-megavision-discussion-materials

25

Megavisión Discussion Materials Strictly Private and Confidential July 2013 Citi Corporate and Investment Banking | Latin America TMT Investment Banking

-

Upload

free-lancer -

Category

Business

-

view

344 -

download

1

Transcript of -megavision-discussion-materials

Megavisión Discussion Materials

Strictly Private and Confidential

July 2013

Citi Corporate and Investment Banking | Latin America TMT Investment Banking

Table of Contents

1. Banchile Citi Latin America Qualifications 1

2. Chilean Macroeconomic Outlook 4

3. Chilean Advertising & TV Market Overview 6

4. Megavisión Overview 9

5. Appendix 15

1. Banchile Citi Latin America Qualifications

Citigroup Global Markets Inc. (“Citi”) and Banchile Citi Global Markets (together “Banchile Citi”) have a dedicated

team of experienced professionals with industry, product and regional knowledge to assist Sony Pictures in the

evaluation of strategic alternatives involving Megavisión S.A. (“Megavisión or “Mega”).

The Citi Investment Banking Team

TMT Investment Banking Latin America Investment Banking Banchile Citi

Ketan Mehta

Managing Director

Global Head of TMT M&A

+1 212 816-2877

Alberto Pandolfi

Managing Director

Head of Investment Banking LatAm

+1 212 816-6177

Jorge Muñoz

Managing Director

Head of Investment Banking Chile

+56 2 2380-8770

Federico Storani

Director

LatAm TMT

+1 212 816-5037

Alfonso Yanez

Director

+56 2 2380-8743

Francesco Piaggio

Associate

+1 212 816-9020

William Stanton

Associate

+56 2 2380-8516

Raniero Lopez

Analyst

+1 212 816-3945

Emilio Vergara

Analyst

+56 2 2380-8160

1

$9,679 $8,334

$7,543 $6,875

Celfin Santander Larraín Vial

Leadership in Local Debt

Capital Market1 2012, US$ mm

$787

$637

$328

$213

IM Trust Santander BBVA

Leadership in Bank & Debt Capital Markets Deals (Selected Debt Transactions)

Active M&A Presence (Selected M&A Transactions)

Local Equity Leadership (Selected Equity Transactions)

Advisor to TimerWarner

in its Acquisition of

Chilevisión

Undisclosed

2010

Advisor to Mitsubishi in

the merger of CMP and

CMH

US$924 mm

2010

Follow On

US$445 mm

2011

Leadership in Local Equity

Capital Market1 2003-2012, US$ mm

IPO

US$373 mm 2011

Corfo’s

Secondary Sale of 30% of

US$984 mm 2011

Follow On

US$130 mm 2011

&

Best Bond House 2011

Best M&A Transaction 2010

Corfo’s Secondary Sale of its stakes

in Essbio and Esval

US$564 mm 2011

Investment Banking Leadership

Banchile Citi Global Markets is the

Investment Banking & Capital Markets arm

of Banco de Chile and Citi in Chile

: Leading Investment Bank in Chile

Advisor to MS Infrastructure Partners on the sale of its 50%

stake in SAESA

Undisclosed 2011

Advisor to ING on

the sale of its life &

health insurance

business

Undisclosed

2009 & 2007

Corfo’s Secondary Sale of its stake in

US$88 mm 2012

Advisor to PreUnic

on its merger with

Undisclosed

2012

Advisor to Enagas on its

announced acquisition of

40% of GNL Quintero US352 mm

2012

Follow On

US$ 174 mm 2011

Follow On

US$ 505 mm

2012

Follow On

US$ 448 mm

2012

Advisor to

Christus Health on its

40% acquisition of

Red Salud UC

Confidential

2013

Local Bond

UF 1.7 mm

UF 3.3 mm

2012

Local Bond

UF 1.5 mm

2012

Best Investment Bank Chile 2012

Republic of Chile

Best Sovereign Bond

US$ 1,520mm - Dual

Currency

International Bond

Best Sovereign Issuer 2010

Best Investment Bank Chile 2013

Follow on

US$ 530 mm 2012-2013

Follow on US$ 500 mm

2013 (ongoing)

Follow on

US$ 5.690 mm 2013

Local Bond UF 1,5 mm

2012

Local Bond UF 7,8 mm

2012

Local Bond UF 2,5 mm

2013

Local Bond UF 6,0 mm

2013

Advisor to Duke Energy

on its acquisition of

US$ 415 mm

2012 Best Investment Bank Chile 2012

Source: (1) Based on Santiago Stock Exchange databases. League tables considers partial credit. Transactions recorded in US$.

