Languages

Pages

Legal

The Southern African Oil & Gas Sector: analysis and

forecast

09 January 2013

I. Introduction to Infield Systems

II. Operations Offshore in Southern & Eastern Africa

a) Offshore Namibia

b) Offshore South Africa

c) Offshore Madagascar

d) Offshore Juan De Nova

e) Offshore Comoros Islands

f) Offshore Mozambique

g) Offshore Tanzania

h) Offshore Kenya

i) Offshore Seychelles

III. Opportunities in Southern & Eastern Africa

a) Opportunities in Namibia

b) Opportunities in South Africa

c) Opportunities in Juan de Nova

d) Opportunities in Mozambique

e) Opportunities in Tanzania

f) Opportunities in Kenya

IV. Market Analysis

a) South & East Africa Subsea wells by Country

b) South & East Africa Pipeline Installations (km) by Country

c) South & East Africa Control Line Installations (km) by Country

d) South & East Africa Platforms by Country

e) South & East Africa Summary of CAPEX ($m)

V. Appendix

VI. Disclaimer

2

Introduction to Infield Systems

SECTION I

O&G Sector Exposure

Infield provides services & products across the full OFS & renewables life cycle

Sources: FMC, Infield Systems4

Products & Services

A leading offshore O&G and associated services consultancy

5

Data, Reports & GIS Mapping Business Strategy and Analysis Transaction Services

• Offshore specific data covering production

infrastructure, rigs, specialist vessels,

construction yards, contracts and OFS

providers

• Sector specific reports

• GIS mapping services covering operational

and forecasted production infrastructure

• Market matching and market tracking –

“Match & Track”

• Complete market intelligence outsourcing

• Bespoke sector services

• Market entry strategy

• Procurement strategy advisory – “Project

Flow”

