Languages

Pages

Legal

Paladin Energy LtdPaladin Energy Ltd

The New Energy In The Markete New e gy e Ma etJohn Borshoff – Managing Director/CEO

Annual General Meeting26 November 2008

1

Disclaimer

This presentation includes certain statements that may be deemed “forward-lookingstatements”. All statements in this presentation, other than statements of historical facts, thataddress future production, reserve or resource potential, exploration drilling, exploitationactivities and events or developments that Paladin Energy Ltd (the “Company”) expects tooccur, are forward-looking statements.

Although the Company believes the expectations expressed in such forward-lookingstatements are based on reasonable assumptions, such statements are not guarantees offuture performance and actual results or developments may differ materially from those in theforward-looking statements Factors that could cause actual results to differ materially fromforward-looking statements. Factors that could cause actual results to differ materially fromthose in forward looking statements include market prices, exploitation and explorationsuccesses, and continued availability of capital and financing and general economic, marketor business conditions.

Investors are cautioned that any such statements are not guarantees of future performanceand actual results or developments may differ materially from those projected in the forward-looking statements. The Company does not assume any obligation to update or revise itsforward-looking statements, whether as a result of new information, future events orotherwise.

2

Presentation Outline

P l di St t• Paladin Status

• Uranium Market (Dustin Garrow)

• Projects Update – Langer Heinrich (Wyatt Buck)

K l k P j t (J h B h ff)– Kayelekera Project (John Borshoff)

– Social Development Component - Malawi (Neville Huxham)

F t re O tlook• Future Outlook

3

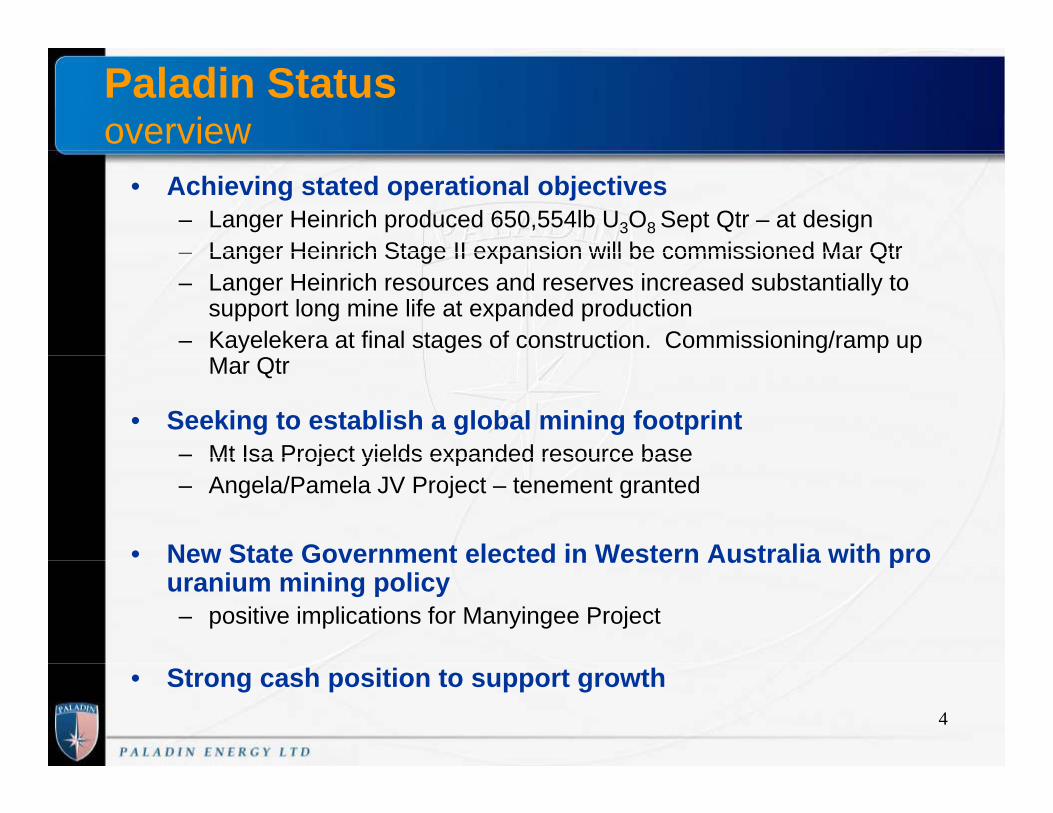

Paladin Statusoverview

• Achieving stated operational objectives– Langer Heinrich produced 650,554lb U3O8 Sept Qtr – at design– Langer Heinrich Stage II expansion will be commissioned Mar Qtr– Langer Heinrich Stage II expansion will be commissioned Mar Qtr– Langer Heinrich resources and reserves increased substantially to

support long mine life at expanded production– Kayelekera at final stages of construction. Commissioning/ramp up

Mar Qtr

• Seeking to establish a global mining footprint– Mt Isa Project yields expanded resource baseMt Isa Project yields expanded resource base– Angela/Pamela JV Project – tenement granted

• New State Government elected in Western Australia with proNew State Government elected in Western Australia with pro uranium mining policy– positive implications for Manyingee Project

• Strong cash position to support growth4

Paladin’s Suite of Uranium Properties staged for sequential developmentg q p

Advanced Exploration Project

Pre Development Project

Construction of MineReserves of 25MlbResources of 35Mlb

jResources of 23Mlb Resource - 85Mlb

pro uranium

pro uranium

Re-activate EvaluationManyingee Resource of 24Mlb

New ProjectAngela/Pamela Deposits

pro uranium

Operating Mine plus expansion

Reserves of 65.8Mlb

DepositsHistorical ~28Mlb

P l di 100%Attributable Pounds

Resources of 164MlbPaladin 42.06% Paladin 50% (plus 81.99% control of Summit –

in its 100% owned properties) Paladin 50% JV Cameco

Paladin 100% Paladin 85%

5Deep Yellow 19.29%

URANIUM MARKETURANIUM MARKET

Dustin GarrowMarketing / Paladin Nuclear Ltd

6

World Nuclear Capacity(October 2008)

