Languages

Pages

Legal

TABLE OF CONTENTS

Page No.

Introduction 1

Part I

Analysis of Broad Indicators of State Finances 3

Revenue Receipts 4

Revenue Expenditure 7

Revenue Deficit 10

Fiscal Deficit 10

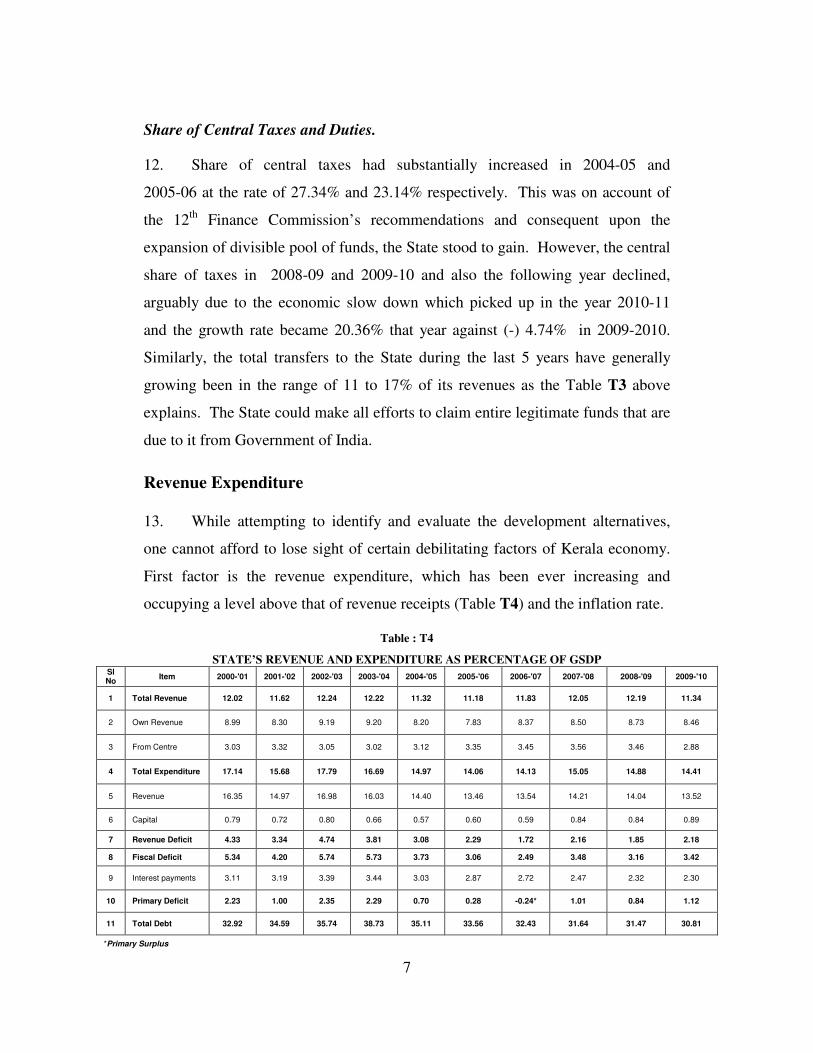

Debt Profile 14

Committed Liabilities 20

Part II

Public Finance 27

Unproductive Expenditure 27

Lapsing of Central Assistance 27

Trend of Balance from Current Revenue 28

Net Accrual from Public Account 29

Part III

Options for the Government 31

LIST OF TABLES

Page No.

T1 GSDP in 2000-01 to 2009-10 3

T2 Trend in Revenue Receipts 5

T3 Revenue Receipts 6

T4 Revenue and Expenditure as percentage of GSDP 7

T5 Trend in Revenue Expenditure 8

T6 Salaries, Pension and Interest Payments 9

T7 Debt of the State 11

T8 Key Financial Indicators 13

T9 Debt Profile 15

T10 Outstanding Commitments causing immediate outflow 19

T11 Balance from Current Revenues 28

T12 Accruals under Public Accounts 30

1

Introduction

1 The UDF Government assumed office on 18.05.2011. It is committed to

place the current status of state finances before the people of Kerala.

Accordingly, it decided to bring out a white paper on the State finances.

2. This White Paper is intended to present the facts about the financial

position of the State and the difficulties being faced by it. It is organized in three

parts :

• The first part contains a brief description of the nature and magnitude

of the problems that the State exchequer is facing today. It mainly

gives an analysis of the fiscal parameters. The historical data and their

analyses have been extensively mentioned in the White paper 2001,

published when the UDF Government had taken over in 2001. Hence

instead of repeatedly referring to a long term past data, this white

paper (2011) takes into account the more recent data over the last

decade i.e., 2001-02 to 2010-11. This is expected to present a

concurrent financial status of the State.

• The second part briefly deals with the issues of public finances and

their analysis.

• The third part deals with the possible options desirable under the

contemporary financial condition.

3. The details that are being provided in this paper are expected to initiate a

wider debate on the state of public finances and analyses thereof. It can only offer

a limited choice of options to address the financial issues facing the State. It

would indeed be difficult to exercise preference of one service over the other in

social sector or preference of one sector over the other. Certainly, these options

and preferences should also be consistent with the structural imperatives of our

2

economy. This paper is therefore intended to facilitate selection of informed

options of economic recovery and fiscal consolidation.

4. Government hopes that this white paper will help in learning important

lessons from the more recent experience in State finances. It is considered

necessary because there are some apparently satisfactory indicators like cash

balance retained in treasury, which is actually a sub optimal option of cash

managements because positive treasury surplus entails a cost of carrying that

surplus which, in ultimate analysis, adds to the liability of the State. An example

can clearly elucidate this proposition. A cash balance of A 3881.94 crore was

available in treasuries on 01.04.2011 in the form of Treasury Bill holdings. It

contained mostly treasury saving bank deposits. But the cost of treasury holding

actually adds to the carrying cost, as higher interest rates are payable on treasury

deposits and the amount blocked in it is not available for deployment on ‘return

based instruments’. There are other examples of certain sectors, which are unable

to significantly utilize even the allocated resources. Source of funds include

borrowings. Part of this borrowed money is held in treasury as unutilized. Hence

at least a part of treasury holding suffers from interest liability at two ends; one at

the time of borrowing and the second at the time of failure in its utilization and

consequent retention in the treasury. Hence one just cannot sigh in relief on

maintaining huge treasury balance.

3

PART – I

ANALYSIS OF BROAD INDICATORS OF STATE FINANCES

5. To understand and appreciate the finances of the State, certain basic

indicators have to be taken into account. Gross State Domestic Product (GSDP)

and its sectoral composition, fiscal deficit, revenue deficit, capital and revenue

expenditure, debts, etc are a few of these indicators. This paper discusses them in

seriatum.

6. Gross State Domestic Product (GSDP) signifies the sum total of the value

of economic activities in the State. A rising GSDP indicates vibrancy of the

economy. A steady or ascending growth rate of GSDP underlines the growth of

economy over a period of time. If we look at the data on Gross State Domestic

Product (GSDP) during the last few years, it has some interesting lessons. During

the UDF rule, we had highest growth of GSDP at 23.34% in 2004-05. Prior to

that, during 2002-03 and 2003-04, it was 11.51% and 11.28%. In 2005-06, it was

14.74%. Even this figure was never achieved by the previous Government in

subsequent five years, as the table T1 reveals. At the current prices, the GSDP

stands at A 230316 crore (2009-10) which signifies a growth of 14.57% over the

last year.