Cross border M&A transactions

2

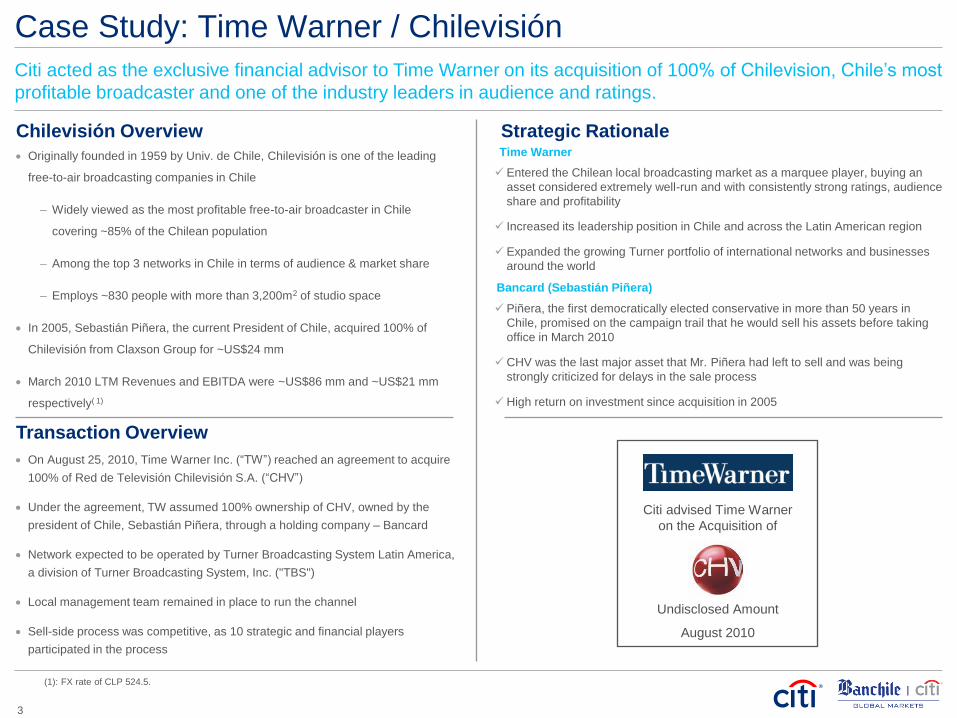

Originally founded in 1959 by Univ. de Chile, Chilevisión is one of the leading

free-to-air broadcasting companies in Chile

– Widely viewed as the most profitable free-to-air broadcaster in Chile

covering ~85% of the Chilean population

– Among the top 3 networks in Chile in terms of audience & market share

– Employs ~830 people with more than 3,200m2 of studio space

In 2005, Sebastián Piñera, the current President of Chile, acquired 100% of

Chilevisión from Claxson Group for ~US$24 mm

March 2010 LTM Revenues and EBITDA were ~US$86 mm and ~US$21 mm

respectively( 1)

Piñera, the first democratically elected conservative in more than 50 years in

Chile, promised on the campaign trail that he would sell his assets before taking

office in March 2010

CHV was the last major asset that Mr. Piñera had left to sell and was being

strongly criticized for delays in the sale process

High return on investment since acquisition in 2005

Case Study: Time Warner / Chilevisión

Citi advised Time Warner

on the Acquisition of

August 2010

Undisclosed Amount

Strategic Rationale

Transaction Overview

Chilevisión Overview

On August 25, 2010, Time Warner Inc. (“TW”) reached an agreement to acquire

100% of Red de Televisión Chilevisión S.A. (“CHV”)

Under the agreement, TW assumed 100% ownership of CHV, owned by the

president of Chile, Sebastián Piñera, through a holding company – Bancard

Network expected to be operated by Turner Broadcasting System Latin America,

a division of Turner Broadcasting System, Inc. ("TBS")

Local management team remained in place to run the channel

Sell-side process was competitive, as 10 strategic and financial players

participated in the process

Entered the Chilean local broadcasting market as a marquee player, buying an

asset considered extremely well-run and with consistently strong ratings, audience

share and profitability

Increased its leadership position in Chile and across the Latin American region

Expanded the growing Turner portfolio of international networks and businesses

around the world

Time Warner

Bancard (Sebastián Piñera)

Citi acted as the exclusive financial advisor to Time Warner on its acquisition of 100% of Chilevision, Chile’s most

profitable broadcaster and one of the industry leaders in audience and ratings.

(1): FX rate of CLP 524.5.

3

2. Chilean Macroeconomic Outlook

(1.0%)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

25.0 125.0 225.0

1.80

1.20

1.10

0.95

0.90

0.80

0.78

0.75

0.72

0.70

0.60

0.60

0.55

0.50

0.30 #15

#14

#13

#12

#11

#10

#9

#8

#7

#6

#5

#4

#3

#2

#1 NorwaySingapore

SwitzerlandSwedenFinlandCanada

AustraliaTaiwan

GermanyChile

New ZelandS. KoreaDenmark

NetherlandsUS

Chile’s highly attractive risk-return profile

Chile’s Key Macroeconomic Strengths

Chile is considered to have the most stable economy in Latin America, due to strong and consistent

macroeconomic fundamentals and policies. Overall, Chile offers a limited risk and high growth profile.

Risk/Return Profile

BlackRock’s Sovereign Risk Rating Index 5-Year CDS Spread and S&P Rating

Highest GDP per capita in Latin America

Only country in South America member of the OECD

Best Latin American sovereign risk rating (AA-)

Low tax on corporate profits (20%)

Ranked among the top 20 destinations for investment by multinational companies

for the next 2 years(1)

Source: Economist Intelligence Unit, Citi research, The BlackRock Sovereign Risk Index Report January 2013 , and FactSet.

