© Grant Thornton LLP. All rights reserved. Doing Business in China Scott Farber Assurance partner...

30

n LLP. All rights reserved. Doing Business in China Scott Farber Assurance partner May 9, 2007

-

Upload

valentine-ford -

Category

Documents

-

view

218 -

download

0

Transcript of © Grant Thornton LLP. All rights reserved. Doing Business in China Scott Farber Assurance partner...

© Grant Thornton LLP. All rights reserved.

Doing Business in China

Scott FarberAssurance partner

May 9, 2007

© Grant Thornton LLP. All rights reserved.

Today's discussion

• Organizational structures in China

• Tax considerations

• Opportunities under WTO

• Building a vision, not a strategy

© Grant Thornton LLP. All rights reserved.

China: A case for growth

• Leadership committed to maintaining economic momentum

• China is “open for business” to foreign companies

• WTO

• Clarity of rules

• Rule of law

• Privatization of state-owned enterprises

© Grant Thornton LLP. All rights reserved.

Growing Chinese domestic market for goods and services

• Emerging urban middle class

• Surge in urban purchasing power

• Purchasing and financing of homes, cars, durable goods

© Grant Thornton LLP. All rights reserved.

Today's discussion

• Organizational structures in China

• Tax considerations

• Opportunities under WTO

• Building a vision, not a strategy

© Grant Thornton LLP. All rights reserved.

Organizational structures in China

• Representative Office (RO)

• Types of direct investment – Foreign Investment Enterprises (FIE)

- Equity Joint Venture (EJV)

- Cooperative Joint Venture (CJV)

- Wholly Foreign Owned Entity (WFOE)

• Direct acquisitions

© Grant Thornton LLP. All rights reserved.

Representative office (RO)

• Limited permitted activities- Market research- Liaison functions- Other preparatory/auxiliary activities

• RO cannot hire Chinese labor

- Must pay fee to use labor service companies (e.g. FESCO)

- RO can sponsor non-Chinese citizens to work in China

© Grant Thornton LLP. All rights reserved.

Joint ventures (JV)

• Why enter into JV arrangement with Chinese partner?- Knowledge of customers and distribution channels

- Relationships with governmental authorities

- Relationships with labor force

© Grant Thornton LLP. All rights reserved.

Joint ventures (JV)

• Why JVs fail…- Chinese partner undercapitalized

- Overstated market knowledge

- Unfamiliar with modern sales methods

- Different objectives and expectations;

- Disputes over expenses, profitability, dividend distributions

- Cultural differences

- Overstated relationship with bureaucracy

© Grant Thornton LLP. All rights reserved.

Equity JV vs. Cooperative JV

• EJV: Income is shared in proportion to amount of investment; inflexible; used for long-term projects (30% cash)

• CJV: Division of profits not limited to amount of investment; parties can define profit sharing in their agreement; rarely used

• Tax treatment similar; EJV law well established

© Grant Thornton LLP. All rights reserved.

Wholly foreign owned entity (WFOE)

• 100% foreign ownership must be permitted

• Previous restriction abolished requiring 50% of manufactured products to be exported

• Advantages of WFOEs:

- Faster establishment, no need to find "right" Chinese partner, negotiate JV contract and other agreements

- Complete management control and profits not shared

- Protect technology and intellectual property

- Make changes to articles of incorporation or registered capital without need for agreement

© Grant Thornton LLP. All rights reserved.

