![Standpoint Juhan Parts [22.09.2011]: Estonian state supports building "Rail Baltica" The City of Tallinn shares the "Rail Baltica" standpoints of Estonian.](https://static.fdocuments.in/doc/165x107/56649eff5503460f94c148af/standpoint-juhan-parts-22092011-estonian-state-supports-building-rail.jpg)

Languages

Pages

Legal

Tallinn University of Technology

Estonian housing market -

before euro adoption

Angelika Kallakmaa

Ene Kolbre

Tallinn University of Technology

Tallinn University of Technology

Estonia 2010

In the same time, when other EU countries deal with government debt and public deficit problems, Estonia fills Maastricht criteria

Tallinn University of Technology

Maastricht criteria

Maastricht criteria Reference value Estonia

Inflation rate 1,0% -0,7 %

Participation in the currency exchange rate mechanism ERM II

2 years The Estonian kroon has been participating in ERM II since 2004

The general government deficit

Must be lower than 3% of GDP

1.7% of GDP

Government debt Must be less than 60% of GDP

7.2% of GDP

Tallinn University of Technology

Economic situation

During 2000 - 2007 Estonia’s output growth was faster than in most emerging market economies

Since 2008, the economy has been experiencing a hard landing period

Restored growth in Estonian exports will be balanced economic situation in Estonia in the second half of 2010

Tallinn University of Technology

Economic background and forecast

2006 2007 2008 2009 2010* 2011* 2012*

GDP (%) 10,0 7,2 -3,6 -14,1 1,0 4,0 3,3

Private consumption expenditure (%)

13,0 9,1 -4,8 -18,9 -5,6 1,6 3,8

Unemployment rate (ILO) (%)

5,9 4,7 5,5 13,8 16,0 14,5 13,2

Real wage growth (%)

10,4 12,0 4,3 -3,8 -4,2 0,1 1,9

Average gross wage growth (%)

16,2 20,4 13,8 -4,6 -3,8 1,2 3,2

Nominal credit growth (%)

51,6 30,2 7,3 -6,4 -2,4 2,3 3,8

Tallinn University of Technology

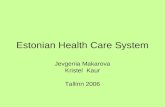

Employment

Housing boom increased employment in the real estate and related sectors

At the end of the growth period, the economy reached the stage of full employment

After real the estate boom the unemployment rate skyrocketed

The unemployment level will probably remain high over the next years

Tallinn University of Technology

The wages and salaries

The average gross wages and salaries have decreased, but the decrease slowed down in the

1st quarter 2010 The real wages,which took into account the

influence of the change in the consumer price index, decreased 2.6% in the 1st quarter 2010

Tallinn University of Technology

Average monthly gross wages and salaries, 1st quarter 2006– 1st quarter 2010 (EUR)

1st quarter 2nd quarter

3rd quarter

4th quarter Year

2006 549 609 580 653 601

2007 660 738 697 784 725

2008 788 850 800 838 825

2009 776 813 752 783

2010 758

Tallinn University of Technology

Information asymmetries between borrowers and lenders

When economic conditions are depressed and collateral values are low, information asymmetries can mean that even borrowers with profitable projects find it difficult to obtain funding

When economic conditions improve and collateral values rise, these firms are able to gain access to external finance and this adds to the economic stimulus.

This explanation of economic and financial cycles is often known as the “financial accelerator”

Tallinn University of Technology

Procyclicality effect

During an economic boom financial sector inclines to strengthen the impact of a business cycle through intensifying lending activity

and vice versa

Tallinn University of Technology

Männasoo 2003

“Since 2001, the growth in loans has accelerated again, reaching markedly high speed in 2002

The share of provisions has decreased and this has supported in keeping capitalisation high

The banking sector’s reaction to the economic upturn indicates some rise of procyclical optimism”

Tallinn University of Technology

Loans granted to individuals (stock, Mln EEK)