Table : T1

GSDP in 2000-01 to 2009-10

Year GSDP (AAAA crore) % Growth

2000-01 72659 5.05

2001-02 77924 7.25

2002-03 86895 11.51

2003-04 96698 11.28

2004-05 119264 23.34

2005-06 136842 14.74

2006-07 153785 12.38

2007-08 175141 13.89

2008-09 201020 14.78

2009-10 230316 14.57

GSDP: Source: Dept of Economics and Statistics, Kerala

4

7. GSDP is contributed by all the sectors of the occupational structure. Going

by the composition, the primary, the secondary and the tertiary sector constituted

15.36%, 23.14% and 61.50% of the GSDP respectively in 2009-10. A further

analysis of primary sector indicates that the agriculture and allied sectors’

contribution to the GSDP had declined from 12.68% in 2007-08 to 12.14% in

2008-09 and later 11.47% in 2009-10. Similarly, the analysis of secondary sector

reveals that within it, the construction activities alone constituted 12.21% and the

manufacturing activities 9.33% of the GSDP in 2009-10. On the same lines, an

analysis of the tertiary sector reveals that ‘trade, hotel and restaurants’ constituted

21.14% and ‘transport, storage and communication 9.40% of the GSDP.

Transport by other means contributed 7.13% to the GSDP. Going by the trend,

one can hypothesize that these are the areas which can ensure better revenue

receipts and also point out potential areas for policy intervention in the medium

term.

8. Slow economic growth leads to lower levels of investment in both public

and private ventures. This in turn retards the pace of economic growth! With one

succeeding into the other, it becomes a vicious cycle, adversely impacting the

revenue generation, thus starving the economy of funds for economic and social

development. If this is appreciated properly for evaluation of development

alternatives, it may offer better options for management of available financial

resources, keeping in view the contemporary development requirements. In this

backdrop, optimizing the resources for the achievement of development

objectives appears to be the only way to address the issues facing our State’s

economy at the moment. Of course, while proceeding on these lines, one has to

remember that ordinarily, increase in resources becomes difficult as one scales the

higher targets.

Revenue Receipts.

9. An analysis of the trend in revenue receipts Table T2 discloses that share

of taxes and duties has been between 80.41% in 2005-06 and 84.35% in 2009-10

5

(This is lesser than 85.49% in 2003-04, the highest in last 10 years). States’ own

taxes and duties have been between 66.40% in 2004-05 and 68.65% in 2002-03.

It has hovered between 64.76% (in 2007-08) and 67.50% (in 2009-10).

Table T2

TREND IN REVENUE RECEIPTS 2000-01 TO 2009-10

(A in crore )

Item 2000-

01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

1 2 3 4 5 6 7 8 9 10 11

I. Taxes and Duties 7455.87 7537.68 9017.76 10100.78 11368.60 12296.82 15153.86 17720.65 20265.70 22023.80

Percentage to total 85.40 83.23 84.77 85.49 84.21 80.40 83.32 83.96 82.68 84.35

Index 408 413 494 553 622 673 830 970.14 1109 1206

(I)Share of Central Taxes 1585.61 1614.26 1715.22 2012.00 2404.95 2518.20 3212.04 4051.70 4275.52 4398.78

Percentage to total 18.16 17.82 16.12 17.03 17.81 16.46 17.66 19.20 17.44 16.85

(ii)State Taxes and Duties 5870.26 5923.42 7302.54 8088.78 8963.65 9778.62 11941.82 13668.95 15990.18 17625.02

Percentage to total 67.24 65.41 68.65 68.46 66.40 63.94 65.66 64.76 65.23 67.50

II. Non-tax Revenue 1274.99 1518.71 1619.63 1714.59 2131.88 2997.71 3032.77 3386.15 4246.47 4085.60

Percentage to total 14.60 16.77 15.23 14.51 15.79 19.60 16.68 16.04 17.32 15.65

Index 221 264 281 298 370 520 526 587.54 737 709

(I)Interest Receipts 36.81 31.08 35.86 32.40 40.51 46.36 44.63 69.65 83.69 152.50

Percentage to total 0.42 0.34 0.34 0.27 0.30 0.30 0.25 0.33 0.34 0.58

(ii)Other non-tax Revenue 1238.18 1487.63 1583.77 1682.19 2091.38 2951.35 2988.14 3316.49 4162.79 3933.10

Percentage to total 14.18 16.43 14.89 14.24 15.49 19.30 16.43 15.71 16.98 15.06

III. Total Revenue 8730.86 9056.39 10637.39 11815.37 13500.49 15294.53 18186.63 21106.79 24512.18 26109.40

Index 363 377 443 492 562 636 757 878 1020 1087

10. Within the States’ own tax receipts, the contribution of sales tax and VAT

had been between 68.56% and 72.46% during the last five years. It may be

recalled that the UDF Government had in 2001-06 been able to raise this share to

74.76% in 2004-05 and 74.07% in 2003-04. Similar is the example of Motor

Vehicle tax in which the growth rate hovered between 5.86% and 6.43% during

the last five years. One may recollect that the previous UDF Government in

2001-06 had been able to achieve the growth 7.24% in 2003-04 and 6.81% in

2004-05.

State’s own Revenue

11. More importantly, the revenue deficit of the State has been over its target

during the last few years. Along side this, the rate of increase of States Own Tax

6

Revenue (SOTR) was 0.91% in 2001-02; it rose to 10.23% in 2009-10. During

the period from 2001-02 to 2010-11, first it grew up to 23.28% in 2002-2003.

Then it was 22.11% in 2006-07 which was on account of introduction of VAT

and resultant additional accrual of tax resources to the Government. The growth

rate of the States Own Tax Revenue has been 10.77% during the year 2003-04

and 10.82% in the year 2005-06. It came up to 14.46% in 2007- 08, and 16.98%

in 2008-09. It however slid to 10.22% in 2009-10. It is obvious from these data

that the SOTR growth rate of 22 to 23% witnessed twice during the last decade is

not easy to sustain in the long run. On the basis of these figures, it would be

reasonable to indicate the general growth rate in the States own tax revenue at 16

to18% in the long run. Similarly although, the States Own Non Tax Revenue

(SONTR) constitute much less in terms of percentage of overall revenue, its

growth rate has been hovering around 0.09% to 29% during the last 5 years. Here

also, it had peaked in 2002-03 when it was 25.37%. And just like SOTR, the

same assumptions apply with regard to the growth rate of SONTR and it will be

reasonable to assume a growth rate of 16-18 % for SONTR too. Its rationale is

clear from the following table T3.

Table : T3

Revenue Receipts AAAA in crore

State’s own Tax

Revenue

State’s own Non Tax

Revenue

State’s Own Revenue

(2+4)

Share of Central

Taxes and Grants

Total Revenue

(6+8) Year

Amount Growth

rate Amount

Growth

rate Amount

Growth

rate Amount

Growth

rate Amount

Annual

Growth rate

2000-01 5870.26 13.03 659.09 24.19 6529.35 14.07 2201.51 -0.72 8730.86 9.94

2001-02 5923.42 0.91 543.38 -17.56 6466.8 -0.96 2589.59 17.63 9056.39 3.73

2002-03 7302.54 23.28 681.26 25.37 7983.8 23.46 2653.58 2.47 10637.38 17.46

2003-04 8088.78 10.77 806.98 18.45 8895.76 11.42 2919.61 10.03 11815.37 11.07

2004-05 8963.65 10.82 819.08 1.50 9782.73 9.97 3717.75 27.34 13500.48 14.26

2005-06 9779.64 9.10 936.77 14.37 10716.41 9.54 4578.11 23.14 15294.52 13.29

2006-07 11941.82 22.11 937.57 0.09 12879.39 20.18 5307.23 15.93 18186.62 18.91

2007-08 13668.95 14.46 1209.55 29.01 14878.50 15.52 6228.29 17.35 21106.79 16.06

2008-09 15990.18 16.98 1559.29 28.92 17549.47 17.95 6962.71 11.79 24512.18 16.13

2009-10 17625.02 10.22 1852.22 18.78 19477.24 10.98 6632.16 -4.74 26109.40 6.52

AAGR 13.16 14.31 13.21 12.02 12.74

7

Share of Central Taxes and Duties.

12. Share of central taxes had substantially increased in 2004-05 and

2005-06 at the rate of 27.34% and 23.14% respectively. This was on account of

the 12th

Finance Commission’s recommendations and consequent upon the

expansion of divisible pool of funds, the State stood to gain. However, the central

share of taxes in 2008-09 and 2009-10 and also the following year declined,

arguably due to the economic slow down which picked up in the year 2010-11

and the growth rate became 20.36% that year against (-) 4.74% in 2009-2010.

