Languages

Pages

Legal

Two Blue-Chips I Bought This Week:

Union Pacific and General Electric

Whitney Tilson

Kase Capital Management

12th Annual Value Investing Seminar

Trani, Italy

July 10, 2015

Kase Capital Management

Manages Three Hedge Funds and is a

Registered Investment Advisor

Carnegie Hall Tower

152 West 57th Street, 46th Floor

New York, NY 10019

(212) 277-5606

Disclaimer

THIS PRESENTATION IS FOR INFORMATIONAL AND EDUCATIONAL PURPOSES ONLY AND SHALL NOT BE CONSTRUED TO CONSTITUTE INVESTMENT ADVICE. NOTHING CONTAINED HEREIN SHALL CONSTITUTE A SOLICITATION, RECOMMENDATION OR ENDORSEMENT TO BUY OR SELL ANY SECURITY OR OTHER FINANCIAL INSTRUMENT.

INVESTMENT FUNDS MANAGED BY WHITNEY TILSON OWN SHARES IN UNION PACIFIC AND GENERAL ELECTRIC. HE HAS NO OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN AND MAY MAKE INVESTMENT DECISIONS THAT ARE INCONSISTENT WITH THE VIEWS EXPRESSED IN THIS PRESENTATION.

WE MAKE NO REPRESENTATION OR WARRANTIES AS TO THE ACCURACY, COMPLETENESS OR TIMELINESS OF THE INFORMATION, TEXT, GRAPHICS OR OTHER ITEMS CONTAINED IN THIS PRESENTATION. WE EXPRESSLY DISCLAIM ALL LIABILITY FOR ERRORS OR OMISSIONS IN, OR THE MISUSE OR MISINTERPRETATION OF, ANY INFORMATION CONTAINED IN THIS PRESENTATION.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS AND FUTURE RETURNS ARE NOT GUARANTEED.

-3-

Union Pacific

-5-

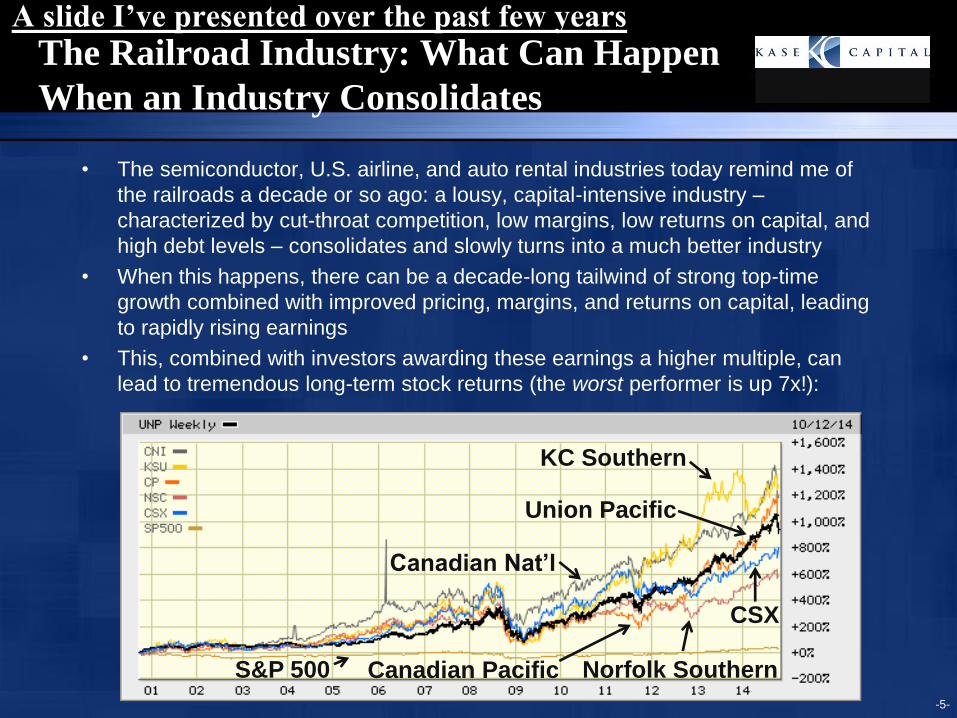

The Railroad Industry: What Can Happen

When an Industry Consolidates

• The semiconductor, U.S. airline, and auto rental industries today remind me of

the railroads a decade or so ago: a lousy, capital-intensive industry –

characterized by cut-throat competition, low margins, low returns on capital, and

high debt levels – consolidates and slowly turns into a much better industry

• When this happens, there can be a decade-long tailwind of strong top-time

growth combined with improved pricing, margins, and returns on capital, leading

to rapidly rising earnings

• This, combined with investors awarding these earnings a higher multiple, can

lead to tremendous long-term stock returns (the worst performer is up 7x!):

