Languages

Pages

Legal

The Global Financial Crisis and Its Impacts on Energy

Insurance Markets Trends & Challenges

Robert P. Hartwig, Ph.D., CPCU, PresidentInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 [email protected] www.iii.org

Insurance Information Institute

April 2, 2009

Presentation Outline

• The Global Economic Storm: What Weakening Economy and the Financial Crisis Mean for the P/C Insurance Industry and Energy Concerns Recession, Growth & Insurance

• Economic Stimulus Package: Worldwide Spending Programs Impacts & Implications for P/C Insurers and the Energy Sector

• Insurer Financial Strength & Ratings Insurers vs. Banks: A Difference of Approach to Risk Management

• Energy Market Review Capacity, Rating, Exposure, Profitability, Reinsurance, ART The Financial Crisis: Global Energy Supply, Demand and Investment

• Insurance Industry Financial Performance• Capital & Capacity• Regulatory Response to Crisis

Emerging Blueprint for Insurance Regulatory Overhaul

THE GLOBAL ECONOMIC

STORMWhat Weakening Economies and the Financial Crisis Mean for the

Insurance Industry &Energy Concerns

Real GDP By Market 2007-2010F(% change from previous year)

2.6%

2.0%

2.0% 3.

0%

11.9

%

0.7% 1.0%

-0.7

%

1.3%

0.7%

9.0%

-2.1

%

-2.5

%

-4.1

% -2.6

%

-2.7

%

6.8%

0.9%

1.0%

0.9% 1.

9%

0.8%

8.0%

2.6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Euro Area Germany Japan US UK China

2007 2008E 2009F 2010F

Source: Blue Chip Economic Indicators, 3/10/09 edition.

All major economies except China and Brazil are in recession.

Steep declines in GDP will negatively impact exposure growth on a global scale

Real GDP for Largest European Economies & Euro Area, 2007-2010F, (% change from prior yr.)

2.6% 3.

0%

2.1%

3.5%

2.8%

0.7% 1.

0%

0.7%

0.7%

2.1%

1.3%

-2.1

%

-2.5

%

-2.7

%

-1.8

% -1.4

%

-1.5

%

0.9% 1.0%

0.8% 1.

0%

0.9% 1.0%

2.6%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Euro Area Germany UK France Netherlands Belgium

2007 2008E 2009F 2010F

Source: Blue Chip Economic Indicators, 3/10/09 edition.

All European economies are in recession

3.7

%

0.8

% 1.6

% 2.5

% 3.6

%

3.1

%

2.9

%

0.1

%

4.8

%

4.8

%

0.9

%

2.8

%

-0.5

%

-2.0

%

0.5

% 1.8

%

2.3

%

2.8

%

2.9

%

3.1

%

-5.3%-6.2%

-0.2%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

US Real GDP Growth*

*Yellow bars are Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 3/09; Insurance Information Institute.

Recession began in December 2007. Economic toll of credit crunch, housing

slump, labor market contraction is growing

The Q4:2008 decline was the steepest since the

Q1:1982 drop of 6.4%

Length of US Recessions,1929-Present*

43

13

811 10

810 11

16

6

16

8 8

16

0

5

10

15

20

25

30

35

40

45

50

Aug.1929

May1937

Feb.1945

Nov.1948

July1953

Aug.1957

Apr.1960

Dec.1969

Nov.1973

Jan.1980

Jul.1981

Jul.1990

Mar.2001

Dec.2007

* As of April 2009

Sources: National Bureau of Economic Research; Insurance Information Institute.

Current recession began in Dec. 2007 and is already the longest since 1981. If is now tied for the longest recession since the Great Depression.

Months in Duration

“We will rebuild. We will recover.”

--President Barack Obama addressing a joint session

of Congress

February 24, 2009

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

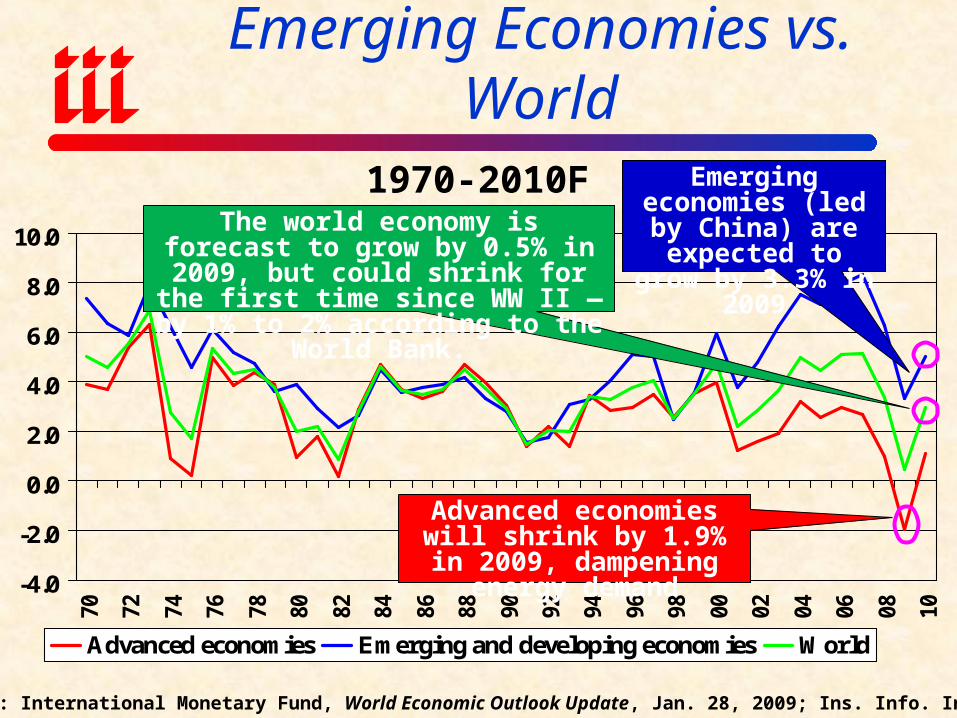

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

Advanced economies Emerging and developing economies World

1970-2010F

Source: International Monetary Fund, World Economic Outlook Update, Jan. 28, 2009; Ins. Info. Institute.

Emerging economies (led by China) are

expected to grow by 3.3% in 2009

GDP Growth: Advanced & Emerging Economies vs. World

Advanced economies will shrink by 1.9% in 2009,

dampening energy demand

The world economy is forecast to grow by 0.5% in 2009, but could shrink for the first time since WW II —by 1% to

2% according to the World Bank.

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

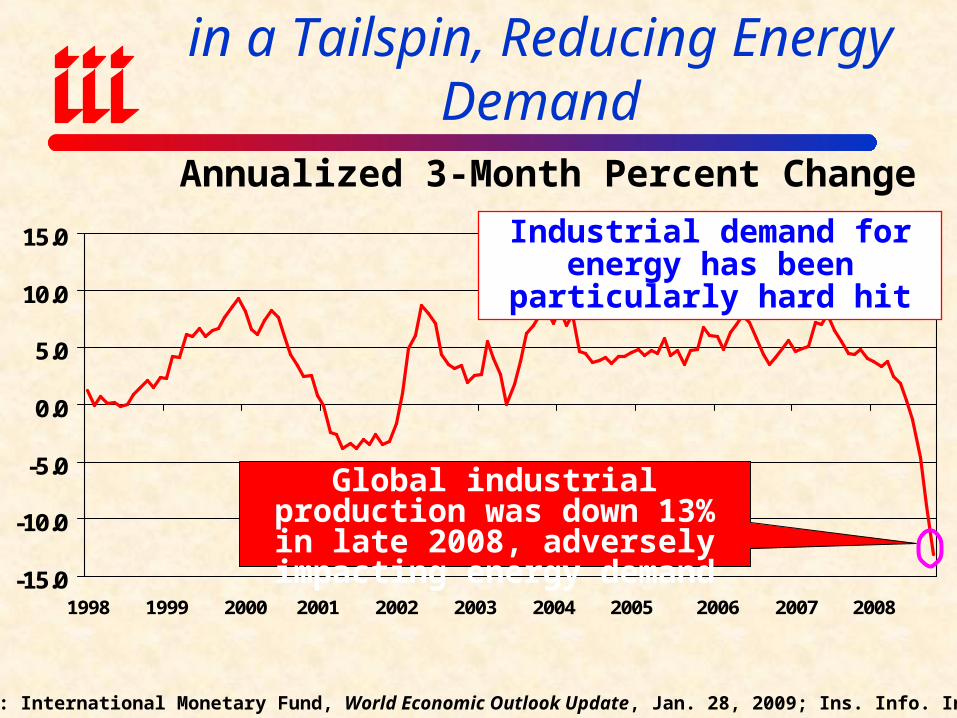

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Annualized 3-Month Percent Change

Source: International Monetary Fund, World Economic Outlook Update, Jan. 28, 2009; Ins. Info. Institute.

Global Industrial Production Is in a Tailspin, Reducing Energy Demand

Global industrial production was down 13% in late 2008, adversely

impacting energy demand

Industrial demand for energy has been particularly hard hit

16.916.916.6

17.117.5

17.817.4

16.516.1

13.1

10.9

12.7

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09F 10F

Weakening economy, credit crunch are hurting auto sales; Gas prices less of a factor now.

New auto/light truck sales are expected to experience a net drop of 6.0 million units annually by 2009 compared

with 2005, a decline of 35.5% and the lowest level

since the late 1960s

Impacts of falling auto sales will have a less pronounced effect on auto insurance exposure growth

than problems in the housing market will on home insurers

Auto/Light Truck Sales,1999-2010F (Millions of Units)

Source: US Department of Commerce; Blue Chip Economic Indicators (2/09); Insurance Information Inst.

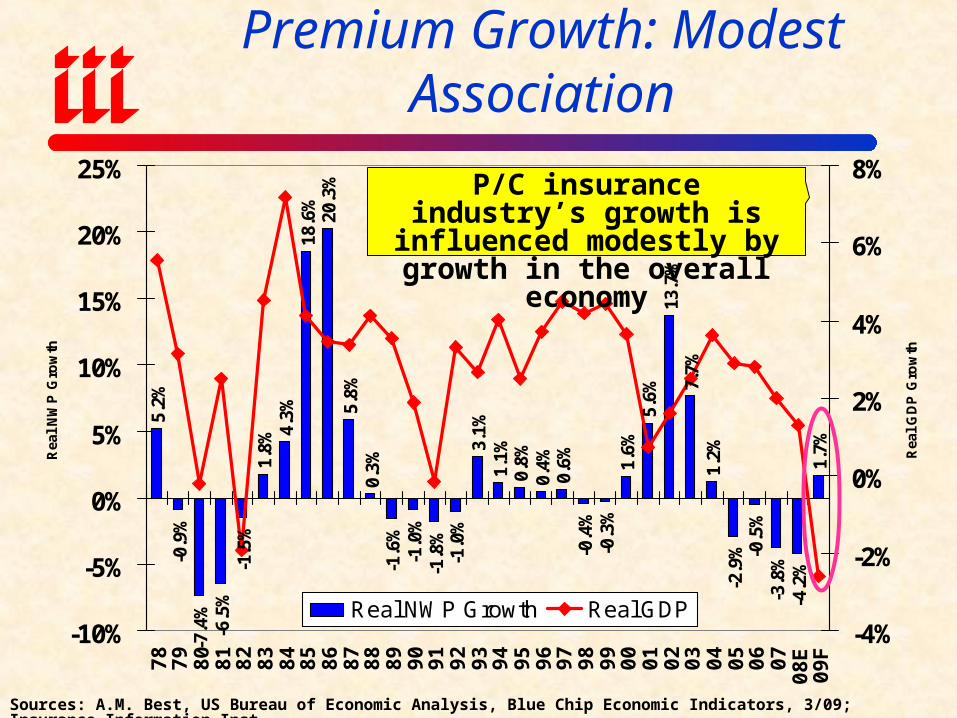

5.2%

-0.9

%-7

.4%

-6.5

%-1

.5%

1.8%

4.3%

18.6

%20

.3%

5.8%

0.3%

-1.6

%-1

.0%

-1.8

%-1

.0%

3.1%

1.1%

0.8%

0.4%

0.6%

-0.4

%-0

.3%

1.6%

5.6%

13.7

%7.

7%1.

2%-2

.9% -0

.5%

-3.8

%-4

.2%

1.7%

-10%

-5%

0%

5%

10%

15%

20%

25%7

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

8E

09

F

Rea

l N

WP

Gro

wth

-4%

-2%

0%

2%

4%

6%

8%

Rea

l G

DP

Gro

wth

Real NWP Growth Real GDP

Real GDP Growth vs. Real P/C Premium Growth: Modest Association

P/C insurance industry’s growth is influenced modestly by growth

in the overall economy

Sources: A.M. Best, US Bureau of Economic Analysis, Blue Chip Economic Indicators, 3/09; Insurance Information Inst.

