Does Debt Policy Matter? Principles of Corporate Finance Brealey and Myers Sixth Edition Slides by...

22

Does Debt Policy Matter? Principles of Corporate Finance Brealey and Myers Sixth Edition Slides by Matthew Will Chapter 17 ©The McGraw-Hill Companies, Inc., 2000 Irwin/McGraw Hill

-

Upload

kaitlin-swain -

Category

Documents

-

view

234 -

download

2

Transcript of Does Debt Policy Matter? Principles of Corporate Finance Brealey and Myers Sixth Edition Slides by...

Does Debt Policy Matter?

Principles of Corporate FinanceBrealey and Myers Sixth Edition

Slides by

Matthew Will Chapter 17

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 2

Topics Covered

Leverage in a Tax Free Environment How Leverage Effects Returns The Traditional Position

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 3

M&M (Debt Policy Doesn’t Matter)

Modigliani & Miller When there are no taxes and capital markets

function well, it makes no difference whether the firm borrows or individual shareholders borrow. Therefore, the market value of a company does not depend on its capital structure.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 4

M&M (Debt Policy Doesn’t Matter)

Assumptions

By issuing 1 security rather than 2, company diminishes investor choice. This does not reduce value if: Investors do not need choice, OR There are sufficient alternative securities

Capital structure does not affect cash flows e.g... No taxes No bankruptcy costs No effect on management incentives

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 5

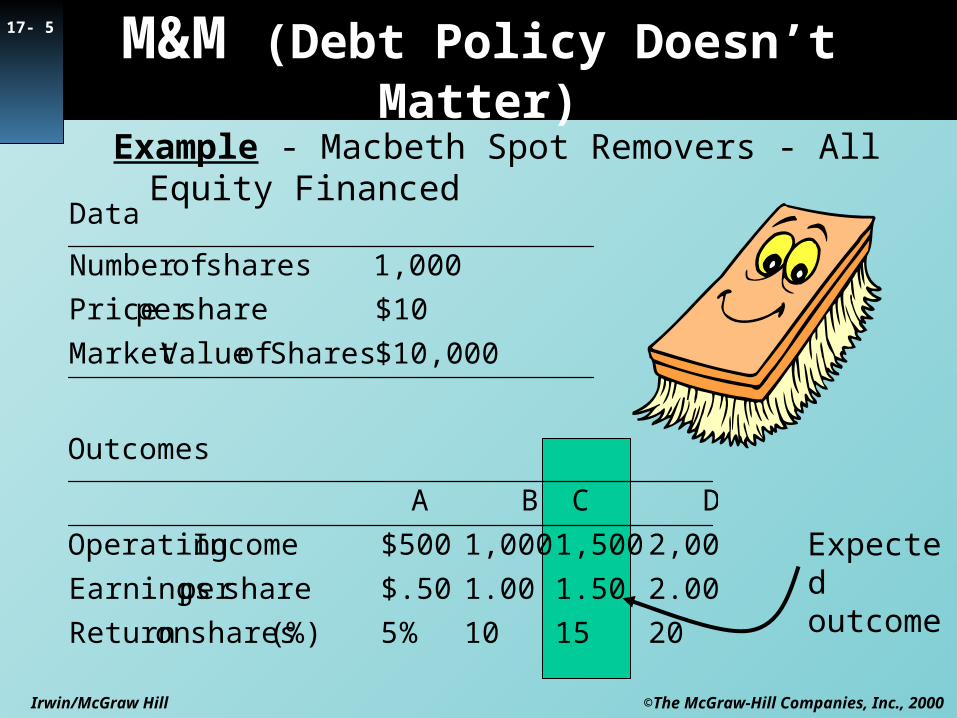

Example - Macbeth Spot Removers - All Equity Financed

201510% 5(%) shares on Return

2.001.501.00$.50shareper Earnings

2,0001,5001,000$500Income Operating

D C BA

Outcomes

10,000 $Shares of ValueMarket

$10shareper Price

1,000shares ofNumber

Data

M&M (Debt Policy Doesn’t Matter)