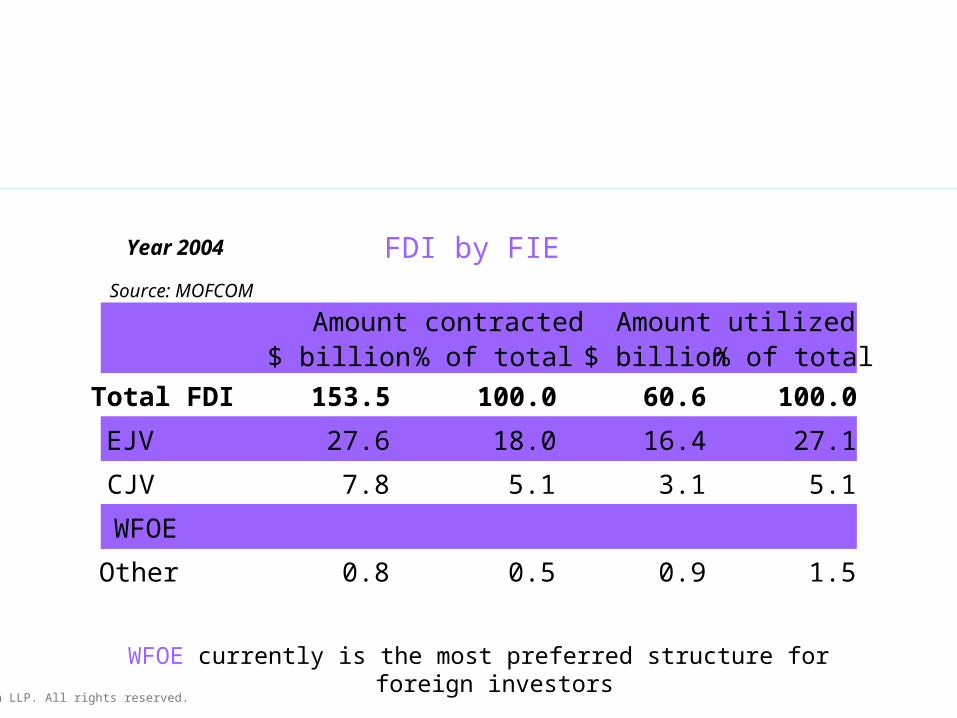

Common structures of foreign invested enterprises (FIE)

WFOE currently is the most preferred structure for foreign investors

Year 2004 FDI by FIE

$ billion % of total $ billion % of total

Total FDI 153.5 100.0 60.6 100.0

EJV 27.6 18.0 16.4 27.1

CJV 7.8 5.1 3.1 5.1

WFOE 117.3 76.4 40.2 66.3

Other 0.8 0.5 0.9 1.5

Amount contracted Amount utilizedSource: MOFCOM

© Grant Thornton LLP. All rights reserved.

Today's discussion

• Organizational structures in China

• Tax considerations

• Opportunities under WTO

• Building a vision, not a strategy

© Grant Thornton LLP. All rights reserved.

Unified Tax Law

• Effective January 1, 2008• Enterprise tax rate of 25%• Applicable to both foreign-invested and domestic

enterprises• Withholding tax of 20% applies to dividends,

royalties, rentals and capital gains

© Grant Thornton LLP. All rights reserved.

Preferential treatment

• Technologically advanced enterprises in encouraged industries enjoy 15% rate

• Agricultural, infrastructure, and environmentally friendly projects are eligible

• Projects in Central & Western China – eligible• Special Economic Zones (Shenzhen) – continue to

receive reduced tax rate & other benefits• Foreign investment enterprises no longer enjoy a

general 2-year exemption or 3-year 50% reduction

© Grant Thornton LLP. All rights reserved.

Grandfather provision

• Five year transition period for enterprises currently enjoying preferential tax rates or newly formed enterprises prior to March 16, 2007

• Companies will continue to enjoy the old rates for the full 5 years

• Tax holidays will continue during the grandfather period and then will lapse

© Grant Thornton LLP. All rights reserved.