439 Reactors

373,247 MWe

30 Countries30 Countries

167 million pounds U3O8 required

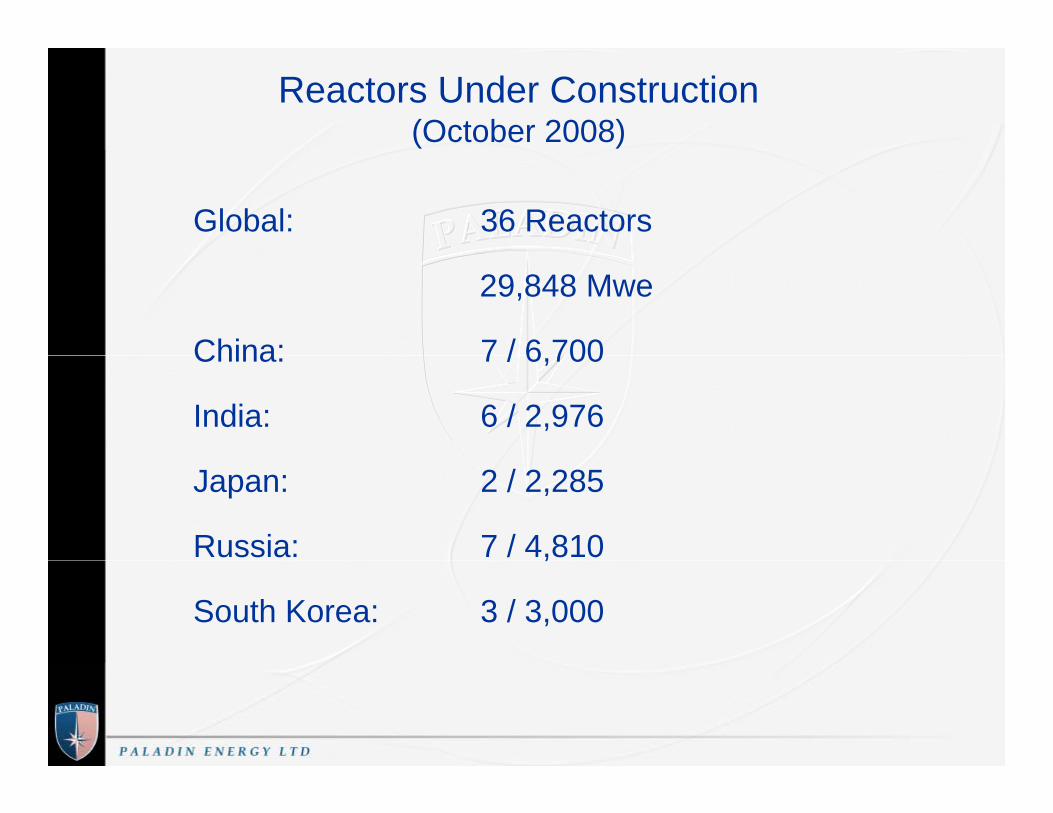

Reactors Under Construction(October 2008)

Global: 36 Reactors

29,848 Mwe

China: 7 / 6 700China: 7 / 6,700

India: 6 / 2,976

Japan: 2 / 2,285

Russia: 7 / 4,810,

South Korea: 3 / 3,000

Reactors - Planned(October 2008)

Global: 99 Reactors

108,675 Mwe

China: 26 / 27,620,

India: 10 / 9,760

Japan: 11 / 14 ,945

Russia: 12 / 14,340

South Korea: 5 / 6,600

United States: 12 / 15 000United States: 12 / 15,000

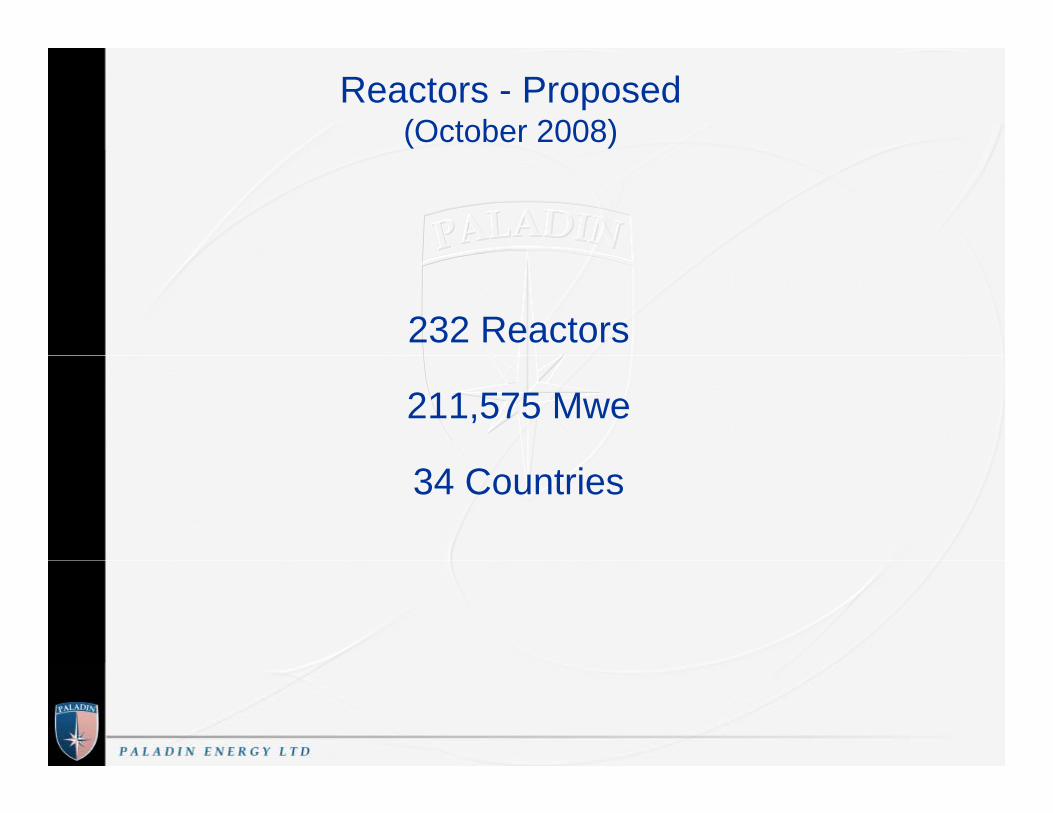

Reactors - Proposed(October 2008)

