© K.Cuthbertson and D.Nitzsche 1 Version 1/9/2001 FINANCIAL ENGINEERING: DERIVATIVES AND RISK...

24

© K.Cuthbertson and D.Nitzsche 1 Version 1/9/2001 FINANCIAL ENGINEERING: DERIVATIVES AND RISK MANAGEMENT (J. Wiley, 2001) K. Cuthbertson and D. Nitzsche LECTURE Foreign Currency Options

-

date post

21-Dec-2015 -

Category

Documents

-

view

218 -

download

0

Transcript of © K.Cuthbertson and D.Nitzsche 1 Version 1/9/2001 FINANCIAL ENGINEERING: DERIVATIVES AND RISK...

© K.Cuthbertson and D.Nitzsche1

Version 1/9/2001

FINANCIAL ENGINEERING:DERIVATIVES AND RISK MANAGEMENT(J. Wiley, 2001)

K. Cuthbertson and D. Nitzsche

LECTURE

Foreign Currency Options

© K.Cuthbertson and D.Nitzsche2

Contracts and Payoffs

Hedging Foreign Currency Receiptsusing Forwards, Options and Futures

Pricing Foreign Currency Options

Topics

© K.Cuthbertson and D.Nitzsche3

Contracts and Payoffs

© K.Cuthbertson and D.Nitzsche4

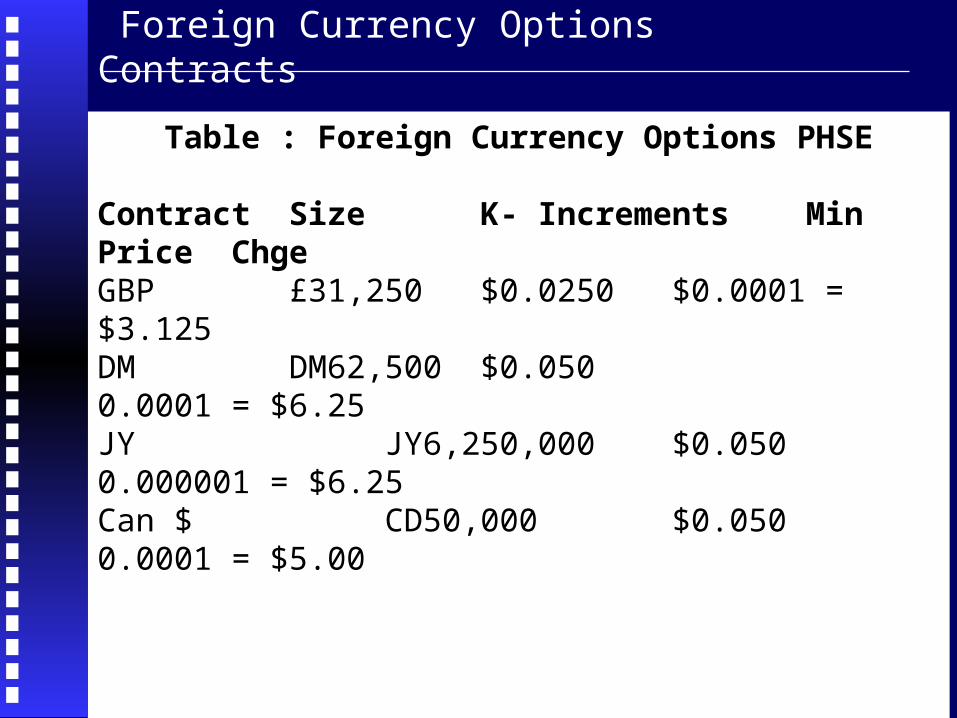

Foreign Currency Options Contracts

Table : Foreign Currency Options PHSE

Contract Size K- Increments Min Price Chge

GBP £31,250 $0.0250 $0.0001 = $3.125

DM DM62,500 $0.050 0.0001 = $6.25

JY JY6,250,000 $0.050 0.000001 = $6.25

Can $ CD50,000 $0.050 0.0001 = $5.00Hold, TVS0 = $2m in diversified equity portfolio and ‘

