· 1 CORPORATE FINANCIAL REPORTING 10 – Liabilities: Notes, Bonds & Leases Long-Lived Assets.

47

· 1 CORPORATE FINANCIAL REPORTING 10 – Liabilities: Notes, Bonds & Leases Long-Lived Assets

-

Upload

beverley-briggs -

Category

Documents

-

view

221 -

download

1

Transcript of · 1 CORPORATE FINANCIAL REPORTING 10 – Liabilities: Notes, Bonds & Leases Long-Lived Assets.

· 1

CORPORATE FINANCIAL REPORTING

10 – Liabilities: Notes, Bonds & Leases

Long-Lived Assets

UNITED CONTINENTAL HOLDINGS, INC. CONSOLIDATED BALANCE SHEETS

(In millions)

At December 31, 2010 2009

Long-term debt 11,434 6,378

Long-term obligations under capital leases 1,036 1,194 Other liabilities and deferred credits: Frequent flyer deferred revenue 3,491 2,720 Postretirement benefit liability 2,344 1,928 Pension liability 1,473 93 Advanced purchase of miles 1,159 1,157

Deferred income taxes 1,585 551

Other 2,704 1,094

12,756 7,450

Liabilities· 2

Liabilities· 3

REMEMBER THE THREE FINANCIAL REPORTING ISSUES

Recognition

Classification

Valuation

Liabilities· 4

RECOGNITION

A liability is an obligation to give an asset to, or perform a service for, another entity in the future.

Remember, liabilities have four characteristics:

Liabilities · 5

LIABILITY CHARACTERISTICS:

1. it is a present obligation for which2. the future sacrifice is measurable3. probable, and $4. is the result of a past transaction. (economic exchange)

Liabilities · 6

CLASSIFICATIONSome companies do not make a distinction, but most distinguish between current and non-current liabilities.

A current liability is one management expects will be paid within the longer of one year or operating cycle.

WINDOW DRESSING

Current assets $200 Current liabilities $150Noncurrent liabilities

350

Noncurrent assets 800 Owners’ equity 500

$1,000 $1,000

Liabilities · 7

Liabilities · 8

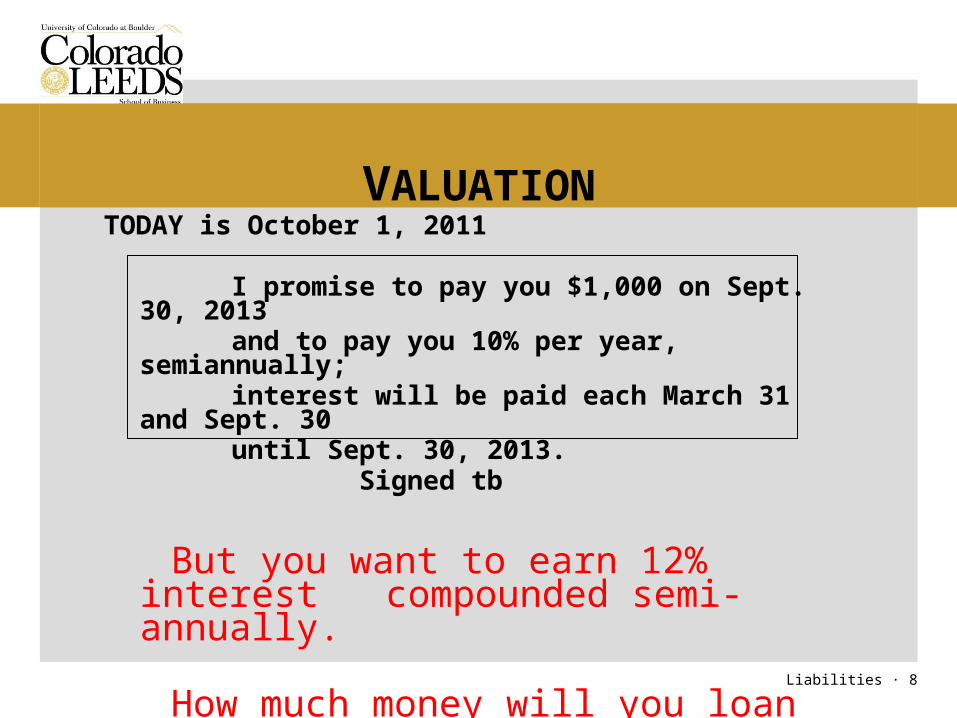

VALUATIONTODAY is October 1, 2011

I promise to pay you $1,000 on Sept. 30, 2013 and to pay you 10% per year, semiannually; interest will be paid each March 31 and Sept. 30 until Sept. 30, 2013. Signed tb

But you want to earn 12% interest compounded semi-annually.