(1) World Investment Report 2011 (United Nations).

(2) Average between Germany, France and UK.

BlackRock’s Sovereign Risk Index

ranks Chile in 10th place out of 44

countries, above countries like

Denmark or the U.S.

Lower Growth/

Higher Risk

Higher Growth /

Higher Risk

Higher Growth/

Lower Risk

Lower Growth/

Lower Risk 2013E

Gro

wth

5 Year CDS Spread – July 5, 2013

July 2013:

Chile: 107 bps

Average(2):54 bps

Spread: +53bps

0

50

100

150

200

250

300

350

Jul/08 Jul/09 Jul/10 Jul/11 Jul/12 Jul/13

Germany (AAA) Chile (AA-) France (AA+) UK (AAA)

4

10.3%

5.5%

3.8%3.0% 2.9%

2.5%

Argentina Brazil Mexico Chile Peru Colombia

Chile’s Macroeconomic Overview

16,870

12,190 11,600 11,210

7,9907,230

Chile Brazil Mexico Argentina Colombia Peru

Foreign Investment (’13 – ’17E, Total - US$ mm)

Nominal GDP per Capita (’13E, US$)

(1)

Inflation Forecasts (’12 – ’17E, Average Inflation – Local Currency)

Peru Chile Colombia Mexico Argentina Brazil

Peru Chile Colombia Mexico Argentina Brazil

Source: EIU data as of May 2013.

(1) IHS Global Insight based on official inflation rates from the Government of Argentina as of May 2013.

5.6%

4.7% 4.5%

3.7% 3.7%3.4%

Peru Chile Colombia Mexico Argentina Brazil

Real GDP Growth (’13 – ’18E, CAGR)

Peru Chile Colombia Mexico Argentina Brazil

342,634

135,000 121,500103,364

61,773 48,200

Brazil Mexico Chile Colombia Peru Argentina

Peru Chile Colombia Mexico Argentina Brazil

5

3. Chilean Advertising & TV Market Overview

436 491 500 527 587 645 659 706 736 771

876 982 998 982

1,143

1,303 1,334

1,436 1,523

1,628

2006 2007 2008 2009 2010 2011 2012 2013E2014E2015E

TV Print Outdoor Internet Others

Free to Air 89%

Pay TV 11%

TV 49%

Print 27%

Outdoor 9%

Internet 8%

Others 7%

Chile Advertising Market

Highlights

There is a high correlation between advertising and GDP growth

Chile’s advertising market is ahead of its Latam peers, but still lags developed

countries:

– Ad-spend per capita in Chile is ~US$78 per year vs. ~US$57(1) in its Latam

peers and ~US$513 in the USA

– Chilean advertising expenditure represented 0.5% of its 2012 GDP, still

substantially below developed countries like USA (1.0%), Japan (0.9%), UK

(0.8%), and Germany (0.7%)

TV remains the most relevant medium for advertising, representing 49% of total

advertising expenditures, with high concentration in FTA

Ad spending remained almost flat during crisis years, while TV spending

continued to grow

Advertising Expenditure by Medium (2012)

Chilean advertising market has grown in line with the country’s GDP, at a nominal rate of approximately 7 - 8%

per year in pre-crisis and post-crisis periods. The market is dominated by free-to-air (“FTA”) television, which

represents 44% of total ad-spend in 2012.

(2)

Total Advertising

US$ 1,334 mm

Sources: Historical Advertising Expenditure from Asociación Chilena de Agencias de Publicidad (“ACHAP”); Projected Advertising Expenditure from ZenithOptimedia, June 2013;

Advertising Expenditure by Country from ZenithOptimedia report of June 2013, and nominal GDP and population from EIU as of May 2013.

Note: Exchange rates as of June 28, 2013 (99.34 JPY/US$; 0.77 EUR/US$; 0.66 GBP/US$; 505.95 CLP/US$).

(1) Average for Chile’s Latam peers: Argentina, Brazil, Colombia, Mexico, Peru and Venezuela. (2) Includes Cinema and Radio.

Total TV

US$ 659 mm

Historical and Projected Advertising Expenditure (‘06 –’15E, US$ mm)

CAGR

06’ –08’

CAGR

10’ –12’

CAGR

12‘–15E’

4.3% 7.2% 5.1%

37.5% 29.1% 21.0%

5.5% 17.7% 4.1%

5.6% 5.0% 6.3%

7.1% 5.9% 5.4%

Projected

Advertising Expenditure by Country (2012)

% of GDP Per Capita (US$)

1.0%

0.9% 0.8%

0.7%

0.5%

0.7%

USA Japan UK Germany Chile

513

329 294 291

78 57

USA Japan UK Germany Chile Latam

Peers (1)

Latam

Peers (1)

(2)

6

Mon Tue Wed Thu Fri Sat Sun

6.00-17.59

18.00-19.59

20.00-24.30

00.30-26.59

Chile FTA TV Market Overview

Key Players Audience Share Evolution (% of Total)

There are 5 main players in the Chilean free to air TV space with total revenues of US$ 528 mm in 2012. Up until

2010, TVN and Canal 13 were dominant players specially in terms of revenue.

