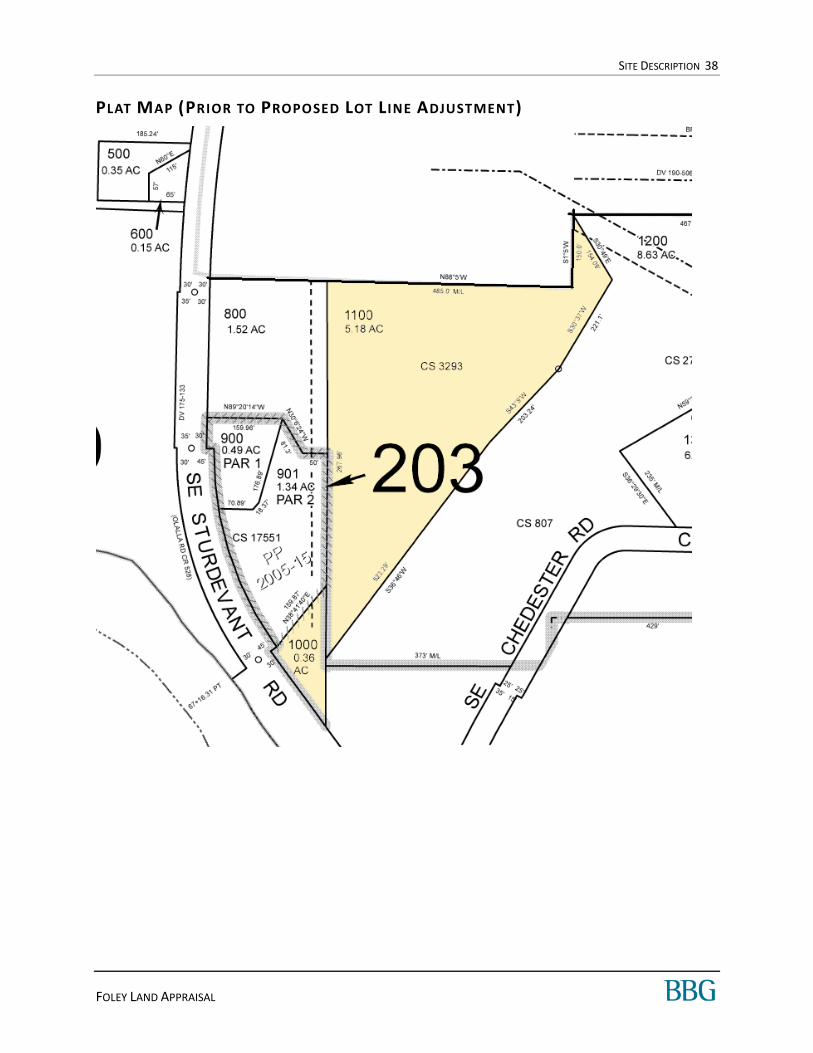

PLAT MAP (PRIOR TO PROPOSED LOT L INE ADJUSTMENT)