© K.Cuthbertson and D.Nitzsche5

Fig11.2:Long , Foreign Currency Call

ST

Profit

Strike price K = $140

6

C = 4

$150$144K = $1400

0+1

© K.Cuthbertson and D.Nitzsche6

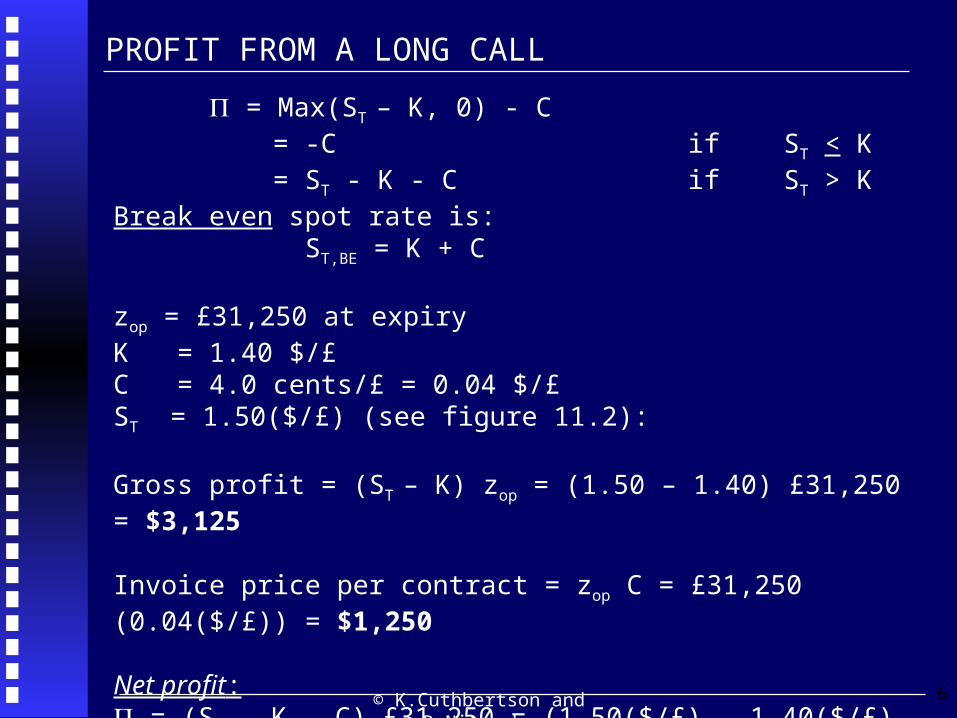

= Max(ST – K, 0) - C = -C if ST < K = ST - K - C if ST > K

Break even spot rate is:ST,BE = K + C

zop = £31,250 at expiryK = 1.40 $/£ C = 4.0 cents/£ = 0.04 $/£ST = 1.50($/£) (see figure 11.2): Gross profit = (ST – K) zop = (1.50 – 1.40) £31,250 = $3,125

Invoice price per contract = zop C = £31,250 (0.04($/£)) = $1,250

Net profit: = (ST - K – C) £31,250 = (1.50($/£) - 1.40($/£) - 0.04($/£)) £31,250 = (0.06($/£))(£31,250) = $1,875

