Languages

Pages

Legal

TOWN OF URANIA, LOUISIANA

Annual Financial Statements

JUNE 30,2006

Under provisions of state law, this report is a publicdocument. A copy of the report has been submitted tothe entity and other appropriate public officials. Thereport is available for public inspection at the BatonRouge office of the Legislative Auditor and, whereappropriate, at the office of the parish cierk of court.

Release Date

TOWN OF URANIA, LOUISIANA

The Town of Urania was incorporated under the Lawrason Act, and operates under the Mayor-Board of Aldermanform of government. The Town provides the following significant services to its residents as provided by its charter:public safety (police and fire), highways and streets, utilities (water and sewer services) and general administrativefunctions, including coordination of related services with parish, state and federal governing bodies.

TOWN OF URANIA, LOUISIANATable of Contents

June 30,2006

Schedule No. Page No.

Management's Discussion and Analysis 1-5

Independent Accountant's Report 6

Independent Accountant's Report on Applying Agreed-Upon Procedures 7-9

Basic Financial Statements

Statement of Net Assets A II

Statement of Activities B 12

Balance Sheet, Governmental Funds C 13

Reconciliation of The Government Funds Balance Sheet to theGovernment-Wide Financial Statement of Net Assets D 14

Statement of Revenues, Expenditures and Changes in Fund Balance -Governmental Funds , E 15

Reconciliation of The Statement of Revenues, Expenditures, and Changesin Fund Balances of Governmental Funds to the Statement of Activities F 16

Statement of Net Assets, Proprietary Funds G 17

Statement of Revenues, Expenses and Changes in Met Assets -Proprietary Funds H 18

Statement of Cash Flows - Proprietary Funds I 19

Statement of Net Assets-Fiduciary Fund J 20

Statement of Changes in Fiduciary Net Assets K 21

Notes to the Basic Financial Statements 22-32

Required Supplemental Information

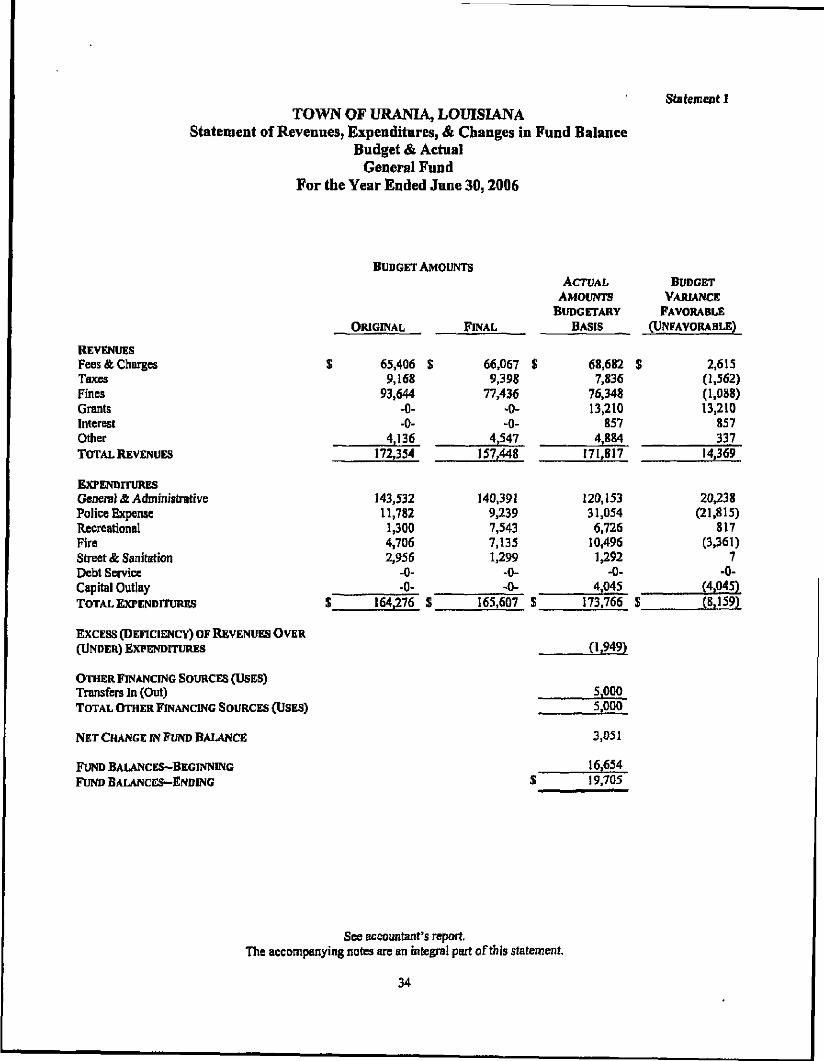

Statement of Revenues, Expenditures, and Changes in Fund Balance -Budget and Actual - General Fund 1 34

Management Letter Comments 35

Management's Summary of Prior Year Findings 36

TOWN OF URANIAPO Box 339

Urania, Louisiana 71480Tel: (318)495-3452Fax:(318)495-3425

MANAGEMENTS DISCUSSION AND ANALYSIS

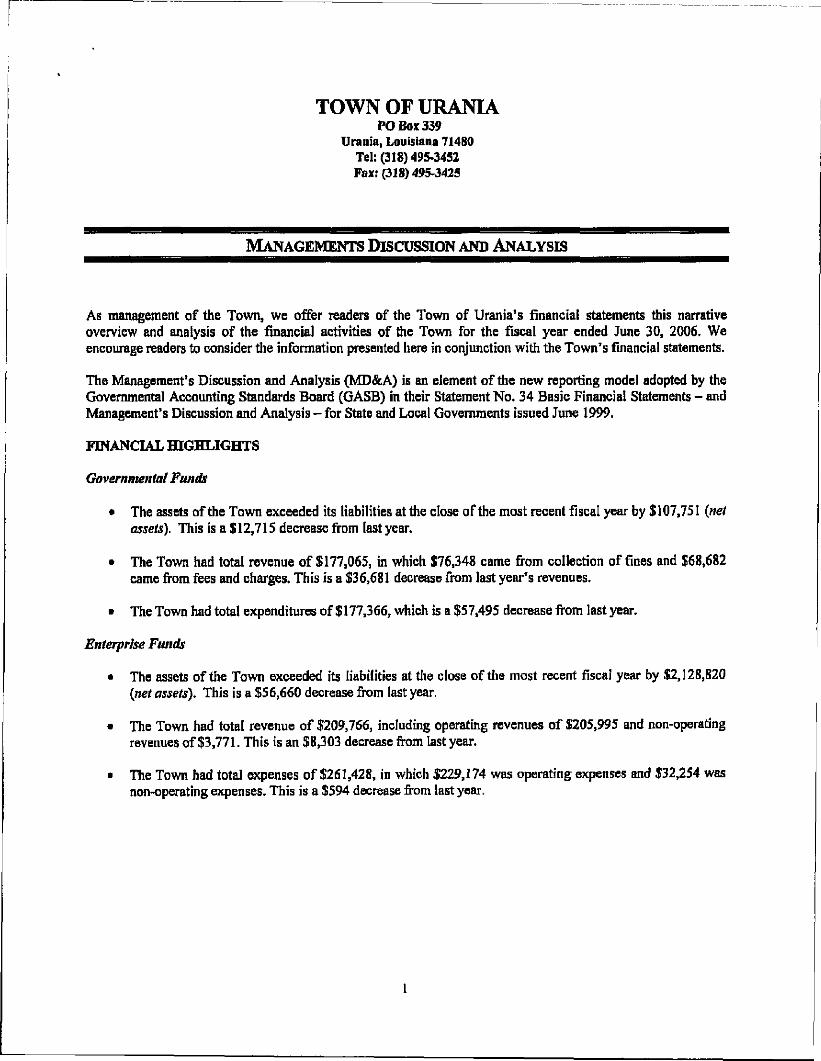

As management of the Town, we offer readers of the Town of Urania's financial statements this narrativeoverview and analysis of the financial activities of the Town for the fiscal year ended June 30, 2006. Weencourage readers to consider the information presented here in conjunction with the Town's financial statements.

The Management's Discussion and Analysis (MD&A) is an element of the new reporting model adopted by theGovernmental Accounting Standards Board (GASB) in their Statement No. 34 Basic Financial Statements - andManagement's Discussion and Analysis - for State and Local Governments issued June 1999.

FINANCIAL HIGHLIGHTS

Governmental Funds

• The assets of the Town exceeded its liabilities at the close of the most recent fiscal year by $107,751 (netassets). This is a $12,715 decrease from last year.

• The Town had total revenue of $177,065, in which $76,348 came from collection of fines and $68,682came from fees and charges. This is a $36,681 decrease from last year's revenues.

• The Town had total expenditures of $177,366, which is a $57,495 decrease from last year.

Enterprise Funds

• The assets of the Town exceeded its liabilities at the close of the most recent fiscal year by $2,128,820(net assets). This is a $56,660 decrease from last year.

• The Town had total revenue of $209,766, including operating revenues of $205,995 and non-operatingrevenues of $3,771. This is an $8,303 decrease from last year.

• The Town had total expenses of $261,428, in which $229,174 was operating expenses and $32,254 wasnon-operating expenses. This is a $594 decrease from last year.

MD&A

OVERVIEW OF THE FINANCIAL STATEMENTS

This discussion and analysis is intended to serve as an introduction to the Town's basic financial statements. TheTown's basic financial statements consist of two components: 1) fund financial statements, and 2) notes to thefinancial statements. This report also contains other supplementary information in addition to the basic financialstatements themselves. The Town is a special-purpose entity engaged only in governmental activities.Accordingly, only fund financial statements are presented as the basic financial statements.

Effective, January 1, 2004, the Town adopted Governmental Accounting Standards (GASB) Statement No. 34,Basic Financial Statements - Management *s Discussion and Analysis -for State and Local Governments.

FUND FINANCIAL STATEMENTS

A. fimd is a grouping of related accounts that is used to maintain control over resources that have been segregatedfor specific activities or objectives. The Town, like other state and local governments, uses fund accounting toensure and demonstrate compliance with finance-related legal requirements.

USING THIS ANNUAL REPORT

The Town's annual report consists of financial statements that show information about the Town's funds,enterprise funds and governmental funds.

Our accountant has provided assurance in his independent accountant's report, located immediately following thisManagement's Discussion and Analysis, that the Basic Financial Statements are fairly stated. Varying degrees ofassurance are being provided by the accountant regarding the other information included in this report. A user ofthis report should read the independent accountant's report carefully to ascertain the level of assurance beingprovided for each of the other parts of this report.

Reporting the Town's Most Significant Funds

The Town's financial statements provide detailed information about the most significant funds. The Town mayestablish other funds to help it control and manage money for particular purposes or to show that it is meetinglegal responsibilities for using grants and other money. The Town's enterprise fund uses the following accountingapproach:

All of the Town's services are reported in an enterprise fund. They are reported using the full accrual method ofaccounting in which all assets and all liabilities associated with the operation of these funds are included on thebalance sheet. The focus of proprietary funds is on income measurement, which, together with the maintenanceof equity, is an important financial indication.