Similarly, the total transfers to the State during the last 5 years have generally

growing been in the range of 11 to 17% of its revenues as the Table T3 above

explains. The State could make all efforts to claim entire legitimate funds that are

due to it from Government of India.

Revenue Expenditure 13. While attempting to identify and evaluate the development alternatives,

one cannot afford to lose sight of certain debilitating factors of Kerala economy.

First factor is the revenue expenditure, which has been ever increasing and

occupying a level above that of revenue receipts (Table T4) and the inflation rate.

Table : T4

STATE’S REVENUE AND EXPENDITURE AS PERCENTAGE OF GSDP Sl No

Item 2000-'01 2001-'02 2002-'03 2003-'04 2004-'05 2005-'06 2006-'07 2007-'08 2008-'09 2009-'10

1 Total Revenue 12.02 11.62 12.24 12.22 11.32 11.18 11.83 12.05 12.19 11.34

2 Own Revenue 8.99 8.30 9.19 9.20 8.20 7.83 8.37 8.50 8.73 8.46

3 From Centre 3.03 3.32 3.05 3.02 3.12 3.35 3.45 3.56 3.46 2.88

4 Total Expenditure 17.14 15.68 17.79 16.69 14.97 14.06 14.13 15.05 14.88 14.41

5 Revenue 16.35 14.97 16.98 16.03 14.40 13.46 13.54 14.21 14.04 13.52

6 Capital 0.79 0.72 0.80 0.66 0.57 0.60 0.59 0.84 0.84 0.89

7 Revenue Deficit 4.33 3.34 4.74 3.81 3.08 2.29 1.72 2.16 1.85 2.18

8 Fiscal Deficit 5.34 4.20 5.74 5.73 3.73 3.06 2.49 3.48 3.16 3.42

9 Interest payments 3.11 3.19 3.39 3.44 3.03 2.87 2.72 2.47 2.32 2.30

10 Primary Deficit 2.23 1.00 2.35 2.29 0.70 0.28 -0.24* 1.01 0.84 1.12

11 Total Debt 32.92 34.59 35.74 38.73 35.11 33.56 32.43 31.64 31.47 30.81

*Primary Surplus

8

14. It will be interesting to see the trend in the revenue expenditure of the

State during the last decade. Table T5 reveals that in 2005-06, rate of growth in

total revenue expenditure was 7.3%, which increased to 13.03% in the next year

and peaked at 19.53% in 2007-08.

Table : T5

Trend in Revenue Expenditure

AAAA in crore

Total Revenue Expenditure Development Expenditure Non Development

Expenditure

Year

Amount

Annual

Growth

Rate

Amount

% to total

Revenue

expenditure

Amount

% to total

Revenue

expenditure

2000-01 11877.92 2.69 6396.50 53.85 5481.42 46.15

2001-02 11662.03 -1.18 6028.34 51.69 5633.69 48.31

2002-03 14756.05 26.53 8064.80 54.65 6691.25 45.35

2003-04 15495.67 5.01 8061.94 52.03 7433.73 47.97

2004-05 17169.41 10.80 9244.45 53.84 7924.95 46.16

2005-06 18423.58 7.30 9757.79 52.96 8665.79 47.04

2006-07 20824.57 13.03 9283.26 44.58 11541.31 55.42

2007-08 24891.64 19.53 12332.42 49.54 12559.22 50.46

2008-09 28223.85 13.39 15154.25 53.69 13069.60 46.31

2009-10 31132.38 10.31 16633.43 53.43 14498.95 46.54

15. However, it dropped to 13.39% in 2008-09 and declined further to 10.3%

in the following year (i.e., 2009-10). The total development expenditure has been

in the range of 44 to 52% during this period. In 2006-07 the development

expenditure declined to 44.58% of the revenue expenditure; it was 49.54% in

2007-08. This may be compared with the first 5 years of the decade 2001-11

when the development expenditure was generally of the order of 51-54% of the

revenue expenditure. It is therefore evident that during these two years viz.,

2006-07 and 2007-08, the development expenditure has suffered correspondingly.

During these two years, the non development expenditure had increased which

was otherwise in the range of 46.31% to 47.04% of the total revenue expenditure

9

Table : T6

Salaries, Pensions and Interest Payments (AAAA in crore)

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

1 Interest Payments 2257.6 2489.47 2946.77 3328.29 3612.54 3799.25 4189.7 4329.65 4659.69 5292.48

2 Pension Payments 1929.48 1837.93 2282.90 2408.83 2600.77 2861.18 3294.58 4924.53 4686.43 4705.5

3 Salaries 4491.61 4200.82 4678.99 5067.09 5345.58 5607.78 6585.45 7693.66 9063.81 9800.20

4 Total (1+2+3) 8678.69 8528.22 9908.66 10804.21 11558.89 12268.21 14069.73 16947.84 18409.93 19798.18

5 Total Revenue Receipts 8730.86 9056.39 10637.39 11815.37 13500.48 15294.53 18186.62 21106.79 24512.18 26109.40

6 Total Revenue

Expenditure 11877.91 11662.03 14756.05 15495.67 17169.40 18423.68 20824.57 24891.64 28223.85 31132.37

7

Salaries + pensions +

interest as % of

Revenue Expenditure

73.07% 73.13% 67.15% 69.72% 67.32% 66.59% 67.56% 68.09% 65.23% 63.59%

8

Salaries + pensions +

interest as % of

Revenue Receipts

99.40% 94.17% 93.15% 91.44% 85.62% 80.21% 77.36% 80.30% 75.11% 75.83%

16. A good proportion of rising revenue expenditure is on account of rise in

the salary, pension and interest liabilities. Second factor is that the results from

investment in the industrial sector have not been optimal. And to sustain even

those sub-optionally performing industrial undertakings, requirement for further

investments have indeed been going up. Third, some of the ventures in the

infrastructure viz, in ports, airports, power, etc have not only been capital

intensive, their gestation period too had virtually been on extension for various

reasons, but significantly on account of delay in land acquisition. And Kerala

having highest population density among the states of India, it becomes a costly

affair to ensure land for any project. The time and cost of land acquisition has

indeed been a spoilsport as far as development initiatives are concerned.

17. Revenue expenditure constituted 91% of the total expenditure. Interest

payments as percentage of revenue receipts ranged between 19 and 25 percent

during the Twelfth Finance Commission award period against the normative

recommendation of 15% by the year under report. Capital expenditure

constituted only 6% of the total expenditure.

10

Revenue Deficit

18. While capital expenditure has been far outweighed by the revenue

expenditure, a good portion of resources has been mobilized through the

borrowings, which were effected at a rising rate of interest.

19. Figures of revenue deficit (i.e., the difference between revenue receipt and

the revenue expenditure) reveal a declining trend. When the UDF government

assumed office in 2001, we had inherited the revenue deficit of 4.33%. Following

the correctional path, that Government was able to bring it down to 3.08% in

2004-05 and finally 2.29% in 2005-06. The revenue deficit has had still further

declined to 1.72%, 2.16%, 1.85% and 2.18% in years 2006-07 to 2009-10 in that

order. But we are still away from the target of zero revenue deficit, that we have

to achieve by 2014-15 under the Medium Term Fiscal Correction Path.

Fiscal Deficit

20. Fiscal deficit i.e., the difference between receipts and disbursals is an

important indicator to gauge the functioning of the economy. By definition, a

declining fiscal deficit signifies consolidation of the resources’ position and the

sustainable functioning of the economy. When the UDF Government assumed

power in 2001-02, the fiscal deficit was 4.2% of GSDP. That Government

worked on the correctional course and brought down the fiscal deficit to 3.06% in

2005-06 (when the last UDF government demitted office in 2006). Subsequent

figures of fiscal deficit explain that although in 2006-07 the fiscal deficit was

2.49%, the last LDF government could not control the deficit that hovered

between 3.48% and 3.16% in next three years.