Expected outcome

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 6

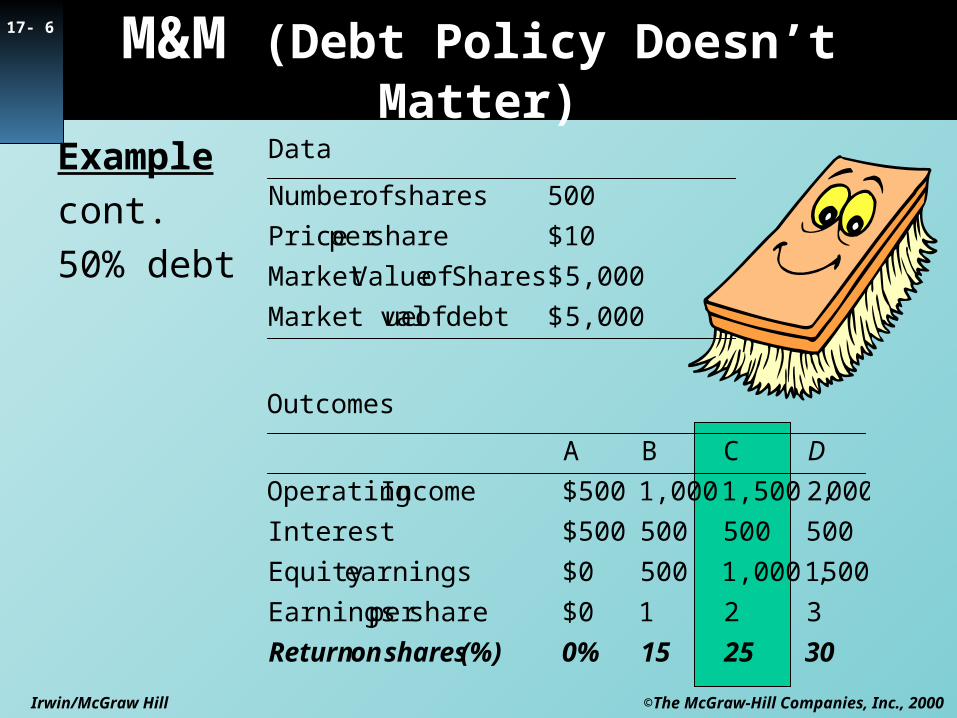

Example

cont.

50% debt

M&M (Debt Policy Doesn’t Matter)

3025150%(%) shares on Return

321$0shareper Earnings

500,11,000500$0earningsEquity

500500500$500Interest

000,21,5001,000$500Income Operating

CBA

Outcomes

5,000 $debt of ueMarket val

5,000 $Shares of ValueMarket

$10shareper Price

500shares ofNumber

Data

D

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 7

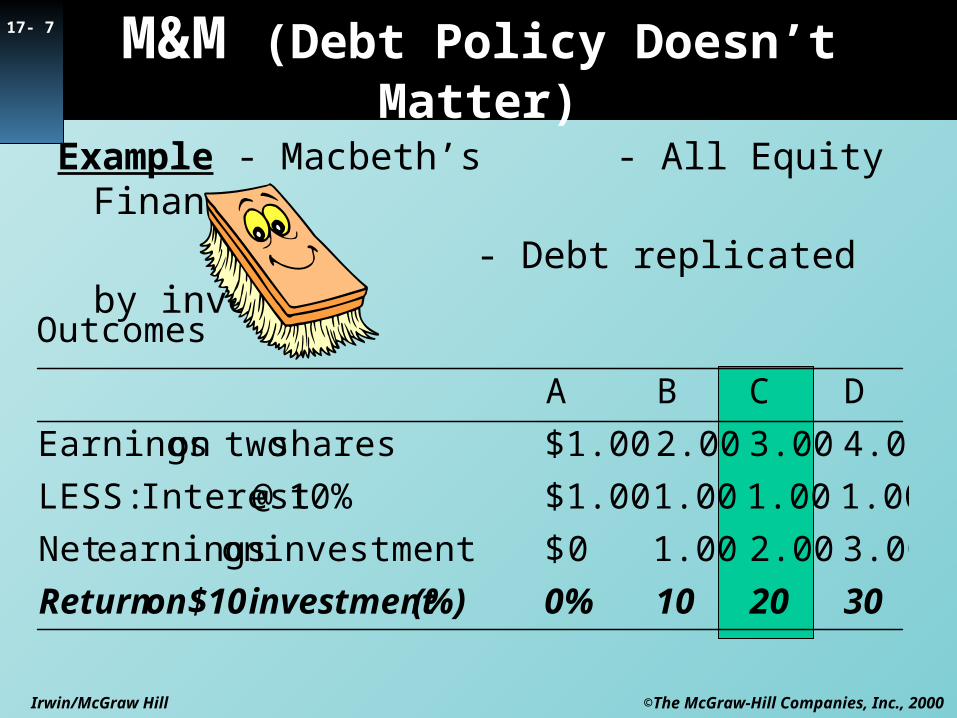

Example - Macbeth’s - All Equity Financed

- Debt replicated by investors

3020100%(%) investment$10 on Return

3.002.001.000 $investment on earningsNet

1.001.001.00$1.0010% @Interest :LESS

4.003.002.00$1.00shares twoon Earnings

DCBA

Outcomes

M&M (Debt Policy Doesn’t Matter)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 8