How much money will you loan me?

• . •

PRESENT VALUE OF FUTURE CASH FLOWS

6 mo. 6 mo. 6 mo. 6 mo.|________|________|________|_______|

50 50 50 50 1,000

Using either Excel PV or NPV function will tell you: $ 965.35

· Liabilities 9

PRESENT VALUE OF FUTURE CASH FLOWS

You loan me $965 and I repay you a total of $1,200

What is the difference?

Liabilities· 10

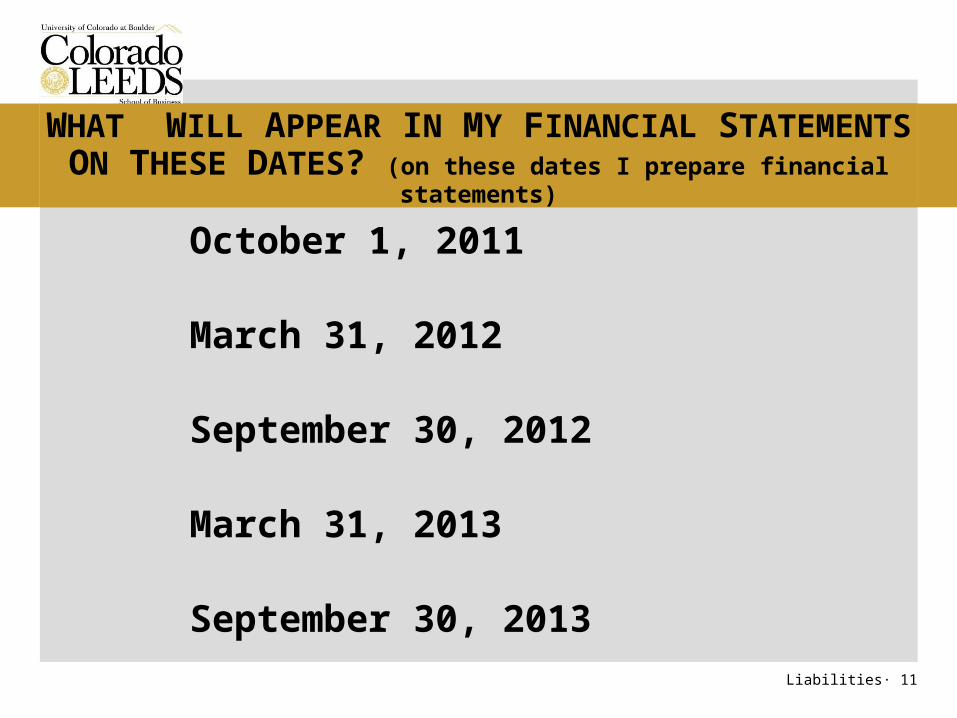

WHAT WILL APPEAR IN MY FINANCIAL STATEMENTS ON THESE DATES? (on these dates I prepare financial statements)

October 1, 2011

March 31, 2012

September 30, 2012

March 31, 2013

September 30, 2013 Liabilities· 11

FAIR VALUE OPTION

Fairly new accounting rule: companies have a choice – do what we did when I borrowed money or show the “fair value” of the debt on their balance sheet.

For example, suppose on Mar. 31, 2012, market interest rates are 16%/year for my company, what is the fair value of my liability and what would appear in my financial statements?

Liabilities· 12

REPORTING, IN THE NOTES, OF FINANCIAL INSTRUMENTS

GAAP requires note disclosure of the fair value of financial instruments, like notes payable, bonds payable, etc., even if the company does not elect to show fair values on the balance sheet.

{keep this in mind when doing the fsa}

Liabilities · 13

Liabilities 14

LEASES: A FINANCIAL REPORTING NIGHTMARE

You fly to San Diego after the fall term is over.

Week 11/2 · 15

LEASES: A FINANCIAL REPORTING NIGHTMARE

Is the car your asset?