21. Fiscal deficit is usually financed by way of borrowings by the State. The

quantum of fiscal deficit has been increasing during the last five years as has the

total revenue been increasing. Obviously, the total debt of the state too has been

increasing over the last decade. In the year 2001-02, it was A 26950 crore which

11

increased to A 70969 crore in 2009-10. As per the latest indications, it will be at

the level of A 78673 crore by 31.03.2011. This is estimated to reach the level of

A 78673 crore by the end of March 2011. The rate of growth of debt during the

period had been hovering between 8.57% and 20.58%. Consequently, the debt

repayment liability too has been increasing correspondingly. Public debt

repayment which was A 750.76 crore in 2001-02, rose to the level of A 2405.68

crore in 2009-10. In addition, increasing reliance on debt for financing current

expenditure (not capital expenditure), increase in the debt liability on account of

loans raised by the SPVs on the strength of government guarantee and the

commitments on account of debt servicing, all manifest in enlargement of the

size of our debt. Details of growth of debt is given in the Table T7.

Table : T7

Debt of the State (2000-01 to 2010-11)

Year Debt

(AAAAin crore) Growth Rate

(in %) Average

Net Addition

(AAAA in crore)

Growth Rate of

Net Addition (in

%)

Average

2000-01 23919 18.55 3743 -16.36

2001-02 26951 12.68 3032 -19.00

2002-03 31060 15.25 4109 35.52

2003-04 37452 20.58 6392 55.57

2004-05 41877.87 11.82

15.77

4425.63 -30.77

4.99

2005-06 45929.05 9.67 4051.18 -8.46

2006-07 49875.18 8.59 3946.13 -2.59

2007-08 55409.57 11.10 5534.39 40.25

2008-09 63269.67 14.19 7860.1 42.02

2009-10 70969.43 12.17

11.14

7699.76 -2.04

13.84

22. The decade 2001-11 had inherited the fiscal deficit at 5.34% of its Gross

State Domestic Product (GSDP) (in 2000-01). It went on decreasing to a lower

level of 3.42% in 2009-10. This by itself may be a little reassuring, but the real

cause of worry is the revenue deficit. The table T2 above shows a trend of

decline in it with 2.18 % in 2009-10. But again, this declining trend per se does

not give any room for complacence; the normative targets stipulated in the

recommendations of the XIII Finance Commission still remain to be achieved.

The target was to restrict the revenue deficit to 1.4% in 2011-12 and eliminate it

12

altogether by 2014-15. This will be a challenging task and has to be achieved

by 2014-15. Further, these targets will attain statutory force once the State’s

Fiscal Responsibility Act is amended in line with the fiscal adjustment path

prescribed by the 12th

Finance Commission. The last Government has not

amended the Act. We have to amend the same to incorporate targets of fiscal

correction course, lest we lose out our share of grants from Government of India.

23. Deficit in the Government accounts represents the gap between revenue

and expenditure. Nature and extent of deficit indicates the extent of prudence

exercised in fiscal management of the government. Equally important is the way

the deficit is financed to determine the fiscal health of the State. It would suffice

to refer to the report of Comptroller and Auditor General of India on State

Finances for 2009-10 (Report No. 1). Main observations contained therein are as

under:-

i. There was an increase of 35.3% in revenue deficit during 2009-10, which was

due to 10.3% increase in revenue expenditure compared to 6.5% increase in

revenue receipts.

ii. Revenue deficit increased to 2.3% of GSDP (from 2%) and the fiscal deficit

grew upto 3.7% in 2009-10 (from 3.5%).

iii. The ratio of revenue deficit to fiscal deficit declined steadily from 74.82% in

2005-06 to 58.5% in 2008-09 but increased again to 63.8% in 2009-10 which

indicated that borrowed funds were increasingly used for revenue expenditure

rather than capital expenditure.

iv. Market borrowings to finance the fiscal deficit constituted 34.8% of the total

financial resources in 2005-06 which grew up to 46.7% in 2006-07 and 59.6%

in 2007-08. It shot up to 75.3% in 2008-09 and declined to 59.8% in 2009-10.

These figures reveal that market borrowings were mainly relied upon to finance

the fiscal deficit.

24. Causes of worry do not stop with the figures of revenue deficit. States

own revenue has been in the range of 8.30% of GSDP (in 2001-02) and 9.20% of

GSDP in 2003-04. In fact, the second half of the preceding decade saw the

13

State’s own revenue at 7.83% in 2005-06, 8.37% in 2006-07, 8.50% in 2007-08,

8.73% of GSDP in 2008-09 and 8.46% in 2009-10. Compared to this, the revenue

expenditure has been growing at much higher rates, hovering between 16.98%

and 13.46% of GSDP in 2002-03 and 2005-06 respectively. Further, capital

expenditure figures hardly offer any hope; it has always been less than 2% of

GSDP.

Table T8

Key Financial Indicators AAAA in crore

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

Revenue Receipts 8730.86 9056.39 10637.39 11815.37 13500.48 15294.53 18186.62 21106.79 24512.18 26109.40

Revenue Expenditure 11877.91 11662.03 14756.05 15495.67 17169.40 18423.68 20824.57 24891.64 28223.85 31132.37

Revenue Deficit 3147.05 -2605.64 -4118.66 -3680.30 -3668.92 -3129.15 -2637.95 -3784.85 -3711.67 -5022.97

Capital Expenditure

(including Loan

Disbursements)

847.89 719.12 948.67 1931.65 878.23 1104.05 1251.97 2367.74 2679.29 2936.06

Fiscal Deficit -3877.80 -3269.41 -4986.54 -5539.05 -4451.90 -4181.70 -3821.88 -6100.21 -6346.21 -7871.60

Primary Deficit(-)/

Surplus(+) -1620.20 -779.94 -2039.77 -2210.76 -839.36 -382.45 367.82 -1770.56 -1686.52 -2579.12

GSDP 72658.83 77923.75 86894.76 96698.03 119264.00 136841.76 153784.88 175141.08 201019.75 230315.55

Revenue Deficit as% of

GSDP 4.33% 3.34% 4.74% 3.81% 3.08% 2.29% 1.72% 2.16% 1.85% 2.18%

Fiscal Deficit as% of GSDP 5.34% 4.20% 5.74% 5.73% 3.73% 3.06% 2.49% 3.48% 3.16% 3.42%

Primary Deficit/ Surplus as

% of GSDP 2.23% 1.00% 2.35% 2.29% 0.70% 0.28% -0.24% 1.01% 0.84% 1.12%

Outstanding Debt 23919 26950 31060 37452 41877 45929 49875 55410 63270 70969

Outstanding Debt as % of

GSDP 32.92% 34.59% 35.74% 38.73% 35.11% 33.56% 32.43% 31.64% 31.47% 30.81%

Interest Payments 2257.6 2489.47 2946.77 3328.29 3612.54 3799.25 4189.7 4329.65 4659.69 5292.48

Interest Payments as % of

GSDP 3.11% 3.19% 3.39% 3.44% 3.03% 2.78% 2.72% 2.47% 2.32% 2.30%

Interest Payments as % of

Revenue Receipts 25.86 27.49 27.70 28.17 26.76 24.84 23.04 20.51 19.01 20.27

Capital Expenditure

(including Loan

Disbursements) as % of

GSDP

1.17% 0.92% 1.09% 1.99% 0.74% 0.81% 0.81% 1.35% 1.33% 1.27%

25. It is a matter of common knowledge that the receipts of the State Government in

general are not able to fully meet the expenditure requirements, and the States seek to fill

the gap by borrowings. This has particularly been a phenomenon from the end of eighties

14

in the last century. In Kerala, huge revenue deficits have been a persistent feature over

last several years. Of course, the XII and XIII Finance Commission recommendations

sought to rein in the fiscal deficit and the revenue deficit. But prior to that, the States had

been resorting to financing non plan expenditure through cuts in their outlays for

development. Faced with these constraints, State Governments have at times diverted

borrowings at costlier rates to meet the requirements of current expenditure. Hence

capital investment programme in general has suffered from resource scarcity. This has

two direct consequences. First, it prevents potential gains in output and productivity

from being realized. Second, it leads to rise in internal debt and interest payment

liabilities of the borrowing state. The resource base of the State is limited to meet the

ever growing expenditure commitments. Tax receipt in the State has not been growing at

uniform and sustainable rate. Hence even if some better growth in tax revenue is

expected or experienced in certain years, the rate of growth of tax revenue itself offers no

assurance, and may not form a stable pattern.