Norfolk Southern

CSX

Union Pacific

Canadian Pacific

KC Southern

Canadian Nat’l

S&P 500

A slide I’ve presented over the past few years

-6-

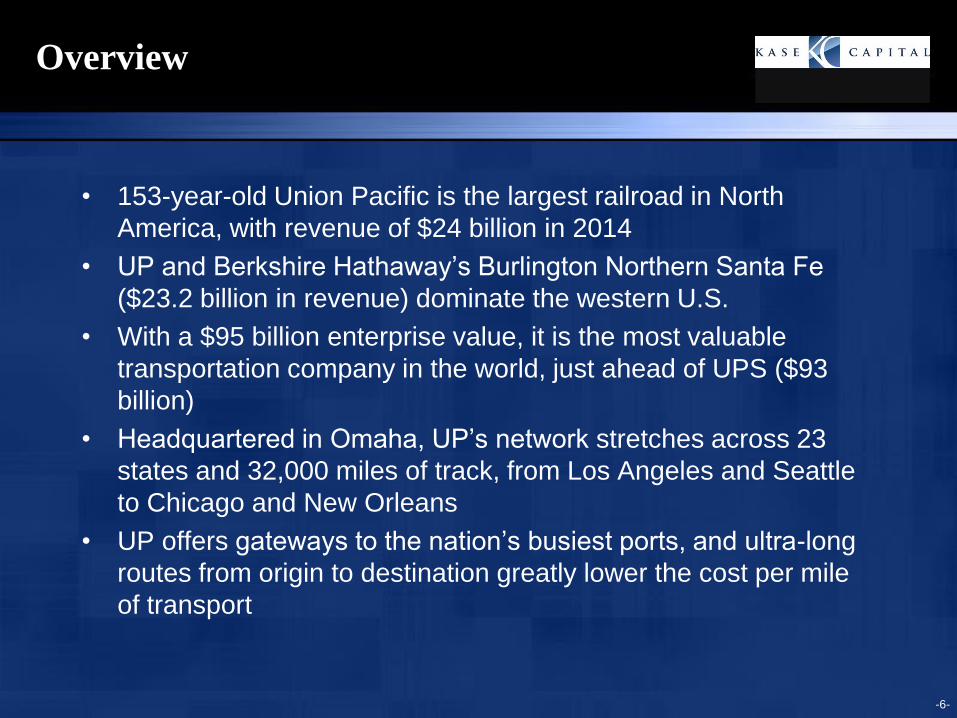

Overview

• 153-year-old Union Pacific is the largest railroad in North

America, with revenue of $24 billion in 2014

• UP and Berkshire Hathaway’s Burlington Northern Santa Fe

($23.2 billion in revenue) dominate the western U.S.

• With a $95 billion enterprise value, it is the most valuable

transportation company in the world, just ahead of UPS ($93

billion)

