Languages

Pages

Legal

Acquisition of assets from DONG Energy AS

Value through

July 2016

Successful E&P company focused on the wider North Sea

Strong track record of delivering growth 10x increase in production since 2009: 7–9 mboepd 2016

30x increase in 2P reserves since 2009: 61 mmboe*

Outstanding exploration record, low finding cost

Successful monetisation of exploration discoveries

Norwegian near-term development projects on-track

Robust balance sheet at low commodity prices: a prudent approach £75.5mm cash balance (31 March 2016)

$30mm debt drawn under an RBL facility

Opex/boe $23 (2015) provided positive cash flow

Norwegian focussed operations Politically stable OECD jurisdiction with very attractive fiscal regime

incentives for exploration, appraisal, development and decommissioning

Offshore Norway is underexplored and underexploited vs. UK

2

Faroe Petroleum overviewValue focused independent E&P company

* CPR Jan 16

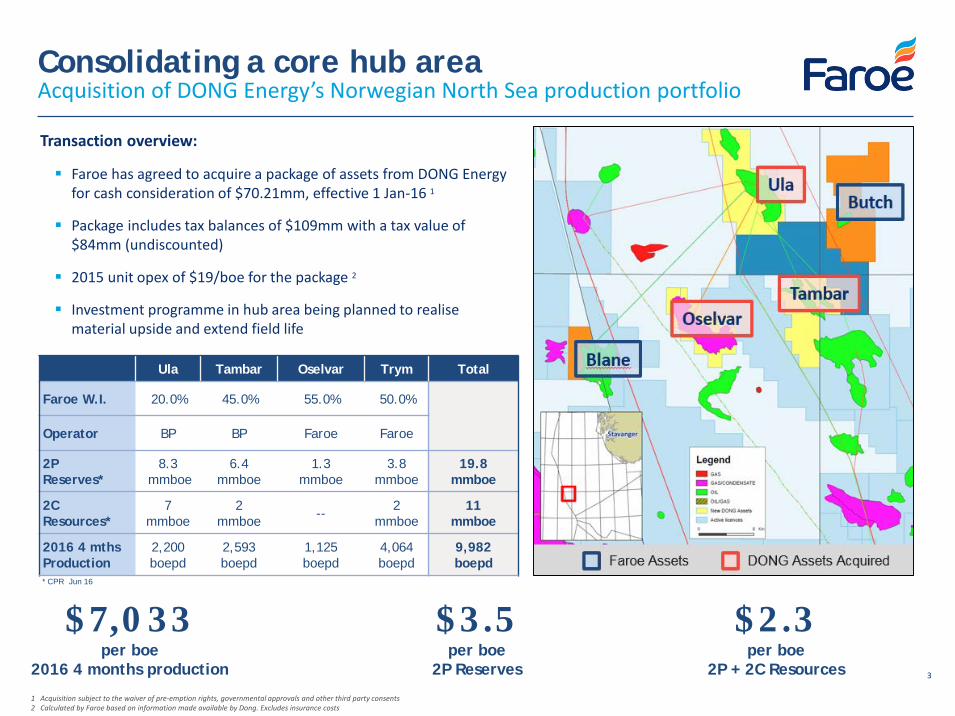

Consolidating a core hub areaAcquisition of DONG Energy’s Norwegian North Sea production portfolio

3

Transaction overview:

Faroe has agreed to acquire a package of assets from DONG Energy for cash consideration of $70.21mm, effective 1 Jan-16 1

Package includes tax balances of $109mm with a tax value of $84mm (undiscounted)

2015 unit opex of $19/boe for the package 2

Investment programme in hub area being planned to realisematerial upside and extend field life