• Ad-hoc sector analysis

• Pre IPO due diligence

• Market overview IPO

• Debt financing analysis

• Distressed asset purchases

• Buy/sell side market due diligence

• Opportunity identification

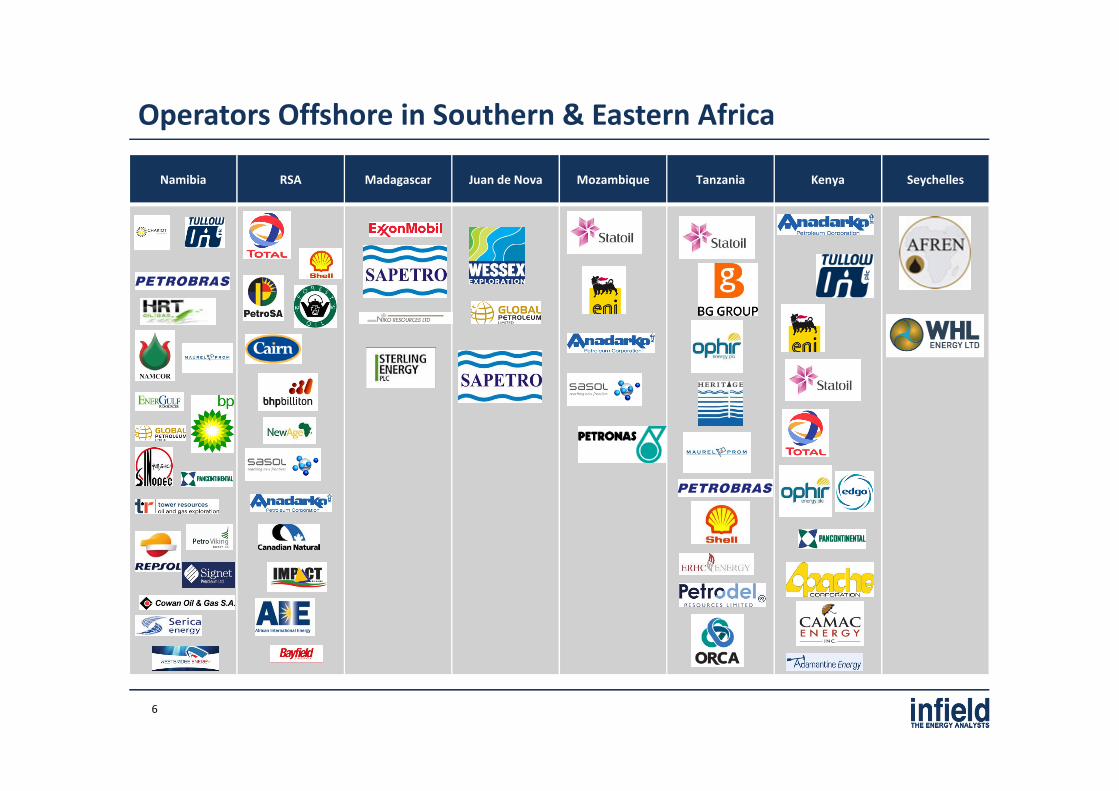

Operators Offshore in Southern & Eastern Africa

6

Namibia RSA Madagascar Juan de Nova Mozambique Tanzania Kenya Seychelles

Offshore Oil & Gas in Namibia

New Sub-Salt province?

Source: Infield Systems7

• Namibia has no offshore upstream production to speak of

• The only development is the much delayed Kudu field. The

field was discovered in 1974 by Chevron & Partners

• Namcor and Gazprom agreed to establish a special purpose

company to take a majority stake in the Kudu gas field from

Tullow Oil. Tullow Oil has resumed negotiations with

NamPower to develop the Kudu gas project.

Offshore Oil & Gas in South Africa

Economic Powerhouse of Southern Africa

Source: Infield Systems8

• The offshore upstream industry in RSA started in the early

90’s in the Mossel Bay area with the discovery of the Oribi

oilfield (1990) and the start of production form the F-A fields

(1992) by PetroSA

• The F-A fields were tied back to the Mossel Bay GTL refinery

which at the time was the worlds largest GTL facility

• The PetroSA operated Sable Gas (E-CE) field came onstream

in 2003

Offshore Oil & Gas in Madagascar

Heavy Oil Central

Source: Infield Systems9

• The existence of oil and gas reserves has been confirmed in

Madagascar but the area is considered to be both

underexplored and underexploited

• Onshore there are proved Heavy Oil deposits such as the

Tsimiroro field on Block 3104 & Bemolanga on Block 3102

• Offshore ExxonMobil, Niko Resources & Sterling Energy

have acreage

Offshore Oil & Gas in Juan de Nova

Frontier Exploration

Source: Infield Systems10

• Juan de Nova is under French control and the permits were

issued French Government in December 2008

• No systematic petroleum exploration has taken place

around Juan de Nova and this area is considered to be a

frontier province. Water depths range from 200 - 3,200m

• SAPETRO recently successful concluded the acquisition of

12,256 km 2-D seismic over the Juan de Nova Maritime

Profund block and Belo Profond (Madagascar)

Offshore Oil & Gas in Comoros Islands

Frontier Exploration

Source: Infield Systems & Bahari Resources11

• The Comoros Islands have one exploration block. This is located over anextension of the Rovuma Delta Fan

• The main potential appears to be the extension of the Rovuma Delta into theComoros, possibly lapping onto Grande Comore. The Rovuma Delta shows aworking petroleum system in the Mnazi Bay discovery near-shore

• Bhahari Resources is undertaking initial exploration on the block. The acreage isadjacent to offshore Area 1 and Area 4 of Mozambique's Rovuma Delta, wherethe recent giant hydrocarbon discoveries have been made by ENI and Anadarko.Bahari will undertake a phased seismic and drilling programme within thelicensed area and will in addition carry out for the Government a regional studyof the entire Comorian territory. The report will be used for the furtherdemarcation of blocks and a future licensing round

• The Comorian Government hopes to have in place by 2013 a Petroleum Codethat will govern all aspects of petroleum exploration and production as well asprovide for the internal structures to be created that will oversee, monitor andcontrol operations

Offshore Oil & Gas in Mozambique

New LNG Hub?

