Languages

Pages

Legal

The World Bank

SuperintendenciaBancaria

Banco de la Republica Colombia

Asobancaria

Building a Technology Framework to Meet the Basel II Requirements

Risk Management Workshop COLOMBIA :From Theory to Implementation

Cartagena, ColombiaFebruary 16, 2004

Presented byDavid M. Rowe, Ph.D.

Executive Vice President for Risk ManagementSunGard Trading and Risk Systems

Agenda

1. Introduction – A Brief History of the Basel Accord

2. Data Issues and Technology Challenges

3. Support for Broader Trends in Risk Management

4. Solution Components to Manage Credit Risk Under Basel II

5. Importance of Communication

Basel Capital Accord – Brief History

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1935 1945 1955 1965 1975 1985 1995

Tota

l E

qu

ity

Cap

ital

to

To

tal A

sset

sU.S. Bank Capital Ratios – 1935 - 1988

Depression thru WWII

Post-War Recovery thru early 1960s

Mid-60s thru Mid-70’s

Mid-70s thru Late-80’s

Basel Capital Accord – Brief History

Basel 1

Proposed: 1986Effective: 1988

CreditRisk

Basel Capital Accord – Brief History

Basel I

1986 – Proposed minimum regulatory capital requirements for banks.

1988 – Capital requirements came into effect with minimum capital rising to 8% of risk adjusted assets by the end of 1992.

The capital calculation was intended to distinguish among assets by risk class, but did so in only the crudest fashion.

Overview of risk weights

The Basel I Approach

Claim

Sovereigns

Assessment

Corporates

Comm. Banks

OECD Non-OECD

0% 100%

20%

20%

100%

100%

OECD Non-OECD All

50%

Multi-National Development Banks

All

Secured ResidentialMortgages

Required data could largely be derived from financial reporting systems.

Basel Capital Accord – Brief History

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1935 1945 1955 1965 1975 1985 1995

Tota

l E

qu

ity

Cap

ital

to

To

tal A

sset

sBank Capital Ratios – 1935 - 1988

Depression thru WWII

Post-War Recovery thru early 1960s

Mid-60s thru Mid-70’s

Mid-70s thru Late-80’s

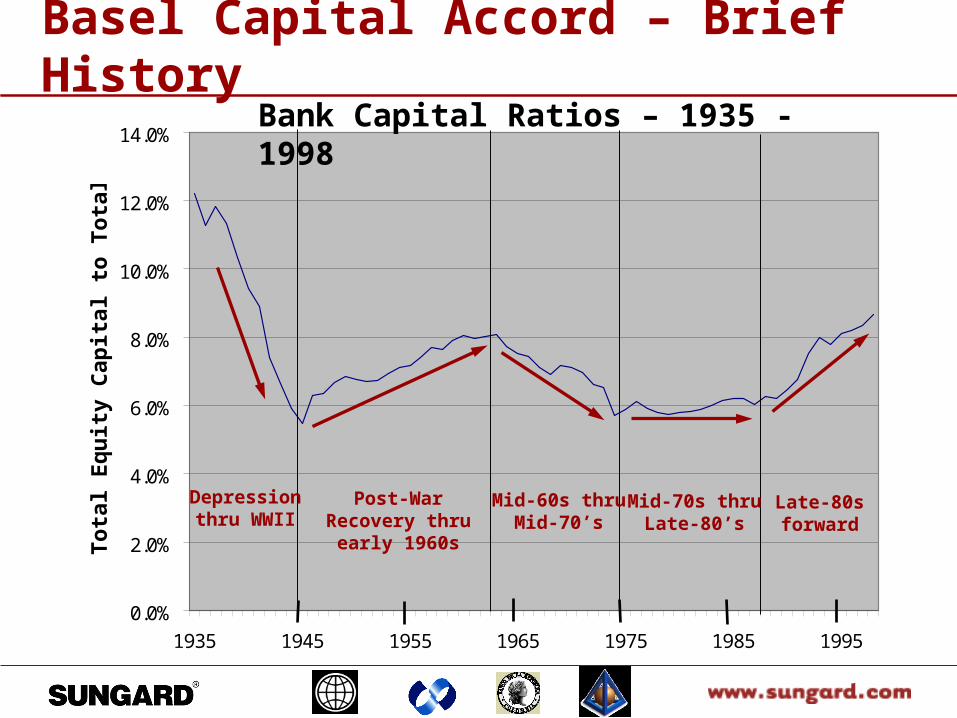

Basel Capital Accord – Brief History

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1935 1945 1955 1965 1975 1985 1995