232 Reactors

211,575 Mwe

34 Countries

Global Uranium Production/Demand

Supply is flat despite strong price/demand growthCumulative planned and

Production 1996-2007120 50112

222 316

Cumulative planned and proposed reactor builds (by year of announcement)

91 92.887.7

80 891.5 94.5 93.7 92.6

104.7 108.9102.5

108

8090

100110120

U3O

8

5050 222

80.8

3040506070

Mill

ion

Poun

ds

0102030

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

M

Spot price2006 Production 102.5Mlb – Down 5%2007 Production 108.0Mlb – Up 5%

Uranium Production

• Announced production cut-backs/start-up delays– Cameco (McArthur River / Rabbit Lake / U.S. ISR / Inkai)– UraniumOne (Dominion closure)– Denison (White Mesa / Midwest)– Uranium Resources (Kingsville Dome / Rosita)( g )– First Uranium (Ezulwini)– KazAtomProm decreased 2009 forecast by 14%

• UxC had been forecasting 2008 global production of 121.8Mlb U3O8 but more likely around 110Mlb - 112Mlb U3O8

• Cigar Lake delay due to mine flooding (October 2006)Cigar Lake delay due to mine flooding (October 2006)

• Olympic Dam expansion delay

Uranium Price Trend2007 - Present

$140.00 $140.00

$100.00

$110.00

$120.00

$130.00

$100.00

$110.00

$120.00

$130.00

$60.00

$70.00

$80.00

$90.00

US

$/lb

U3O

8

$60.00

$70.00

$80.00

$90.00

$20.00

$30.00

$40.00

$50.00

$20.00

$30.00

$40.00

$50.00

$10.00

$20.00

Jan-07 Jan-08 Jan-09$10.00

$20.00

Average U3O8 Spot Price Long-Term U3O8 Price

Spot Uranium Market

• Through mid-November, 2008 spot market volume exceeded 37 0Mlb; September volume set new monthlyexceeded 37.0Mlb; September volume set new monthly record of over 8.3Mlb transacted

N l tiliti i th l t i l b i ith• Nuclear utilities remain the largest single buying group with primary producers making large purchases

• China Guangdong Nuclear Power entered spot market for the delivery of 800 MTU (2.1Mlb) by mid-2009

• Recent spot price rise from $44/lb to $55/lb reflecting favourable market fundamentals

Term Uranium Market

• Long-Term price indications began 2008 at $95/lb butdeclined through the year to current level of $70/lbdeclined through the year to current level of $70/lb.

• Anticipate increased buying activity commencing early2009 as nuclear utilities look to cover forward uranium2009 as nuclear utilities look to cover forward uraniumneeds (2010/2011 and beyond)

• Purchase uranium for initial reactor fuel loadings (new• Purchase uranium for initial reactor fuel loadings (newbuild) expected

• On-going uranium supply constraints expected to place• On-going uranium supply constraints expected to placeupward pressure on term price

• INDIA (?)• INDIA (?)

LANGER HEINRICH UPDATELANGER HEINRICH UPDATE

Wyatt BuckGM - Production

16

STAGE I AT DESIGN PRODUCTION STAGE III EXPANSION IN DESIGN PHASE

STAGE II EXPANSION ON SCHEDULE LARGE RESOURCE UPGRADE

LHU Temporary Tailings Dam2 Nov 2008

Pit A & B 2 Nov 2008

Langer Heinrich Projectlarge resource/reserve upgradeg pg

MINERAL RESOURCES

250ppm Cut-off Mt Grade % U3O8 t U3O8 Mlb U3O8

Measured Resources 32.8 0.06 19,582 43.158

Indicated Resources 23.8 0.06 13,278 29.260

Measured + Indicated 56.4 0.06 32,858 72.418

Inferred Resources 70.7 0.06 41,557 91.591

JORC / NI 43 101 li t

46% increase

65% increase

JORC / NI 43-101 compliant

MINING RESERVES @ US$60/lb U3O8

250ppm Cut-off Mt Grade % U3O8 Tonnes U3O8

Proven Ore Reserves 30.0 0.06 17,924 (39.50Mlb)

Probable Ore Reserves 20.6 0.06 11,950 (26.34Mlb)

