Languages

Pages

Legal

MANAGEMENT TRAINEESHIP SEGMENT

“Action Research in NRLM Resource Block For Social Mobilization And

Financial Inclusion”

Project Duration: 22nd July, 2013 to 22nd Sep, 2013

KIIT SCHOOL OF RURAL MANAGEMENT, BHUBANESHWAR, ORISSA

SELF

HELP

GROUPS

Host Organization: Uttar Pradesh State Rural Livelihood Mission (UPSRLM)

2

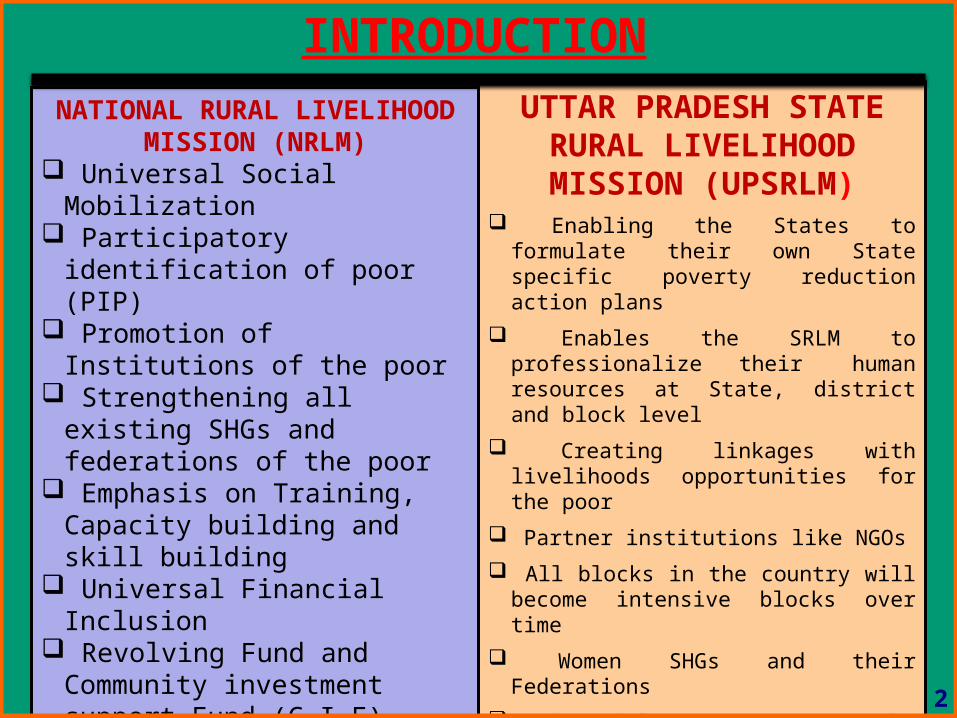

NATIONAL RURAL LIVELIHOOD MISSION (NRLM)

Universal Social Mobilization Participatory identification of poor

(PIP) Promotion of Institutions of the poor Strengthening all existing SHGs and

federations of the poor Emphasis on Training, Capacity

building and skill building Universal Financial Inclusion Revolving Fund and Community

investment support Fund (C.I.F) Provision of Interest Subvention Funding Pattern Phased Implementation Intensive blocks Rural Self Employment Training

Institutes (RSETIs)

UTTAR PRADESH STATE RURAL LIVELIHOOD MISSION (UPSRLM)

Enabling the States to formulate their own State specific poverty reduction action plans

Enables the SRLM to professionalize their human resources at State, district and block level

Creating linkages with livelihoods opportunities for the poor

Partner institutions like NGOs

All blocks in the country will become intensive blocks over time

Women SHGs and their Federations

Financial Assistance to the SHGs

Capital Subsidy has been discontinued under NRLM

Supervision and monitoring of the Scheme

INTRODUCTION

3

Acces

s to

Entitlem

ents

Last Mile Delivery

of Public Services

Financial & Capital Services

Human and Social Capital

(Leaders, CRPs, Community Para-

Professionals)

Dedicated Support Institutions

(Professionals,Learning PlatformM & E Systems)

Producti

on &

Producti

vity

Market Linkages

Institutional Platforms of Poor

(Aggregating and Federating Poor, Women, Small &

Marginal Farmers, SCs and STs)

INNOVATIONS

Livelihood Services

Building Enabling EnvironmentPartnerships and Convergence

NRLM

4

NRLM Path

Identification of the Poor

Organising the Poor

Building their capacities

Show them the path to capital

Facilitating them to choose good livelihoods

Social Development

Safety nets

5

SGSY and NRLM

SGSY NRLM

DRDA as main implementation agency with very limited role at State level

Dedicated professionally managed support organization from State to sub-block level to mobilize poor and nurture their institutions

