Languages

Pages

Legal

Trade patterns in the coal market

Ajay Baral, globalCOAL

Copyright © by globalCOAL 2001 - 2015

For today’s discussion…

• Changes in trade flows

• Price trends in the thermal coal market

• The derivatives market

• SCoTA Overview

• The NEWC index – Asia’s price benchmark

• Conclusions

Copyright © by globalCOAL 2001 - 2015

globalCOAL ownership

Global HubCo BV

Individual Shareholders

Copyright © by globalCOAL 2001 - 2015

Coal brokerage

Screen Trading (Standard contracts)

Voice brokering (Any coal,

any location)

SCoTA

Contract updates and revisions

Development of new hubs

Indices and market data

Index calculation

Coal Market Report

Historical Index data

Delayed Price Feed

What does globalCOAL do?

Changes in Trade Flows: The Exporters

Copyright © by globalCOAL 2001 - 2015

The Seaborne Coal Market

6

0

200

400

600

800

1000

1200

1400

Mill

ion

tonn

es

Thermal Coal Coking Coal

Seaborne Coal Volumes 1990-2013 (Mt)

Source: IEA Coal Information (2014)

Copyright © by globalCOAL 2001 - 2015

Major Exporters

7

Australia New destinations

Indonesia From zero to hero

South Africa Looking East

USA Looking to the

Far East

Colombia Europe’s supplier

Copyright © by globalCOAL 2001 - 2015

South Africa turns to the East

Sources: globalCOAL, IHS McCloskey

Forecasted RBCT Thermal Coal Exports by Destination, 2005-2040

0

10

20

30

40

50

60

70

80

90

100

2005 2010 2015 2020 2030 2040

Mill

ion

tonn

es

Atlantic Pacific

Copyright © by globalCOAL 2001 - 2015

South Africa turns to the East

Sources: globalCOAL, IHS McCloskey

RBCT Thermal Coal Exports to Key Asian Destinations, 2006-2014

0

5

10

15

20

25

30

35

40

45

2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mill

ion

tonn

es

Taiwan China India

*2014 annualised from Aug’14

Copyright © by globalCOAL 2001 - 2015

Australia Diversifies

10

Australian Thermal Coal Exports by Major Asian Destination, 2000-2014

0

20

40

60

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mill

ion

tonn

es

China Taiwan South Korea Japan

Sources: globalCOAL, IHS McCloskey

*2014 annualised from Aug’14

Copyright © by globalCOAL 2001 - 2015

Where to for Indonesia?

Sources: globalCOAL, IHS McCloskey

Forecasted Growth of Total Indonesian Coal Exports, 2000-2040

0

100

200

300

400

500

600

700

2000 2005 2010 2015 2020 2025 2030 2035 2040

Mill

ion

tonn

es

Copyright © by globalCOAL 2001 - 2015

Where to for Indonesia?

12 Sources: globalCOAL, IHS McCloskey

Indonesian Coal Exports by Product, 2000-2014

*2014 annualised from Jun’14

0

50

100

150

200

250

300

350

400

450

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

Mill

ion

tonn

es

Sub-bituminous, Lignite & Other

Bituminous

Copyright © by globalCOAL 2001 - 2015

Where to for Indonesia?

Sources: globalCOAL, IHS McCloskey

Indonesian Coal Exports by destination, 2000-2014

*2014 annualised from Jun’14

Sub-bituminous, Lignite & Other

Bituminous

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014*

?

South Korea

Taiwan

Japan India & Pakistan

China

Other

Changes in Trade Flows: The Importers

Copyright © by globalCOAL 2001 - 2015

Major Importers

15

Europe Stalling?