Overview of Chilean TV Demand

Revenue Share Evolution (% of Total)

Content Launch Ownership Aud. Share

(2012)

All segments, with expertise in Reality

Shows 1958

Grupo Luksic / Catholic University

27.0%

All segments, with great success in Morning

Shows and Soap Opera 1968 State Owned 23.6

All segments, with good rating in Soap Opera

1960 Time Warner 21.8

All segments, with focus in off prime time

1990 Grupo Bethia 20.2

Generalist programs, Films

1991 Remigio Angel

Gonzalez 7.4

0%

5%

10%

15%

20%

25%

30%

35%

40%

2005 2006 2007 2008 2009 2010 2011 2012

C13 TVN CHV Mega Red

0%

5%

10%

15%

20%

25%

30%

35%

40%

2005 2006 2007 2008 2009 2010 2011 2012

C13 TVN CHV Mega Red

TBC WS Off Prime

Prime

Off Prime

Off P

rim

e

Transition

Off P

rim

e

Source: Audience share Timelbope.

(1) % Revenue Share / % Rating Share.

Acquisition of C13 by Luksic

Acquisition of CHV by Time Warner

Power

Ratio(1)

1.2

1.2

1.0

0.6

0.4

Acquisition of Mega

by Bethia

7

Key Media Regulatory Considerations Topic Comments

Federal

Regulators

Undersecretary of Telecommunications (Subtel): acts on behalf of the Ministry of Transportation and Telecommunications

CNTV (“Consejo Nacional de Televisión”): reporting to the President through the General Secretary Ministry

Responsibilities / Mandates include:

– Promoting deregulation and market competition

– Granting concessions

– Executing day-to-day regulation/supervision of concessionaires and ensuring compliance; evaluating bids submitted for concessions and

opining on grant assignment and extension

Tribunal de la Libre Competencia (TDLC): antitrust agency; approves the assignment or transfer of television and telecommunications concessions

Concessions

Television Broadcasting licenses are awarded by service areas through a public bidding process coordinated by CNTV, on the basis of technical

and economic offers as overseen by the Subsecretaria de Telecomunicaciones (SUBTEL)

– Until 1992, concessions were granted for an indefinite term

– From 1992 onwards, concessions have a maximum 25-year term with a ROFR in the new bidding process; no separation between national

and regional licenses (maximum 1 license per area); license covers analogue TV services only

With the DTT platform migration underway, the regulatory framework is currently under discussion (see DTT migration below)

Convergence

(Triple-Play)

The General Law of Telecommunications, issued in 1982, allows concessionaires to provide complementary services through their networks and

thus, offer triple-play packages

Content

Restrictions

Minimum of 40% of programming must be locally produced

Minimum of 1 hour per week of cultural programming in prime time

Restrictions on

Advertising

Tobacco advertisements are required to display a clear and precise warning of damaging effects of its consumption

– Warning message should cover at least 50% of the total ad area and may not be broadcasted during non-adult programming

Foreign

Ownership Limits

There are no restrictions on foreign investment in Chile

Chilean law states that presidents, managers, directors and legal representatives of a terrestrial broadcasters must be Chilean

– Foreigners can hold Director positions, provided they do not constitute a majority

DTT Migration

The project is still in final discussion in Congress. Approval is expected for end of year. Four main issues are still being discussed

– “Retransmision consentida” - considers the payment from cable providers to FTA TV channels

– If the investment will be shared among TV channels

– Timeframes – likely to be 3 years to reach 85% coverage, and 5 years to reach 100% coverage

– Length of concessions – 20-year term for owned concessions, and 5-year term for concessions from third parties, with a ROFR in the new