Community institutional architecture comprised of only SHGs

While SHGs remain the basic unit, higher order structures like SHG federations, producer organizations are planned for last mile service delivery and market access

Income generation focus of SHGs Scope to address multiple dimensions of poverty – assets, skills, incomes, consumption and risks (including food and health risks)

Economic activity focus on investment in common assets and activities

Economic activity focus for provision of support services and aggregation for access to markets

6

7

OBJECTIVESOF THE STUDY

Social Mobilization

To map out and study the SHGs

(promoted by SJGSY,NGO or other

institutions ) in the resource block.

To do Social Mobilization of

people residing in resource block

using PIP approach along with

NRLM guidelines.

Financial Inclusion

To know the problems being faced

by NGO, bank & SHGs.

Suggestions for Role of financial

inclusion through Self help group

To Study the linkage of SHGs

with Nearby banks for Financial

services.

8

Financial constraint.

Response rate is low.

Quality of data (authentication)

Quality of interviewing.

The climatic conditions are not favourable.

Researchers error (sample bias & confounding factors).

Government Officials (block office) support was very discouraging.

RESEARCH LIMITATIONS

Social Mobilization and Financial Inclusion

The study was confined to Hardoi district of Uttar Pradesh state covering only two Gram Panchayat (AHIRORI & KHAKHEDA) with 13 villages.

RESEARCH METHODOLOGY?

9

10

Primary Data Collection

Household & SHG Survey Group Discussion Personal Interviews

INTENT

To know about SHG, and their current status

To know the perception of villagers regarding women SHG

Reason behind deformed SHGs Role of Banks & Block

Secondary Data Collection Block Office, NGOs record books Previous reports & Studies Websites

INTENT

To know no. of SHGs, and their current status

Active or Non-Active SHGs Reason behind deformed SHGs Role of Banks & Block and NGOs To find out Households and BPL list

Tools used: Structured Questionnaire, Group Discussions, Interviews and Observation

RESEARCH METHODOLOGY

RESEARCH DESIGN: Exploratory Research Method

DISTRIBUTION OF LOCATION FOR SURVEY

AHIRORI: Ahirori, Ekghara, Bhanwarja, Nara Purwa, Vayas Purwa, Niranjan Purwa

KHADAKHEDA: Khadakheda, Umari, Baleha, Sarainya, Khapra, Farkan purwa, Dali purwa

11

SELECTION OF THE RESPONDENTS

Gram Panchayat: Ahirori

Sl. No. Village/ Majare Total Households Sampled Households

1 Ahirori 355 79

2 Niranjan Purwa 120 27

3 Vayas Purwa 54 12

4 Nara Purwa 83 18

5 Bhanwarja 78 17

6 Ekghara 210 47

Total 900 200

Gram Panchayat: KhadakhedaSl. No. Village/ Majare Total Households Sampled Households

1 Khadakheda 920 107

2 Umari 286 33

3 Baleha 96 11

4 Sarainya 112 13

5 Khapra 264 31

6 Dali purwa 20 02

7 Farkan purwa 20 02

Total 1718 200

12

Gram Panchayat: Ahirori

Gram P. : Khadakheda

SELECTION OF SHGs for Group Discussion

Total Sampled SHG = 17

For our research study we prepared three types of questionnaire, one for HHS (Household Survey) Another for SHG (Self Help Groups) is to know how

women are performing And third questionnaire was for Bank to know financial activity of respondents.

Sample Size (SHG survey)

S. No. Location Target

1 Ahirori 08

2 Bhawarja 02

Total Sample Size 10

Sample Size (SHG survey)