PROFIT FROM A LONG CALL

© K.Cuthbertson and D.Nitzsche7

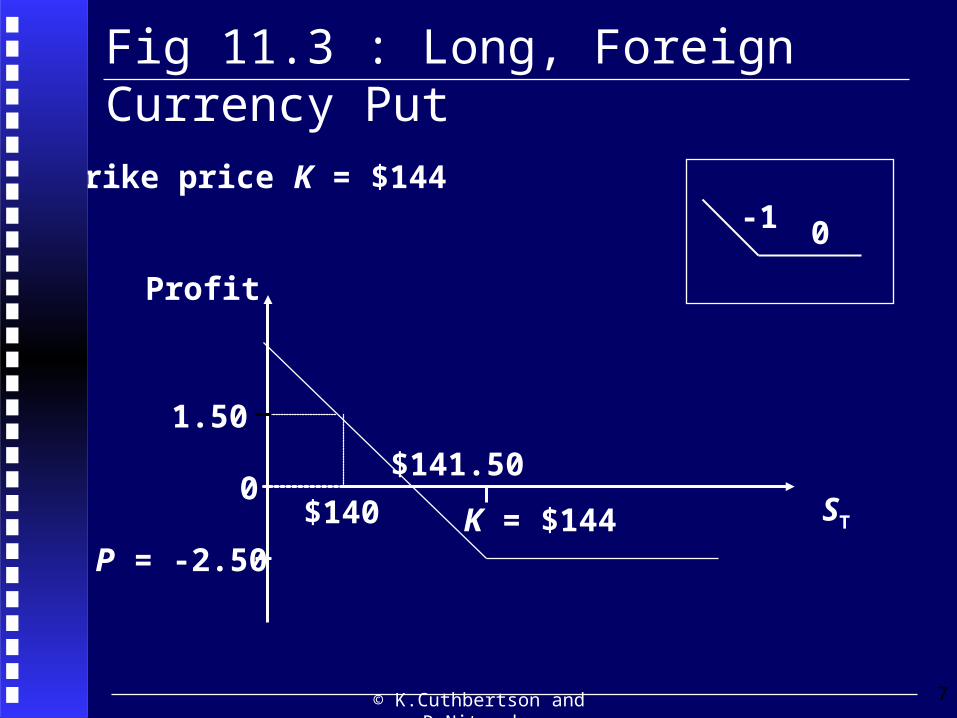

Fig 11.3 : Long, Foreign Currency Put

Strike price K = $144

ST

Profit

1.50

P = -2.50

$141.50

$140 K = $1440

0-1

© K.Cuthbertson and D.Nitzsche8

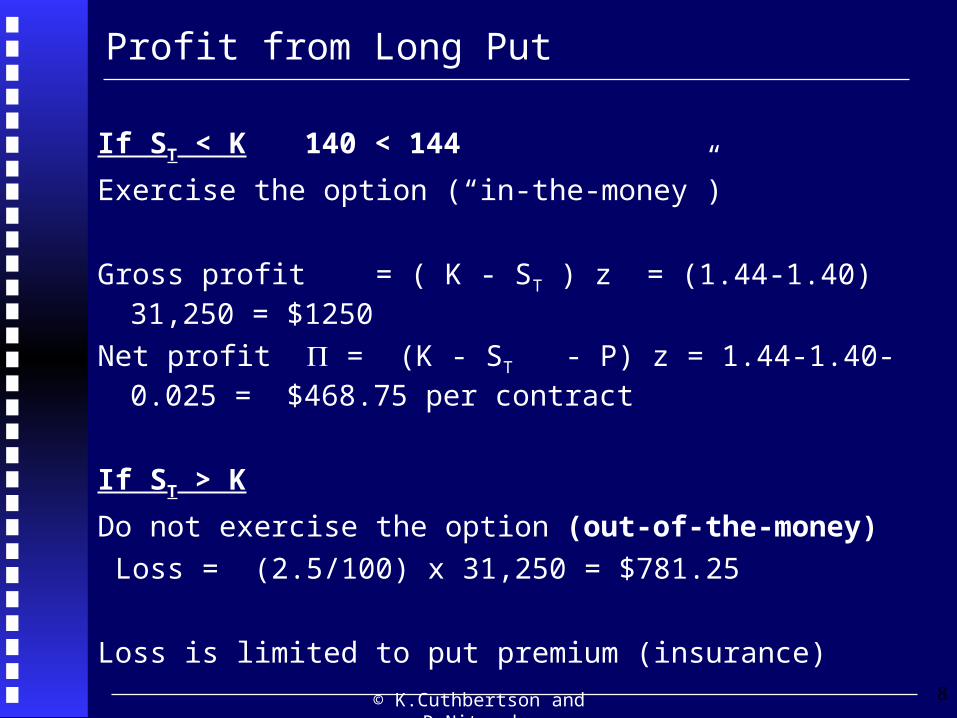

Profit from Long Put

If ST < K 140 < 144

Exercise the option (“in-the-money”)

Gross profit = ( K - ST ) z = (1.44-1.40) 31,250 = $1250

Net profit = (K - ST - P) z = 1.44-1.40-0.025 = $468.75 per contract

If ST > K

Do not exercise the option (out-of-the-money)

Loss = (2.5/100) x 31,250 = $781.25

Loss is limited to put premium (insurance)

© K.Cuthbertson and D.Nitzsche9

Buy (long) call on sterling if you expect sterling to appreciate.