• Headquartered in Omaha, UP’s network stretches across 23

states and 32,000 miles of track, from Los Angeles and Seattle

to Chicago and New Orleans

• UP offers gateways to the nation’s busiest ports, and ultra-long

routes from origin to destination greatly lower the cost per mile

of transport

-7-

Union Pacific’s Network

-8-

Union Pacific’s Stock Has Soared Over the

Past Decade…

-9-

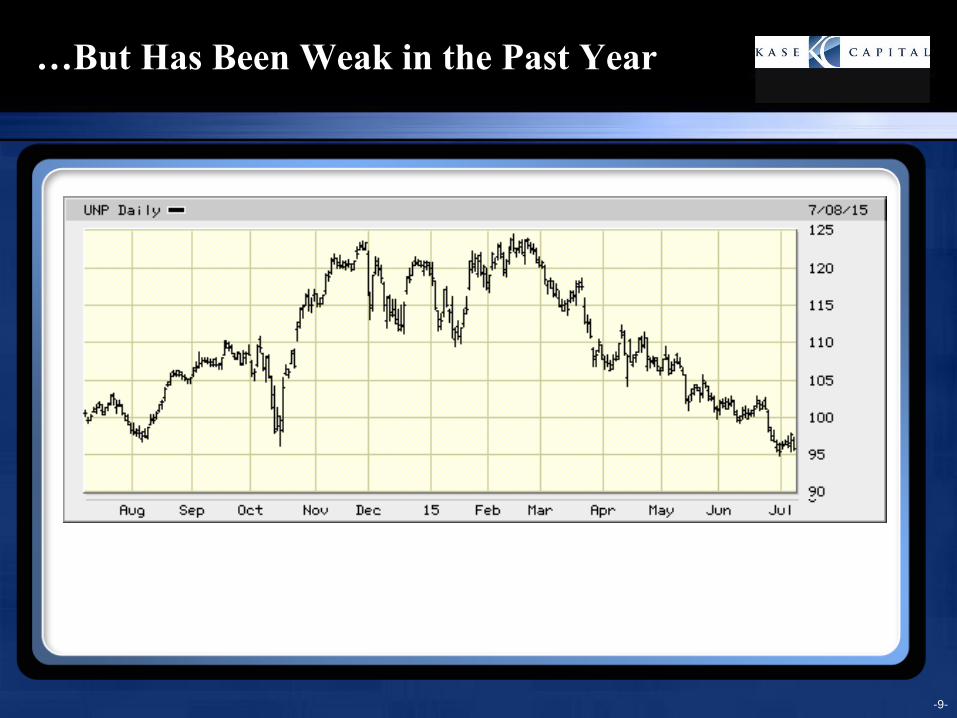

…But Has Been Weak in the Past Year

-10-

Union Pacific Is a Spectacular Business

• A duopoly with an extremely rational competitor

• There will no new competitors

• A ~5x cost advantage over trucking

– Trucks ship a ton of freight an average of 120 miles on a gallon of

diesel fuel; railroads can move the same cargo 600 miles on that

gallon

• Strong revenue growth

• Substantial pricing power, leading to rising margins over time

• Net margin: 22%

• Return on equity: 25%

-11-

Union Pacific’s Revenue Has Doubled in

the Past Decade

$0

$5

$10

$15

$20

$25

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

$B

-12-

Union Pacific’s Profit Margin and ROE

Have Soared as Well

0%

5%

10%

15%

20%

25%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Return on Equity %

Net Income Margin %

UP’s net margin of 21.9% rivals Apple (22.5%)

and exceeds Goldman Sachs (21.1%), Intel

(20.9%), Google (20.2%) and Pfizer (18.4%)

-13-

Valuation

• Stock price (7/9/15): $95.85

• Market cap: $84.2 billion

• EV: $94.9 billion

• P/E (trailing and 2015): 16.4x

• P/E (2016): 14.4%

• EV/EBITDA: 8.8x

• Dividend yield: 2.3%

-14-

Why Has the Stock Been Weak?

• Thanks to coal, shale oil, grain and autos, Union Pacific’s

volumes soared 7% in 2014, ~4-5x the 1.5% or so that’s normal

in a good economy

• Two of UP’s major growth engines, coal and shale oil, are

currently under pressure

• Labor strife at the ports in Los Angeles and Long Beach caused

a big drop in shipments of imports from Asia

• The sudden pullback in these businesses, following a big

buildup in 2014, has temporarily saddled Union Pacific with too

many people and too much equipment, so it has idled some

locomotives and furloughed 600 workers (1.3% of 47,200)

• Revenue is expected to fall ~3% in 2015 and EPS will only rise

~2%

-15-

Reasons for Optimism

• Railroads enjoy a big, and growing, cost advantage over trucks for

long-haul shipments, so the shift of cargoes from trucks to trains

will continue and be UP’s principal growth engine in the future

• The Long Beach and LA ports are returning to normal

• The logjams from the surge in business in 2014 are now easing

• The oil business (sand, drilling pipe and crude oil), even at its

peak in 2014, was only 4.5% of revenue

• Four major franchises — intermodal freight, chemicals,

automotive, and agricultural products — are all showing strong

gains

– More than a dozen big chemical companies are building tens of

billions of dollars in petrochemical plants along the Gulf Coast, where

UP has the best rail network

– Virtually all the world’s major automakers have announced or

completed major manufacturing hubs in Mexico, and UP transports

two out of three of the new cars that Mexico exports to the U.S.