S. No. Location Target

1 Khadakheda 05

2 Khapra 02

Total Sample Size 07

QUESTIONNAIRE DESIGN

13

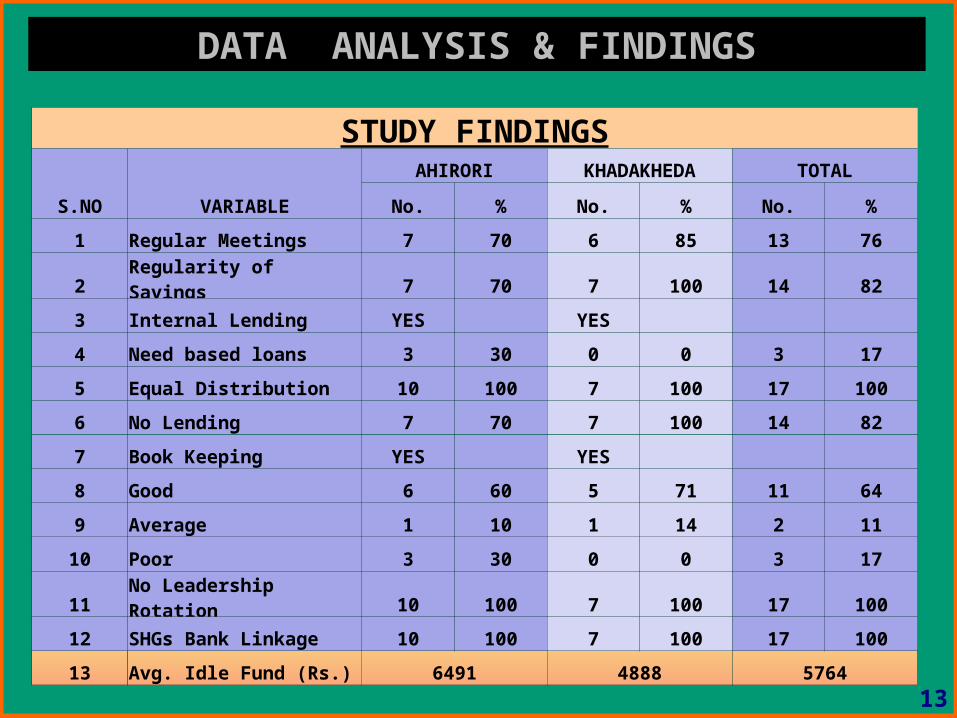

DATA ANALYSIS & FINDINGS

STUDY FINDINGS

S.NO VARIABLE

AHIRORI KHADAKHEDA TOTAL

No. % No. % No. %

1 Regular Meetings 7 70 6 85 13 76

2 Regularity of Savings 7 70 7 100 14 82

3 Internal Lending YES YES

4 Need based loans 3 30 0 0 3 17

5 Equal Distribution 10 100 7 100 17 100

6 No Lending 7 70 7 100 14 82

7 Book Keeping YES YES

8 Good 6 60 5 71 11 64

9 Average 1 10 1 14 2 11

10 Poor 3 30 0 0 3 17

11 No Leadership Rotation 10 100 7 100 17 100

12 SHGs Bank Linkage 10 100 7 100 17 100

13 Avg. Idle Fund (Rs.) 6491 4888 5764

Data Analysis: Section -I

Social Mobilization using PIP Approach

Gram Panchayat : Ahirori (a) Occupation/ Source of Income:

Farm

er

Homem

aker

Artisa

n

Agri-L

abour

Non A

gri-L

abou

r

Stud

ent

Others

0

20

40

60

80

100

120

140

160

180174

7

28

112

76

15

0

Occupation/ Source of Income

Dependence on farming

Landless and marginal farmer depended more on agri and non agri- labour

No industrial zone in near by area

Artisan at a marginal rate but potential to grow

Source: Primary Data

(b) Card Holder Details : Population of No Card

Holders more Although their names listed in BPL 2002 Census list

BPL Card Holder less No land ,No Pacca House and

No job but still come in No card Holders

(c) Average Monthly Income:

Population dependent on Agri and non agri labour more

No Financial support from Bank and Block

Illiteracy

16%

44%

41%

Card Holders Details

BPL

APL

No Card

0-1000 1001-5000 5001-10000 10001-20000

20001 & Above

050

100150200

16

166

12 4 2

Average Monthly Income

Source: Primary Data

Source: Primary Data

(B) SOCIAL MOBILIZATION AND FINANCIAL INCLUSION

(a). SHGs Working Status:

SGSY

2 2 2

1 1

SGSY SHGs Working Status

Bhootnath Gayatri Jai shri ram Shri balaji Durga

RGMPV

1 1 1 1 1

RGMPV SHGs Working Status

Ekta Mahilla Durga mahila Roshni Mahilla

Ekta Mahilla2 New Roshni

Two SHG’s Balaji and Jai Shri Ram are active in the SGSY yojna till now. But, still not get 1st Grading from bank.

Two SHG’s Bhootnath and Gayatri , worked from the year 2002 and closed on 2012-13 . Both SHG’s done their 1st & 2nd grading .

In RGMVP , All SHG’s are active and participatory in nature. In RGMVP, No SHG’s done their 1st & 2nd Grading .