MD&A

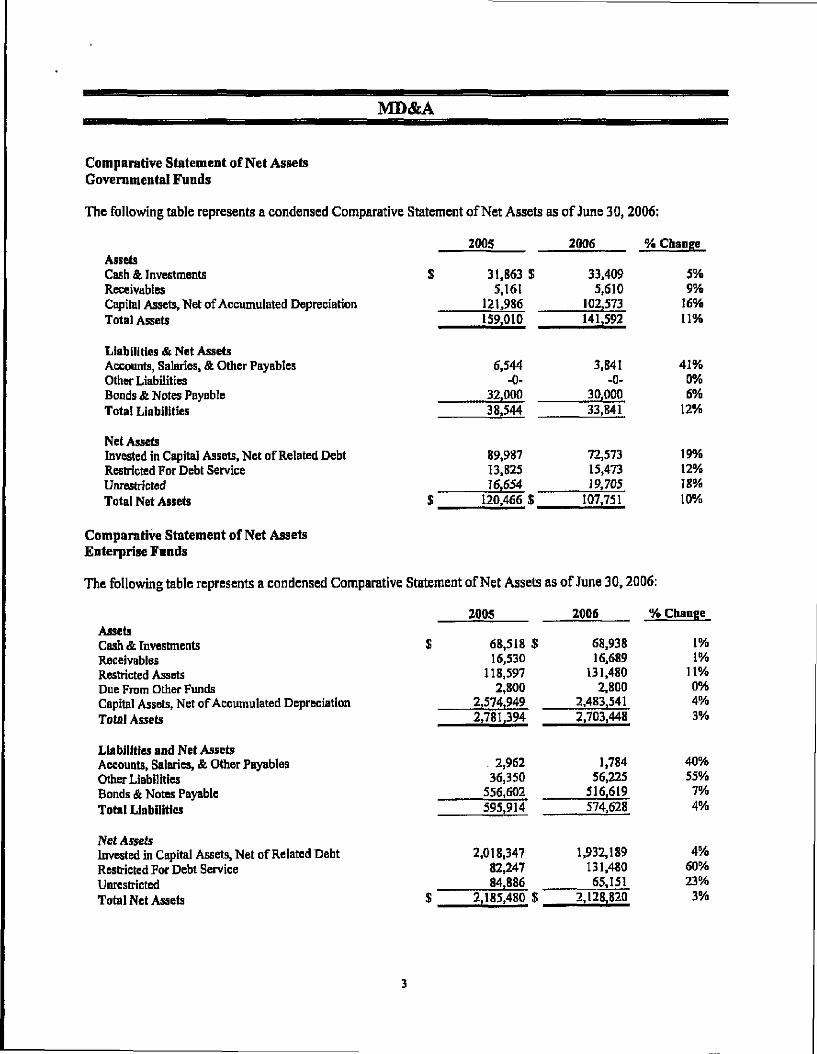

Comparative Statement of Net AssetsGovernmental Funds

The following table represents a condensed Comparative Statement of Net Assets as of June 30,2006:

2005 2006 % ChangeAssetsCash & InvestmentsReceivablesCapital Assets, Net of Accumulated DepreciationTotal Assets

Liabilities & Net AssetsAccounts, Salaries, & Other PayablesOther LiabilitiesBonds & Notes PayableTotal Liabilities

Net AssetsInvested in Capital Assets, Net of Related DebtRestricted For Debt ServiceUnrestrictedTotal Net Assets

Comparative Statement of Net AssetsEnterprise Funds

The following table represents a condensed Comparative

AssetsCash & InvestmentsReceivablesRestricted AssetsDue From Other FundsCapital Assets, Net of Accumulated DepreciationTotal Assets

Liabilities and Net AssetsAccounts, Salaries, & Other PayablesOther LiabilitiesBonds & Notes PayableTotal Liabilities

Net AssetsInvested in Capital Assets, Net of Related DebtRestricted For Debt ServiceUnrestrictedTotal Net Assets

$ 31,863 $5,161

121,986159,010

6,544-0-

32,00038,544

89,98713,82516,654

$ 120,466 $

33,4095,610

102,573141,592

3,841-0-

30,00033,841

72,57315,47319,705

107,751

5%9%

16%11%

41%0%6%

12%

19%12%18%10%

Statement of Net Assets as of June 30, 2006:

2005

$ 68,518 $16,530

118,5972,800

2,574,9492,781,394

2,96236,350

556,602595,914

2,018,34782,24784,886

$ 2,185,480 $

2006 %

68,93816,689

131,4802,800

2,483,5412,703,448

1,78456,225

516,619574,628

1,932,189131,48065,151

2,128,820

Chance

1%1%

11%0%4%3%

40%55%7%4%

4%60%23%

3%

MD&A

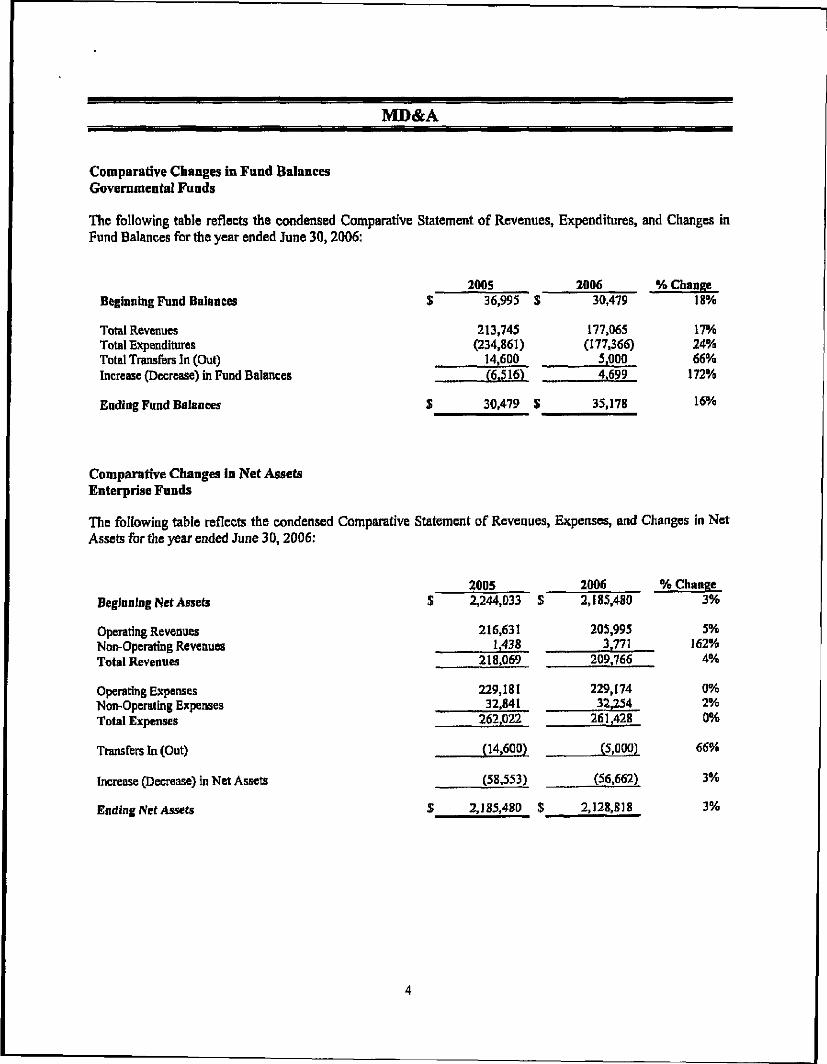

Comparative Changes in Fund BalancesGovernmental Funds

The following table reflects the condensed ComparativeFund Balances for the year ended June 30, 2006;

Beginning Fund Balances

Total RevenuesTotal ExpendituresTotal Transfers In (Out)Increase (Decrease) in Fund Balances

Ending Fund Balances

Comparative Changes in Net AssetsEnterprise Funds

The following table reflects the condensed ComparativeAssets for the year ended June 30, 2006:

Beginning Net Assets

Operating RevenuesNon-Operating RevenuesTotal Revenues

Operating ExpensesNon-Operating ExpensesTotal Expenses

Transfers In (Out)

Increase (Decrease) in Net Assets

Ending Net Assets

Statement of Revenues,

2005$ 36,995 $

213,745(234,861)

14,600(6,516)

$ 30,479 $

Statement of Revenues,

2005$ 2,244,033 $

216,6311,438

218,069

229,18132,841

262,022

(14,600)

(58,553)

$ 2, 185,480 $

Expenditures,

200630,479

177,065(177,366)

5,0004,699

35,178

Expenses, and

20062,185,480

205,9953,771

209,766

229,17432,254

261,428

(5,000)

(56,662)

2,128,818

and Changes in

% Change18%

17%24%66%

172%

16%

Changes in Net

% Change3%

5%162%

4%

0%2%0%

66%

3%

3%

MD&A

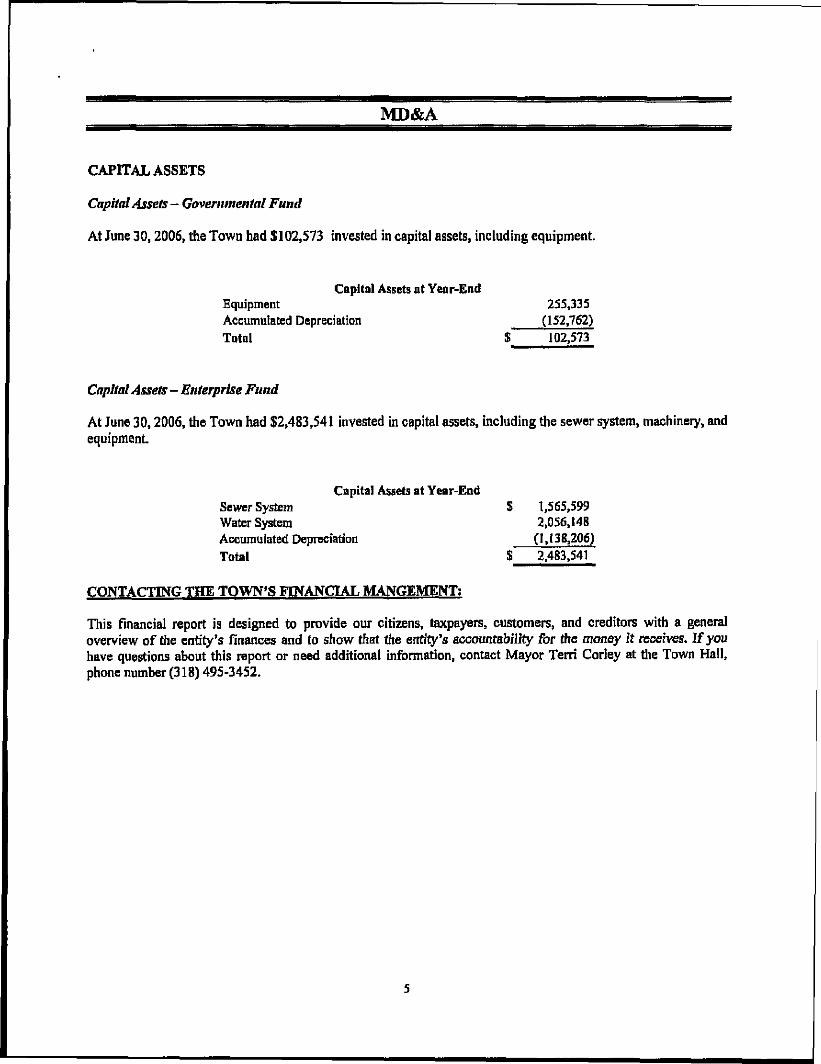

CAPITAL ASSETS

Capital Assets - Governmental Fund

At June 30,2006, the Town had $102,573 invested in capital assets, including equipment.

Capital Assets at Year-EndEquipment 255,335Accumulated Depreciation (152,762)Total $ 102,573

Capital Assets - Enterprise Fund

At June 30,2006, the Town had $2,483,541 invested in capital assets, including the sewer system, machinery, andequipment.

Capital Assets at Year-EndSewer System $ 1,565,599Water System 2,056,148Accumulated Depreciation (1,138,206)Total S 2,483,541

CONTACTING THE TOWN'S FINANCIAL MANGEMENT;

This financial report is designed to provide our citizens, taxpayers, customers, and creditors with a generaloverview of the entity's finances and to show that the entity's accountability for the money it receives. If youhave questions about this report or need additional information, contact Mayor Terri Corley at the Town Hall,phone number (318) 495-3452.

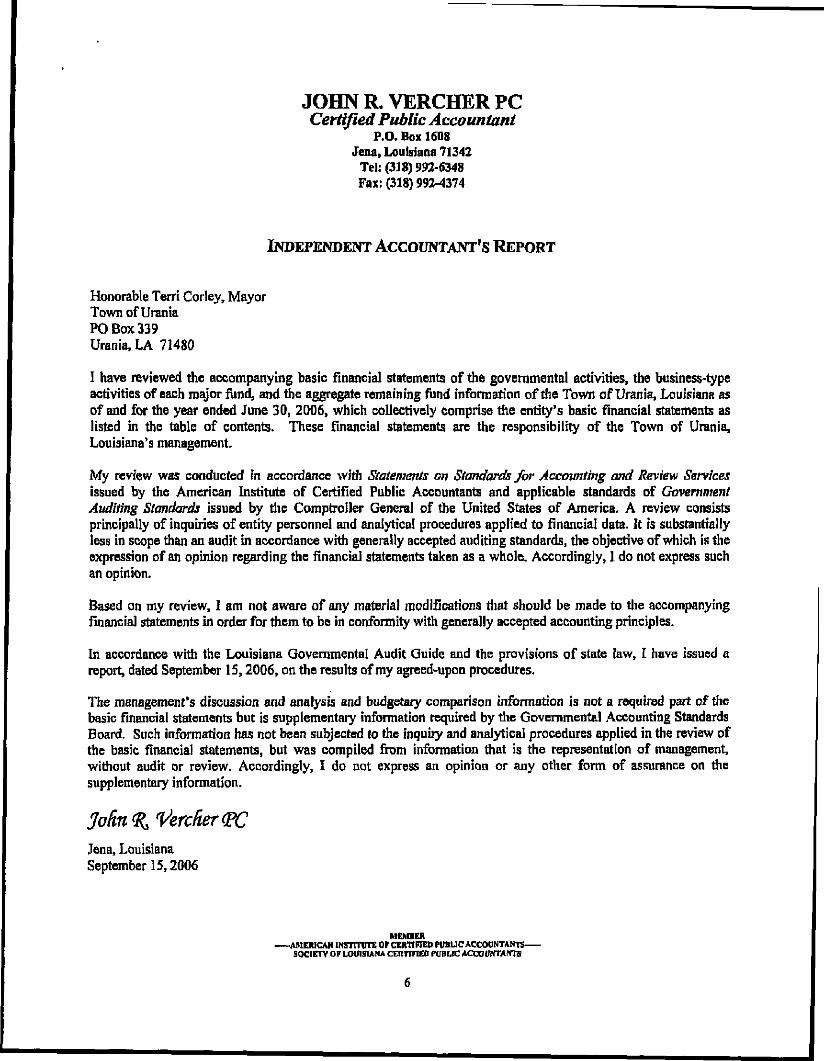

JOHN R, VERCHER PCCertified Public Accountant

P.O. Box 1608Jena, Louisiana 71342

Tel: (318) 992-6348Fax:(318)992-4374

INDEPENDENT ACCOUNTANT'S REPORT

Honorable Terri Corley, MayorTown of UraniaPO Box 339Urania, LA 71480

I have reviewed the accompanying basic Financial statements of the governmental activities, the business-typeactivities of each major fund, and the aggregate remaining fund information of the Town of Urania, Louisiana asof and for the year ended June 30, 2006, which collectively comprise the entity's basic financial statements aslisted in the table of contents. These Financial statements are the responsibility of the Town of Urania,Louisiana's management.