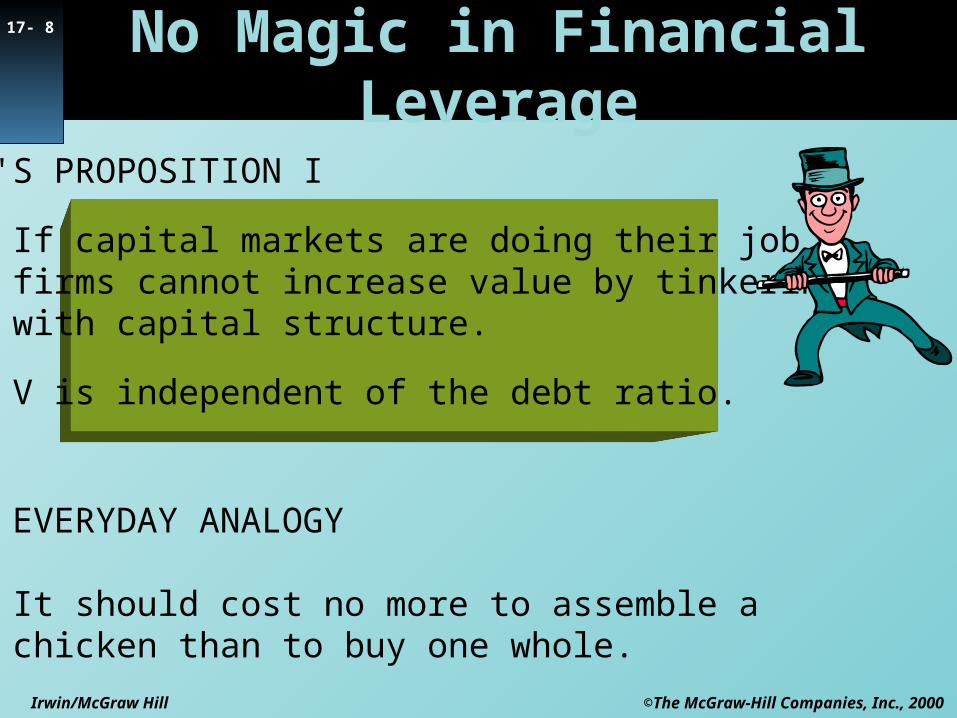

MM'S PROPOSITION I

If capital markets are doing their job, firms cannot increase value by tinkering with capital structure.

V is independent of the debt ratio.

AN EVERYDAY ANALOGY

It should cost no more to assemble a chicken than to buy one whole.

