Languages

Pages

Legal

Supplementary Appendix to:

“Uncertainty Shocks and the Cross-Border Funding of Banks:

Unmasking Heterogeneity”

Agustın Benetrix∗

Trinity College Dublin

Michael Curran†

Villanova University

The structure of this appendix is as follows. We report data sources and detail data con-struction in Section S1. Section S2 presents tabular and graphical evidence of the dynamicbehavior of cross-border bank flows. We plot individual time-series for each country’s ag-gregate cross-border liabilities as well as cross-border funding vis-a-vis banks and vis-a-visnon-banks. This Section also illustrates cumulative distribution functions for average growthrates, standard deviations, and persistence of growth rates of cross-border liabilities. We alsoinclude tables of moments for funding growth. Here we plot dispersion as measured by thedifferent quantiles over countries at each point in time and averages against a measure ofturbulence, the correlation of each country’s international rank across the current and priorperiod. In Section S3, similarly, we report tabular and graphical evidence of the dynamicbehavior of the uncertainty measures. We show a correlation matrix between our uncertaintymeasures and we plot cumultative distribution functions for the persistence of uncertaintyas measured by the (i) auto-regressive coefficient and (ii) half-life coefficient. This sectiongraphs dispersion and turbulence of uncertainty measures and reports a table of moments foruncertainty measures. Section S4 presents bivariate and multivariate regression results forthe one period lag of uncertainty variables.

∗Email: [email protected]; Phone: (+353) 1-896-2259Address: Economics Dept., Trinity College Dublin, Dublin 2, Ireland.

†Email: [email protected]; Phone: (+1) 610-519-8867Address: Economics Dept., Villanova School of Business, Villanova University, 800 E Lancaster Ave, PA 19085, USA.

1

2 BENETRIX AND CURRAN

S1 Data Sources and Construction

S1.1 Data Sources

To construct real GDP growth, we obtain data on GDP, exchange rates, GDP deflators, andCPI mostly from the IMF’s IFS.1 We regress GDP deflators on CPI to extend GDP deflatorseries in some instances and use GDP deflators, along with bilateral exchange rates withrespect to the US dollar, to convert nominal GDP to real GDP in billions of US dollars. Formost countries we use seasonally unadjusted data and subsequently seasonally adjust withX12-ARIMA. Data on stock market capitalization is sourced from Bloomberg.2 Inflation ratesare based on CPI from Bloomberg. We use quarter-on-quarter growth in our analysis for realGDP growth, stock market growth, and the inflation rate. Monetary policy rates are sourcedfrom Bloomberg, from BIS central bank policy rates, and by our calculations from nationalcentral bank websites. Data on exchange rates come from the IMF IFS, where we use nominaleffective exchange rate growth in our analysis. Data on exchange rates come from the IMFIFS.3 We investigate effective exchange rates in robustness checks. Credit growth is bankcredit growth to the private non-financial sector and is sourced from BIS. We take externaldebt-to-GDP as outstanding debt securities from the BIS as a percentage of GDP. We restrictour sample to the core group of 24 countries over the period 2003Q1-2018Q4 to achieve abalanced sample. Table S1 lists these core countries.

Table S1: Stock Market Indexes For 24 Core Countries

Reporter BBG Index Reporter BBG Index Reporter BBG Index

Australia AS52 France CAC Portugal BVLXAustria ATX Germany DAX Singapore STIBelgium BELPRC India SENSEX Spain IBEXBrazil IBOV Ireland ISEQ Sweden OMXCanada SPTSX Italy ITLMS Switzerland SPIChile IGPA Japan NKY Turkey XU100Denmark KAX Netherlands AEX UK UKXFinland HEX Norway OSEBX USA SPX

Notes: We source data from Bloomberg. We use Bloomberg’s OVM function to computeimplied volatility at the money for one- and three-month maturities and take the last valuein each quarter. We use quarterly frequency US Dollar nominal price index data to buildmeasures of realized volatility. The full BIS set of 48 reporting countries is the following:Australia, Austria, Bahamas, Bahrain, Belgium, Bermuda, Brazil, Canada, Cayman Islands,Chile, China, Curacao, Cyprus, Denmark, Finland, France, Germany, Greece, Guernsey,Hong Kong, India, Indonesia, Ireland, Isle of Man, Italy, Japan, Jersey, Luxembourg, Macao,Malaysia, Mexico, Netherlands, Norway, Panama, Philippines, Portugal, Russia, Singapore,South Africa, South Korea, Spain, Sweden, Switzerland, Taiwan, Turkey, UK, and USA.

1In a few cases we source data from Bloomberg, OECD, St. Louis FRED, Eurostat, and national centralbank websites.

2We extend the sample by interpolating annual data from the World Bank’s World Development Indicators.3An increase in the exchange rate against the US dollar corresponds to a a weakening or depreciation of

the local currency.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 3

S1.2 Construction

Real GDP

Nominal GDP in domestic currency (GDPDC) is converted to real GDP in billions of USdollars (RGDPUSD), where b = 2010Q3 is the base period, using nominal exchange rate (E)and price level (P ) through the equation

RGDPUSDt =

GDPDCt ×Et

Pt

Pb

Et

Eb

Monetary Policy Target Rates

Australia: RBA cash rate target [RBATCTR].

Brazil : Selic target rate [BZSTSETA].

Canada: Bank of Canada overnight lending rate [CABROVER].

Chile: monetary policy rate (TPM): [CHOVCHOV].

Denmark : repurchase rate repo [DERE].

Euro area: ECB main refinancing operation announcement rate [EURR002W].

India: Reserve Bank of India repurchase effective cut off rate [INRPYLD].

Japan: Bank of Japan unsecured overnight call rate [MUTKCALM].

Norway : deposit rate Norges bank announcement rate [NOBRDEPA].

Singapore: overnight rate: annualized rate of interest bank charges for lending or pay forborrowing a currency [SDDR1T].

Sweden: repo rate (decision rate) [SWRRATEI].

Switzerland : national bank Libor target [SZLTTR].

Turkey : 1 week repo announcement [TUBR1WRA].

United Kingdom: Bank of England official bank rate [UKBRBASE].

United States: US Fed target rate midpoint and US Fed Funds effective rate (source: BIS).

4 BENETRIX AND CURRAN

S2 Dynamic Behavior of Cross-Border Liabilities

Figure S1: Cross-border liabilities

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Australia

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Austria

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Belgium4.

55

5.5

6

2002q3 2006q3 2010q3 2014q3 2018q3

Brazil

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Canada

44.

55

5.5

6

2002q3 2006q3 2010q3 2014q3 2018q3

Chile

Notes: Total cross-border liabilities reported to BIS by country. Log-level of index=100 for 2002Q1.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 5

Figure S2: Cross-border liabilities

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Denmark

45

67

8

2002q3 2006q3 2010q3 2014q3 2018q3

Finland4.

55

5.5

66.

5

2002q3 2006q3 2010q3 2014q3 2018q3

France

4.6

4.8

55.

25.

4

2002q3 2006q3 2010q3 2014q3 2018q3

Germany

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

India

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Ireland

Notes: Total cross-border liabilities reported to BIS by country. Log-level of index=100 for 2002Q1.

6 BENETRIX AND CURRAN

Figure S3: Cross-border liabilities

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Italy

4.6

4.8

55.

25.

45.

6

2002q3 2006q3 2010q3 2014q3 2018q3

Japan4.

55

5.5

6

2002q3 2006q3 2010q3 2014q3 2018q3

Netherlands

4.5

55.

56

6.5

7

2002q3 2006q3 2010q3 2014q3 2018q3

Norway

44.

55

5.5

2002q3 2006q3 2010q3 2014q3 2018q3

Portugal

4.6

4.8

55.

25.

4

2002q3 2006q3 2010q3 2014q3 2018q3

Singapore

Notes: Total cross-border liabilities reported to BIS by country. Log-level of index=100 for 2002Q1.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 7

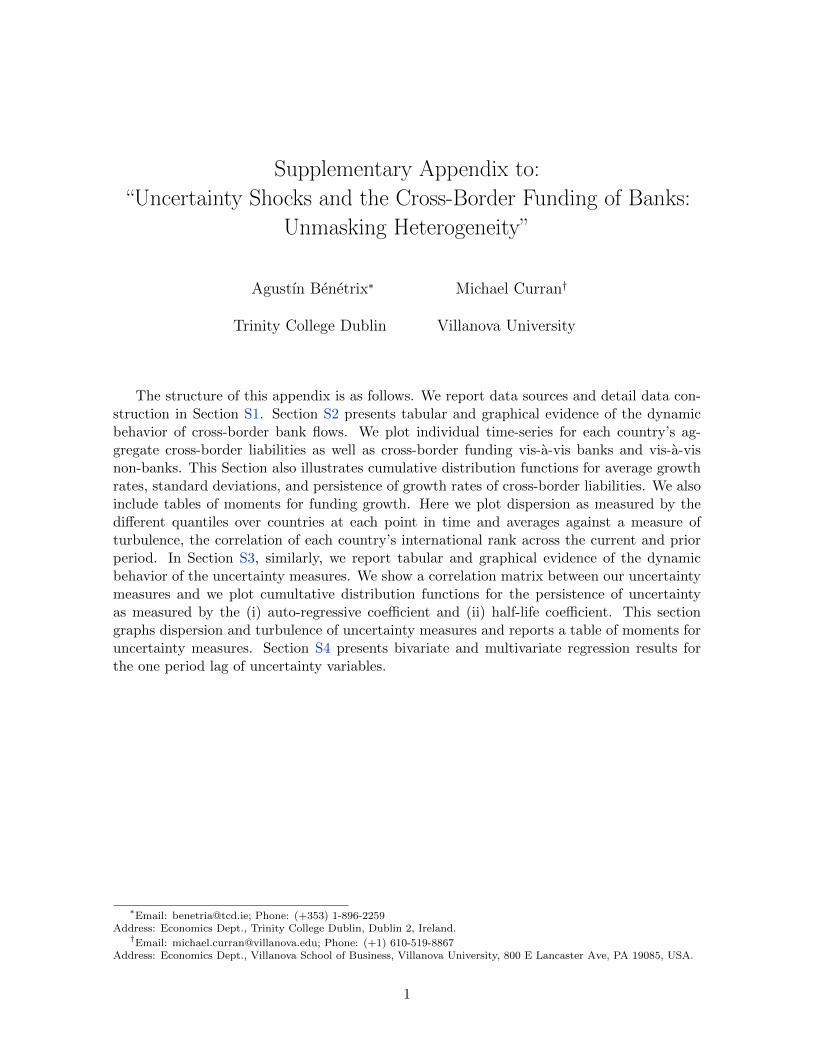

Figure S4: Cross-border liabilities

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Spain

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Sweden4.

64.

85

5.2

5.4

2002q3 2006q3 2010q3 2014q3 2018q3

Switzerland

45

67

8

2002q3 2006q3 2010q3 2014q3 2018q3

Turkey

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

United States

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

United Kingdom

Notes: Total cross-border liabilities reported to BIS by country. Log-level of index=100 for 2002Q1.