My review was conducted in accordance with Statements on Standards for Accounting and Review Servicesissued by the American Institute of Certified Public Accountants and applicable standards of GovernmentAuditing Standards issued by the Comptroller General of the United States of America. A review consistsprincipally of inquiries of entity personnel and analytical procedures applied to financial data. It is substantiallyless in scope than an audit in accordance with generally accepted auditing standards, the objective of which is theexpression of an opinion regarding the financial statements taken as a whole. Accordingly, 1 do not express suchan opinion.

Based on my review, I am not aware of any material modifications that should be made to the accompanyingfinancial statements in order for them to be in conformity with generally accepted accounting principles.

In accordance with the Louisiana Governmental Audit Guide and the provisions of state law, I have issued areport, dated September 15,2006, on the results of my agreed-upon procedures.

The management's discussion and analysis and budgetary comparison information is not a required part of thebasic Financial statements but is supplementary information required by the Governmental Accounting StandardsBoard. Such information has not been subjected to the inquiry and analytical procedures applied in the review ofthe basic financial statements, but was compiled from information that is the representation of management,without audit or review. Accordingly, I do not express an opinion or any other form of assurance on thesupplementary information.

Jena, LouisianaSeptember 15,2006

MEMBER-AMERICAN INSTITUTE OP CERTIFIED PUBLIC ACCOUNTANTS

SOCIETY OF LOUISIANA CEimFIEO PUBLIC ACCOUNTANTS

JOHN R. VERCHER PCCertified Public Accountant

P.O. Box 1608Jena, Louisiana 71342

Tel: (318) 992-6348Fax: (318) 992-4374

INDEPENDENT ACCOUNTANT'S REPORTON APPLYING AGREED-UPON PROCEDURES

Honorable Terri Corley, MayorTown of UraniaPO Box 339Urania, LA 71480

I have performed the procedures included in the Louisiana Government Audit Guide and enumerated below,which were agreed to by the management of the Town of Urania, Louisiana and the Legislative Auditor, State ofLouisiana, solely to assist the users in evaluating management's assertions about the Town of Urania, Louisiana'scompliance with certain laws and regulations during the year ended June 30,2006 included in the accompanyingLouisiana Attestation Questionnaire. This agreed-upon procedures engagement was performed in accordancewith standards established by the American Institute of Certified Public Accountants. The sufficiency of theseprocedures is solely the responsibility of the specified users of the report. Consequently, I make no representationregarding the sufficiency of the procedures described below either for the purpose for which this report has beenrequested or for any other purpose.

Public Bid Law

1. Select all expenditures made during the year for material and supplies exceeding $20,000, or public worksexceeding $100,000, and determine whether such purchases were made in accordance with LSA-RS 38:2211-2251 (the public bid law).

*During my review of expenditures, I found no such expenditures.

2. Obtain from management a list of the immediate family members of each board member as defined by LSA-RS 42:1101-1124 (the code of ethics), and a list of outside business interests of all board members andemployees, as well as their immediate families.

* Management provided me with the required list including the noted information.

3. Obtain from management a listing of all employees paid during the period under examination.

* Management provided me with the required list.

4. Determine whether any of those employees included in the listing obtained from management in agreed-uponprocedure (3) were also included on the listing obtained from management in agreed-upon procedure (2) asimmediate family members.

* None of the employees included on the list of employees provided by management [agreed-upon procedure (3)]appeared on the list provided by management in agreed-upon procedure (2).

MEMBERAMERICAN INSTITUTE OP CERTIFIED PUBLIC ACCOUNTANTSSOCIETY OP LOUISIANA CERTIFIED fUBLIC ACCOUNTANTS

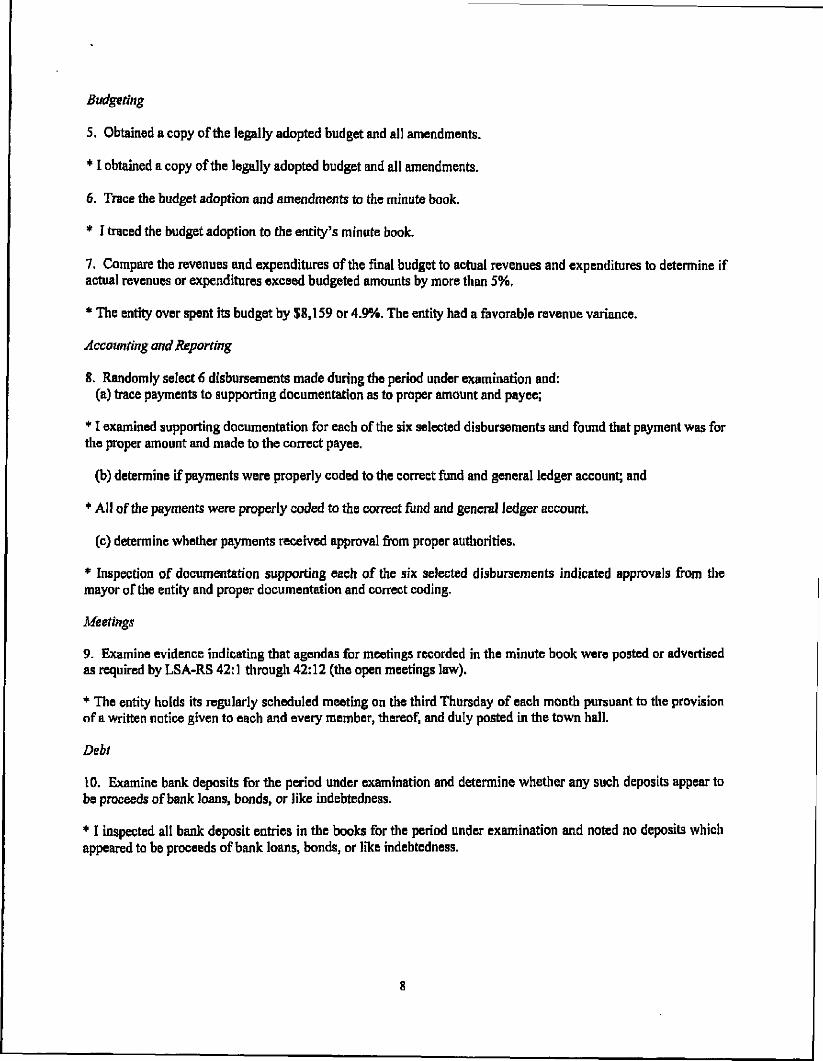

Budgeting

5. Obtained a copy of the legally adopted budget and all amendments.

* I obtained a copy of the legally adopted budget and all amendments.

6. Trace the budget adoption and amendments to the minute book.

* I traced the budget adoption to the entity's minute book.

7. Compare the revenues and expenditures of the final budget to actual revenues and expenditures to determine ifactual revenues or expenditures exceed budgeted amounts by more than 5%,

* The entity over spent its budget by $8,159 or 4.9%. The entity had a favorable revenue variance.

Accounting and Reporting

8. Randomly select 6 disbursements made during the period under examination and:(a) trace payments to supporting documentation as to proper amount and payee;

* I examined supporting documentation for each of the six selected disbursements and found that payment was forthe proper amount and made to the correct payee.

(b) determine if payments were properly coded to the correct fund and general ledger account; and

* All of the payments were properly coded to the correct fund and general ledger account.

(c) determine whether payments received approval from proper authorities.

* Inspection of documentation supporting each of the six selected disbursements indicated approvals from themayor of the entity and proper documentation and correct coding.

Meetings

9. Examine evidence indicating that agendas for meetings recorded in the minute book were posted or advertisedas required by LSA-RS 42:1 through 42:12 (the open meetings law).

* The entity holds its regularly scheduled meeting on the third Thursday of each month pursuant to the provisionof a written notice given to each and every member, thereof, and duly posted in the town hall.

Debt

10. Examine bank deposits for the period under examination and determine whether any such deposits appear tobe proceeds of bank loans, bonds, or like indebtedness.

* I inspected all bank deposit entries in the books for the period under examination and noted no deposits whichappeared to be proceeds of bank loans, bonds, or like indebtedness.

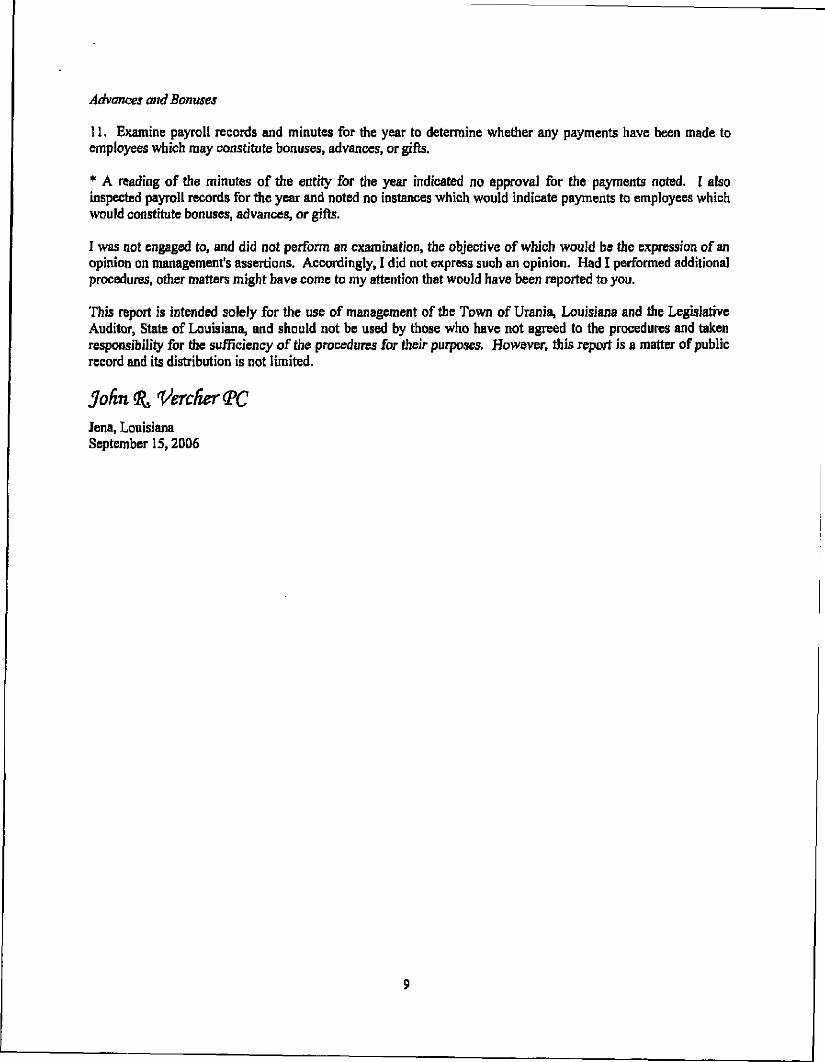

Advances and Bonuses

1 1. Examine payroll records and minutes for the year to determine whether any payments have been made toemployees which may constitute bonuses, advances, or gifts.

* A reading of the minutes of the entity for the year indicated no approval for the payments noted. I alsoinspected payroll records for the year and noted no instances which would indicate payments to employees whichwould constitute bonuses, advances, or gifts.

I was not engaged to, and did not perform an examination, the objective of which would be the expression of anopinion on management's assertions. Accordingly, I did not express such an opinion. Had I performed additionalprocedures, other matters might have come to my attention that would have been reported to you.

This report is intended solely for the use of management of the Town of Urania, Louisiana and the LegislativeAuditor, State of Louisiana, and should not be used by those who have not agreed to the procedures and takenresponsibility for the sufficiency of the procedures for their purposes. However, this report is a matter of publicrecord and its distribution is not limited.