Buy long put on sterling if you expect sterling to depreciate

Calls and Puts: Speculation

© K.Cuthbertson and D.Nitzsche10

Hedging Foreign Currency Receiptsusing

Forwards, Optionsand Futures

© K.Cuthbertson and D.Nitzsche11

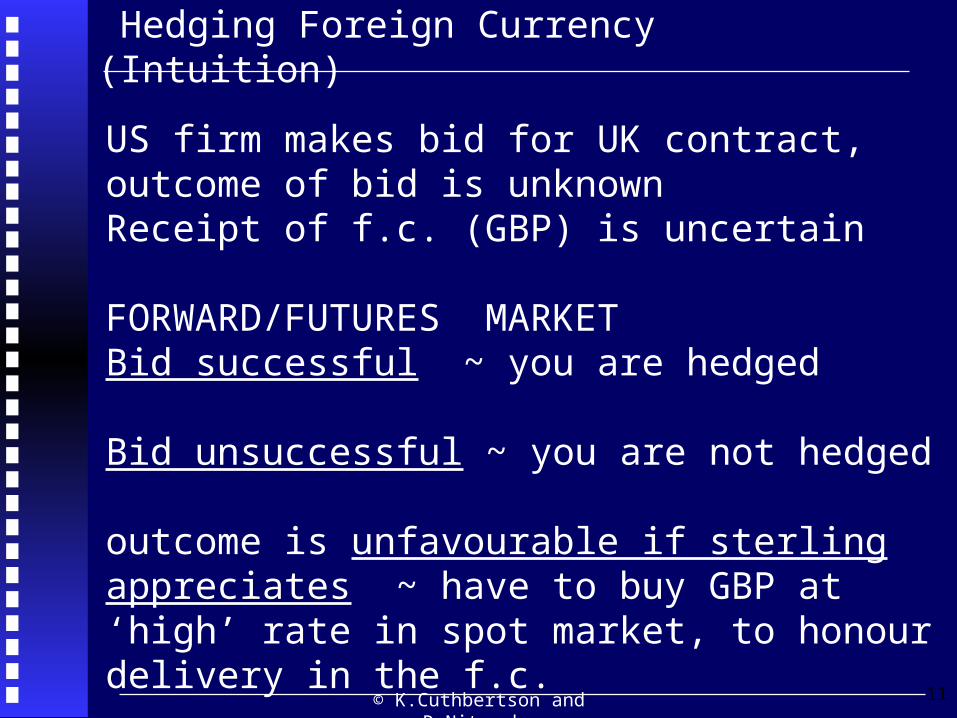

Hedging Foreign Currency (Intuition)

US firm makes bid for UK contract, outcome of bid is unknownReceipt of f.c. (GBP) is uncertain

FORWARD/FUTURES MARKETBid successful ~ you are hedged

Bid unsuccessful ~ you are not hedged outcome is unfavourable if sterling appreciates ~ have to buy GBP at ‘high’ rate in spot market, to honour delivery in the f.c.

© K.Cuthbertson and D.Nitzsche12

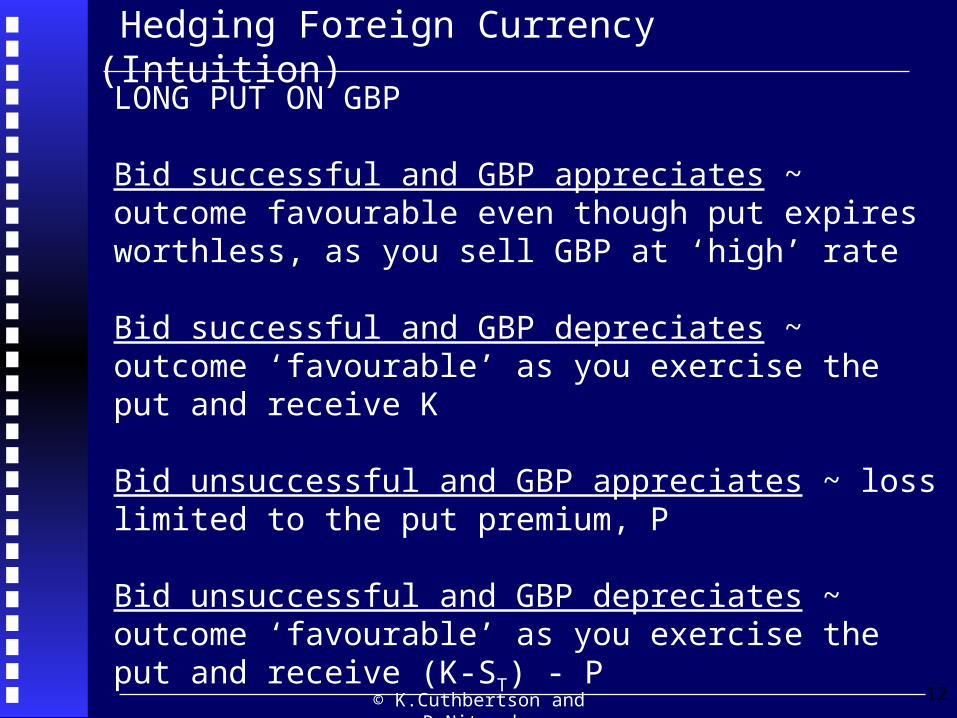

Hedging Foreign Currency (Intuition)