8 BENETRIX AND CURRAN

Figure S5: Cross-border liabilities vis-a-vis banks and non-banks4

56

78

9

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Australia

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Austria

44.

55

5.5

6

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Belgium

4.5

55.

56

6.5

7

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Brazil

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Canada

44.

55

5.5

66.

5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Chile

Notes: Total cross-border liabilities reported to BIS by country broken down between banks and non-banks. For cases where vis-a-vis bank data were not available, we compute it as the residual betweentotal liabilities and liabilities vis-a-vis non-banks. These cases are indicated with green vertical linesfor cases where this approach was followed to fill in missing data. Log-level of index=100 for 2002Q1.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 9

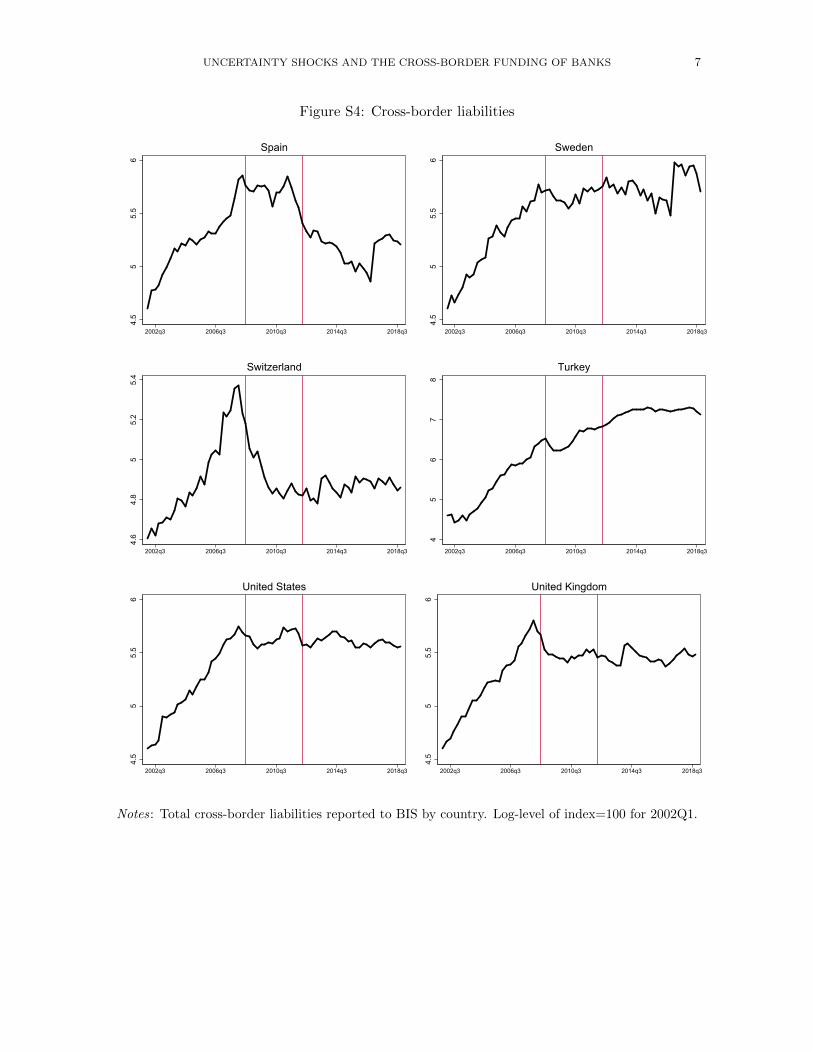

Figure S6: Cross-border liabilities vis-a-vis banks and non-banks4.

55

5.5

66.

5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Denmark

46

810

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Finland

45

67

8

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

France

44.

55

5.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Germany

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

India

4.5

55.

56

6.5

7

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Ireland

Notes: Total cross-border liabilities reported to BIS by country broken down between banks and non-banks. For cases where vis-a-vis bank data were not available, we compute it as the residual betweentotal liabilities and liabilities vis-a-vis non-banks. These cases are indicated with green vertical linesfor cases where this approach was followed to fill in missing data. Log-level of index=100 for 2002Q1.

10 BENETRIX AND CURRAN

Figure S7: Cross-border liabilities vis-a-vis banks and non-banks4.

55

5.5

66.

5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Italy

4.5

55.

56

6.5

7

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Japan

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Netherlands

4.5

55.

56

6.5

7

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Norway

44.

55

5.5

6

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Portugal

4.5

55.

5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Singapore

Notes: Total cross-border liabilities reported to BIS by country broken down between banks and non-banks. For cases where vis-a-vis bank data were not available, we compute it as the residual betweentotal liabilities and liabilities vis-a-vis non-banks. These cases are indicated with green vertical linesfor cases where this approach was followed to fill in missing data. Log-level of index=100 for 2002Q1.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 11

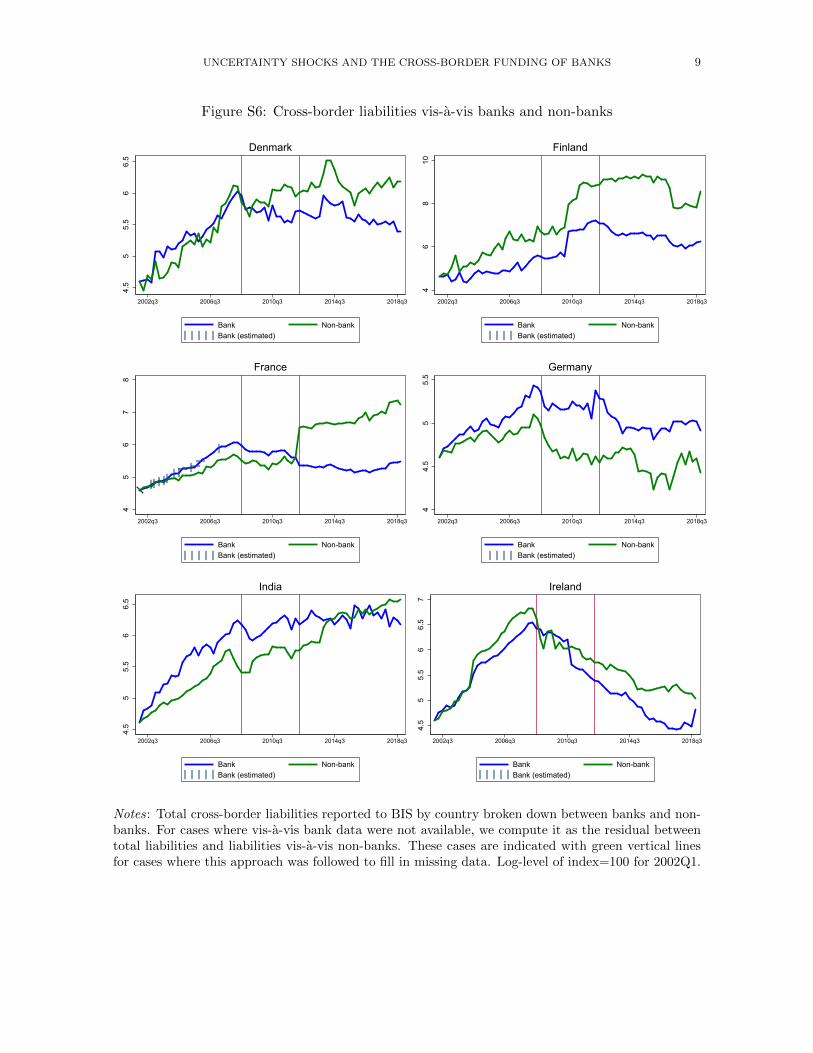

Figure S8: Cross-border liabilities vis-a-vis banks and non-banks4

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Spain

44.

55

5.5

66.

5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Sweden

4.4

4.6

4.8

55.

25.

4

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Switzerland

45

67

89

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

Turkey

4.5

55.

56

6.5

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

United States

4.5

55.

56

2002q3 2006q3 2010q3 2014q3 2018q3

Bank Non-bankBank (estimated)

United Kingdom

Notes: Total cross-border liabilities reported to BIS by country broken down between banks and non-banks. For cases where vis-a-vis bank data were not available, we compute it as the residual betweentotal liabilities and liabilities vis-a-vis non-banks. These cases are indicated with green vertical linesfor cases where this approach was followed to fill in missing data. Log-level of index=100 for 2002Q1.