Source: Infield Systems12

• Mozambique launched its First Offshore Licensing Round on

31 March 2000. This bidding round offered 14 blocks mainly

in the Mozambique Basin covering the shallow and deep

Zambezi delta area

• Sasol was the first to strike Gas with the Njika in Block

16/19. This is still being evaluated

• Anadarko struck it big with the Windjammer discovery in

2010 (6.5TCF). This along with the Lagosta (4TCF), Tubarao

(3TCF), Camarao (6.5TCF) & Golfinho/Atum (10TCF) have

been grouped together to form the Prosperidade

development

• Shortly on the heels of Anadarko, ENI announced the

discovery of the Mamba South gas field (8TCF) in Rovuma

Offshore Area 4 in 2011. Area 4 has yield other sizable gas

discoveries with Mamba North/Northeast (7TCF) & Coral

(5TCF). The resources exclusively located in Area 4 are now

estimated at about 23 tcf plus of gas in place and the full

potential of Mamba Complex estimated at 75 tcf of gas in

place, which will be assessed with the coming delineation

wells.

Offshore Oil & Gas in Tanzania

First east African Production

Source: Infield Systems13

• Gas production started off Tanzania in 2004, with the SongoSongo field. The discovery well was drilled in l974 by AGIP(now ENI SpA). Songo Songo is conected to an onshore gasprocessing plant then a great proportion of the gas went tofuel the Songas Ubungo power plant in Dar es Salaam togenerate about 190MW of electricity (45% of the country'scapacity)

• In 1981 ENI discovered the Mnazi Bay gas field. Maurel &Prom is continuing to develop this area, with the 2012Mnazi Bay work programme which also includes workoverson three existing wells and either one appraisal or additionalexploration well

• BG Exploration & Production Tanzania Ltd’s recent Mzia gasfind in Block 1 has been stated as having an in placeresource estimate of 4-9TCF

• Tanzania is to review all contracts with oil and gasexploration companies by the end of November. Tanzaniaplans to restructure its state-run petroleum company. TheTanzania Petroleum Development Corporation (TPDC) couldbe split into two separate entities, one to act as anupstream regulator of the fast-growing gas industry and theother as a publicly-owned commercial oil company

Offshore Oil & Gas in Kenya

New Gas Province?

Source: Infield Systems14

• The Mbawa-1 exploration well in the L8 licence area is the

first offshore Discovery in Kenya. Gas was found in three

separate zones

• Tullow have discovered Oil & Gas with the onshore Twiga

South-1 well. Three sandstone reservoir zones, analogous to

Ngamia-1, were encountered and moveable oil, with an API

greater than 30 degrees was discovered

• Anadarko Petroleum is scheduled to begin exploring for oil

and gas in Kenya in December. The two wells, known as the

Kiboko prospect in block L11B and the Kubwa prospect in

block L7, will be drilled back to back and cost about $140

million each

• Simba Energy has announced the results of the Infrasonic

Passive Differential Spectroscopy (or 'passive seismic')

survey recently completed over Block 2A, Kenya, where it

has a 100% working interest

Offshore Oil & Gas in Seychelles

New areas of exploration

Source: Infield Systems15

• Afren (via East Africa Exploration) & WHL Energy are active

in exploration off the Seychelles

• Afren in Dec 2012 started the countries 1st 3D seismic

programme on its acreage, having previously completed a

2D seismic survey. The company’s licence areas have been

estimated to hold gross unrisked prospective resources of

2.8 billion barrels of oil equivalent

• Seychelles will undertake a licensing round this year

Opportunities in Namibia

New Sub Salt province?

Source: Chariot Oil & Gas16

• Kudu will be developed as a Gas to Power project withTullow remaining as operator after Gazprom/NAMCORfarmed in

• Recent offshore exploration activity has confirmed thatsource rock extending down the entire coastal line ofNamibia contains a subsalt petroleum system equivalent toBrazil and other offshore African plays such as Angola

• Chariot Oil & Gas plans more drilling in Namibia next year.The first one likely to be drilled will be Delta 1 in the Centrallicence area with the second to be confirmed after furtherevaluation and integration of recently acquired data setsfrom both the Tapir South and Kabeljou-1 wells