Jena, LouisianaSeptember 15, 2006

B^

BASIC FINANCIAL STATEMENTS

10

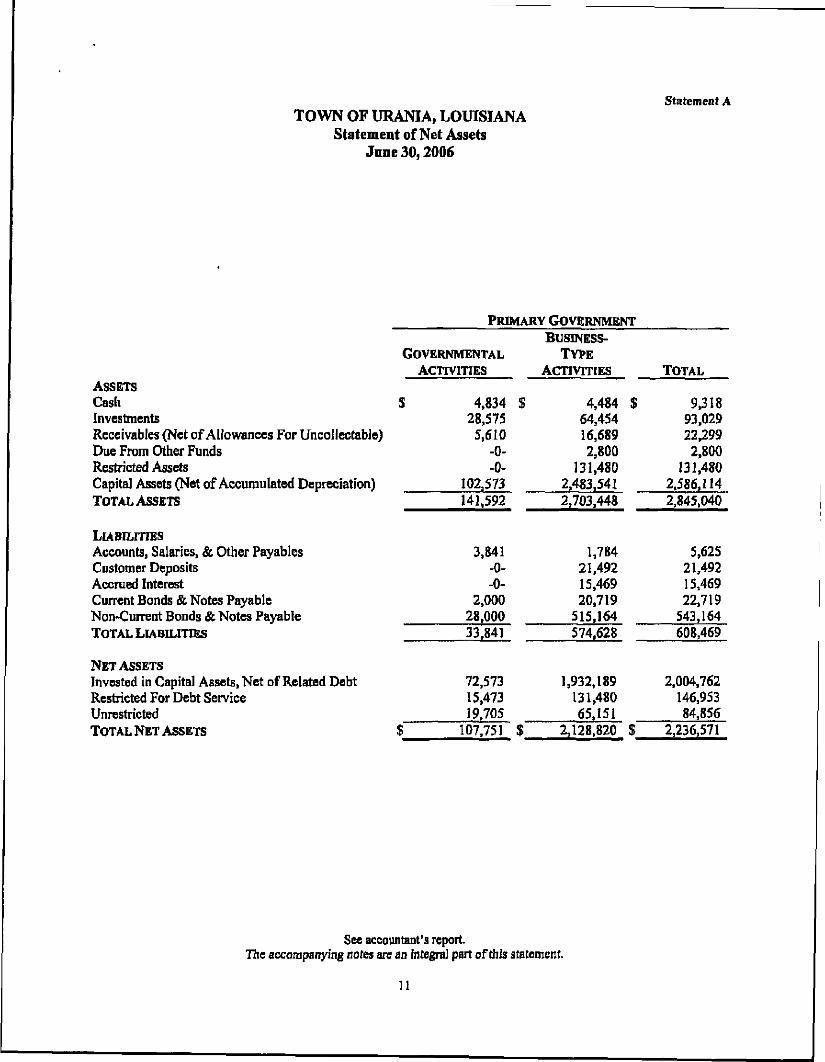

TOWN OF URANIA, LOUISIANAStatement of Net Assets

June 30,2006

Statement A

ASSETSCashInvestmentsReceivables (Net of Allowances For Uncollectable)Due From Other FundsRestricted AssetsCapital Assets (Net of Accumulated Depreciation)TOTAL ASSETS

LIABILITIESAccounts, Salaries, & Other PayablesCustomer DepositsAccrued InterestCurrent Bonds & Notes PayableNon-Current Bonds & Notes PayableTOTAL LIABILITIES

NET ASSETSInvested in Capital Assets, Net of Related DebtRestricted For Debt ServiceUnrestrictedTOTAL NET ASSETS

PRIMARY GOVERNMENT

GOVERNMENTAL

$

$

ACTIVITIES

4,834 S28,575

5,610-0--0-

102,573141,592

3,841-0--0-

2,00028,00033,841

72,57315,47319,705

107,751 $

BUSINESS-TYPE

ACTIVITIES

4,484 $64,45416,6892,800

131,4802,483,5412,703,448

1,78421,49215,46920,719

515,164574,628

1,932,189131,48065,151

2,128,820 $

TOTAL

9,31893,02922,2992,800

131,4802,586,1142,845,040

5,62521,49215,46922,719

543,164608,469

2,004,762146,95384,856

2,236,571

See accountant's report.The accompanying notes are an integral part of this statement.

11

pa•wauSu•wI

ernm

enct

iviti

es

of-"

/— 1oo

d

/•— *r-csCN

C

o*VOvo"

O00"'i'w-T00*— <CM"

oCNooooIS

rs"

oo oCN ;-; fs

IIH

1BE04

,-j,

9-f c nV q) o

63, OS

/-S f~*

S8oo voON* —•'G*' '

i1•5

mtj1

»n

R^f<n"*C<

P5>,vo00

y*a en

«« *" c J3 .H

Opera

ting

Gra

nts

&antrib

utio

ns

U

24nfn

o

m

4 4 o(Nen

v u s M8 « o I J laa u tt p£ < w^n S 5 < o j T — ^, u a| § eS« « M«S .H o q « z ' •^ ^ ^ s S -S aae^ u<!i2 a> 1 s= w o 5 -2 « - W - M« S -5 E o A vo

w w OH 3 H H U Z 2:

•2 3

eH

in

Va

|4o"

w

S3^- VOrn -|ON

00oo"in

o00

**!*fON

go

00

>— 1VD

>r»ON

VI

S

00

**»^H

vO

00

vo"m

w

ooo

vo

^1~•K.S2

^

•^ S

It§CO vtuU ou 5Cfl C

00€

o

s

u<

co

s £ *«g g £ Ioojs S

auS

£•nS

*CPk

S

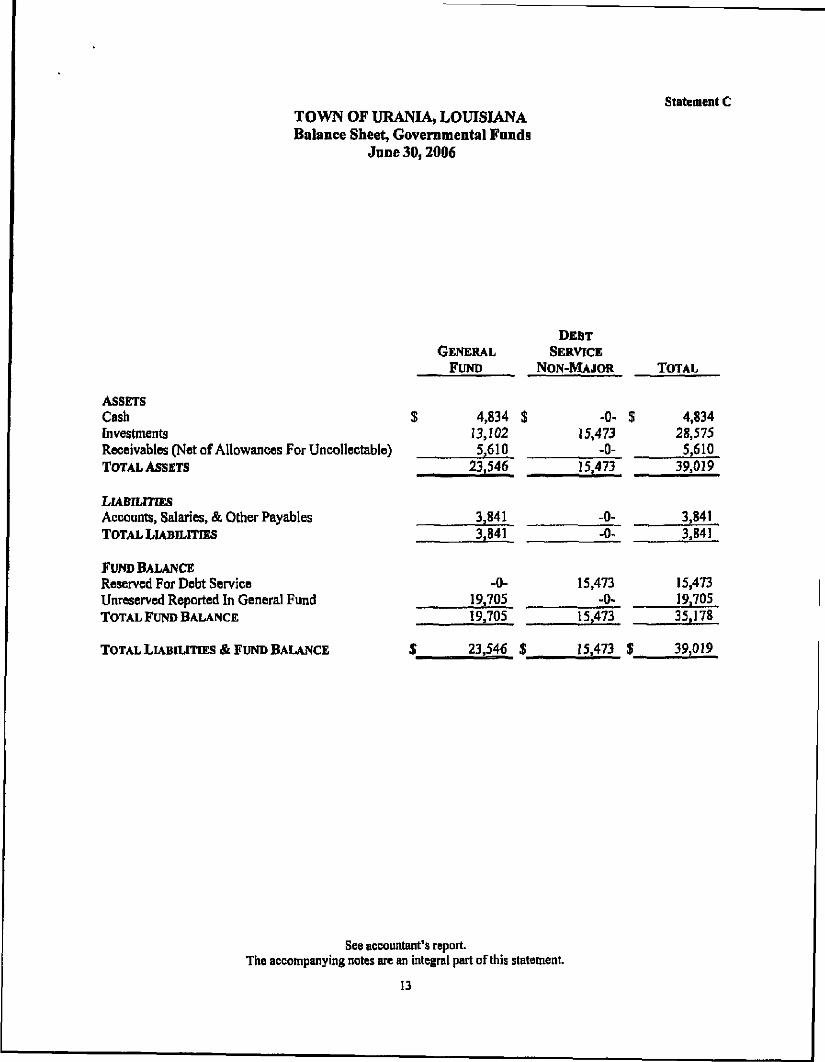

TOWN OF URANIA, LOUISIANABalance Sheet, Governmental Funds

June 30,2006

Statement C

ASSETSCashInvestmentsReceivables (Net of Allowances For Uncollectable)TOTAL ASSETS

LIABILITIESAccounts, Salaries, & Other PayablesTOTAL LIABILITIES

FUND BALANCEReserved For Debt ServiceUnreserved Reported In General FundTOTAL FUND BALANCE

TOTAL LIABILITIES & FUND BALANCE

DEBTGENERAL SERVICE

FUND NON-MAJOR

J 4,834 $13,1025,610

23,546

3,8413,841

-0-19,70519,705

: 23,546 $

-0- $15,473

-0-15,473

-0--0~

15,473-0-

15,473

15,473 $

TOTAL

4,83428,575

5,61039,019

3,8413,841

15,47319,70535,178

39,019

See accountant's report.The accompanying notes are an integral part of this statement

13

Statement DTOWN OF URANIA, LOUISIANA

Reconciliation of The Government Funds Balance Sheetto the Government-Wide Financial Statement of Net Assets

June 30,2006

Amounts reported for governmental activities in the Statement of Net Assets are different because:

Fund Balance, Total Governmental Funds (Statement C) $ 35,178

Capital assets used in governmental activities are not financialresources and, therefore, are not reported in the governmentalfunds. 102,573

Long-term liabilities including bonds payable are not due andpayable in the current period and, therefore, are not reportedin the governmental funds.

Other (30,000)

Net Assets of Governmental Activities (Statement A) $ 107,751

See accountant's report.The accompanying notes are an integral part of this statement.

14

TOWN OF URANIA, LOUISIANAStatement of Revenues, Expenditures &

Changes in Fund BalancesGovernmental Funds

For the Year Ended June 30,2006

Statement E

REVENUESFees & ChargesTaxesFinesGrantsInterestOtherTOTAL REVENUES

EXPENDITURESGeneral & AdministrativePolice ExpenseRecreationalFireStreet & SanitationDebt ServiceCapital OutlayTOTAL EXPENDITURES

EXCESS (DEFICIENCY) OF REVENUES OVER(UNDER) EXPENDITURES

OTHER FINANCING SOURCES (USES)Transfers In (Out)TOTAL OTHER FINANCING SOURCES (USES)

NET CHANGE IN FUND BALANCE

FUND BALANCES-BEGINNINGFUND BALANCES-ENDING

GENERAL

$ 68,682 $7,836

76,34813,210

8574,884

171,817

120,15331,0546,726

10,4961,292

-0-4,045

173,766

(1,949)

5,0005,000

3,051

16,654$ 19,705 $

DEBTSERVICE

NON-MAJOR

-0- $5,076

-0"-0--0-172

5,248

-0--0--0--0--0-

3,600-0-

3,600

1,648

-0--0-

1,648

13,82515,473 $

TOTAL

68,68212,91276,34813,210

8575,056

177,065

120,15331,0546,726

10,4961,2923,6004,045

177,366

(301)

5,0005,000

4,699

30,47935,178

See accountant's report.The accompanying notes are an integral part of this statement

15

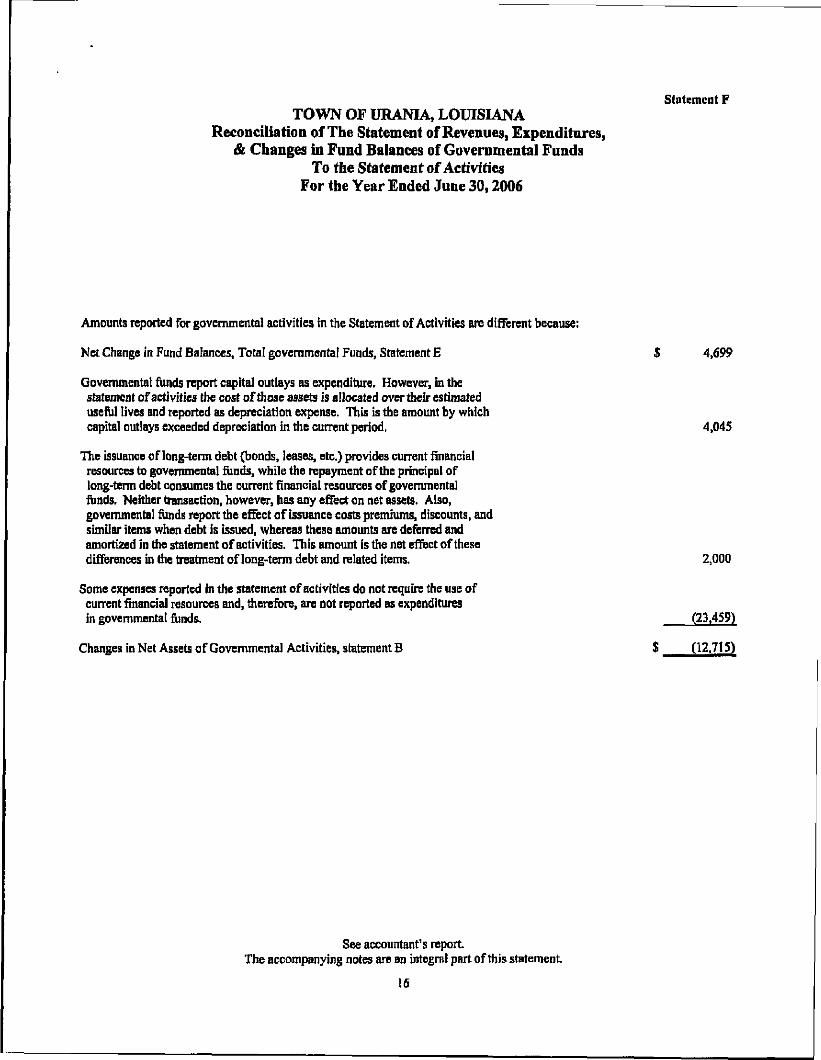

Statement FTOWN OF URANIA, LOUISIANA

Reconciliation of The Statement of Revenues, Expenditures,& Changes in Fund Balances of Governmental Funds