bidding process

The ISDB-T standard (with MPEG4) was selected

8

4. Megavisión Overview

News 24%

Entertainment 20%

Talk Shows 16%

Movies 12%

Soap Opera 11%

Series 11%

Other 6%

27%

24%

22%

20%

7%

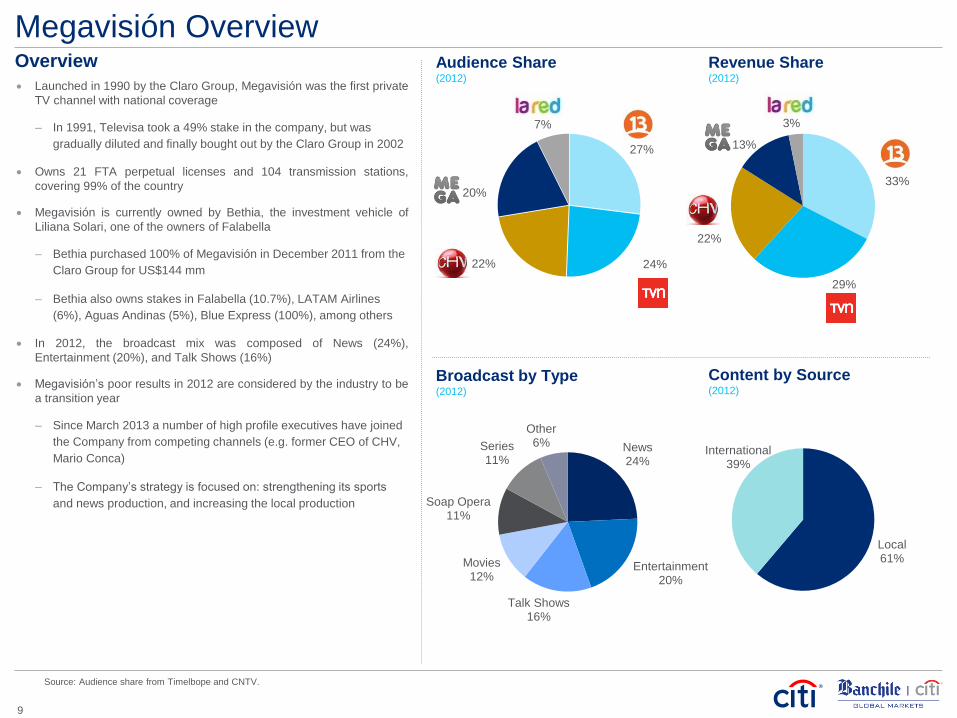

Megavisión Overview

Launched in 1990 by the Claro Group, Megavisión was the first private

TV channel with national coverage

– In 1991, Televisa took a 49% stake in the company, but was

gradually diluted and finally bought out by the Claro Group in 2002

Owns 21 FTA perpetual licenses and 104 transmission stations,

covering 99% of the country

Megavisión is currently owned by Bethia, the investment vehicle of

Liliana Solari, one of the owners of Falabella

– Bethia purchased 100% of Megavisión in December 2011 from the

Claro Group for US$144 mm

– Bethia also owns stakes in Falabella (10.7%), LATAM Airlines

(6%), Aguas Andinas (5%), Blue Express (100%), among others

In 2012, the broadcast mix was composed of News (24%),

Entertainment (20%), and Talk Shows (16%)

Megavisión’s poor results in 2012 are considered by the industry to be

a transition year

– Since March 2013 a number of high profile executives have joined

the Company from competing channels (e.g. former CEO of CHV,

Mario Conca)

– The Company’s strategy is focused on: strengthening its sports

and news production, and increasing the local production

Audience Share (2012)

Source: Audience share from Timelbope and CNTV.

Broadcast by Type (2012)

Revenue Share (2012)

Local 61%

International 39%

Content by Source (2012)

33%

29%

22%

13%

3%

Overview

9

Bethia S.A. (“Grupo Bethia” or “Bethia”) is the investment vehicle of Liliana Solari,

and owns 10.7% of S.A.C.I. Falabella (“Falabella”) shares

Falabella has a market capitalization of ~US$25 bn, making it Bethia’s main asset

Falabella has presence in Chile, Colombia, Peru, Argentina and Brazil with

different business lines (department stores, financial services, home

improvement, supermarkets, and real estate):

Other Investments of Grupo Bethia include:

– Agribusiness

– Transport

– Telecom

– Equestrian

– Real estate

– Wine

– Healthcare

– Potable water

Mega represents less than 5% of Grupo Bethia’s total assets

Business Unit Revenues (LTM (1) in US$ bn) Presence

Department Stores 4.5

Home Improvement 5.4

Supermarkets 1.9

Financial Services 6.0

Real Estate n.a.

Bethia Group Overview

Source: Grupo Bethia web page, Falabella’s Corporate Presentation of June 2013, Superintendencia de Valores y Seguros de Chile, and Bloomberg.

(1) LTM as of March 2013.

(2) Citi estimates considering Mega’s firm value the same as when acquired by Bethia.

(3) Exchange rate 519 CLP/US$.

(2)

Transaction Valuation

Transaction Overview

In December 2011, Bethia agreed to acquire 100% of Megavisión from

CIECSA, a subsidiary of Cristalerías de Chile and controlled by the Claro

Group

– Bethia paid US$144 mm plus cash available at the moment of the

purchase

– Transaction included the Megavisión channel along with the children's

channel “ETC…TV” and the radio station “Candela”

– Cristalerías de Chile reported a profit of US$59 mm from the sale

With the purchase of Megavisión, Bethia completed its objective of entering the

Chilean TV market. Previously, Bethia had actively participated in the sale

process of both Chilevisión and Canal 13, which were finally sold to Time

Warner and the Luksic Group, respectively

Case Study: Bethia’s Acquisition of Megavisión

Transaction Valuation US$ mm(3)

Purchase Price $169.6

% Acquired 100.0

Implied Equity Value 169.6

(+) Debt 0.0

(+) Minority Interest 0.2

(-) IUCS 0.0

(-) Cash (26.1)

