Languages

Pages

Legal

8/6/2019 Will Equities Stay Resilient as the Economy Slows?

http://slidepdf.com/reader/full/will-equities-stay-resilient-as-the-economy-slows 1/[email protected] Fundamental and technical analysis, but mostly judgment 1

MosaicGlobalPerspectivesFundamen ta l and Techn i ca l Ana l y s i s , bu t Mos t l y J udgmen t

M o s a i c M a r k e t R e s e a r c h , L L C

K e v i n A . L e n o x , C F A

W e b s i t e : M o s a i c m a r k e t r e s e a r c h . c o m

E m a i l : K l e n o x @ M o s a i c m a r k e t r e s e a r c h . c o m

WillEquitiesStayResilientastheEconomySlows?

Althoughthecurrentsoftpatchineconomicgrowthiswidelyexpectedtobetransitory,ourmostimportantmetricsformonitoringfinancialconditionsandleadingindicatorssuggestthattheequitymarketsarevulnerable.EventhoughtheS&P500justsetapost-recoveryhighlastFriday,there’sbeenapronouncedflight-to-qualitythemeoverthepastfourtofiveweacrossmultipleassetclassesthattypicallyprecedeanegativereturnenvironmentforequities.OurassessmentisthatthecurrentsynchronizedweaknessinU.S.andglobalgrowthwillprovetobesomewhatmoreprotractedthancurrentconsensestimates.However,globalinterbanklendingandswapspreadsarenotyetreflectinganincreaseinsystemicstresswithinfinancialsystem.Atthispoint,theweightoftheevidenceisprovidingaclearsignaltoreduceportfoliorisklevels.Wehave

highlevelofconvictionthatportfoliosshouldbetacticallyunderweightinequities,especiallysmallcap,andhighyield.

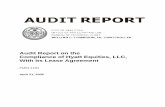

WefindthattheISMManufacturingandISMServicesPMIscanoffervaluableinsightregardingthecurrentstageofthebusinesscycle.ThemoreeconomicallysensitiveISMManufacturingPMIhasremainedabove50for20consecutivemontandnearhistoricallypeaklevelsover60forthefourthstraightmonth.AccordingtoarecentstudybyRBCCapitalMarketstheS&P500hasrallied21.1percentintheyearleadinguptotheISMreaching60,andonly6.5percentoverthesubsequ12-monthperiod.Whilethere’snothingmagicalaboutreadingsover60thatshouldpromptinvestorstoimmediatelygetdefensive,itdoesmeanthatinvestorsneedtobekeenlyawarethattherisk/returnprofileislessattractiveatthispointofthcycle.Forexample,thesharpdeclineinboththeJPMorganGlobalServicesPMIandtheU.S.ISMServicesneworderscomponenthasbeenconsistentwithpriorperiodsofslowereconomicgrowththatpersistsforseveralmonths.OurpremisethattheISMbusinesscycleindicatoriscurrentlyintheso-calledpeak-to-50stage.Thisisveryconsistentwiththerotationawayfromcyclicalstockstomoredefensivestockswithabove-averagedividendyields.

Investorshadbegunrotatingfromeconomicallysensitivecyclicalstockstomoredefensiveandhigherdividendyieldingequitiesinmid-February,butthemomentumhasacceleratedoverthepastfiveweeks.Despitestrongfirstquarterearningresults,particularlycyclicals,investorsareclearlypositioningforamorechallengingeconomicenvironment.WefinditnoteworthythatwhileGDPestimatesarebeingratcheteddownfor2011and2012,S&P500earningsaremostlybeingrevisedhigherduetothestronger-than-expectedfirstquarterresults.Equitiesarepoisedtofaceadditionalsellingpressurwhenearningsforsubsequentquartersarerevisedtoaccountfortheweakeningeconomiclandscape.

Pleasesee ,Page2

10

20

30

40

50

60

70

80

90

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2005 2006 2007 2008 2009 2010 2011

RealGDPandISMNewOrders

Real GDP (LHS) ISM Mfg. NO (RHS) ISM Non-Mfg. NO (RHS)

10

20

30

40

50

60

70

80

90

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

2005 2006 2007 2008 2009 2010 2011

RealGDPandI SMNewOrders

Real GDP (LHS) ISM Mfg. New Orders (RHS) ISM Non-Mfg. New Orders (RHS)

Da t e : 5 / 0 9 / 2 0 1

S o u r c e : U . S . B E A , I n s t i t u t e f o r S u p p l y M a n a g e m e n t