To the Statement of ActivitiesFor the Year Ended June 30,2006

Amounts reported for governmental activities in the Statement of Activities are different because:

Net Change in Fund Balances, Total governmental Funds, Statement E S 4,699

Governmental funds report capital outlays as expenditure. However, in thestatement of activities the cost of those assets is allocated over their estimateduseful lives and reported as depreciation expense. This is the amount by whichcapital outlays exceeded depreciation in the current period. 4,045

The issuance of long-term debt (bonds, leases, etc.) provides current financialresources to governmental funds, while the repayment of the principal oflong-term debt consumes the current financial resources of governmentalfunds. Neither transaction, however, has any effect on net assets. Also,governmental funds report the effect of issuance costs premiums, discounts, andsimilar items when debt is issued, whereas these amounts are deferred andamortized in the statement of activities. This amount is the net effect of thesedifferences in the treatment of long-term debt and related items. 2,000

Some expenses reported in the statement of activities do not require the use ofcurrent financial resources and, therefore, are not reported as expendituresin governmental funds. (23,459)

Changes in Net Assets of Governmental Activities, statement B $ (12.715)

See accountant's reportThe accompanying notes are an integral part of this statement.

16

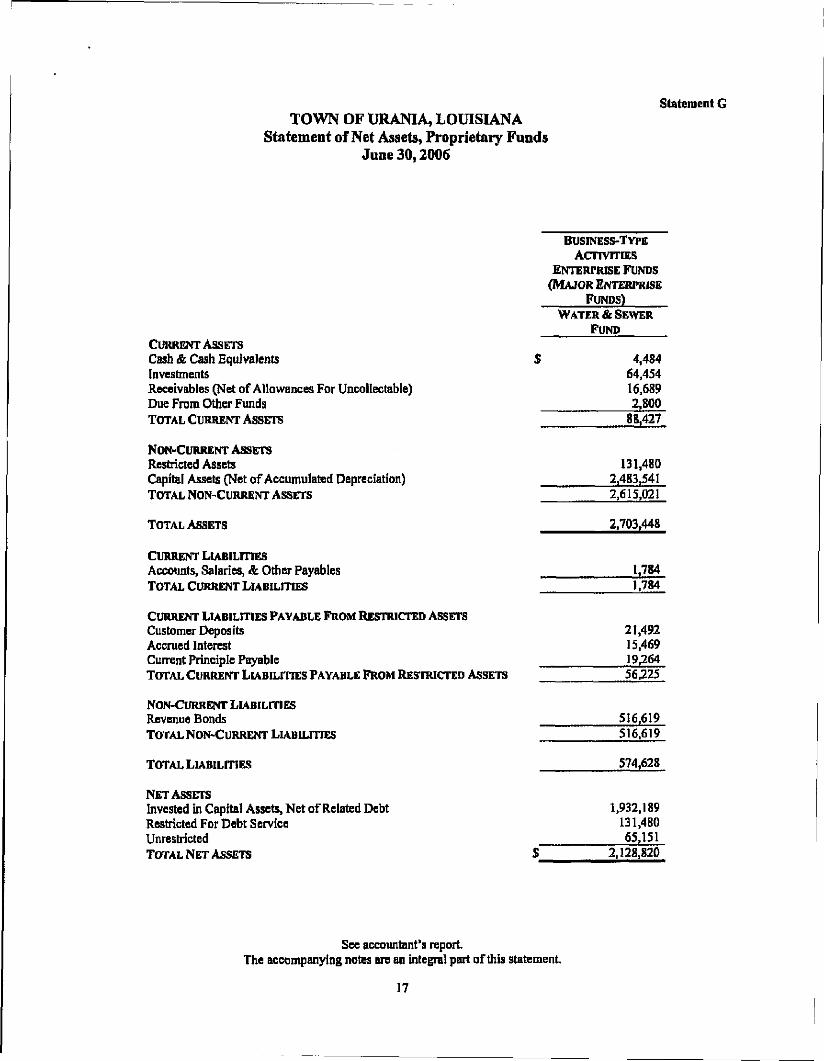

Statement GTOWN OF URANIA, LOUISIANA

Statement of Net Assets, Proprietary FundsJune 30,2006

BUSINESS-TYPEACTIVITIES

ENTERPRISE FUNDS(MAJOR ENTERPRISE

FUNDS)WATER & SEWER

FUNDCURRENT ASSETSCash & Cash Equivalents $ 4,484Investments 64,454Receivables (Net of Allowances For Uncollectable) 16,689Due From Other Funds 2,800TOTAL CURRENT ASSETS 88,427

NON-CURRENT ASSETSRestricted Assets 131,480Capital Assets (Net of Accumulated Depreciation) 2,483,541TOTAL NON-CURRENT ASSETS 2,615,021

TOTAL ASSETS 2,703,448

CURRENT LIABILITIESAccounts, Salaries, & Other Payables 1,784TOTAL CURRENT LIABILITIES 1.784

CURRENT LIABILITIES PAYABLE FROM RESTRICTED ASSETSCustomer Depos its 21,492Accrued Interest 15,469Current Principle Payable 19,264TOTAL CURRENT LIABILITIES PAYABLE FROM RESTRICTED ASSETS 56,225

NON-CURRENT LIABILITIESRevenue Bonds 516,619TOTAL NON-CURRENT LIABILITIES 516.619

TOTAL LIABILITIES 574,628

NET ASSETSInvested in Capital Assets, Net of Related Debt 1,932,189Restricted For Debt Service 131,480Unrestricted 65,151TOTAL NET ASSETS $ 2.128,820

See accountant's reportThe accompanying notes are an integral part of this statement.

17

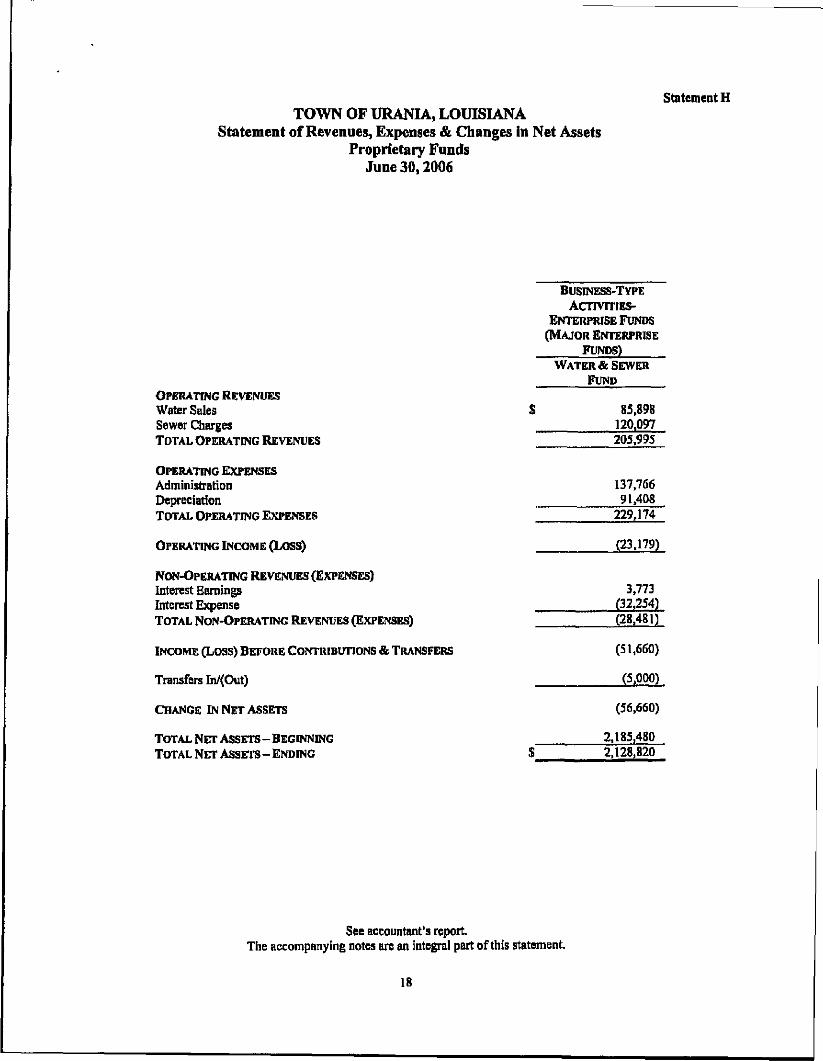

Statement HTOWN OF URANIA, LOUISIANA

Statement of Revenues, Expenses & Changes in Net AssetsProprietary Funds

June 30,2006

OPERATING REVENUESWater SalesSewer ChargesTOTAL OPERATING REVENUES

OPERATING EXPENSESAdministrationDepreciationTOTAL OPERATING EXPENSES

OPERATING INCOME (Loss)

NON-OPERATING REVENUES (EXPENSES)Interest EarningsInterest ExpenseTOTAL NON-OPERATING REVENUES (EXPENSES)

INCOME (Loss) BEFORE CONTRIBUTIONS & TRANSFERS

Transfers In/(Out)

CHANGE IN NET ASSETS

TOTAL NET ASSETS - BEGINNINGTOTAL NET ASSETS - ENDING

BUSINESS-TYPEAcnvrriES-

ENTERPRISE FUNDS(MAJOR ENTERPRISE

FUNDS)WATER & SEWER

FUND

85,898120,097205,995

137,76691,408

229,174

(23,179)

3,773(32,254)(28,481)

(51,660)

(53000)

(56,660)

2.185.4802,128.820

See accountant's reportThe accompanying notes are an integral part of this statement.

18

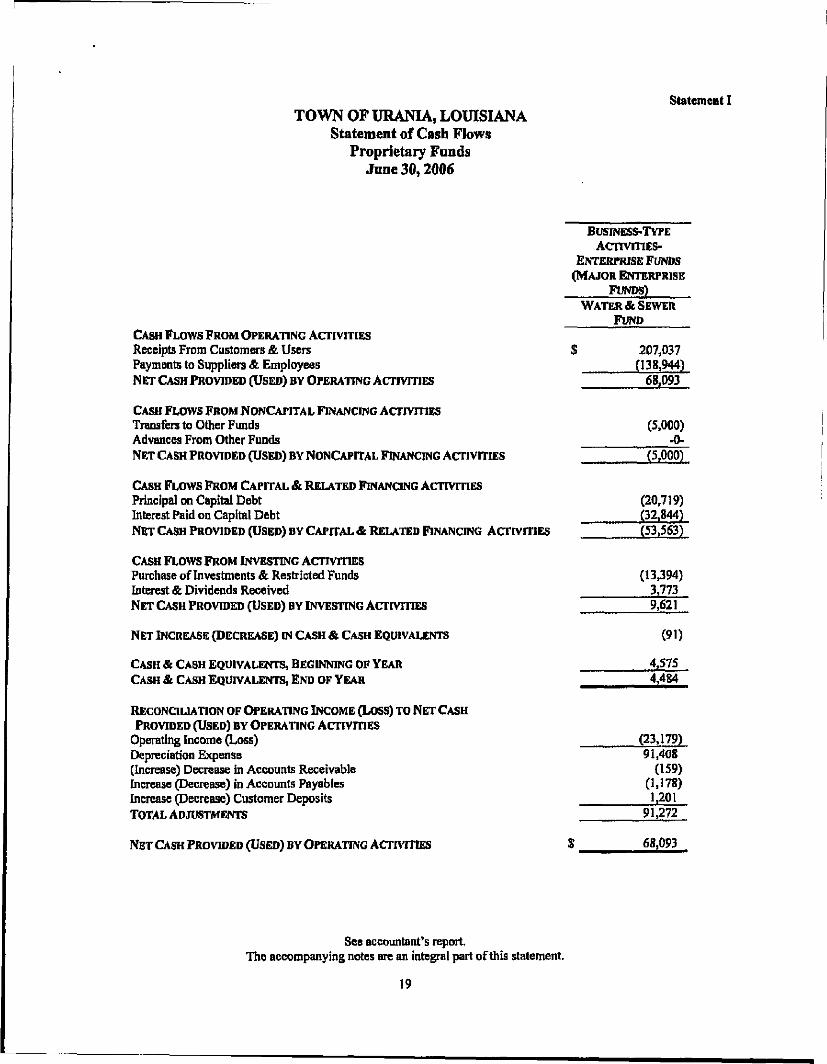

Statement ITOWN OF URANIA, LOUISIANA

Statement of Cash FlowsProprietary Funds

June 30,2006

CASH FLOWS FROM OPERATING ACTIVITIESReceipts From Customers & UsersPayments to Suppliers & EmployeesNET CASH PROVIDED (USED) BY OPERATING ACTIVITIES