Tota

l E

qu

ity

Cap

ital

to

To

tal A

sset

sBank Capital Ratios – 1935 - 1998

Depression thru WWII

Post-War Recovery thru early 1960s

Mid-60s thru Mid-70’s

Mid-70s thru Late-80’s

Late-80s forward

Basel Capital Accord – Brief History

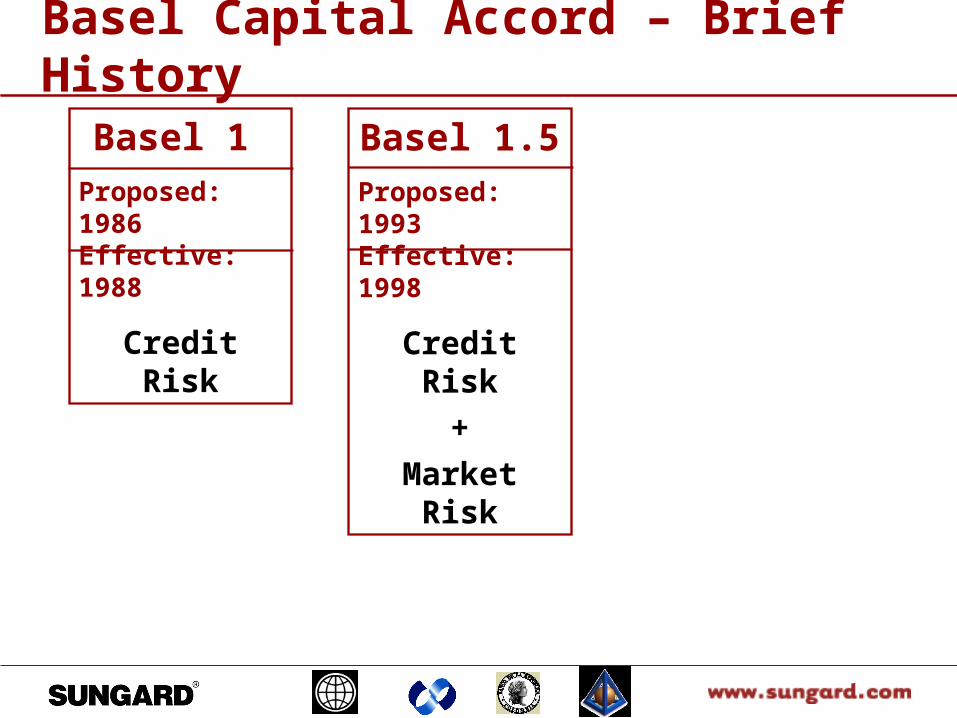

Basel 1.5

Proposed: 1993Effective: 1998

CreditRisk

+

MarketRisk

Basel 1

Proposed: 1986Effective: 1988

CreditRisk

Basel Capital Accord – Brief History

April, 1993 – Initial “prescriptive” proposal.

April, 1995 – Proposed allowing use of internal market risk models for calculation of regulatory capital (subject to supervisory review and approval.)

Jan 1, 1998 - Market risk amendment took effect with internal VaR models as a major source of risk estimates.

Basel I

Market Risk Amendment

Basel Capital Accord – Brief History

Basel 1.5

Proposed: 1993Effective: 1998

CreditRisk

+

MarketRisk

Basel 1

Proposed: 1986Effective: 1988

CreditRisk

Basel 2

Proposed: 1999Effective: 2007

CreditRisk

(Enhanced)

+

MarketRisk

(No change)

+

Op Risk(New)

Key sources of required work for affected banks.

Agenda

1. Introduction – A Brief History of the Basel Accord

2. Data Issues and Technology Challenges

3. Support for Broader Trends in Risk Management

4. Solution Components to Manage Credit Risk Under Basel II

5. Importance of Communication

By Country US JP AU JPBy Industry Finan Steel Chem

By Corporate Family Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Internal Region ProductLoans

EMEA Trade CreditDerivative TradingLoans

Asia Trade CreditDerivative TradingLoans

Americas Trade CreditDerivative Trading

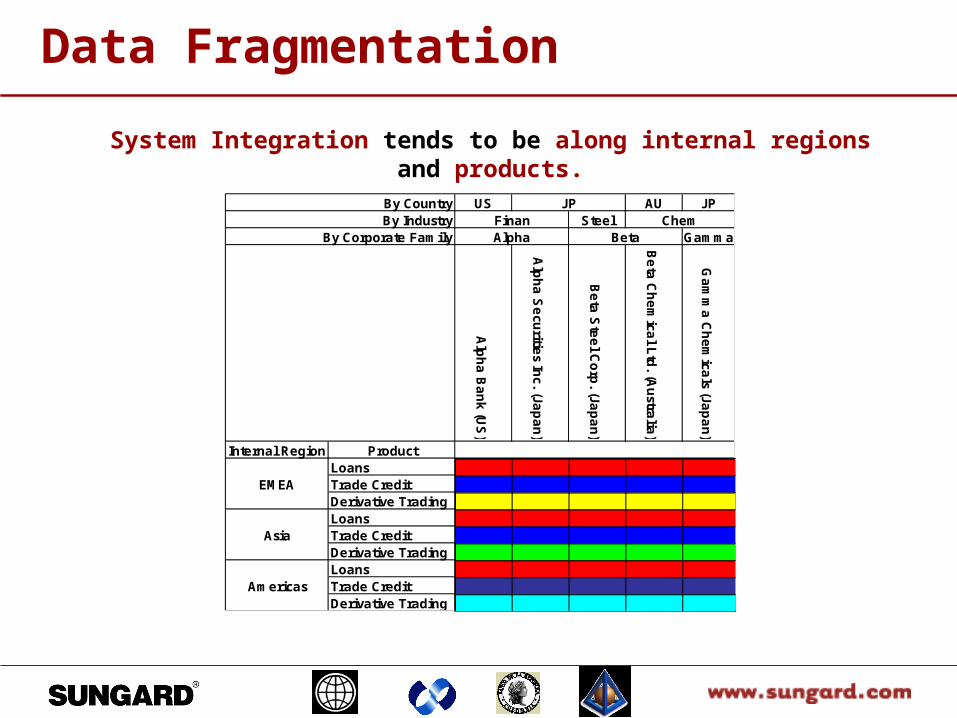

Data Fragmentation

System Integration tends to be along internal regions and products.