12 BENETRIX AND CURRAN

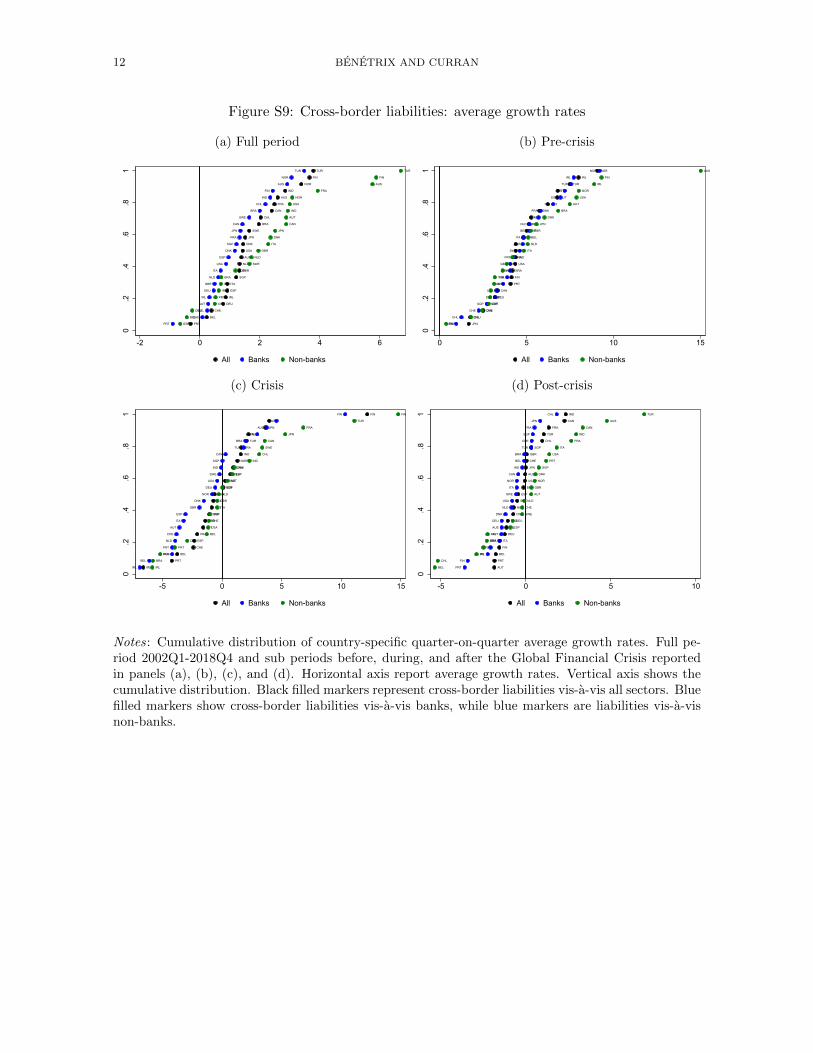

Figure S9: Cross-border liabilities: average growth rates

(a) Full period

PRT

BEL

CHE

DEU

IRL

ESP

ITA

SGP

GBR

NLD

AUT

USA

DNK

JPN

SWE

BRA

CHL

CAN

FRA

AUS

IND

NOR

FIN

TUR

PRT

CHE

BEL

AUT

IRL

DEU

GBR

NLD

ITA

USA

ESP

DNK

SGP

FRA

JPN

CAN

SWE

BRA

CHL

IND

FIN

AUS

NOR

TUR

ESP

BEL

DEU

CHL

PRT

IRL

CHE

BRA

SGP

SWE

NLD

GBR

ITA

DNK

JPN

CAN

AUT

IND

USA

NOR

FRA

AUS

FIN

TUR

0.2

.4.6

.81

-2 0 2 4 6

All Banks Non-banks

(b) Pre-crisis

JPN

CHL

CHE

SGP

DEU

CAN

PRT

FIN

BRA

USA

IND

SWE

GBR

ITA

ESP

BEL

NLD

DNK

AUS

AUT

FRA

TUR

IRL

NOR

JPN

CHL

CHE

SGP

DEU

USA

CAN

FIN

BRA

GBR

PRT

SWE

AUT

ITA

BEL

NLD

DNK

FRA

IND

ESP

AUS

TUR

IRL

NOR

ESP

DEU

CAN

CHE

SGP

PRT

SWE

TUR

IND

CHL

FRA

ITA

NLD

BEL

GBR

JPN

DNK

BRA

AUT

USA

NOR

IRL

FIN

AUS

0.2

.4.6

.81

0 5 10 15

All Banks Non-banks

(c) Crisis

IRL

PRT

BEL

CHE

ESP

FRA

AUT

GBR

DNK

NLD

ITA

USA

SGP

SWE

DEU

CAN

NOR

IND

BRA

TUR

AUS

JPN

CHL

FIN

IRL

BEL

FRA

PRT

NLD

CHE

AUT

ITA

ESP

GBR

DNK

NOR

DEU

USA

SWE

IND

SGP

CAN

TUR

BRA

JPN

AUS

CHL

FIN

IRL

BRA

AUS

PRT

DEU

BEL

USA

CHE

SGP

ITA

GBR

NLD

NOR

AUT

ESP

DNK

IND

CHL

SWE

CAN

JPN

FRA

TUR

FIN

0.2

.4.6

.81

-5 0 5 10 15

All Banks Non-banks

(d) Post-crisis

AUT

PRT

BEL

FIN

ITA

DEU

IRL

NLD

DNK

NOR

SWE

ESP

BRA

USA

AUS

JPN

CHE

GBR

SGP

CHL

TUR

FRA

CAN

IND

PRT

FIN

IRL

ESP

GBR

AUT

AUS

DEU

DNK

NLD

USA

SWE

ITA

NOR

CAN

IND

BEL

BRA

TUR

CHE

SGP

FRA

JPN

CHL

BEL

CHL

IRL

JPN

BRA

FIN

ESP

DEU

SWE

CHE

NLD

AUT

GBR

NOR

DNK

SGP

PRT

USA

ITA

FRA

IND

CAN

AUS

TUR

0.2

.4.6

.81

-5 0 5 10

All Banks Non-banks

Notes: Cumulative distribution of country-specific quarter-on-quarter average growth rates. Full pe-riod 2002Q1-2018Q4 and sub periods before, during, and after the Global Financial Crisis reportedin panels (a), (b), (c), and (d). Horizontal axis report average growth rates. Vertical axis shows thecumulative distribution. Black filled markers represent cross-border liabilities vis-a-vis all sectors. Bluefilled markers show cross-border liabilities vis-a-vis banks, while blue markers are liabilities vis-a-visnon-banks.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 13

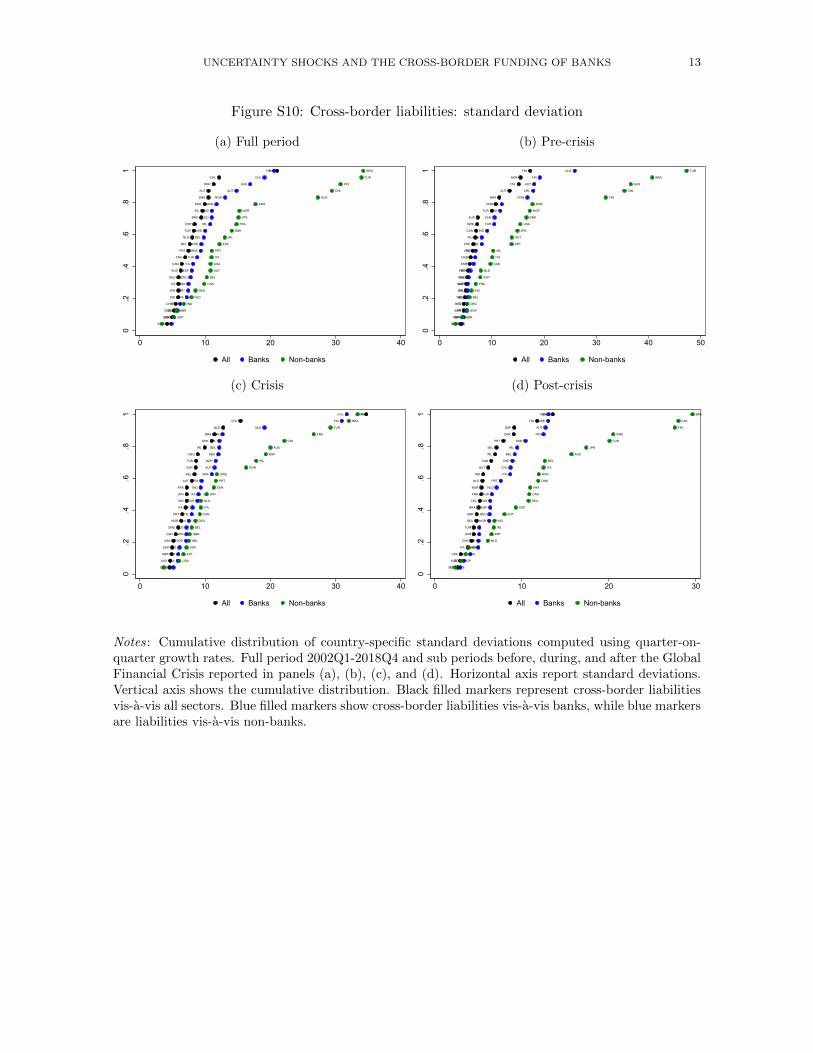

Figure S10: Cross-border liabilities: standard deviation

(a) Full period

SGP

USA

GBR

CHE

IND

JPN

ITA

DEU

AUS

CAN

FRA

PRT

BEL

NLD

TUR

ESP

BRA

IRL

SWE

DNK

AUT

NOR

CHL

FIN

USA

GBR

SGP

JPN

FRA

PRT

CAN

DEU

ESP

ITA

TUR

BRA

CHE

BEL

SWE

IRL

NLD

IND

DNK

NOR

AUT

AUS

CHL

FIN

CHE

SGP

GBR

IND

NLD

DEU

CAN

BEL

AUT

USA

ITA

PRT

ESP

IRL

DNK

FRA

JPN

NOR

SWE

AUS

CHL

FIN

TUR

BRA

0.2

.4.6

.81

0 10 20 30 40

All Banks Non-banks

(b) Pre-crisis

DEU

GBR

SGP

BEL

IND

ITA

NLD

USA

PRT

ESP

FRA

JPN

CHE

IRL

CAN

SWE

AUS

TUR

DNK

BRA

AUT

CHL

NOR

FIN

USA

FRA

PRT

ITA

BEL

DEU

GBR

NLD

ESP

IRL

JPN

SGP

SWE

CAN

IND

TUR

CHE

BRA

DNK

NOR

CHL

AUT

FIN

AUS

CHE

GBR

SGP

DEU

BEL

IND

FRA

ESP

NLD

CAN

ITA

IRL

PRT

AUT

JPN

USA

DNK

NOR

SWE

FIN

CHL

AUS

BRA

TUR

0.2

.4.6

.81

0 10 20 30 40 50

All Banks Non-banks

(c) Crisis

CHE

AUS

GBR

SGP

USA

CAN

SWE

NOR

PRT

ITA

IND

JPN

FRA

AUT

BEL

ESP

TUR

DEU

IRL

DNK

BRA

NLD

CHL

FIN

GBR

USA

PRT

SWE

SGP

JPN

AUS

CAN

CHE

ESP

TUR

ITA

IND

FRA

BRA

AUT

NOR

DEU

BEL

IRL

DNK

NLD

FIN

CHL

CHE

USA

AUT

SGP

IND

GBR

BEL

DEU

CAN

ITA

NLD

JPN

DNK

PRT

SWE

NOR

IRL

ESP

AUS

CHL

FRA

TUR

BRA

FIN

0.2

.4.6

.81

0 10 20 30 40

All Banks Non-banks

(d) Post-crisis

SGP

AUS

USA

ITA

CHE

JPN

TUR

DEU

GBR

BRA

CHL

FRA

NOR

NLD

IND

AUT

CAN

IRL

BEL

PRT

DNK

ESP

FIN

SWE

GBR

SGP

USA

BRA

JPN

TUR

FRA

NOR

DEU

ESP

CAN

AUS

NLD

PRT

ITA

CHL

CHE

BEL

IRL

DNK

FIN

AUT

SWE

IND

CHE

SGP

USA

GBR

NLD

PRT

IRL

IND

AUT

ESP

DEU

CAN

FRA

DNK

NOR

ITA

BEL

AUS

JPN

TUR

SWE

FIN

CHL

BRA

0.2

.4.6

.81

0 10 20 30

All Banks Non-banks

Notes: Cumulative distribution of country-specific standard deviations computed using quarter-on-quarter growth rates. Full period 2002Q1-2018Q4 and sub periods before, during, and after the GlobalFinancial Crisis reported in panels (a), (b), (c), and (d). Horizontal axis report standard deviations.Vertical axis shows the cumulative distribution. Black filled markers represent cross-border liabilitiesvis-a-vis all sectors. Blue filled markers show cross-border liabilities vis-a-vis banks, while blue markersare liabilities vis-a-vis non-banks.