No Magic in Financial Leverage

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 9

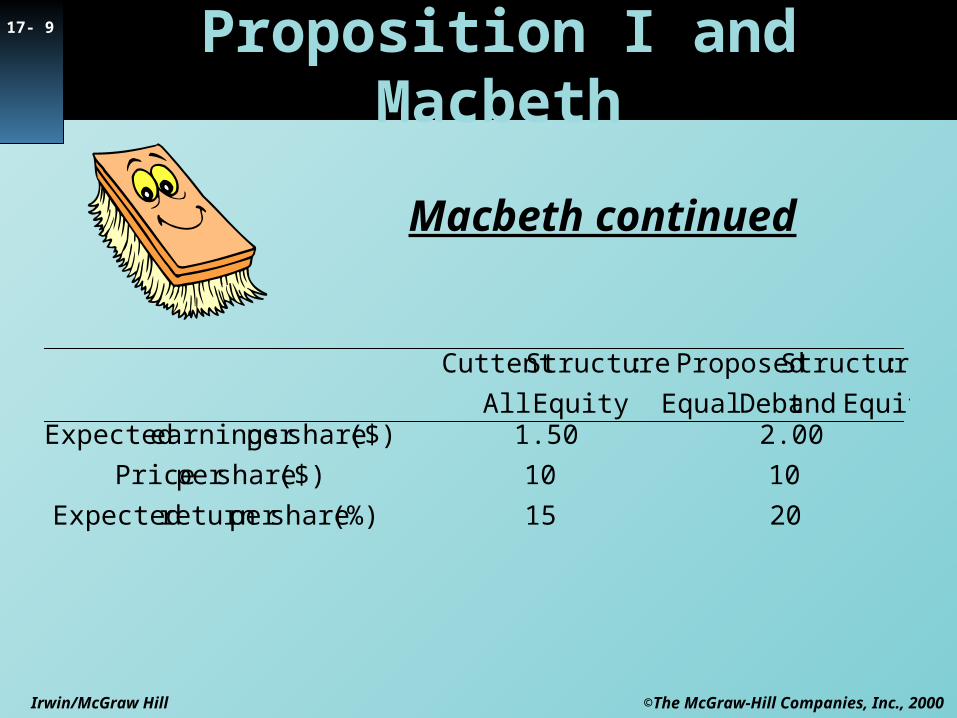

Proposition I and Macbeth

2015(%) shareper return Expected

1010($) shareper Price

2.001.50($) shareper earnings Expected Equityand Debt Equal

:Structure Proposed

EquityAll

:StructureCuttent

Macbeth continued

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 10

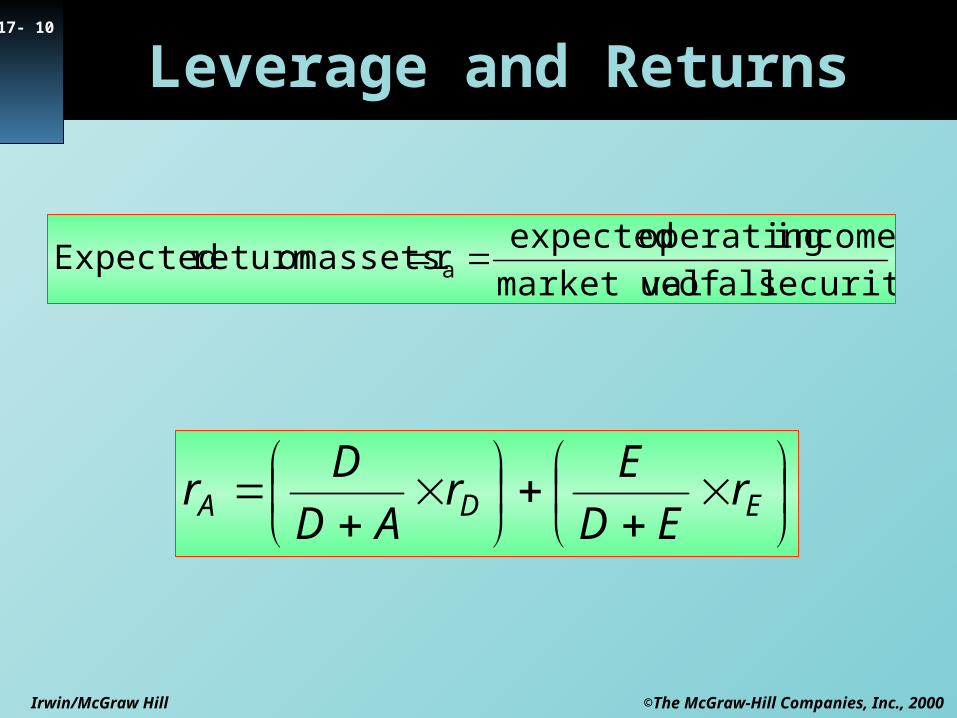

Leverage and Returns

securities all of uemarket val

income operating expectedr assets on return Expected a