Implied Firm Value $143.7

EBITDA 2011 17.1

Net Income 2011 10.9

Transaction Multiples

FV / EBITDA 2011 8.4x

Equity Value / Net Income 2011 15.5x

10

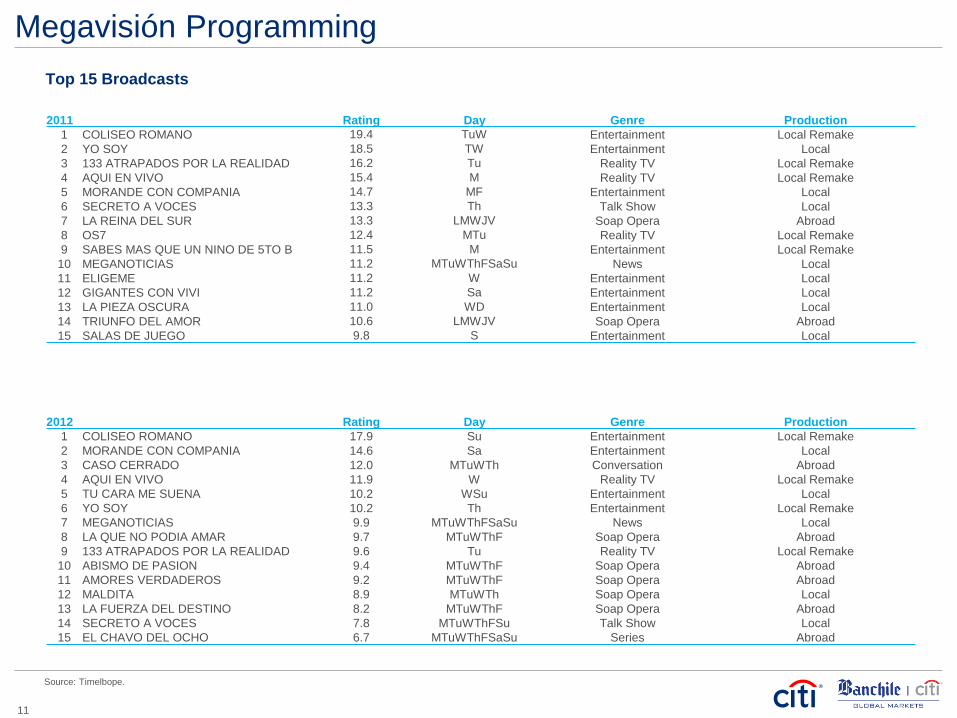

Megavisión Programming

Top 15 Broadcasts

2011 Rating Day Genre Production

1 COLISEO ROMANO 19.4 TuW Entertainment Local Remake

2 YO SOY 18.5 TW Entertainment Local

3 133 ATRAPADOS POR LA REALIDAD 16.2 Tu Reality TV Local Remake

4 AQUI EN VIVO 15.4 M Reality TV Local Remake

5 MORANDE CON COMPANIA 14.7 MF Entertainment Local

6 SECRETO A VOCES 13.3 Th Talk Show Local

7 LA REINA DEL SUR 13.3 LMWJV Soap Opera Abroad

8 OS7 12.4 MTu Reality TV Local Remake

9 SABES MAS QUE UN NINO DE 5TO B 11.5 M Entertainment Local Remake

10 MEGANOTICIAS 11.2 MTuWThFSaSu News Local

11 ELIGEME 11.2 W Entertainment Local

12 GIGANTES CON VIVI 11.2 Sa Entertainment Local

13 LA PIEZA OSCURA 11.0 WD Entertainment Local

14 TRIUNFO DEL AMOR 10.6 LMWJV Soap Opera Abroad

15 SALAS DE JUEGO 9.8 S Entertainment Local

2012 Rating Day Genre Production

1 COLISEO ROMANO 17.9 Su Entertainment Local Remake

2 MORANDE CON COMPANIA 14.6 Sa Entertainment Local

3 CASO CERRADO 12.0 MTuWTh Conversation Abroad

4 AQUI EN VIVO 11.9 W Reality TV Local Remake

5 TU CARA ME SUENA 10.2 WSu Entertainment Local

6 YO SOY 10.2 Th Entertainment Local Remake

7 MEGANOTICIAS 9.9 MTuWThFSaSu News Local

8 LA QUE NO PODIA AMAR 9.7 MTuWThF Soap Opera Abroad

9 133 ATRAPADOS POR LA REALIDAD 9.6 Tu Reality TV Local Remake

10 ABISMO DE PASION 9.4 MTuWThF Soap Opera Abroad

11 AMORES VERDADEROS 9.2 MTuWThF Soap Opera Abroad

12 MALDITA 8.9 MTuWTh Soap Opera Local

13 LA FUERZA DEL DESTINO 8.2 MTuWThF Soap Opera Abroad

14 SECRETO A VOCES 7.8 MTuWThFSu Talk Show Local

15 EL CHAVO DEL OCHO 6.7 MTuWThFSaSu Series Abroad

Source: Timelbope.

11

10

13 12

18 18

0 -3

0

15% 17% 16%

20% 21%

0%

-19%

-1%

2007 2008 2009 2010 2011 2012 Mar/12 Mar/13

Megavisión Financial Overview

Source: SVS and Company Filings.

Note: All figures converted to USD at an FX rate of CLP / USD of 505. In 2010 Megavisión changed accounting standards from Chilean GAAP to IFRS.

(1) Prime time defined as from 20:00 to 00:30 hrs, off prime from 06:00 to 20:00 hrs.