SITE DESCRIPTION 39

FOLEY LAND APPRAISAL

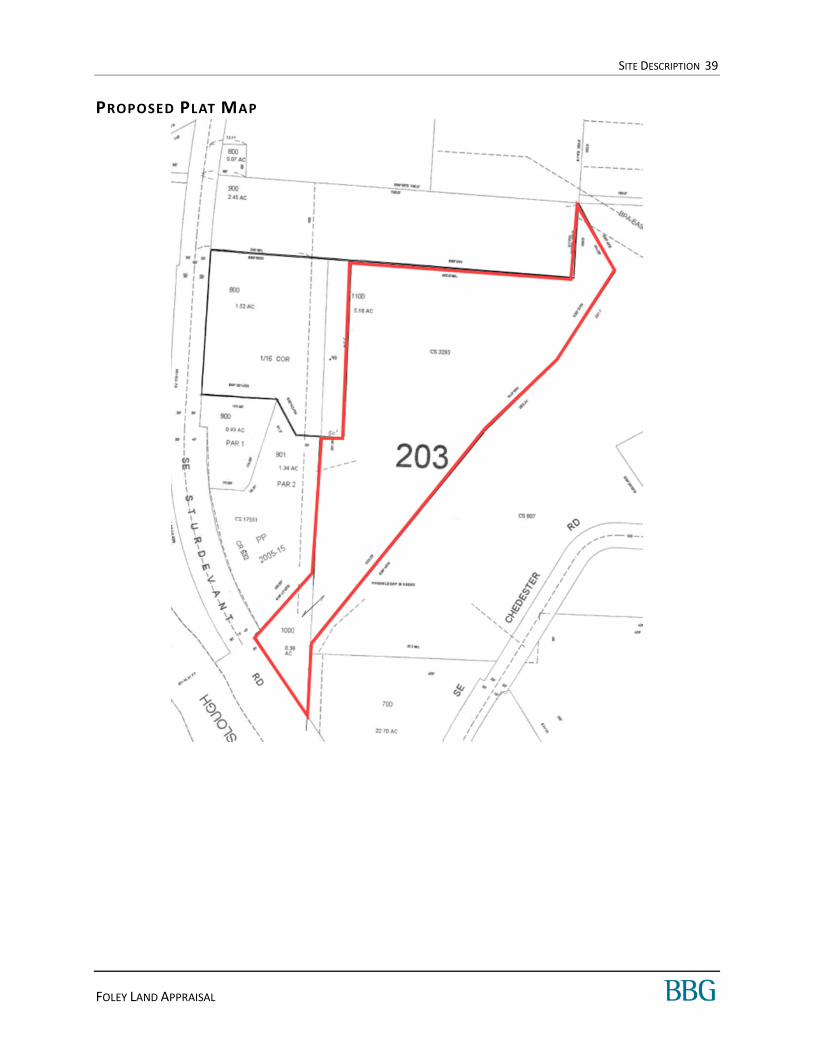

PROPOSED PLAT MAP

SITE DESCRIPTION 40

FOLEY LAND APPRAISAL

ZONING MAP – L INCOLN COUNTY

Subject’s approximate location

SITE DESCRIPTION 41

FOLEY LAND APPRAISAL

ZONING MAP – C ITY OF TOLEDO

SITE DESCRIPTION 42

FOLEY LAND APPRAISAL

FLOOD MAP

SITE DESCRIPTION 43

FOLEY LAND APPRAISAL

SUBJECT PHOTOS

PROPERTY TAX ANALYSIS 44

FOLEY LAND APPRAISAL

PROPERTY TAX ANALYSIS

State and local taxation in Oregon relies on income taxation at the state level and property taxes at the local level. The following is a summary of the Oregon property tax system.

Real estate taxes in the state and this jurisdiction represent ad valorem taxes, meaning a tax applied in proportion to assessed value.

Property taxes are collected locally to fund schools and governments in the area. The State does not receive any property tax revenue.

Property taxes are divided into school taxes and non-school taxes; non-school taxes raise revenue for City and County Governments, and educational service districts (community colleges, etc.).

In 1998, assessed value was rolled back to the 1996 real market value less 10%, and growth in assessed value was limited to 3% per year. Thus, property taxes are no longer directly tied in with real market value. There are some exceptions with respect to the 3% growth limit, such as new construction.

Property taxes may not exceed a limit of $5.00 per $1,000 of real market value for schools and $10.00 per $1,000 for non-schools

The limitation does apply to exempt bond levies that are approved by general election with at least half of the registered voters eligible to vote.

The tax year runs from July 1 through June 30, and the County Assessor's Office estimates value as of January 1 of each year. Property taxes are due and payable on November 15. A 3% discount is available if paid in full by November 15. A 2% discount is also obtainable if two-thirds of the amount is paid by this date. Another alternative is to make three equal (one-third) payments, on or before the 15th of November, February and May. Any balance owed begins to accrue interest after May 15, and counties initiate foreclosure if three years of taxes become delinquent.

Real estate taxes and assessments for the current tax year are shown in the following table.

Based on the concluded market value of the subject, the assessed value appears low. However, this is typical of the area and reassessment is not anticipated until development occurs.

Tax ID Land Improvements Total Mil lage Rate Assessed Value Real Estate Taxes

A portion of R273276 $99,470 $0 $99,470 15.67792208 $3,850 $60

R508704 $1,800 $0 $1,800 40.11538462 $780 $31

Totals $101,270 $0 $101,270 $4,630 $92

Assessor's Real Market Value Taxes and Assessments

REAL ESTATE TAXES 2020-2021

HIGHEST AND BEST USE 45

FOLEY LAND APPRAISAL

H IGHEST AND BEST USE

INTRODUCTION

The highest and best use is the reasonable, probable, and legal use of vacant land or an improved property that is physically possible, legally permissible, appropriately supported, financially feasible and that results in the highest value. These criteria are often considered sequentially. The tests of legal permissibility and physical possibility must be applied before the remaining tests of financial feasibility and maximal productivity. A financially feasible use is precluded if it is legally prohibited or physically impossible. If a reasonable possibility exists that one of the prior, unacceptable conditions can be changed, is it appropriate to proceed with the analysis with such an assumption.

H IGHEST AND BEST USE CRITERIA

The site’s highest and best use is analyzed both as vacant and as improved, and if improvements are proposed then an as proposed analysis is required. In all cases, the property’s highest and best use must meet four criteria: (1) legally permissible; (2) physically possible; (3) financially feasible; and (4) maximally productive.