Change in Producer Prices for Construction vs. Consumer Prices, 2003 - 2008

100

110

120

130

140

150

12/03 12/04 12/05 12/06 12/07

PPI for inputs to construction industries: 33%

Consumer price index: 14%

12/08

Source: Associated General Contractors from BLS (CPI, PPI)12

Dec. 2008

The inflationary spike of 2008 has been reversed—for now—easing concerns over claims severities

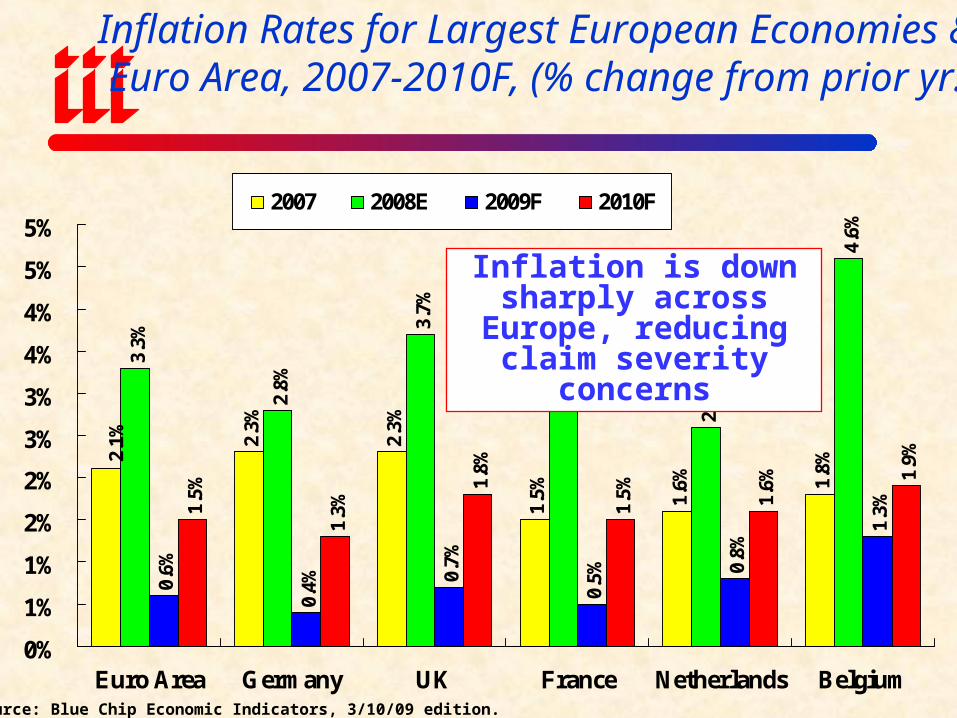

Inflation Rates for Largest European Economies & Euro Area, 2007-2010F, (% change from prior yr.)

2.3%

2.3%

1.5% 1.6% 1.

8%

3.3%

2.8%

3.7%

2.8%

2.6%

4.6%

0.6%

0.4% 0.

7%

0.5% 0.

8%

1.3%1.

5%

1.3%

1.8%

1.5% 1.6% 1.

9%2.1%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

5%

Euro Area Germany UK France Netherlands Belgium

2007 2008E 2009F 2010F

Source: Blue Chip Economic Indicators, 3/10/09 edition.

Inflation is down sharply across Europe, reducing claim severity concerns

THE $2.75 TRILLION GLOBAL ECONOMIC

STIMULUS Countries Trying to Spend Their Way Out of Recession Will Need More Energy &

More Insurance

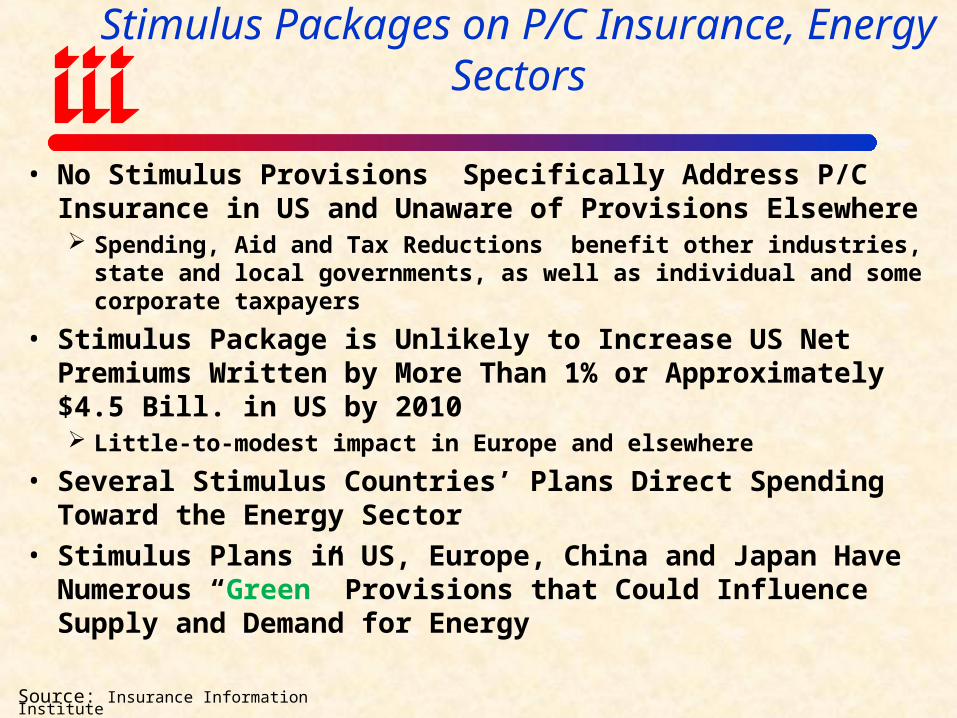

Summary of Short-Run Impacts of Global Stimulus Packages on P/C Insurance, Energy Sectors

• No Stimulus Provisions Specifically Address P/C Insurance in US and Unaware of Provisions Elsewhere Spending, Aid and Tax Reductions benefit other industries, state and local

governments, as well as individual and some corporate taxpayers

• Stimulus Package is Unlikely to Increase US Net Premiums Written by More Than 1% or Approximately $4.5 Bill. in US by 2010 Little-to-modest impact in Europe and elsewhere

• Several Stimulus Countries’ Plans Direct Spending Toward the Energy Sector

• Stimulus Plans in US, Europe, China and Japan Have Numerous “Green” Provisions that Could Influence Supply and Demand for Energy

Source: Insurance Information Institute

$5

.8

$2

.0

$1

30

.4

$3

3.0

$7

5.3

$8

.0

$7

.6

$6

.9

$2

.8

$1

.8

$5

86

.1

$4

85

.9

$11

.3

$2

8.0

$7

.4

$1

3.7

$3

6.8

$787

$4

0.8

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

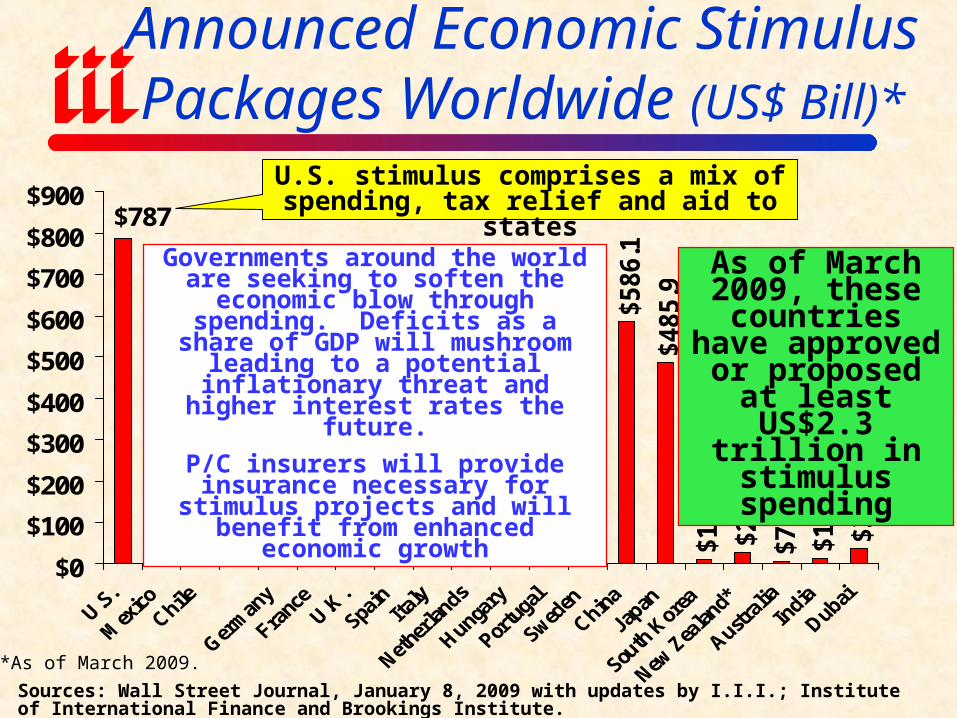

Announced Economic Stimulus Packages Worldwide (US$ Bill)*

Sources: Wall Street Journal, January 8, 2009 with updates by I.I.I.; Institute of International Finance and Brookings Institute.

U.S. stimulus comprises a mix of spending, tax relief and aid to states

*As of March 2009.

Governments around the world are seeking to soften the economic blow

through spending. Deficits as a share of GDP will mushroom leading to a

potential inflationary threat and higher interest rates the future.

P/C insurers will provide insurance necessary for stimulus projects and will benefit from enhanced economic growth

As of March 2009, these countries

have approved or proposed at least US$2.3 trillion in stimulus spending

$ Billions

$221.3

$54.2

$94.1

$12.4

$0 $200 $400 $600 $800 $1,000

India

Japan

China

Europe

US $787B Total

Source: “Energy Sector Looks for Private, Public Help,” WSJ, 3/9/09, p. A2 from HSBC, New Energy Finance; Ins. Info. Inst.

Green Energy Spending: An Important Component of Some Stimulus Plans

European green energy stimulus spending = $54.2B

$634.1B Total

$586.1B Total

$485.9B Total

$13.7B Total

Green energy stimulus spending totals $382B in US, Japan and Europe, or 18.1% of their combined $2.1 trillion in stimulus spending

US Economic Stimulus Package: Where the $787B Goes—5% to Energy Projects

Tax Relief, $288 , 38%

State & Local Fiscal Relief, $144 , 18%

Infrastructure & Science, $111 , 14%

Protecting the Vulnerable, $81 , 10%

Health Care, $59 , 7% Education & Training, $53 , 7%

Energy, $43 , 5%

Other, 8, 1%

US stimulus package allocates $43B or 5% or total spending to energy

programs

Source: http://www.recovery.gov/ accessed 2/18/09; Insurance Information Institute.

$ Billions

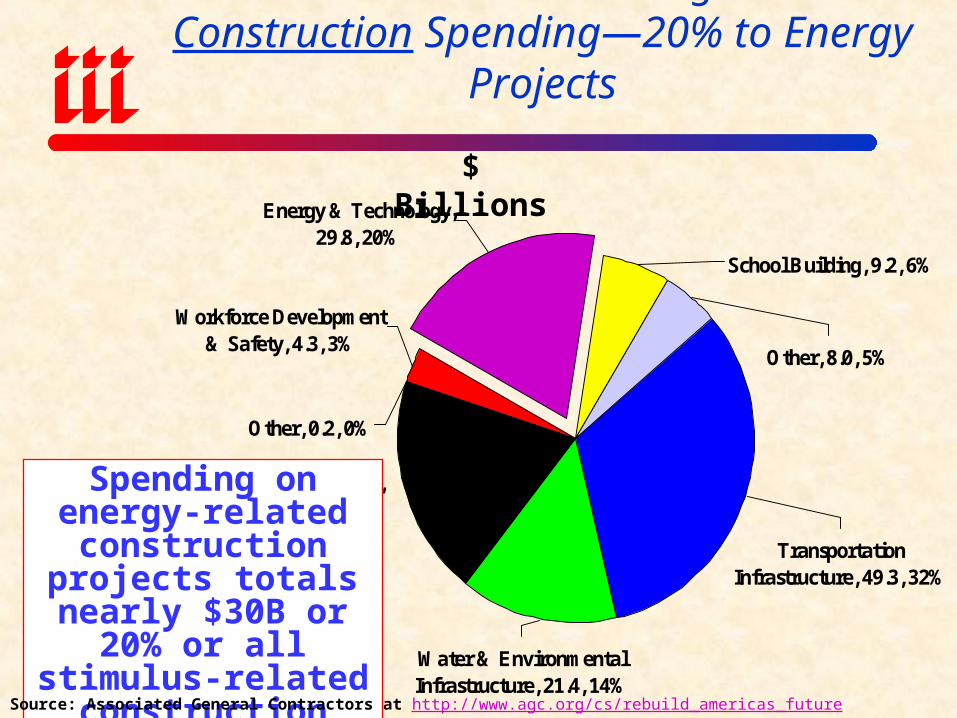

US Economic Stimulus Package: $143.4 in Construction Spending—20% to Energy Projects

Transportation Infrastructure, 49.3, 32%

Water & Environmental Infrastructure, 21.4, 14%

Building Infrastructure, 29.6, 20%

Other, 0.2, 0%

Workforce Development & Safety, 4.3, 3%

Energy & Technology, 29.8, 20%

School Building, 9.2, 6%

Other, 8.0, 5%

Spending on energy-related construction projects totals nearly $30B or 20% or all

stimulus-related construction spending

Source: Associated General Contractors at http://www.agc.org/cs/rebuild_americas_future (2/18/09); Insurance Info. Inst..