LONG PUT ON GBP

Bid successful and GBP appreciates ~ outcome favourable even though put expires worthless, as you sell GBP at ‘high’ rate

Bid successful and GBP depreciates ~ outcome ‘favourable’ as you exercise the put and receive K

Bid unsuccessful and GBP appreciates ~ loss limited to the put premium, P

Bid unsuccessful and GBP depreciates ~ outcome ‘favourable’ as you exercise the put and receive (K-ST) - P

© K.Cuthbertson and D.Nitzsche13

US firm :bid for sterling contract, V= £12.5mAt F0 = 1.61($/£), USD equivalent of$20.125m.

PUT CONTRACTStrike Price K = 1.60 ($/£)Size of Contract, zp = £31,250Put Premium P = 0.025 ($/£)Cost, one Put contract (= zpP) = $781.25

Number of Put Contracts NP = (V/zp) = (£12.5m / £31,250) = 400 contracts

Cost of Np puts = Np (zp P) = VP = $312,500 (Note that V = Np zp )

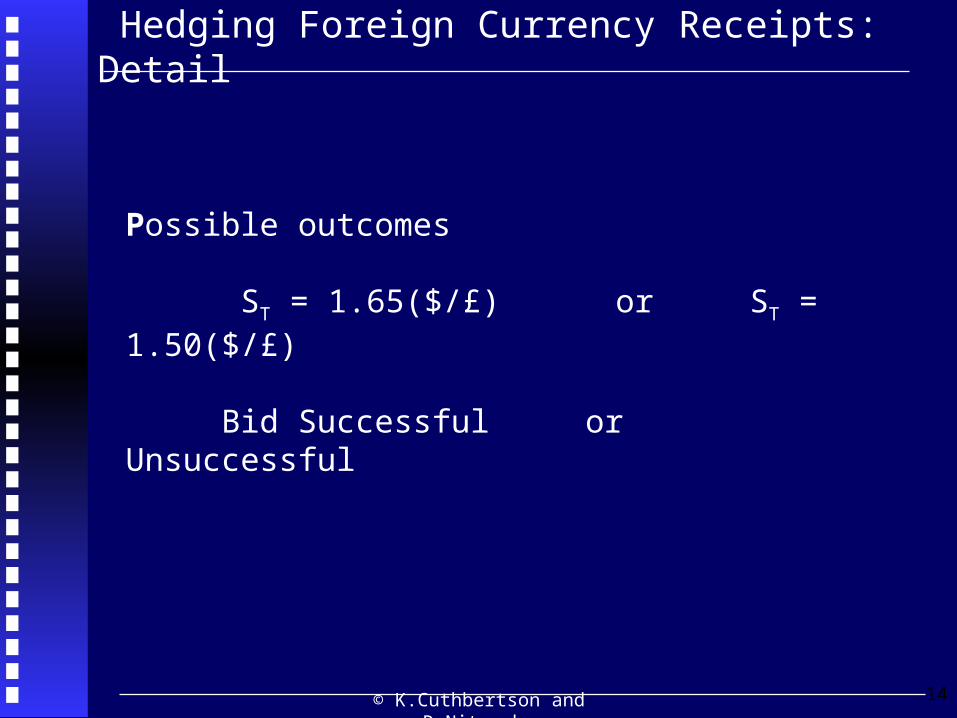

Hedging Foreign Currency Receipts: Detail

© K.Cuthbertson and D.Nitzsche14

Possible outcomes

ST = 1.65($/£) or ST = 1.50($/£)