Liabilities 16

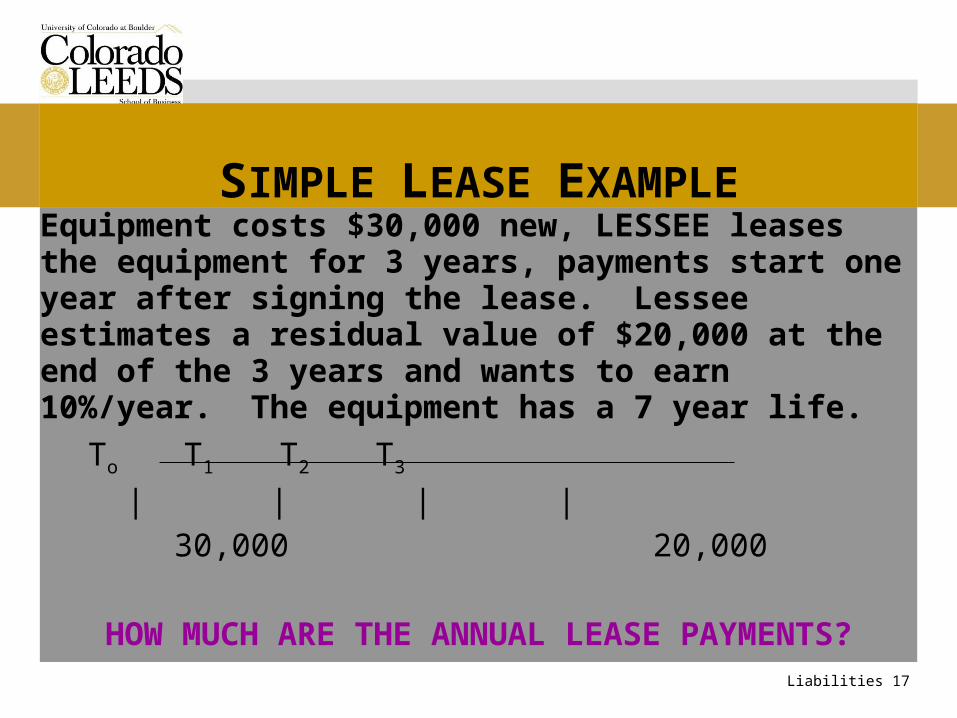

SIMPLE LEASE EXAMPLEEquipment costs $30,000 new, LESSEE leases the equipment for 3 years, payments start one year after signing the lease. Lessee estimates a residual value of $20,000 at the end of the 3 years and wants to earn 10%/year. The equipment has a 7 year life.

To T1 T2 T3

| | | | 30,000 20,000

Liabilities 17

SIMPLE LEASE EXAMPLEEquipment costs $30,000 new, LESSEE leases the equipment for 3 years, payments start one year after signing the lease. Lessee estimates a residual value of $20,000 at the end of the 3 years and wants to earn 10%/year. The equipment has a 7 year life.

To T1 T2 T3

| | | | 30,000 20,000

HOW MUCH ARE THE ANNUAL LEASE PAYMENTS?

Liabilities 18

SIMPLE LEASE EXAMPLEHOW MUCH ARE THE ANNUAL LEASE PAYMENTS?

To T1 T2 T3

| | | | $ 30,000 20,000 ( 15,026) pv $14,974

Liabilities 19

SIMPLE LEASE EXAMPLEHOW MUCH ARE THE ANNUAL LEASE PAYMENTS?

To T1 T2 T3

| | | | $ 30,000 20,000 ( 15,026) pv $14,974

What future annuity gives a pv of $14,974?

Liabilities 20

SIMPLE LEASE EXAMPLEHOW MUCH ARE THE ANNUAL LEASE PAYMENTS?

To T1 T2 T3

| | | | $ 30,000 20,000 ( 15,026) pv $14,974

What future annuity gives a pv of $14,974? Answer: RENT (or payment) = $6,021.

Liabilities 21

SIMPLE LEASE EXAMPLE

If you were the CEO of a publicly traded company

leasing this equipment, would you like to record this

equipment as your asset and liability?

Liabilities 22

SIMPLE LEASE EXAMPLE

Suppose you believed the equipment was not your asset and so you did not record the asset or liability – in financial reporting terminology you would be saying the lease was an “operating lease.”