By Country US JP AU JPBy Industry Finan Steel Chem

By Corporate Family Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Internal Region ProductLoans

EMEA Trade CreditDerivative TradingLoans

Asia Trade CreditDerivative TradingLoans

Americas Trade CreditDerivative Trading

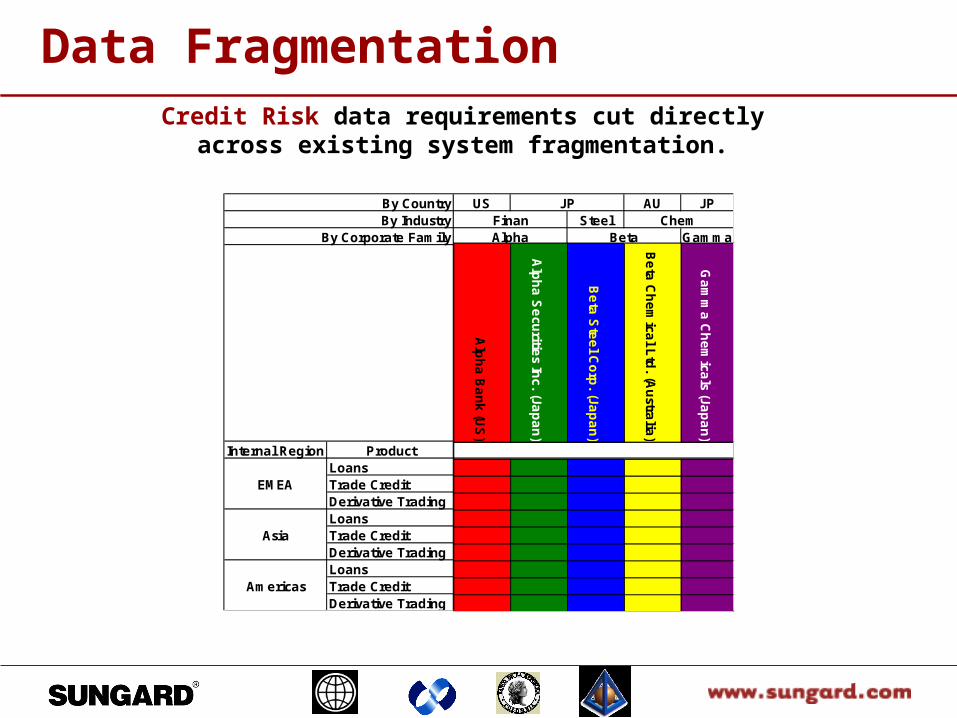

Data Fragmentation Credit Risk data requirements cut directly across

existing system fragmentation.

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

By Country US JP AU JPBy Industry Finan Steel Chem

By Corporate Family Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Internal Region ProductLoans

EMEA Trade CreditDerivative TradingLoans

Asia Trade CreditDerivative TradingLoans

Americas Trade CreditDerivative Trading

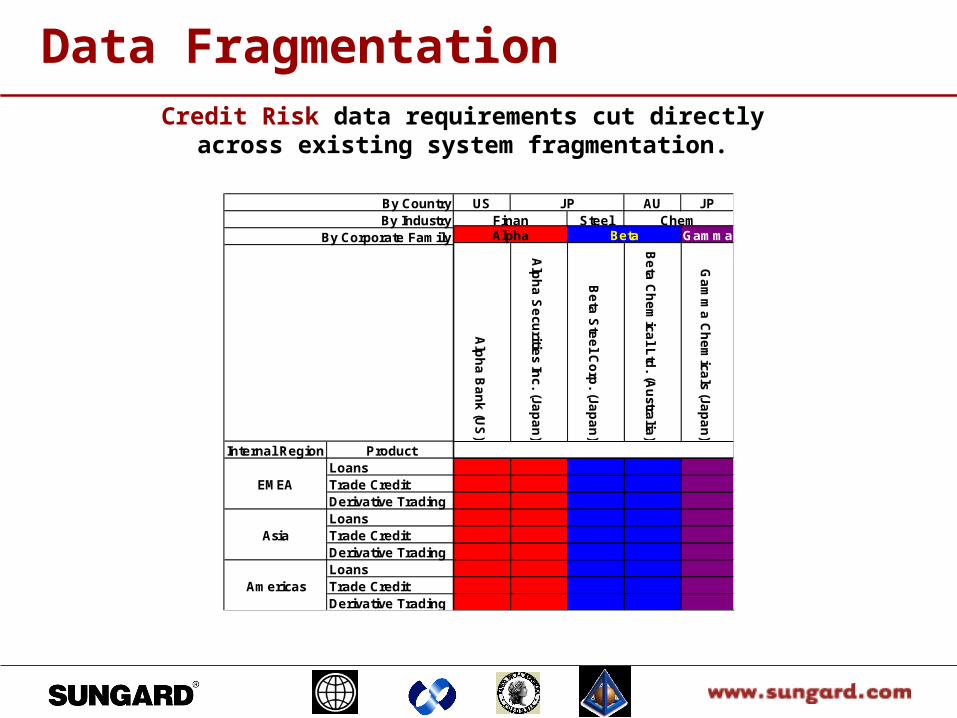

Data Fragmentation Credit Risk data requirements cut directly across

existing system fragmentation.

Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

By Country US JP AU JPBy Industry Finan Steel Chem

By Corporate Family Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Internal Region ProductLoans

