Languages

Pages

Legal

Tieto Q4’09Sales down, profitability on the right track - shifting focusthe right track shifting focus to growth

10 February 201010 February 2010Helsinki, Finland

Hannu Syrjälä – President and CEO

eto

Cor

pora

tion

Hannu Syrjälä President and CEOSeppo Haapalainen – CFOReeta Kaukiainen – VP, Comms&IR

© 2

010

Tie

M k t d tMarkets and customers:IT markets stabilizing – markets bottomed out in 2009g• IT market relevant for Tieto down approximately 5% in 2009• Finance and telecom sectors bottomed out• Finance and telecom sectors bottomed out• Mixed development in other industry sectors continue• Modest growth expected in 2010

• Market for projects expected to pick up only in the second half 2010• Robust demand for

• Outsourcingg• New service models e.g. cloud computing

• New energy-efficient data centres under construction in Finland, Sweden and Russia to support future growthRussia to support future growth

• Recent customer wins: • Finland: Local Government Pension Institution, Metsäliitto Group, Metso, NSN, Tradeka

S d Bil i K k ll i N k M i i li S fi K K f li• Sweden: Bilprovningen, Kammarkollegiet, Nacka Municipality, Smurfit Kappa Kraftliner• International: China mobile, Lukoil

© 2010 Tieto Corporation2

Q4 financial highlights:Q4 financial highlights:Profitability improvement continues