14 BENETRIX AND CURRAN

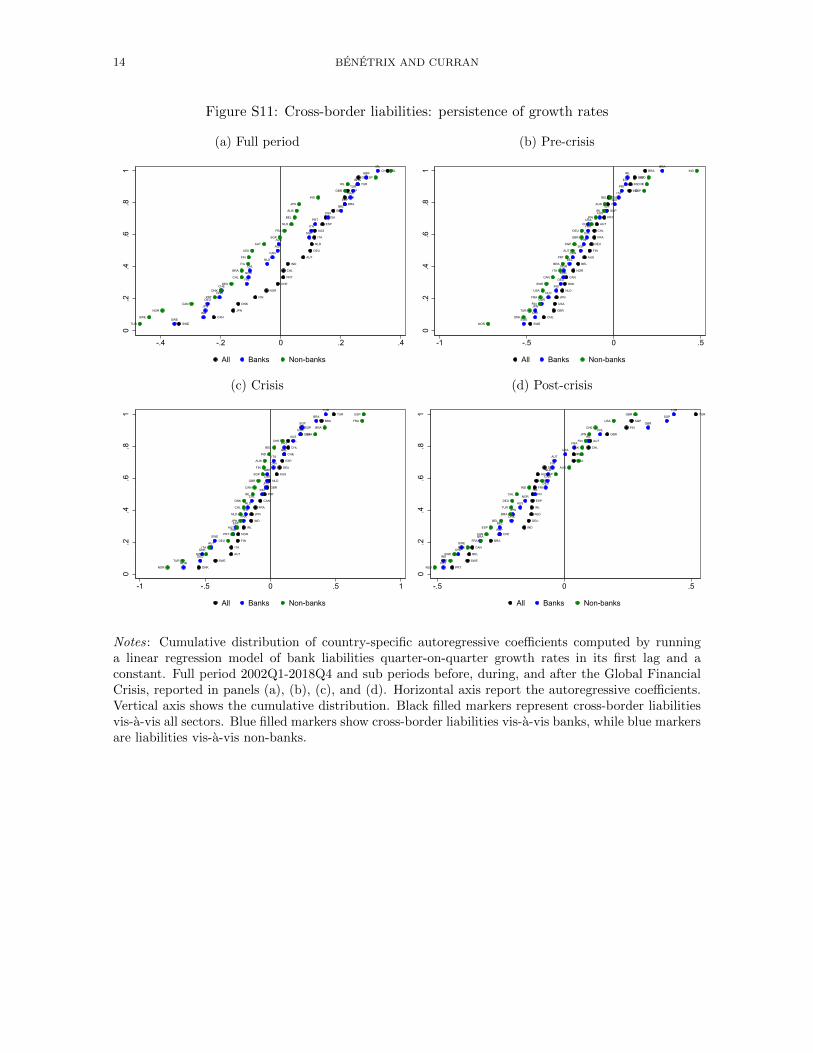

Figure S11: Cross-border liabilities: persistence of growth rates

(a) Full period

SWE

CAN

JPN

DNK

FIN

NOR

CHE

PRT

CHL

IND

AUT

DEU

NLD

ITA

AUS

ESP

USA

BEL

BRA

FRA

SGP

TUR

GBR

IRL

SWE

IND

JPN

DEU

DNK

CHE

FIN

NOR

CHL

NLD

CAN

AUT

AUS

SGP

ITA

PRT

USA

BEL

ESP

FRA

TUR

BRA

GBR

IRL

TUR

SWE

NOR

CAN

PRT

DNK

DEU

CHL

BRA

ITA

FIN

USA

AUT

SGP

FRA

NLD

BEL

AUS

JPN

IND

GBR

IRL

ESP

CHE

0.2

.4.6

.81

-.4 -.2 0 .2 .4

All Banks Non-banks

(b) Pre-crisis

SWE

CHE

GBR

USA

JPN

NLD

DNK

CAN

NOR

BEL

AUS

FIN

DEU

FRA

CHL

AUT

PRT

SGP

ITA

TUR

IND

IRL

ESP

BRA

SWE

CHE

JPN

GBR

NLD

IND

DEU

DNK

NOR

BEL

CAN

SGP

FIN

CHL

FRA

USA

AUS

TUR

AUT

ITA

PRT

ESP

IRL

BRA

NOR

DNK

TUR

FIN

FRA

USA

SWE

CAN

ITA

BRA

PRT

AUT

SGP

GBR

DEU

CHL

JPN

IRL

AUS

BEL

ESP

CHE

NLD

IND

0.2

.4.6

.81

-1 -.5 0 .5

All Banks Non-banks

(c) Crisis

DNK

SWE

AUT

ITA

FIN

NOR

IRL

IND

JPN

FRA

CAN

PRT

GBR

NLD

AUS

DEU

ESP

CHE

CHL

BEL

USA

SGP

BRA

TUR

NOR

DEU

DNK

AUT

SWE

FIN

ESP

FRA

IRL

NLD

CHL

IND

JPN

CHE

GBR

CAN

ITA

BEL

PRT

AUS

USA

SGP

BRA

TUR

NOR

TUR

SWE

ITA

DEU

PRT

AUT

JPN

NLD

CHL

DNK

IRL

CAN

GBR

SGP

FIN

AUS

IND

BEL

CHE

USA

BRA

FRA

ESP

0.2

.4.6

.81

-1 -.5 0 .5 1

All Banks Non-banks

(d) Post-crisis

PRT

SWE

BEL

CAN

BRA

CHE

IND

DEU

NLD

IRL

ESP

JPN

FRA

NOR

AUS

DNK

USA

ITA

CHL

AUT

GBR

FIN

SGP

TUR

PRT

IND

CHE

SWE

BRA

ESP

BEL

DNK

JPN

AUS

NOR

ITA

DEU

CAN

NLD

FIN

AUT

USA

FRA

IRL

CHL

GBR

SGP

TUR

NLD

PRT

SWE

NOR

FRA

CAN

ESP

BEL

BRA

TUR

DEU

CHL

IND

IRL

SGP

AUS

ITA

AUT

DNK

FIN

JPN

CHE

USA

GBR

0.2

.4.6

.81

-.5 0 .5

All Banks Non-banks

Notes: Cumulative distribution of country-specific autoregressive coefficients computed by runninga linear regression model of bank liabilities quarter-on-quarter growth rates in its first lag and aconstant. Full period 2002Q1-2018Q4 and sub periods before, during, and after the Global FinancialCrisis, reported in panels (a), (b), (c), and (d). Horizontal axis report the autoregressive coefficients.Vertical axis shows the cumulative distribution. Black filled markers represent cross-border liabilitiesvis-a-vis all sectors. Blue filled markers show cross-border liabilities vis-a-vis banks, while blue markersare liabilities vis-a-vis non-banks.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 15

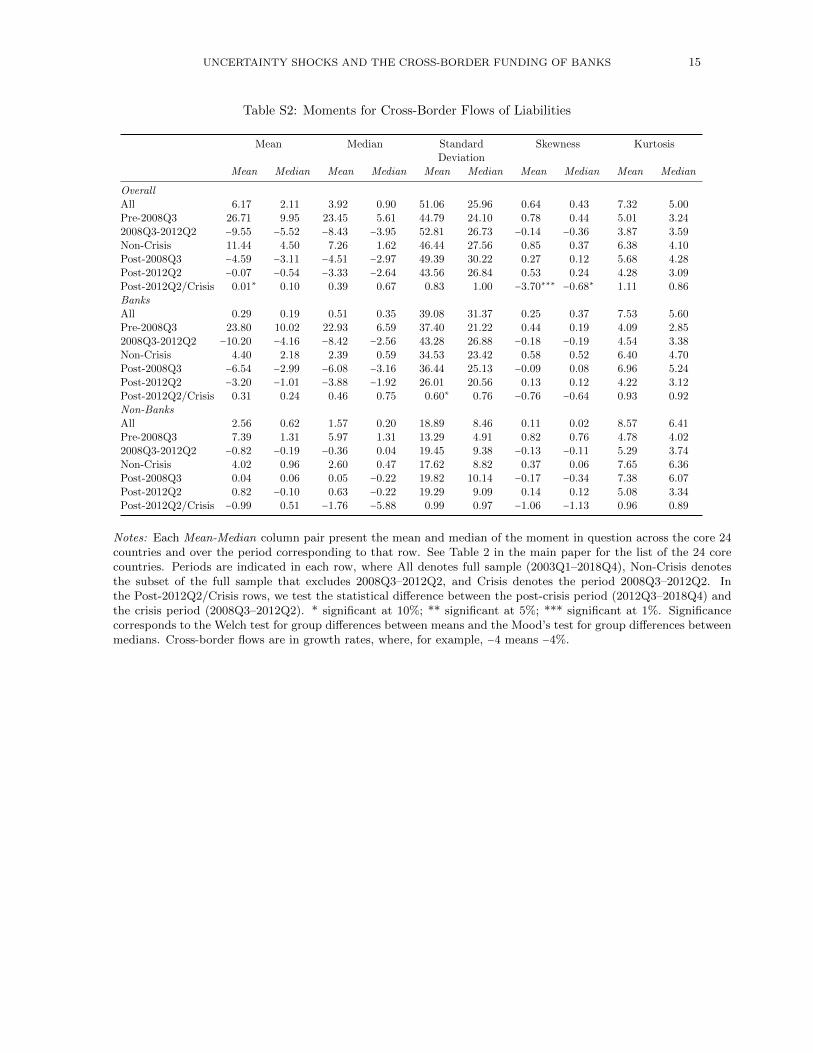

Table S2: Moments for Cross-Border Flows of Liabilities

Mean Median Standard Skewness KurtosisDeviation

Mean Median Mean Median Mean Median Mean Median Mean Median

OverallAll 6.17 2.11 3.92 0.90 51.06 25.96 0.64 0.43 7.32 5.00Pre-2008Q3 26.71 9.95 23.45 5.61 44.79 24.10 0.78 0.44 5.01 3.242008Q3-2012Q2 −9.55 −5.52 −8.43 −3.95 52.81 26.73 −0.14 −0.36 3.87 3.59Non-Crisis 11.44 4.50 7.26 1.62 46.44 27.56 0.85 0.37 6.38 4.10Post-2008Q3 −4.59 −3.11 −4.51 −2.97 49.39 30.22 0.27 0.12 5.68 4.28Post-2012Q2 −0.07 −0.54 −3.33 −2.64 43.56 26.84 0.53 0.24 4.28 3.09Post-2012Q2/Crisis 0.01∗ 0.10 0.39 0.67 0.83 1.00 −3.70∗∗∗ −0.68∗ 1.11 0.86BanksAll 0.29 0.19 0.51 0.35 39.08 31.37 0.25 0.37 7.53 5.60Pre-2008Q3 23.80 10.02 22.93 6.59 37.40 21.22 0.44 0.19 4.09 2.852008Q3-2012Q2 −10.20 −4.16 −8.42 −2.56 43.28 26.88 −0.18 −0.19 4.54 3.38Non-Crisis 4.40 2.18 2.39 0.59 34.53 23.42 0.58 0.52 6.40 4.70Post-2008Q3 −6.54 −2.99 −6.08 −3.16 36.44 25.13 −0.09 0.08 6.96 5.24Post-2012Q2 −3.20 −1.01 −3.88 −1.92 26.01 20.56 0.13 0.12 4.22 3.12Post-2012Q2/Crisis 0.31 0.24 0.46 0.75 0.60∗ 0.76 −0.76 −0.64 0.93 0.92Non-BanksAll 2.56 0.62 1.57 0.20 18.89 8.46 0.11 0.02 8.57 6.41Pre-2008Q3 7.39 1.31 5.97 1.31 13.29 4.91 0.82 0.76 4.78 4.022008Q3-2012Q2 −0.82 −0.19 −0.36 0.04 19.45 9.38 −0.13 −0.11 5.29 3.74Non-Crisis 4.02 0.96 2.60 0.47 17.62 8.82 0.37 0.06 7.65 6.36Post-2008Q3 0.04 0.06 0.05 −0.22 19.82 10.14 −0.17 −0.34 7.38 6.07Post-2012Q2 0.82 −0.10 0.63 −0.22 19.29 9.09 0.14 0.12 5.08 3.34Post-2012Q2/Crisis −0.99 0.51 −1.76 −5.88 0.99 0.97 −1.06 −1.13 0.96 0.89

Notes: Each Mean-Median column pair present the mean and median of the moment in question across the core 24countries and over the period corresponding to that row. See Table 2 in the main paper for the list of the 24 corecountries. Periods are indicated in each row, where All denotes full sample (2003Q1–2018Q4), Non-Crisis denotesthe subset of the full sample that excludes 2008Q3–2012Q2, and Crisis denotes the period 2008Q3–2012Q2. Inthe Post-2012Q2/Crisis rows, we test the statistical difference between the post-crisis period (2012Q3–2018Q4) andthe crisis period (2008Q3–2012Q2). * significant at 10%; ** significant at 5%; *** significant at 1%. Significancecorresponds to the Welch test for group differences between means and the Mood’s test for group differences betweenmedians. Cross-border flows are in growth rates, where, for example, −4 means −4%.