China The big unknown

India Critical…

Japan Levelling off

Copyright © by globalCOAL 2001 - 2015

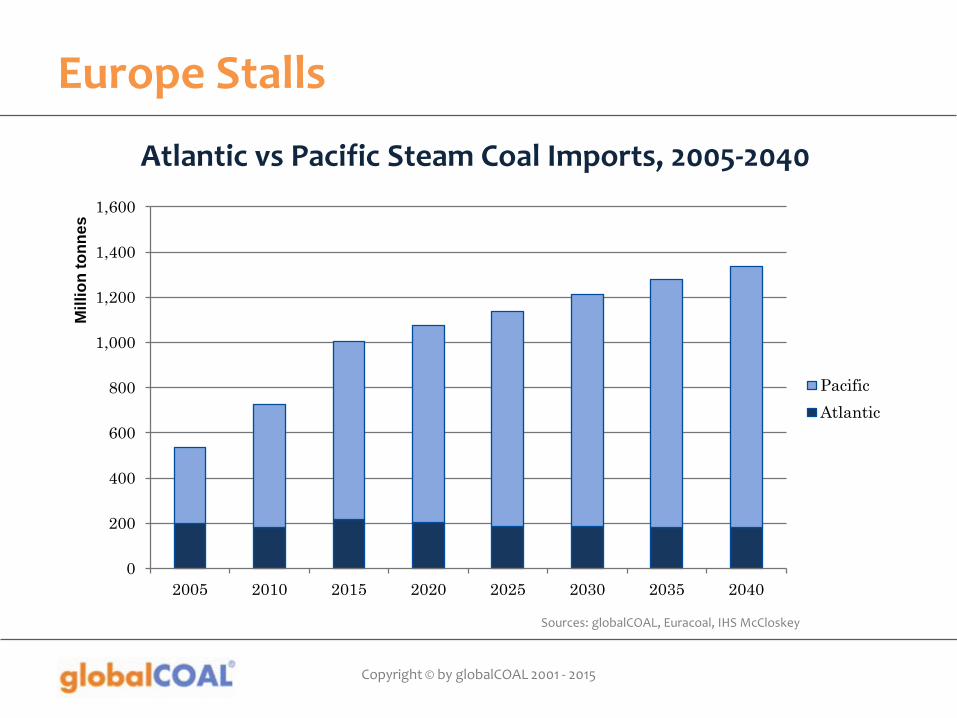

Europe Stalls

16

0

200

400

600

800

1,000

1,200

1,400

1,600

2005 2010 2015 2020 2025 2030 2035 2040

Mill

ion

tonn

es

Pacific Atlantic

Sources: globalCOAL, Euracoal, IHS McCloskey

Atlantic vs Pacific Steam Coal Imports, 2005-2040

Copyright © by globalCOAL 2001 - 2015

China

• The largest producer of coal

• The largest consumer of coal

• Imports are marginal compared to consumption (7.6% in 2013) but have huge impact on international market

• Unlike India, China doesn’t have a coal deficit

• Imports to arbitrage prices between domestic and international coal

17

Copyright © by globalCOAL 2001 - 2015

China’s Coal Imports

18

0

50

100

150

200

250

300

350

Mill

ion

tonn

es

Source: IEA Coal Information (2014)

All Coals, 1990-2013 (Mt)

Copyright © by globalCOAL 2001 - 2015

The Future for Chinese Coal Imports

• Ever changing landscape

• Uncertainty over new regulations affecting imported coal

• Likely that China will impose strict limits on trace elements in imported coal

• Major exemptions (eg. Indonesia)

• Uncertain impact

19

http

s://w

ww

.wis

dom

prod

ucts

.com

/imag

es/p

rodu

cts/

lega

cy/la

rge/

7027

0.jp

g

Copyright © by globalCOAL 2001 - 2015

India

• Large resources, large production but limited growth in extractive capacity

• Indigenous resource also tends to be far from demand centres

• Coal imports are critical to make up shortfall

• Assuming GDP growth rate of 8%, imports will top 350Mt/annum within 20 years

20

Copyright © by globalCOAL 2001 - 2015

India

21 Source: IEA Coal Information (2014)

All Coal Imports, 1990-2013 (Mt)