Total 50.6 0.06 29,874 (65.84Mlb) 75% increase

JORC / NI 43-101 compliant

20

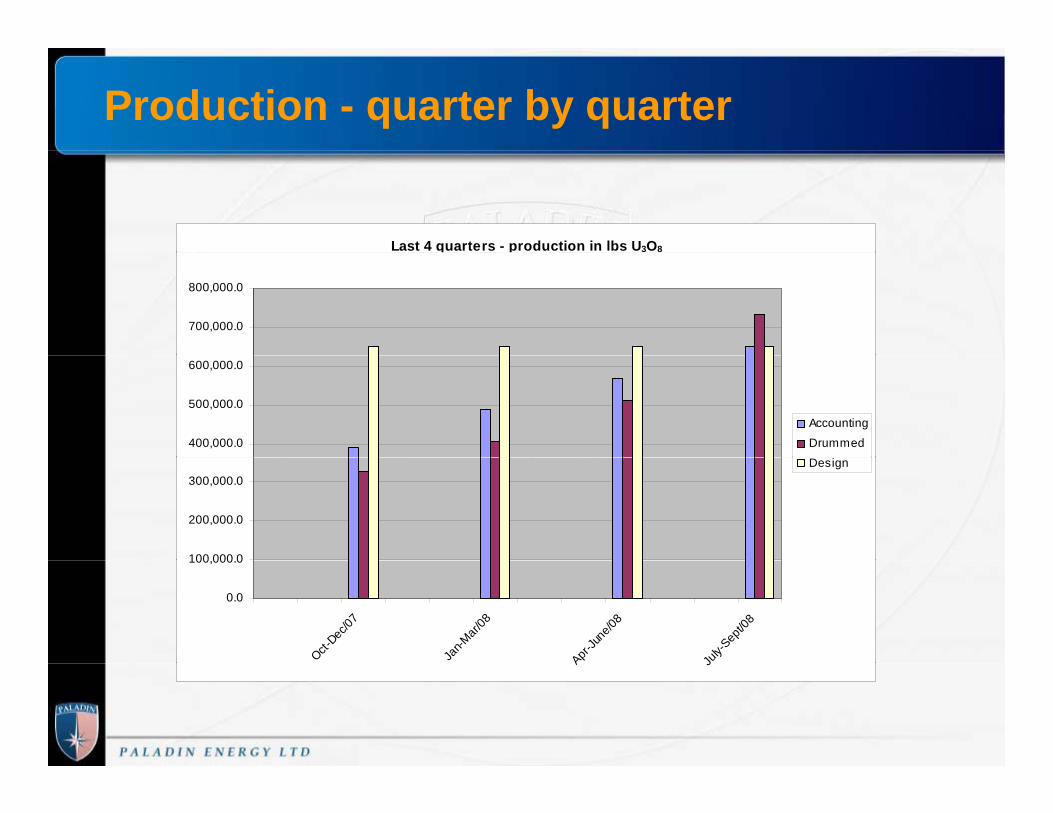

Production - quarter by quarter

Last 4 quarters - production in lbs U3O8q p

700,000.0

800,000.0

400,000.0

500,000.0

600,000.0

Accounting

Drummed

100 000 0

200,000.0

300,000.0Design

0.0

100,000.0

Oct-Dec

/07

Jan-M

ar/08

Apr-Ju

ne/08

July-

Sept/0

8

A J

Production – month by month

Production - lbs U3O8

250,000

300,000

150,000

200,000Accounting

drumming

design

-

50,000

100,000

Apr May June July Aug Sept Oct

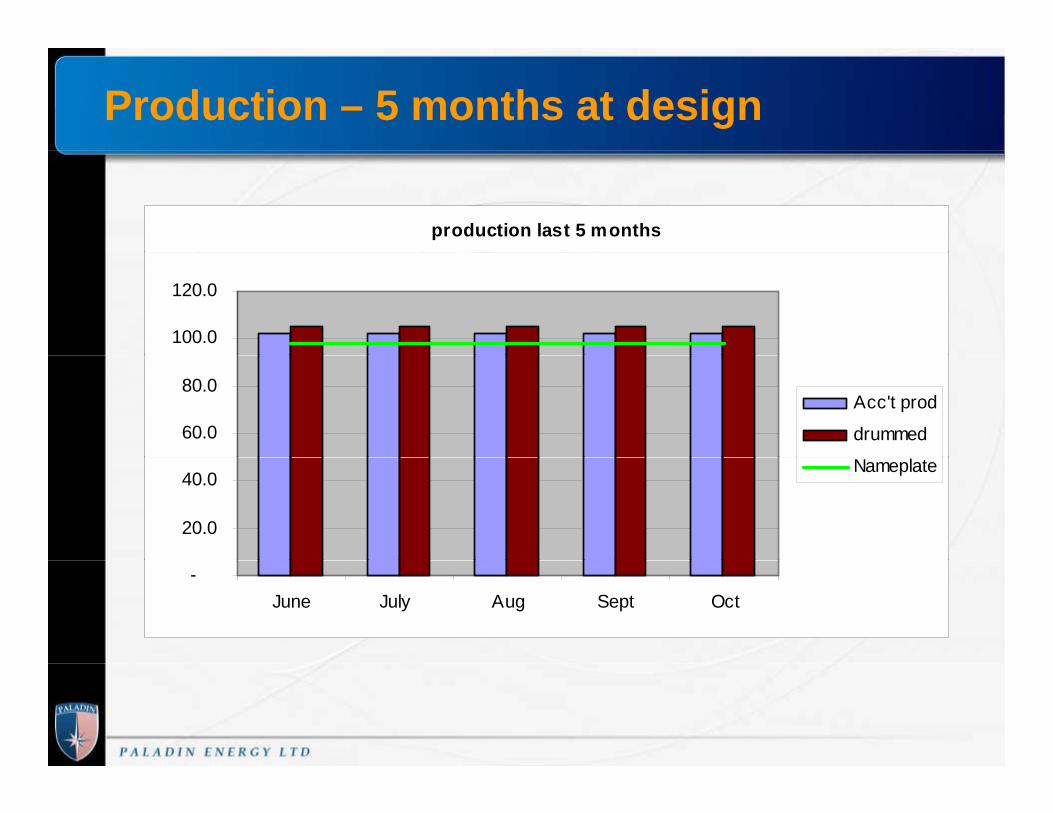

Production – 5 months at design

production last 5 months

100.0

120.0

60.0

80.0Acc't prod

drummed

20.0

40.0Nameplate

-June July Aug Sept Oct

Plant Performance – Cash Unit Cost

Unit Cost

30.00

35.00

15.00

20.00

25.00

5.00

10.00

5 00

0.00July Aug Sept Oct

Stage II Expansion

2 Nov 20082 Nov 2008

Questions?