8/6/2019 Will Equities Stay Resilient as the Economy Slows?

http://slidepdf.com/reader/full/will-equities-stay-resilient-as-the-economy-slows 2/[email protected] Fundamental and technical analysis, but mostly judgment 2

ThecreditmarketshavehistoricallybeenareliableleadingindicatorofimportantinflectionpointsintheS&P500.Inparticular,wemonitorseveraldifferentgaugesofOASandCDScreditspreadsbetweenhighyieldandinvestmentgradecorporatebonds.Inaggregate,thesespreadshavecontinuedtowidensincemid-February,andthere’sadistinctflight-to-qualitytrendthatshouldmakeequityinvestorstakenote.

Thebull-flatteningtrendofthe2s10scurveisaconfirming,butoftendelayedindicatoroffutureeconomicweakness.Interestingly,the10-yeargovernmentbondyieldshavefallenforalloftheG-7countriesoverthepastfourweeks.Theweaknessinthebankingindustryappearstobeaconfirmingsignalthatthecurvewillcontinuetoflatten.Also,theGermanBundcurveisinabear-flatteningpatternthatpointstowardagrowingthreatofstagflationintheEurozone.

Thepriceofcopperpeakedinmid-February,andclosedthisweekbelowthe200-daymovingaverage.Weviewcopperaskeygaugeofglobalgrowthtrends,andithasbeenaconspicuouslaggardastheS&P500reachedapost-recoveryhighlaFriday.Ourbasketofcopperproducingstockshavebeenunderperformingtheprimaryglobalequityindicesoverthepastweeks,whilethemajorstockmarketindicesforcommodityproducingcountriessuchasAustralia,Brazil,CanadaandRushaveallfollowedaverysimilarpatternduringthissameperiod.Inourview,thisdataisconsistentwithamoreprotractedperiodofglobalgrowththatwilllikelyresultinfurtherdownwardrevisionstoglobalGDPestimates.

Thesteeplossesthisweekinbothcommoditiesandequitieshelpedtriggerinvestorstoreducetheirexposuretomorerisk

currenciesliketheAussie.Inaddition,therewasahugespeculativepositionintheEurobasedontheexpectationofhigheinterestratedifferentials.Intheeventofanunexpectedsurgeofriskaversion,adisorderlyunwindingofthecrowdeddollafundedcarrytradewouldcreateaddedsellingpressureforrisk-orientedassetclasses.

Althoughthebalanceofrisksaretiltedtothedownside,ourindicatorsareportrayinganorderlyadjustmenttoalower-thanconsensustrajectoryofeconomicgrowth.Thestrongdegreeofcorrelationamongleadingindicatorsandcross-marketanalysisprovidesahighdegreeofconfidencethatinvestorsshouldbetacticallyunderweightinequitiesandhighyieldboSmallcapstocksappearparticularlyvulnerablebasedonthecurrentstageofthebusinesscycle,valuationanddeterioratibreadth.

S l o w i n g E c o n o m y , C o n t i n u e d

D i s c l a i m e r Allopinions expressedare solely theopinionof theauthor.You should nottreat anyopinionexpressed asa specificinducementto makea particuinvestmentorfollowaparticularstrategy,butonlytheexpressionofanopinion.Suchopinionsarebaseduponinformationtheauthorconsidersreliable,bushouldnotberelieduponassuch.

Theauthorisnotunderanyobligationtoupdateorcorrectanyinformationavailableinthisreport.Theauthormaybeactivelyinvolvedinsecuritiesdiscussherein.Also,the opinionsexpressedmaybe short-term innatureand aresubject tochangewithoutnotice. Past performanceis notindicativeof futresults.

Youshouldbeawareoftherealriskoflossinfollowinganystrategyorinvestmentdiscussedinthisreport.Strategiesorinvestmentsdiscussedmayfluctuinpriceorvalue.Investorsmaygetbacklessthaninvested.Investmentsorstrategiesmentionedinthisreportmaynotbesuitableforyou.Thismaterialdnottakeintoaccountyourparticularinvestmentobjectives,financialsituationorneedsandisnotintendedasrecommendationsappropriateforyou.

Youmustmakeanindependentdecisionregardinginvestmentsorstrategiesmentionedinthisreport.Beforeactingonanyinformation,youshouldconswhetheritissuitableforyourparticularcircumstancesandstronglyconsiderseekingadvicefromyourownfinancialorinvestmentadvisor.

Top Related