EMEA Trade CreditDerivative TradingLoans

Asia Trade CreditDerivative TradingLoans

Americas Trade CreditDerivative Trading

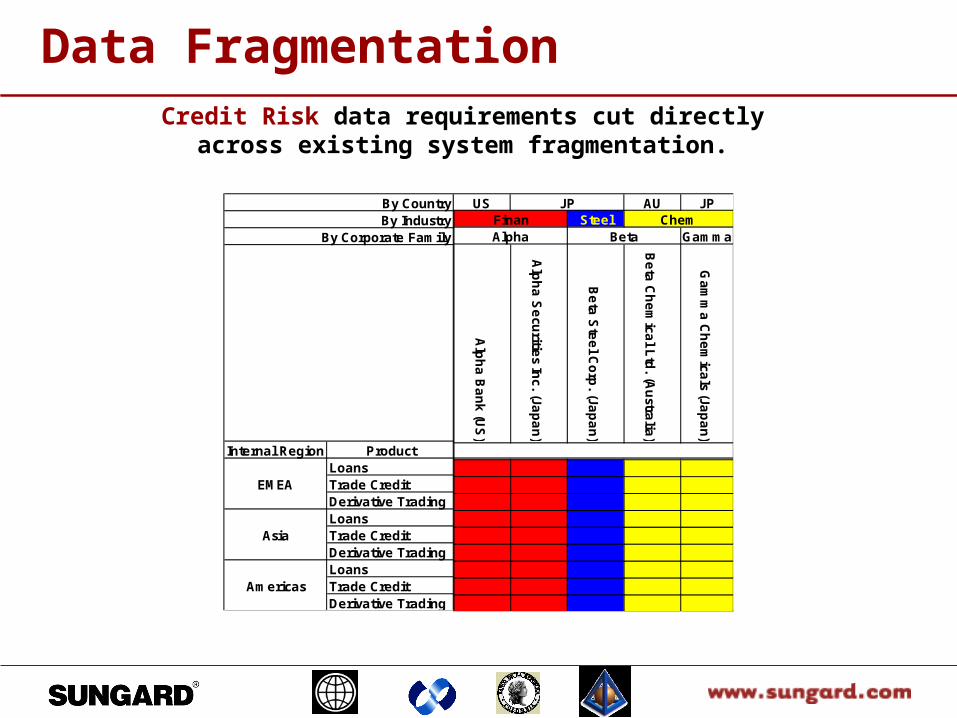

Data Fragmentation Credit Risk data requirements cut directly across

existing system fragmentation.

Finan Steel ChemAlpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

By Country US JP AU JPBy Industry Finan Steel Chem

By Corporate Family Alpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Internal Region ProductLoans

EMEA Trade CreditDerivative TradingLoans

Asia Trade CreditDerivative TradingLoans

Americas Trade CreditDerivative Trading

Data Fragmentation Credit Risk data requirements cut directly across

existing system fragmentation.

US JP AU JPFinan Steel ChemAlpha Beta Gamma

Alp

ha

Ba

nk (U

S)

Alp

ha

Se

curitie

s Inc. (Ja

pa

n)

Be

ta S

tee

l Co

rp. (Ja

pa

n)

Be

ta C

he

mica

l Ltd

. (Au

stralia

)

Ga

mm

a C

he

mica

ls (Jap

an

)

Overview of risk weights

Credit Risk - Standardised Approach

Claim

Sovereigns

Assessment

Option 1

Option 2

Corporates

Banks

AAA to AA-

A+ to A-BBB+

to BBB-BB+ to B- Below B- Unrated

0% 20% 50% 100% 150% 100%

20%

20%

20%

50%50%

50% 100%

100%50%

100%

100%

150%

150%

150%

100%

100%

50%

AAA to AA-

A+ to A-BBB+to BB-

Below BB- Unrated

Required data must come from risk systems.

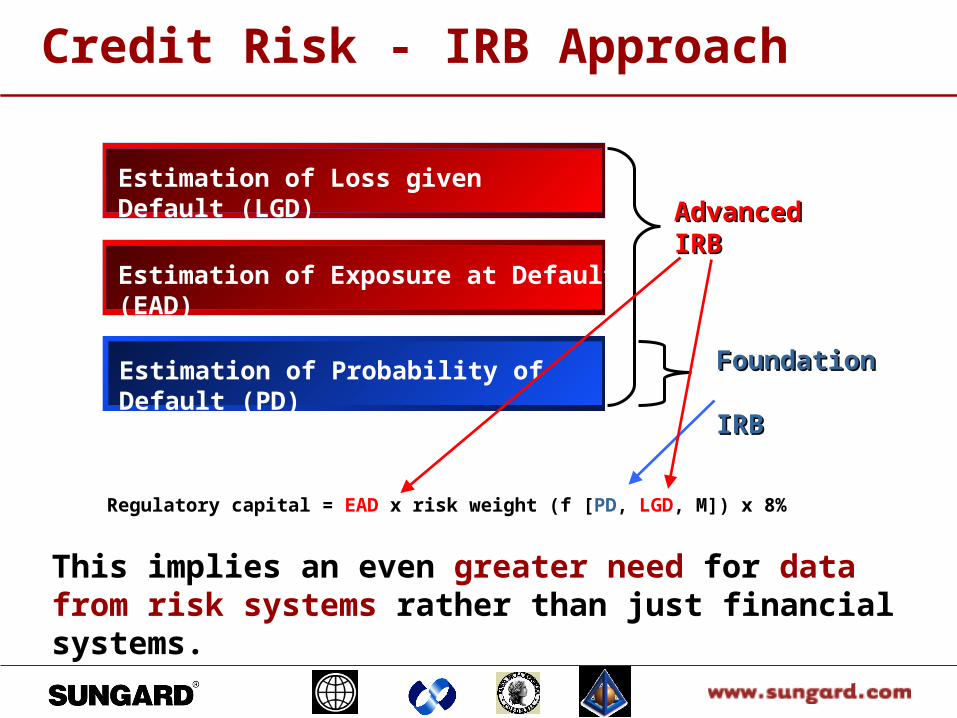

Credit Risk - IRB Approach

Regulatory capital = EAD x risk weight (f [PD, LGD, M]) x 8%

This implies an even greater need for data from risk systems rather than just financial systems.

Regulatory capital = EAD x risk weight (f [PD, LGD, M]) x 8%

Estimation of Probability of Default (PD) FoundatioFoundation n IRBIRB

Estimation of Exposure at Default (EAD)

Estimation of Loss given Default (LGD)Advanced Advanced IRBIRB

Regulatory capital = EAD x risk weight (f [PD, LGD, M]) x 8%

The First Challenge: Data Integration

Consolidating exposure across products, regions and systems (by obligor or by risk characteristics.)

Maintaining clean and consistent legal entity and facilities definition data.

Integrating collateral, guarantees and other credit enhancement data with items 1 and 2.