0

20000

40000

60000

80000

100000

120000

140000

31.12.00 31.12.01 31.12.02 31.12.03 31.12.04 31.12.05 31.12.06 31.12.07 31.12.08 31.12.09

Loans to individuals

housing loans

Tallinn University of Technology

Loans granted to individuals during a month 2000-2010

Loans to individuals

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

11/30/00 10/31/01 09/30/02 08/31/03 07/31/04 06/30/05 05/31/06 04/30/07 03/31/08 02/28/09 01/31/10

Loans to individuals

Tallinn University of Technology

Campell (2006)

Household’s behaviour is difficult to measure and they are not always fully rational when they making financial decisions

Households make investment mistakes, given the complexity of their financial planning problem and the often confusing financial products that are offered to them

Tallinn University of Technology

Questionnaire 2010 April

Purpose:

Evaluate the access to bank loans during the housing boom time

Expectations about real estate market movements

Tallinn University of Technology

Questionnaire 2010 April

There were 350 repliers (287 female, 62 male) 57 % are owners of their living space, others live

with parents or rent Persons who don’t own the living space – more

then half of them don’t plan to buy real estate in the next years

(Reason – 34 % real estate prices are still too high, 45 % disposable income is too low to take a loan)

Tallinn University of Technology

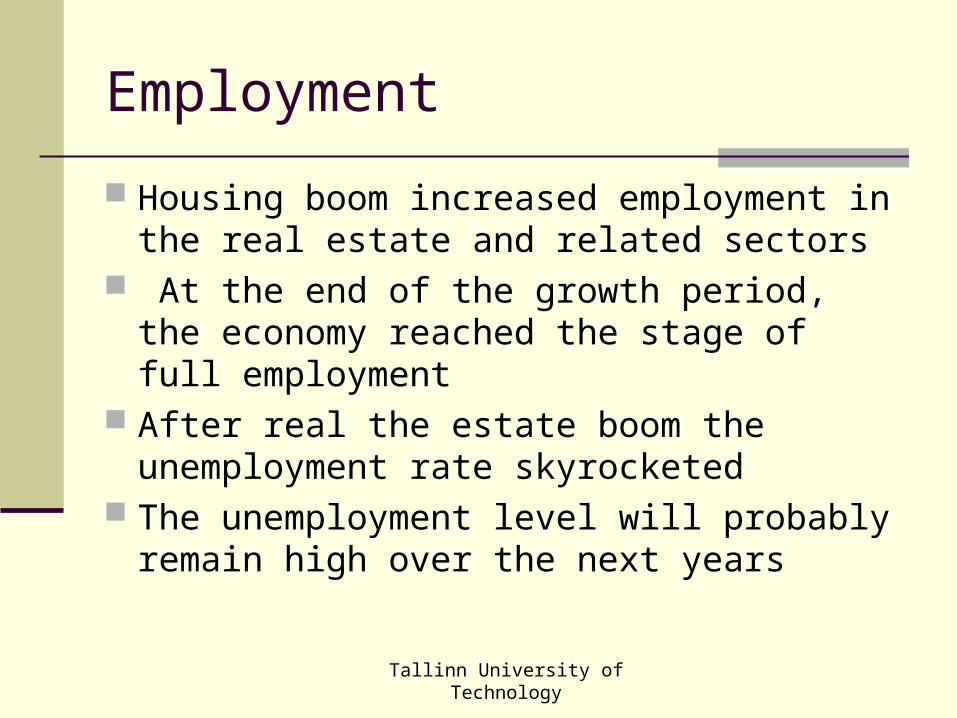

Credit availability to households housing loans

43% of repliers found that it was too easy to get loan from banks

19 % bank condition was that loan must be taken jointly with another person

Only 1% answered that bank asked too high self financing amount

Tallinn University of Technology

Influence for consumption

45 % housing loan repayment amount is 30 % of disposable income

30% of repliers found that increase in interest rates will make their loan payments difficult (part of repliers did not answer at all)