Yes-1 , No-2

Source: Primary Data

(b) Organizations promoted the SHG:

0

5 5

0 0

SHG Promotion

Bank/Financial Institution NGO(RGMVP) Govt. department(SGSY)

Cooperative society Any other

Two Institution ,one Government SGSY and another RGMVP NGO, Promoted the SHG’s .

RGMVP SHG’s working Better on capacity building

approach .

(c) Educational Status:

Illitrate 1st - 5th 6th - 8th 9th - 10th 11th - 12th Above 12th

37

8 5 3 2 1

49

5 1 1 1 2

Educational Status

SGSY RGMVP

Only Three Members educated above 12th One done M.A. and Two B.A

Illiterates in Gram Panchayat at very high rate

Source: Primary Data

Source: Primary Data

(d)

Training details of SHG:

(e) Inter- Lending for activities:

024

Inter Lending

Emergencies Agriculture Animal Husbandry

Income Generations Any Others

Max

Min

Inter lending loan maximum for agriculture as it is prevalent and well known practice among villagers .

Minimum in income generation activities as they not get capacity building training for that .

SHG Health Skills development Livestock0

2

4

6

8

10

10

6

4

7

Training

SHG

Health

Skills development

Livestock

Training on Livestock, skill development and also on health is socializing the members .

Capacity building provided them for make them capable in their activities .

Capacity building on skill development lead them towards more awareness .

Source: Primary Data

Source: Primary Data

Data Analysis: Section -II

Social Mobilization using PIP Approach

Gram Panchayat : Khadakheda(a) Occupation/ Source of Income:

Dependence on farming more

Landless and marginal farmer depended more on agri and non agri labour .

No industrial zone near by there .

Artisan at a marginal rate but potential to grow

81

25

9

94

69

OCCUPATION

FarmerHomemakerArtisianAgri-labourNon agri-labourStudentOthers

Source: Primary Data

(b) Card Holder Details :

Population of No Card Holders more Although their names listed in BPL 2002 Census list .

BPL Card Holder less No land ,No Pacca House and No

job but still come in No card Holders

APL Card Holder were Moderate . Those have BPL Cards but not get

food at the right time .

(c) Average Monthly Income:

Population dependent on Agri and non agri labors more .

No Financial support from Bank and Block .

Education rate fall down No scheme benefited Unawareness among people more

.

APL BPL No Card0

20

40

60

80

100

120

CARD HOLDER

APL BPL No Card

36%

56%

8%

AVERAGE MONTHLY INCOME

0-1000

1001-5000

5001-10000

10001-20000

20001 & Above

Source: Primary Data

Source: Primary Data

(B) SOCIAL MOBILIZATION AND FINANCIAL INCLUSION:

(a) SHGs Working Status:

Eight SHG’s are active in the RGMVP yojna till now. But, still all not done 1st Grading .

Six SHG’s are deformed but the reason behind this is either bank support or coordination problem

In RGMVP , inter-coordination problem leads conflict between females this generally occurs when 1 member takes loan and does not repay it.

Yes-1 , No-2

22

2

2221

11

11 1 1 1

SHG's StatusMaa Veshnu Swayam Sahayata Samuh Sabera Swayam Sahayata SamuhAnokhi Swayam Sahayata Samuh Ekta Swayam Sahayata SamuhaGomti Mahila Swayam Sahayata Samuh ganga Mahila Swayam Sahayata SamuhKarya baba Swayam Sahayata Samuh Aarti Mahila Swayam Sahayat SamuhSaraswati Mahila Swayam Sahayata Samuh Jagrati Swayam Sahayata Samuh

Working-1Not working -2

Source: Primary Data

(b) Organizations promoted the SHG:

0

14 0

0 0

SHG Promotion

Bank/Financial Institution NGO(RGMVP) Govt. department(SGSY)

Cooperative society Any other

No Government Scheme made SHG’s and only RGMVP NGO , Promoted the SHG’s in khadakheda .

RGMVP SHG’s working Better on capacity building

RGMVP Guidelines are same with NRLM .

RGMVP is better approach .

(c) Educational Status:

No Members educated 12th and above 12th..

Illiterates in Gram Panchayat at very high rate . Specially women are more

This Illiteracy causes them towards unawareness .84%

10%

1% 2% 2%

Educational Status

NIL1st - 5th6th - 8th9th - 10th11th - 12thAbove 12th

Source: Primary Data

Source: Primary Data

(d) Training details of SHG: :

Training on Livestock, skill development and also on health is socializing the awareness among members .

Capacity building provided them for make them capable in their activities .

Capacity building on skill development lead them towards more awareness .

(e) No. of transactions in Bank: Maya Mahila SHG’s done

more transaction with banks. Its mean , this SHG is more active .