16 BENETRIX AND CURRAN

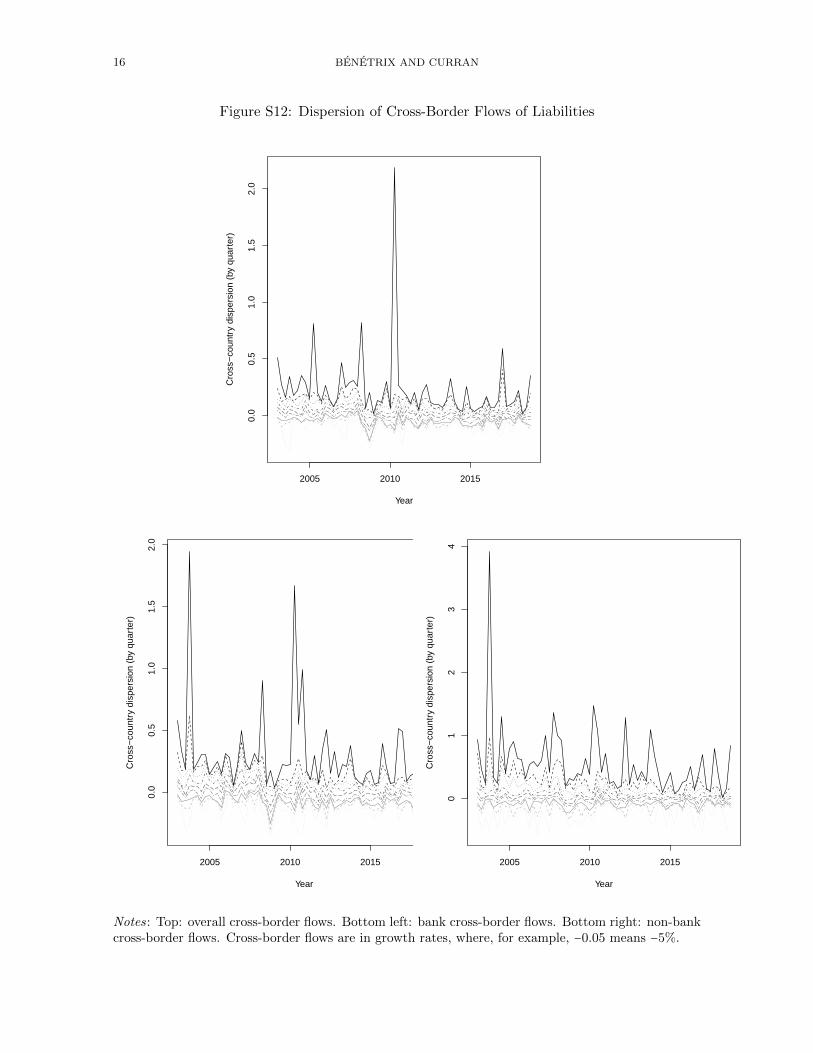

Figure S12: Dispersion of Cross-Border Flows of Liabilities

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

0.0

0.5

1.0

1.5

2.0

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

0.0

0.5

1.0

1.5

2.0

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

01

23

4

Notes: Top: overall cross-border flows. Bottom left: bank cross-border flows. Bottom right: non-bankcross-border flows. Cross-border flows are in growth rates, where, for example, −0.05 means −5%.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 17

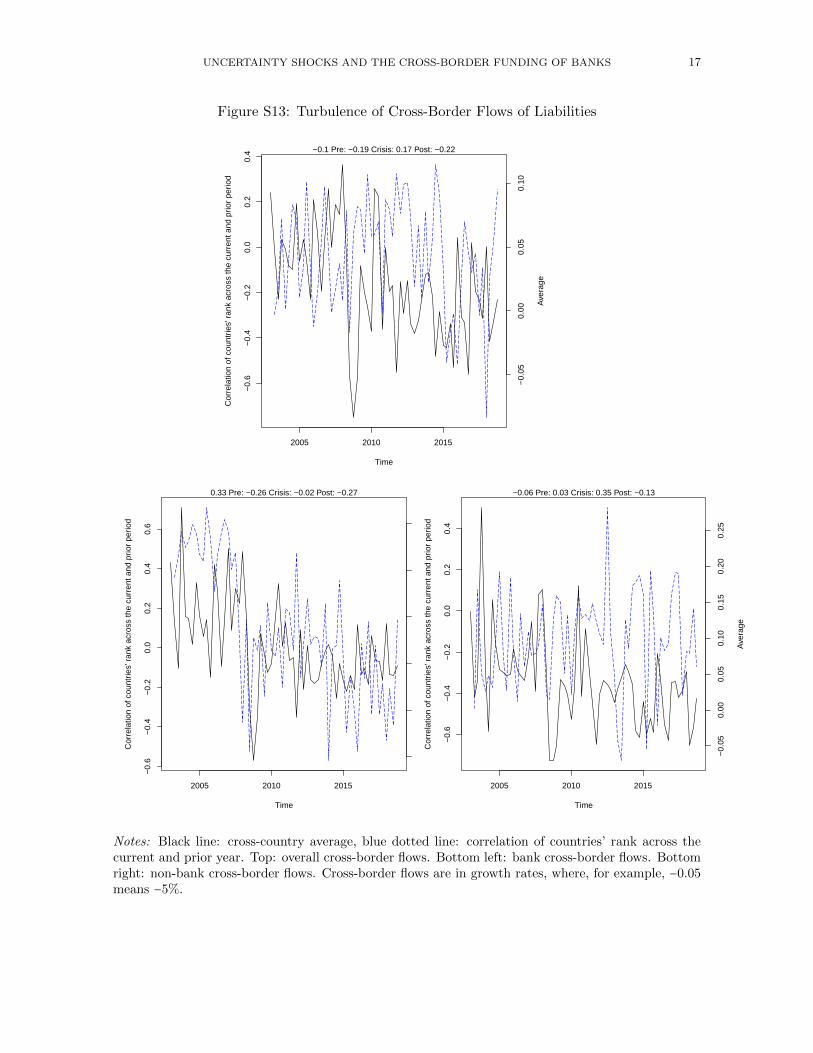

Figure S13: Turbulence of Cross-Border Flows of Liabilities

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

−0.

6−

0.4

−0.

20.

00.

20.

4

−0.

050.

000.

050.

10

Ave

rage

−0.1 Pre: −0.19 Crisis: 0.17 Post: −0.22

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

−0.

6−

0.4

−0.

20.

00.

20.

40.

6

−0.

10−

0.05

0.00

0.05

0.10

0.15

Ave

rage

0.33 Pre: −0.26 Crisis: −0.02 Post: −0.27

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

−0.

6−

0.4

−0.

20.

00.

20.

4

−0.

050.

000.

050.

100.

150.

200.

25

Ave

rage

−0.06 Pre: 0.03 Crisis: 0.35 Post: −0.13

Notes: Black line: cross-country average, blue dotted line: correlation of countries’ rank across thecurrent and prior year. Top: overall cross-border flows. Bottom left: bank cross-border flows. Bottomright: non-bank cross-border flows. Cross-border flows are in growth rates, where, for example, −0.05means −5%.

18 BENETRIX AND CURRAN

S3 Dynamic Behavior of Uncertainty Measures

Table S3: Correlation Matrix Between Uncertainty Measures

Uncertainty IV3 IV1 RV EPU WUI FD

IV3 1.0000 0.8779 0.1698 0.0940 −0.0172 0.0307IV1 0.8779 1.0000 0.1711 0.0203 −0.0060 −0.0012RV 0.1698 0.1711 1.0000 0.0244 0.0007 −0.0552

EPU 0.0940 0.0203 0.0244 1.0000 0.1513 −0.1632WUI −0.0172 −0.0060 0.0007 0.1513 1.0000 −0.1909FD 0.0307 −0.0012 −0.0552 −0.1632 −0.1909 1.0000

Notes: Correlation matrix for uncertainty measures: implied volatility at three- and one-month maturities, realizedvolatility, EPU, WUI, and forecast dispersion.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 19

Table S4: Moments for Uncertainty Measures

Mean Median Standard Skewness KurtosisDeviation

Mean Median Mean Median Mean Median Mean Median Mean Median

IV3All 2.91 2.93 2.87 2.89 0.37 0.36 0.72 0.70 3.98 3.31Pre-2008Q3 2.81 2.79 2.79 2.74 0.33 0.34 0.42 0.46 2.46 2.312008Q3-2012Q2 3.12 3.19 3.02 3.03 0.38 0.37 0.83 0.67 3.23 2.85Non-Crisis 2.81 2.82 2.78 2.77 0.31 0.30 0.42 0.36 3.18 2.55Post-2008Q3 2.96 2.97 2.91 2.93 0.37 0.34 0.93 0.84 4.06 3.46Post-2012Q2 2.81 2.79 2.76 2.74 0.27 0.26 0.43 0.31 2.78 2.09Post-2012Q2/Crisis 0.90∗∗∗ 0.87∗∗∗ 0.91∗∗∗ 0.90∗∗∗ 0.69 0.70∗∗∗ 0.52∗∗∗ 0.46∗∗∗ 0.86 0.73∗∗∗