$ Billions

$542

$160$150$98

$60$33

$0

$100

$200

$300

$400

$500

$600

2004 2005 2006 2007 2008 2030

Current investment in green energy falls far short of what some believe is necessary to address climate change issue

Annual investment needed through 2030 in renewable energy and energy efficiency to keep atmospheric CO2 concentration below 450 parts per million—an amount many scientists claim is necessary to prevent serious

consequences from climate change

Global Green Energy Spending* ($ Billion)

*Estimated from source below.Source: “Energy Sector Looks for Private, Public Help,” WSJ, 3/9/09, p. A2; New Energy Finance interpretation of International Energy Agency data; Ins. Info. Inst.

Stimulus: Reading The Economic Tea Leaves for the Next 4 to 8 Years

Source: Insurance Information Institute

• Growing Role of Government: 2009 Stimulus Packages and Other Likely Spending Initiatives in US and Elsewhere Guarantee Government Will Play a Much Larger Role Than at Any Other Time in Recent History Every industry, including insurance, will and must attempt to

maximize direct and indirect benefits from this paradigm shift• Obama Administration Priorities: Stimulus Package

Acts as “Economic Tea Leaf” on the Administration’s Fiscal Priorities for the Next Several Years

• These Include: Alternative Energy Environmental Spending Health Care Aging/New Infrastructure Aid to States

• Global Financial Services Regulatory Reform Includes insurance

FINANCIAL STRENGTH &

RATINGS Industry Has Weathered

the Storms Well

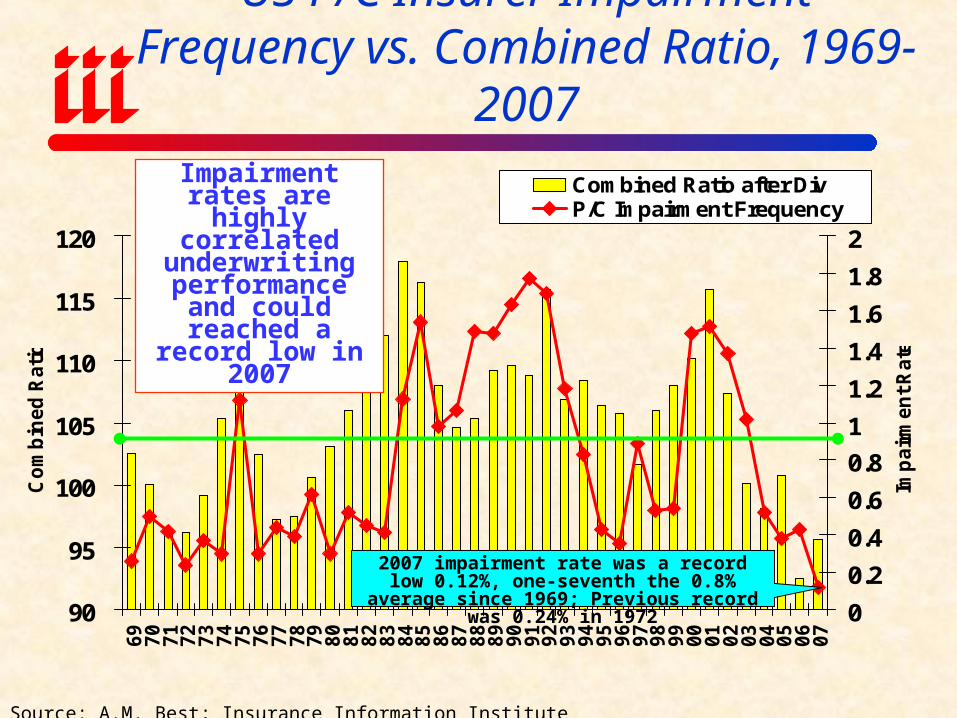

US P/C Insurer Impairment Frequency vs. Combined Ratio, 1969-2007

90

95

100

105

110

115

120

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

Co

mb

ined

Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Imp

air

men

t R

ate

Combined Ratio after DivP/C Impairment Frequency

Impairment rates are highly correlated

underwriting performance and could reached a

record low in 2007

Source: A.M. Best; Insurance Information Institute

2007 impairment rate was a record low 0.12%, one-seventh the 0.8% average since 1969;

Previous record was 0.24% in 1972

Summary of A.M. Best’s P/C Insurer Ratings Actions in 2008*

Under Review, 63 , 4.3%

Upgraded, 59 , 4.0%

Initial, 41 , 2.8%

Other, 59 , 4.0%

Affirm, 1,183 , 81.0%

Downgraded, 55 , 3.8%

*Through December 19.Source: A.M. Best.

24

Despite financial market turmoil, high cat losses and a soft market in 2008, 81% of ratings actions by A.M. Best

were affirmations; just 3.8% were downgrades

and 4.0% upgrades

P/C insurance is by design a resilient in business. The dual threat of financial

disasters and catastrophic losses are

anticipated in the industry’s risk

management strategy.

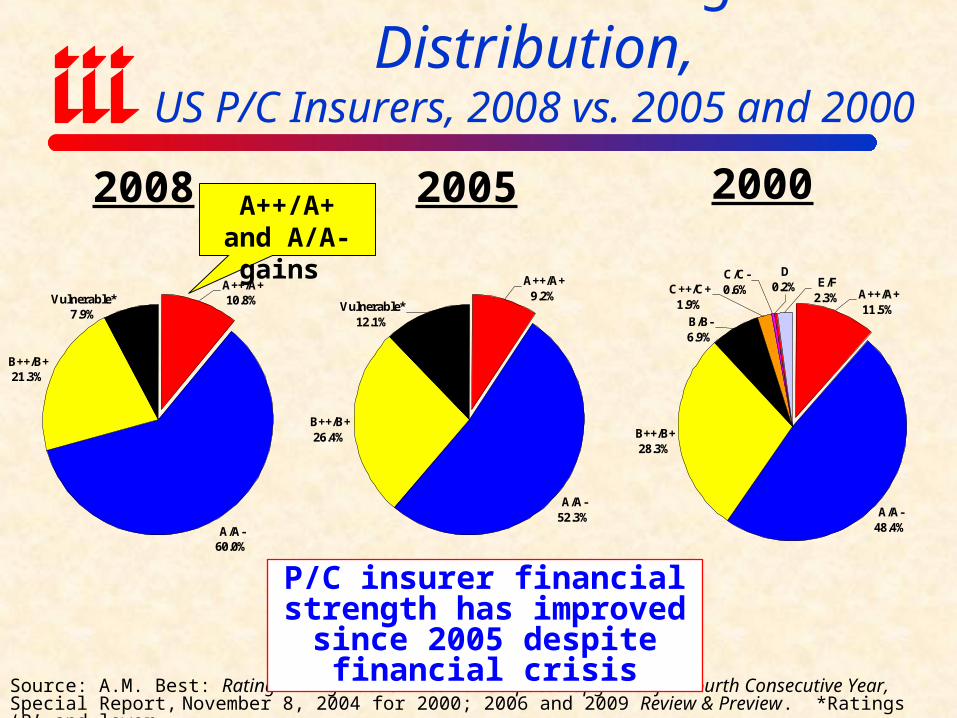

Historical Ratings Distribution,US P/C Insurers, 2008 vs. 2005 and 2000

Source: A.M. Best: Rating Downgrades Slowed but Outpaced Upgrades for Fourth Consecutive Year, Special Report, November 8, 2004 for 2000; 2006 and 2009 Review & Preview. *Ratings ‘B’ and lower.

A/A-48.4%

D0.2%C++/C+

1.9%

E/F2.3% A++/A+

11.5%

C/C-0.6%

B++/B+28.3%

B/B-6.9%

2008 2005

P/C insurer financial strength has improved since 2005 despite financial crisis

A/A-52.3%

A++/A+9.2%

B++/B+26.4%

Vulnerable*12.1%

A/A-60.0%

A++/A+10.8%

B++/B+21.3%

Vulnerable*7.9%

2000A++/A+ and A/A- gains

Reasons for US P/C Insurer Impairments, 1969-2005

*Includes overstatement of assets.

Source: A.M. Best: P/C Impairments Hit Near-Term Lows Despite Surging Hurricane Activity, Special Report, Nov. 2005;

Catastrophe Losses8.6%

Alleged Fraud11.4%

Deficient Loss

Reserves/In-adequate Pricing62.8%

Affiliate Problems

8.6%

Rapid Growth

8.6%

2003-2005 1969-2005

Deficient reserves,

CAT losses are more important factors in

recent years

Reinsurance Failure3.5%

Rapid Growth16.5%

Misc.9.2%

Affiliate Problems

5.6%

Sig. Change in Business

4.6%

Deficient Loss

Reserves/In-adequate Pricing38.2%

Investment Problems*

7.3%

Alleged Fraud8.6%

Catastrophe Losses6.5%

Critical Differences Between P/C

Insurers and BanksSuperior Risk Management Model

& Low Leverage Makea Big Difference

$600

$106

$780

$205

$0

$100

$200

$300

$400

$500

$600

$700

$800

Banks Insurers

Losses as of Sept 2008

Total expected losses

Financial Institutions Globally FacingHuge Losses from the Credit Crunch*

*Global losses since the beginning of 2007.Source: IMF Global Financial Stability Report, October 2008, IIF, Bloomberg, cited in a presentation by Thomas Hess (Chief Economist, Swiss Re) October 23, 2008, accessed via Geneva Association web site.

Billions

The IMF estimates total “credit- turmoil-related” losses will

eventually amount to $1.4 trillion

$205B or 20.8% of estimated total (bank+insurer) losses will be

sustained by insurers worldwide

28

How Insurance Industry Stability Has Benefitted Consumers

BOTTOM LINE:• Insurance Markets—Unlike Banking—Are Operating

Normally• The Basic Function of Insurance—the Orderly Transfer

of Risk from Client to Insurer—Continues Uninterrupted• This Means that Insurers Continue to:

Pay claims (whereas 42 banks have gone under as of 3/13) The Promise is Being Fulfilled

Renew existing policies (banks are reducing and eliminating lines of credit)

Write new policies (banks are turning away people who want or need to borrow)

Develop new products (banks are scaling back the products they offer)

Source: Insurance Information Institute29

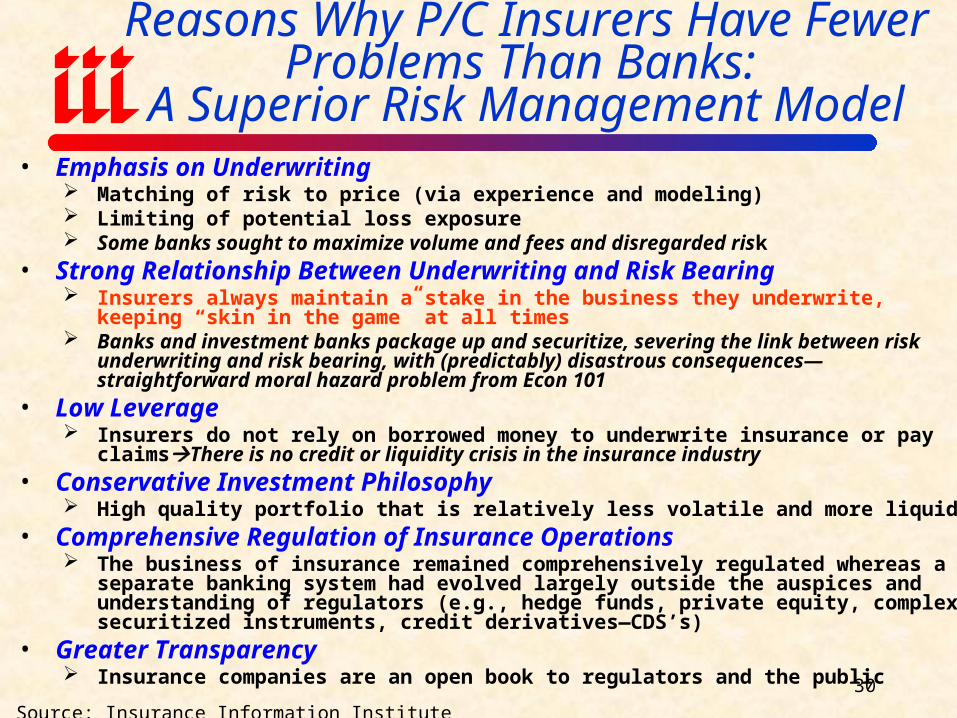

• Emphasis on Underwriting Matching of risk to price (via experience and modeling) Limiting of potential loss exposure Some banks sought to maximize volume and fees and disregarded risk