0

20

40

60

80

100

120

140

160

180

200

Mill

ion

tonn

es

Copyright © by globalCOAL 2001 - 2015

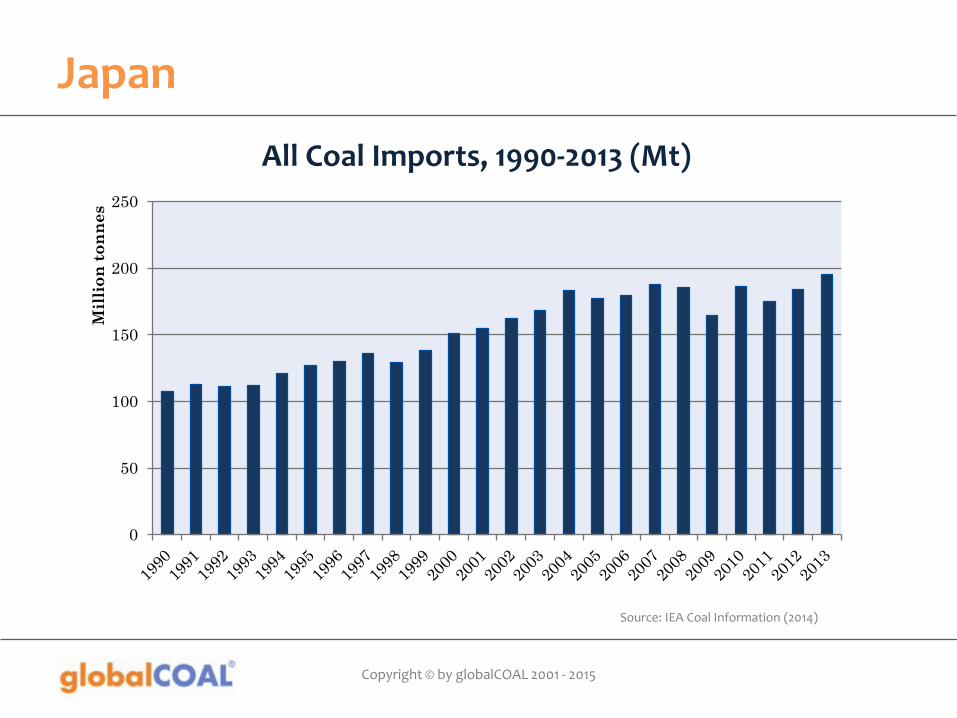

Japan’s Coal Imports

• Historically the largest thermal coal importer

• Surpassed by China in 2010

• Moving away from nuclear power after Fukushima disaster of 2011

• Coal demand expected to level out

22

Copyright © by globalCOAL 2001 - 2015

Japan

23

0

50

100

150

200

250

Mill

ion

tonn

es

Source: IEA Coal Information (2014)

All Coal Imports, 1990-2013 (Mt)

Price Trends in Seaborne Markets

Copyright © by globalCOAL 2001 - 2015

Price Trend – Last Decade

25

0

50

100

150

200

250

01/2

004

06/2

004

11/2

004

04/2

005

09/2

005

02/2

006

07/2

006

12/2

006

05/2

007

10/2

007

03/2

008

08/2

008

01/2

009

06/2

009

11/2

009

04/2

010

09/2

010

02/2

011

07/2

011

12/2

011

05/2

012

10/2

012

03/2

013

08/2

013

01/2

014

06/2

014

11/2

014

USD

/mt

RB DES ARA NEWC

globalCOAL Indices, 2004-2014 (USD/mt)

Source: globalCOAL

Copyright © by globalCOAL 2001 - 2015

Price Trend – Last 3 years

globalCOAL Indices, 2011-2014 (USD/mt)

Source: globalCOAL

0

20

40

60

80

100

120

140

01/2

011

03/2

011

05/2

011

07/2

011

09/2

011

11/2

011

01/2

012

03/2

012

05/2

012

07/2

012

09/2

012

11/2

012

01/2

013

03/2

013

05/2

013

07/2

013

09/2

013

11/2

013

01/2

014

03/2

014

05/2

014

07/2

014

09/2

014

11/2

014

01/2

015

USD

/mt

RB DES ARA NEWC

The Derivatives Market

Copyright © by globalCOAL 2001 - 2015

Building Blocks of a Derivative Market

28

Standard Contract

Screen Trading Market Data

Market Liquidity & Transparency

Copyright © by globalCOAL 2001 - 2015

2014 Derivatives Market Snapshot

API#2 2.5Bt

API#4 500Mt

NEWC 278Mt

API#8 34Mt

S/B Indo 18Mt

Copyright © by globalCOAL 2001 - 2015

Significant growth in recent years

*2014 annualised from Sept’14 Sources: globalCOAL, ICE, CME, SGX, EEX, FSA, LEBA

Growth in Coal Derivatives Volume, 2001-2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Mill

ion

tonn

es

∆+7.8%

Copyright © by globalCOAL 2001 - 2015

Growth in clearing vs OTC

Sources: globalCOAL, ICE, CME, SGX, EEX, FSA, LEBA

Cleared and OTC Derivatives Volumes Growth, 2001-2014

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

500

1000

1500

2000

2500

3000

3500

4000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

% Cl

eare

d

Mill

ion

tonn

es

Cleared OTC % Cleared (right axis)