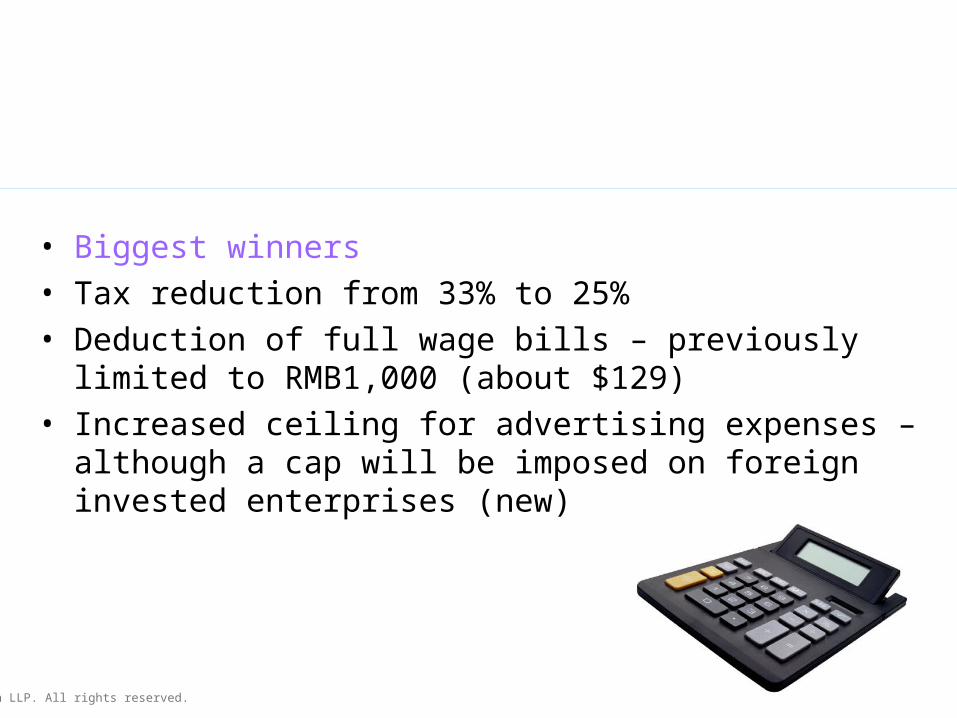

Domestic companies

• Biggest winners• Tax reduction from 33% to 25%• Deduction of full wage bills – previously limited to

RMB1,000 (about $129)• Increased ceiling for advertising expenses –

although a cap will be imposed on foreign invested enterprises (new)

© Grant Thornton LLP. All rights reserved.

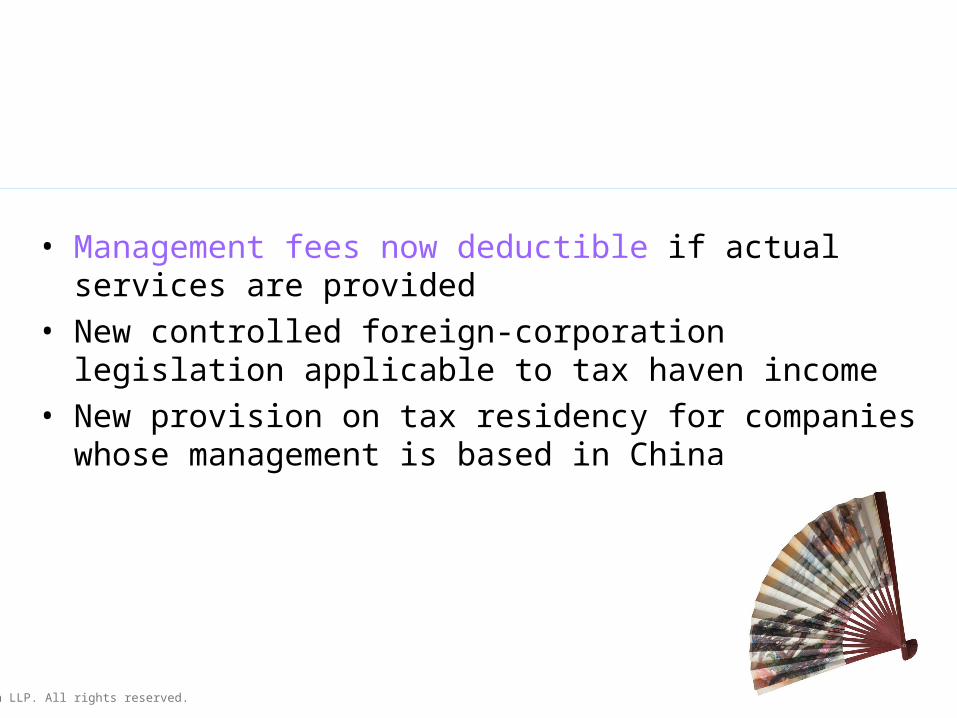

Other provisions

• Management fees now deductible if actual services are provided

• New controlled foreign-corporation legislation applicable to tax haven income

• New provision on tax residency for companies whose management is based in China

© Grant Thornton LLP. All rights reserved.