IV1All 2.86 2.88 2.82 2.86 0.42 0.40 0.61 0.48 3.56 2.94Pre-2008Q3 2.75 2.73 2.70 2.66 0.38 0.39 0.52 0.45 2.68 2.532008Q3-2012Q2 3.07 3.15 2.99 3.00 0.42 0.39 0.63 0.53 2.81 2.38Non-Crisis 2.76 2.75 2.72 2.67 0.37 0.36 0.53 0.47 3.43 2.79Post-2008Q3 2.91 2.92 2.86 2.86 0.41 0.38 0.74 0.62 3.51 3.04Post-2012Q2 2.76 2.72 2.72 2.67 0.33 0.32 0.61 0.47 3.30 2.61Post-2012Q2/Crisis 0.90∗∗∗ 0.86∗∗∗ 0.91∗∗∗ 0.89∗∗∗ 0.80∗∗ 0.83∗∗ 0.98 0.89 1.17 1.10Realized VolatilityAll 3.01 3.01 2.96 2.92 0.39 0.41 0.78 0.74 3.88 3.68Pre-2008Q3 2.93 2.87 2.88 2.84 0.29 0.30 0.79 0.77 3.16 2.902008Q3-2012Q2 3.30 3.32 3.21 3.21 0.40 0.40 0.82 0.86 3.41 3.31Non-Crisis 2.89 2.85 2.86 2.82 0.30 0.30 0.43 0.34 3.06 2.96Post-2008Q3 3.06 3.06 3.02 3.00 0.42 0.43 0.67 0.69 3.69 3.55Post-2012Q2 2.83 2.79 2.80 2.74 0.29 0.29 0.28 0.30 2.91 2.71Post-2012Q2/Crisis 0.86∗∗∗ 0.84∗∗∗ 0.87∗∗∗ 0.85∗∗∗ 0.74∗∗∗ 0.74∗∗∗ 0.34∗∗ 0.35∗∗∗ 0.86∗∗ 0.82∗∗

EPUAll sample 4.74 4.70 4.76 4.69 0.45 0.47 −0.03 0.02 2.63 2.55Pre-2008Q3 4.37 4.37 4.35 4.36 0.37 0.35 0.59 0.64 3.59 3.592008Q3-2012Q2 4.94 4.93 4.94 4.92 0.31 0.34 −0.03 −0.07 2.40 2.25Non-Crisis 4.68 4.65 4.70 4.64 0.47 0.50 0.11 0.10 2.61 2.67Post-2008Q3 4.94 4.83 4.93 4.85 0.35 0.35 0.10 0.14 2.74 2.71Post-2012Q2 4.94 4.81 4.95 4.84 0.33 0.33 0.20 0.14 2.89 2.72Post-2012Q2/Crisis 1.00 0.98 1.00 0.98 1.09 0.98 −5.89∗ −2.12 1.21∗∗ 1.21∗∗∗

WUIAll sample 2.43 2.48 2.72 2.77 1.20 1.24 −0.89 −1.08 3.34 3.09Pre-2008Q3 2.07 2.19 2.25 2.35 1.14 1.20 −0.58 −0.64 2.64 2.362008Q3-2012Q2 2.31 2.35 2.54 2.74 1.24 1.28 −0.80 −0.70 3.45 2.06Non-Crisis 2.53 2.55 2.79 2.83 1.15 1.14 −0.91 −1.02 3.33 2.96Post-2008Q3 2.62 2.65 2.85 2.98 1.18 1.19 −1.19 −1.33 4.24 3.93Post-2012Q2 2.90 2.96 3.11 3.21 0.93 0.93 −1.10 −1.26 4.48 3.74Post-2012Q2/Crisis 1.26∗∗∗ 1.26∗∗∗ 1.23∗∗ 1.17∗∗ 0.75∗∗∗ 0.72∗∗ 1.37 1.79 1.30 1.82∗∗

Forecast DispersionAll sample 2.48 3.01 2.37 2.89 0.70 0.64 0.18 0.26 2.65 2.36Pre-2008Q3 2.75 2.91 2.78 2.81 0.62 0.57 −0.12 −0.19 2.31 2.262008Q3-2012Q2 2.46 3.09 2.24 3.03 0.68 0.67 0.35 0.30 2.76 2.27Non-Crisis 2.45 2.82 2.50 2.81 0.68 0.61 −0.01 −0.03 2.40 2.20Post-2008Q3 2.36 3.00 2.19 2.99 0.67 0.67 0.42 0.37 3.03 2.78Post-2012Q2 2.27 2.73 2.14 2.84 0.61 0.55 0.20 0.20 2.52 2.42Post-2012Q2/Crisis 0.92 0.88 0.95 0.94 0.90 0.83 0.58 0.67 0.91 1.06

Notes: See notes to Table S2. To ensure consistency across uncertainty measures throughout the analysis, we useln (EPU + 1) for EPU. Similarly, denoting WUI and the forecast-based measures by x, we transform x to ln (100x + 1).

20 BENETRIX AND CURRAN

Figure S14: Dispersion of Uncertainty Measures

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

23

45

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 20152

34

5

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

2.0

2.5

3.0

3.5

4.0

4.5

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

3.5

4.0

4.5

5.0

5.5

6.0

6.5

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

01

23

45

Year

Cro

ss−

coun

try

disp

ersi

on (

by q

uart

er)

2005 2010 2015

01

23

45

Notes: Top row from left to right: implied-volatility at 3 month maturity (IV3), implied-volatilityat 1 month maturity (IV1), realized volatility (RV). Bottom row from left to right: economic policyuncertainty (EPU) index, world uncertainty index (WUI), forecast dispersion. See Section 2 in themain paper for detailed description of uncertainty measures.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 21

Turbulence of Uncertainty Measures

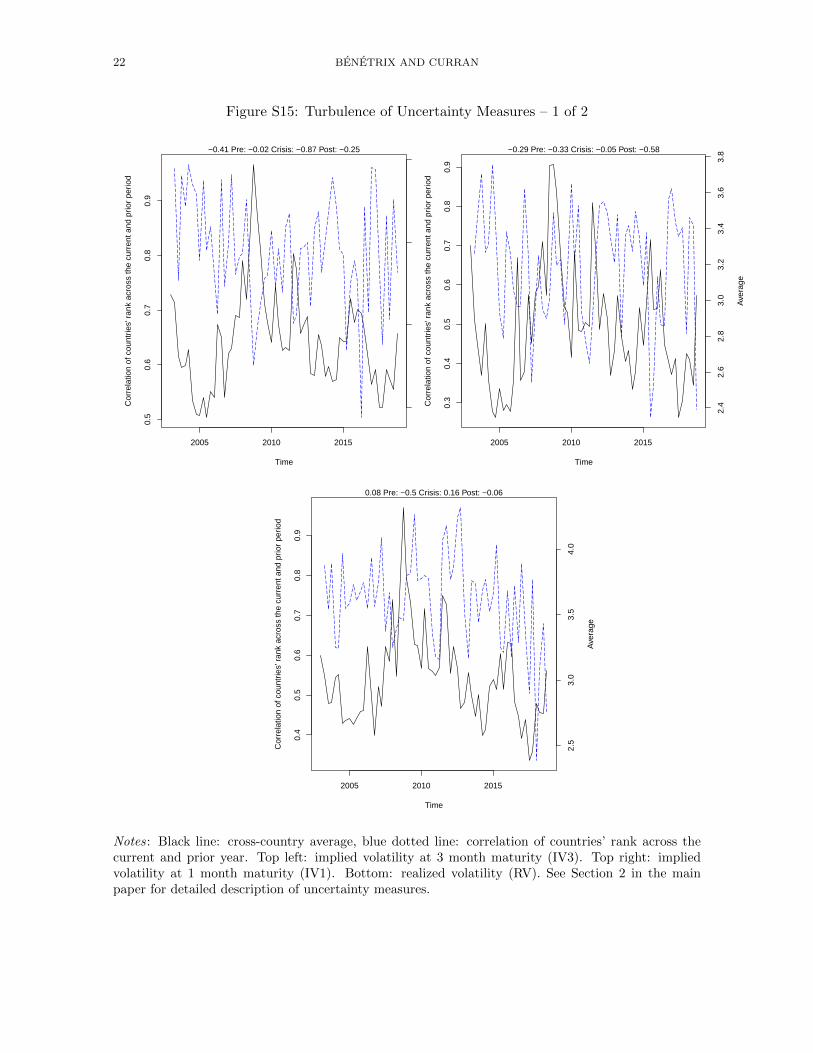

Turbulence is negatively correlated with averages for measures of realized volatility, EPU,WUI, and bank flows of liabilities. That is, there is little turbulence when these variables arehigh. In contrast, turbulence is strong when the following variables are high: implied volatility,forecast dispersion, and overall and non-bank flows of liabilities. Sub-samples display hetero-geneity. Serial correlation of countries’ rank is positive (low turbulence) with large differencesover time for realized volatility, implied volatility, and WUI. Turbulence for realized volatilityand implied volatility displays a modest increase during the crisis, while turbulence marginallydecreases over time for WUI. Turbulence displays no discernible patterns being roughly con-stant with small changes for EPU and forecast-based measures of uncertainty. With bankingflows, large changes occur in the serial correlation of countries’ rank over time. For overalland non-bank flows of liabilities, serial correlation of countries’ rank is weakly positive (someturbulence), with large, regular, seesaw-like oscillations over time akin to white noise. Forbank flows of liabilities, this rank order correlation becomes negative (strong turbulence) fromthe crisis onward.

22 BENETRIX AND CURRAN

Figure S15: Turbulence of Uncertainty Measures – 1 of 2

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

0.5

0.6

0.7

0.8

0.9

2.5

3.0

3.5

4.0

Ave

rage

−0.41 Pre: −0.02 Crisis: −0.87 Post: −0.25

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 20150.

30.

40.

50.

60.

70.

80.

9

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

Ave

rage

−0.29 Pre: −0.33 Crisis: −0.05 Post: −0.58

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

0.4

0.5

0.6

0.7

0.8

0.9

2.5

3.0

3.5

4.0

Ave

rage

0.08 Pre: −0.5 Crisis: 0.16 Post: −0.06

Notes: Black line: cross-country average, blue dotted line: correlation of countries’ rank across thecurrent and prior year. Top left: implied volatility at 3 month maturity (IV3). Top right: impliedvolatility at 1 month maturity (IV1). Bottom: realized volatility (RV). See Section 2 in the mainpaper for detailed description of uncertainty measures.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 23

Figure S16: Turbulence of Uncertainty Measures – 2 of 2

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

0.75

0.80

0.85

0.90

0.95

4.0

4.5

5.0

5.5

Ave

rage

0.35 Pre: −0.3 Crisis: 0.14 Post: 0.42

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 20150.

00.

20.

40.

60.

8

1.5

2.0

2.5

3.0

3.5

Ave

rage

0.16 Pre: −0.18 Crisis: −0.53 Post: −0.21

Time

Cor

rela

tion

of c

ount

ries'

ran

k ac

ross

the

curr

ent a

nd p

rior

perio

d

2005 2010 2015

0.80

0.85

0.90

0.95

0.15

0.20

0.25

0.30

0.35

0.40

0.45

Ave

rage

−0.04 Pre: 0 Crisis: −0.26 Post: −0.23

Notes: Black line: cross-country average, blue dotted line: correlation of countries’ rank across the cur-rent and prior year. Top left: economic policy uncertainty (EPU) index. Top right: world uncertaintyindex (WUI). Bottom: forecast dispersion. See Section 2 in the main paper for detailed description ofuncertainty measures.