Copyright © by globalCOAL 2001 - 2015

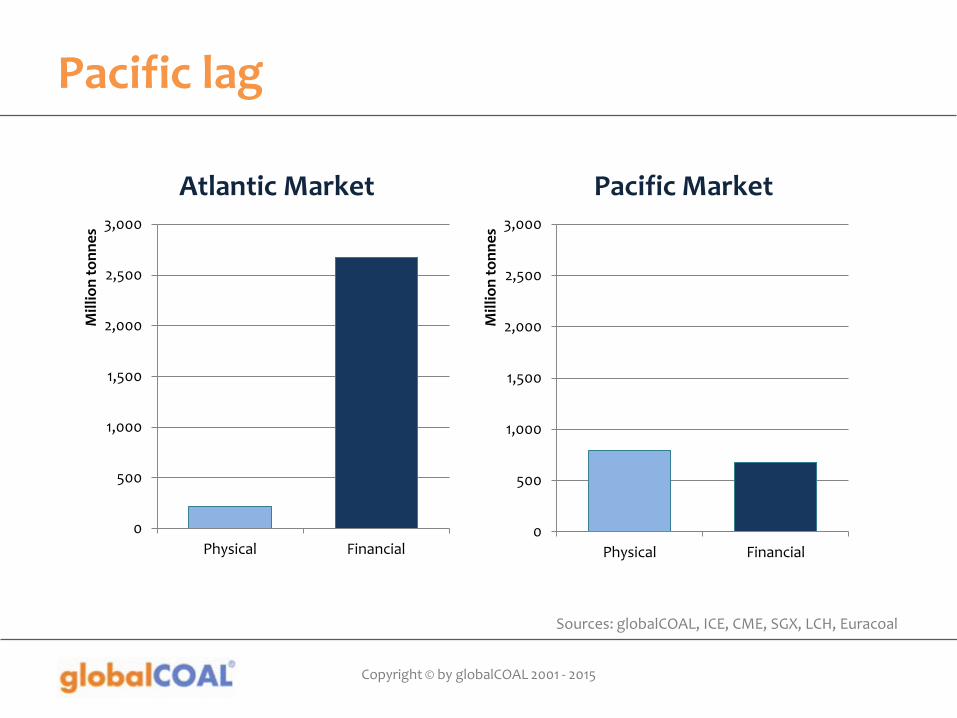

Pacific lag

Sources: globalCOAL, ICE, CME, SGX, LCH, Euracoal

Atlantic Market Pacific Market

0

500

1,000

1,500

2,000

2,500

3,000

Physical Financial

Mill

ion

tonn

es

0

500

1,000

1,500

2,000

2,500

3,000

Physical Financial

Mill

ion

tonn

es

SCoTA Overview

Copyright © by globalCOAL 2001 - 2015

A brief history of SCoTA…

• Following the collapse of ENRON in 2001, the thermal coal market demanded reliable, transparent thermal coal pricing

• globalCOAL was established in 2001 by coal market producers, consumers and traders to establish a standardised coal market:

– Introduced a standardised coal trading agreement: SCoTA

– Online trading platform to facilitate the trade of standardised seaborne thermal coal, with all trades underlied by SCoTA

– Pricing data derived from the platform provided objective, transparent price points to the market for the first time

Copyright © by globalCOAL 2001 - 2015

Benefits of Standardised Screen Trading

Screen Trading

Accessible to all

Quick and easy route to standardised

market Ability to reverse positions quickly

Real-time, transparent & objective spot and forward

prices

Efficiency & speed of execution

(click & trade)

Anonymity until point of execution

Copyright © by globalCOAL 2001 - 2015

What defines a commodity market?

• The product is traded without qualitative differentiation

• Negotiations are focussed on price rather than quality

• The price is international and fluctuates on global supply / demand

• The product is traded in a transparent market

• There is an active spot and risk management market

Copyright © by globalCOAL 2001 - 2015

Is coal a commodity?