Bid Successful or Unsuccessful

Hedging Foreign Currency Receipts: Detail

© K.Cuthbertson and D.Nitzsche15

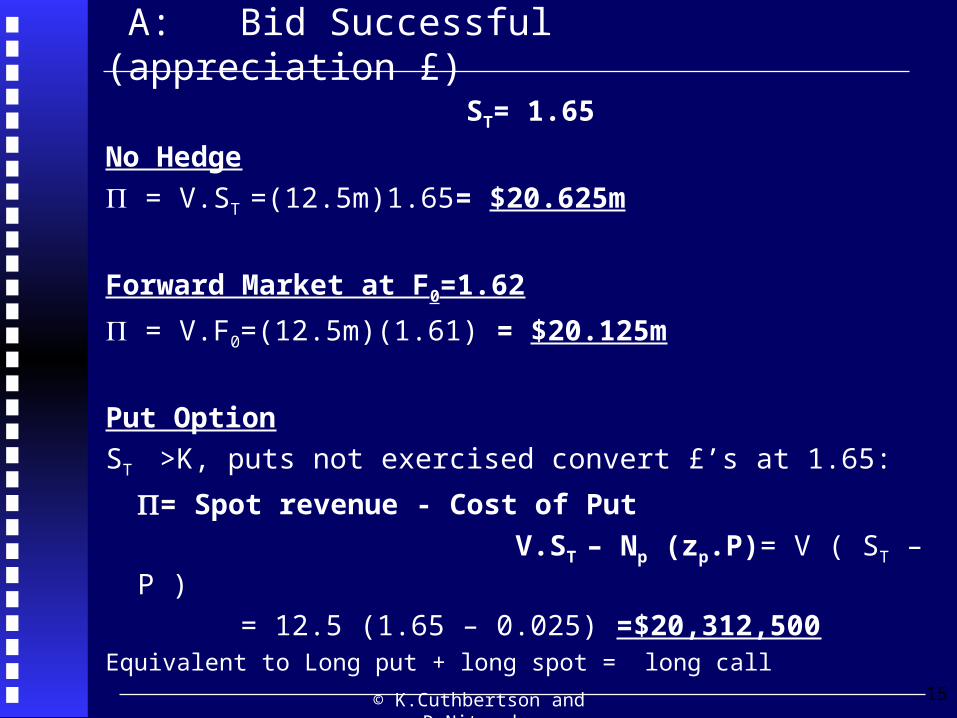

A: Bid Successful (appreciation £)

ST= 1.65

No Hedge

= V.ST =(12.5m)1.65= $20.625m

Forward Market at F0=1.62

= V.F0=(12.5m)(1.61) = $20.125m

Put Option

ST >K, puts not exercised convert £’s at 1.65:

= Spot revenue - Cost of Put

V.ST – Np (zp.P)= V ( ST – P )

= 12.5 (1.65 – 0.025) =$20,312,500Equivalent to Long put + long spot = long call

© K.Cuthbertson and D.Nitzsche16

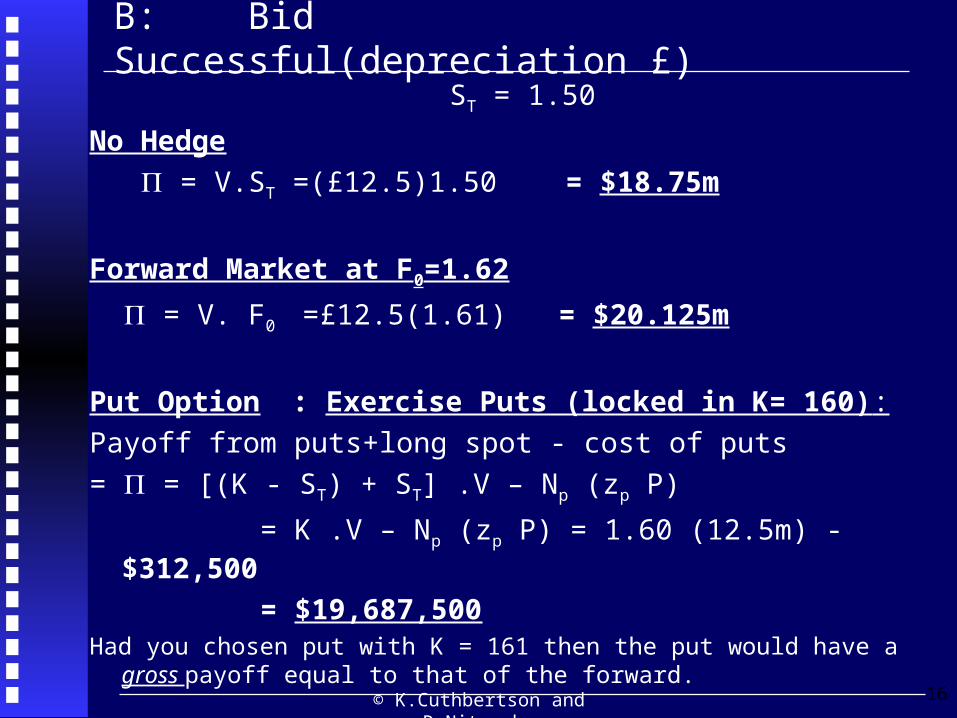

B: Bid Successful(depreciation £)