Liabilities 23

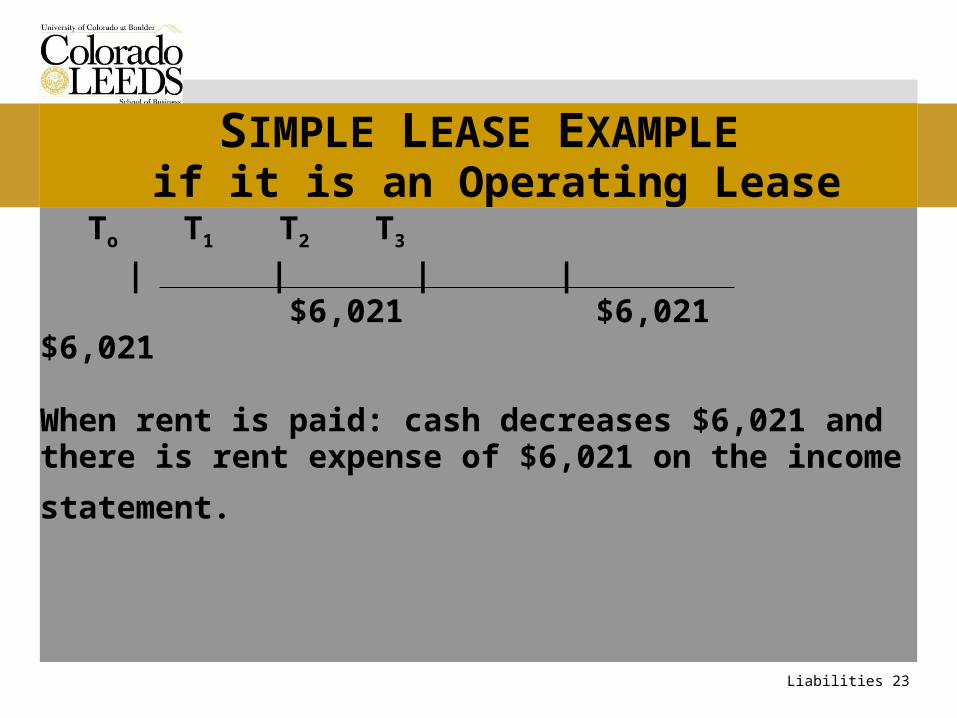

SIMPLE LEASE EXAMPLEif it is an Operating Lease

To T1 T2 T3

| | | | $6,021 $6,021 $6,021

When rent is paid: cash decreases $6,021 and there is rent expense of $6,021 on the income

statement.

Liabilities 24

SIMPLE LEASE EXAMPLEif it is a Capital Lease

Now, suppose you believed the equipment was your asset - you would show the equipment as an asset and also a liability – in reporting terminology you would be saying the lease were a “capital” (or finance) lease.

Liabilities 25

SIMPLE LEASE EXAMPLEif it is a Capital Lease

To T1 T2 T3

| | | | $ 30,000 20,000

At To: When lease is signed: show an asset and liability for the present value of future payments of ($6,021) which would be $14,974. (Assume for now, the residual value was not guaranteed by the lessee.)

ses

Liabilities 26

SIMPLE LEASE EXAMPLEif it is a Capital Lease

Lessee is making 3 payments of $6,021- a total of $18,063; the liability is recorded at $14,974. The difference of $3,089 represents what?

Liabilities 27

SIMPLE LEASE EXAMPLEif it is a Capital Lease

To T1 T2 T3

| | | | $ 30,000 20,000

At T1 - T3 : When each payment is made, part of the payment is interest and part a payment toward the lease liability.

Also, the asset has been used for a year and shouldbe depreciated.

Liabilities 28

COMPARISON OF INCOME STATEMENTSWhich has more expense over the life of the lease:

OPERATING CAPITAL

Liabilities 29

LEASES – REPORTING SUMMARYBalance sheet: a capital lease increases liabilities (and the “worst ones” at that) and increases non-current assets.

Income statement: a capital lease reduces income more in the early years of the lease.

Cash flow statement: Opposite effect! capital lease payments are divided between operating activity and financing activity, while operating leases are operating activities.

Liabilities 30

LEASES – WHICH IS IT?(OR WHAT TO DO TO AVOID capital LEASES)

Can the lessee cancel the lease? no yes

BOO ! CAPITAL LEASE

HURRAY ! OPERATING LEASE

Liabilities 31

LEASES – WHICH IS IT?(OR WHAT TO DO TO AVOID capital LEASES)

Can the lessee cancel the lease? no yes Does title transfer at the lease end? yes BOO !

no CAPITAL LEASE

HURRAY ! OPERATING LEASE

Liabilities 32

LEASES – WHICH IS IT?(OR WHAT TO DO TO AVOID capital LEASES)

Can the lessee cancel the lease? no yes Does title transfer at the lease end? yes BOO !