Debt Profile

26. The debt’s growth rate during the last five years has been meandering from

9.67% in 2005-06 and 8.59% in 2006-07 to 11.10% 14.19% and 12.17% in years

2007-08, 2008-09 and 2009-10 respectively. Despite the declining trend in 2005-06 and

2006-06 the debt has shown the tendency to grow to higher levels in 2007-08, 2008-09

and 2009-10.

27. As indicated earlier in table T7, the total debt of the State has been going up,

particularly during the last 10 years. It stood at A 70969 crore by the end of 2009-10

against A 26950 crore in 2001-02. This would be reaching the level of A 78673 crore by

the end of 2010-11. The rate of growth of debt during the decade 2001-2010 has been in

the range of 8.59% to 20.58%.

28. In addition, there is yet another indicator which is quite alarming and indeed

disturbing. The per capita debt in the State has been going up during the last few years. It

was A 11478 in 2004 but it has gone up to A 16074 in the year 2008. Per capita debt at

the national level is A 10018. Hence the per capita debt of Kerala is almost 60% above

the national average of per capita debt. Further, it is also more than the per capita debt of

15

A 8901 in Karnataka and A 9692 in Tamil Nadu (in 2008). Arguably, debt per se may be

a necessity for the economy at a particular juncture of time. But it cannot be

untrammeled by the imperatives of efficient financial resource management; it is rather

saddled with certain hard options for the management of State resources as its condition

precedent.

29. The Internal Debt comprising Market Loans, special Securities issued to

NSSF, Negotiated loans, bonds, etc. stood at A 43368 crore in 2009-10. That was

Table : T9

Debt Profile of the State (2000-01 to 2009-10) (A crore)

Item 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10

Receipts 483.11 780.7 1192.86 968.17 1482.11 603.29 205.01 416.43 768.04 562.34

Disbursements 284.01 536.12 1004.44 1875.09 1699.25 596.71 250.64 255.57 292.05 265.68

Interest 732.27 778.56 805.02 809.92 671.60 436.44 432.73 429.48 435.23 425.31

Gross Retention 199.1 244.58 188.42 -906.92 -217.14 6.58 -45.63 160.86 475.99 296.66

Lo

an

s a

nd

Ad

van

ces

fro

m G

overn

men

t o

f In

dia

Net Retention -533.17 -533.98 -616.60 -1716.84 -888.74 -429.86 -478.36 -268.62 40.76 -128.65

Receipts 6295.44 5917.95 8147.87 7011.55 6317.80 6181.49 5838.15 6601.46 10136.03 10109.02

Disbursements 5332.26 4830.23 6770.85 5824.84 6523.40 6738.29 6818.20 6404.44 8780.28 8176.42

Interest 386.75 479.82 627.01 662.72 668.7 634.13 782.59 548.97 515.99 760.13

Gross Retention 963.18 1087.72 1377.02 1186.71 -205.60 -556.8 -980.05 197.02 1355.75 1932.60

Sm

all S

avin

gs a

nd

D

ep

osit

s

Net Retention 576.43 607.90 750.01 523.99 -874.3 -1190.93 -1762.64 -351.95 839.76 1172.47

Receipts 1722.62 1268.51 1685.99 1761.58 1578.63 1595.75 2058.83 2821.66 3082.01 2814.04

Disbursements 1033.71 1284.34 1546.29 1323.33 985.53 988.85 1385.45 1695.17 1848.70 1897.35

Interest 391.03 290.03 375.98 353.86 449.14 537.38 500.67 624.21 699.62 753.30

Gross Retention 688.91 -15.83 139.70 438.25 593.10 606.90 673.38 1126.49 1233.31 916.69

Sta

te P

rovid

en

t F

un

ds

Net Retention 297.88 -305.86 -236.28 84.39 143.96 69.52 172.71 502.28 533.69 163.39

Receipts 6975.36 7849.70 10518.26 14120.87 14442.36 11366.48 11577.39 12212.07 10074.33 6693.80

Disbursements 5083.63 6134.59 8113.70 8446.95 10187.07 7371.99 7278.96 8162.06 5279.26 2140.00

Interest 747.71 941.14 1140.29 1502.06 1823.45 2216.21 2380.17 2727.71 3009.31 3353.17

Gross Retention 1891.73 1715.11 2404.56 5673.92 4255.29 3994.49 4298.43 4050.01 4795.07 4553.80

Inte

rnal D

eb

t

Net Retention 1144.02 773.97 1264.27 4171.86 2431.84 1778.28 1918.26 1322.30 1785.76 1200.63

Receipts 15476.53 15816.86 21544.98 23862.17 23820.90 19747.01 19679.38 22051.62 24060.41 20179.20

Disbursements 11733.61 12785.28 17435.28 17470.21 19395.25 15695.84 15733.25 16517.24 16200.29 12479.45

Interest 2257.76 2489.55 2948.30 3328.56 3612.89 3824.16 4096.16 4330.37 4660.15 5291.91

Gross Retention 3742.92 3031.58 4109.70 6391.96 4425.65 4051.17 3946.13 5534.38 7860.12 7699.75To

tal D

eb

t

Net Retention 1485.16 542.03 1161.40 3063.40 812.76 227.01 -150.03 1204.01 3199.97 2407.84

16

12.03% higher than its previous year’s total that stood at A 38814 crore which

itself was 11.73% more than its previous year. The percentage by themselves

may look innocent and do not convey the ferocity of the quantum as the

borrowing has increased the per capita debt from A 12503 in 2005 to A 16074 in

2008 and A 19626 in 2010.

30. The liabilities on account of Small Savings, Provident Funds and other

debts also have been increasing during the last few years. In 2001-02 its rate of

growth was 10.52% (A 11261.65 crore). However, it had increased to 15.44%

(A 21296 crore) during the year 2009-10. In this regard, a bitter fact has to be

appreciated. These debts are costlier and put the state in a piquant situation where

it results into surplus cash balance in the treasury but the state has to pay higher

rate of interest on these treasury saving deposit and PF accounts. Then there is an

opportunity cost of revision of projects and programmes for which funds were

drawn and kept in treasury. But not utilizing these sums in time, projects are

revised upward on account of delay, seeking more funds later. Obviously, it is a

costly surplus. Hence there is a need to revisit the entire issue.

31. Comptroller and Auditor General of India in his Report on State Finances

for 2009-10 (Report No. 1) has further observed as under :

“Apart from the magnitude of debt of the State Government, it is

important to analyze various indicators that determine the debt

sustainability of the State”

32. Debt sustainability refers to the state’s ability to maintain a constant

debt-GDP ratio over a period of time. Thus it implies State’s ability to service the

debt. It would therefore mean sufficiency of liquid assets to meet the current or

committed obligations and the capacity to maintain a balance between cost of

additional borrowings and the returns from the borrowings. It would also mean

that the rise in fiscal deficit must match the increase in capacity to service the

debt.

17

33. Stability of debt can be achieved if the rate of growth of economy exceeds

the interest rate or the cost of public borrowings. Then the debt GDP ratio can be

used as an indicator provided primary balances are positive or zero or marginally

negative. Debt sustainability can be achieved if the quantum spread (debt

multiplied by the rate spread ; rate spread is GSDP growth rate minus interest

rate) together with primary deficit is zero. Then the debt GSDP ratio would be

constant or the debt would eventually stabilize. If however, quantum spread and

the primary deficit together is negative, the debt-GSDP ratio would be rising.