Ula Tambar Oselvar Trym Total

Faroe W.I. 20.0% 45.0% 55.0% 50.0%

Operator BP BP Faroe Faroe

2P Reserves*

8.3mmboe

6.4mmboe

1.3mmboe

3.8mmboe

19.8mmboe

2C Resources*

7mmboe

2mmboe -- 2

mmboe11

mmboe

2016 4 mthsProduction

2,200 boepd

2,593boepd

1,125boepd

4,064boepd

9,982 boepd

$7,033per boe

2016 4 months production

$3.5per boe

2P Reserves

$2.3per boe

2P + 2C Resources

* CPR Jun 16

1 Acquisition subject to the waiver of pre-emption rights, governmental approvals and other third party consents2 Calculated by Faroe based on information made available by Dong. Excludes insurance costs

113

227

2015 2015 Pro-formaDONG

+101%

60

126

2015 2015 Pro-formaDONG

4

Faroe taking advantage of a ‘buyers market’

Majors, utilities and large independents looking to rationalise portfolios

Faroe, as pre-qualified operator in Norway, with balance sheet strength and flexibility is one of a limited number of possible buyers

Significantly increases Faroe's scale

Doubles current production

33% increase in 2P reserves* - acquired assets all on production

Deepening in a core area by buying into the Ula hub brings operating synergies with Faroe's producing Blane field and planned Butch development

Becoming Norwegian production operator opens new opportunities for Faroe

Adds material cash flow immediately

New cash flow and debt capacity will materially strengthen the company’s finances

Profits from acquired production will provide valuable tax shelter for planned development programme

Acquisition funded through equity to maintain balance sheet strength and flexibility

Significant upside in acquired assets and hub area

Multiple projects to increase production across the Ula field hub

Investment programme for new assets – to be funded from cash flow - includes Tambar artificial lift project

Upside value is not included in consideration price

Transaction rationaleA transformational deal for Faroe: perfect strategic fit

Revenue1 (£mm)

EBITDAX1 (£mm)

+110%

* CPR June 16

1 Average realised oil price of $50/bbl and $47/bbl in 2015 for Faroe and the Dong assets respectively

2 4

24 24 28

30

61

81

1 Jan2009

1 Jan2010

1 Jan2011

1 Jan2012

1 Jan2013

1 Jan2014

1 Jan2015

1 Jan2016

9

1 1

3

7 6

9

11

2009 2010 2011 2012 2013 2014 2015 2016 PF

Continuing our track record of delivery Consistent growth in reserves and production

5

2P Reserves (mmboe) W.I. Production (mboepd)

15 – 17

40x increasebetween

2010-2016

16x increasebetween

2009-2016

Faroe

DONG Assets

Faroe

DONG Assets

(1) 2P Reserves as per 1 January provided in the yearly CPRs(2) The CPR estimates of 2P reserves of the Faroe’s assets and the new DONG assets

8

7 - 9

(2)

(1)