• Strong Relationship Between Underwriting and Risk Bearing Insurers always maintain a stake in the business they underwrite, keeping “skin in the game”

at all times Banks and investment banks package up and securitize, severing the link between risk

underwriting and risk bearing, with (predictably) disastrous consequences—straightforward moral hazard problem from Econ 101

• Low Leverage Insurers do not rely on borrowed money to underwrite insurance or pay claimsThere is no

credit or liquidity crisis in the insurance industry• Conservative Investment Philosophy

High quality portfolio that is relatively less volatile and more liquid• Comprehensive Regulation of Insurance Operations

The business of insurance remained comprehensively regulated whereas a separate banking system had evolved largely outside the auspices and understanding of regulators (e.g., hedge funds, private equity, complex securitized instruments, credit derivatives—CDS’s)

• Greater Transparency Insurance companies are an open book to regulators and the public

Source: Insurance Information Institute30

Reasons Why P/C Insurers Have Fewer Problems Than Banks:

A Superior Risk Management Model

ENERGY MARKET REVIEW

Global Energy Business Is Deeply Impacted by

Crisis, but Other Factors Matter Too

Key Trends

Capacity & RatingExposure

ProfitabilityReinsurance

Global Energy Insurance Markets: Key Trends

INSURANCE CAPACITYAggregate commercial property/casualty (nonlife) capacity fell sharply in

2008 due to• Reduced Asset Values• Higher Underwriting Losses• Sharply Lower Investment Returns

Surprisingly, overall energy market capacity levels for 2009 have increased, despite start of early stage of market hardening, financial crisis and dislocations of key competitors

Higher capacity and basic laws of supply and demand temper extent of market hardening and limit price gains

Capacity freed up due in part to reduced construction activity and reduced business interruption levels

Fallout from Gulf of Mexico windstorm causes some supply issues for offshore and onshore risks

Source: Willis Energy Market Review March 2009

Upstream Operating Underwriting Capacities, 2000-08 (Excl. GOM)

Source: Willis Energy Market Review: March 2009

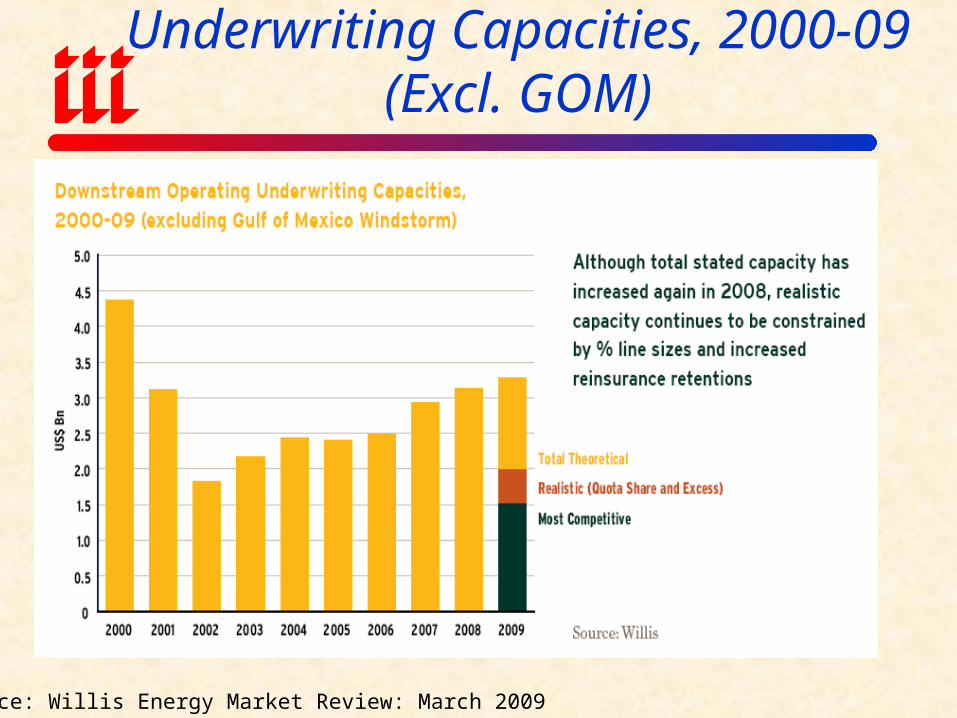

Downstream Operating Underwriting Capacities, 2000-09 (Excl. GOM)

Source: Willis Energy Market Review: March 2009

Upstream Capacities and Average Rating Levels, 1993-2009 (Excl. GOM)

Source: Willis Energy Market Review: March 2009

Onshore Capacities and Average Rating Levels, 1993-2009 (Excl. GOM)

Source: Willis Energy Market Review: March 2009

Total Theoretical Liability Capacity, 2000-09

Source: Willis Energy Market Review: March 2009

Global Energy Insurance Markets: Key Trends

INSURED EXPOSUREGlobal economic downturn, reduced energy demand and

collapse of oil prices hit energy industry project activity and asset values with negative impact on energy insurers’ exposure and therefore premium income levels

Impact is especially acute for industrial energy demandCredit crisis impacting project viability as wellBOTTOM LINE IN 2009: Crisis will have little impact on

long-run demand and supply for energy and energy assets• Global energy demand will begin to rebound in late 2009• Fuel prices are already beginning to rise• Insurance industry will be able to meet the short, intermediate and

long-term demands despite current challenges

Source: Willis Energy Market Review March 2009; Insurance Information Institute.

Global Energy Insurance Markets: Key Trends

PROFITABILITYSharp decline in investment returns in 2008, unlikely to

turnaround anytime soonLoss of investment return necessarily increases pressure on

(re)insurers to generate underwriting profitsMany insurers will also need to protect capital in 2009 via

increased reliance on reinsuranceHigher cost of capital could be a major issue if capital raises

are necessary among for insurers and reinsurersBOTTOM LINE IN 2009: Stable and profitable energy sector

(for the most part) particularly for low Nat Cat business• Movement toward disciplined underwriting is necessary

Source: Willis Energy Market Review March 2009; Insurance Information Institute.

Energy Losses vs. Global Energy Premium Income 1990-2008*

*Figures include both insured and uninsured losses

Source: Willis Energy Market Review: March 2009

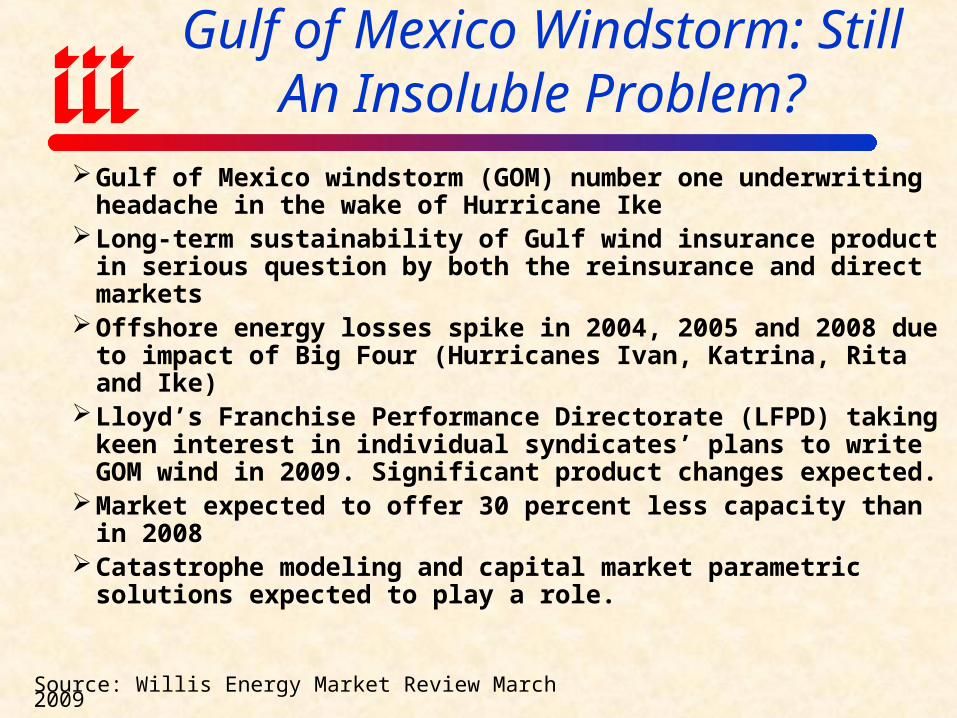

Gulf of Mexico Windstorm: Still An Insoluble Problem?

Gulf of Mexico windstorm (GOM) number one underwriting headache in the wake of Hurricane Ike

Long-term sustainability of Gulf wind insurance product in serious question by both the reinsurance and direct markets

Offshore energy losses spike in 2004, 2005 and 2008 due to impact of Big Four (Hurricanes Ivan, Katrina, Rita and Ike)

Lloyd’s Franchise Performance Directorate (LFPD) taking keen interest in individual syndicates’ plans to write GOM wind in 2009. Significant product changes expected.

Market expected to offer 30 percent less capacity than in 2008

Catastrophe modeling and capital market parametric solutions expected to play a role.

Source: Willis Energy Market Review March 2009

Reinsurance & Alternative Risk

Transfer

Capacity is Down, Demand is Up

Reinsurance Market TrendsAmid global capital markets turmoil and economic downturn

global reinsurance industry has faired relatively well (with a small number of exceptions)

Capacity, however, is down due to investment issuesBut reinsurers seeking price increases as of 1 January and risk

appetite more constrained (e.g., U.S. catastrophe risk)Primary insurers exploring lower retentions and other

reinsurance mechanisms to protect and enhance their capital positions

Increasing syndication of risk as insurers seek to use portfolio diversification to mitigate counterparty exposure

Opportunity for traditional reinsurance market to win back market share as some alternative forms of risk transfer have dried up

Source: Willis Energy Market Review March 2009; Insurance Information Institute.

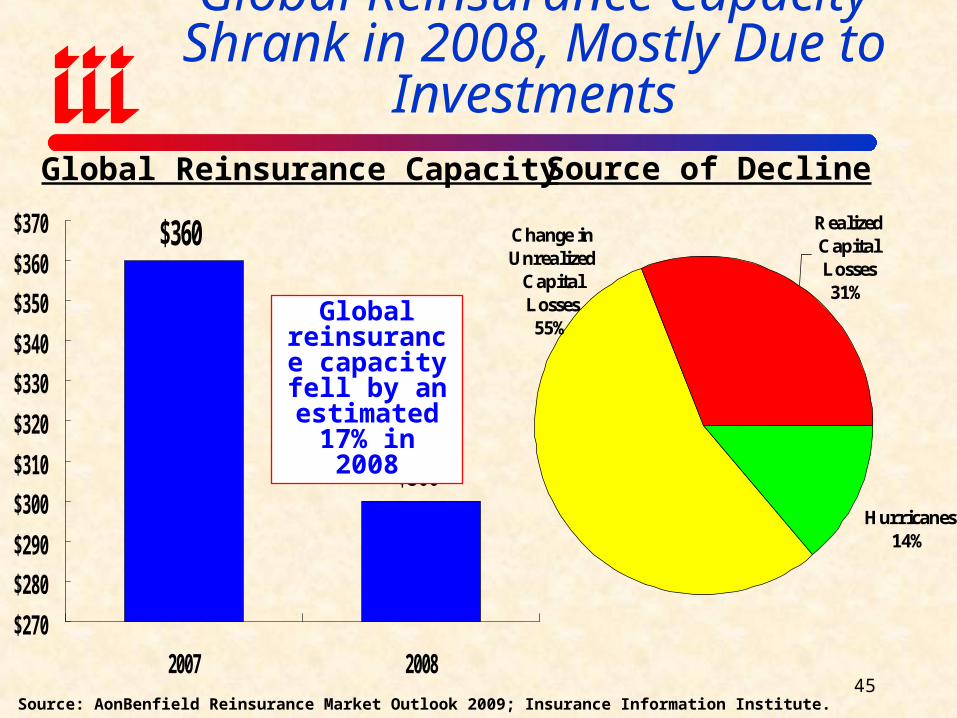

Global Reinsurance Capacity Shrank in 2008, Mostly Due to Investments

$360

$300

$270

$280

$290

$300

$310

$320

$330

$340

$350

$360

$370

2007 2008

Global Reinsurance Capacity

Global reinsurance

capacity fell by an estimated 17% in 2008

45

Hurricanes14%

Change in Unrealized

Capital Losses55%

Realized Capital Losses31%

Source of Decline

Source: AonBenfield Reinsurance Market Outlook 2009; Insurance Information Institute.