Collection and maintenance of external historic data (market data, industry defaults, etc.)

Providing audit trails and reconciliation to source systems.

Archive facilities to refine analysis and validate results. Proper data security to limit unauthorized access.

The Second Challenge: Analytics

Implementation of multiple sophisticated credit ratings models.– Scoring or Merton-style models for PD.– Behavioral models for EAD.– Structural and external conditions models for LGD.

Advanced economic capital allocation framework (Pillar II.)

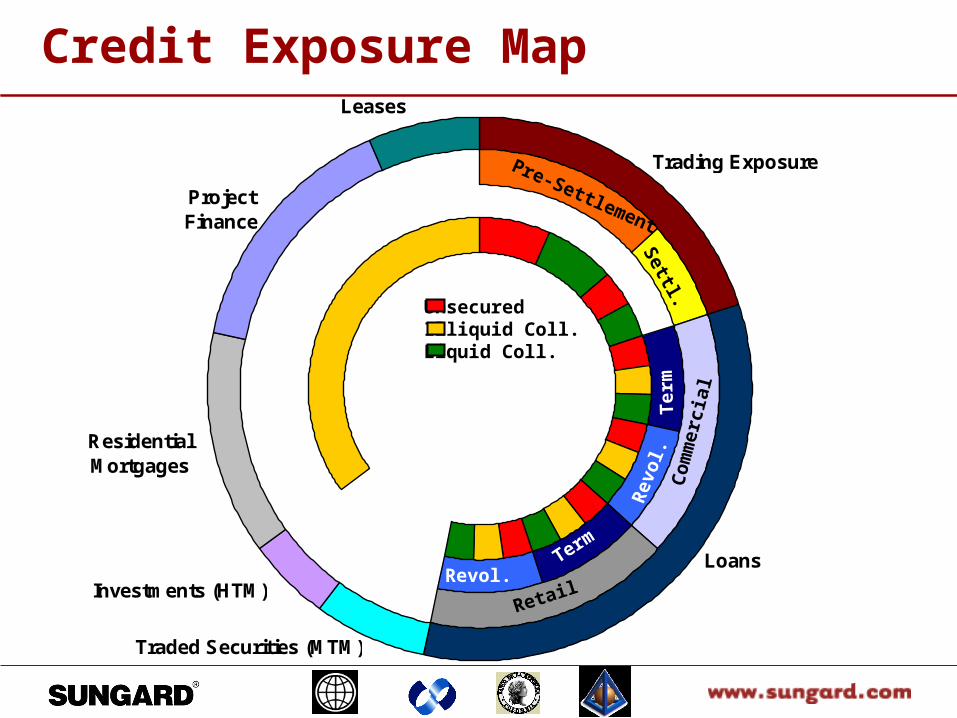

Credit Exposure Map

Trading Exposure

Loans

Investments (HTM)

Traded Securities (MTM)

Residential Mortgages

Leases

Project Finance

Retail

Co

mm

erci

al

Pre-Settlement

Settl.

Ter

m

Term

Revol.

Rev

ol.

UnsecuredIlliquid Coll.Liquid Coll.

Additional Information and Analytics

Mkt Data

Vols &Correl

Static Data

DefaultAnalytics

ExposureAnalytics

LGDAnalytics

Legal &Netting

Guarantees,

Cr Derivatives

and Other

Credit Risk

Mitigants

Credit Ratings

Credit Exposure and Supporting Data

Trading Exposure

Loans

Investments (HTM)

Traded Securities (MTM)

Residential Mortgages

Leases

Project Finance

Retail

Co

mm

erci

al

Pre-Settlement

Settl.

Ter

m

Term

Revol.

Rev

ol.

Mkt Data

Vols &Correl.