More transactions with bank leads show good inter-coordination within members .

More transaction with bank lead them towards CCL quickly .

On SHG Skill devel-opment

Livestock Health

Duration 3 8 7 5

No. of Mem-bers

2 1 3 3

5%

25%

45%

65%

85%

Training details of SHGs

8 4 2 1

134 6

No. of transactions in Bank

Source: Primary Data

Source: Primary Data

24

ROLE & MOTIVES OF STAKEHOLDER’S

FinancialInstitution NGO’s BanksIncentives Guidance

Approach for LoanSHG’s

Approval for Loan

Interest for Loan

Econ

omy

Incen

tives

Incom

e

Interest

PROFITS

25

Marginal FarmersLandless Farmers Oral LesseesSelf EmployedMigrantsWomenMinoritiesWomenSocial excluded groupsSenior citizens

Who are excluded ?

26

SHG's made by the NGO (RGMVP) are working in a much better than SGSY SHG's.

Not providing as such any training to SGSY SHG's was one of the main reason

of mismanagement.

Due to this, women's showing reluctance towards NRLM Scheme.

Most of People in villages does not aware with the new government schemes , which lead them towards more poverty.

Women does not have freedom of speech and action.

Due to illiteracy no one takes interest in knowing new things regarding schemes.

IMPLICATION AND LESSION LEARNED

27

RECOMMENDATION & SUGGESTIONS

1. SHG Formation - The target approach to group formation need not be adopted rigidly. Officers should have the time to ‘nurture’ the groups once the names of members have been collected.

2. Grading - Financial targets as well as grading targets should be increased to include left over groups before they loose hope and get defunct like many others.

3. Loan/Financing - The current limits should be immediately revised. Moreover loan financing should be done at lesser rates of 6%-7% as in case of KCC and if possible interest subsidy should also be given.

4. MIS - Proper monitoring of groups needs be done at various stages of their growth. A centralized MIS should be created through which the status of each and every SHG in the remotest part could be monitored.

5. Training - It is essential to draw up a training plan according to the specific requirement of each group. It should be made sure to provide training only for the activity being undertaken or willing to be performed by the group, not any other

6. Shortage of Staff - The number of officers/ADOs needs to be increased. No other work except implementation of NRLM should be given to ADOs.

28

Continued…..7. Economic activity - SHG's members need not be pressured in the matter of choice of

economic activity. Rather they should be provided guidance in terms of viability or sustainability of a particular activity depending on available resources and market.

8. Financial Services - Accountability of Banks needs to be set. Unless and until it is done this scheme can never produce results. Since bankers are also pressurized under their work, separate Bank employees specifically working for Government policies should be appointed.

9. Marketing - Market survey as an important component especially of group activities needs to be stressed. Marketing survey should be conducted for each and every possible economic activity in the rural areas to know about the demand patterns of various products.

10. Float of Funds: The funds which is demand driven by the SHG can be submitted to village federation, they will look after it and than the proposal is forwarded to block federation, they will finalise it and send the same to the bank. This framework will help the in making healthy bank relation and also reduce the bank issues faced by SHG members.

11. Awareness: The villagers does not have any source of getting information regarding schemes. Through this programme this issue can be solved out by giving responsibility to some field workers of demonstration schemes and it benefits.

29

Continued…..

12. Monitoring and Evaluation: This is the backbone of any programme to achieve success. The team of people can be given this job which will help to look after SHG situation and the feedback on it will help to bring necessary changes to make it successful.

13. Marketing - Market survey as an important component especially of group activities needs to be stressed. Marketing survey should be conducted for each and every possible economic activity in the rural areas to know about the demand patterns of various products.

14. Miscellaneous - A programme such as NRLM is not enough to pull the poor out of their poverty without a holistic package of inputs. In addition to the credit programme, they must be supported by at least two welfare programmes of social security and public distribution.

30

For the Groups~ The groups studied rate high on quantity parameters like savings,

lending and bank-linkage, but score a depressing low in terms of quality parameters.

High levels of distrust: A cause for equal distribution of funds and conflicts as a consequence.

Lack of direction and guidance: A cause for increasing number of defunct groups

For the SHG- Bank Linkage~ Stress on optimum savings to extend loans leading to high idle

funds in the groups. Bankers insists that the bank loan be treated as a separate entity

to ensure prompt repayment.

Conclusion

31

PRESENTED BY:

Prachi Mishra (12201029)

Banbasi Sinku (12201008)

Anoop Kr. Mishra (12201005)

Sudhir Kumar (12201038)

32THANK YOU

Top Related