-16-

Target Stock Price

• Revenue and EPS are expected to rise ~7% and ~14%,

respectively in 2016

• At 18-20x consensus analysts’ estimates of 2016 EPS of $6.72

results in a share price of $121-$134, 26-40% above today’s

levels

General Electric

-18-

Overview

• Founded in 1889, GE is the only one of the original 12

companies still in the Dow Jones Industrial Average

• The 17th largest business in the world by revenue in 2014, with

$148 billion

• GE is shedding most of GE Capital and its appliance business,

so revenue is expected to decline by ~15% to $125 billion in

2015

• Earnings are expected to decline from $1.51 in 2014 to $1.38 in

2015 (excluding one-time charges)

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

-19-

General Electric’s Revenue Is Flat

Over the Past Eight Years

$B

-20-

General Electric’s Profit Margin Has Been Flat

and ROE Has Declined Over Two Decades

0%

5%

10%

15%

20%

25%

30%Return on Equity %

Net Income Margin %

-21-

Not Surprisingly, General Electric’s

Stock Is Where It Was 17 Years Ago

-22-

General Electric’s Remaining

Businesses Are of Exceptional Quality

Note: Revenue estimates for GE Capital and Appliances & Lighting are for 2016 to reflect pending sales

2015 2015 Est.

Estimated Operating

Segment Revenue Margin

Power & Water $35.4 15.9%

Aviation $25.8 21.5%

Healthcare $18.3 17.2%

Oil & Gas $16.5 13.1%

Energy Management $9.7 5.2%

GE Capital $9.5 15.0%

Transportation $6.1 21.1%

Appliances & Lighting $1.5 5.5%

-23-

Valuation

• Stock price (7/9/15): $26.26

• Market cap: $261 billion

• P/E (2015 adjusted): 19.0x

• P/E (2016 adjusted): 16.6%

• Dividend yield: 3.5%

-24-

Why Is the Stock Interesting?

• GE is selling assets more rapidly than expected and getting

better-than-expected prices

• When GE is finished shedding assets next year, what remains

will be one of the premier global industrial businesses with high

margins, solid growth and strong backlogs

• The stock will likely command a premium multiple (P/E of 16-20)

• Analysts project earnings of ~$2.00 in 2018, but I believe

earnings will be $2.50, assuming:

– The Alstom deal goes through

– Power & Water margins rebound to 2009-13 levels (20%) by 2018

– Share repurchases average ~6% annually in 2016-18

• At 16-20x $2.50 results in a share price of $40-$50 in 2018, 54-

93% above today’s levels – and you get paid a 3.5% dividend

while you wait

-25-

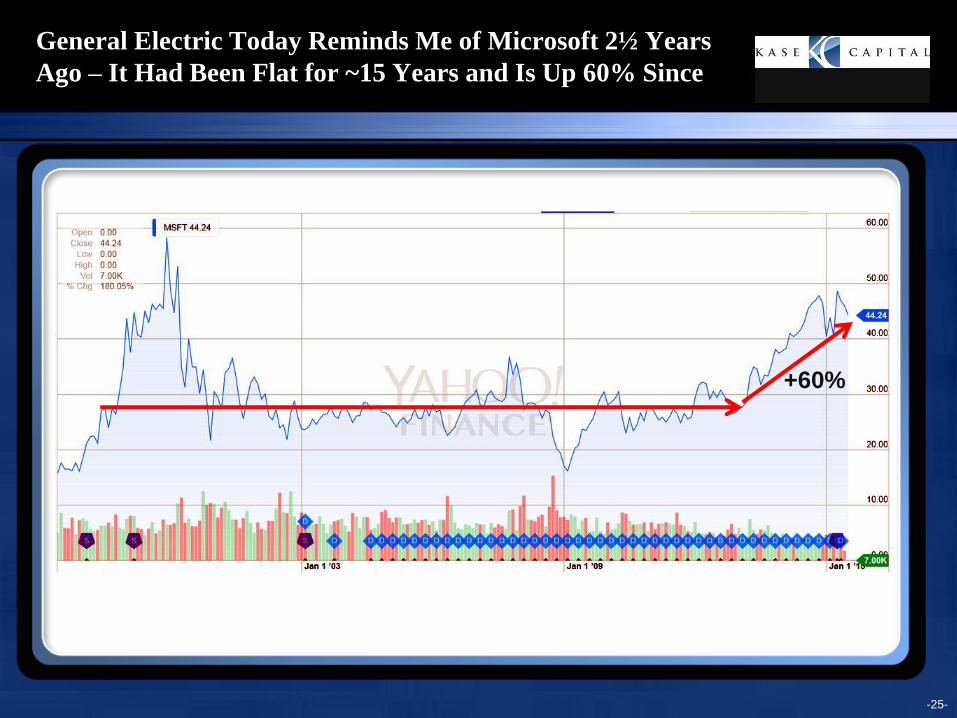

General Electric Today Reminds Me of Microsoft 2½ Years

Ago – It Had Been Flat for ~15 Years and Is Up 60% Since

+60%

-26-

General Electric Also Reminds Me of AIG ~3 Years

Ago When It Was In the Midst of Selling Off Assets

+100%

Top Related