EDA r

ED

Er

AD

Dr

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

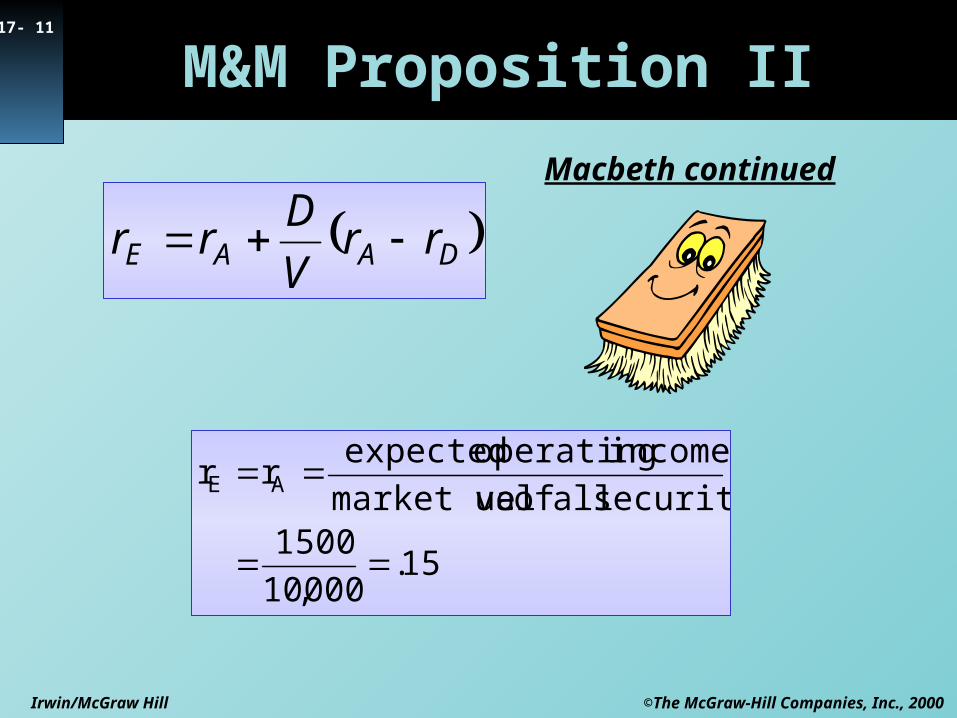

17- 11

M&M Proposition II

15.000,10

1500securities all of uemarket val

income operating expectedr r AE

DAAE rrV

Drr

Macbeth continued

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

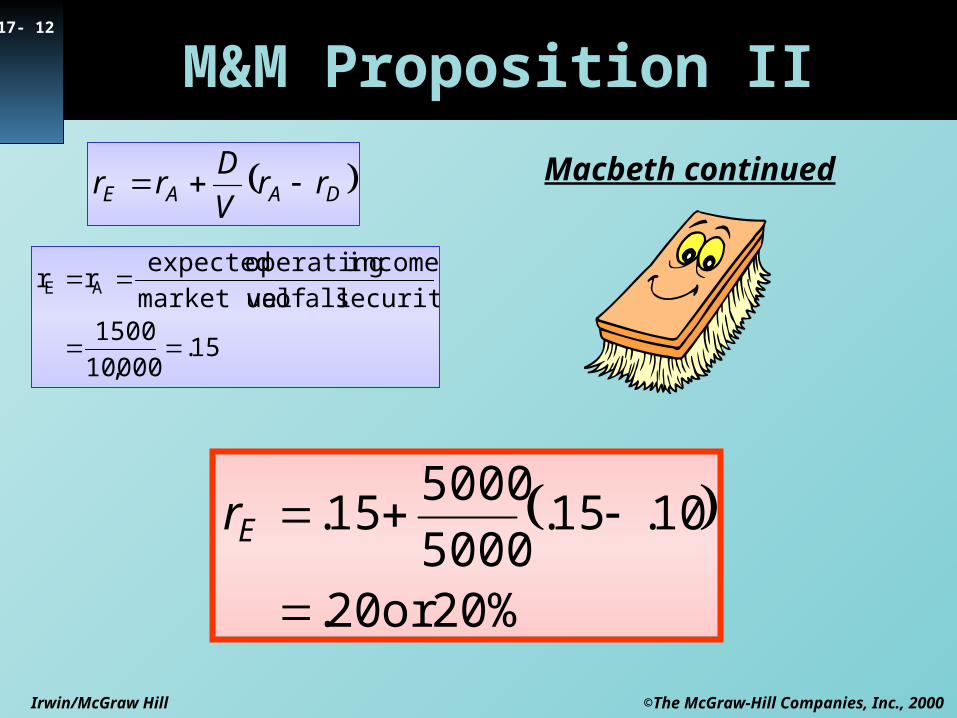

17- 12

M&M Proposition II

15.000,10

1500securities all of uemarket val

income operating expectedr r AE

DAAE rrV

Drr

20%or 20.

10.15.5000

500015.