34. It is on this principle that CAG has observed in the Report referred in para

23 above as under :-

“During 2007-08 to 2009-10, the quantum spread together with

primary deficit was positive, indicating declining trend in debt GSDP

ratio. The resource gap (sufficiency of non-debt receipt) was negative

throughout the period 2007-10 which showed that the incremental

non-debt receipts were inadequate to finance incremental primary

expenditure and incremental interest burden. This means that the

government will have no option but to go for debt receipts to meet its

operational expenditure, Moreover, the net availability of borrowed

funds after providing for interest and repayment of principal decreased

during 2009-10 from the previous years which shows that a larger part

of borrowings was used for current consumption including debt

servicing, leaving only a small portion of the borrowed funds to be

spent for developmental activities. The burden of interest payment

(interest payment to revenue receipt ratio) was much higher in Kerala

(20%) than the TFC recommended norm of 15%.”

35. There is another comment by CAG in his report “Union and state Finance

At a Glance 2009-10”, which is quoted below.

18

“… As on 31 March 2010, as many as 17 States have more liabilities

than financial assets. West Bengal, Kerala and Punjab have financial

liabilities more than double of their financial assets ….”

36. Kerala’s ratio of financial assets to liabilities of the state in the years

2007-08, 2008-09 and 2009-10 had been 36,39 and 39. This indicator explains

why Kerala has been included in the list of debt stressed states, along with West

Bengal and Punjab.

Contingent Liabilities

37. Yet another area of concern is the government guarantees. It is true that

the quantum of guaranteed amount as well as amount outstanding has come down

to A 10225.78 crore and A 7495 crore respectively in 2009-10. However, an

increased possibility of invoking government guarantees has been a matter of

concern because, if invoked, these guarantees may put an unexpected pressure on

the State exchequer. Perhaps the time has come we should seriously review the

economics of contingent liabilities

38. The surplus cash balance in the State Government’s account as on

18.5.2011 was A 1963.47 crore. As explained earlier, it gives an impression of

comfortable liquidity position but it is actually quite discomforting. This amount

has accumulated because of the fact that a portion of the committed liabilities of

2010-11 had spilled over to the current financial year. A major component of this

treasury surplus will have to be spent on Pay Revision Pension Revision arrears.

Even though the 9th

pay revision is applicable w.e.f. 01.07.2009, the process of

eliciting options and processing the same for preparation of arrears could not be

completed within March 2011. Consequently, major share of this liability will

fructify for payment in 2011-12, and payments will have to be effected

immediately. The table below (T10) indicates the liabilities that were committed

during the previous year(s), resulting in immediate outflow from State’s

exchequer.

19

Table : T10

Outstanding Commitments causing immediate outflow

AAAA in crore

Arrears of Salaries and Pension 800

Outstanding payments to contractors 425

Electricity subsidy to farmers 27

Farmers’ debt relief 27

Cost of Medicines / equipments, etc. 13.80

MLAs’ Special Development Fund – Additional allocation 35

Kerala State Co-operative Bank-Share Capital 136

Social Security Pensions & Welfare Pensions at enhanced rate 200

Ration Subsidy (food grains @ 2 per kg.) 266

Arrears of compensation for paddy procurement & market

intervention operations (to Supplyco) 125

Land acquisition charges 100

Total 2154.80

39. During the last 10 years, the fiscal deficit and revenue deficit as also the

primary deficit have all been coming down. In fact, the state witnessed negative

primary deficit in 2006-07. Since primary deficit is comprised of the fiscal deficit

minus interest payment, this only gives a partial view of the financial health of the

state. Thus negative primary deficit by itself does not give room for

complacence. Our other main concerns are the revenue deficit and the fiscal

deficit. The 13th

Finance Commission’s recommendation is to eliminate the

revenue deficit by the year 2014-15 and restrict the fiscal deficit to 3.0% from

2013-14 onwards. The targets for the current year are at 1.4% and 3.5% for the

revenue deficit and the fiscal deficit respectively. Immediate past data show that

the fiscal deficit has generally been within the limits prescribed under the fiscal

correction path, ranging between 2.49% and 3.42% during the period from

2006-07 onwards. But during the same period, revenue deficit has not been

showing any uniform pattern; it has ranged between 1.72% to 2.17% from

2006-07 onwards. The table T4 in para 13 ante indicates it.

20

Committed Liabilities

40. In the light of the current financial situation of the State, it is obvious that,

today; government finds it extremely difficult to allocate resources for its priority

sectors as it has to discharge the committed liabilities first. Committed

expenditures themselves tend to consume a lion’s share out of available resources.

41. The fiscal year 2011-12 has to inherit a substantial share of liabilities of

2010-11, which remained unsettled by 31st March 2011. These are briefly

indicated in succeeding paragraphs. These will fructify in course of 2011-12 and

later.

Arrears of salary and pension to employees and pensioners

42. Revision of Pay and Pension of State Government Employees and

Pensioners has always been putting State’s finances under severe pressure,

affecting the resources for developmental spending. The State Government had in

2010-11 revised the Pay and Pensions effective from 01.07.2009. The annual

financial commitment on this account is estimated as A 1964 crore. The arrears of

pay and pension payable from 01.07.2009 to 31.03.2011 accounts for

A 2861 crore. These together works out to a total liability of A 4825 crore.

43. Resultant on this additional liability on account of revision of salaries and

pensions and also new payments of DA/DR payable in 2011-12 their budget

allocation for 2011-12 stands substantially enhanced. The budget allocation made

for salaries and pensions in 2011-12 is A 16325 crore and A 7311 crore

respectively. Showing a total increase of A 6518 crore over the previous year’s

total outlay of A 17119 crore for these items. This has effectively reduced

Government’s opportunities for allocating sufficient resources for developmental

activities of its choice and priority.

21

Dues payable to Co-operative Institutions/ Banks etc.

(i) Agriculture Production cost Relief Scheme.

44. Government is to provide relief to credit Co-operatives under Agriculture

Production Cost Relief Scheme sanctioned in G.O. (Ms) No. 11/92/Co-op. dated

07.03.1992. Pending claims under this scheme up to 2009-10 accounts for

A 44 crore.

(ii) Grant to CAPE against Deposit Mobilisation through Co-operatives

45. In terms of G.O. (Rt) No. 1911/2000/Fin dated 29.03.2000, the State

Government is also committed to provide grant in aid to Co-operative Academy

of Professional Education (CAPE) to the extent of 25% of the deposits mobilised

from primary Co-operative Societies as a part of resource mobilisation drive

under the Treasury small savings Fixed Deposit Scheme. Against A 81.91 crore

due to CAPE on this account, A 40.86 crore has been released so far.

A 40.85 crore is still outstanding.

(ii) Additional Share Participation in Kerala State Co-operative Bank

46. For the revitalization of the Kerala State Co-operative Bank, an action

plan has been drawn up in 2010-11 with the approval of NABARD and

Government of India. The Action Plan aims at the Bank achieving a positive net

worth by improving its financial position over a period of 3 year by augmenting

its share capital base by A 344 crore. Government released A 150 crore in

2010-11 as State’s equity contribution to the Bank. The balance contribution of

A 194.20 crore is to be made during 2011-12 and 2012-13.

Paddy Procurement and market Intervention operations by Kerala State

Civil Supplies Corporation

47. Government procure paddy from farmers through the Kerala State Civil

Supplies Corporation (Supplyco) and compensate the Corporation for its losses on

22

this account. Apart from this compensation is payable to Kerala State Civil

Supplies Corporation for its market intervention operations. Government has also

to meet the milling charges. Claims to the tune of A 291 crore submitted by the

Kerala State Civil Supplies Corporation (KSCSC) Ltd. for the period up to

31.03.2011 was pending to be settled, against the available budget provision of

A 75 crore.

Payment towards free electricity to small and marginal farmers

48. Agriculture Department provides subsidy to small and marginal farmers

towards electricity used for agricultural purposes. As on 31.03.2011, an amount

of A 27 crore was due for payment to Kerala State Electricity Board on this

account.

Ration subsidy

49. The previous Government during the last quarter of 2010-11 extended the

scheme of distribution of food grains @ A 2 per kg. to all ration card holders.