6% said they have difficulties in everyday life Only 2% of repliers are ready to sell their property

when they have difficulties with loan payments

Tallinn University of Technology

Conclusions

It is common to own your living space, not to rent it Access to bank credit was too easy during the real estate

boom Clients with problems don’t want to renounce their

property, only 2 % admit to the possibility of selling their flat or house

Not owners are not planning to buy, they preferred to live with parents or rent the living space

Housing loans have an important influence to the consuming activity

Tallinn University of Technology

There was the procyclical effect in lending activity Credit risk was underestimated in the boom time It seems to be that the overheating was stronger

than the downturn

Tallinn University of Technology

According to the Estonian institute of economic research:

In 2009 was the consumer confidence lowest of all the survey period (since 1992)

48 % of consumers assesses that the economic situation of their household was worse then a year ago

Only 4% had a better situation

Tallinn University of Technology

Individuals loans and deposits

0

20000

40000

60000

80000

100000

120000

140000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Deposits of individuals (stock)

Loans to individuals

Tallinn University of Technology

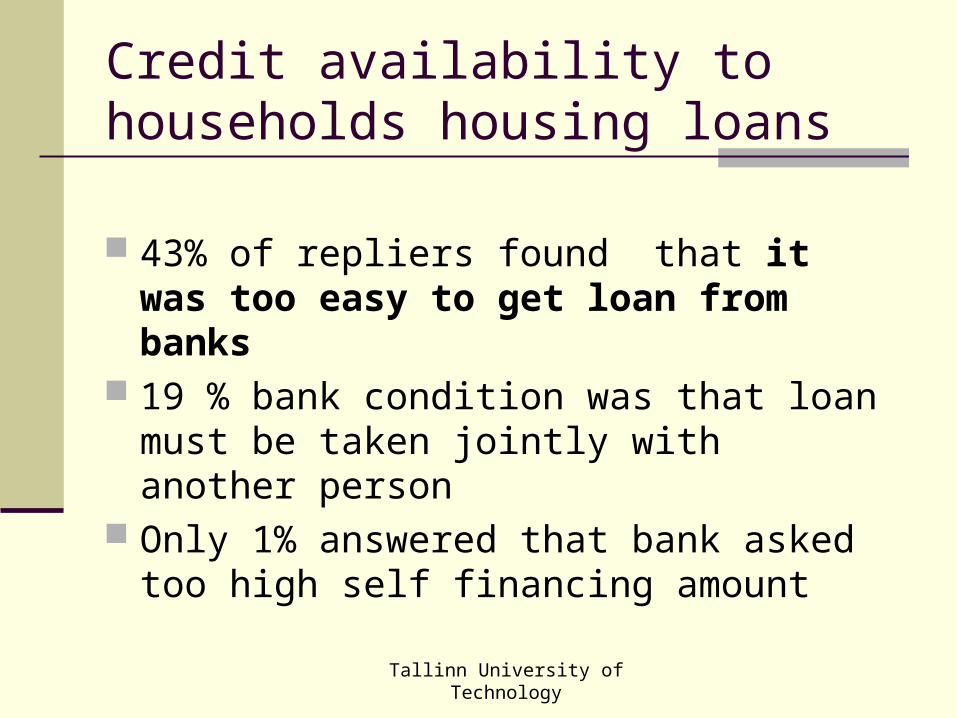

Overdue loans and overdue housing loans (1997-2009 annual basis, 2010 monthly basis)

0

2000

4000

6000

8000

10000

12000

mln

EE

K

Overdue amount of loans Overdue amount of housing loans

Tallinn University of Technology

Overdue loans

The stock of overdue loans did not change much in 2010

The share of housing loans overdue by more than 60 days increased, reaching 4.6%

Improvement in the quality of the loan portfolio is a time-consuming process, which will take years even if economic activity picks up