• Is it traded without qualitative differentiation?

Yes; SCoTA defines standard quality parameters => pools of liquidity form around most commonly traded hubs

• Are negotiations focussed on price rather than quality?

Yes; Indices for the main hubs NEWC, RB & ARA give clear price markers

• Is the price international and fluctuating on supply/demand?

Yes; market participants trade coal globally

• Is the product traded in a transparent market?

Yes; bids, offers and trades on gC are communicated to the market

• Is there an active spot and risk management market?

Yes; 2.7 Billion tonnes of cleared derivatives traded in 2014 YTD

Copyright © by globalCOAL 2001 - 2015

Who uses SCoTA?

There are 2,300+ companies licensed to use SCoTA worldwide and 161 globalCOAL Market Members

Principals

• Utilities

• Miners

• Physical coal traders

• Financial institutions

OTC Brokers

•globalCOAL •Other brokers: •LCB •GFI •Ginga •ICAP

Copyright © by globalCOAL 2001 - 2015

Geographic spread of SCoTA users

226

273

218

222

186

171

145

108

70

55

26

Top 5 Countries

1. Indonesia 2. Australia 3. USA 4. India 5. UK

Copyright © by globalCOAL 2001 - 2015

Total brokered physical SCoTA volumes

Source: globalCOAL & other brokers

-

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 *

Mill

ion

Tonn

es

* 2014 – estimate

Copyright © by globalCOAL 2001 - 2015

The SCoTA market in perspective

Production Intl Trade Seaborne Trade Thermal Coal Market

Source: VdKI, Euracoal, globalCOAL & other brokers (2010 data)

7.2Bt Domestically produced & consumed

1.1Bt Int’l Trade

971Mt Seaborne

Trade

99Mt Overland

726Mt Thermal Coal

245Mt Coking Coal

155 Mt Brokered

SCoTA

571 Mt Bilatera

l standard and non-standard

coal

Copyright © by globalCOAL 2001 - 2015

SCoTA today… • SCoTA v8

• Master Agreement (v8 MA)

• SCoTA v8 General Terms and Conditions (v8 GTC)

• 15 RSSs on a range of INCO delivery terms

• Build your own RSS

• SCoTA-based transactions underpin 99% of API#2 and 100% of API#4 and gC NEWC Index

• Indonesian and Indian governments use NEWC as a component of their price assessment for coal and power

Copyright © by globalCOAL 2001 - 2015

DES ARA Multi-origin ACPRSU

Richards Bay FOB

3 qualities

Newcastle (NEWC) FOB

COL FOB

4 load ports

INDO A B C FOB or FAS 3 qualities NCIG

FOB

DAP RTM Multi-origin ACPRSU

Lower min CV

Standard hubs covered by SCoTA

CFR China Multi-origin 2 qualities

CFR Krishnapatnam Multi-origin 2 qualities

High Ash Aus FOB

Lower CV

The gC NEWC Index

Copyright © by globalCOAL 2001 - 2015

• The benchmark price for coal in Asia Pacific

• Used by governmental agencies around Asia:

– 25% component of HBA in Indonesia (25% NEX, 25% FOB Kalimantan, 25% ICI)

– 25% component of CERC in India (25% API4, 50% Indonesian Coal)

– Chinese government is considering the use of international indices (including gC NEWC) in its forward planning for pricing electricity

• Coaltrans Bali survey in 2011:

– 64% of respondents stated the NEWC Index is the most trusted Index by Indonesian producers, end users & traders

– 64% stated that the NEWC Index is the most suitable to establish end-user prices for Indonesian coal (versus 18% for the Argus-ICI)

The globalCOAL NEWC index

Copyright © by globalCOAL 2001 - 2015

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

2009 2010 2011 2012 2013 2014

Mill

ion

tonn

es

Spot trades Forward trades % Asia-Pac based trader

More spot trading in NEWC

Source: globalCOAL

Spot vs forward NEWC volume on the globalCOAL screen and % of NEWC tonnage traded from APAC

50%

Some conclusions

& your questions?

CONTACT US

London +44 207 776 5900 Singapore +65 6311 4571

New Delhi +91 1204 26 48 90

Top Related