Languages

Pages

Legal

www.powerexindia.com

Session 3

Advance Metering Infrastructure, Power Trading and Cloud Computing

Transmission, Distribution and Metering India

(Enabling Smart Grid & Smart Metering)

Nov 10, 2010

Mrs. Rupa Devi Singh, MD & CEO

Power Exchange India Limited

www.powerexindia.com

Power Exchange India Limited- Voluntary but Institutionally promoted

EQUITY PARTNERSCentral Government Entities State Government Entities Private power producers

Power Finance Corporation Limited

GUVNL JSW Energy Limited

MPPTCL Tata Power

WBSEDCL GMR Energy Limited

The foremost power sector organizations in India, partnering for a vibrant power market

PROMOTERSNational Stock Exchange

(NSE ) National Commodity and Derivatives Exchange

(NCDEX)

PXIL leverages on promoter and shareholder experience :- NSE -largest stock exchange in India and 3rd largest in the world

- Govt entities discharging the Universal service obligation - Leading Private producers in the country

www.powerexindia.com

Indian Power Sector

One of the largest interconnected power systems in the worldGeneration Capacity of 164,836 MW(Sep 2010)-800,000 GW by 2030Energy deficit of about -9.6% and peak demand deficit of -10.5% (Sep 2010)Predominant focus on fossil fuels, especially coal

Sour

ce: C

EA, N

LDC

*Defi

cit n

umbe

rs fo

r Jan

201

0

88.00%

6.00%

4.00%

2.00%Types of Transactions (Sep 2010)

Long Term PPAs

Bilateral Short Term

Balancing

PXs

www.powerexindia.com

Indian Power Sector -Installed Capacity

Installed Capacity as on September 2010 Installed Capacity-Fuel Mix

Source- CEA

Installed Capacity MWCoal 87944Gas 17374Diesel 1199Nuclear 4560Hydro 37329RES 16429Total 164835

www.powerexindia.com

Indian Power Sector

Demand – Supply Summary Forecasts

Xth Plan 2006-07

XIth Plan 2011-12

XIIth Plan 2016-17

690969

1392

624821

1098

Energy Requirements (in BU)Energy Availability* (in BU)

Xth Plan 2006-07

XIth Plan 2011-12

XIIth Plan 2016-17

100

153

218

96115

154

Peak Load (in GW)Peak Served* (in GW)

Even with higher rates (6% y-o-y) of capacity addition and energy generation, India would continue to remain a power deficit country

Source: CEA *Extrapolated by PXIL

www.powerexindia.com

India’s Projected Energy & Capacity requirements

XI Plan XII Plan XIII Plan XIV Plan XV Plan0

200

400

600

800

1000

1200

67 86119

150203220

306

425

575

778

78 104151

197

275233

337

488

685

960

8% Growth Rate

Cummulative Capacity @8% Growth rate

9% Growth Rate

Cummulative Capacity @9% Growth rate

GW

2007-122027-32

Immense task ahead in terms of capacity addition requirements

www.powerexindia.com

ROLE AND IMPACT OF POWER EXCHANGES IN ENERGY MARKET DEVELOPMENT

www.powerexindia.com

Electricity Act 2003- transition to a market

Development of a multi-buyer multi-seller market in powerCompulsory Unbundling of utilitiesComplete De-licensing of generation “Trading” of Electricity – a licensed activity

Provides Consumer level choice of supplierSeparation of “transmission ownership” and “system operation”Universal Open Access to transmission networks for all consumers over 1 MW

Robust Policy framework providing ground rules for competition National Electricity Policy detailing roadmap for development of markets - PXs Mandated Competitive procurement of power by uitilitiesGlobal competitive bidding for projects in transmission

A proactive approach for development of a market in renewables

Committed the Nation to Development of a Vibrant Market in Electricity

www.powerexindia.com

Indian Power Sector – Post Reforms Transition

MonopolyGovernment Ownership (Vertically integrated)