no CAPITAL Is there a bargain purchase option? yes LEASE

no

HURRAY ! OPERATING LEASE

Liabilities 33

LEASES – WHICH IS IT?(OR WHAT TO DO TO AVOID capital LEASES)

Can the lessee cancel the lease? no yes Does title transfer at the lease end? yes BOO !

no CAPITAL Is there a bargain purchase option? yes LEASE

no Is the lease for ≥ ¾ of the asset’s useful life? yes

no

HURRAY ! OPERATING LEASE

Liabilities 34

LEASES – WHICH IS IT?(OR WHAT TO DO TO AVOID capital LEASES)

Can the lessee cancel the lease? no yes Does title transfer at the lease end? yes BOO !

no CAPITAL Is there a bargain purchase option? yes LEASE

no Is the lease for ≥ ¾ of the asset’s useful life? yes

no Is the PVMLP ≥ 90% assets fair value? yes

no HURRAY ! OPERATING LEASE

· 35

LEASESINTERNATIONAL VIEW

Risks include:• possibility of losses from idle capacity or

technological obsolescence • variations in return because of changing

economic conditions

Rewards are:• the expectation of profitable operation over

the asset’s life• gain from appreciation in value of residual

value.

· 36

IAS 17 stipulates that if any one of these criteria are met, substantially all of the risks or rewards of ownership are

deemed to have been transferred:1. the lease transfers ownership of the asset to the

lessee by the end of the lease term; 2. the lessee has the option to purchase the asset at a

price which is expected to be sufficiently lower than fair value at the date the option becomes exercisable that, at the inception of the lease, it is reasonably certain that the option will be exercised;

3. the lease term is for the major part of the economic life of the asset, even if title is not transferred;

4. at the inception of the lease, the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset; and

5. leased assets are of a specialized nature such that only the lessee can use them without major modifications being made.

· 37

Further indicators suggesting that a lease might be properly considered to be a finance lease are:

6. in the lessee can cancel the lease, the lessor’s losses associated with the lease are to be borne by the lessee,

7. gains or losses resulting from fluctuations in the fair value of the residual will accrue to the lessee, and

8. the lessee has the ability to continue the lease for a supplementary term at a rent that is substantially lower than market rent (i.e., there is a bargain rental option).

Liabilities 38

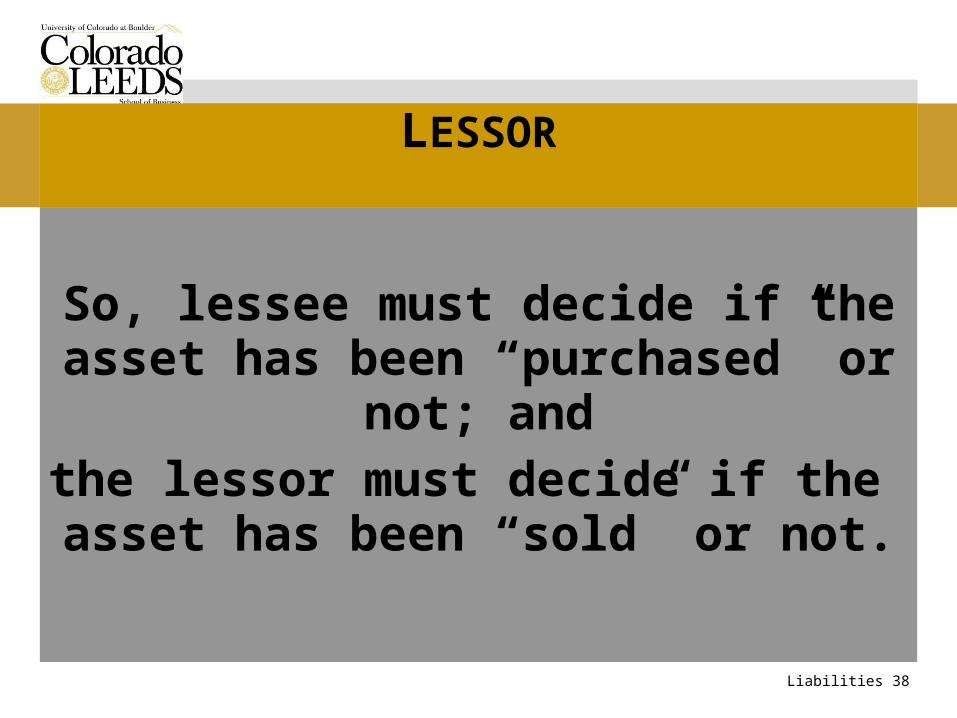

LESSOR

So, lessee must decide if the asset has been “purchased” or

not; andthe lessor must decide if the asset has been “sold” or not.