Catastrophe Bond and Sidecar Issuance, 2004-2008

$1.14 $1.50

$4.69

$7.62

$2.73

$0.00

$2.33

$3.85

$1.75

$0.28$0

$2

$4

$6

$8

$10

2004 2005 2006 2007 2008

$ Billions

The credit crisis and decline in global capital have taken their

toll on alternative forms of catastrophe risk transfer

46Source: AonBenfield Reinsurance Market Outlook 2009; Insurance Information Institute.

The Global Financial Crisis Affects Energy Industry Supply and Demand & Insurance

Exposure

Severe Recession is Depressing US Energy Demand: Change 2009 vs. 2008

-2.2%

-1.3%-1.7% -1.7%

-6.4%-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

Oil Natural Gas Electricty(Industrial)

Electricty (All) Coal forElectricity

Sources: Energy Information Administration.

Industrial consumption of electricity has

experienced the most severe declines

Percentage Change in Consumption, 2009 vs. 2008

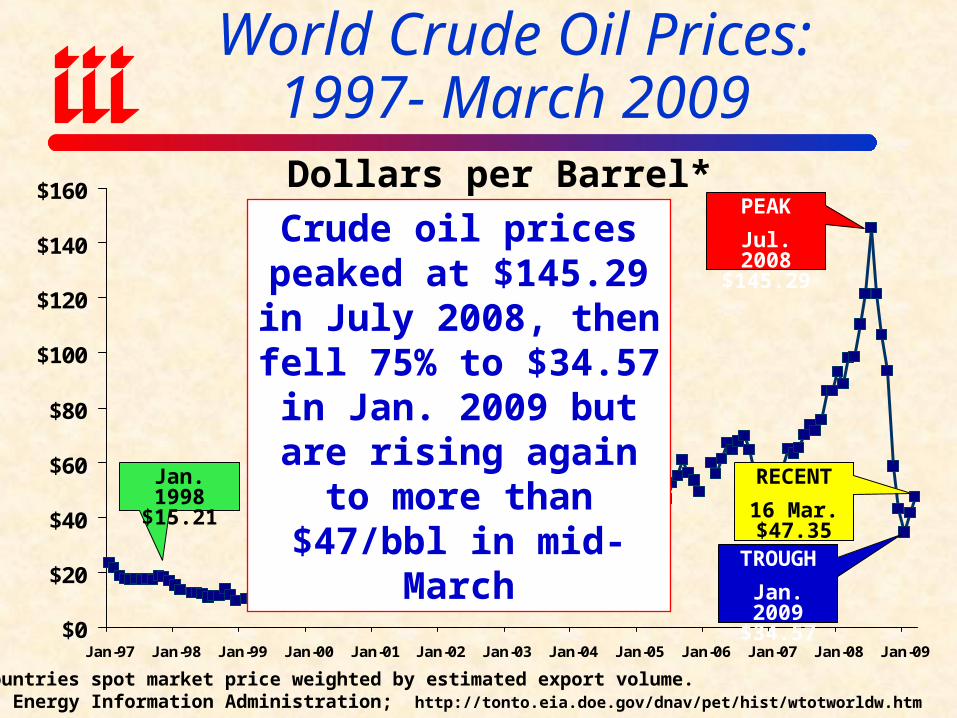

World Crude Oil Prices: 1997- March 2009

*All countries spot market price weighted by estimated export volume. Source: Energy Information Administration; http://tonto.eia.doe.gov/dnav/pet/hist/wtotworldw.htm

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

Dollars per Barrel*

Crude oil prices peaked at $145.29 in July 2008, then fell 75% to $34.57

in Jan. 2009 but are rising again to more than

$47/bbl in mid-MarchJan. 1998

$15.21

PEAK

Jul. 2008 $145.29

TROUGH

Jan. 2009 $34.57

RECENT

16 Mar. $47.35

0%

2%

4%

6%

8%

10%

12%

14%

83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Percentage of GDP

Source: Energy Information Administration, Short-Term Energy Outlook, March 10, 2009; Ins. Info. Inst.

US Energy Expenditures as a % of GDP Have Been Hurt by Recession

The energy price bubble pushed energy expenditures to 9.9% of GDP in 2008. The bursting of the bubble and recession pushed expenditures down to 7.0% of GDP in 2009.

Recession and 2008 energy price spike sharply

decreased energy demand

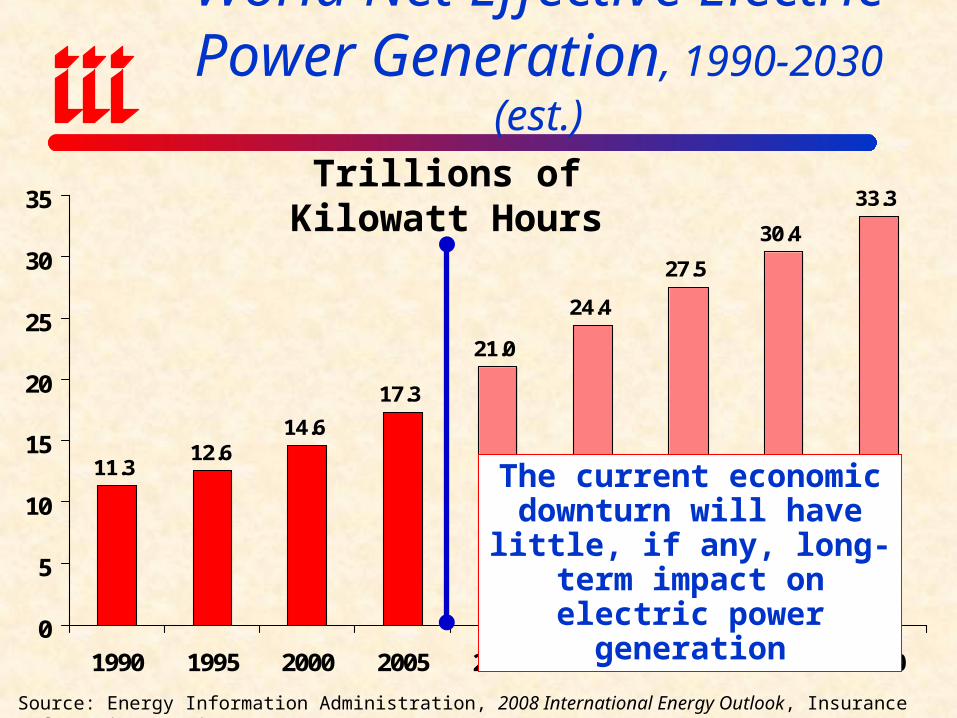

11.3

14.6

17.3

21.0

24.4

27.5

30.4

33.3

12.6

0

5

10

15

20

25

30

35

1990 1995 2000 2005 2010 2015 2020 2025 2030

World Net Effective Electric Power Generation, 1990-2030 (est.)

Source: Energy Information Administration, 2008 International Energy Outlook, Insurance Information Institute.

The current economic downturn will have little, if any, long-term impact on electric power generation

Trillions of Kilowatt Hours

Electricity Supply Infrastructure: Despite Crisis, Huge Investments Needed

Along With Insurance: 2001-2030 (Est.)

$ Billions

$1,351

$1,876

$809

$377

$744

$258

$609$783$799

$1,913

$0

$500

$1,000

$1,500

$2,000

$2,500

Eu

rop

e

No

rth

Am

eric

a

Pac

ific

Ru

ssia

Ch

ina

E.

Asi

a

S.

Asi

a

Lat

inA

mer

ica

Mid

dle

Eas

t

Afr

ica

Source: International Atomic Energy Agency , World Outlook for Electricity Investment.

Investments in electricity supply infrastructure

globally are expected to total $9.841 trillion

between 2001 and 2030

European investment could total $1.351 trillion

52

World Energy Supply Infrastructure Investment by Category: 2001-2030 (Est.)

Generation-New, $4,080 , 42%

Generation-Refurbished, $439 , 4%

Transmission, $1,568 , 16%

Distribution, $3,755 , 38%

Generation will account for 46% or $4.5 trillion

of all investment through 2030 to meet

rising demand. Current downturn will have no impact on long-term

global energy demand and the need to develop supply infrastructure

$ Billions

Source: International Atomic Energy Agency , World Outlook for Electricity Investment.

World Electricity Generation by Fuel 2005-2030F

2.63 3.

16 3.42

2

7.15

2

0.76

4

3.75

4 4.99

6

8.38

9

15.3

61

0.95

6

0

2

4

6

8

10

12

14

16

18

Liquids Nuclear Renewables Natural Gas Coal

2005 2010 2015 2020 2025 2030

Source: US Department of Energy Report #:DOE/EIA-0484 ( Sept. 2008); Insurance Information Institute

The sharp increase in generation and the

changing composition of fuel source will influence

insurance demand and the nature of products sold

Trillions of Kilowatt Hours

Natural Gas20%

Renewables18%

Liquids6%

Coal41%

Nuclear15%

2005 2030

World Electricity Generation by Fuel Source Share: 2005 vs. 2030F

Natural Gas25%

Renewables15%

Liquids2%

Coal47%

Nuclear11%

Surprisingly, coal as a source of electricity generation is

expected rise through 2030. CO2, pollution issues?

Source: Insurance Information Institute from data reported in US Department of Energy Report #:DOE/EIA-0484 ( Sept. 2008).

European Electricity Generation,by Fuel: 2005-2030F

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2005 2010 2015 2020 2025 2030

Liquids Coal Natural Gas Renewables Nuclear

Source: US Department of Energy Report #:DOE/EIA-0484 ( Sept. 2008); Insurance Information Institute

Gas, renewables grow, coal shrinks, implying

different insurance needs in Europe

Trillions of Kilowatt Hours

3.303.70

3.97 4.21 4.444.67

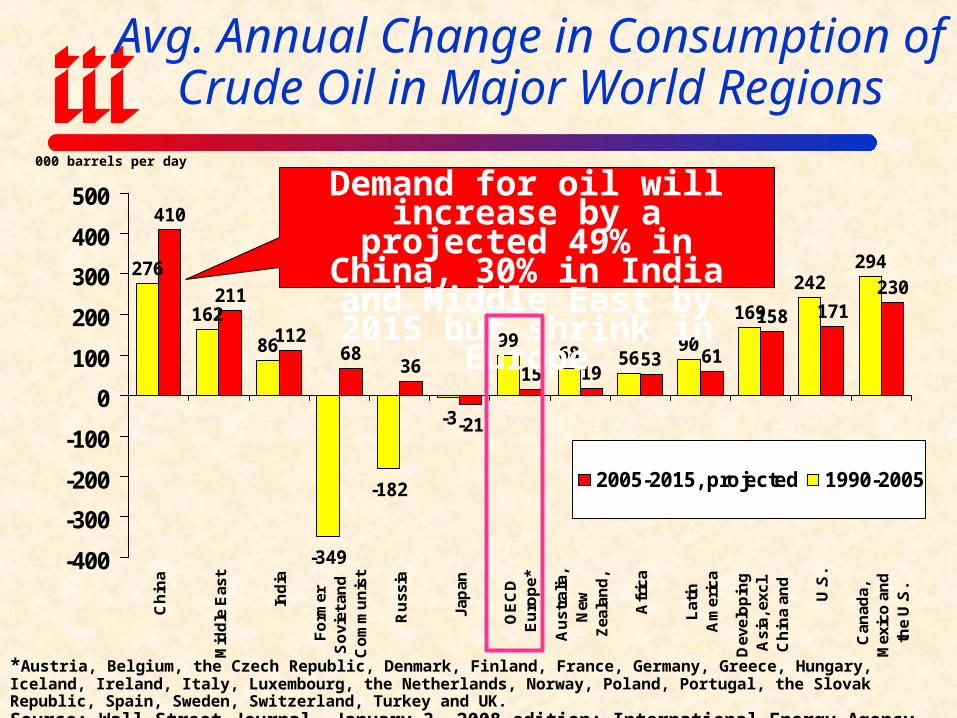

Avg. Annual Change in Consumption of Crude Oil in Major World Regions

171158

61531915

-21

3668

112

211

410

294242

169

905668

99

-3

-182

-349

86

162

276230

-400

-300

-200

-100

0

100

200

300

400

500

Can

ada,

Mex

ico

an

dth

e U

.S.

U.S

.

