Languages

Pages

Legal

Emerging Low-cost Mid-tier Zinc Producer

June 2015

TSX-V: IZN

This presentation contains certain statements that may be deemed "forward-looking statements". All statements in thispresentation, other than statements of historical fact, that address future production, reserve potential, explorationdrilling, exploitation activities and events or developments that the Company expects to occur, are forward-lookingstatements. Forward-looking statements are statements that are not historical facts and are generally, but not always,identified by the words "expects", "plans" "anticipates", "believes", "intends", "estimates", "projects", "potential" andsimilar expressions, or that events or conditions "will", "would", "may", "could" or "should" occur. Information inferredfrom the interpretation of drilling results and information concerning mineral resource estimates may also be deemed tobe forward-looking statements, as it constitutes a prediction of what might be found to be present when and if a projectis actually developed.

Although the Company believes the expectations expressed in such forward-looking statements are based onreasonable assumptions, such statements are not guarantees of future performance and actual results may differmaterially from those in the forward-looking statements. Factors that could cause the actual results to differ materiallyfrom those in forward-looking statements include market prices, exploitation and exploration successes, and continuedavailability of capital and financing, and general economic, market or business conditions. Investors are cautioned thatany such statements are not guarantees of future performance and actual results or developments may differ materiallyfrom those projected in the forward-looking statements. Forward-looking statements are based on the beliefs, estimatesand opinions of the Company's management on the date the statements are made. The Company undertakes noobligation to update these forward-looking statements in the event that management's beliefs, estimates or opinions, orother factors, should change.

Chris Staargaard, P.Geo., a Qualified Person as defined in NI43-101, has approved the technical content of thispresentation.

2

Cautionary Statement

TSX-V: IZN

InZinc MiningEmerging Low-Cost Mid-Tier Zinc Producer

100% interest in the West Desert zinc-iron-copper project in Utah

o One of the best located and larger undeveloped zinc resources

Excellent results from updated West Desert PEA (April 2014)

o One of best returning zinc projects within peer group

o Simple, conventional mining and processing

o Significant upside potential

Drill program first step in pre-feasibility

Ready for the metal cycle

3

TSX-V: IZN

Issued and Outstanding 72,205,419Warrants 4,866,819Options 2,650,000

Fully Diluted 79,722,238

Institutional Shareholders 17.6%Management/Board (fully diluted) 17.8%

Working Capital C$1.05 millionShare Price (6-8-15) C$0.11Market Cap C$7.9 million

InZinc MiningCapital Structure

4

TSX-V: IZN

Chris Staargaard, M.Sc. (Geochemistry), P.GeoPresident, CEO, Director35+ years worldwide exploration experience with Kennecott, Kidd Creek, Homestake and as consultant to numerous public companies and investment dealers; with InZinc since inception in 2002

Ken Puchlik, M.Sc. (Geology)Utah-based Consultant30+ years experience with Freeport, Independence, Cyprus-Amax and Pegasus Gold, including development of 2.4 Moz Kubaka mine; Director of Utah Geological Survey; Geology Manager for Sumitomo at Pogo Mine

Joyce Musial, B.Sc. (Hons) in GeologyCorporate Communications25+ years experience in resource sector with focus on investor relations, communication, corporate development, and community, governmental & aboriginal relations

Steve Vanry, C.F.A, C.I.M.CFO17 years experience in strategic planning, regulatory compliance and financial reporting with publicly traded natural resource companies

Kerry Curtis, B.Sc. (Geology), P.Geo.Chairman, Director Chair of Compensation Committee30 years experience – base and precious metals, exploration through feasibility and development financing; former CEO of Cumberland Resources which was acquired by Agnico Eagle for $730 million

Wayne Hubert, B.Sc. (Eng), MBA Utah-based Director Chair of Audit Committee20+ years experience mining corporate development, initially with Meridian Gold and then as CEO with Andean Resources which was acquired by Goldcorp for US$3.5 billion

Louis Montpellier, L.L.B.Director Chair of Governance Committee30 years specializing in international mining law and finance; former VP – Corporate Development and Counsel for Exeter Resource Corp.

InZinc Mining Ltd.Board Focused on Delivering Value

5

TSX-V: IZN

West Desert Project Excellent Jurisdiction – Surrounded by Infrastructure

Utah business and mining friendly

Mine permitting straightforward and efficient

Easy logistics

Road access and grid power

Multiple transcontinental rail networks within 90 km

Interstate gas pipeline within 90 km

Multiple US ports provide access to global shipping networks

6

TSX-V: IZN

UTAH

BINGHAM COPPER

WESTDESERT

160 km southwest of Salt Lake City, Utah

Paved road to within 30 km – all weather gravel roads to property

Railheads within 90 km

Grid power at site

Two major power plants within 90 km

Natural gas pipeline within 90 km

Close to Bingham Copper – one of the world’s most prolific copper mines contributing $1.2B to Utah’s economy yearly for 100+ years