6

10 10

13 11

-9

-6

-2

9%

14% 14% 15% 13%

-13%

-45%

-11%

2007 2008 2009 2010 2011 2012 Mar/12 Mar/13

Megavisión has seen a drop in its revenues and net income in 2012 with respect

to 2011

– This is explained by a drop in average home ratings from 7.7 to 6.6 points

that impacted revenues (decrease of 19%) and an increase in costs due to

a more expensive programming lineup (increase of 12%)

The drop in ratings was experienced both in prime(1) (from 9.9 to 8.1 points) and

off prime(1) (from 6.8 to 6.0 points)

– The drop in ratings is explained in large part by the market share captured

by Canal 13 in prime time and the underperformance of Megavisión

programming including the late night soap opera “Maldita”

In the second quarter of 2013, Megavisión has had success with third party

programming such as “Pablo Escobar” and “El Barco”, which should translate to

an increase in revenues in upcoming quarters

Megavisión recently purchased the transmission rights for football matches of the

Chilean national team for US$106 mm for the 2014 - 2018 world cup campaign,

as well as the transmission rights for the Champions League 2014 – 2017

Overview Revenues and Rating (US$ mm and points of rating)

Net Income and Net Income Margin (US$ mm and %)

EBITDA and EBITDA Margin (US$ mm and %)

68 75 74

90 84

68

13 17

9.0 9.3 8.6 8.3 7.7

6.6

2007 2008 2009 2010 2011 2012 Mar/12 Mar/13

7.5 8.1 8.6 10.9 10.9 10.3

Revenues / Rating (US$ mm per Point of Rating)

Gross margin dropped from 32%

in 2011 to 6% in 2012

12

25% 23% 23% 21%

8%

Canal 13 TVN Mega CHV Red

Compared to its peers, Megavisión has a relatively larger positioning in Off Prime and C3-D segments.

28% 26%

22%

18%

6%

Canal 13 TVN CHV Mega Red

Audience Share by Time Slot and Socio - Economic Segment

Positioning by Time Slot Prime Audience Share %

Off- Prime Audience Share %

32%

24%

20%

16%

8%

Canal 13 TVN CHV Mega Red

26% 23% 23% 21%

7%

Canal 13 TVN CHV Mega Red

Positioning by Socio-Economic Segment ABC1 – C2 (Higher Segment) Audience Share %

C3-D (Lower Segment) Audience Share %

Source: Audience share from Timelbope.

13

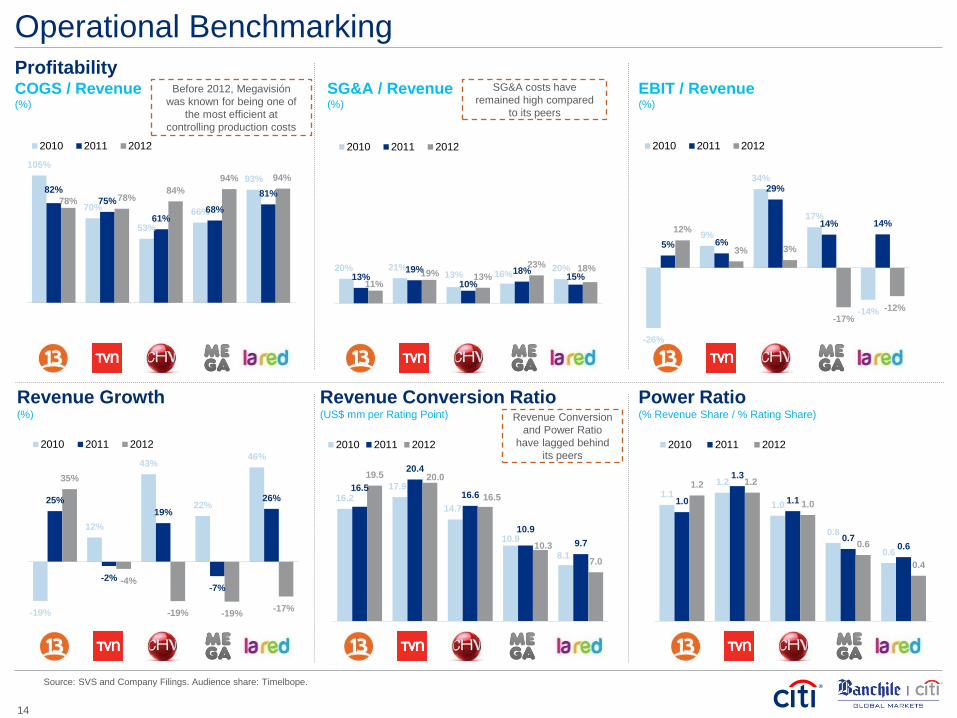

-19%

12%

43%

22%

46%

25%

-2%

19%

-7%

26%

35%

-4%

-19% -19% -17%

2010 2011 2012

Operational Benchmarking Profitability

Revenue Conversion Ratio (US$ mm per Rating Point)

Power Ratio (% Revenue Share / % Rating Share)

16.2

17.9

14.7

10.9

8.1

16.5

20.4

16.6

10.9

9.7

19.5 20.0

16.5

10.3

7.0

2010 2011 2012

1.1

1.2

1.0

0.8

0.6

1.0

1.3

1.1

0.7 0.6

1.2 1.2

1.0

0.6

0.4

2010 2011 2012

COGS / Revenue (%)

SG&A / Revenue (%)

EBIT / Revenue (%)

105%

70%

53%

66%

93% 82%

75%

61% 68%

81% 78% 78%

84%

94% 94%

2010 2011 2012

20% 21% 13% 16%

20% 13%

19%

10%

18% 15%

11% 19% 13%

23% 18%

2010 2011 2012

-26%

9%

34%

17%

-14%

5% 6%

29%

14% 14% 12%

3% 3%

-17%

-12%

2010 2011 2012

Source: SVS and Company Filings. Audience share: Timelbope.