7

10

2010 2011 2012 2013 2014 2015 2016 2016 PF

Faroe Assets DONG Assets Butch Njord, Hyme andSnilehorn

Pil and Bue 2021

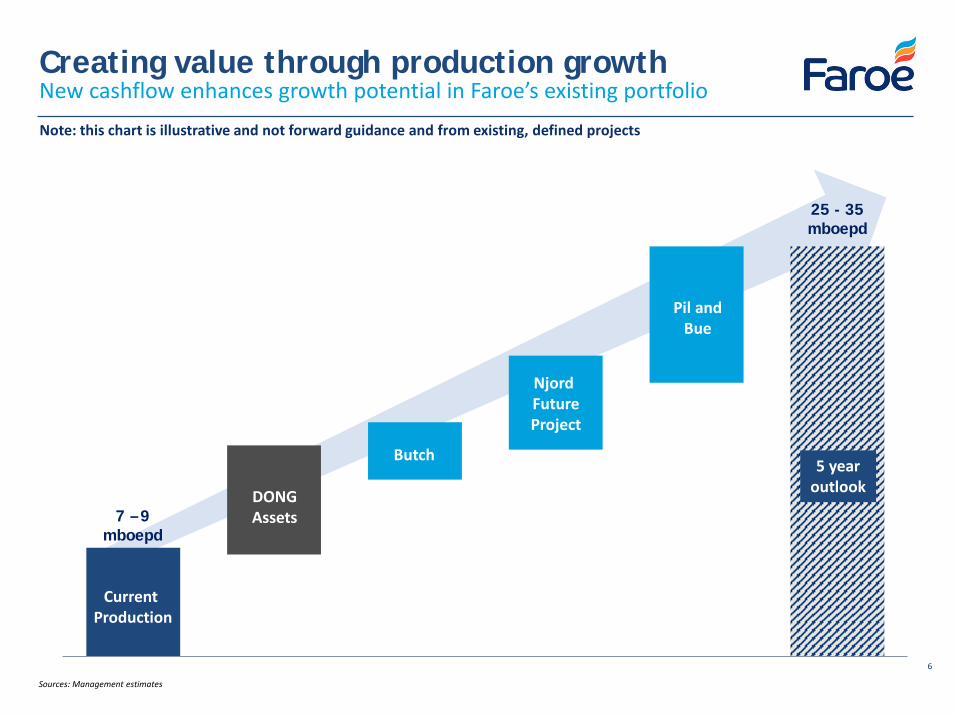

Creating value through production growthNew cashflow enhances growth potential in Faroe’s existing portfolioNote: this chart is illustrative and not forward guidance and from existing, defined projects

Current Production

DONGAssets

Butch

Njord FutureProject

Pil andBue

7 – 9mboepd

25 - 35mboepd

5 yearoutlook

6

Sources: Management estimates

Core Ula hub: UlaSignificant upside from further infill drilling and WAG reinjection scheme

7

Faroe W.I. 20.0%

Operator BP

Partners# BP (80.0%)

2P Reserves Gross (Net)1 42 (8.3) mmboe

2C Resources Gross (Net) 1 34 (7) mmboe

2016 4 months Production Gross2 (Net) 11,000 (2,200) boepd

Field development

3 bridge-linked steel jacket platforms, 7 producing wells, 4 Water Alternating Gas (“WAG”) wells

Host facility for the Blane, Oselvar and Tambar fields and the future host of the Butch development

Oil exported via Ekofisk to Teesside

‒ Gas used for WAG injection for increased oil recovery

Operatorship to be transferred to Aker BP following the proposed merger of Det Norske with BP Norway

‒ Expected to result in renewed exploitation drive

Upside potential

Additional associated gas from Tambar and Butch will allow increased WAG injection scheme

Several infill targets identified, which can be matured to project execution

‒ Triassic reservoir underexploited, only one well drilled to date

Satellite production, infill drilling and increased WAG scheme is expected to result in a significant reduction in Ula unit opex

# Acquisition of Ula is conditional on waiver of pre-emption rights1 CPR Jun 162 Grossed up based on Faroe’s working interest

Faroe W.I. 45.0%

Operator BP

Partners BP (55.0%)

2P Reserves Gross (Net) 1 14 (6.4) mmboe

2C Resources Gross (Net) 1 5 (2) mmboe

2016 4 months Production Gross2 (Net) 5,762 (2,593) boepd

Core Ula hub: TambarLow cost production asset with upside from infill drilling

8

Field development

Unmanned wellhead platform located 16km southeast of Ula

‒ Products transported through Tambar pipeline to Ula for processing

3 production wells, no water injection

‒ Field currently suffers from a lack of artificial lift

Aker BP new operator

Low cost production

Opex per barrel < $20 (including tariff paid to Ula)

Upside potential

Tambar Artificial Lift (TAL) project involves the installation of gas lift in wells to improve the production

‒ Project is at concept select gate, requires approval by Faroe

Two infill wells defined to improve recovery

1 CPR Jun 162 Grossed up based on Faroe’s working interest

Core Ula hub: OselvarMature producing field

9

Faroe W.I. 55.0%

Operator Faroe

Partners CapeOmega (45.0%)