Liabilities 39

LESSORTo treat the lease as a “sale”

At least one of the 4 criteria must be met:

title transfer,bargain purchase option,

lease ≥ 75% of economic life,PVMLP ≥ 90% assets fair value

ANDlessor must believe lessee will make

payments & lessor must not have any material uncertain costs related to the

lease.

Liabilities 40

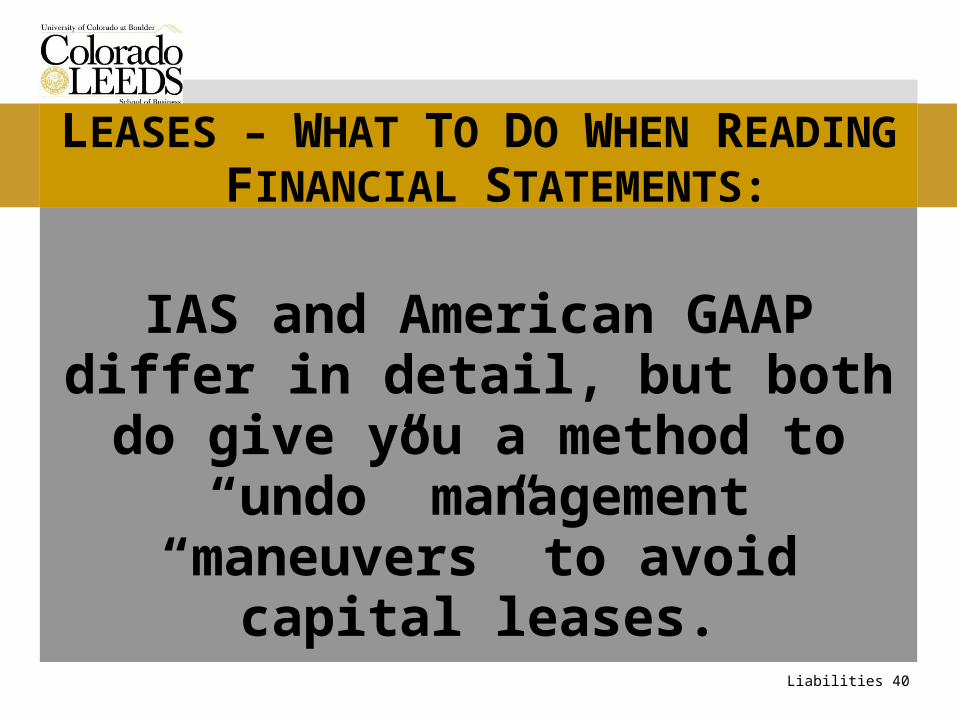

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

IAS and American GAAP differ in detail, but both do

give you a method to “undo” management “maneuvers” to

avoid capital leases.

Liabilities 41

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

Using Sony Corporation as an example.

•http://www.sony.net/SonyInfo/IR/financial/ar/2006/index.html

Liabilities 42

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

Sony CorporationBalance Sheet(in $ million)

{original}

Current assets 3,218 Current liabilities 27,352PP&E 11,868 Long-term liabilities 35,613

Other assets 75,579 Owners’ equity 27,700

Total assets 90,665 Total L. & OE 90,665

es

Liabilities 43

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

Sony CorporationBalance Sheet(in $ million)

Current assets 3,218 Current liabilities ??PP&E ?? Long-term liabilities ??

Other assets 75,579 Owners’ equity 27,700

Total assets Total L. & OE

Liabilities 44

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

s

Liabilities 45

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

in $ millionYear ending CAPITAL OPERATINGMarch 31: LEASES LEASE

2007 157 4062008 82 2972009 46 2272010 26 1392011 18 98

Later years 40 504Total 369 1,671less interest (42) Present value 327 less current portion (145) Long-term portion 182

Liabilities 46

LEASES – WHAT TO DO WHEN READING FINANCIAL STATEMENTS:

Sony CorporationBalance Sheet(in $ million)

{revised}

Current assets 3,218 Current liabilities ??PP&E ?? Long-term liabilities ??

Other assets 75,579 Owners’ equity 27,700

Total assets Total L. & OE

Liabilities 47

LEASES

QUESTIONS?