24 BENETRIX AND CURRAN

Figure S17: AR(1) Persistence of Uncertainty

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGPESP

SWE

CHE

TUR

USA

GRB

0.2

.4.6

.81

.988 .99 .992 .994 .996RV

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESP

SWE

CHE

TUR

USA

GRB

AUSBRA

CAN

CHL

FRA

DEU

INDIRL

ITAJPN

NDL

SGP

ESP

SWEUSA

GRB

0.2

.4.6

.81

.6 .7 .8 .9 1

WUI EPU

AUS

AUT

BEL

BRA

CAN

CHLDNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESPSWE

CHE

TUR

USA

GRB

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FINFRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESP

SWE

CHE

TUR

USA

GRB

0.2

.4.6

.81

.95 .96 .97 .98 .99 1

IV3 IV1

AUS

BRA

CAN

CHL

FRA

DEU

IND

ITA

NDL

SGP

ESP

SWE

CHE

TUR

GRB

0.2

.4.6

.81

.4 .6 .8 1FD

Notes: Cumulative distributions of AR(1) coefficients (ρ) from ∆UNCt = ρUNCt−1 + εt. Resultsare robust to the inclusion of the constant term. Top left: realized volatility (RV). Top right: worlduncertainty index (WUI) and economic policy uncertainty (EPU) index. Bottom left: implied volatilityat 3 and 1 month maturities (IV3 and IV1). Bottom right: forecast dispersion (FD). See Section 2 inthe main paper for detailed description of uncertainty measures.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 25

Figure S18: Half-Life Persistence of Uncertainty

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESP

SWE

CHE

TUR

USA

GRB

0.2

.4.6

.81

.5 1 1.5 2RV

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NORPRT

SGP

ESP

SWE

CHE

TUR

USA

GRB

AUSBRA

CAN

CHL

FRA

DEU

IND

IRL

ITAJPN

NDL

SGP

ESP

SWE

USA

GRB

0.2

.4.6

.81

.5 1 1.5 2 2.5 3

WUI EPU

AUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRA

DEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESP

SWE

CHETUR

USA

GRBAUS

AUT

BEL

BRA

CAN

CHL

DNK

FIN

FRADEU

IND

IRL

ITA

JPN

NDL

NOR

PRT

SGP

ESP

SWE

CHE

TUR

USA

GRB

0.2

.4.6

.81

0 1 2 3

IV3 IV1

AUS

BRA

CAN

CHL

FRA

DEU

IND

ITA

NDL

SGP

ESP

SWE

CHE

TUR

GRB

0.2

.4.6

.81

0 .5 1 1.5FD

Notes: cumulative distributions of half-life coefficients (h) from ∆UNCt = ρUNCt−1 + εt as computed

by h =ln(0.5)ln(γ) , where γ = 1 + ρ > 0 is a complete scalar measure of persistence. Under mean reversion

a proportion γn of any shock will remain after n periods. Results are robust to the inclusion of theconstant term. Top left: realized volatility (RV). Top right: world uncertainty index (WUI) andeconomic policy uncertainty (EPU) index. Bottom left: implied volatility at three- and one-monthmaturities (IV3 and IV1). Bottom right: forecast dispersion (FD). See Section 2 in the main paperfor detailed description of uncertainty measures.

26 BENETRIX AND CURRAN

S4 Lagged Uncertainty Variables

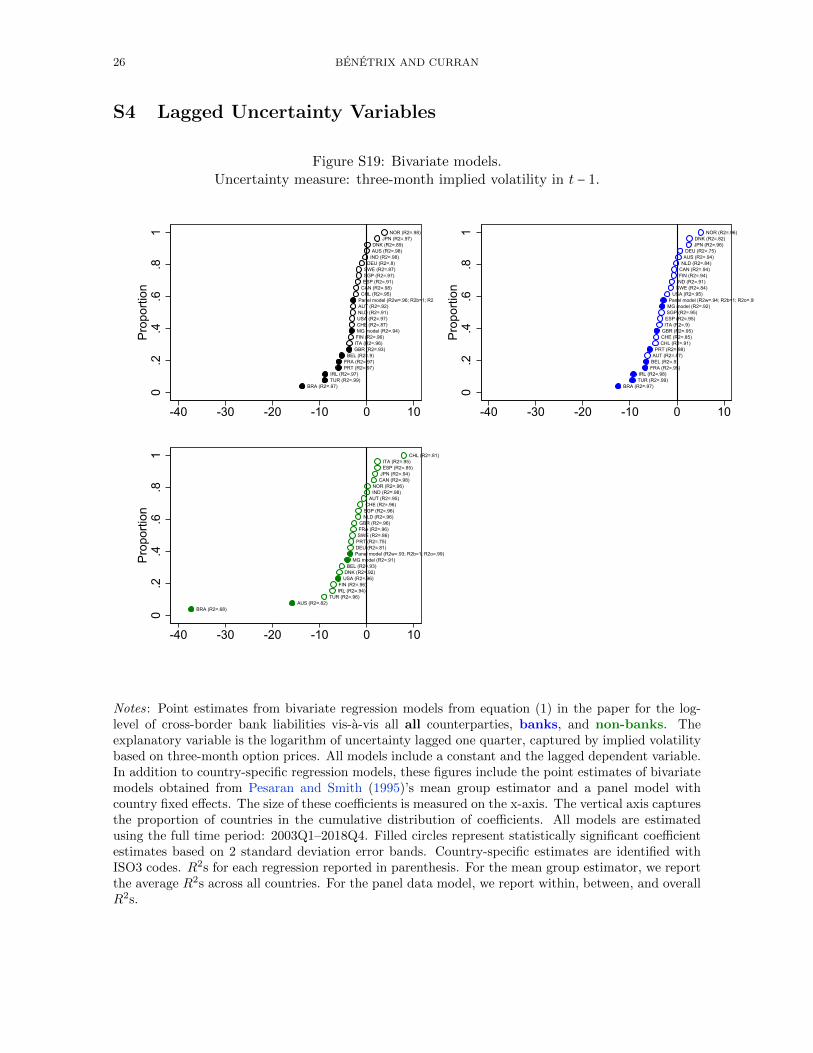

Figure S19: Bivariate models.Uncertainty measure: three-month implied volatility in t − 1.

BRA (R2=.97)TUR (R2=.99)IRL (R2=.97)

PRT (R2=.97)FRA (R2=.97)

BEL (R2=.9)GBR (R2=.93)

MG model (R2=.94)

Panel model (R2w=.96; R2b=1; R2o=1)

ITA (R2=.96)FIN (R2=.96)

CHE (R2=.87)USA (R2=.97)NLD (R2=.91)AUT (R2=.92)

CHL (R2=.95)CAN (R2=.98)ESP (R2=.91)SGP (R2=.97)SWE (R2=.87)

DEU (R2=.8)IND (R2=.98)AUS (R2=.98)DNK (R2=.89)

JPN (R2=.97)NOR (R2=.98)

0.2

.4.6

.81

Prop

ortio

n

-40 -30 -20 -10 0 10

BRA (R2=.97)TUR (R2=.99)IRL (R2=.98)

FRA (R2=.95)BEL (R2=.9)

PRT (R2=.98)

GBR (R2=.95)

MG model (R2=.92)Panel model (R2w=.94; R2b=1; R2o=.99)

AUT (R2=.87)

CHL (R2=.91)CHE (R2=.85)

ITA (R2=.9)ESP (R2=.95)SGP (R2=.95)

USA (R2=.95)SWE (R2=.84)IND (R2=.91)FIN (R2=.94)CAN (R2=.94)NLD (R2=.84)AUS (R2=.94)DEU (R2=.75)

JPN (R2=.96)DNK (R2=.82)

NOR (R2=.96)

0.2

.4.6

.81

Prop

ortio

n

-40 -30 -20 -10 0 10

BRA (R2=.68)AUS (R2=.82)

USA (R2=.96)

MG model (R2=.91)Panel model (R2w=.93; R2b=1; R2o=.99)

TUR (R2=.96)IRL (R2=.94)FIN (R2=.96)

DNK (R2=.92)BEL (R2=.93)

DEU (R2=.81)PRT (R2=.75)SWE (R2=.86)FRA (R2=.96)GBR (R2=.96)

NLD (R2=.96)SGP (R2=.96)CHE (R2=.96)

AUT (R2=.95)IND (R2=.98)NOR (R2=.96)

CAN (R2=.98)JPN (R2=.94)ESP (R2=.85)ITA (R2=.95)

CHL (R2=.81)

0.2

.4.6

.81

Prop

ortio

n

-40 -30 -20 -10 0 10

Notes: Point estimates from bivariate regression models from equation (1) in the paper for the log-level of cross-border bank liabilities vis-a-vis all all counterparties, banks, and non-banks. Theexplanatory variable is the logarithm of uncertainty lagged one quarter, captured by implied volatilitybased on three-month option prices. All models include a constant and the lagged dependent variable.In addition to country-specific regression models, these figures include the point estimates of bivariatemodels obtained from Pesaran and Smith (1995)’s mean group estimator and a panel model withcountry fixed effects. The size of these coefficients is measured on the x-axis. The vertical axis capturesthe proportion of countries in the cumulative distribution of coefficients. All models are estimatedusing the full time period: 2003Q1–2018Q4. Filled circles represent statistically significant coefficientestimates based on 2 standard deviation error bands. Country-specific estimates are identified withISO3 codes. R2s for each regression reported in parenthesis. For the mean group estimator, we reportthe average R2s across all countries. For the panel data model, we report within, between, and overallR2s.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 27

Figure S20: Multivariate models.Uncertainty measure: one-month implied volatility in t-1.