2P Reserves Gross (Net) 1 2 (1.3) mmboe

2016 4 months Production Gross2 (Net) 2,045 (1,125) boepd

Field Development

3 well subsea tie-back to the Ula platform (23km to the northeast)

Production currently scheduled to cease in 2018 to accommodate the Butch development

Compensation payment to be paid by Butch partners (including Faroe at 15%) to Oselvar partners (Faroe 55%), with potential upside adjustments for production and oil price performance

Upside Potential

Compensation payment expected to make a material contribution towards abandonment costs

Limited decommissioning with potential for cost savings

‒ Potential to recover further value through sale and/or reuse of subsea kit

Faroe to consider subsurface potential for future recommencement

1 CPR Jun 162 Grossed up based on the Faroe’s working interest

Core Ula hub: Butch synergy (existing portfolio)Simple, high-return oil development via Ula hub infrastructure

10

* CPR Jan 2016 (Senergy)

Development Project

Located in 66m water depth

‒ Excellent quality reservoir, light oil

Subsea tie-back to the Ula platform via Oselvar infrastructure

2 production wells and 1 water injection well

FEED project on track for completion during Q3 2016

FDP submission currently planned for end 2016

Gross capex expected at c.$645m

Plateau production of c.35,000 boepd gross (c.5,250 boepd net to Faroe)1

First oil expected in 2019

Extracting synergies in the Ula hub

Faroe to capture 55% of Butch compensation payment to Oselvar (Faroe 55%) and 20% of tariff paid to Ula partners (Faroe 20%)

Faroe W.I. 15.0%

Operator Centrica (40.0%)

Partners Suncor (30.0%), Tullow Oil (15.0%)

2P Reserves Gross (Net)* 42 (6.3) mmboe*

1 Based on 100% uptime

Operated Trym gas fieldLow cost production with upside potential

11

Faroe W.I. 50.0%

Operator Faroe

Partners Bayerngas (50.0%)

2P Reserves Gross (Net) 1 8 (3.8) mmboe

2C Resources Gross (Net) 1 4 (2.1) mmboe

2016 4 mnths Production Gross2 (Net) 8,128 (4,064) boepd

Field Development

Subsea tie-back to Mærsk operated Harald facility in the Danish sector

Export via Mærsk operated Tyra platform

‒ Shut-down in Q4 2018 unless a solution found for Tyra subsidence

Acquisition case and 2P case assumes cessation of production in 2018

Upside Potential

Further lowering of the inlet pressure at the gas compressor at Haraldwill allow for extended production and higher reserves

In event of production extending beyond 2018, 2C Resources would be converted to 2P producing reserves

Compensation from Harald partners in case the Harald field is decommissioned before Trym stops producing

Trym

Harald

Tyra

DK

N

1 CPR Jun 162 Grossed up based on Faroe’s working interest

SummaryAttractive value play in the North Sea, enhanced by the transaction

12

Acquisition of DONG assets is transformational

Bilateral deal secures production portfolio in core hub area

Material impact on production, reserves, cash flow and debt capacity

Significant increase in scale

Deal creates material asset base

Balanced and diversified portfolio with stronger production base

New cashflow enhances growth potential in Faroe’s existing portfolio

Continued exposure to significant exploration in Norway

Financially robust

Balance sheet strength and flexibility maintained

Cash generative, low cost operations

Appendices

Prospect EquityQ1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Brasse 50 %

Brasse sidetrack 50 %

Njord NF2 7.5%

Dazzler/Bonè 20 %

Oshun 20 %

Dobby 7.5%

Aerosmith/Iris 20 %

Fogelberg appraisal 25 %

Cassidy 15 %South East Tor 85 %

2016 2017 2018

E&A Drilling activityExploration and appraisal focussing on near field opportunities

14

All exploration wells are in Norway – benefiting from 78% tax rebate incentive

Further attractive exploration well opportunities are being matured including Rungne, Frisbee and Yoshi

Faroe continues to build its portfolio of exploration licences organically

‒ 5 APA exploration licences won in Norway in January 2015 and a further 6 in January 2016