• Sales down by 10% to EUR 441 million

600 8

Net sales EBIT %MEURmillion• 7.6% EBIT driven by successful

streamlining actions• All country segments profitable

500

600

7

8

• All country segments profitable• Strong net cash flow of EUR 71.7

million400

5

6

• EPS EUR 0.36

• Dividend proposal EUR 0.50 200

300

3

4

Dividend proposal EUR 0.50

1001

2

0Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

0

© 2010 Tieto Corporation3

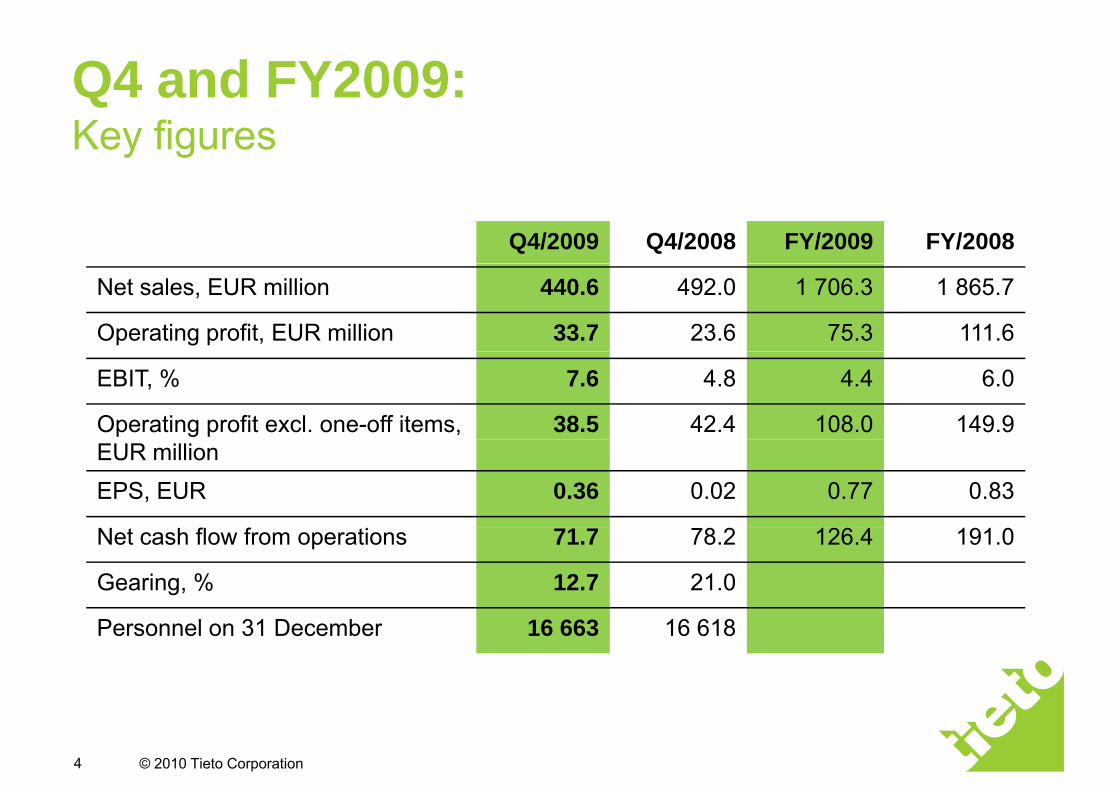

Q4 and FY2009:Q4 and FY2009: Key figures

Q4/2009 Q4/2008 FY/2009 FY/2008

Net sales, EUR million 440.6 492.0 1 706.3 1 865.7

Operating profit, EUR million 33.7 23.6 75.3 111.6

EBIT, % 7.6 4.8 4.4 6.0

Operating profit excl. one-off items, 38.5 42.4 108.0 149.9EUR millionEPS, EUR 0.36 0.02 0.77 0.83

Net cash flow from operations 71.7 78.2 126.4 191.0

Gearing, % 12.7 21.0

Personnel on 31 December 16 663 16 618

© 2010 Tieto Corporation4

Q4 and FY2009:Q4 and FY2009:Income statement

EUR millionQ4

2009Q4

2008Change

%FY

2009FY

2008Change

%

Net sales 440.6 492.0 -10 1 706.3 1 865.7 -9

Other operating income 4.7 2.4 96 17.5 10.8 62

Employee benefit expenses 243.3 278.8 -13 986.7 1 056.0 -7p y p

Depreciation and amortization 17.5 16.8 4 70.7 66.1 7

Other operating expenses 150.8 175.2 -14 591.1 642.8 -8

Operating profit (EBIT) 33 7 23 6 43 75 3 111 6 33Operating profit (EBIT) 33.7 23.6 43 75.3 111.6 -33

Interest and other financial income 2.1 3.7 -43 5.8 8.8 -34

Interest and other financial expenses -4.2 -4.0 5 -13.7 -16.8 -19

Net exchange losses/gains 0.6 -16.7 - 2.9 -21.2 -

Profit before taxes 32.2 6.6 388 70.3 82.4 -15

Income taxes -6.5 -4.8 35 -15.2 -21.9 -31Income taxes 6.5 4.8 35 15.2 21.9 31

Net profit for the period 25.7 1.8 1 328 55.1 60.5 -9

© 2010 Tieto Corporation5

Streamlining actions:Streamlining actions:Savings targets for 2009 achieved

Savings targets • EUR 70 million in 2009• EUR 100 million in 2010

Achievements* • Cost base down in line with the EUR 70 million target of which• approx. 50% from lower personnel costs

25% from business expenses• 25% from business expenses• 20% from less subcontracting

One-off costs • EUR 50.8 million in nine months• EUR 4.8 million in Q4

* Excluding non-recurring and exchange ratesg g g

© 2010 Tieto Corporation

FY2009 recap:FY2009 recap: Strong execution in an exceptionally tough environment

+• New operating model implemented

-• Growth ambitions hit by recessionNew operating model implemented

successfully• Renewed company brand and culture

positively acknowledged

Growth ambitions hit by recession • Sales down by 9% −

6% in local currenciesSi ifi t i i ll ipositively acknowledged

• Improved employee satisfaction• Savings target achieved

• Significant price pressure − especially in telecom

• Project services hit hard • Significant quality and efficiency

improvements• Offshore rate at 30%Offshore rate at 30%• Steady profitability improvement after Q1• Good cash-flow