Before 2012, Megavisión

was known for being one of

the most efficient at

controlling production costs

SG&A costs have

remained high compared

to its peers

Revenue Conversion

and Power Ratio

have lagged behind

its peers

Revenue Growth (%)

14

5. Appendix

Latin America Media Comparables

Note: Stock prices as of July 2, 2012. Multiples calculated in local currency.

Source: Company financials and Wall Street research.

15

Stock Market Firm FV / Revenues FV / EBITDA P/E CAGR '12 - '15E LTM EBITDA

(US$ in mm, except stock pr.) Price Cap. Value 2013E 2014E 2013E 2014E 2013E 2014E Revenue EBITDA Margin

Televisa $4.28 $12,203 $13,366 2.5x 2.3x 6.4x 6.1x 18.5x 16.8x 5.2% 2.2% 40.8%

TV Azteca 0.66 1,961 2,060 2.1 1.9 5.6 5.3 NA NA 1.6 0.6 34.7

Median -- -- -- 2.3x 2.1x 6.0x 5.7x 18.5x 16.8x 3.4% 1.4% 37.8%

Mean -- -- -- 2.3 2.1 6.0 5.7 18.5 16.8 3.4 1.4 37.8

5.1x

10.5x

16.3x

13.8x

10.9x

0.0x

7.0x

8.4x

Latin America Media Precedents

NA

Median: 10.5x

Oct-02 Oct-04 Dec-06 Oct-07 Mar-10 Aug-10 Aug-10 Dec-11

CIECSA Bancard

Inversiones

Prisa TBS Time Warner Luksic Group Time Warner Bethia

Megavisión Chilevisión Ibero-american Claxson HBO LatAm Canal 13 Chilevisión Megavisión

$29 $34 $102 $234 $1,033 $55 $155 $144

Acquiror:

Target:

Value (US$ mm):

Note: Multiple = FV / LTM EBITDA, based on public information.

Source: SDC, Bloomberg and Citi Deal Intelligence.

(1) EBITDA of Canal 13 was negative at the time of purchase, as a reference, the FV / LTM Sales as of June 2010 was 0.8x.

(1)

FV / LTM EBITDA

~

~

16

4,721 4,658

3,918

2,431 2,237

Santander Celfin MerrillLynch

BBVA

9,679

8,267 7,543

6,875

5,150 4,485

3,988

3,025 2,519

1,923

16.1%

13.7% 12.5%

11.4%

8.6% 7.5%

6.6% 5.0% 4.2% 3.2%

Celfin Santander Larraín Vial Merrill Lynch IMTrust JP Morgan Deutsche BBVA Credit Suisse

1,602 1,590

1,275 1,121 1,054

IMTrust Santander Larraín Vial Celfin

3,635 3,374

3,056

2,575 2,251

Larraín Vial Celfin IMTrust Merrill Lynch

Follow-On (1)

US$ mm

IPO (1)

US$ mm

Block Trades (1)

US$ mm

: #1 Chilean Equity House of the Decade

# Deals 13 7 14 2 4 7 6 5 12 6 25 19 21 10 5

Total Issuances 2003 – 2012 YTD – Full Credit (1)

US$ mm

# Deals 38 41 17 46 8 21 7 5 6 2

Source: Banchile Citi estimates based on public information from SVS (Chilean SEC), Santiago Stock Exchange, and companies filings.

(1) Includes transactions over US$ 20 million with a known advisor. Excludes transactions with holding companies, debt capitalization, and others that could be considered

as part of a M&A process.

#1

#1 #2

After capital markets re-opening in Chile, over US$25 bn have been placed in ECM, including IPOs, Follow-Ons

and Block Trades.

#2

17

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our

own environmental footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position

Statement, the first US financial institution to do so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology,

and other carbon-emission reduction activities; (c) committing to an absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of

carbon neutral power for our operations over the last three years; (e) establishing in 2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of

electric power projects; (f) producing equity research related to climate issues that helps to inform investors on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the

issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

efficiency, renewable energy and mitigation

© 2013 Citigroup Global Markets Inc. Member SIPC. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by

you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice

based on your particular circumstances from an independent tax advisor.

In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering into a derivatives

transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or

purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the

information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting

characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b)

there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to

such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with

respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also

request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are

not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or

may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our

affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or

negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in

research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and

research personnel to specifically prescribed circumstances.

![[MATERIALS Enabling DISCUSSION] Electrification](https://static.fdocuments.in/doc/165x107/61bd023461276e740b0e6ad3/materials-enabling-discussion-electrification.jpg)