ST = 1.50

No Hedge

= V.ST =(£12.5)1.50 = $18.75m

Forward Market at F0=1.62

= V. F0 =£12.5(1.61) = $20.125m

Put Option : Exercise Puts (locked in K= 160):

Payoff from puts+long spot - cost of puts

= = [(K - ST) + ST] .V – Np (zp P)

= K .V – Np (zp P) = 1.60 (12.5m) - $312,500

= $19,687,500 Had you chosen put with K = 161 then the put would have a gross payoff

equal to that of the forward.

© K.Cuthbertson and D.Nitzsche17

C: Bid Unsuccessful (appreciation £)

ST = 1.65

No Hedge: No Cash Flow

Forward Market at F0=1.62

Purchase £12.5m at a cost of ST = 1.65 and receive F0 =1.61

=(Fo – ST).V == (1.61 – 1.65) £12.5= - $500,000

(Equivalent to open short position in the F.C. and you are exposed to potential large losses as S increases)

Put Option :Not Exercised:(equiv to naked put)

Lost put premium = Np (zp P) = V. P = $312,500

© K.Cuthbertson and D.Nitzsche18

D: Bid Unsuccessful (depreciation £)

ST = 1.50

No Hedge: No Cash Flow

Forward Market at F0=1.61

Purchase £12.5m at a cost of ST = 1.50 and

receive F0 =1.62 on (£12.5m)

=(Fo – ST)V == (1.61 – 1.50) £12.5= $1.375m

(Equivalent to open short position in the F.C. and you have potential large gains as S increases)

Put Option : Exercise Puts:(equiv to naked put)

Purchase, at ST= 1.50 and exercise puts K = 1.60

= (K - ST – P ) V=(1.60– 1.50 –0.025) 12.5 = $937,500

© K.Cuthbertson and D.Nitzsche19

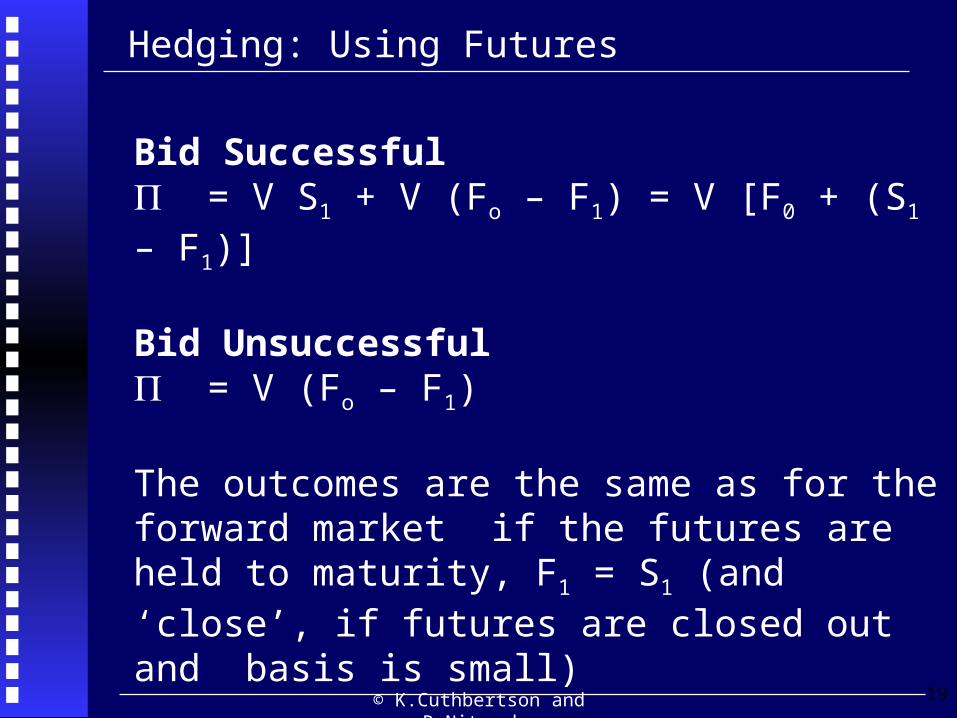

Bid Successful = V S1 + V (Fo – F1) = V [F0 + (S1 – F1)]