• Chariot have been awarded the Second Renewal Phase Northern Blocks 1811 A&B and of Licence 15 which encompasses Southern Block 2714B offshore Namibia. The Second Renewal Phase of these Licences runs from 27 October 2012 until 26 October 2014

• HRT may drill 4 wells in Namibian waters in 2013

• Repsol is planning to drill at least one exploration well in2014

Opportunities in South Africa

New areas of exploration

Source: Infield Systems17

• The west coast of RSA has attached interest with Cairn India

recently farming into Orange Basin Block 1 on the border

with Namibia. This is a historically underexplored area. Shell

and BHP Billiton are also active in this area

• Forest Exploration plans to supply gas to a power station at

Saldanha or Island Point. This field may come onstream

around 2017 via a mini TLP with separation, dehydration &

compression facilities

• Project Ikhwezi comprises a 39 km subsea tieback of the F-O

gas field to the existing F-A Platform. Major subsea

structures are being built by DCD Marine

• The deepwaters to the south of Mossel bay are under

exploration by Total who has extensive deep water

experience. The deepwater is thought to be analogous to

the North Falkland Basin where Rockhopper Exploration

found oil with its Sea Lion find in 2010.

Opportunities in South Africa

New areas of exploration

Source: Infield Systems18

• Whilst most offshore oil & gas production in RSA has

focused around the Mossel bay area, exploration licences

are well subscribed with many international players involved

• Licences in the Tuglea basin off the east coast are still in the

early stages of exploration with players such as Silver Wave

Energy, Sasol & Impact Africa active

• Anadarko recent farmed in to blocks 5, 6 & 7 off southern

South Africa (Anadarko 80% PetroSA 20%). Dolphin

Geophysical AS has signed an agreement with Anadarko

South Africa (Pty) Ltd for the acquisition of approximately

6250 kms, 2D survey offshore. The survey will be acquired

by Artemis Atlantic and commenced in December 2012.

Opportunities in South Africa

Shale Gas

Source: Shell19

• In September 2012 the RSA government lifted its moratorium on

shale gas exploration in SA.

• The US Energy Information Administration (EIA) has previously

estimated the potential recoverable shale gas resources in South

Africa to be around 485 TCF (EIA estimates there are about 480

recoverable TCF of shale gas in the U.S.).

• The Karoo Basin offers a potential exploration opportunity for

shale gas. In December 2010, Shell submitted three separate

exploration licence applications for areas of around 30,000

square kilometres each. These areas are in the Western Cape,

Eastern Cape and Northern Cape provinces of South Africa.

• According to Shell The Karoo’s natural gas potentials could

provide South Africa with a stable, alternative energy source for

power generation that is 40% more energy-efficient and emits

50-70% less CO2 than coal.

• Hydraulic fracking in this arid region could be assisted by the

publication of the Karoo Groundwater Atlas in Feb 2012. This

identifies the occurrence and characteristics of groundwater in

the Karoo area.

http://www-static.shell.com/static/zaf/downloads/media/karoo_groundwater_atlas.pdf

Opportunities in South Africa

Shale Gas

Source: Infield Systems20

• Other Companies with Shale Gas interests in South Africa

include:

• Sunset Energy – Cranmere & Thelma Areas

• Falcon Oil & Gas/Chevron – South West Karoo

• SASOL/Statoil/Chesapeake – North Karoo

• Anglo Coal – Eastern Karoo

• There is no regional pipeline network for oil and gas except for

the gas pipeline that connects SA with Mozambique

• As a comparison In 2010 alone the US shale gas capex was

24.8$bn on upstream and 8.4$bn in infrastructure according to

Americas Natural Gas Alliance. This is projected to rise to

39.6$bn on Upstream & 94$bn Infrastructure in 2015 (Drilling

(40%), Completions (50%), Facilities (10%))

• A study by Econometrix Ltd commissioned by Shell showed

that developing a 10th of South Africa’s resources may boost

the economy by about 200 billion rand ($24 billion) a year

• South Africa has also awarded CBM exploration permits to

several companies Some 20TCF od Gas is Place reserves have

been suggested. The potential for CBM extraction also extends

to the north into Botswana.