Economic robustness is a crucial element of pre-commitment screening work

committedexpected possible

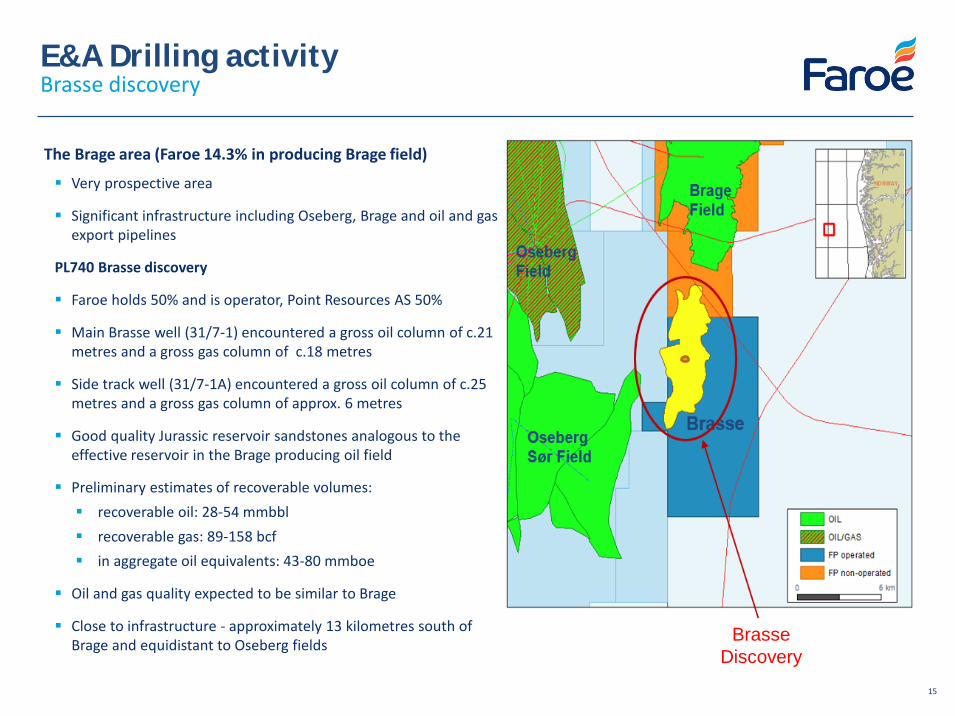

The Brage area (Faroe 14.3% in producing Brage field)

Very prospective area

Significant infrastructure including Oseberg, Brage and oil and gas export pipelines

PL740 Brasse discovery

Faroe holds 50% and is operator, Point Resources AS 50%

Main Brasse well (31/7-1) encountered a gross oil column of c.21 metres and a gross gas column of c.18 metres

Side track well (31/7-1A) encountered a gross oil column of c.25 metres and a gross gas column of approx. 6 metres

Good quality Jurassic reservoir sandstones analogous to the effective reservoir in the Brage producing oil field

Preliminary estimates of recoverable volumes: recoverable oil: 28-54 mmbbl recoverable gas: 89-158 bcf in aggregate oil equivalents: 43-80 mmboe

Oil and gas quality expected to be similar to Brage

Close to infrastructure - approximately 13 kilometres south of Brage and equidistant to Oseberg fields

E&A Drilling activityBrasse discovery

15

BrasseDiscovery

Greater Njord Area Key area for next phase of organic growth

GNA has remaining reserves around 300mmboe*

Njord/Hyme/Snilehorn over 200 mmboe* gross (Faroe over 15mmboe net)

Pil 95 mmboe* gross (Faroe 24 mmboe net)

Bue and Boomerang offer further upside

Njord Future Project: Njord, Hyme, Snilehorn

Njord facility to be refurbished and upgraded

‒ Production stopped June 2016

FDP of scheduled for early 2017

First production targeted for 2020/21

Pil, Bue and Boomerang (Faroe 25%) – 2014 and 2015 Faroe discoveries

Pil development maturing towards concept selection

‒ Njord and Draugen identified as possible tie-back opportunities

‒ Redeployment of FPSO a stand alone alternative

Maturing prospects for possible follow-on exploration opportunities

Njord – Statoil operated Draugen – Shell operated

16* CPR Jan 2016 (Senergy)