Static Data

DefaultAnalytics

ExposureAnalytics

LGDAnalytics

Legal &Netting

GuaranteesCredit Ratings

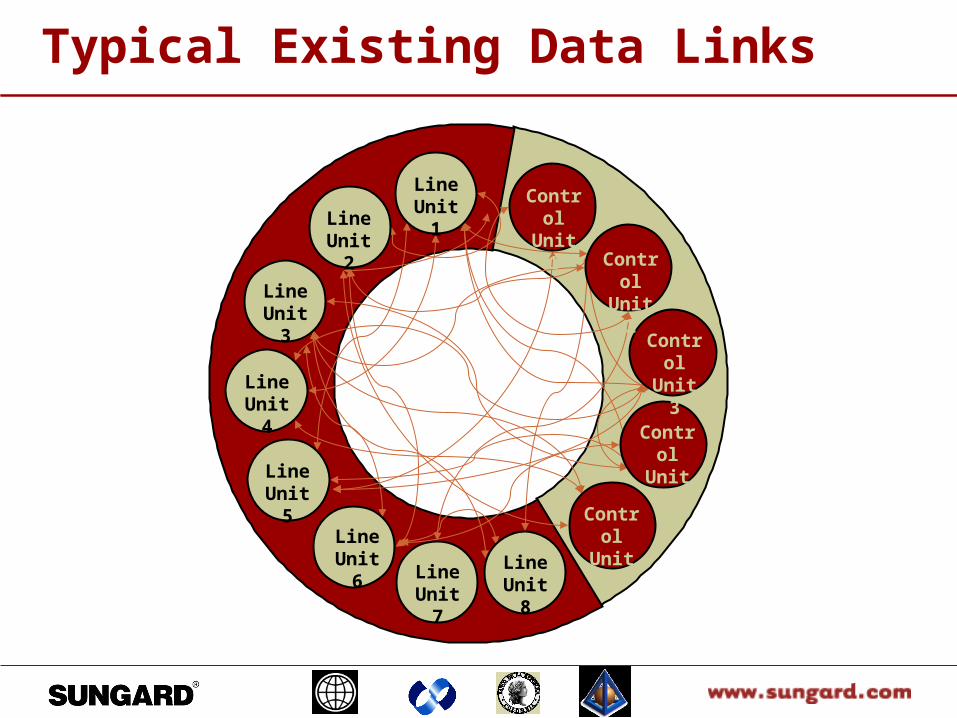

Typical Existing Data Links

LineUnit 1

LineUnit 5

LineUnit 6

LineUnit 7

LineUnit 8

LineUnit 2

LineUnit 3

LineUnit 4

ControlUnit 4

ControlUnit 3

ControlUnit 2

ControlUnit 1

ControlUnit 5

Ideal Data Linkage Configuration

LineUnit 1

LineUnit 5

LineUnit 6

LineUnit 7

LineUnit 8

LineUnit 2

LineUnit 3

LineUnit 4

ControlUnit 4

ControlUnit 3

ControlUnit 2

ControlUnit 1

ControlUnit 5

• Content translation

XML Protocols FpML, NTM...

MiddlewareMQSeries, MINT...

• Bridging operating systems & network protocols

• Delivery and routing

Semantic Adapters

• Central repository for portfolio data and analytics

Practical Data Linkage Configuration

LineUnit 1

LineUnit 5

LineUnit 6

LineUnit 7

LineUnit 8

LineUnit 2

LineUnit 3

LineUnit 4

ControlUnit 4

ControlUnit 3

ControlUnit 2

ControlUnit 1

ControlUnit 5

• Content translation

• Central repository for portfolio data and analytics

• Bridging operating systems & network protocols

• Delivery and routing

Middleware

Data Mapping & Consolidation

Software

Agenda

1. Introduction – A Brief History of the Basel Accord

2. Data Issues and Technology Challenges

3. Support for Broader Trends in Risk Management

4. Solution Components to Manage Credit Risk Under Basel II

5. Importance of Communication

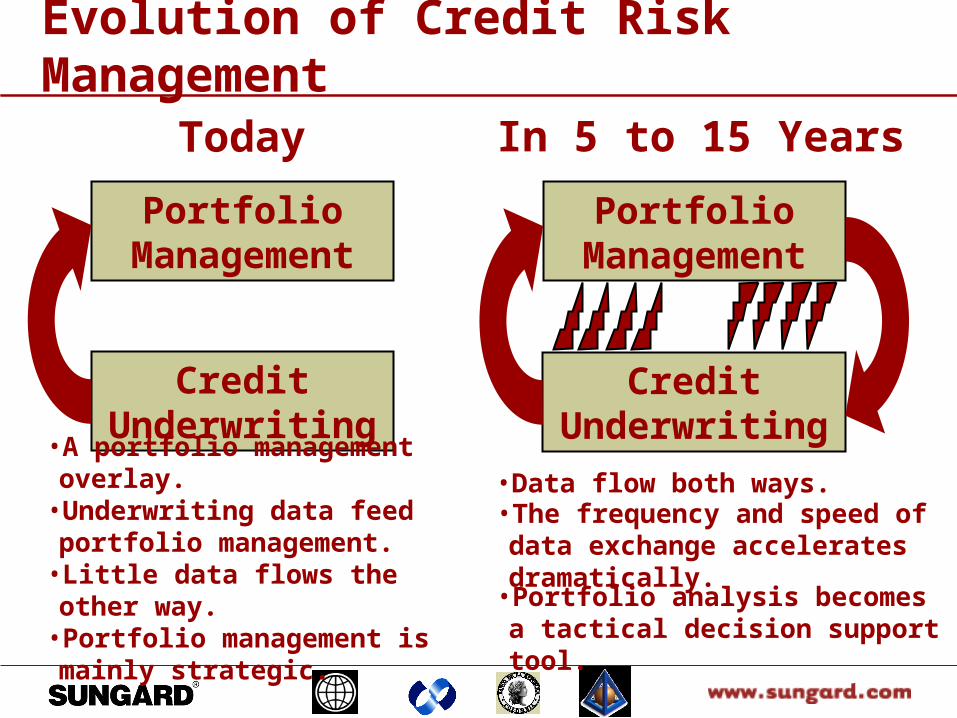

Evolution of Credit Risk Management

Credit Underwriting

1985 Portfolio Management

Credit Underwriting

Today

•Credit risk management was dominated by careful underwriting.

•The watchword tended to be “We only make good loans.”

•A portfolio management overlay.•Underwriting data feed portfolio management.

•Few data flow the other way.•Portfolio management is mainly strategic.

Evolution of Credit Risk Management

Portfolio Management

Credit Underwriting

Today

•A portfolio management overlay.•Underwriting data feed portfolio management.

•Little data flows the other way.•Portfolio management is mainly strategic.

In 5 to 15 Years

Portfolio Management

Credit Underwriting

•Data flow both ways.•The frequency and speed of data exchange accelerates dramatically.

•Portfolio analysis becomes a tactical decision support tool.