Opportunities in Madagascar

Frontier Province

Source: Infield Systems21

• In the Ampasindava block (2001C) the large Sifaka prospect

is ready to drill and has been independently estimated to

contain gross un-risked best estimate prospective

recoverable resources of 1.2 billion barrels (RISC Competent

Persons Report, March 2008). ExxonMobil (WI 70%,

Operator) and Sterling plan to drill this well once political

stability is re-established

Opportunities in Juan de Nova

New island Opportunity

Source: Wessex Petroleum22

Schematic Cross Section Across the Mozambique Channel

• Wessex Exploration (70%) & Jupiter Petroleum (30%) are jointly looking to farm-out their interest and are offering an incoming

party the opportunity to enter the exploration of this area through a low cost phased farm-in

• Wessex Exploration has completed the first phase of interpreting 1000 kilometres of reprocessed seismic shot six years ago by

TGS-Nopec over its Juan de Nova East

Opportunities in Mozambique

New LNG hub

23

• Anadarko & ENI have been in talks to build a LNG plant in Mozambique as part of a plan to jointly develop their recent major gasdiscoveries offshore

• This may lead to cooperation on the offshore development. Which has been proposed as a subsea to shore development with somedegree of compression 10 years after initial production. The Anadarko Prosperidade gas project will be from an initial 30 to 35 subseaproduction wells

• The most likely market for this LNG produced would be Asia. The total cost of offshore development and construction of a new two-trainLNG terminal will be around US$15bn. The FEED for the Prosperidade development is due to be awarded soon

• Total reached a farm-in agreement with Petronas, for the acquisition of a 40% interest in the PSC covering the offshore blocks Area 3 andArea 6 located in the Rovuma Basin. Petronas will retain the operatorship

Opportunities in Mozambique

New LNG hub

24

• Five options have arisen for the site of LNG & Gas utilisation facilities:

- Two initial LNG trains at Palma, commissioned by 2018, with two more added every two years until the site plays host to 10 trains

- Palma as the LNG hub, fed also with Rovuma basin onshore supplies, with power utilisation, fertiliser production and gas-to-liquids

output also coming online in 2018, 2019 and 2020, respectively

- Pemba centred development with the addition of gas supplies from the southern offshore Rovuma basin with an initial two LNG trains

and then another two trains by 2020. There would also gas pipeline running from Palma to Pemba, where the fertiliser and GTL

production would be sited

- GTL and fertiliser facilities focused in Nacala, gas-fuelled power generation in Palma and a pipeline between Pemba and Nacala

- LNG trains located at Palma but with gas piped also to Beira for fertiliser and GTL production

Opportunities in Mozambique

New Gas/LNG hub

Source: Government of Mozambique25

• The Mozambican government is seeking to draw up a Gas

Master Plan (MGMP) which implies the clear definition of

the cycle of production and of transport of the gas.

Mozambique Ministers have stated the huge energy

resource must be handled in such a way as optimize the

benefits for Mozambican society, including the growth of

institutional capacities in both public and private sectors,

the development of roads and other infrastructures, and an

expansion in access to training and to employment

• An agreement was signed between the government and the

Sasol in 2000, allowing the building of a pipeline 865

kilometres long to carry the gas from Temane to Secunda in

South Africa. Exports of the Inhambane gas began in 2004

• The plans to produce LNG in Cabo Delgado require an

estimated investment of US18$bn. The earliest possible

date for the start of LNG production is 2018

Opportunities in Tanzania

26

• BG Exploration & Production Tanzania Ltd has discovered six fields over Block 1, 3 & 4. Whilst Statoil has made two discoveries in Block 2

• These discoveries have resulted in the some 19.3 TCF being realised. Tanzania is also working on Gas Master Plan the results of which are

due for release later this year. Tanzania will be looking to build gas processing plants & power plants. A financial deal for the construction

of a 532km gas pipeline from Dar es Salaam to Mtwara was signed in June 2012 with China’s Export-Import Bank

• BG Group are looking towards the port of Mtwara as train LNG export hub, whilst is said to favour Statoil Lindi some 60km to the

northwest. Block 1 could support two LNG trains whilst discoveries in block 2 could support a third.