Er

Macbeth continued

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 13

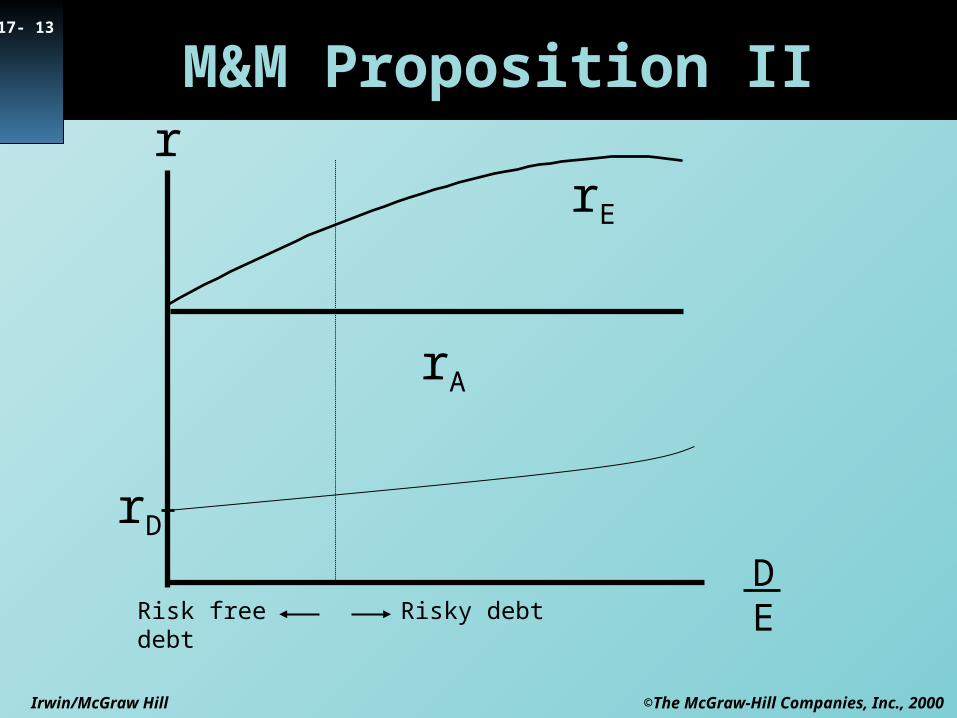

r

DE

rD

rE

M&M Proposition II

rA

Risk free debt Risky debt

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 14

Leverage and Risk

200shares on Return

20($) shareper Earnings:debt % 50

155shares on Return

1.50.50($) shareper Earningsequity All$1,500

Income

$500

Operating

200shares on Return

20($) shareper Earnings:debt % 50

155shares on Return

1.50.50($) shareper Earningsequity All$1,500

Income

$500

Operating

Macbeth continued

Leverage increases the risk of Macbeth shares

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 15

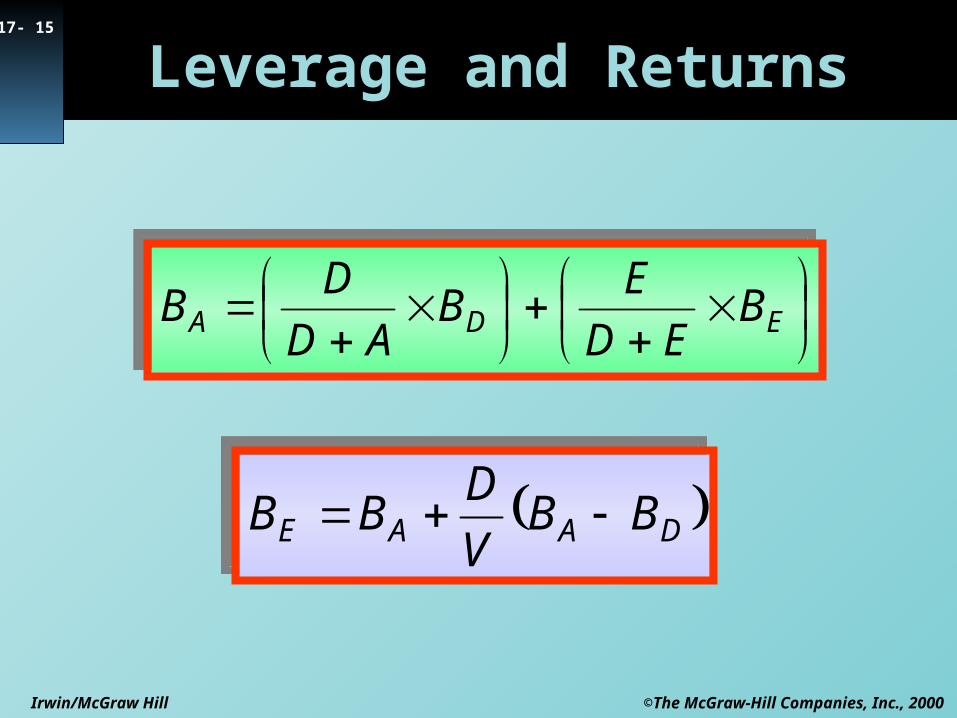

Leverage and Returns

EDA B

ED

EB

AD

DB

EDA B

ED

EB

AD

DB

DAAE BBV

DBB DAAE BB

V

DBB

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 16

WACC

EDA r

V

Er

V

DrWACC

EDA r

V

Er

V

DrWACC

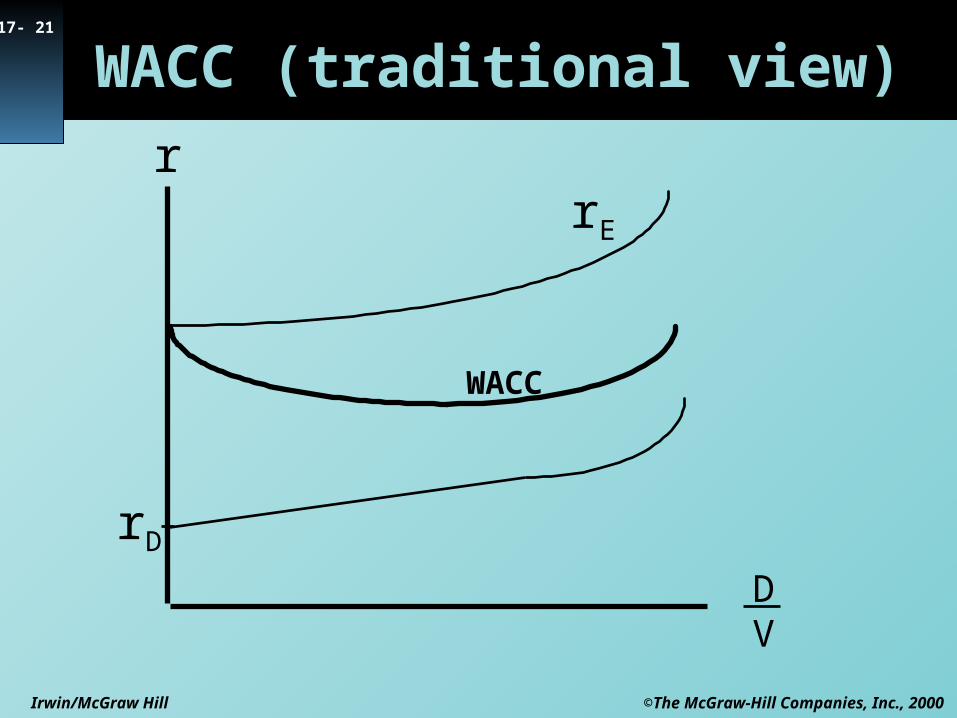

WACC is the traditional view of capital structure, risk and return.