Dev

elo

pin

gA

sia,

exc

l.C

hin

a an

d

Lat

inA

mer

ica

Afr

ica

Au

stra

lia,

New

Zea

lan

d,

OE

CD

Eu

rop

e*

Jap

an

Ru

ssia

Fo

rmer

So

viet

an

dC

om

mu

nis

t

Ind

ia

Mid

dle

Eas

t

Ch

ina

2005-2015, projected 1990-2005

*Austria, Belgium, the Czech Republic, Denmark, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Poland, Portugal, the Slovak Republic, Spain, Sweden, Switzerland, Turkey and UK.Source: Wall Street Journal, January 3, 2008 edition; International Energy Agency

000 barrels per day

Demand for oil will increase by a projected 49% in China, 30%

in India and Middle East by 2015 but shrink in Europe

Lessons from Energy Boom of 2008

Oil/Energy is a Chief Source of Global Economic Instability

LESSONS OF 2008 ENERGY PRICE BUBBLESteeply rising oil/energy prices lead to severe economic

dislocation and hardship on a global scaleReduced economic growth globally (except energy

exporting countries)Fuels InflationMakes investment decisions in exploration more

uncertain Encourages collateral boom in other commoditiesDisastrous for transport sector (e.g., airlines)Food, energy costs are acute problems in poorest parts of

the world Increases the power and wealth of certain unstable

countries (e.g., Iran, Nigeria, Venezuela)Influence on biofuels/alternative energy policies

P/C INSURANCE FINANCIAL

PERFORMANCE

A Resilient Industry in Challenging Times

Profitability

Historically Volatile

P/C Net Income After Taxes1991-2009F ($ Millions)*

$14,

178

$5,8

40

$19,

316

$10,

870

$20,

598

$24,

404 $3

6,81

9

$30,

773

$21,

865

$3,0

46

$30,

029

$61,

940

$5,4

21

-$6,970

$65,

777

$44,

155

$20,

559

$38,

501

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08F

*ROE figures are GAAP; 1Return on avg. surplus. 2008 numbers are annualized based on 9-mos. Actual of $4.066 billion.Sources: A.M. Best, ISO, Insurance Information Inst.

2001 ROE = -1.2%2002 ROE = 2.2%2003 ROE = 8.9%2004 ROE = 9.4%2005 ROE= 9.4%2006 ROE = 12.2%2007 ROAS1 = 12.3%2008 ROAS = 1.1%*

Insurer profits in US and

globally peaked in 2006/2007

62

-5%

0%

5%

10%

15%

20%

25%

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 0608

F09

F10

F

1975: 2.4%

1977:19.0% 1987:17.3% 1997:11.6% 2006:12.2%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years10 Years

9 Years

Note: 2009 figure is actual 9-month result.Sources: ISO; Insurance Information Institute.

2008F: 1.1%

P/C Insurance Industry ROEs,1975 – 2010F*

2010F: 6.0%

2009F: 4.5%

63

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08*

ROE Cost of Capital

ROE vs. Equity Cost of Capital:US P/C Insurance:1991-2008:Q3

*Excludes mortgage and financial guarantee insurers.Source: The Geneva Association, Ins. Information Inst.

The p/c insurance industry fell well short of is cost of capital in 2008

-13.

2 p

ts

US P/C insurers missed their cost of capital by an average 6.7 points from 1991 to 2002, but on

target or better 2003-07

-1.7

pts

+2.

3 p

ts

-9.0

pts

The cost of capital is the rate of return

insurers need to attract and retain

capital to the business

-9.7

pts

64

Presidential Politics & P/C Insurance

How is Profitability Affected by the President’s Political Party?

15.10%10.13%

8.93%8.65%

8.35%7.98%

7.68%6.98%6.97%

5.43%5.03%

4.83%4.43%

3.55%

16.43%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Carter

Reagan II

G.W. Bush II

Nixon

Clinton I

G.H.W. Bush

Clinton II

Reagan I

Nixon/Ford

Truman

Eisenhower I

Eisenhower II

G.W. Bush I

Johnson

Kennedy/Johnson

*ROE for 2008 based on H1 data. Truman administration ROE of 6.97% based on 3 years only, 1950-52.Source: Insurance Information Institute

OVERALL RECORD: 1950-2008*

Democrats 8.05%

Republicans 8.02%

Party of President has marginal bearing on profitability of P/C insurance industry

P/C Insurance Industry ROE byPresidential Administration,1950-2008*

-5%

0%

5%

10%

15%

20%

25%

50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08*

BLUE = Democratic President RED = Republican President

Source: Insurance Information Institute. *2008 based 9-month data.

Tru

man

Nixon/FordKennedy/ Johnson

Eisenhower Carter Reagan/Bush Clinton Bush

P/C Insurance Industry ROE by Presidential Party Affiliation,

1950–2008*

P/C Premium Growth

Primarily Driven by the Industry’s Underwriting Cycle, Not the Economy

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

22%

24%

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

F20

09F

Sources: A.M. Best (historical and forecast), ISO, Insurance Information Institute

Strength of Recent Hard Marketsby NWP Growth

1975-78 1984-87 2000-03Shaded areas denote “hard

market” periods

Net written premiums fell 1.0%

in 2007 (first decline since 1943)

and by 0.4% in 2008, the first back-

to-back decline since 1930-33

69

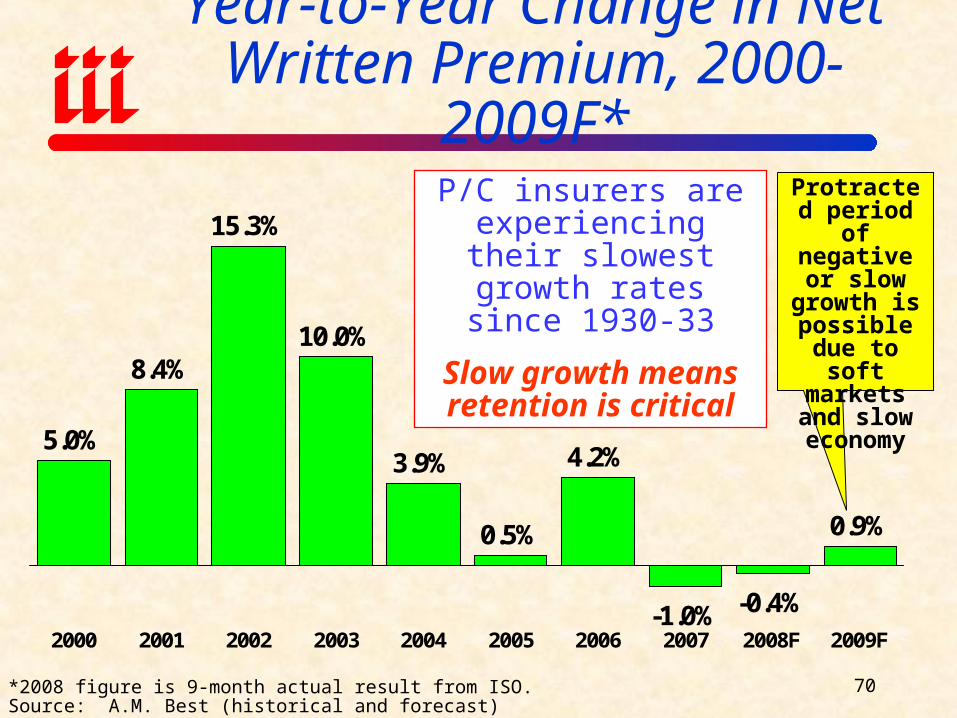

Year-to-Year Change in Net Written Premium, 2000-2009F*

*2008 figure is 9-month actual result from ISO.Source: A.M. Best (historical and forecast)

5.0%

8.4%

15.3%

10.0%

3.9%

0.5%

4.2%

-1.0% -0.4%

0.9%

2000 2001 2002 2003 2004 2005 2006 2007 2008F 2009F

P/C insurers are experiencing their

slowest growth rates since 1930-33

Slow growth means retention is critical

Protracted period of

negative or slow growth is possible due to soft

markets and slow

economy

70

Capital/Policyholder

Surplus

Shrinkage, but Capital is Within Historic Norms

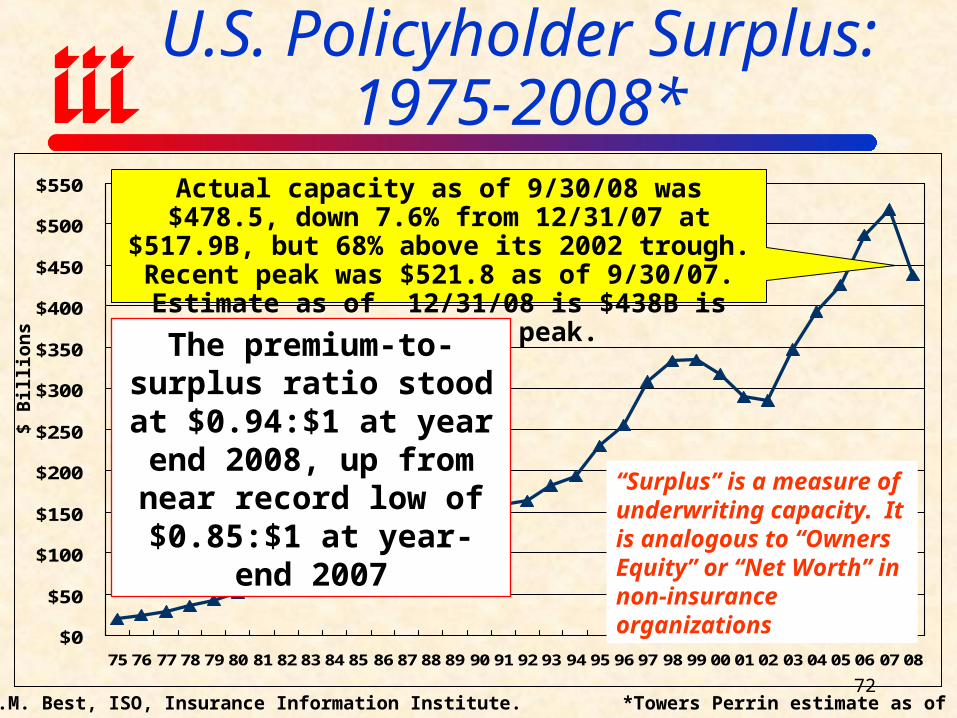

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

U.S. Policyholder Surplus: 1975-2008*

Source: A.M. Best, ISO, Insurance Information Institute. *Towers Perrin estimate as of 12/31/08

$ B

illi

ons

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations

Actual capacity as of 9/30/08 was $478.5, down 7.6% from 12/31/07 at $517.9B, but 68% above its 2002

trough. Recent peak was $521.8 as of 9/30/07. Estimate as of 12/31/08 is $438B is 16% below 2007

peak.

The premium-to-surplus ratio stood at $0.94:$1 at year end 2008, up from

near record low of $0.85:$1 at year-end 2007

72

Policyholder Surplus, 2006:Q4 – 2008:Q4(Est.)

$ Billions

$487.1$496.6

$512.8$521.8

$478.5

$438.0

$505.0$515.6

$517.9

$380

$400

$420

$440

$460

$480

$500

$520

$540

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4

Source: ISO (historical); Towers Perrin (Oct. 21) estimates for Q4 2008. Q4 assumes no major Investment market recovery before year-end 2008.

Declines Since 2007:Q3 Peak

Q2: -$16.6B (-3.2%) Q3E: -$43.3B (-8.3%)

Q4E: -$84B (-16.1%)

Capacity peaked at $521.8 as of 9/30/07

73

0.8

1.0

1.2

1.4

1.6

1.8

2.0

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 0708:Q3

U.S. P/C Industry Premiums-to-Surplus Ratio: 1985-2008:Q3

Sources: A.M. Best, ISO, Insurance Information Institute.

19980.85:1–the lowest

(strongest) P:S ratio in recent history.

Premiums measure risk accepted; surplus is funds beyond reserves to pay unexpected losses. The larger

surplus is in relation to premiums—the lower the ratio of premiums to surplus—the greater the

industry’s capacity to handle the risk it has accepted.

0.92:1 as of

9/30/08

P/C insurers remain well capitalized despite recent

erosion of capital

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

*

NWP % changeSurplus % change

*Actual 9-month 2008 result.Sources: A.M. Best, ISO, Insurance Information Institute

Historically, Hard Markets Follow When Surplus “Growth” is Negative

Sharp decline in capacity is a necessary but not sufficient

condition for a true hard market

Investment Performance

Investments are the Principle Source of Declining

Profitability

Distribution of P/C Insurance Industry’s Investment Portfolio

Cash & Short-Term Investments

7.2%

Common Stock17.9%

Bonds66.7%

Preferred Stock1.5%

Real Estate0.8%

Other5.9%

Portfolio Facts

•Invested assets totaled $1.3 trillion as of 12/31/07

•Insurers are generally conservatively invested, with 2/3 of assets invested in bonds as of 12/31/07

•Only about 18% of assets were invested in common stock as of 12/31/07

•Even the most conservative of portfolios was hit hard in 2008

Source: NAIC; Insurance Information Institute research;.

As of December 31, 2007

77

Property/Casualty Insurance Industry Investment Gain:1994- 2008:Q3 1

$ Billions

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$63.6

$28.3

$56.9$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

1Investment gains consist primarily of interest, stock dividends and realized capital gains and losses. 2006 figure consists of $52.3B net investment income and $3.4B realized investment gain. *2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

Investment gains are off sharply in 2008 due to lower yields and poor equity market conditions.