H IGHEST AND BEST USE AS VACANT

LEGALLY PERMI SSI BLE

The subject is currently zoned R-1 Medium Density Residential which is a County Zone. This zone permits the development of residences on lots as small as 6,000 SF in urbanized areas with access to public utilities. Without utilities, the smallest parcel size is 2 acres. The property is in the UGB for the City of Toledo and the owner is currently in the process of annexing it. Upon annexation, the property will be zoned R-S, Single-Family Residential. The smallest residential lots permitted are 7,000 SF, assuming public utilities are at the site. Larger lots (as per review by the planning department) would be required if no sewer or water were available. In both jurisdictions and zones, government uses are permitted, although with a conditional use permit in some instances.

As has been mentioned in the Description section, the owner of the property has applied for annexation into the City of Toledo. He has expressed an intention to subdivide the property for development. As of the writing of this report, though, that is still a speculative idea only. There is no completed subdivision plat, no plat approvals from the City or the County. Subdivision would require those approvals, engineering, and additional survey and legal work.

While subdivision is likely legally permissible, the property’s legal status as of the effective date of this report is as a large lot with speculative potential.

A small portion of the property is in a flood zone, which cannot be developed with structures.

No other legal restrictions have been identified that would limit development of the property beyond the development standards stipulated by municipal code.

HIGHEST AND BEST USE 46

FOLEY LAND APPRAISAL

PHYSICA LLY POSSIBLE

The subject site contains 241,322 square feet or 5.54 acres of Medium Density Residential zoned land. It is currently being incorporated in the City of Toledo and will be zoned R-S, Single Family Residential. The site is irregularly shaped and has sloping topography. The shape is not ideal but would not impact the development of the site. Topography is not steep and also would not impact development.

The south portion of the property is in a flood zone. However, this area would be developed to an access drive and/or would be in the required setbacks. The remainder of the property is outside of the flood hazard area.

The site size and zoning requirements would permit subdivision and the development of multiple residences. However, according to the associated planning departments, the size of the lots would be determined by zoning and the availability of sewer and water. Larger lots would only be approved if sewer was not brought to the site. Sewer and water are reported to be 500-600’ feet away.

Overall, the physical characteristics of the site and the availability of utilities result in functional utility suitable for a variety of uses including those permitted by zoning. We are not aware of any other restrictions on development.

F INA NC IA LLY FEA SIBLE

The subject is not connected to public sewer, though public water is reportedly available in the street at the property corner. According to the planning department, sewer hookups are approximately 500-600’ feet away. The cost to extend, as reported by various market participants and sources is $875-$1,000 per foot. In the process of this appraisal we interviewed brokers and other market participants who indicated for similar properties, the cost to pull from significant distances is a barrier to most. Instead, they purchase parcels as an investment and/or on a speculative basis and wait until the City pays for extension or the parcels may be subdivided into larger lots with septic.

Sales in this report include parcels with no public utility access and others with public utilities in the street. Based on larger markets we have appraised in, we anticipated parcel value would be impacted by the availability and distance of public utilities. One participant stated the presence of public water and sewer in the street had a positive impact on value. Another stated they did not adjust their asking price, despite the availability of utilities to a parcel. We were unable to find any market data which supported an adjustment related to utility proximity. Considering these factors, speculative extension of the water and sewer line is not financially feasible.

As demonstrated in the Market Survey, residential demand has increased in the market over the past 12 months. Marketing times since January 2021 have dropped on average to less than 1 month. Currently there is approximately 1 month of inventory available. Despite this increased demand, we are not aware of any speculative development in the area. That strong demand for homes has not yet enticed subdivision approvals or development on any currently vacant acreage lots.

We anticipated zoning density would also impact value, but again were unable to locate any support for this factor. Instead, properties in or near designated communities, zoned for residential uses, are valued similarly by the market. However, when speaking with brokers, they stated higher values are associated with incorporated properties. To support this, we completed a survey of unincorporated, UGB, and incorporated (City or Planned Community) sales. We found incorporated properties sell for about 45% to

HIGHEST AND BEST USE 47

FOLEY LAND APPRAISAL

50% higher than unincorporated or UGB properties. Based on these factors, the annexation of the subject is considered ideal and financially feasible.

MAXI MA LLY PR ODUC TIV E

Based on the factors discussed under Financially Feasible, the annexation of the subject into the City of Toledo is maximally productive. Also retention of the site until utilities are extended by the City is also maximally productive. Immediate-term speculative subdivision or development of the property is not supported by the market.

In the course of the research for this appraisal, the appraisers identified a number of acreage lots with homes already constructed. Those were purchased by buyers who intended to immediately move in and use those homes. That is not the same as the subject, which has no home and will still require entitlements work prior to even the issuance of a building permit. The buyer of an existing home on acreage is not likely the same as the potential buyer for the subject. In other words, those properties do not share the subject’s highest and best use.