Due to the large number of APL card holders being brought under the scheme, the

total financial commitment would increase to A 458 crore whereas the budget

provision available is A 250 crore. This will result in an additional outflow of

A 250 crore during the current financial year. Further, the rates of commission to

ration dealers were also increased and an amount of A 15.68 crore is required to

clear its arrears. The total additional liability works out to A 266 crore.

Debt Relief to farmers

50. Applications for debt relief numbering around 4.14 lakh have been

received by the Kerala State farmers Debt Relief Commission. Of this about

1.71 lakh applications have been disposed off by the Commission with a total

compensation of A 89.69 crore out of this, A 62.45 crore has been disbursed so

far. The balance of A 27.24 crore is pending to be disbursed. The budget

23

provision available is A 8 crore and hence A 19.24 crore is to be provided

additionally now. Apart from this, the pending 2.43 lakh applications, when

disposed off, can result in additional liability of around A 175 crore, even when

assessed with a very nominal compensation of A 7500 on an average.

Payments towards medicine equipments, water charges etc. of Medical

College Hospitals.

51. A 13.81 crore is outstanding to be paid towards the cost of medicines and

equipments purchased and water charges payable to Kerala Water Authority by

the Medical College Hospitals.

Road up gradation works taken up under MLA SDF

52. An additional allocation of A 25 lakh per Constituency was sanctioned in

2010-11 exclusively for taking up road up gradation work under the Special

Development Fund for MLA. Majority of works have been taken up and

completed and payments are due now. A 35.25 crore is the additional requirement

on this account.

Compensation for Land Acquisition

53. About A 100 crore will be immediately required to settle the outstanding

claims in land acquisition cases including commitments on account of satisfaction

of Court decrees in LAR cases and settlements reached through Lok Adalaths.

Stimulus package

54. During 2009-10 an anti recession stimulus package was announced for a

total amount of A 10,000 crore, consisting of A 5000 crore for Water Supply,

Irrigation, Public Work sectors and another A 5000 crore on projects implemented

by LSGIs, PSUs, etc. No budget provision was made for this package during

2009-10. 1280 works with estimated cost of A 3000 crore were sanctioned in

PWD during 2009-10. For PWD, works bill amount to A 324.26 crore were paid

24

till 31.03.2011. The additional financial commitment on account of spill over

works under this package will be around A 1600 crore.

55. Under Irrigation sector, 10 works with a total outlay of A 468.16 crore

were sanctioned under this stimulus package. Works bills amounting to A 30.66

crore only is so far paid. The balance payment of around A 320 crore will fall due

in the coming months.

56. Under the Water Supply Sector,73 works costing A 515.91 crore were

sanctioned under the stimulus package. The payments so far effected on the

works executed under this package is A 41.08 crore. The residual payments of

about A 355 crore will have to be effected during the course of the succeeding few

months.

Works under 'Vision 2010'

57. The scheme 'Vision 2010', envisaging infrastructure development works in

all legislative assembly constituencies of the State was initiated by PWD during

2007-08. Works costing one crore each were sanctioned for each Constituency

for the years 2007-08 and 2008-09 and all works were to be completed by 2010.

Forty such works are still going on and thirteen still remain to be arranged. The

liability on account of spill of over works under 'Vision 2010' would cost the state

exchequer an amount of A 115.38 crore.

Indiscriminate sanctions for works

58. During the five year period from 2006-07 to 2010-11, Government issued

Administrative Sanction for civil works costing A 1922.59 crore in the Public

Works (Roads and Bridges) Department against total budget provision of

A 161.20 crore. The total sanctions thus works out to 1192 % of the budgeted

outlay for these 5 years, which is gross violation of the existing norms relating

issue of administrative sanctions for works in PWD and against principles fiscal

prudence.

25

59. As per the prevailing norms cost of administrative sanction issued during a

year should not exceed 150% of the budget outlay for the year. During the last

4 years, the total cost of the works sanctioned has exceeded the budget provision

by over 1000%. In the year 2009-10 the excess was over 2000%. The additional

commitment on account of these excessive sanctions is estimated to be above

A 1300 crore. For 2011-12 alone, A 715 crore will be required for effecting

payment of work bills of this category.

Social Security Pension

60. In his budget speech, the former Finance Minister has announced his

Government’s intention to enhance the monthly rate of Social Security Pension

and other welfare pensions from A 300 to A 400. As this Government can not do

way with the proposed enhancement, an additional liability of A 200 crore is to be

taken over during the current year.

Kerala State Road Transport Corporation

61. Currently the KSRTC is incurring an operating loss of around A 40 crore

every month. The annual operating loss will come to A 480 crore. But for the

liberal financial support from State Government, KSRTC will not be able to carry

out its regular operations. This will add additional pressure on State’s finances.

Kerala State Housing Board

62. The Kerala State Housing Board has been in deep financial crisis for

several years now. KSHB’s outstanding liabilities with HUDCO alone is A 750

crore State Government is committed to clear at least ⅓ of this liability

immediately, lest the State Government will not be able to avail any more loans

from HUDCO. Hence the State Government is now compelled to take over a

liability of A 250 crore.

63. The additional financial liability on account of the above commitments

would be AAAA 10197 crore for the financial year 2011-12. However, only an

26

amount of A 5133 crore was provided in the budget 2011-12 for defraying

expenses on account of pay and pension revision and part of liability under

anti-recession stimulus package. Deducting the above amount from the total

commitment of A 10197 crore, an uncovered commitment of AAAA 5064 crore

remains for which no provision was made at all in the budget 2011-12 presented

in February 2011. This additional liability is a heavy burden, resulting in severe

strain on State’s finances

27

Part-II

PUBLIC FINANCE

Unproductive Expenditure 64. In terms of the recommendations of the 12

th Finance Commission, a

scheme of debt waiver of principal portion of central loans based on reduction to

be achieved in revenue deficit consistently from 2005-06 was introduced by

Government of India. The 12th

Finance Commission computed the eligible sum

to the State as A 1063.05 crore under the scheme. As against this, the State could

avail only A 250.26 crore. The failure in availing the balance of A 812.79 crore

was due to the inability of the Government to reduce revenue deficit in a regular

manner. This was because of the non plan revenue expenditure (NPRE) growing

by nearly 100 percent from the figure of A 15227 crore in 2005-06 to A 29403

crore in 2010-11. This was against a growth of just 53 percent during the period

2000-01 to 2005-06. This brings to light the extravaganza of the previous

Government in favour of unproductive expenditure.

Lapsing of Central Assistance

65. In the meantime, an amount of A 414 crore that was receivable as grants

under 12th

Finance Commission award was allowed to lapse because of the

non-compliance of ‘not so severe’ conditionalities stipulated by the 12th

Finance

Commission and also due to the inefficiency of the Government in spending and

furnishing utilization certificates in time. In the case of grants relating to PWD, a

sum of A 174 crore was allowed to lapse just because adequate Non Plan Revenue

Expenditure (NPRE) for maintenance was not incurred. In sectors like 'Inland

Waterways and Canal' and 'Coastal Zone Management' the Government was

virtually in the dark and could not finalise workable projects till the end of the

12th

Finance Commission award period. That resulted in the loss of A 240 crore.

28

Trends of Balance from Current Revenue

66. Though there was proliferation in NPRE the expenditure could not reach

the required level in the targeted areas. Also there was failure in availing debt

waiver and eligible grants from the Centre. This resulted in deterioration of

Balance from Current Revenue (BCR) as well. The previous UDF Government

had addressed this issue and was able to avoid massive hike in negative BCR in

the first three years viz. 2001-02, 2002-03 and 2003-04. The Government

succeeded in its attempt in reducing the negative BCR by 24.6% (to A 1496 crore)

in 2004-05. It was further reduced by 52.7% (to A 707.60 crore) in 2005-06.

However, such a trend was reversed by the previous Government. The negative

BCR increased by 88.4% in the year 2006-07 and by 177% in 2007-08. The

figure remained consistently high even in the next two years though there was a

decline from 2007-08 figure. It ended at (-)A 1624 crore in 2009-10 as can be

seen from Table T11 below.