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

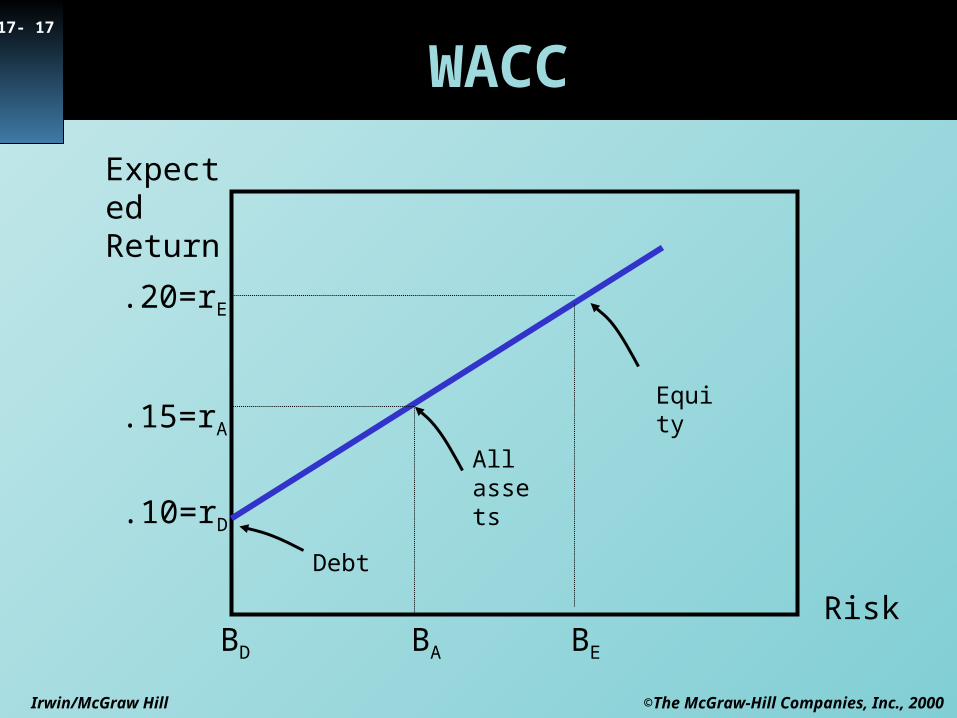

17- 17

WACC

.10=rD

.20=rE

.15=rA

BEBABDRisk

Expected Return

Equity

All assets

Debt

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 18

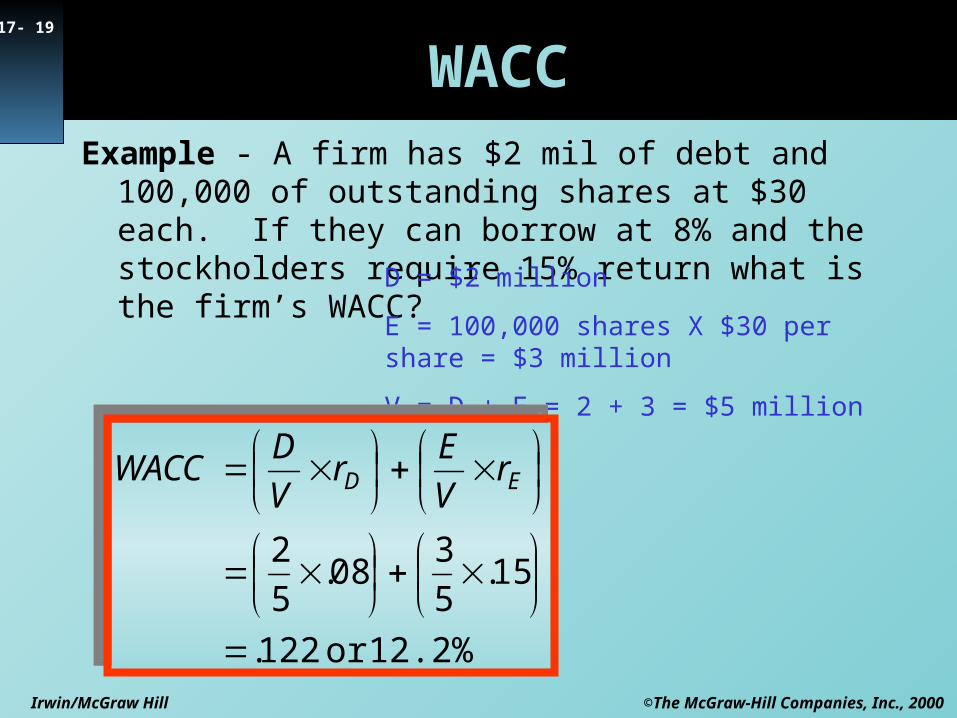

WACC

Example - A firm has $2 mil of debt and 100,000 of outstanding shares at $30 each. If they can borrow at 8% and the stockholders require 15% return what is the firm’s WACC?

D = $2 million

E = 100,000 shares X $30 per share = $3 million

V = D + E = 2 + 3 = $5 million

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 19

WACCExample - A firm has $2 mil of debt and 100,000 of

outstanding shares at $30 each. If they can borrow at 8% and the stockholders require 15% return what is the firm’s WACC? D = $2 million

E = 100,000 shares X $30 per share = $3 million

V = D + E = 2 + 3 = $5 million

12.2%or 122.

15.5

308.