78

P/C Insurer Net Realized Capital Gains, 1990-2008:Q3

$2.88$4.81

$9.89

$1.66

$6.00

$9.24$10.81

$13.02

$16.21

$6.63

-$1.21

$6.61

$8.97

-$9.71

$18.02

$3.52

$9.70$9.13$9.82

-$10-$8-$6-$4-$2$0$2$4

$6$8

$10$12$14$16$18$20

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08:Q

3

Sources: A.M. Best, ISO, Insurance Information Institute.

Realized capital gains exceeded $9 billion in 2004/5 but fell sharply in

2006 despite a strong stock market. Nearly $9 billion again in 2007, but

$-9.7 billion in 2008 through Q3.

$ Billions

79

-45%

-35%

-25%

-15%

-5%

5%

15%

25%

35%

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

Source: Ibbotson Associates, Insurance Information Institute. *Through March 18, 2009.

Total Returns for Large Company Stocks: 1970-2009*

S&P 500 is down 12.1% in 2009*

The market crash of 2008 was the biggest since 1931

80

Treasury Bond Yields HaveGenerally Been Falling

-2%

0%

2%

4%

6%

8%

10%

90

91

92

93

94

95

96

97

98

99 00

01

02

03

04

05

06

07

08

09

F

10

F

U.S. Treasury 10-Year Note Yield

Sources: US Bureau of Labor Statistics (history); Blue Chip Economic Indicators, February 2009 issue (forecasts)

ForecastJuly 1990-March 1991

recession

March 2001-November 2001

recession

December 2007 – Present

(Current Recession)

Investment yields on the safest assets

are near multi-decade lows

82

0.22% 0.30% 0.46% 0.62%0.98%

1.37%

1.87%2.30%

2.87%

3.83%3.59%

4.82% 4.96% 5.04% 4.96% 4.82% 4.82% 4.88% 4.93% 5.00% 5.19% 5.11%

0%

1%

2%

3%

4%

5%

6%

1M 3M 6M 1Y 2Y 3Y 5Y 10Y 20Y 30Y

Current Yield Curve*Pre-Crisis (July 2007)

Treasury Yield Curves: Pre-Crisis vs. Current*

*February 2009.Sources: Federal Reserve; Insurance Information Institute.

Stock dividend cuts will further pressure investment income

Treasury Yield Curve is at its most depressed level in at least 45 years. Investment income will fall

significantly as a result.

Underwriting Trends

Financial Crisis Does Not Directly Impact Underwriting

Performance: Cycle, Catastrophes Were 2008’s Drivers

90

95

100

105

110

115

120

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

F

Combined Ratios

1970s: 100.3

1980s: 109.2

1990s: 107.8

2000s: 102.0*

Sources: A.M. Best; ISO, III *A.M. Best year end estimate of 103.2; Actual 9-mos. result was 105.6.

P/C Insurance Combined Ratio, 1970-2008F*

84

115.8

107.5

100.198.4

100.8

92.6

101

103.3101.2

95.7

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2008* 2009F

P/C Insurance Industry Combined Ratio, 2001-2009E

*Includes Mortgage & Financial Guarantee insurers. Sources: A.M. Best.

Best combined ratio since 1949

(87.6)

As recently as 2001, insurers paid out nearly $1.16 for every

$1 in earned premiums

Relatively low CAT

losses, reserve releases

Including Mortgage

& Fin. Guarantee insurers

Cyclical Deterioration

85

2005 ratio benefited from heavy use of reinsurance which lowered net losses

-55-50-45-40-35-30-25-20-15-10-505

101520253035

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

Source: A.M. Best, ISO; Insurance Information Institute * Includes mortgage & finl. guarantee insurers

$ B

illi

ons

Insurers earned a record underwriting profit of $31.7 billion in 2006, the largest ever but only the

second since 1978. Cumulative underwriting deficit from 1975 through 2007 is $422 billion.

Underwriting Gain (Loss)1975-2008:Q3*

$19.877 Bill underwriting loss in 08:9M incl. mort. & FG insurers

86

Number of Years With Underwriting Profits by Decade, 1920s –2000s

67

10

8

45

0 0

3

0

2

4

6

8

10

1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s*

Note: Data for 1920 – 1934 based on stock companies only.Sources: Insurance Information Institute research from A.M. Best Data. *2000 through 2008.

Number of Years with Underwriting ProfitsUnderwriting profits were common before the 1980s (40 of the 60 years

before 1980 had combined ratios below 100)—but then they vanished. Not a single underwriting profit was recorded in the 25 years from 1979

through 2003.

87

Commercial Lines

110.

3

110.

2

107.

6

103.

9

109.

7

112.

3

111.

1

122.

3

110.

2

102.

5

105.

4

91.1

95.1

106.

5

105.

1

102.

0

112.

5

85

90

95

100

105

110

115

120

125

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08E 09F

2006/07 benefited from favorable loss cost trends, improved tort environment, low CAT

losses, WC reforms and reserve releases. Most of these trends reversed in 2008 and

mortgage and financial guarantee segments have big influence. 2009 is transition year.

Commercial coverages have exhibited significant

variability over time.

Commercial Lines Combined Ratio, 1993-2009F

Mortgage and financial guarantee may account for up to 4 points on the commercial

combined ratio in 2008

Sources: A.M. Best (historical and forecasts)

Average Commercial Rate Change,All Lines, (1Q:2004 – 4Q:2008)

-3.2

%

-5.9

%

-7.0

%

-9.4

%

-9.7

% -8.2

%

-4.6

% -2.7

%

-3.0

%

-5.3

%

-9.6

%

-11.

3%

-11.

8%

-13.

3% -12.

0%

-13.

5%

-12.

9% -11.

0%

-6.0

%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

Source: Council of Insurance Agents & Brokers; Insurance Information Institute

KRW Effect

-0.1

% Magnitude of price declines is now

shrinking. Reflects shrinking capital,

reduced investment gains, deteriorating

underwriting performance and

costlier reinsurance

Catastrophe Losses

The Energy Sector is Vulnerable to a Increasing

Natural Catastrophe Activity

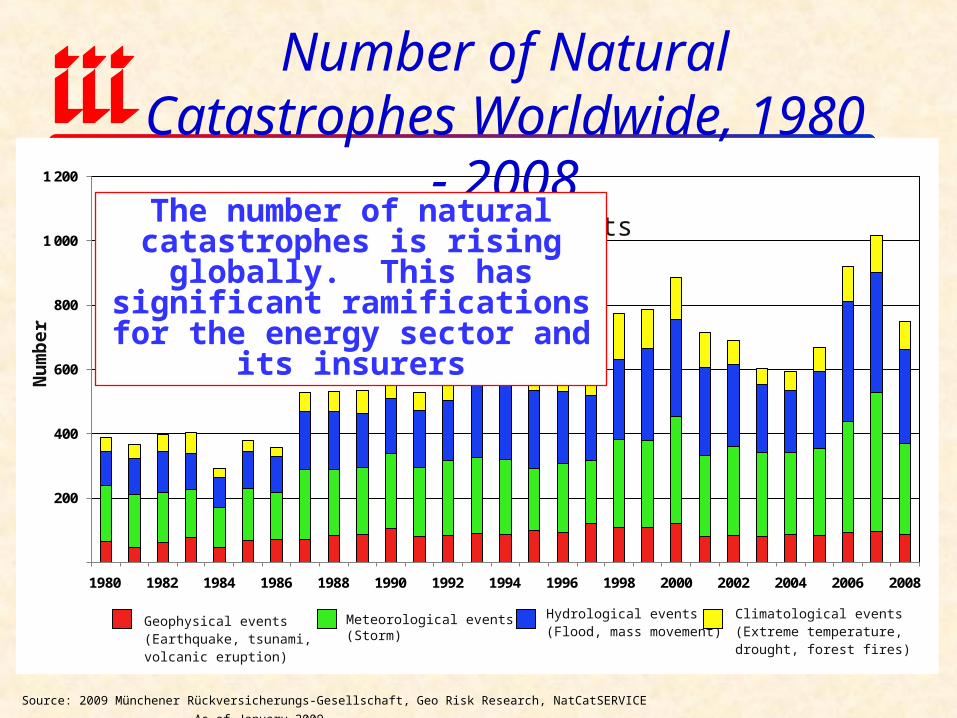

Natural Catastrophes in 2008 by Type and Location

Geophysical (earthquake, tsunami, volcanic)

Meteorological (storm)

Hydrological (flood, mass movement)

Climatological (extreme temperature, drought, wildfire)

Significant loss events

750 natural hazard losses events

Great natural catastrophesHurricane Ike ( Sept. 6-14, 2008) Caribbean, USACyclone Nargis (May 2-5, 2008) Myanmar

Earthquake (May 12, 2008) China

Winter damage (Jan 10–Feb 13, 2008) China

Source: 2009 Münchener Rückversicherungs-Gesellschaft, Geo Risk Research, NatCatSERVICE As of January 2009

Energy sector was impacted significantly by catastrophes in 2008: Ike, European

Wind/Winter Storms, China Earthquake

Deadliest catastrophesDate Event Area DeathsMay Cyclone Nargis Myanmar 84,500

May Earthquake China 70,000

January Cold wave Afghanistan, Kyrgyzstan, Tajikistan

1,000

August/September Floods India, Nepal, Bangladesh 635

Costliest catastrophes (overall losses) US$mMay Earthquake China 85,000

September Hurricane Ike Caribbean, USA 30,000

January/February Winter damage China 21,100

August/September Hurricane Gustav Caribbean, USA 10,000

Costliest catastrophes (insured losses) US$mSeptember Hurricane Ike Caribbean, USA 15,000

August/September Hurricane Gustav Caribbean, USA 5,000

January/February Winter damage China 1,600

March Winter storm Emma Europe 1,500

Some of the Costliest Natural Catastrophes in 2008 Impacted the Energy Business and

Its Insurers Significantly

Source: 2009 Münchener Rückversicherungs-Gesellschaft, Geo Risk Research, NatCatSERVICE As of January 2009

200

400

600

800

1 000

1 200

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

Number of Natural Catastrophes Worldwide, 1980 - 2008

Number of events

Nu

mb

er

Climatological events (Extreme temperature, drought, forest fires)

Hydrological events (Flood, mass movement)

Meteorological events(Storm)

Geophysical events (Earthquake, tsunami, volcanic eruption)

Source: 2009 Münchener Rückversicherungs-Gesellschaft, Geo Risk Research, NatCatSERVICE As of January 2009

The number of natural catastrophes is rising globally. This has significant ramifications for the

energy sector and its insurers

50

100

150

200

250

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

US

$b

n

Overall losses (2008 values) Insured losses (2008 values)

Overall and Insured Losses from Natural Catastrophes Worldwide, 1980 - 2008

The overall and insured costs from natural

catastrophes has been on the rise in recent year.

This has significant implications for the energy

sector and its insurers

Source: 2009 Münchener Rückversicherungs-Gesellschaft, Geo Risk Research, NatCatSERVICE As of January 2009

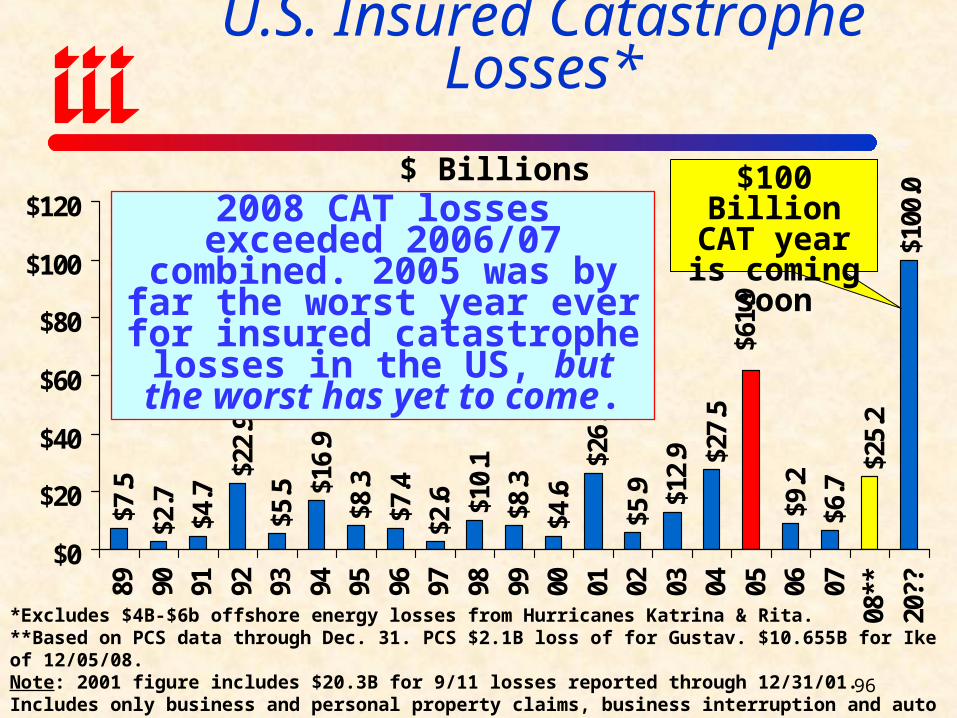

U.S. Insured Catastrophe Losses*$7

.5

$2.7

$4.7

$22.