Public Corporation

Private Corporation

Purchasing Agency

Commercialization

Corporatization

Privatization

Competition

Wholesale Competition Retail Competition

Introduction of

Power Exchanges

www.powerexindia.com

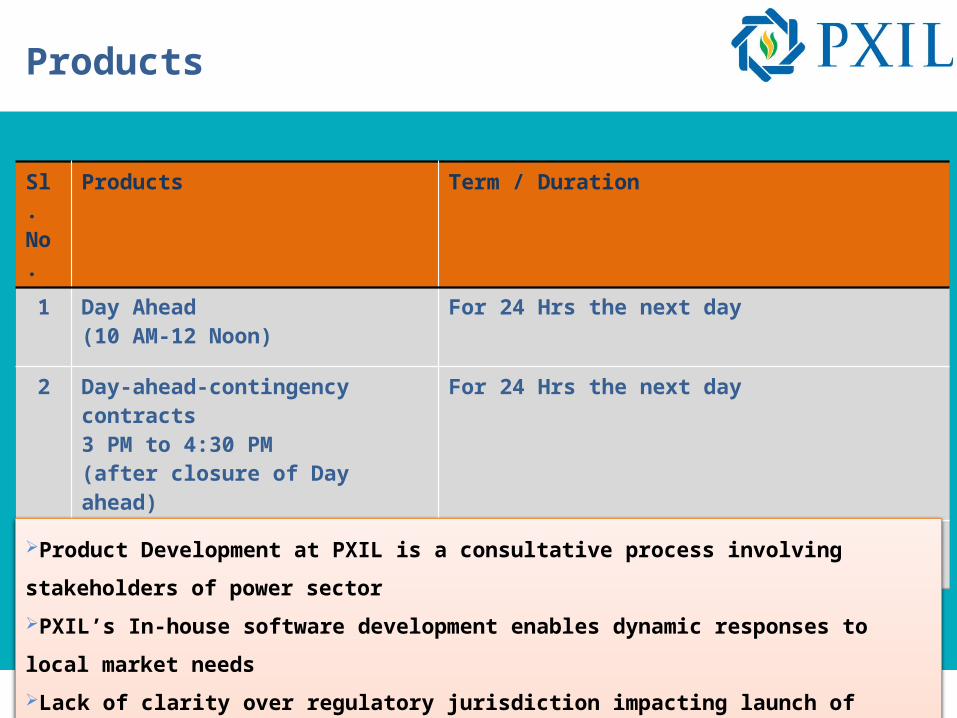

Products

Sl. No.

Products Term / Duration

1 Day Ahead (10 AM-12 Noon)

For 24 Hrs the next day

2 Day-ahead-contingency contracts 3 PM to 4:30 PM(after closure of Day ahead)

For 24 Hrs the next day

3 Weekly contracts For pre-defined calendar weeks upto a month ahead

Product Development at PXIL is a consultative process involving stakeholders of power sector

PXIL’s In-house software development enables dynamic responses to local market needs

Lack of clarity over regulatory jurisdiction impacting launch of forwards and futures

www.powerexindia.com

Volumes Transacted

Volumes on Exchanges have shown an increasing trend as percentage of total generation

Proactive approach from the regulator and efficient grid management by the system operator

Absence of Universal Service Obligation on Utilities resulting in reduced demand

Dec-09 Jan-10 Mar-10 May-10 Jun-10 Aug-10 Sep-100

200

400

600

800

1000

1200

1400

1600

Increased Transactions Through Power Exchanges

Volumes Transacted through PXs 0 1 2 3 4 5 6 7

0.00200.00400.00600.00800.00

1000.001200.001400.001600.001800.00

Cumulative Monthly Transacted Volumes

20092010

Month of FY 2010-11

Mill

ion

Uni

ts

www.powerexindia.com

Prices

Average Price of electricity Traded over Exchanges

2008 Rs. 7.57/kWh* 2009 Rs. 5.73/kWh

Traded in OTC market 2008 Rs. 7.04/kWh 2009 Rs. 6.41/kWh

Prices in 2010 exhibit a further declining trend.

* Exchanges were in operation only during the last three quarters of the year

Efficient Price Discovery leads to Lower prices on exchange

Softer Prices at the exchange cast a spill over effect on the OTC market

Average Daily Prices exhibit a declining trend

2009

2010

Days of the year

Ave

rage

Dai

ly P

rice

(Rs.

/kW

h)

www.powerexindia.com

Participation

29 States More than 300 participantsMore than 400 portfoliosMaximum Volumes Transacted

Day Ahead Market 65.5 MUs on 21st Aug 2010Term Ahead (weekly) Market 22 MUs on for the delivery week 19/07/2010 to 25/07/2010

Access – Easy, Electronic and Efficient

Information Dissemination – Fast and reliable

Evolution of the market from utility based to industrial consumers oriented

www.powerexindia.com

Services

Information DisseminationRegion-wise hourly price dataCongestion occurrence and detailsClose interaction with System Operator

Capacity Building – Power Markets Centre of ExcellencePower Markets Leadership Programme

Jointly organized with premier institutes like IIM Ahmedabad/IIT Mumbai More than 150 participants

Power Markets Certification Programme Jointly organized with NPTI/ASCI/ISPE More than 50 participants

PXIL’s two pronged strategy for services

To be the thought leaders in the Indian Power Markets

Knowledge sharing amongst stakeholders through continuous engagement

www.powerexindia.com

Achievements of Exchanges

Lowered cost of participation as well as transaction costIncreased participation with Industrial consumers, small captivesIncreased depth and liquidityAvailability of different types of membership to suit the context