Basis for growth established

© 2010 Tieto Corporation

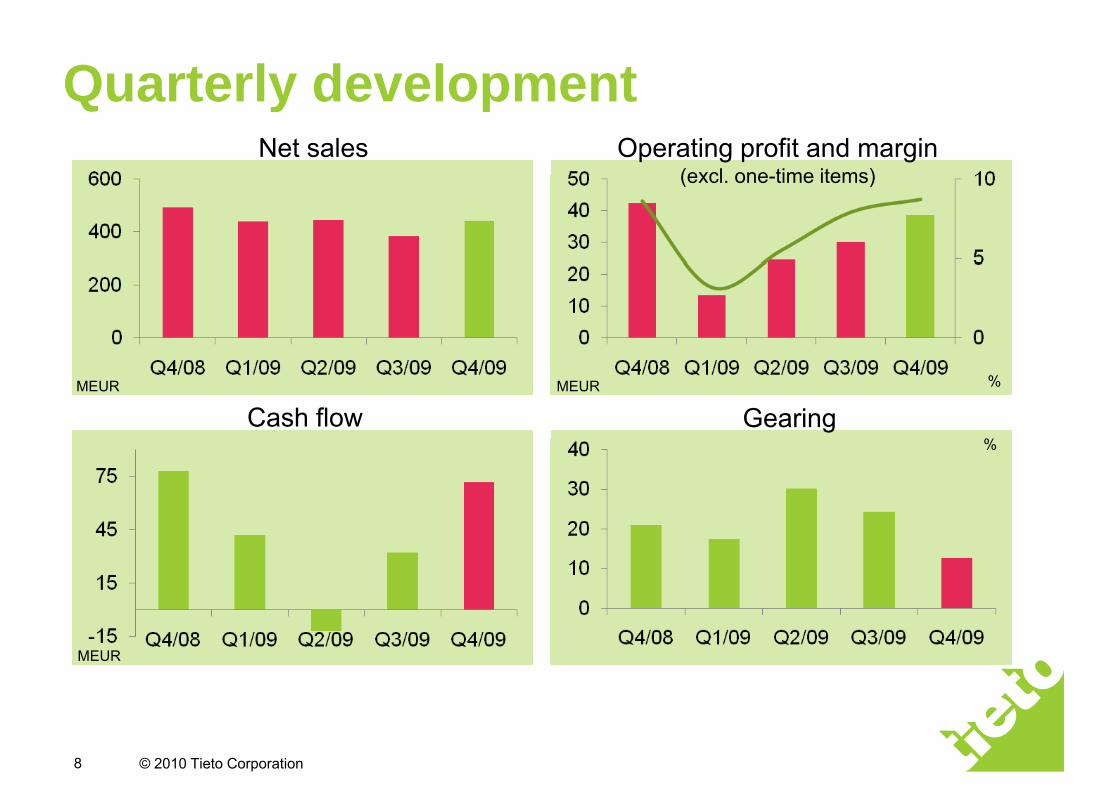

Quarterly developmentQuarterly developmentNet sales Operating profit and margin

(excl one time items)(excl. one-time items)

Cash flow GearingMEUR %

%

MEUR

%

MEUR

© 2010 Tieto Corporation8

Offshoring ratio at 30%:Offshoring ratio at 30%:India and China growing fast

6000 35 %

4000

5000

25 %

30 %

3000

4000

15 %

20 %

1000

2000

5 %

10 %

15 %

0

04 04 05 05 06 06 07 07 08 08 09 09

0 %

5 %

Q1 0 Q3 0 Q1 0 Q3 0 Q1 0 Q3 0 Q1 0 Q3 0 Q1 0 Q3 0 Q1 0 Q3 0

Czech and Poland Baltics, Russia and BelarusI di Chi M l i d I d i Off h f t t l %

© 2010 Tieto Corporation9

India, China, Malaysia and Indonesia Offshore of total, %

Country sales by quarter

600

y y q

152141 143 139

500

600

141 119 116 125

141 143130

139

300

400

239 227 230 199 233

119 6103

100

200239 227 230 199 233

0

100

eto

Cor

pora

tion Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

Finland Sweden International

© 2

009

Tie

Note: Internal sales included

Finland• Q4 sales down by 3%• Strong outsourcing market e.g. NSN and Metso deals• Continuously strong profitability• Continuously strong profitability• Healthy order backlog

Sales, MEUR EBIT, %Q4/2009 Q4/2008 FY/2009 FY/2008

Sales, MEUR 233 239 888 900

239 227 230 199 233

Sales, MEUR 233 239 888 900

EBIT, MEUR 34.0 28.3 110.3 114.2

EBIT, % 14.6 11.9 12.4 12.7

Employees 5 758 6 021239 227 230 199 233

Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

Employees 5 758 6 021

© 2010 Tieto Corporation11

SwedenQ %• Q4 sales down by 11%

• Half of the drop caused by telecom

• Operating profit lower than year agop g p y g• Strong execution of streamlining measures lead to significant profitability

improvement during the second half of 2009• Improved sales pipeline• Improved sales pipeline

Q4/2009 Q4/2008 FY/2009 FY/2008

Sales, MEUR 125 141 463 548

141 119 116 103 125

Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

EBIT, MEUR 7.9 17.6 -2.7 48.7

EBIT, % 6.3 12.5 -0.6 8.9

Employees 3 102 3 291

Sales, MEUR EBIT, %

© 2010 Tieto Corporation12

International• Q4 sales down by 9% • Telecom in Denmark and Germany, finance in the UK

continued as the most challenging areascontinued as the most challenging areas• Profitability improved due to restructuring• Increased offshore capabilities