5

2

ED r

V

Er

V

DWACC

12.2%or 122.

15.5

308.

5

2

ED r

V

Er

V

DWACC

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

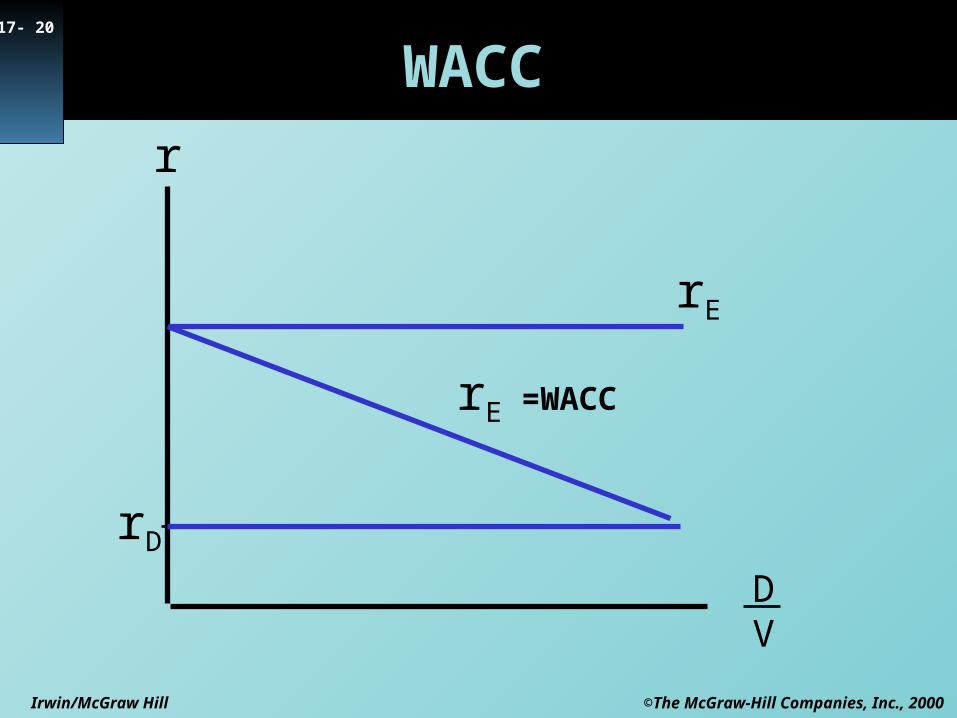

17- 20

r

DV

rD

rE

rE =WACC

WACC

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

17- 21

r

DV

rD

rE

WACC

WACC (traditional view)

©The McGraw-Hill Companies, Inc., 2000Irwin/McGraw Hill

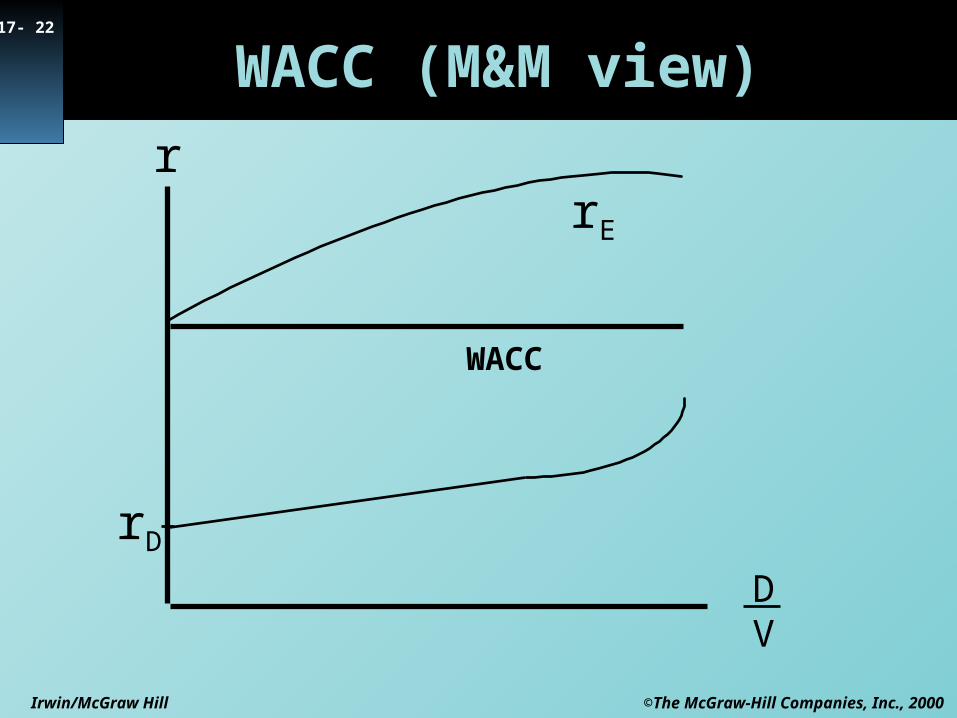

17- 22

r

DV

rD

rE

WACC

WACC (M&M view)