BRA (R2=.98)

GBR (R2=.93)

Panel model (R2w=.96; R2b=1; R2o=1)

MG model (R2=.95)

SWE (R2=.88)IRL (R2=.98)NLD (R2=.91)

FRA (R2=.97)PRT (R2=.98)FIN (R2=.97)

TUR (R2=1)DNK (R2=.89)

DEU (R2=.82)

USA (R2=.97)NOR (R2=.98)CAN (R2=.98)SGP (R2=.97)ESP (R2=.92)IND (R2=.98)AUT (R2=.93)CHE (R2=.89)

BEL (R2=.93)JPN (R2=.97)ITA (R2=.97)AUS (R2=.98)

CHL (R2=.96)

0.2

.4.6

.81

Prop

ortio

n

-30 -20 -10 0 10

BRA (R2=.98)

Panel model (R2w=.94; R2b=1; R2o=.99)

AUS (R2=.94)

SWE (R2=.85)IRL (R2=.98)USA (R2=.96)PRT (R2=.99)

TUR (R2=.99)SGP (R2=.95)FRA (R2=.96)GBR (R2=.96)

CHE (R2=.87)DNK (R2=.83)IND (R2=.85)FIN (R2=.95)MG model (R2=.92)NOR (R2=.97)DEU (R2=.79)BEL (R2=.92)ITA (R2=.92)ESP (R2=.96)

CAN (R2=.95)JPN (R2=.96)

NLD (R2=.86)CHL (R2=.92)

AUT (R2=.88)

0.2

.4.6

.81

Prop

ortio

n

-30 -20 -10 0 10

AUS (R2=.8)

DEU (R2=.87)

GBR (R2=.96)

SWE (R2=.87)

BRA (R2=.67)DNK (R2=.93)

NLD (R2=.96)IRL (R2=.95)

NOR (R2=.97)FRA (R2=.97)MG model (R2=.92)

CAN (R2=.98)Panel model (R2w=.93; R2b=1; R2o=.99)

CHE (R2=.96)IND (R2=.98)

ITA (R2=.95)SGP (R2=.96)BEL (R2=.94)PRT (R2=.79)USA (R2=.97)ESP (R2=.86)JPN (R2=.95)CHL (R2=.84)AUT (R2=.95)

FIN (R2=.97)TUR (R2=.97)

0.2

.4.6

.81

Prop

ortio

n

-30 -20 -10 0 10

Notes: Point estimates from bivariate regression models from equation (1) in the paper for the log-levelof cross-border bank liabilities vis-a-vis all counterparties, banks, and non-banks. The explanatoryvariable is the logarithm of uncertainty lagged one quarter, captured by the EPU index. All modelsinclude a constant and the lagged dependent variable. In addition to country-specific regression models,these figures include the point estimates of bivariate models obtained from Pesaran and Smith (1995)’smean group estimator and a panel model with country fixed effects. The size of these coefficients ismeasured on the x-axis. The vertical axis captures the proportion of countries in the cumulativedistribution of coefficients. All models are estimated using the full time period: 2003Q1–2018Q4.Filled circles represent statistically significant coefficient estimates based on 2 standard deviation errorbands. Country-specific estimates are identified with ISO3 codes. R2s for each regression reported inparenthesis. For the mean group estimator, we report the average R2s across all countries. For thepanel data model, we report within, between, and overall R2s.

28 BENETRIX AND CURRAN

Figure S21: Bivariate models.Uncertainty measure: Economic Policy Uncertainty in t-1.

IRL (R2=.97)

NLD (R2=.92)

ITA (R2=.96)

MG model (R2=.94)

BRA (R2=.97)

Panel model (R2w=.96; R2b=1; R2o=1)

SWE (R2=.87)

CHL (R2=.95)

USA (R2=.97)

SGP (R2=.97)

DEU (R2=.81)

FRA (R2=.97)

ESP (R2=.91)

GBR (R2=.93)

AUS (R2=.98)

CAN (R2=.98)

IND (R2=.98)

JPN (R2=.97)

0.2

.4.6

.81

Prop

ortio

n

-.1 -.05 0 .05

NLD (R2=.85)

IRL (R2=.98)

ITA (R2=.91)

MG model (R2=.92)

FRA (R2=.95)

Panel model (R2w=.94; R2b=1; R2o=1)

GBR (R2=.95)

SWE (R2=.84)

BRA (R2=.97)

DEU (R2=.76)

ESP (R2=.95)

USA (R2=.95)

SGP (R2=.95)

CAN (R2=.94)

AUS (R2=.94)

CHL (R2=.91)

IND (R2=.91)

JPN (R2=.96)

0.2

.4.6

.81

Prop

ortio

n

-.1 -.05 0 .05

IRL (R2=.95)

AUS (R2=.81)

CHL (R2=.82)

USA (R2=.96)

DEU (R2=.82)

NLD (R2=.96)

MG model (R2=.9)

SGP (R2=.96)

ITA (R2=.95)

SWE (R2=.85)

Panel model (R2w=.89; R2b=1; R2o=.99)

ESP (R2=.85)

GBR (R2=.96)

IND (R2=.98)

BRA (R2=.65)

FRA (R2=.96)

CAN (R2=.98)

JPN (R2=.94)

0.2

.4.6

.81

Prop

ortio

n

-.1 -.05 0 .05

Notes: Point estimates from bivariate regression models from equation (1) in the paper for the log-levelof cross-border bank liabilities vis-a-vis all counterparties, banks, and non-banks. The explanatoryvariable is the logarithm of uncertainty lagged one quarter, captured by realized volatility. All modelsinclude a constant and the lagged dependent variable. In addition to country-specific regression models,these figures include the point estimates of bivariate models obtained from Pesaran and Smith (1995)’smean group estimator and a panel model with country fixed effects. The size of these coefficients ismeasured on the x-axis. The vertical axis captures the proportion of countries in the cumulativedistribution of coefficients. All models are estimated using the full time period: 2003Q1–2018Q4.Filled circles represent statistically significant coefficient estimates based on 2 standard deviation errorbands. Country-specific estimates are identified with ISO3 codes. R2s for each regression reported inparenthesis. For the mean group estimator, we report the average R2s across all countries. For thepanel data model, we report within, between, and overall R2s.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 29

Figure S22: Multivariate models.Uncertainty measure: World Uncertainty Index in t-1.

ESP (R2=.93)

FIN (R2=.97)NOR (R2=.98)

TUR (R2=1)SWE (R2=.88)

CAN (R2=.98)ITA (R2=.97)

BRA (R2=.97)JPN (R2=.97)

CHL (R2=.96)AUS (R2=.98)Panel model (R2w=.96; R2b=1; R2o=1)MG model (R2=.95)IRL (R2=.98)PRT (R2=.98)

DNK (R2=.89)NLD (R2=.9)CHE (R2=.89)

DEU (R2=.82)AUT (R2=.93)BEL (R2=.93)USA (R2=.97)

FRA (R2=.97)

GBR (R2=.93)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

NOR (R2=.97)SWE (R2=.85)

FIN (R2=.95)TUR (R2=.99)

CHL (R2=.92)CAN (R2=.95)

JPN (R2=.96)IRL (R2=.98)

BRA (R2=.98)MG model (R2=.92)

DEU (R2=.79)AUT (R2=.88)Panel model (R2w=.94; R2b=1; R2o=.99)

DNK (R2=.83)ITA (R2=.92)PRT (R2=.99)

BEL (R2=.92)CHE (R2=.87)

AUS (R2=.93)NLD (R2=.86)

ESP (R2=.96)GBR (R2=.96)USA (R2=.96)

FRA (R2=.96)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

FIN (R2=.97)PRT (R2=.8)

NOR (R2=.97)SWE (R2=.86)

IRL (R2=.95)BRA (R2=.67)

TUR (R2=.97)AUT (R2=.95)

Panel model (R2w=.93; R2b=1; R2o=.99)JPN (R2=.95)CHE (R2=.96)CAN (R2=.98)USA (R2=.97)DNK (R2=.93)MG model (R2=.92)

NLD (R2=.96)DEU (R2=.85)

BEL (R2=.94)ITA (R2=.95)

AUS (R2=.77)GBR (R2=.96)FRA (R2=.97)

ESP (R2=.87)CHL (R2=.84)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

Notes: Point estimates from bivariate regression models from equation (1) in the paper for the log-levelof cross-border bank liabilities vis-a-vis all counterparties, banks, and non-banks. The explanatoryvariable is the logarithm of uncertainty lagged one quarter, captured by the World Uncertainty Index(WUI). All models include a constant and the lagged dependent variable. In addition to country-specificregression models, these figures include the point estimates of bivariate models obtained from Pesaranand Smith (1995)’s mean group estimator and a panel model with country fixed effects. The size ofthese coefficients is measured on the x-axis. The vertical axis captures the proportion of countriesin the cumulative distribution of coefficients. All models are estimated using the full time period:2003Q1–2018Q4. Filled circles represent statistically significant coefficient estimates based on 2 stan-dard deviation error bands. Country-specific estimates are identified with ISO3 codes. R2s for eachregression reported in parenthesis. For the mean group estimator, we report the average R2s acrossall countries. For the panel data model, we report within, between, and overall R2s.

30 BENETRIX AND CURRAN

Figure S23: Multivariate models.Uncertainty measure: Forecast Dispersion in t-1.

ESP (R2=.93)

FIN (R2=.97)NOR (R2=.98)

TUR (R2=1)SWE (R2=.88)

CAN (R2=.98)ITA (R2=.97)

BRA (R2=.97)JPN (R2=.97)

CHL (R2=.96)AUS (R2=.98)Panel model (R2w=.96; R2b=1; R2o=1)MG model (R2=.95)IRL (R2=.98)PRT (R2=.98)

DNK (R2=.89)NLD (R2=.9)CHE (R2=.89)

DEU (R2=.82)AUT (R2=.93)BEL (R2=.93)USA (R2=.97)

FRA (R2=.97)

GBR (R2=.93)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

NOR (R2=.97)SWE (R2=.85)

FIN (R2=.95)TUR (R2=.99)

CHL (R2=.92)CAN (R2=.95)

JPN (R2=.96)IRL (R2=.98)

BRA (R2=.98)MG model (R2=.92)

DEU (R2=.79)AUT (R2=.88)Panel model (R2w=.94; R2b=1; R2o=.99)

DNK (R2=.83)ITA (R2=.92)PRT (R2=.99)

BEL (R2=.92)CHE (R2=.87)

AUS (R2=.93)NLD (R2=.86)

ESP (R2=.96)GBR (R2=.96)USA (R2=.96)

FRA (R2=.96)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

FIN (R2=.97)PRT (R2=.8)

NOR (R2=.97)SWE (R2=.86)

IRL (R2=.95)BRA (R2=.67)

TUR (R2=.97)AUT (R2=.95)

Panel model (R2w=.93; R2b=1; R2o=.99)JPN (R2=.95)CHE (R2=.96)CAN (R2=.98)USA (R2=.97)DNK (R2=.93)MG model (R2=.92)

NLD (R2=.96)DEU (R2=.85)

BEL (R2=.94)ITA (R2=.95)

AUS (R2=.77)GBR (R2=.96)FRA (R2=.97)

ESP (R2=.87)CHL (R2=.84)

0.2

.4.6

.81

Prop

ortio

n

-4 -2 0 2 4

Notes: Point estimates from bivariate regression models from equation (1) in the paper for the log-levelof cross-border bank liabilities vis-a-vis all counterparties, banks, and non-banks. The explanatoryvariable is the logarithm of uncertainty lagged one quarter, captured by the professional forecastsurvey dispersion (FD). All models include a constant and the lagged dependent variable. In additionto country-specific regression models, these figures include the point estimates of bivariate modelsobtained from Pesaran and Smith (1995)’s mean group estimator and a panel model with countryfixed effects. The size of these coefficients is measured on the x-axis. The vertical axis capturesthe proportion of countries in the cumulative distribution of coefficients. All models are estimatedusing the full time period: 2003Q1–2018Q4. Filled circles represent statistically significant coefficientestimates based on 2 standard deviation error bands. Country-specific estimates are identified withISO3 codes. R2s for each regression reported in parenthesis. For the mean group estimator, we reportthe average R2s across all countries. For the panel data model, we report within, between, and overallR2s.

UNCERTAINTY SHOCKS AND THE CROSS-BORDER FUNDING OF BANKS 31

References

Pesaran, M. H. and Smith, R. (1995). Estimating Long-Run Relationships from DynamicHeterogeneous Panels. Journal of Econometrics, 68 (1), 79–113.

Top Related