• Resources doubled in China• Over 1 000 employees in India

Q4/2009 Q4/2008 FY/2009 FY/2008

Sales MEUR 139 152 553 572152 141 143 130 139

Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

Sales, MEUR 139 152 553 572

EBIT, MEUR 2.7 -0.9 -7.1 3.8

EBIT, % 2.0 -0.6 -1.3 0.7

E l 7 803 7 306

Net sales, MEUR EBIT, %

Employees 7 803 7 306

© 2010 Tieto Corporation13

Customers in 2009:Customers in 2009:Top 10 accounted 36% of sales

Share of Group sales b c stomer sector

Apoteket Healthcare & Welfare/ RetailEricsson Telecom by customer sectorEricsson TelecomIF Insurance FinanceKesko Retail

45%34%The National Board

of Taxes (FI)Government

N ki T l21%

Nokia TelecomNordea FinanceOP-Pohjola Group Finance

Telecom Finance Industry sectors

OP Pohjola Group FinanceTeliaSonera TelecomVarma Finance

Customers are listed in alphabethical order

© 2010 Tieto Corporation14

Customers are listed in alphabethical order.

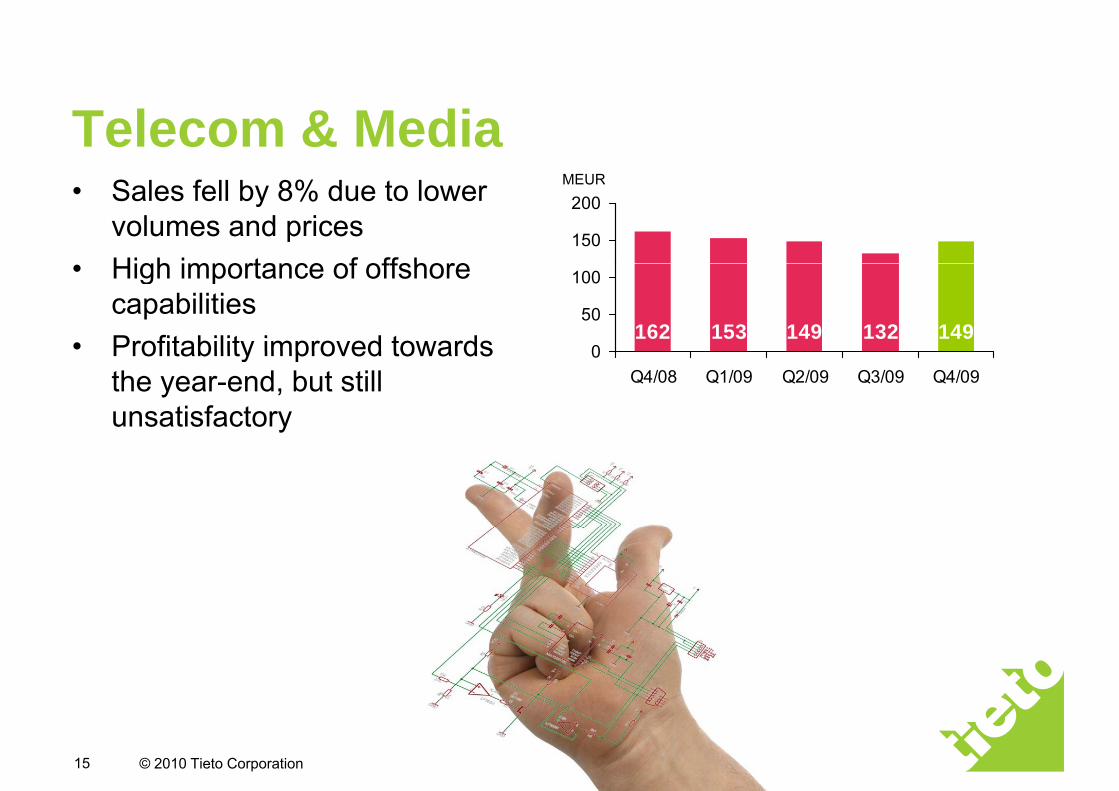

Telecom & MediaMEUR• Sales fell by 8% due to lower

volumes and prices High importance of offshore

150

200MEUR

• High importance of offshore capabilities

• Profitability improved towards 162 153 149 132 1490

50

100

Profitability improved towards the year-end, but still unsatisfactory

0Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

© 2010 Tieto Corporation15

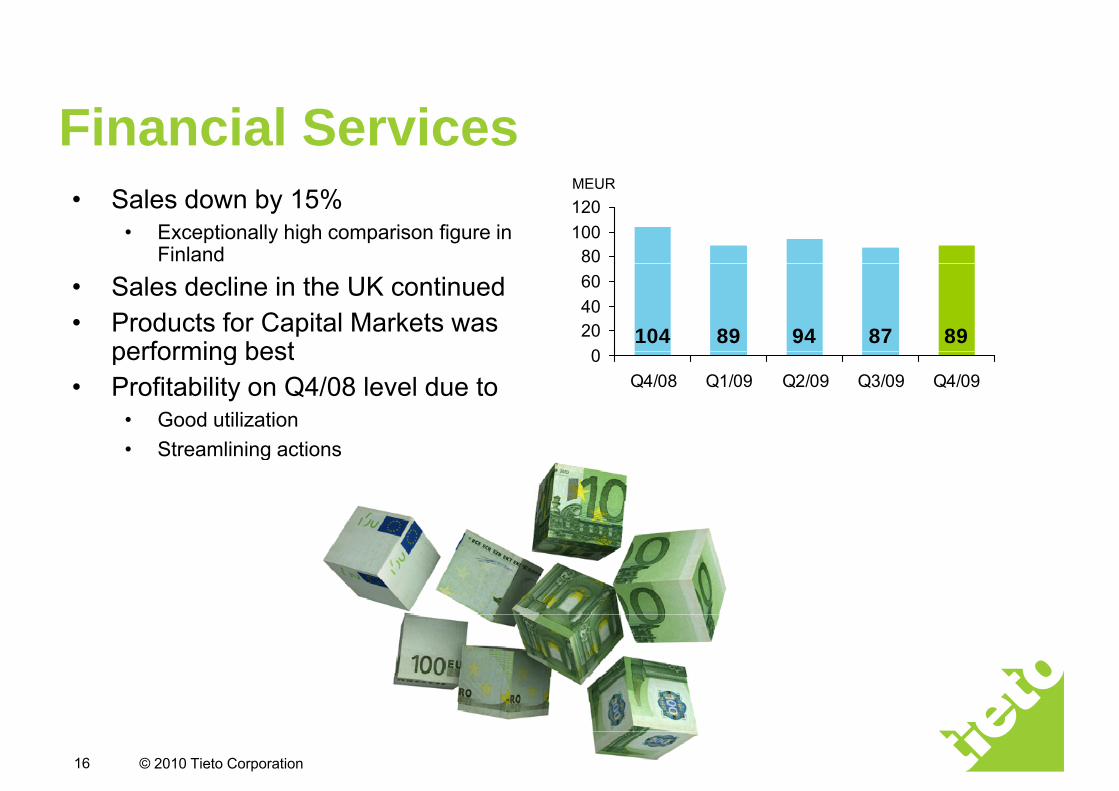

Financial Services• Sales down by 15%

• Exceptionally high comparison figure in Finland 80

100120MEUR

• Sales decline in the UK continued• Products for Capital Markets was