Utah is a politically stable, business friendly jurisdiction in which mines are being permitted

West Desert Project The Right Address

7

NEVADA

TSX-V: IZN

West Desert Project Low Project Execution Risk

No major towns or communities in close proximity to the project

Resources are almost entirely contained on private land

InZinc owns water rights – two water wells on property

All exploration permits, bonds in place to continue work

8

WEST DESERT DEPOSIT

TSX-V: IZN

West Desert Project2014 Independent PEA Highlights

1.6 billion lbs LOM zinc production

Important by-products include iron, copper, indium

After tax economics:o 23% IRR

o $258M NPV8

o $377M NPV5

14.8 year mine life

3.7 year payback

$247M initial CAPEX

9

Note 1: 100% equity basis; US$; zinc = $1 /lb, copper = $3 /lb, iron = $105 /t, indium = $600 /kg, silver = $21 /oz, gold = $1,300 /oz.

Note 2: The PEA is considered preliminary in nature. It includes Inferred mineral resources that are considered too speculative to have the economic considerations applied that would enable classification as mineral reserves. There is no certainty that the conclusions within the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

TSX-V: IZN

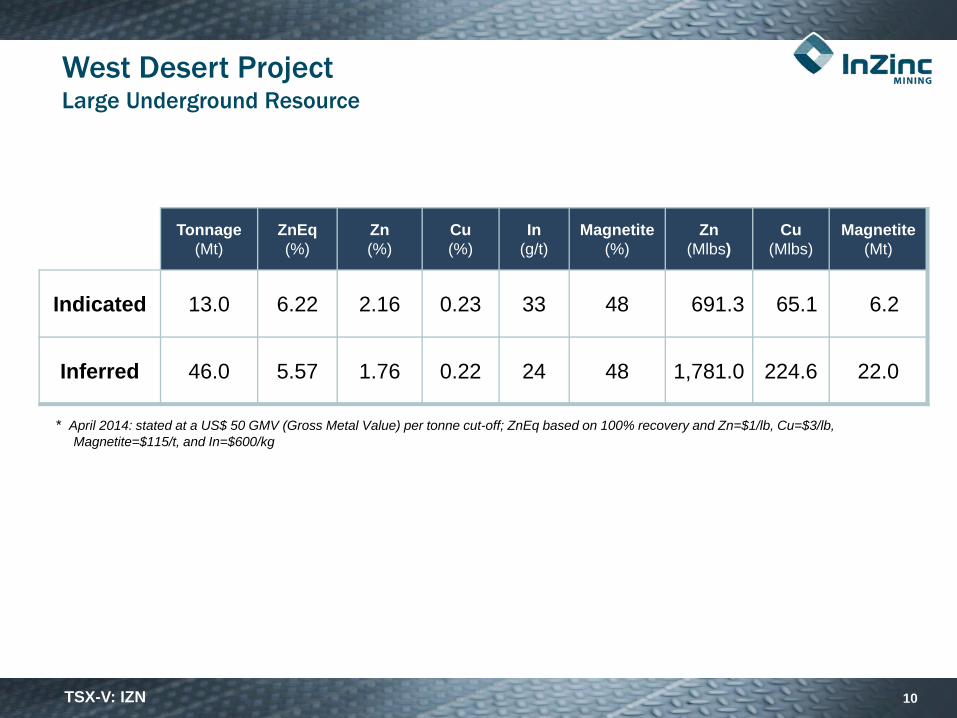

West Desert ProjectLarge Underground Resource

10

Tonnage(Mt)

ZnEq(%)

Zn(%)

Cu(%)

In(g/t)

Magnetite(%)

Zn(Mlbs)

Cu(Mlbs)

Magnetite(Mt)

Indicated 13.0 6.22 2.16 0.23 33 48 691.3 65.1 6.2

Inferred 46.0 5.57 1.76 0.22 24 48 1,781.0 224.6 22.0

* April 2014: stated at a US$ 50 GMV (Gross Metal Value) per tonne cut-off; ZnEq based on 100% recovery and Zn=$1/lb, Cu=$3/lb, Magnetite=$115/t, and In=$600/kg

TSX-V: IZN

West Desert ProjectAmenable to Low Cost, Bulk Underground Mining

Initial mining rate of 5,000 tpd

Increases to 6,500 tpd in year 3

Longhole open stoping

Access via two ramps

Conveyor haulage is cost effective and flexible

Resource open for expansion

11

Proposed stopes in yellow

oxideresource

Underground Resource

Indicated 13 Mt at 6.2% ZnEqInferred 46 Mt at 5.6% ZnEq

W E

100

200

300

400

500

600

700m depth

TSX-V: IZN 12

West Desert ProjectSimple Conventional Processing Produces Three Clean Concentrates