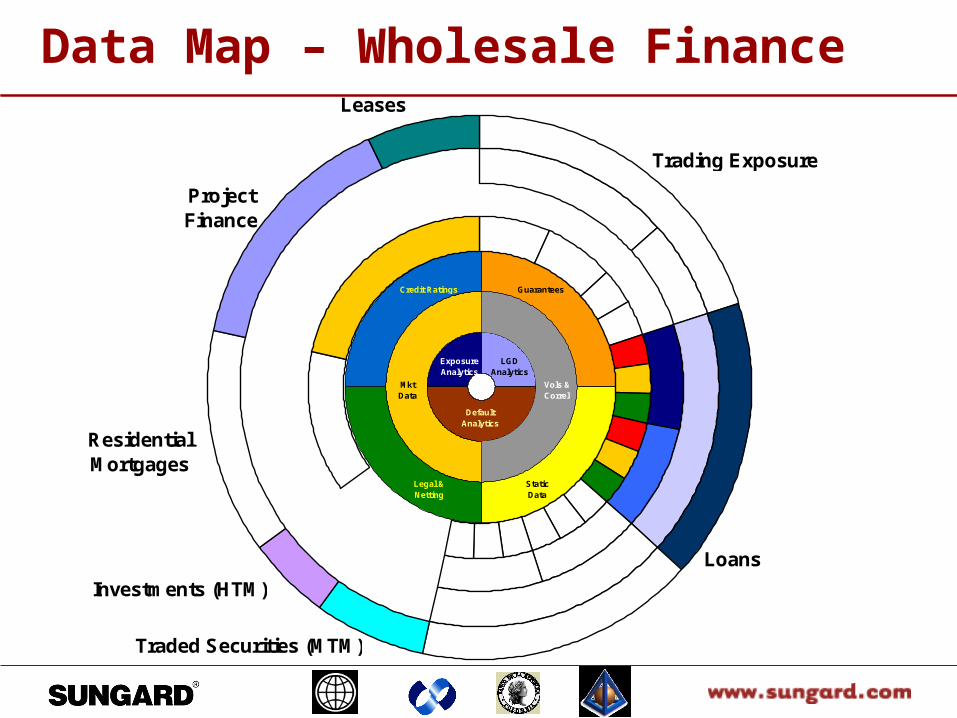

Data Map – Wholesale Finance

Retail

Co

mm

erci

al

Pre-Settlement

Settl.

Ter

m

Term

Revol.

Rev

ol.

Mkt Data

Vols &Correl.

Static Data

DefaultAnalytics

ExposureAnalytics

LGDAnalytics

Legal &Netting

GuaranteesCredit Ratings

Trading Exposure

Loans

Investments (HTM)

Traded Securities (MTM)

Residential Mortgages

Leases

Project Finance

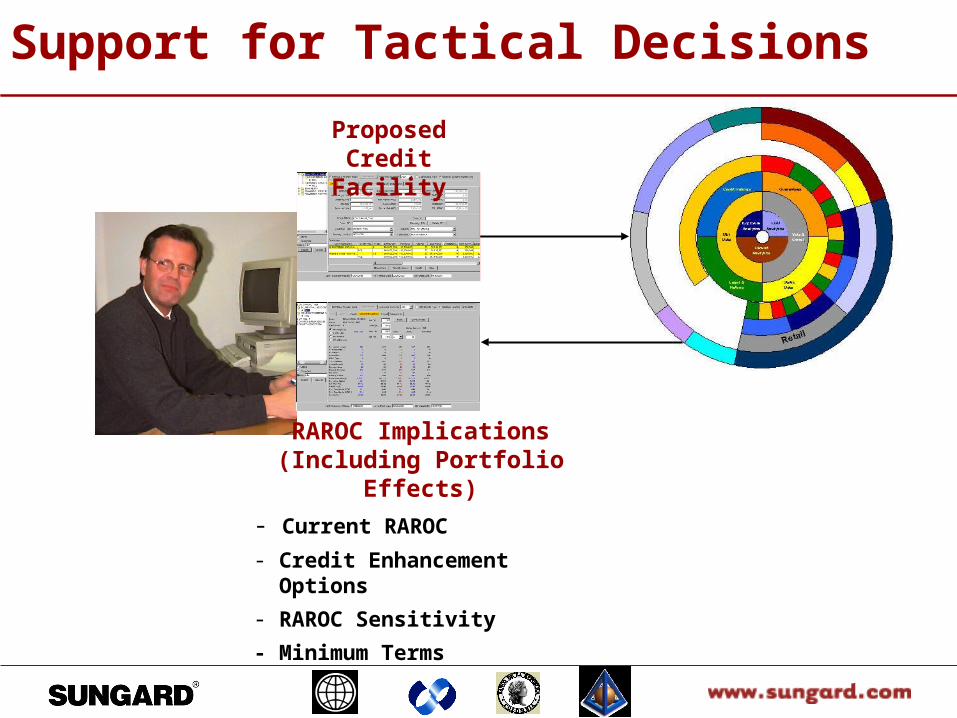

Support for Tactical Decisions

Proposed Credit Facility

RAROC Implications(Including Portfolio Effects)

- Current RAROC

- Credit Enhancement Options

- RAROC Sensitivity

- Minimum Terms

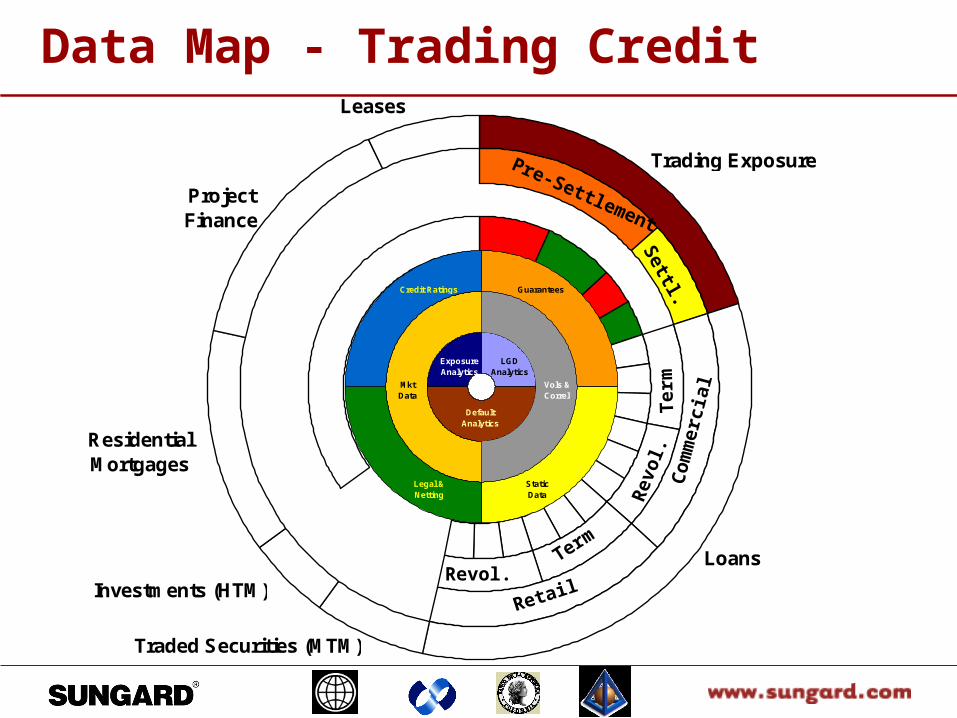

Trading Exposure

Loans

Investments (HTM)