Today's discussion

• Organizational structures in China

• Tax considerations

• Opportunities under WTO

• Building a vision, not a strategy

© Grant Thornton LLP. All rights reserved.

World Trade Organization

• Acceded to WTO in December 2001• Covers agricultural, industrial and services sectors• Substantial market access commitments to be

accomplished over a time frame• 2,300 laws amended & 800 abolished• Clear commitment to participate in global economy

© Grant Thornton LLP. All rights reserved.

Investment Categories

• Encouraged

- VAT & tariff-free imports of M&E

- 256 industries (up from 186)

• Permitted

- WFOE for distribution, storage, warehousing and transportation

- Down to 78 industries

• Restricted – generally limits ownership %• Prohibited

© Grant Thornton LLP. All rights reserved.

Commitments under WTO

• Tariff reductions• Removal of import license requirements• Trading & distribution rights• Liberalize telecom, financial & professional services

© Grant Thornton LLP. All rights reserved.

Today's discussion

• Organizational structures in China

• Taxation

• Opportunities under WTO

• Building a vision, not a strategy

© Grant Thornton LLP. All rights reserved.

Building a vision, not a strategy…

• Don’t have a China strategy…

- Have a China "vision" and ambition, but focus within your resources to understand and execute

- Flexibility to approach the market is critical

- Build for export or local consumption

© Grant Thornton LLP. All rights reserved.

Business Objectives

Profit Repatriation

Exchange Control

Financing/Capital Requirements

Type of Business

Human Resources

Where to organize

StructuringTransfer Pricing

IP Protection

Property Issues

Exit Strategy

China

Business Plan

Key considerations

© Grant Thornton LLP. All rights reserved.

Current issues

Strategy People

• Lack of alignment with overall organizational vision and strategy

• Lack of alignment of goals/ objectives with local business partners

• Selection of location

• Culture and communication

• Rural migration

• Understanding management time and commitment

• Selection of General Manager

© Grant Thornton LLP. All rights reserved.

Current issuesCurrent issues

Finance Resources

• RMB revaluation• Bank restructuring• State owned

enterprises• Managing foreign

exchange matters

• Energy shortage• Environmental

problems• Availability of raw

materials• Changing regulatory

environment• Intellectual property

rights/protection

© Grant Thornton LLP. All rights reserved.

Making a move

• When is the right time for your company to be looking at China and other overseas opportunities?

© Grant Thornton LLP. All rights reserved.

Questions?

•Question and answer session

© Grant Thornton LLP. All rights reserved.

Disclaimers

Tax Professional Standards StatementIn accordance with certain professional standards, we inform you that this proposal supports Grant Thornton LLP’s marketing of professional services, and is not written tax advice directed at the particular facts and circumstances of any person. We encourage you to discuss with us or an independent tax advisor the potential application of this proposal to your particular situation. Nothing herein shall be construed as imposing a limitation on any person from disclosing the tax treatment or tax structure of any matter addressed herein. To the extent this document may be considered to contain written tax advice, any written advice contained in, forwarded with, or attached to this document is not intended by Grant Thornton to be used, and cannot be used, by any person for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

Standard disclaimer and copyright© 2007 Grant Thornton LLP, the U.S. member firm of Grant Thornton International. All rights reserved. Printed in the U.S.A. This proposal is the work of Grant Thornton LLP, the U.S. member firm of Grant Thornton International, and is in all respects subject to negotiation, agreement and signing of specific contracts. The information contained within this document is intended only for the entity or person to which it is addressed and contains confidential and/or privileged material. Dissemination to third-parties, copying or use of this information is strictly prohibited without the prior consent of Grant Thornton LLP.