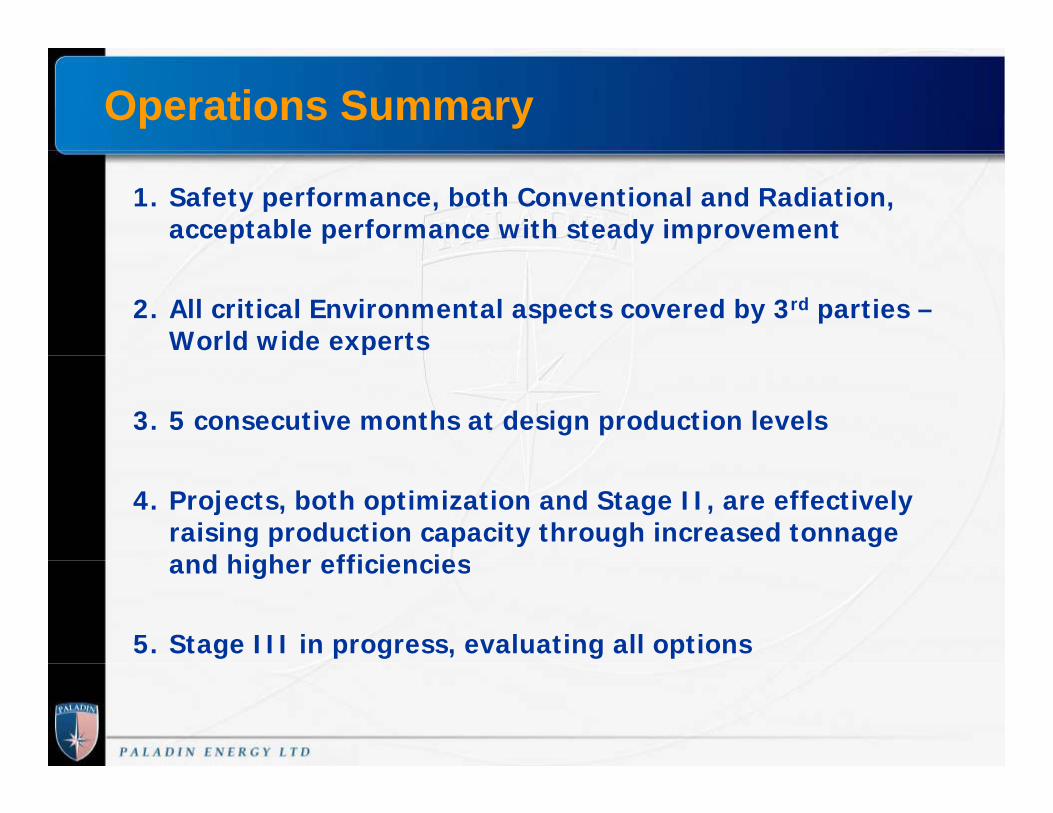

Operations Summary

1. Safety performance, both Conventional and Radiation, acceptable performance with steady improvement

2. All critical Environmental aspects covered by 3rd parties –World wide experts

3. 5 consecutive months at design production levels

4. Projects, both optimization and Stage II, are effectively raising production capacity through increased tonnage and higher efficienciesand higher efficiencies

5. Stage III in progress, evaluating all options

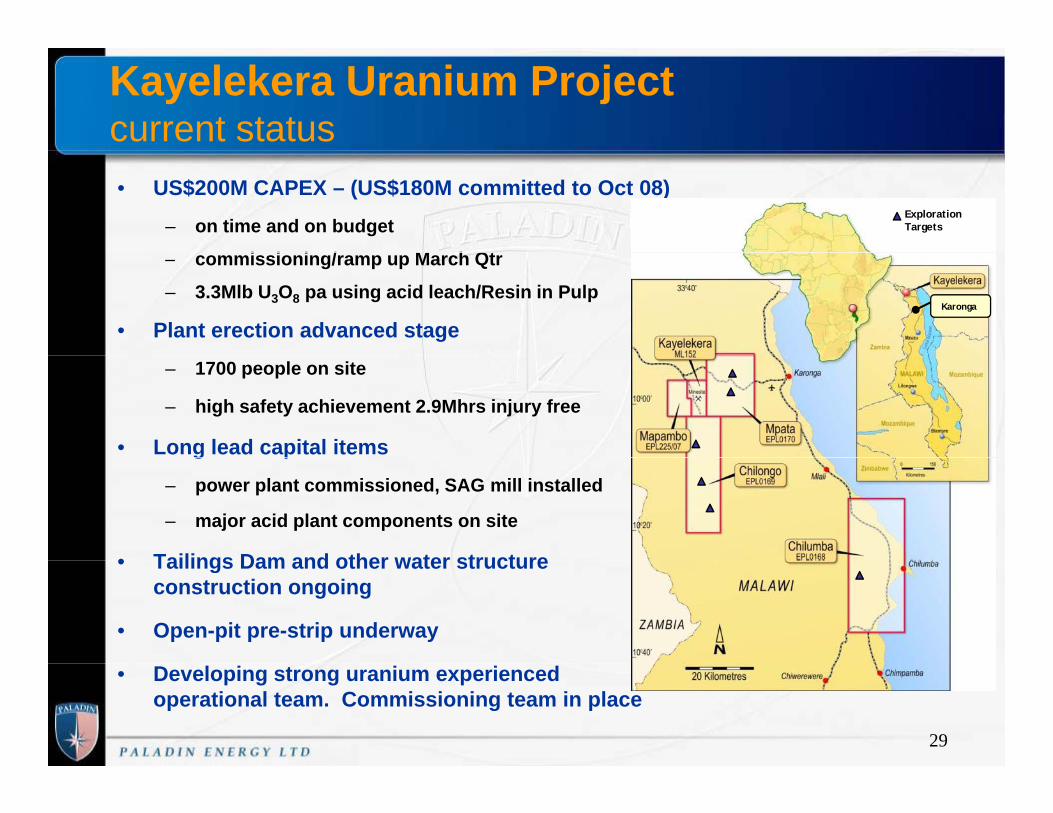

Kayelekera Uranium Project St tStatus

Paladin (Africa) Ltd

Kayelekera Uranium Projectcurrent status• US$200M CAPEX – (US$180M committed to Oct 08)

– on time and on budget

i i i / M h Qt

Exploration Targets

– commissioning/ramp up March Qtr

– 3.3Mlb U3O8 pa using acid leach/Resin in Pulp

• Plant erection advanced stageKaronga

– 1700 people on site

– high safety achievement 2.9Mhrs injury free

• Long lead capital items g p

– power plant commissioned, SAG mill installed

– major acid plant components on site

• Tailings Dam and other water structure• Tailings Dam and other water structure construction ongoing

• Open-pit pre-strip underway

• Developing strong uranium experiencedoperational team. Commissioning team in place

29

Getting ready for commissioning Conveyors Mill and Pre-LeachConveyors Mill and Pre-Leach

Paladin (Africa) LtdTailings ThickenerCrusher

(mineral sizer)