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESTransfers to Other FundsAdvances From Other FundsNET CASH PROVIDED (USED) BY NONCAPITAL FINANCING ACTIVITIES

CASH FLOWS FROM CAPITAL & RELATED FINANCING ACTIVITIESPrincipal on Capital DebtInterest Paid on Capital DebtNET CASH PROVIDED (USED) BY CAPITAL & RELATED FINANCING ACTIVITIES

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of Investments & Restricted FundsInterest & Dividends ReceivedNET CASH PROVIDED (USED) BY INVESTING ACTIVITIES

NET INCREASE (DECREASE) IN CASH & CASH EQUIVALENTS

CASH & CASH EQUIVALENTS, BEGINNING OF YEARCASH & CASH EQUIVALENTS, END OF YEAR

RECONCILIATION OF OPERATING INCOME (Loss) TO NET CASHPROVIDED (USED) BY OPERATING AcnvrriES

Operating Income (Loss)Depreciation Expense(Increase) Decrease in Accounts ReceivableIncrease (Decrease) in Accounts PayablcsIncrease (Decrease) Customer DepositsTOTAL ADJUSTMENTS

NET CASH PROVIDED (USED) BY OPERATING ACTIVITIES

BUSINESS-TYPEAcnvmES-

ENTERPRISE FUNDS(MAJOR ENTERPRISE

FUNDS)WATER & SEWER

FUND

$ 207,037(138,944)

68,093

(5,000)-0-

(5,000)

(20,719)(32,844)(53,563)

(13,394)3,7739,621

(91)

4,5754,484

(23,179)91,408

(159)0,178)

1,20191,272

68.093

See accountant's report.The accompanying notes are an integral part of this statement.

19

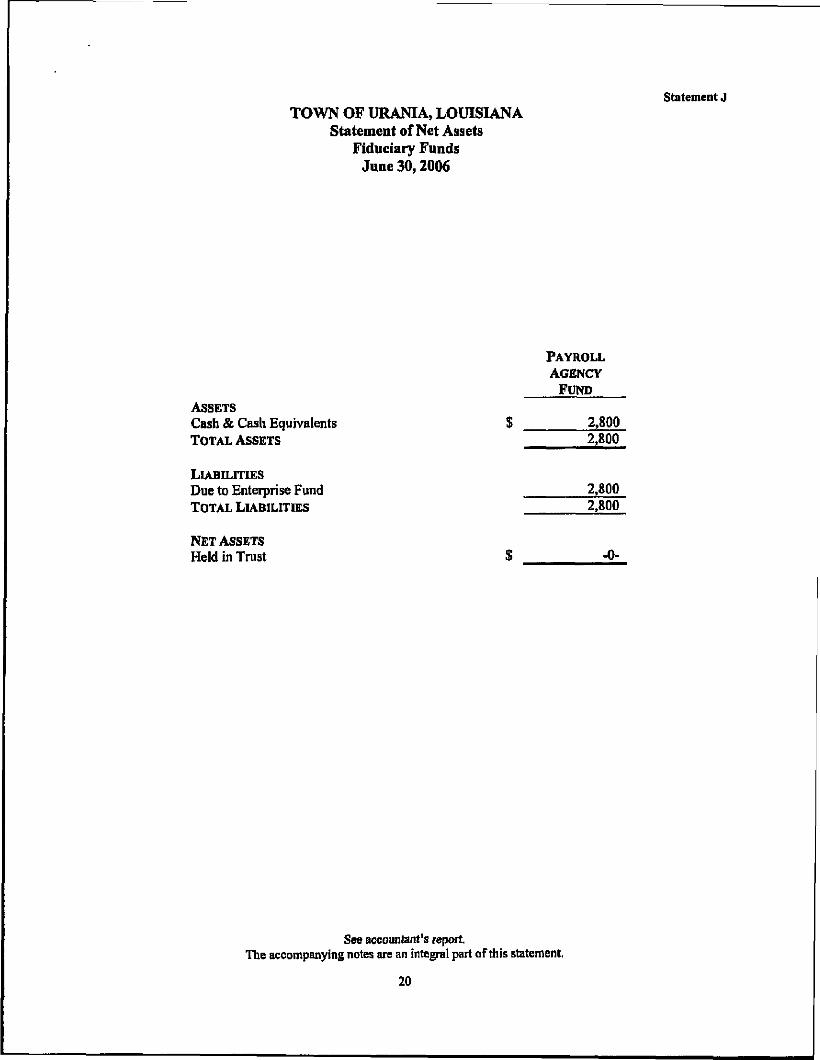

Statement JTOWN OF URANIA, LOUISIANA

Statement of Net AssetsFiduciary Funds

June 30,2006

PAYROLLAGENCY

FUNDASSETSCash & Cash Equivalents $ 2,800TOTAL ASSETS 2,800

LIABILITIESDue to Enterprise Fund 2,800TOTAL LIABILITIES 2,800

NET ASSETSHeld in Trust $ -0-

See accountant's reportThe accompanying notes are an integral part of this statement.

20

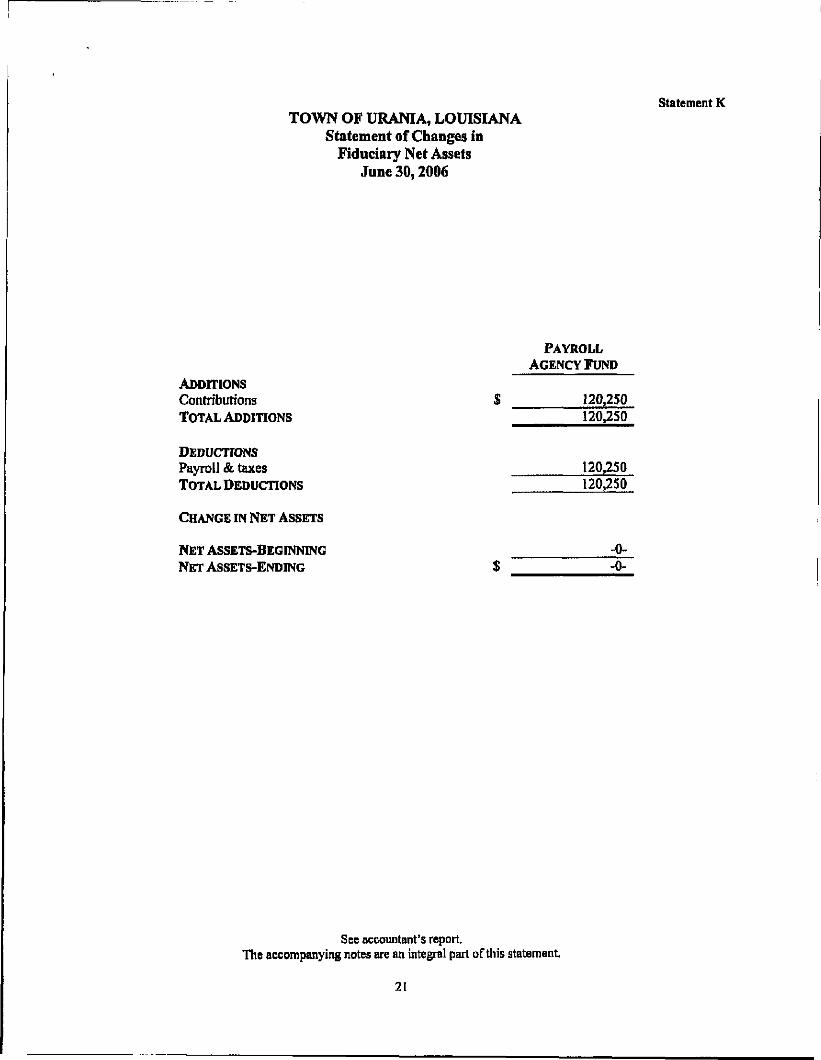

Statement KTOWN OF URANIA, LOUISIANA

Statement of Changes inFiduciary Net Assets

June 30,2006

PAYROLLAGENCY FUND

ADDITIONSContributions $ 120,250TOTAL ADDITIONS 120,250

DEDUCTIONSPayroll & taxes 120,250TOTAL DEDUCTIONS 120,250

CHANGE IN NET ASSETS

NET ASSETS-BEGINNING -0-NET ASSETS-ENDING $ -o-

Sce accountant's report.The accompanying notes are an integral part of this statement

21

iH^tMw^%ijigiflgnn^it^itt^

NOTES To THE BASICFINANCIAL STATEMENTS

22

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS

(1) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Town of Urania was incorporated under the provisions of the Lawrason Act. The entity operates under theMayor-Board of Alderman form of government. The entity provides the following significant services to itsresidents as provided by its charter: public safety (police and fire), highways and streets, utilities (water, gas andsewer services) and general administrative functions, including coordination of related services with parish, stateand federal governing bodies.

The entity applies all GASB pronouncements as well as the Financial Accounting Standards Boardpronouncements issued on or before November 30, 1989, unless those pronouncements conflict with or contradictGASB pronouncements.

The accounting and reporting policies of the Town of Urania conform to generally accepted accounting principlesas applicable to governments. Such accounting and reporting procedures also conform to the requirements ofLouisiana Revised Statutes 24:517 and to the guides set forth in the Louisiana Municipal Audit and AccountingGuide, and to the industry audit guide, Audits of State and Local Governmental Units.

The following is a summary of certain significant accounting policies:

A. GOVERNMENT-WIDE AND FUND FINANCIAL STATEMENTS

The government-wide financial statements (i.e., the statement of net assets and the statement of changes in netassets) report information on all of the nonfiduciary activities of the primary government and its component units.For the most part, the effect of interfund activity has been removed from these statements. Governmentalactivities, which normally are supported by taxes and intergovernmental revenues, are reported separately frombusiness-type activities, which rely to a significant extent on fees and charges for support Likewise, the primarygovernment is reported separately from certain legally separate component units for which the primarygovernment is financially accountable.

The statement of activities demonstrates the degree to which the direct expenses of a given function or segmentare offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function orsegment. Program revenues include 1) charges to customers or applicants who purchase, use or directly benefitfrom goods, services, or privileges provided by a given function or segment and 2) grants and contributions thatare restricted to meetings the operational or capital requirements of a particular function or segment. Taxes andother items not properly included among program revenues are reported instead as general revenues.

Separate financial statements are provided for governmental funds, proprietary funds, and fiduciary funds, eventhrough the latter are excluded from the government-wide financial statements. Major individual governmentalfunds and major individual enterprise funds are reported as separate columns in the fund financial statements.

B. MEASUREMENT Focus, BASIS OF ACCOUNTING, AND FINANCIAL STATEMENT PRESENTATION

The government-wide financial statements are reported using the economic resources measurement focus and theaccrual basis of accounting, as arc the proprietary fund and fiduciary fund financial statements. Revenues arerecorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of relatedcash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similaritems are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met.

23

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

Governmental fund financial statements are reported using the current financial resources measurement focus andthe modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable andavailable. Revenues are considered to be available when they are collectible within the current period or soonenough thereafter to pay liabilities of the current period. For this purpose, the government considers revenues tobe available if they are collected within 60 days of the end of the current fiscal period. Expenditures generally arerecorded when a liability is incurred, as under accrual accounting. However, debt service expenditures, as well asexpenditures related to compensated absences and claims and judgments, are recorded only when payment is due.

Property taxes, franchise taxes, licenses, and interest associated with the current fiscal period are all considered tobe susceptible to accrual and so have been recognized as revenues of the current fiscal period. All other revenueitems are considered to be measurable and available only when cash is received by the government.

The municipality reports the following major governmental funds:

The General Fund is the municipality's primary operating fund. It accounts for all financial resources ofthe general government, except those required to be accounted for in another fund

The municipality reports the following major proprietary funds:

• Water and Sewer Fund

Private-sector standards of accounting and financial reporting issued prior to December 1, 1989, generally arefollowed in both the government-wide and proprietary fund financial statements'to the extent that those standardsdo not conflict with or contradict guidance of the Governmental Accounting Standards Board, Governments alsohave the option of following subsequent private-sector guidance for their business-type activities and enterprisefunds, subject to this same limitation. The government has elected not to follow subsequent private-sectorguidance.

As a general rule the effect of interfund activity has been eliminated from the government-wide financialstatements. Exceptions to this general rule are payments-In-lieu of taxes and other charges between thegovernments enterprise operations. Elimination of these charges would distort the direct costs and programrevenues reported for the various functions concerned.