Traded Securities (MTM)

Residential Mortgages

Leases

Project Finance

Data Map - Trading Credit

Mkt Data

Vols &Correl.

Static Data

DefaultAnalytics

ExposureAnalytics

LGDAnalytics

Legal &Netting

GuaranteesCredit Ratings

Retail

Co

mm

erci

al

Pre-Settlement

Settl.

Ter

m

Term

Revol.

Rev

ol.

Simulation-Based Trading Credit Exp.

Limit Query

Trading Systems

Trade Entry

Portfolio Trade Data

Fast AnalyticExposure Calculator

Before & After Exposure Profiles and Limits

Marginal Credit Loss and Credit Capital Charges

Real-Time Process

Credit Risk Server

Summary Trade Data

Middleware & XML Messages

Agenda

1. Introduction – A Brief History of the Basel Accord

2. Data Issues and Technology Challenges

3. Support for Broader Trends in Risk Management

4. Solution Components to Manage Credit Risk Under Basel II

5. Importance of Communication

Needed Components for a Basel II Credit Solution

Data Consolidation

and Quality Control

Credit Rating Models

(PD, EAD, LGD)

Credit rating workflow

• static customer data

• financial statements

• credit ratings

Operational credit systems

environment

Loans, limits, exposure analytics, etc.

IRB regulatory and economic

capital calculations &

validation framework

Internal and external reporting

Basel II Credit Risk Architecture Overview

Exposures

Collateral

Exposures

Trading/Banking Book (Corp./Banks/Sov.)

Banking book: SME / Retail Book

Credit system

Credit system

Collateral

B2 CapitalCalculator

Internal Credit Rating

Systems

PD, EAD, LGD

Ratings and Loss Data

Regulatory Capital

CalculationsRegulatoryReporting

RegulatoryCapital

Validation Framework

RegulatoryValidationReports

Historical Data

Analysis

InternalReporting

EconomicCapital

Calculations

EconomicCapital

Allocation

Tactical Decision Support

B2

Da

ta Co

ns

olid

ator

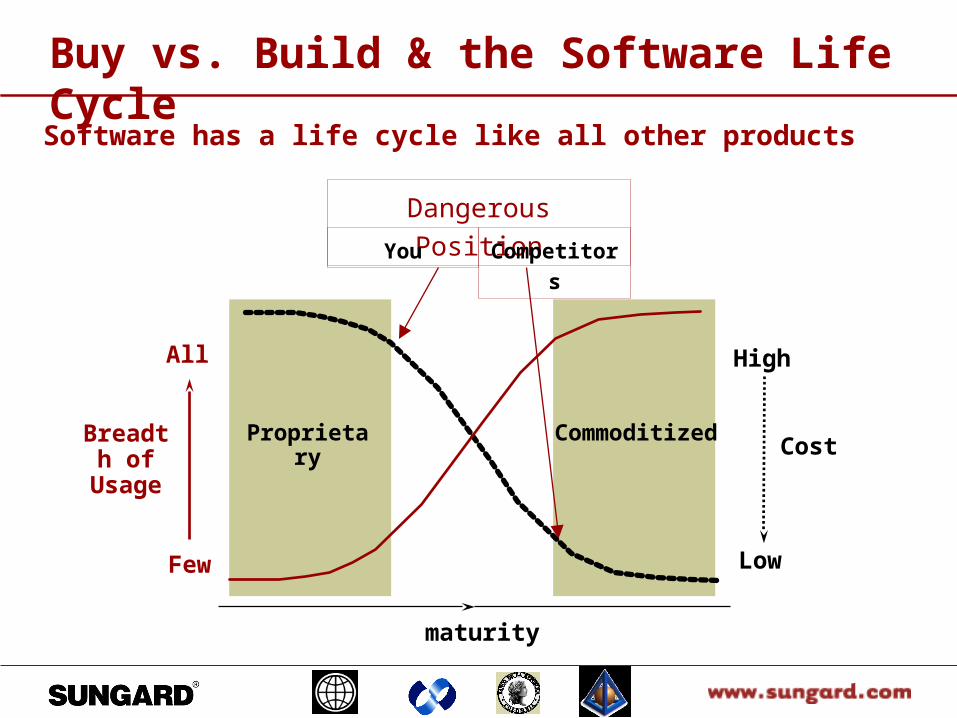

Buy vs. Build & the Software Life Cycle

Software has a life cycle like all other products

CommoditizedProprietaryBreadth of

Usage

All

Few

Cost

High

Low

maturity

Dangerous Position

You Competitors

Agenda

1. Introduction – A Brief History of the Basel Accord

2. Data Issues and Technology Challenges

3. Support for Broader Trends in Risk Management

4. Solution Components to Manage Credit Risk Under Basel II

5. Importance of Communication

The Third Challenge: Communication

Keeping the credit underwriters on board.

Providing information support for informed credit judgments.

Make validation constructive not threatening.

The motto should be:

Technology in Support of Sound Judgment

Top Related