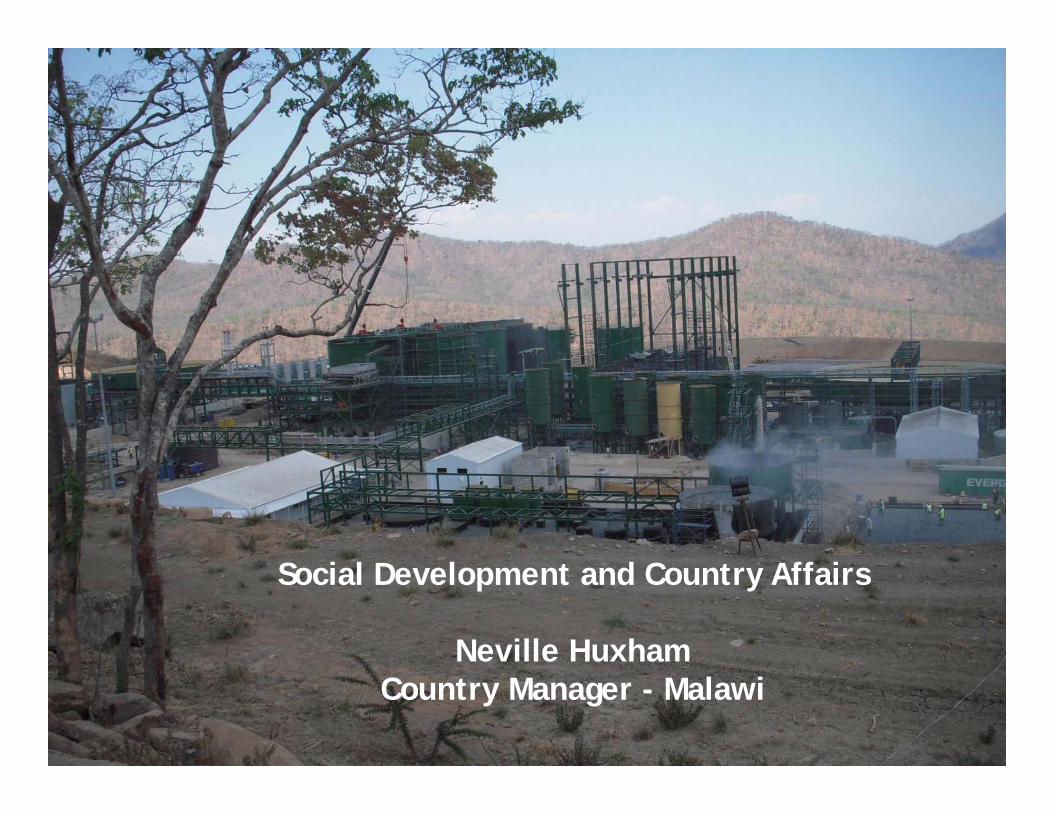

Social Development and Country Affairs

Neville Huxham

Paladin (Africa) Ltd

Country Manager - Malawi

Malawi - Social Management Objectives

Protecting Paladin’s Good Nameg

StrategicObjectives Enhancing Our Corporate Reputationj

Maintaining Project Value

• Engaging with civil societies (NGO’s) and local communities and preserving accord

• Managing Government and key stakeholder relationships to promote Company interestsCompany interests.

• Maintaining an “early warning” system to detect and deal with issues before they become “incidents”.

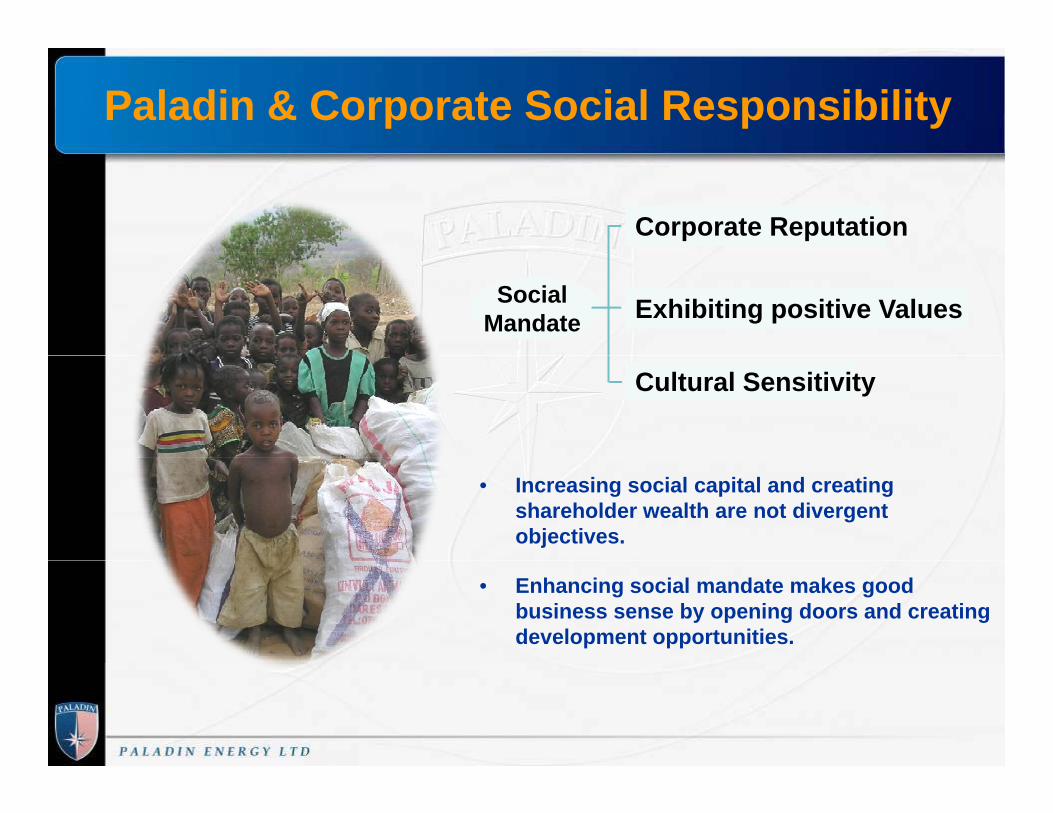

Paladin & Corporate Social Responsibility

Corporate Reputation

Social Mandate Exhibiting positive Values

Cultural Sensitivity

• Increasing social capital and creating shareholder wealth are not divergent objectives.

• Enhancing social mandate makes good business sense by opening doors and creating development opportunities.

Social Responsibility Program Focus

Lack of irrigation and subsistence farming lead to crop failure, poverty and famine.

Better food production

HIV/AIDS, tuberculosis and malaria are major killers in MalawiHealth

Issuesmalaria are major killers in Malawi.