Njord

Draugen

Snilehorn& Hyme

Pil & Bue

Graham StewartChief Executive Officer

• Instrumental in founding Faroe Petroleum in 1998

• Over 25 years’ experience in oil and gas technical and commercial affairs

• Previously finance director and commercial director at Dana Petroleum 1997 to 2002

• Experience with Schlumberger, DNV Technica, Petroleum Science & Technology Institute

• Offshore Engineering degree (Heriot-Watt University) and MBA (University of Edinburgh )

Helge Hammer Chief Operating Officer

• Joined Faroe Petroleum in 2006

• Over 25 years’ technical & business experience, incl. Shell (Norway, Oman, Australia and Holland)

• Managing Director of wholly owned Norwegian subsidiary, Faroe Petroleum Norge AS

• Previously Asset Manager and Deputy Managing Director at Paladin Resources

• Economics degree (Institut Françaisdu Pétrole, Paris)

• Petroleum Engineering degree (NTH University of Trondheim)

Jonathan Cooper Chief Financial Officer

• Joined Faroe Petroleum as Chief Financial Officer in July 2013

• Former Finance Director of Gulf Keystone Petroleum and Sterling Energy and CFO of Lamprell plc

• Former Director of the Oil and Gas Corporate Finance Team of Dresdner Kleinwort Wasserstein

• Broad range of experience from mergers and acquisitions, public offerings and financing

• Chartered accountant by training having qualified with KPMG

• PhD Mechanical Engineering (University of Leeds)

Executive team

17

Disclaimer

These materials do not constitute or form any part of any offer or invitation to sell or issue or purchase or subscribe for any shares inFaroe Petroleum plc (the “Company”) nor shall they or any part of them, or the fact of their distribution, form the basis of, or be reliedon in connection with, any contract with the Company relating to any securities. Any decision regarding any proposed acquisition ofshares in the Company must be made solely on the basis of public information on the Company. These materials are not intended tobe distributed or passed on, directly or indirectly, to any other persons. They are available to you solely for your information and maynot be reproduced, forwarded to any other person or published, in whole or in part, for any other purpose.

No reliance may be placed for any purpose whatsoever on the information contained in these materials or on their completeness.Any reliance thereon could potentially expose you to a significant risk of losing all of the property invested by you or the incurring byyou of additional liability. No representation or warranty, express or implied, is given by the Company, its directors or employees, ortheir professional advisers as to the accuracy, fairness, sufficiency or completeness of the information, opinions or beliefs containedin these materials. Save in the case of fraud, no liability is accepted for any loss, cost or damage suffered or incurred as a result ofthe reliance on such information, opinions or beliefs.

Certain statements and graphs throughout these materials are “forward-looking statements” and represent the Company’sexpectations or beliefs concerning, among other things, future operating results and various components thereof, including financialcondition, results of operations, plans, objectives and estimates (including resource estimates), the Company’s anticipated futurecash-flow and expenditure and the Company’s future economic performance. These statements, which may contain the words“anticipate”, “believe”, “intend”, “estimate”, “expect” and words of similar meaning, reflect the directors’ beliefs and expectations andinvolve a number of risks and uncertainties as they relate to events and depend on circumstances that will occur in the future.Forward-looking statements speak only as at the date of these materials and no representation is made that any of these statementsor forecasts will come to pass or that any forecast results will be achieved. The Company expressly disclaims any obligation toupdate or revise any forward-looking statements in these materials, whether as a result of new information or future events.

If you are considering buying shares in the Company, you should consult a person authorised by the Financial Conduct Authoritywho specialises in advising on securities of companies such as Faroe Petroleum plc.

18

Top Related