• KBR is to perform Pre-FEED studies for Statoil for a prospective LNG facility

• Tanzania and its semi-autonomous islands of Zanzibar have agreed on the sharing of any future hydrocarbon revenues. This will allow

work on blocks 9, 10, 11 and 12 held under force majeure by Shell for over ten years.

Discovery Chaza (Block 1) Jodari (Block 1) Mzia (Block 1) Papa (Block 3) Pweza (Block 4) Chewa (Block 4) Zafarani (Block 2) Lavani (Block 2)

Operator BG BG BG BG BG BG Statoil Statoil

Resource TCF 0.47 3.4 4.5 1.0 1.7 1.8 4.5 2.0

Discovery Date 07-Feb 11 26-Mar 11 26-Mar 12 26-Mar 12 22-Oct 10 01-Dec 10 01-Mar 12 10-Mar 12

Opportunities in Kenya

Source: Pancontinental27

• BG & partners L10A and L10B plan to carry out a new 3D surveyof 2,280 sq km in the western portion of the licence areas. Thenew 3D survey is planned to commence in November 2012. Fullinterpreted results are expected Q2 2013

• Kenya will move to bidding rounds for its oil exploration blocks.This will move away from the open block one-to-one negotiationswith oil companies.

• Kenya also plans to increase the signature bonus companies arerequired to pay when there are granted a new licence.

• The size of new exploration blocks will be reduced in size so morecompanies can explore acreage.

• Kenya aims to take a bigger slice of the profits from its naturalresources exploration boom by seeking a 25 percent stake in theproduction activities of oil and gas companies operating in theeast African nation. The proposal announced by Kenya's energyminister is one of many the government has put forward in thepast month to increase the state's take from oil and gasresources, including new capital gains tax rules, a morecompetitive licensing process and higher fees for petroleumexplorers. At present most of Kenya's contracts with oil explorersgive state-owned National Oil Corporation of Kenya (NOCK) a 10percent stake in the production business once commercialquantities of oil or gas are found. This means that NOCKcontributes 10 percent of production costs and receives 10percent of profit. However, the government now wantscompanies to give NOCK an initial 10 percent stake, increasing to25 percent once production has started

South & East Africa Market OverviewSouth & East Africa Subsea wells by Country

South & East Africa Subsea wells by Country28

0

5

10

15

20

25

30

2008 2009 2011 2014 2016 2017 2018 2019 2020 2021

Mozambique Namibia Republic Of South Africa Tanzania

Country 2008 2009 2011 2014 2016 2017 2018 2019 2020 2021 Grand Total

Mozambique 0 0 0 0 0 0 2 9 13 3 27

Namibia 0 0 0 0 0 1 5 0 0 0 6

Republic Of South Africa 1 1 2 4 5 8 6 3 6 3 39

Tanzania 0 0 0 0 0 2 2 10 7 3 24

Grand Total 1 1 2 4 5 11 15 22 26 9 96

South & East Africa Market OverviewSouth & East Africa Pipeline Installations by Country (km)

South & East Africa Pipeline Installations by Country (km) 29

Country 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Grand Total

Mozambique 0 0 0 0 0 0 0 0 0 1 62 351 414

Namibia 0 0 0 0 0 0 0 0 0 0 8 0 8

Republic Of South Africa 101 0 7 0 40 0 1 5 1 190 1 31 377

Tanzania 0 0 0 0 0 3 25 0 0 40 190 25 283

Grand Total 101 0 7 0 40 3 26 5 1 231 261 407 1,083

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Mozambique Namibia Republic Of South Africa Tanzania

South & East Africa Market OverviewSouth & East Africa Control Line Installations by Country (km)

South & East Africa Control Line Installations by Country (km) 30

Country 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Grand Total

Mozambique 0 0 0 0 0 0 0 0 0 0 6 133 139

Namibia 0 0 0 0 0 0 0 0 0 0 4 0 4

Republic Of South Africa 39 0 7 0 40 0 0 3 1 110 0 16 216

Tanzania 0 0 0 75 0 0 0 0 0 0 4 19 98

Grand Total 39 0 7 75 40 0 0 3 1 110 15 168 457

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Mozambique Namibia Republic Of South Africa Tanzania