Access to Education

Creating the foundation for a productive and fulfilling life.

FosteringBusiness

To provide job opportunities and foster local business opportunities to supply Paladin and others with goods y gand services.

Health Clinic Work in Progress

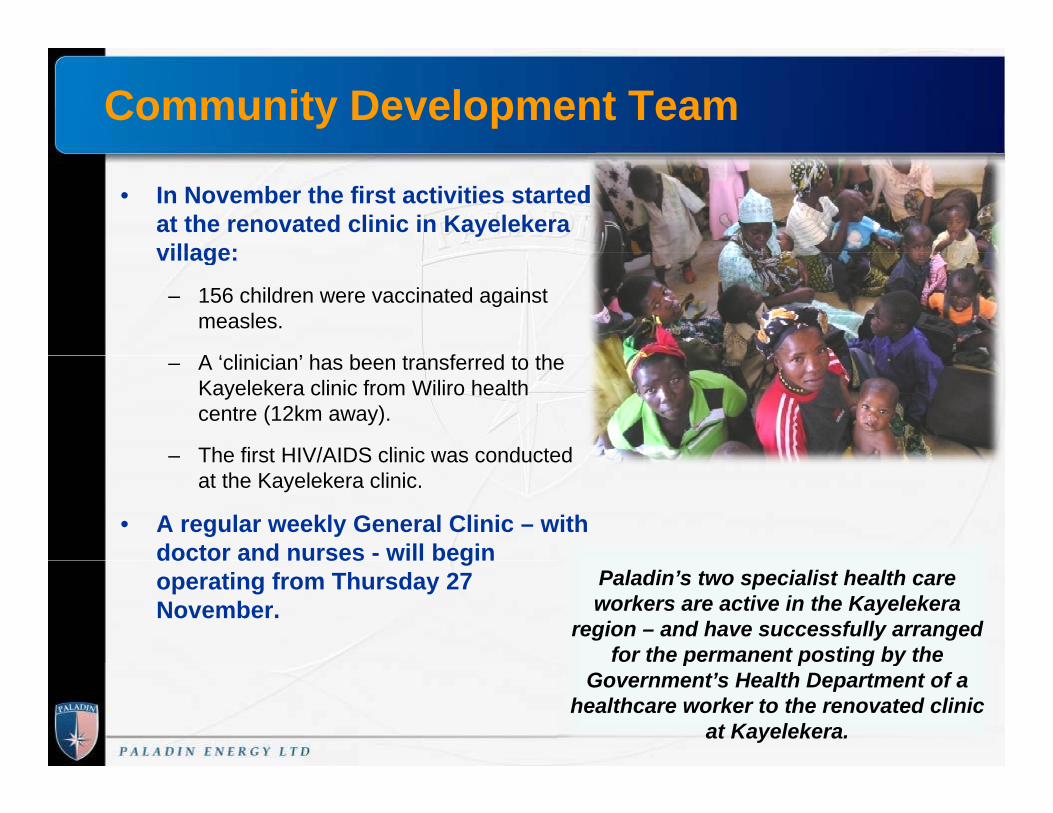

Community Development Team

• In November the first activities started at the renovated clinic in Kayelekera village:village:

– 156 children were vaccinated against measles.

A ‘ li i i ’ h b t f d t th– A ‘clinician’ has been transferred to the Kayelekera clinic from Wiliro health centre (12km away).

– The first HIV/AIDS clinic was conductedThe first HIV/AIDS clinic was conducted at the Kayelekera clinic.

• A regular weekly General Clinic – with doctor and nurses - will begindoctor and nurses will begin operating from Thursday 27 November.

Paladin’s two specialist health care workers are active in the Kayelekera

region – and have successfully arranged for the permanent posting by the p p g y

Government’s Health Department of a healthcare worker to the renovated clinic

at Kayelekera.

Garnet Halliday Karonga Water Supply Project - Update j p

• Agreement concluded with Northern Region Water B d bli fi l d i f P j tBoard enabling final design for Project.

• Upgraded water supply to provide sustainable, safe drinking for Karonga Town’s projected population ofdrinking for Karonga Town s projected population of 45,000 people.

• Plan to utilise local labour (job creation/income generation).