Bid Unsuccessful = V (Fo – F1)

The outcomes are the same as for the forward market if the futures are held to maturity, F1 = S1 (and ‘close’, if futures are closed out and basis is small)

Hedging: Using Futures

© K.Cuthbertson and D.Nitzsche20

Pricing Foreign Currency Options

© K.Cuthbertson and D.Nitzsche21

Pricing

Replace q= dividend yield by rf

[11.13] C = S N(d1) - K N(d2) [11.14] P = K N(-d2) - S N(-d1)

d1 =

d2 = = d1 -

S is measured as $ per £ (or cents per £),

T

TrrKS fd

)2/()/ln( 2

T

TrrKS fd

)2/()/ln( 2

T

© K.Cuthbertson and D.Nitzsche22

Pricing: Alternative Representation

[11.16] S = F

Substituting [11.16] in [11.13] and [11.14]::

[11.17] C = [F N(d1) - K N(d2)]

[11.18] P = [K N(-d2) – F N(-d1)]

d1 =

d2 =

Trr fde )(

T

TKF

)2/()/ln( 2

T

TKF

)2/()/ln( 2

© K.Cuthbertson and D.Nitzsche23

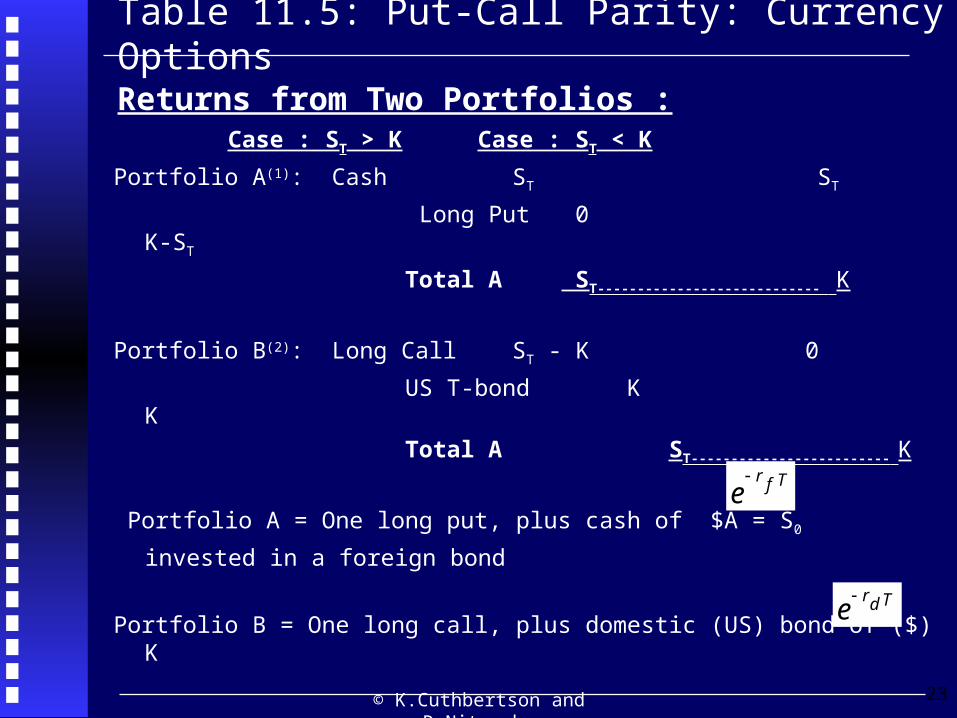

Table 11.5: Put-Call Parity: Currency Options

Case : ST > K Case : ST < K

Portfolio A(1): Cash ST ST

Long Put 0 K-ST

Total A ST---------------------------- K

Portfolio B(2): Long Call ST - K 0

US T-bond K K

Total A ST------------------------- K

Portfolio A = One long put, plus cash of $A = S0

invested in a foreign bond

Portfolio B = One long call, plus domestic (US) bond of ($) K

Tfre

Tdre

Returns from Two Portfolios :

© K.Cuthbertson and D.Nitzsche24

END OF SLIDES