Lowered the minimum bid from 1 MW to 0.1 to 0.01 MWIncreased liquidityIncreased participation

Introduced Professional Clearing Membership as a categoryMembership to funding agencies like PFC to provide funds for bids

New Bidding MethodologyBidding in week ahead market which is quasi – continuous to suit Indian context

www.powerexindia.com

Impact of Power Exchanges

AccessUtilitiesIndustrial ConsumersOpen Access ConsumersCaptive sellers

Transparency & EfficiencyBetter price discoverySpill over effect on OTC market

Demand ManagementFreedom to choose amongst products for better portfolio management

PXs have demonstrated that National market for electricity is feasible

PXs have reached their second stage of development to be mandated platforms

Exchanges have made the Open Access Dream; A Reality

www.powerexindia.com

KEY ISSUES AND CHALLENGES

www.powerexindia.com

Electricity Act 2003- transition to a market

Compulsory Unbundling of utilities

Complete De-licensing of generation

Separation of “transmission ownership” and “system operation”

Universal Open Access to transmission networks

Consumer level choice of supplier

Development of a multi-buyer multi-seller market in power

The intent and the ethos of EA 2003 towards creating competition at the utility level

as well as the end customer level is still elusive

www.powerexindia.com

Key issues and Challenges-Multiple State level markets

Mixed response to national legislationMultiple States and JurisdictionsMany still vertically integratedIsolated nearly self sufficient marketsOpen Access to transmission lines controlled by State Transmission Utilities Limited Inter - connector capacityInter-connector capacities not with the exchanges

Exchanges and OTC compete for capacity

www.powerexindia.com

Creating Markets

Historically illiquid market Planned dependence on PPA-only 8% of electricity produced traded through short term marketTrading of electricity only a few years old A stable Day Ahead spot market on the Exchange

Pricing Challenges Long term price view yet to emergeDeclining trend in merchant power prices-with near zero cost of avoidable loadExposure to international coal prices-consumer level pricing shocks ?

Sudden Unrestrained growthHigh capacity addition might lead to excess supply or stranding Issues on fuel availability /fuel mix may emerge in the long run

www.powerexindia.com

Transmission Pricing

Infrastructure5 Electrical Regions, More than 25 Control areasTransmission constraints across regions

Transmission pricing based on tenure of transactionsLong Term – More than 25 years

Transmission access given for specific seller and buyer Transmission pricing based on cost of asset and socialized over all beneficiaries in the Region

Short Term – Upto 3 months Transmission access given for each transaction separately for a specific seller and buyer pair Transmission pricing arrived at as a percentage of long term transmission pricing Earnings used to reduce the cost of asset for long term transmission consumers

Day-Ahead Spot Market – For the next day only Transmission access for trades through Power Exchanges - Collective transactions Point of connection tariff – equal price for connection from anywhere in India

Balancing – Real time Power system frequency based pricing Penalty or reward based on deviation from schedule in any 15 min time block

www.powerexindia.com

Transmission Access

Priority to Transmission Open Access given to Long term, followed by Short term and then power exchanges

Based on timing of application for Short Term

Congestion charge applied only on transactions happening through PXs

Different Products treated differentlyCollective transactions for DAS

FCFS for Term Ahead (Weekly) Product

www.powerexindia.com

FUTURE OUTLOOK

www.powerexindia.com

Renewable Energy CertificatesMarket based instruments for trade between the Eligible Generating firms and Entities carrying Renewable Obligation Initially Non-transferable contracts, mandated to be traded on PXs

Energy Efficiency CertificatesMarket based mechanism to promote energy efficiency in 9 identified industrial sectorsFirms maintaining higher efficiency than set Targets would sell certificates whereas firms with lower efficiency would need to buy

Industrial consumers also carry renewable purchase obligation

Mainstreaming Environmental Products

PXs evolve from being voluntary to mandated platformsPXs evolve from being voluntary to mandated platforms

www.powerexindia.com

Delivery Based ForwardsMonthly Contracts CERC has initiated the process to develop the product attributes to suit the market For delivery contract

Ancillary Services ContractConcept paper floated by NLDC

Financial Products Envisaged in future

Longer Tenure Products

www.powerexindia.com

Future Outlook - PXIL

PXIL remains committed to delivering to its participants contextual products and services on the following principles

AccessibilityAffordabilityReliabilityQuality Availability

www.powerexindia.com

THANK YOUAddress POWER EXCHANGE INDIA LIMITED

"B" Wing, 3rd Floor, Exchange PlazaBandra Kurla Complex, Bandra (E)Mumbai - 400051, India.

Email [email protected]

Website www.powerexindia.com

Telephone No:Fax No:

+91 22 2653 0500+91 22 2659 8397

Contact Details

Top Related