Amounts reported as program revenues include I) charges to customers or applicants for goods, services, orprivileges provided, 2) operating grants and contributions, and 3) capital grants and contributions, includingspecial assessments. Internally dedicated resources are reported as general revenues rather man as programrevenues. Likewise, general revenues include all taxes.

Proprietary funds distinguish operating revenues and expenses from nonoperating items. Operating revenues andexpenses generally result from providing services and producing and delivering goods in connection with aproprietary fund's principal ongoing operations. The principal operating revenues are charges for services andsales taxes. Operating expenses for enterprise funds include the cost of sales and services, administrativeexpenses, and depreciation on capital assets. All revenues and expenses not meeting this definition are reportedas nonoperating revenues and expenses.

24

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

C. FIXED ASSETS & LONG-TERM LIABILITIES

For the year ended June 30, 2006, no interest costs were capitalized for construction of fixed assets.

Depreciation of all exhaustible fixed assets is charged as an expense against its operations. Accumulateddepreciation is reported on the proprietary fund balance sheet and governmental fund statement of activities.Depreciation has been provided over the estimated useful lives using the straight-line method. The estimateduseful lives are as follows:

Life In YearsWater System 40Sewer System 40Buildings 40Equipment 5-10

D. BUDGETS & BUDGETARY ACCOUNTING

The entity follows these procedures in establishing the budgetary data reflected in these financial statements:

(1) The Town clerk prepares a proposed budget based on departmental group budget requests, andsubmits the same to the Mayor and Board of Aldermen for approval.

(2) The entity does not utilize the budget in comparison form in financial statement presentation duringthe year.

(3) All budgetary appropriations lapse at the end of the fiscal year.

(4) The entity does not utilize encumbrance accounting.

(5) The budget was amended during the year.

E. CASH & INVESTMENTS

All cash and investments (CD's over 90 days) are reported at cost and are on deposit at federally insured banks:

It is the entity's policy for deposits to be 100% secured by collateral at market or par, whichever is lower,less the amount of the Federal Deposit Insurance Corporation insurance. The entity's deposits arecategorized to give an indication of the level of risk assumed by the entity at fiscal year-end. Thecategories are described as follows:

• Category 1 - Insured or collateralized with securities held by the entity or by its agent in theentity's name.

• Category 2 - Collateralized with securities held by the pledging financial institution's trustdepartment or agent in the entity's name.

• Category 3 - Uncollateralized.

25

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

BankSabine State Bank and Concordia Bank & Trust

Bank Balance6-30-2006

238,767

Amounts on deposit at the batik are secured by thefollwving.

DescriptionFDIC (Category 7)

Market Value238.767

F. INVENTORIES

Immaterial amounts of inventory are maintained for general fund and enterprise fund operations and, accordingly,these supplies are expensed as purchased.

G. ACCOUNTS RECEIVABLE & BAD DEBTS - GENERAL FUND & ALLOWANCE FOR BAD DEBTS -ENTERPRISE FUND

At June 30, 2006 no reserve for bad debts in the general fund was required since the estimated uncollectablereceivables outstanding were considered immaterial.

EnterpriseFund

GovernmentalFund

Water and SewerFund

Fees & Charges $CustomerAllowance for Bad DebtsTotal $

-0- $17,567(878)

16t689 $

GeneralFund

5,610-0-•0-

5,610

H. COMPENSATED ABSENCES

The entity has no compensated absence policy.

26

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

I. RESERVES

The entity records reserves to indicate that a portion of its net assets balances are legally restricted for a specificfuture use. The following is a list of such reserves and a description of each:

Reserved for System Maintenance

This amount represents monies reserved for repairs and replacement of the water system.

Reserved- Revenue Bonds

This amount represents monies reserved as required by the revenue bond indentures.

Reserved for Debt Service

Certain assets have been reserved in the Debt Service Fund for future payment of long-term liabilities ofthe governmental funds.

(2) AD VALOREM TAXES

The entity levies taxes on real and business personal property located within its boundaries. The entity utilizes theservices of the LaSalle Parish Tax Assessor to assess the property values and prepare the entity's property tax roll.The entity bills and collects its own property taxes.

Property Tax Calendar

Assessment Date January 1Levy Date No Later Than June 1Tax Bills Mailed On or About October 15Total Taxes Are Due December 31Penalties and Interest are Added January 1Lien Date January 1

For the year ended June 30, 2006, taxes of 8.2 mills were levied against property having a valuation of some$1,628,140 which produced some $13,352 in revenue.

Ad Valorem Taxes are broken down as follows:

MillsUrania Debt Service - General Obligation Bonds 1.625Urania Sewer District No. 1 - General Obligation Bonds 1.625General Alimony 4.95Total 8.2

27

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

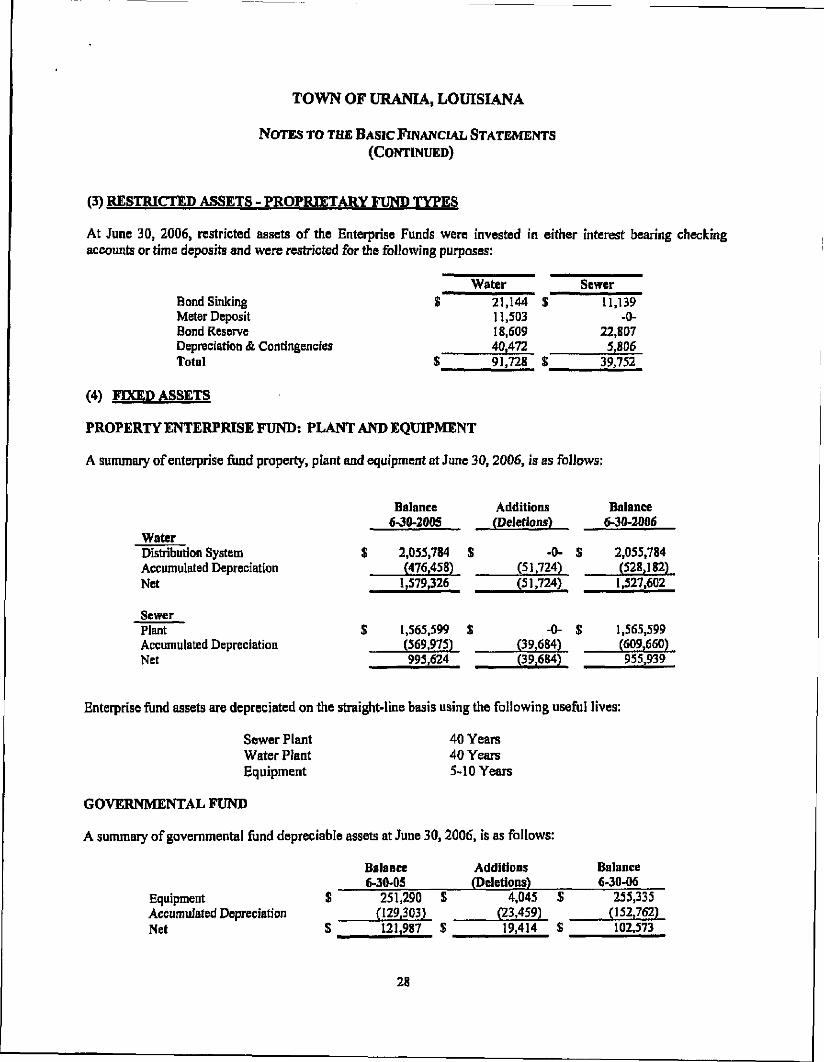

(3) RESTRICTED ASSETS - PROPRIETARY FUND TYPES

At June 30, 2006, restricted assets of the Enterprise Funds were invested in either interest bearing checkingaccounts or time deposits and were restricted for the following purposes:

Bond Sinking £Meter DepositBond ReserveDepreciation & ContingenciesTotal $

(4) FIXED ASSETS

PROPERTY ENTERPRISE FUND: PLANT AND EQUIPMENT

A summary of enterprise fund property, plant and equipment at June 30,2006, is as follows;

Water21,14411,50318,60940,47291,728

$

$

Sewer11,139

-0-22,8075,806

39,752

WaterDistribution SystemAccumulated DepreciationNet

SewerPlantAccumulated DepreciationNet

Balance Additions6-30-2005 (Deletions)

2,055,784 $(476,458)

1,579,326

1,565,599 $(569,975)995,624

-0- S(51,724)(51,724)

-0- $(39,684)(39,684)

Balance6-30-2006

2,055,784(528,182)1.527,602

1,565,599(609,660)955,939

Enterprise fund assets are depreciated on the straight-line basis using the following useful lives:

Sewer PlantWater PlantEquipment

40 Years40 Years5-10 Years

GOVERNMENTAL FUND

A summary of governmental fund depreciable assets at June 30,2006, is as follows:

EquipmentAccumulated DepreciationNet

£

S

Balance6-30-05

251,290(129,303)121,987

Additions(Deletions)

$

$

4,045(23,459)19,414

$

$

Balance6-30-06

255,335(152,762)102,573

28

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

Government fund assets are depreciated on the straight-line basis using the following useful lives:

Equipment 5-10 Years

Buildings 40 Years

(5) CHANGES IN LONG-TERM DEBT

The following is a summary of bond transactions of the Town of Urania for the year ended June 30,2006:

General Obligation | RevenuePublic

Public ImprovementImprovement District #1 Water

(Sewer) Sewer Utility Sewer TotalBonds Payable 06/30/2005 $ 16,000 $ 16,000 $ 450,602 $ 106,000 $ 588,602Principal Retirement (1,000) (1,000) (14,719) (6j)QO) (22,719)Bonds Payable 06/30/2006 $ 15,000 $ 15,000 $ 435,883 $ 100,000 $ 565,883

Notes and bonds payable at June 30,2006 are comprised of the following individual issues:

General Obligation Bonds Administer bv the Debt Service Fund:

Two 1977 issues of $42,935 each serial bonds due in annual installments of $1,000, increasingto $3,000 annually at maturity at September 28,2016; interest at 5%. $ 30,000

Revenue bonds administered bv the Water and Sewer Enterprise Fund;

$185,000 water serial bonds due annually in installments of $2,935, increasing in increments of$1,000 to $10,000 annually at maturity at March 1,2012; interest at 5%. 54,000

$197,400 sewer serial bonds due annually in installments of $2,935, increasing in increments of$1,000 to $12,935 annually at maturity at September 28,2016; interest at 5%. 100,000

$454,000 water serial bonds issued November 14,1990,40 year maturity, $44,000 @ 6% withannual installments of $2,944 and $410,000 @ 6.25% with annual installments of $27,855. 381,883

Total $ 565,883

29

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

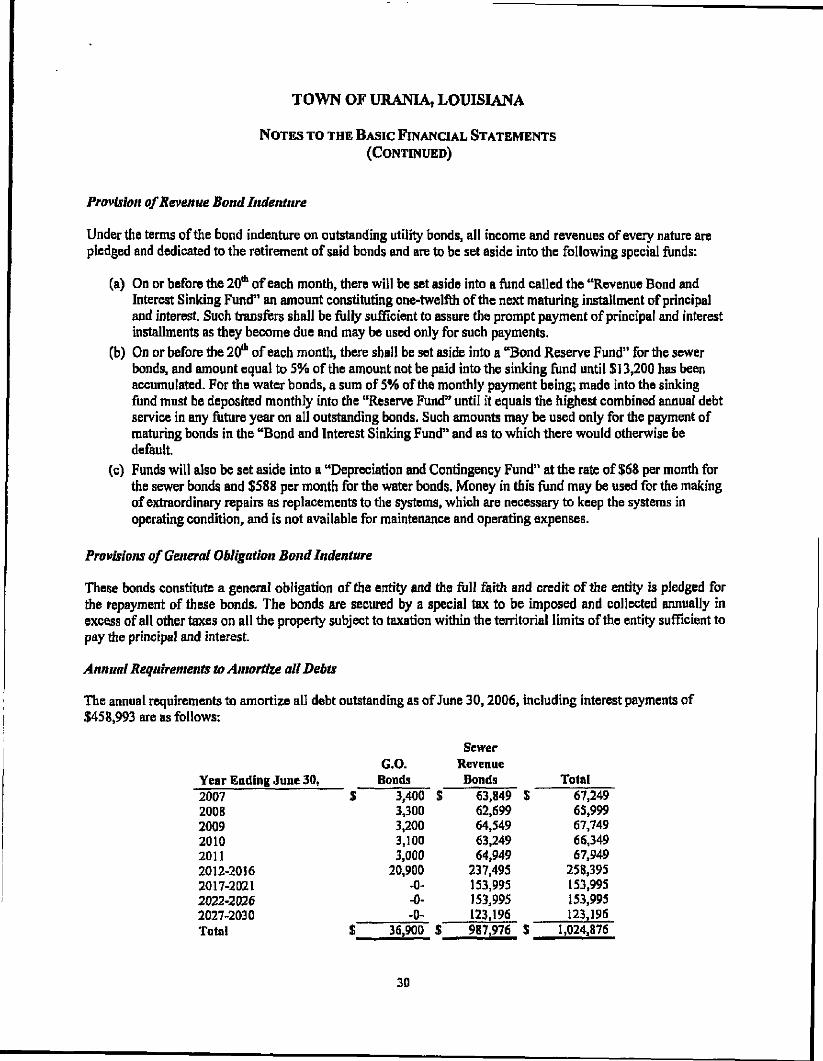

Provision of Revenue Bond Indenture

Under the terms of the bond indenture on outstanding utility bonds, all income and revenues of every nature arepledged and dedicated to the retirement of said bonds and are to be set aside into the following special funds:

(a) On or before the 20th of each month, there will be set aside into a fund called the "Revenue Bond andInterest Sinking Fund" an amount constituting one-twelfth of the next maturing installment of principaland interest. Such transfers shall be fully sufficient to assure the prompt payment of principal and interestinstallments as they become due and may be used only for such payments.