Table : T11

Balance from Current Revenues

(AAAA in crore)

2001-02 (-) 1724

2002-03 (-) 1811

2003-04 (-)1983

2004-05 (-)1496

2005-06 (-) 707

2006-07 (-)1332

2007-08 (-) 3691

2008-09 (-) 2259

2009-10 (-) 1624

29

67. The worsening contribution from revenue account for plan financing

resulted not only in excessive dependence on borrowings but also reduced the

availability of resources for financing capital expenditure. Had the better Balance

from Current Revenues (BCR) in 2005-06, continued in subsequent years also, it

would have improved not only the revenue deficit but also the capital expenditure.

If serious thoughts were given to achieving the targets of Kerala Fiscal

Responsibility Act (KFRA) 2003, the lapses of such magnitude would not have

occurred.

Net accruals under Public Account

68. The Constitution envisages maintaining 'Public Account' in respect of

which the state has to act as a trustee and has to function as a banker for some

limited essential items of inflows and outflows in the smooth conduct of

Government business. But in the State the Public Account has been extensively

utilized with a view to secure additional funds by exhorting the Welfare Fund

Boards and other government institutions to deposit their money with treasury at

an interest rate higher than the interest rate payable on open market borrowings.

As a result, the outstanding liabilities under Public Account have swollen to

A 21296 crore in 2009-10 from A 14841 crore in 2005-06. This can upset the

financial planning of Government, if funds are withdrawn at large scale from

these accounts at call.

69. Another unhealthy practice is the provision of maintaining TSB account

and PD accounts by the departments, quasi government institutions and Local Self

Government Institutions (LSGIs). Transfers to these accounts are without cash

flows that is, through accounting adjustments from service heads in the nature of

an actual expenditure. Hence expenditure eventhough booked in the service

heads would happen in a later date only. The claims arising during a later period

will put State’s liquidity under pressure. The increase in the net liabilities under

Public Account in the last five years is illustrated in the table T12:

30

Table : T12

Accruals under Public Account (net)

(A in crore)

2005-06 331

2006-07 (-) 287.56

2007-08 1891

2008-09 916

2009-10 3062

70. The danger of promoting deposits to Public Account, in excess of the

manageable limits is that a liquidity crisis looms large over the government as had

prevailed in the State in the later half of 1990's when the cheques issued by

Government authorities failed to be honoured, questioning the credibility of

sovereign instruments. This kind of situation would affect the process of planning

and budgeting and also implementation of programmes.

31

Part III

Options for the Government

71. In view of the stress on resources as elucidated in foregoing chapters,

government has very little options for the management of its finances. Some

possible options are briefly mentioned in succeeding paragraphs.

72. Diversification from agriculture to industrial sector and expansion of

tertiary sector is expected to add considerably to the gross domestic product.

However, the Kerala economy has for long been dependent on the growth of

service sector rather than the growth of agriculture and industrial sectors. The

state is lagging behind in the agricultural and industrial sector even though fertile

soil, suitable climate, skilled manpower and capital are in abundance. The

productive sector is far behind the national trend. It is the high time to zero in on

the factors responsible for this backwardness and rectify the mistakes without

losing further time.

73. Union Government has come out with a draft manufacturing policy to

raise the share of manufacturing in GDP to 25 percent from 16 percent at present

with the intention of generating employment. The policy brought out by the

Centre can be adopted by Kerala with modifications wherever required. As we

are aware, the number of unemployed persons registered with the employment

exchange has swollen to a whopping 45 lakh. With careful and thoughtful

diversification into secondary and tertiary sectors, employment opportunities can

be enhanced. Further improvement in the occupational structure can also be

achieved by such diversification. Within secondary sector, micro, small and

medium enterprises need to be promoted as these ventures have the potentiality to

employ the vast number of qualified skilled labour. As its corollary, marketing of

products too will have to be organized for ensuing remunerative returns to these

ventures.

32

74. Industrial sector in the state needs rejuvenation. But it should not mean

that such a rejuvenation would be only through the public sector undertakings. In

addition to public sector, partnership of private sector is essential for major

investments. The State should not shy away from private capital. But in order to

facilitate extensive private investment, the state has to organize basic facilitating

infrastructure. Accordingly, it seeks massive investment in infrastructure such as

seaport, airports, roads and transportation sector. But the state having inherited

massive committed liability, finds it difficult at this juncture to allocate sufficient

funds for investments in infrastructure.

75. The state has to manage its finances in accordance with the targets set by

the 13th

Finance Commission in course of the larger macro economic management

of the country. We are aware that confrontationist attitude with Centre will not be

beneficial to the state economy. Further, fiscal consolidation in the state cannot

be achieved by compressing the social sector expenditure and the expenditure on

much needed public goods. Compression of expenditure has to be limited to

those sectors where private investments are relatively easy to come by or where

the investments will not fetch the desired results at this point of time.

Augmentation of revenue alone cannot result in fiscal consolidation. In fact,

economic tremors can occasionally pull down revenue in medium term. Hence

the two pronged approach of revenue augmentation and avoiding wasteful or

inefficient expenditure can lend credence to the fiscal consolidation efforts.

76. Outstanding dues of all kinds will have to be cleared in a phased manner

so that budgetary planning and MTFP targets are not vitiated.

77 The Kerala Fiscal Reforms Act 2003 will have to be amended in

compliance of the 13th

Finance Commission recommendations so that the fiscal

consolidation process are rolled on in the State and the benefits recommended in

the 13th

FC are availed as far as possible.

33

78. Debt sustainability will have to be achieved through prudent financial

interventions. The composition of debt has remained almost the same during the

last five years. The internal debt as a percent of total debt stock is 63.46 per cent

while the loan from the Centre is at 8.56 percent in 2011-12. PF, Small Savings

etc constitute 28.28 percent of debt stock. The debt as a per centage of GSDP has

come down to 28.99 in 2011-12 (Alt). The Debt/GSDP limit proposed by the 13th

Finance Commission for 2011-12 is 32.3 percent. The FD/GSDP and RD/GSDP

ratios allowed by the 13th

Finance Commission for 2011-12 are 3.5 percent and

1.4 percent respectively. But in the year 2011-12, the RD/GSDP ratio is expected

to be at an increased level of 1.81 per cent whereas FD/GSDP ratio will remain

within the limit. It may be made clear that non achievement of RD/GSDP target

is due to the provisioning for pay and pension revision arrears in 2011-12. The

RD/FD ratio which was as high as 74.82 per cent has come down to 52.66 percent

in 2011-12 (Alt.). Thus the RD/FD ratio shows that the quality of fiscal deficit

has been improving.

79. Government has already chalked out the Medium Term Fiscal Policy Plan

for 2011-12 and 2012-13. The main objectives mentioned there are indicated

below:-

• Inadequate infrastructure of international standard hinders Kerala’s

image as an attractive investment destination. Given the resource

constraints of Government, infrastructure will be built up with private

participation. Major infrastructure projects will have to be put a fast

track mode.

• Measures will have to be taken to focus Kerala as an attractive

investment destination.

• Agriculture and industry will have to be the thrust areas for creating

employment opportunities through diversification and resource /

technical collaborations.

34

• Not only growth but also development with equity without sacrificing

the interest of the poor has to be the prime concern.

80. Sustained growth of the State’s own tax revenues is essential to reduce

fiscal imbalances. Therefore tax administration has to be strengthened further and

rationalised.

81. As against a legislative ceiling of A 14000 crore in respect of contingent

liabilities, the outstanding liabilities are A 7495 crore. State will have to be

careful and prudent in incurring further contingent liability.

82. It is obvious that the intricacies of finances of the state has to be

understood properly and addressed. It cannot be done in a year or through a

year’s budget. It has to follow a sustained train of efforts over next new years.

Effort has to maximize its usage subject to the constraints of the economy.

Management of revenue gap is never a one-step effort. It combines proverbial

‘tightening of the belt’ with increasing the economic efficiency of expenditure

based on informed options of spending, without compromising on the social

commitment and economic imperatives.

35

Top Related