Presentation Outline

FUTURE OUTLOOK

38

4 Year Production Outlook

9.310

6.6

8.4

7

8

9Actual Forecast

3 354

5

6MlbU3O8

1.71

3.35

1

2

3

4

0

1

2007/08 2008/09 2009/10 2010/11 2011/12

Langer Heinrich Production Kayelekera Production

39

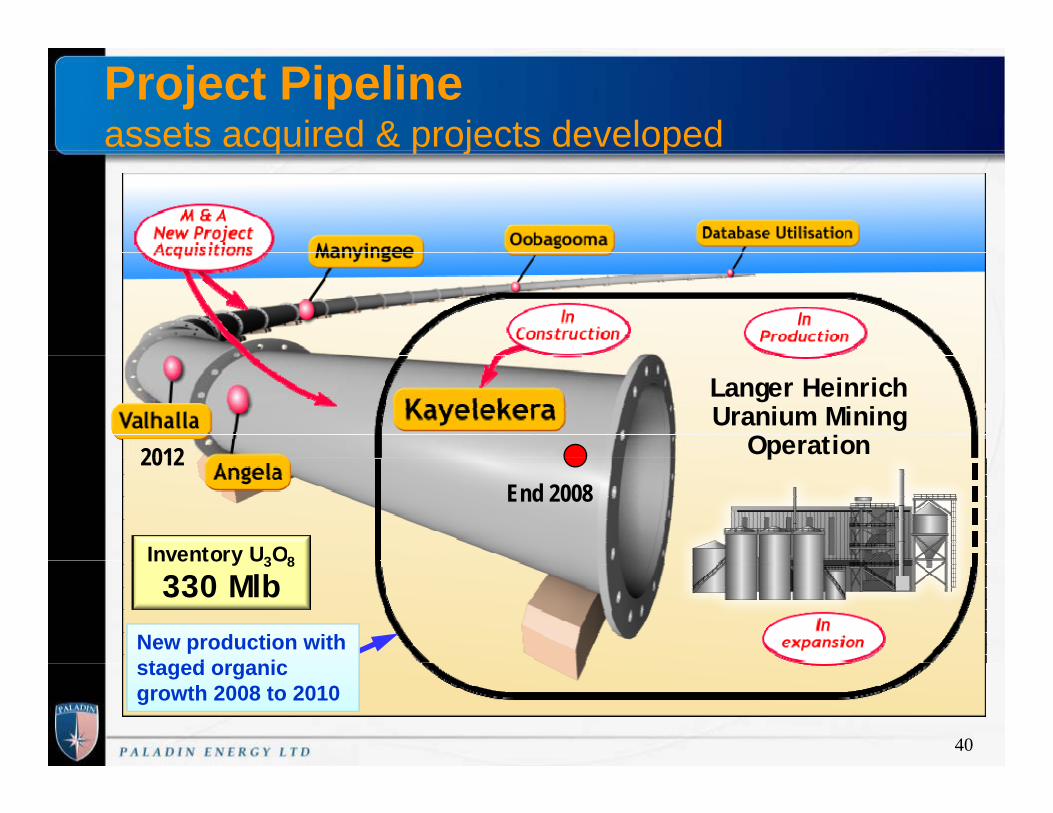

Project Pipelineassets acquired & projects developedq p j p

2012

Langer HeinrichUranium Mining

Operation

End 20082012

Inventory U3O8

p

Inventory U3O8

330 Mlb

New production with t d istaged organic

growth 2008 to 2010

40

Paladin Offers Excellent Upside key outcomes for 2008/09y

• Langer Heinrich (Namibia)– achieve 1.4Mlb to 1.55Mlb for H2 2008 (CY)– complete Stage II expansion (2.6Mlb to 3.7Mlb pa) early 2009– planning/design for Stage III expansion – produce 3.1Mlb U3O8 for 12 month period end June 09

• Kayelekera (Malawi) y ( )– construction completed end 2008– produce 0.3Mlb U3O8 by June 09

• Mt Isa Project (Queensland - Australia)Mt Isa Project (Queensland Australia)– new resource estimate Dec Qtr – complete prefeasibility study

• Angela/Pamela Uranium Deposit (Northern Territory Australia)• Angela/Pamela Uranium Deposit (Northern Territory – Australia)– commence field work June quarter 09

• Manyingee (Western Australia)exploration start up– exploration start up

Significant opportunity to increase overall resource base in 08/0941

Conclusion

• MAINTAINING STRONG PRODUCTION PROFILE FY 08/09

• CONTINUED EXPANSION AT LANGER HEINRICH (STAGE III)

• SUSTAINED DEVELOPMENT FROM PROJECT PIPELINESUSTAINED DEVELOPMENT FROM PROJECT PIPELINE– progress Mt Isa and Angela Projects for development start 2012+

• FOCUSSED M&A ACTIVITYFOCUSSED M&A ACTIVITY– opportunity to establish a global uranium mining house

• URANIUM MARKET STRENGTHENING

• STRONG BALANCE SHEET

42

PALADIN ENERGY LTd

Q ti ?Questions?

43

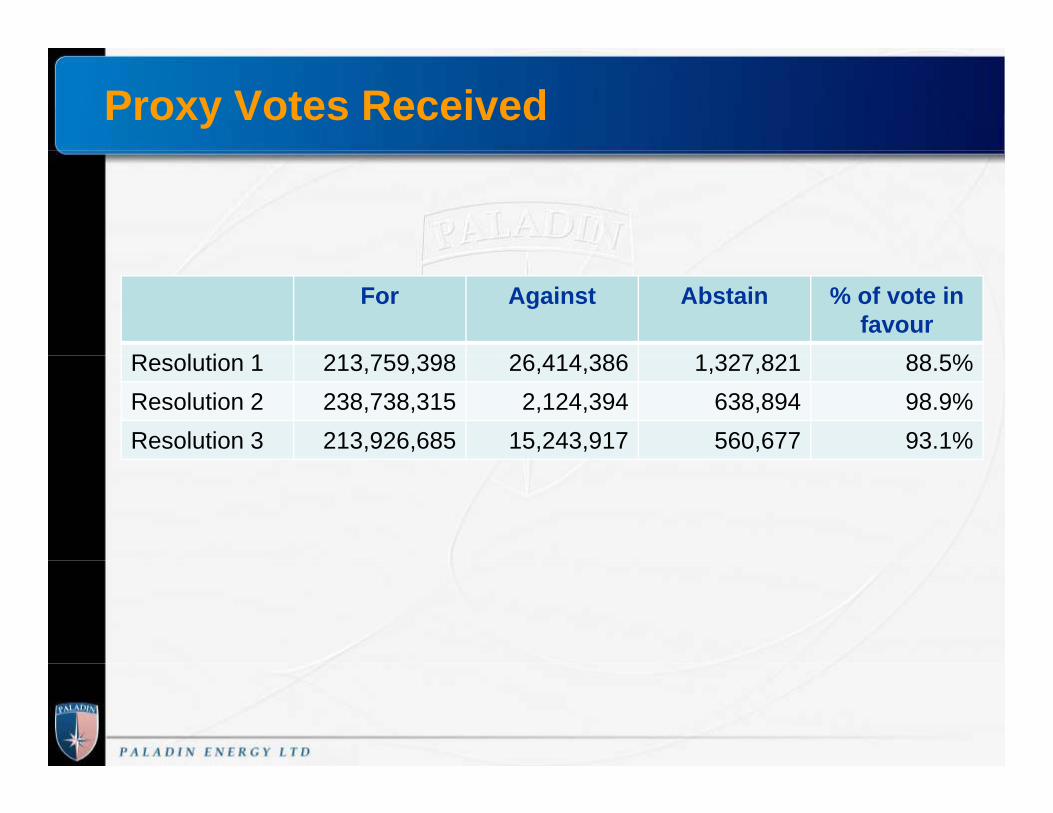

Proxy Votes Received

For Against Abstain % of vote infavour

R l ti 1 213 759 398 26 414 386 1 327 821 88 5%Resolution 1 213,759,398 26,414,386 1,327,821 88.5%Resolution 2 238,738,315 2,124,394 638,894 98.9%Resolution 3 213,926,685 15,243,917 560,677 93.1%

Top Related