performing best 104 89 94 87 890

204060

performing best• Profitability on Q4/08 level due to

• Good utilization

0Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

• Streamlining actions

© 2010 Tieto Corporation16

Industry sectors*• Sales down by 10%• Manufacturing was the weakest sector

St f i th bli t200

250

MEUR

• Strong performance in the public sector• Profitability at a healthy level

226 197 201 165 20350

100

150

226 197 201 165 2030

Q4/08 Q1/09 Q2/09 Q3/09 Q4/09

* A t ti f t h lth d lf

© 2010 Tieto Corporation17

* Automotive, energy, forest, healthcare and welfare,manufacturing, public, retail and logistics

Actions for 2010Actions for 20101. Manage profitability

• ”Leaning” the organization and cost base• Continued focus on Sweden and International

2. Drive quality and sales excellence• Stronger sales force• Best in class customer care

3. Increase efficiency and productivity• Offshore target 35% in 2010

4. Transform Telecom R&D• Ramp-up Asia• Transform competences from R&D to IT

5. Investments in new offerings• E.g. cloud computing, financial value chain and

unified communications 6. Execute portfolio adjustments

© 2010 Tieto Corporation

Outlook for 2010• Tieto anticipates that the IT markets have now bottomed out• In 2010, Tieto expects its net sales to develop in line with the IT

i k t l t t thservices market relevant to the company• Tieto expects its operating profit to be higher than in 2009

© 2010 Tieto Corporation19

Questions and answersQuestions and answerset

o C

orpo

ratio

n©

201

0 Ti

e

20

Top Related