(b) On or before the 20th of each month, there shall be set aside into a "Bond Reserve Fund" for the sewerbonds, and amount equal to 5% of the amount not be paid into the sinking fund until $13,200 has beenaccumulated. For the water bonds, a sum of 5% of the monthly payment being; made into the sinkingfund must be deposited monthly into the "Reserve Fund** until it equals the highest combined annual debtservice in any future year on all outstanding bonds. Such amounts may be used only for the payment ofmaturing bonds in the "Bond and Interest Sinking Fund" and as to which there would otherwise bedefault.

(c) Funds will also be set aside into a "Depreciation and Contingency Fund" at the rate of $68 per month forthe sewer bonds and $588 per month for the water bonds. Money in this fund may be used for the makingof extraordinary repairs as replacements to the systems, which are necessary to keep the systems inoperating condition, and is not available for maintenance and operating expenses.

Provisions of General Obligation Bond Indenture

These bonds constitute a general obligation of the entity and the fulJ faith and credit of the entity is pledged forthe repayment of these bonds. The bonds are secured by a special tax to be imposed and collected annually inexcess of all other taxes on all the property subject to taxation within the territorial limits of the entity sufficient topay the principal and interest.

Annual Requirements to Amortize all Debts

The annual requirements to amortize all debt outstanding as of June 30,2006, including interest payments of$458,993 are as follows;

TotalYear Ending June 30,200720082009201020112012-20162017-20212022-20262027-2030Total

G.O.Bonds

$ 3,400 $3,3003,2003,1003,000

20,900-0--0--0-

$ 36,900 $

SewerRevenueBonds

63,84962,69964,54963,24964,949

237,495153,995153,995123,196987,976

$ 67,24965,99967,74966,34967,949

258,395153,995153,995123,196

S 1,024,876

30

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

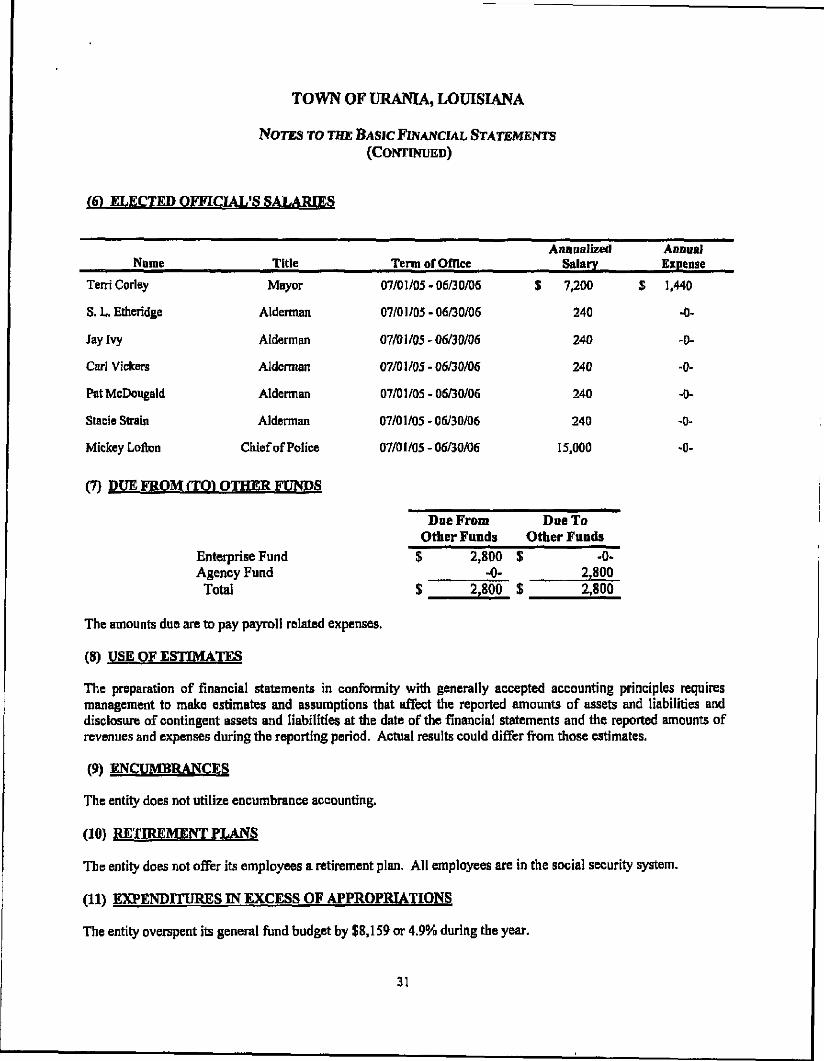

(6) ELECTED OFFICIAL'S SALARIES

Name

Terri Corley

S. L. Etheridge

Jay Ivy

Carl Vickers

Pat McDougald

Stacie Strain

Mickey Lofton

Title

Mayor

Alderman

Alderman

Alderman

Alderman

Alderman

Chief ofPolice

Term of Office

07/01/05-06/30/06

07/01/05-06/30/06

07/01/05-06/30/06

07/01/05-06/30/06

07/01/05-06/30/06

07/01/05-06/30/06

07/01/05-06/30/06

AnnualizedSalary

$ 7,200

240

240

240

240

240

15,000

AnnualExpense

$ 1,440

-0-

-0-

-0-

-0-

-0-

-0-

m DUE FROM (TO) OTHER FUNDS

Enterprise FundAgency Fund

Total

Due FromOther Funds

$ 2,800-0-

$ 2,800

Due ToOther Funds

$ -o.2,800

$ 2,800

The amounts due are to pay payroll related expenses.

(8) USE OF ESTIMATES

The preparation of financial statements in conformity with generally accepted accounting principles requiresmanagement to make estimates and assumptions that affect the reported amounts of assets and liabilities anddisclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts ofrevenues and expenses during the reporting period. Actual results could differ from those estimates.

(9) ENCUMBRANCES

The entity does not utilize encumbrance accounting.

(10) RETIREMENT PLANS

The entity does not offer its employees a retirement plan, All employees are in the social security system.

(11) EXPENDITURES IN EXCESS OF APPROPRIATIONS

The entity overspent its general fund budget by J8,159 or 4.9% during the year.

31

TOWN OF URANIA, LOUISIANA

NOTES TO THE BASIC FINANCIAL STATEMENTS(CONTINUED)

(12) TRANSFERS

Transfers between funds were made for operational purposes.

32

REQUIRED SUPPLEMENTALINFORMATION

33

TOWN OF URANIA, LOUISIANAStatement of Revenues, Expenditures, & Changes in Fund Balance

Budget & ActualGeneral Fund

For the Year Ended June 30,2006

Statement 1

REVENUESFees & ChargesTaxesFinesGrantsInterestOtherTOTAL REVENUES

EXPENDITURESGeneral & AdministrativePolice ExpenseRecreationalFireStreet & SanitationDebt ServiceCapital OutlayTOTAL EXPENDITURES

EXCESS (DEFICIENCY) OF REVENUES OVER(UNDER) EXPENDITURES

OTHER FINANCING SOURCES (USES)Transfers In (Out)TOTAL OTHER FINANCING SOURCES (USES)

NET CHANGE IN FUND BALANCE

FUND BALANCES-BEGINNINGFUND BALANCES-ENDING

BUDGET AMOUNTS

ORIGINAL

65,4069,168

93,644•0--0-

4,136172,354

143,53211,7821,3004,7062,956

-0-±_

164,276 $

FINAL

66,067 S9,398

77,436-0--0-

4,547157,448

140,3919,2397,5437,1351,299

-0--0-

165,607 $

S

ACTUALAMOUNTS

BUDGETARYBASIS

68,6827,836

76,34813,210

8574,884

171,817

120,15331,0546,726

10,4961,292

-0-4,045

173,766

(1,949)

5,0005,000

3,051

16,65419,705

BUDGETVARIANCE

FAVORABLE(UNFAVORABLE)

$ 2,615(1,562)(1,088)13,210

857337

14,369

20,238(21,815)

817(3,361)

7-0-

(4,045)$ (8,159)

See accountant's report.The accompanying notes are an integral part of this statement

34

TOWN OF URANIA, LOUISIANA

MANAGEMENT LETTER COMMENTS

During the course of my audit, I observed conditions and circumstances that may be improved. Below aresituations that may be improved (if any) and recommendations for improvements.

CURRENT YEAR MANAGEMENT LETTER COMMENTS

There are no current year management letter comments.

35

TOWN OF URANIA, LOUISIANA

MANAGEMENT'S SUMMARYOF PRIOR YEAR FINDINGS

Legislative AuditorState of LouisianaBaton Rouge, Louisiana 70804-9397

The management of the Town or Urania, Louisiana has provided the following action summaries relating to auditfindings brought to their attention as a result of their financial audit for the year ended June 30,2005.

PRIOR YEAR FINDINGS

There were no prior year findings.

36

LOUISIANA ATTESTATION QUESTIONNAIRE

September 11,2006

JOHN R. VERCHER PCCertified Public AccountantP.O. Box 1608Jena, Louisiana 71342Tel: (318) 992-6348Fax:(318)992-4374

In connection with your review of our financial statements as of June 30,2006 and for the year then ended, and asrequired by Louisiana Revised Statute 24:513 and the Louisiana Governmental Audit Guide, we make thefollowing representations to you. We accept full responsibility for our compliance with the following laws andregulation and the internal controls over compliance with such laws and regulations. We have evaluated ourcompliance with the following laws and regulations prior to making these representations.

These representations are based on the information available to us as of July 30.2006.

Public Bid LawIt is true that we have complied with the public bid law, LSA-RS Title 38:2212, and, where applicable, theregulations of the Division of Administration, State Purchasing Office.

Yes[x] No[ ]

Code of Ethics for Public Officials and Public EmployeesIt is true mat no employees or officials have accepted anything of value, whether in the form of a service, loan, orpromise, from anyone that would constitute a violation of LSA-RS 42:1101-1124.

Yes[x] No[ ]

It is true that no member of the immediate family of any member of the governing authority, or the chiefexecutive of the governmental entity, has been employed by the governmental entity after April 1, 1980, undercircumstances that would constitute a violation of LSA-RS 42:1119.

Yes|> ] No[ ]

BudgetingWe have complied with the state budgeting requirements of the Local Government Budget Act (LSA-RS39:1301-14) or the budget requirements of LSA-RS 39:34.

Yes[x] No[ ]

Accounting and ReportingAll non-exempt governmental records are available as a public record and have been retained for at least threeyears, as required by LSA-RS 44:1,44:7,44:31, and 44:36.

Yes[x] No[ ]

We have filed our annual financial statements in accordance with LSA-RS 24:514, 33:463, and/or 39:92, asapplicable.

Yes[x]No[ ]

We have had our financial statements audited or compiled in accordance with-LSA-RS 24:513.

Yes [ x ] No [ ]MeetingsWe have complied with the provisions of the Open Meetings Law, provided in RS 42:1 through 42:12.

Yes[x] No[ ]DebtIt is true we have not incurred any indebtedness, other than credit for 90 days or less to make purchases in theordinary course of administration, nor have we entered into any lease-purchase agreements, without the approvalof the State Bond Commission, as provided by Article VII, Section 8 of the 1974 Louisiana Constitution, ArticleVI, Section 33 of the 1974 Louisiana Constitution, and LSA-RS 39:1410.60.

Yes fx ] No[ ]

Advances and BonusesIt is true we have not advanced wages or salaries to employees or paid bonuses in violation of Article VII, Section14 of the 1974 Louisiana Constitution, LSA-RS 14:138, and AG opinion 79-729.

Yes[x] No[ ]

We have disclosed to you all known noncompliance of the foregoing laws and regulations, as well as anycontradictions to the foregoing representations. We have made available to you documentation relating to theforegoing laws and regulations.

We have provided you with any communications from regulatory agencies or other sources concerning anypossible noncompliance with the foregoing laws and regulations, including any communications received betweenthe end of the period under examination and the issuance of this report. We acknowledge our responsibility todisclose to you any known noncompliance which may occur subsequent to the issuance of your report.

Title:

Top Related