South & East Africa Market OverviewSouth & East Africa Summary of CAPEX (US$m)

South & East Africa Summary of CAPEX (US$m)31

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Mozambique Namibia Republic Of South Africa Tanzania

Country 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Grand Total

Mozambique 0 0 0 0 0 0 0 0 230 430 942 2,389 3,991

Namibia 0 0 0 0 0 0 0 0 59 143 182 68 451

Republic Of South Africa 223 30 17 13 186 3 47 130 509 578 211 233 2,419

Tanzania 0 0 30 36 11 42 19 0 138 421 951 698 2,344

Grand Total 223 30 47 49 197 44 66 130 934 1,572 2,285 3,388 9,205

South & East Africa Market Overview

32

South & East Africa Platforms by Country

Country FixtureType 2015 2016 2017 2018 2019 2020 Grand Total

Mozambique Fixed 0 0 1 0 0 0 1

Floating 0 0 1 1 0 0 2

Namibia Floating 0 1 0 0 0 0 1

Republic Of South Africa Floating 2 2 0 0 1 0 5

Tanzania Floating 0 0 1 0 2 1 4

Grand Total 2 3 3 1 3 3 13

Country Platform Type Installation Year Status

RSA Mossel Bay E-BK FSO FSO (Conversion) 2015 Possible

RSA Mossel Bay E-BK FPS FPS SemiSub (Conversion) 2015 Possible

RSA Ibhubesi TLP-A FPS TLP (New Build) 2016 Possible

RSA Mossel Bay LNG Import FSRU FPSO (Conversion) 2016 Possible

Namibia Kudu FPSO FPSO (Conversion) 2016 Possible

Mozambique Windjammer (Prosperidade APC) Fixed 2017 Possible

MozambiqueWindjammer (Prosperidade FPS)

FPS SemiSub (New Build) 2017 Possible

Tanzania Jodari (Block 1) FPS TLP (New Build) 2017 Probable

Mozambique Golfinho/Atum FPS TLP (New Build) 2018 Possible

RSA Ibhubesi West FPS TLP (New Build) 2019 Possible

Tanzania Chewa (Block 4) FPS TLP (New Build) 2019 Probable

Tanzania Chaza FPS TLP (New Build) 2019 Possible

Tanzania Zafarani (Block 2) FPS TLP (New Build) 2020 Possible

Security

Source: NATO Shipping Centre33

• This maps show piracy attacks in the last year in the Indian

Ocean

• Mozambique has requested Naval & Air support from South

Africa to secure its waters against Somali piracy

Infield South & East Africa Map

34

Disclaimer

35

The information contained in this document is believed to be accurate, but no representation or warranty, express or implied, is made by Infield Systems

Limited as to the completeness, accuracy or fairness of any information contained in it, and we do not accept any responsibility in relation to such information

whether fact, opinion or conclusion that the reader may draw. The views expressed are those of the individual contributors and do not represent those of the

publishers.

Some of the statements contained in this document are forward-looking statements. Forward looking statements include, but are not limited to, statements

concerning estimates of recoverable hydrocarbons, expected hydrocarbon prices, expected costs, numbers of development units, statements relating to the

continued advancement of the industry’s projects and other statements which are not historical facts. When used in this document, and in other published

information of the Company, the words such as "could," "forecast”, “estimate," "expect," "intend," "may," "potential," "should," and similar expressions are

forward-looking statements.

Although the Company believes that its expectations reflected in the forward-looking statements are reasonable, such statements involve risk and uncertainties

and no assurance can be given that actual results will be consistent with these forward-looking statements. Various factors could cause actual results to differ

from these forward-looking statements, including the potential for the industry’s projects to experience technical or mechanical problems or changes in

financial decisions, geological conditions in the reservoir may not result in a commercial level of oil and gas production, changes in product prices and other

risks not anticipated by the Company. Since forward-looking statements address future events and conditions, by their very nature, they involve inherent risks

and uncertainties.

© Infield Systems Limited 2012

Top Related