Low IntensityMagnetic Separation

Copper Flotation

Zinc FlotationTailings

97% recovery63% Fev low SiO2, P2O5

74% recovery29% Cupayable Au, Agno penalties

92% recovery55% Znhigh indiumno penalties

IronConcentrate

CopperConcentrate

Zinc Concentrate

U/G Crushing

Surface SAG Mill

50% of milled tonnage

base metals retained in tails:grades double

CleanNon-acid generating

TSX-V: IZN

Revenue Distributionat PEA Metal Prices

West Desert ProjectMultiple Projected Payable Metals

13

Commodity Units Annual LOM

Zinc M lbs 107.9 1,594.3

Magnetite (iron) M t 1.0 14.5

Copper M lbs 9.9 146.7

Indium t 38.3 566.1

Gold K oz 7.6 113.0

Silver K oz 76.9 1,137.0

Zinc42%

Copper15%

Indium12%

Magnetite25%

Gold5%

Silver1%

TSX-V: IZN 14

West Desert ProjectCash Costs (C1) in the Lowest 5% of Global Production

C1 - Direct Cash Cost ($0.04)/lb

C2 - Production Cost $0.45/lb

C3 - Fully Allocated Cost $0.50/lb

C1 Cost ($/lb payable Zn)

Wes

tDes

ert

(after Brook Hunt / Wood Mackenzie, Lundin Mining, Jan 2014)

TSX-V: IZN 15

West Desert ProjectWell Leveraged to Zinc Price

ZincPrice($/lb)

Pre-Tax (M $) After-Tax (M $)Payback (Years)NPV (5%) NPV (8%) IRR NPV (5%) NPV (8%) IRR

0.80 312 208 19% 238 146 17% 4.9

1.00 507 357 27% 377 258 23% 3.7

1.20 693 506 34% 507 363 29% 3.0

Note: Base case in bold; US$

TSX-V: IZN

West Desert ProjectSignificant Upside Potential

16

Expand higher grade, zinc-rich resource in three directions

Add recoverable zinc and copper at depth - within the current magnetite resource

Discover additional mineralized zones

Optimize transportation costs for iron concentrate (magnetite)

Reduce cost of tailings facility

Evaluate recovery of molybdenum in deeper parts of deposit

Evaluate near surface oxide zinc mineralization

TSX-V: IZN

OPEN

0m surface

100

200

300

400

500

600

700m depth

OPEN

W E

West Desert ProjectOpen for Expansion and New Discoveries

17

Historic 2.7M ozsilver mine

3.05m intercept @ 7.65% Zn, 3.5% Cu, 0.17% MoS2,

28 g/t Agzone of multiple molybdenum intercepts

TSX-V: IZN

West Desert ProjectNext Steps: Continuing to Build Value

Pre-feasibility study to commence with drilling

o Phase 1 infill drilling to upgrade resource classification

o Phase 2 infill and expansion drilling

Additional objectives

o Baseline studies for permitting

o Build on favourable initial metallurgy of near surface oxide resources

18

TSX-V: IZN

West Desert ProjectProposed Drilling – Plan View

19

ResourceFootprint

Historic SilverMine

Phase 1 drilling

Phase 2 drilling

Existing drill holes 100m

TSX-V: IZN

Why Invest in Zinc?A Key Industrial Metal

20

* ILZSG (2015)

consumer products

6%

industrial machinery

7%

infrastructure16%

transport20%

construction51%

Global Market

By First Use By End Use

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012 2013 2014

mill

ions

of t

onne

s Zn

Production

Consumption

other4%

oxides and chemicals

6%

semi‐manufact.products

6%

die‐casting alloys17%

brass semis and castings17%

galvanizing50%

TSX-V: IZN

Zinc Inventories Decreasing: Unlike Copper, Nickel

21

*Bloomberg data from May 21, 2015 Scotia Daily Mining Scoop

TSX-V: IZN 22

Glencore: Zinc Supply Will Not Meet Demand

*Glencore presentation (Oct 2014)

TSX-V: IZN 23

Teck: Zinc Supply Will Not Meet Demand

*Teck presentation (Mar 2015)

TSX-V: IZN

InZinc Mining

24

An Emerging Low-Cost Mid-Tier Zinc Producer

Mid-tier zinc production potential

Important byproduct iron, copper and indium

Very favorable location resulting in lower capital requirement and straightforward permitting

One of the lowest cost potential producers

One of the highest returning projects in peer group

Significant upside potential

Drill program first step in pre-feasibility

Permitted for drilling

InZinc Mining Ltd.912 – 510 West Hastings StreetVancouver, BC Canada V6B 1L8(604) 687-7211

For further information contact:C.F. (Chris) Staargaard, President & CEO

Joyce Musial, Corporate Communications(604) 317-2728

www.inzincmining.com

Top Related