9

$5.5 $1

6.9

$8.3

$7.4

$2.6 $1

0.1

$8.3

$4.6

$26.

5

$5.9 $1

2.9 $2

7.5

$6.7

$25.

2$1

00.0

$61.

9

$9.2

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

08**

20??

*Excludes $4B-$6b offshore energy losses from Hurricanes Katrina & Rita.**Based on PCS data through Dec. 31. PCS $2.1B loss of for Gustav. $10.655B for Ike of 12/05/08.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B.Source: Property Claims Service/ISO; Insurance Information Institute

$ Billions2008 CAT losses exceeded

2006/07 combined. 2005 was by far the worst year ever for

insured catastrophe losses in the US, but the worst has yet to come.

$100 Billion CAT year is coming soon

96

Rising Number of U.S. Landfalling Tropical Cyclones Has Been Very Costly

for Energy Insurers

Source: Munich Re from NOAA

Six tropical cyclones made landfall in the

US in 2008

Key Issues & Threats Facing P/C

Insurers Amid Financial Crisis

Manageable Challenges

Important Issues & Threats Facing P/C Insurers in 2009

Source: Insurance Information Inst.

1. Reloading Capital After “Capital Event” Continued asset price erosion coupled with major “capital event”

could lead to shortage of capital among some companies P/C insurers have come to assume that large amounts of capital can be

raised quickly and cheaply after major events (post-9/11, Katrina). This assumption may be incorrect in the current environment.

Cost of capital is much higher today, reflecting both scarcity & risk Implications: P/C insurers need to protect capital today and develop

detailed contingency plans to raise fresh capital & generate internally2. Long-Term Loss of Investment Return

Low interest rates, risk aversion toward equities and many categories of fixed income securities lock in a multi-year trajectory toward ever lower investment gains

Many insurers have not adjusted to this new investment paradigm Regulators will not readily accept it; Many will reject it Implication 1: Industry must be prepared to operate in environment

with investment earnings accounting for a smaller fraction of profits Implication 2: Implies underwriting discipline of a magnitude not

witnessed in this industry in more than 30 years Lessons from the period 1920-1975

Source: Insurance Information Inst.

3. Regulatory Overreach P/C insurers get swept into vast federal regulatory

overhaul and subjected to inappropriate , duplicative and costly regulation

4. Tort Threat No tort reform (or protection of recent reforms) is

forthcoming from the current Congress or Administration Erosion of recent reforms is a certainty (already

happening) Innumerable legislative initiatives will create opportunities

to undermine existing reforms and develop new theories and channels of liability

Historically extremely costly to p/c insurance industry

Important Issues & Threats Facing P/C Insurers in 2009 (cont’d)

AFTERSHOCK: Regulatory Response

Could Be Harsh

All Financial Segments Including InsurersWill Be Impacted

Post-Crunch: Fundamental Issues To Be Examined Globally

Source: Ins. Info. Inst.

• Failure of Risk Management, Control & Supervision at Financial Institutions Worldwide: Global Impact Colossal failure of risk management (and regulation) Counterparty risk and collateral management were systemic failure points Implications for Enterprise Risk Management (ERM)? Misalignment of management financial incentives

• Focus Will Be on Risk Controls: Implies More Stringent Capital & Liquidity Requirements; Prevention of Systemic Risks Data reporting requirements also likely to be expanded Non-Depository Financial Institutions in for major regulation Changes likely under US and European regulatory regimes Will new regulations be globally consistent? Can overreactions be avoided?

• Accounting Rule Changes?? Problems arose under FAS, IAS Asset Valuation, including Mark-to-Market Structured Finance & Complex Derivatives

• Ratings on Financial Instruments New approaches to reflect type of asset, nature of risk

Emerging Blueprint for Financial Services Regulatory Overhaul

*http://financialservices.house.gov/press110/press0320082.shtml

Source: Wall Street Journal, “Frank Backs Regulator for Systemic Risk,” 2/4/09, p. C3; I.I.I. research.

Phase I: Systemic Risk Regulation/Regulator Identification of systemic risk points in the financial system Design of appropriate regulation to prevent future collapses Will require international consultation (US can’t manage systemic risk

alone) • Oversight Responsibility: Likely With Federal Reserve

Fed would have capacity and power to assess risk across financial markets regardless of corporate form and to intervene when appropriate *

Fed could oversee (according to House FS Committee Chairman Barney Frank: Hedge funds (need to ensure “complete transparency”) Credit ratings agencies Executive compensation (to curb “perverse risk incentives”)

TIMELINE: Frank wants “general outline” by April 2 meeting of G20 industrialized and developing nations

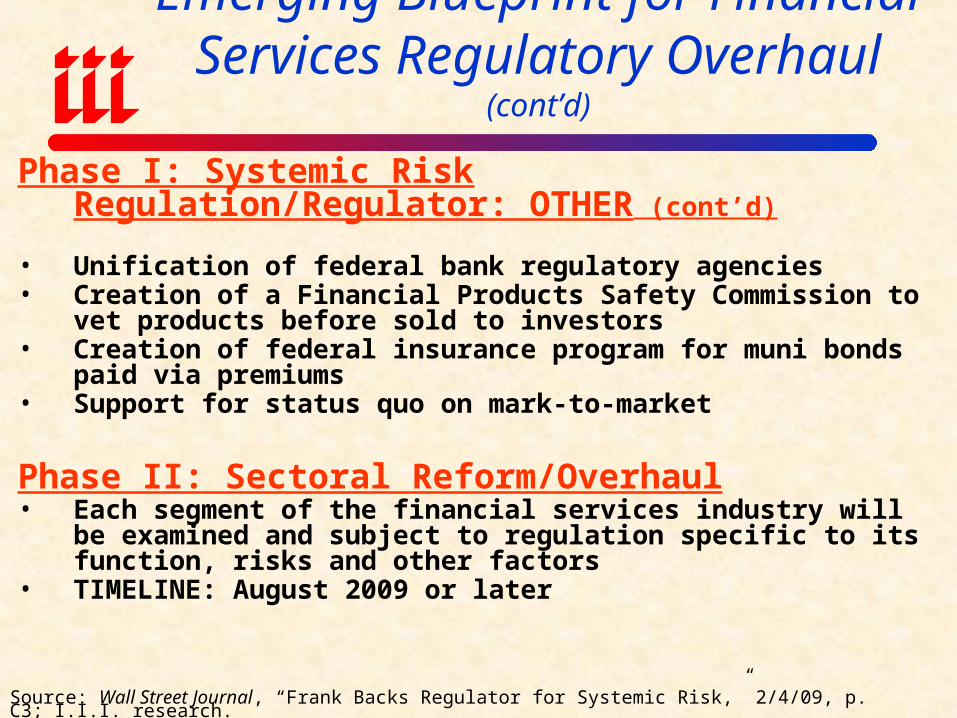

Emerging Blueprint for Financial Services Regulatory Overhaul (cont’d)

Phase I: Systemic Risk Regulation/Regulator: OTHER (cont’d)

• Unification of federal bank regulatory agencies• Creation of a Financial Products Safety Commission to vet products

before sold to investors• Creation of federal insurance program for muni bonds paid via premiums• Support for status quo on mark-to-market

Phase II: Sectoral Reform/Overhaul• Each segment of the financial services industry will be examined and

subject to regulation specific to its function, risks and other factors• TIMELINE: August 2009 or later

Source: Wall Street Journal, “Frank Backs Regulator for Systemic Risk,” 2/4/09, p. C3; I.I.I. research.

Post-Crunch: Fundamental Regulatory Issues & Insurance

Source: Insurance Information Institute

• Federal Encroachment on Regulation of Insurance in Certain Amid a Regulatory Tsunami $150 billion in aid to AIG makes increased federal involvement in

insurance regulation a certainty States will lose some of their regulatory authority What Feds get/what states lose is unclear

• Removing the “O” from “OFC”? Treasury in March proposed moving solvency and consumer

protection authority to a federal “Office of National Insurance” Moving toward more universal approach for regulation of financial

services, perhaps under Fed/Treasury? Is European (e.g., FSA) approach in store? Treasury proposed assuming solvency and consumer protection roles

while also eliminating rate regulation Expect battle over federal regulatory role to continue to be a divisive

issue within the industry States will fight to maximize influence, arguing that segments of the

financial services industry under their control had the least problems

Possible Regulatory Scenarios for P/C Insurers as of Year-End 2009

Source: Insurance Information Inst.

• Status Quo: P/C Insurers Remain Entirely Under Regulatory Supervision of the States Unlikely, but some segments of the industry might welcome this

outcome above all others• Federal Regulation: Everything is Regulated by Feds

Unlikely that states will be left totally in the cold• Optional Federal Charter (OFC): Insurers Could Choose

Between Federal and State Regulation Unlikely to be implemented as envisioned for past several years by

OFC supporters• Dual Regulation: Federal Regulation Layer Above State

Feds assume solvency regulation, states retain rate/form regulation• Hybrid Regulation: Feds Assume Regulation of Large

Insurers at the Holding Company Level• Systemic Risk Regulator: Feds Focus on Regulation of

Systemic Risk Points in Financial Services Sector What are these points for insurers? P/C vs. Life?

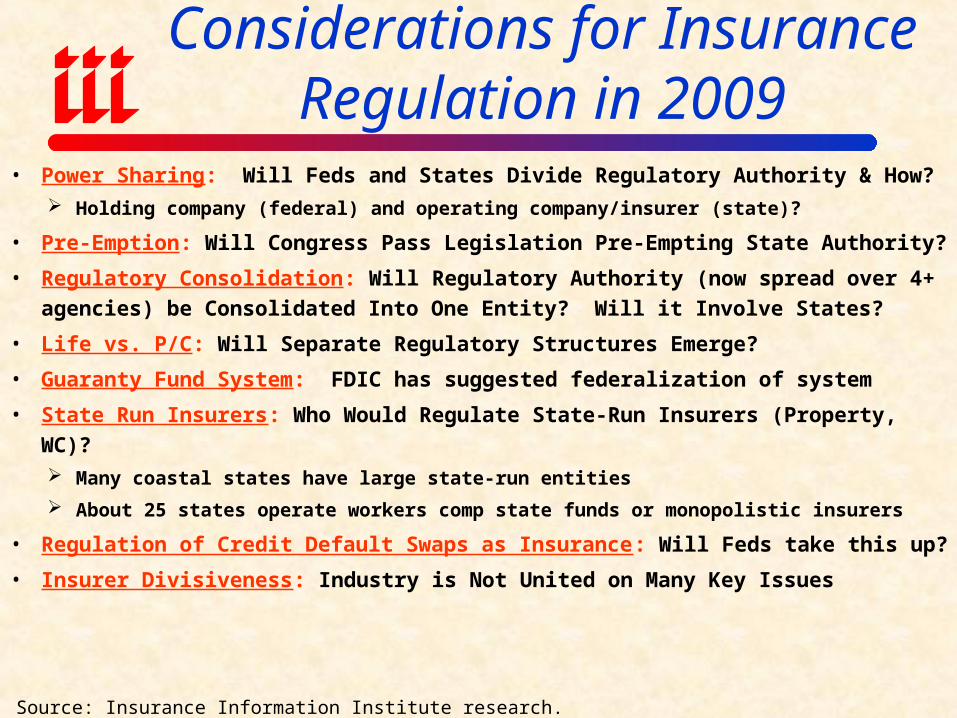

Major Regulatory Considerations for Insurance Regulation in 2009

• Power Sharing: Will Feds and States Divide Regulatory Authority & How?

Holding company (federal) and operating company/insurer (state)?

• Pre-Emption: Will Congress Pass Legislation Pre-Empting State Authority?

• Regulatory Consolidation: Will Regulatory Authority (now spread over 4+

agencies) be Consolidated Into One Entity? Will it Involve States?

• Life vs. P/C: Will Separate Regulatory Structures Emerge?

• Guaranty Fund System: FDIC has suggested federalization of system

• State Run Insurers: Who Would Regulate State-Run Insurers (Property, WC)?

Many coastal states have large state-run entities

About 25 states operate workers comp state funds or monopolistic insurers

• Regulation of Credit Default Swaps as Insurance: Will Feds take this up?

• Insurer Divisiveness: Industry is Not United on Many Key Issues

Source: Insurance Information Institute research.

Insurance Information Institute On-Line

THANK YOU FOR YOUR TIME AND

YOUR ATTENTION!

108

Top Related