VALUATION PROCESS 48

FOLEY LAND APPRAISAL

VALUATION PROCESS

Valuation in the appraisal process generally involves three techniques, including the Cost Approach, Sales Comparison Approach and the Income Capitalization Approach.

These three valuation methods are defined in the following table:

VALUATION METHODS DEFINITION

Cost Approach In this approach, value is based on adding the contributing value of any improvements (after deductions for accrued depreciation) to the value of the land as if it were vacant based on its highest and best use. If the interest appraised is other than fee simple, additional adjustments may be necessary for non-realty interest and/or the impact of existing leases or contracts.1

Sales Comparison Approach In this approach, recent sales of similar properties in the marketplace are compared directly to the subject property. This comparison is typically accomplished by extracting “units of comparison”, for example, price per square foot, and then analyzing these units of comparison for differences between each comparable and the subject. The reliability of an indication found by this method depends on the quality of the comparable data found in the marketplace.

Income Capitalization Approach In this approach, a property is viewed through the eyes of a typical investor, whose primary objective is to earn a profit on the investment principally through the receipt of expected income generated from operations and the ultimate resale of the property at the end of a holding period.

VALUATION METHODS UTILIZED

This appraisal employs only the Sales Comparison Approach. Based on our analysis and knowledge of the subject property type and relevant investor and buyer profiles, it is our opinion that this approach would be considered necessary and applicable for market participants. Since no improvements exist on site, the Cost Approach is not relevant. The property generates no income and is not typically marketed, purchased or sold on the basis of anticipated lease income; thus, the Income Capitalization Approach was precluded.

The valuation process is concluded by analyzing each approach to value used in the appraisal. When more than one approach is used, each approach is judged based on its applicability, reliability, and the quantity and quality of its data. A final value opinion is chosen that either corresponds to one of the approaches to value, or is a correlation of all the approaches used in the appraisal.

LAND VALUATION 49

FOLEY LAND APPRAISAL

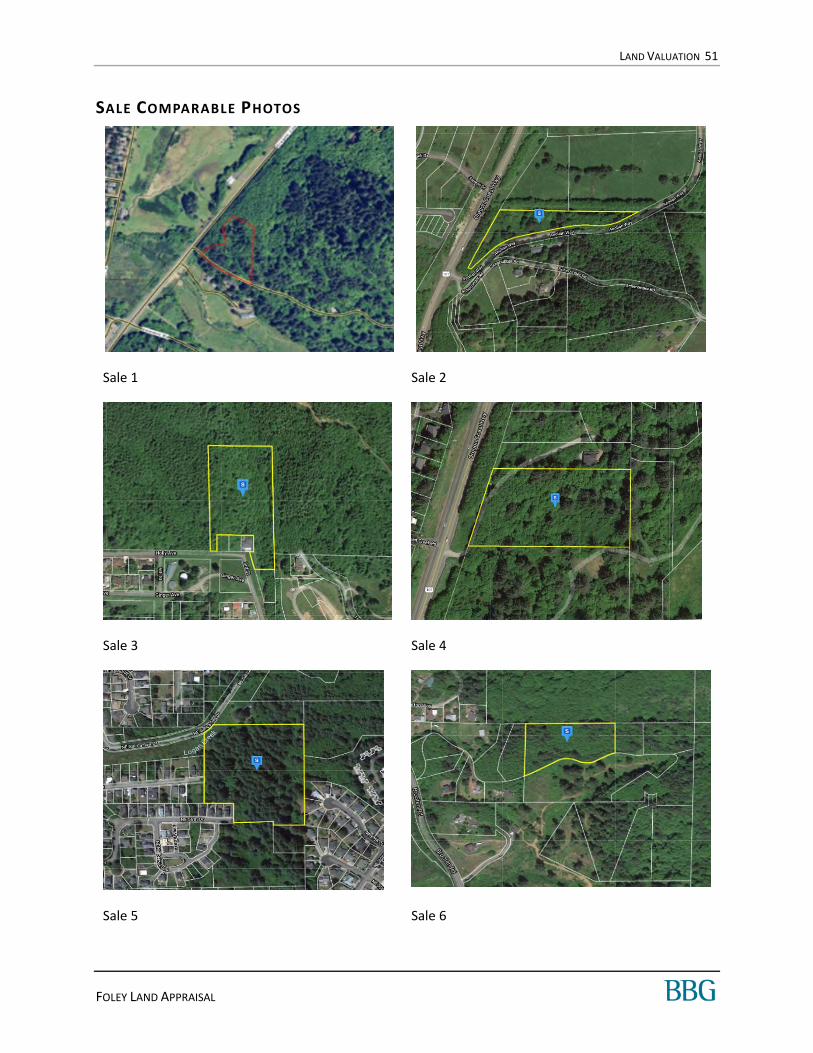

LAND VALUATION

METHODOLOGY