Tallinn University of Technology

Housing finance market activity remained sluggish

demand for housing loans is low

( irrespective of the relatively low price level of real estate)

The stock of new housing loans issued within the April 2010 was 13% smaller than the average level of 2009

Tallinn University of Technology

Housing market

Prices of apartments started to rise rapidly in 2005 when the annual price rise was over 50%

The growth rate of transactions started to slow down in the middle of 2006

The price rise turned to decline in 2007 when the housing prices reached the maximum

Average price fall since spring 2007 has been 40-45%

Tallinn University of Technology

Real estate purchase and sales transactions 2000-2010

0

10000

20000

30000

40000

50000

60000

70000

80000

Number of contracts

Value of contracts (mln EEK)

Tallinn University of Technology

Housing demand

Total volume of housing loans has increased as a result of low interest rate and tight competition in the banking sector

The rise in housing market was mostly driven by consumers expectations (stories of unprecedented

price increases etc) easy access to credit (housing loan standards )

Tallinn University of Technology

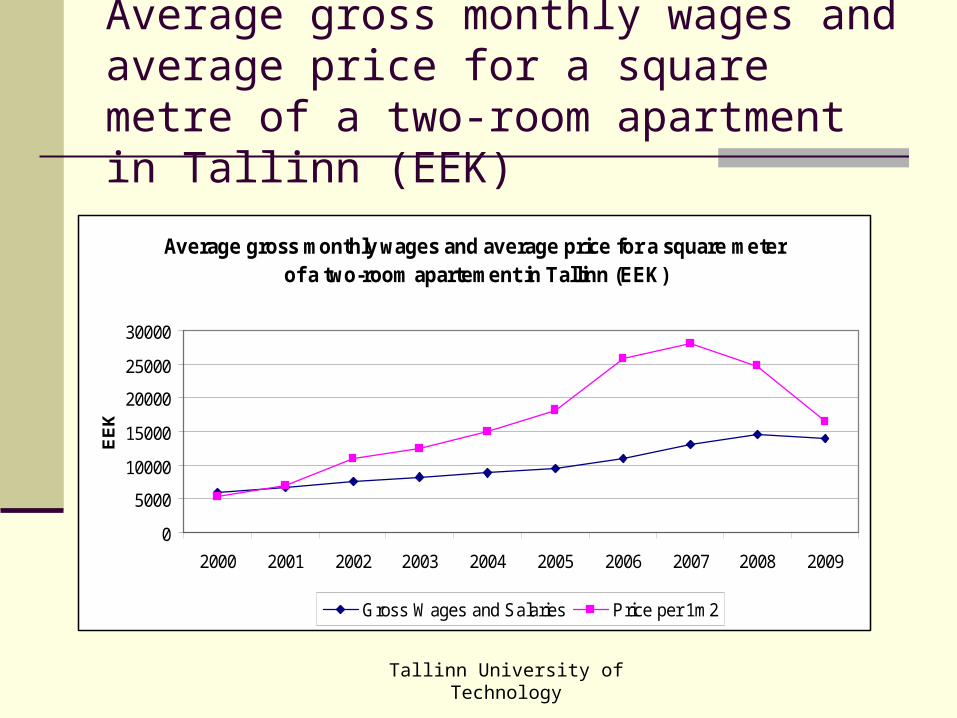

Average gross monthly wages and average price for a square metre of a two-room apartment in Tallinn (EEK)

Average gross monthly wages and average price for a square meter of a two-room apartement in Tallinn (EEK)

0

5000

10000

15000

20000

25000

30000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

EE

K

Gross Wages and Salaries Price per 1m2

Tallinn University of Technology

Number of square meters of a two-room apartment in Tallinn obtainable for average gross monthly wages

Number of square meters of two-room apartment in Tallinn obtainable for average gross monthly wages

0,00

0,20

0,40

0,60

0,80

1,00

1,20

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Tallinn University of Technology

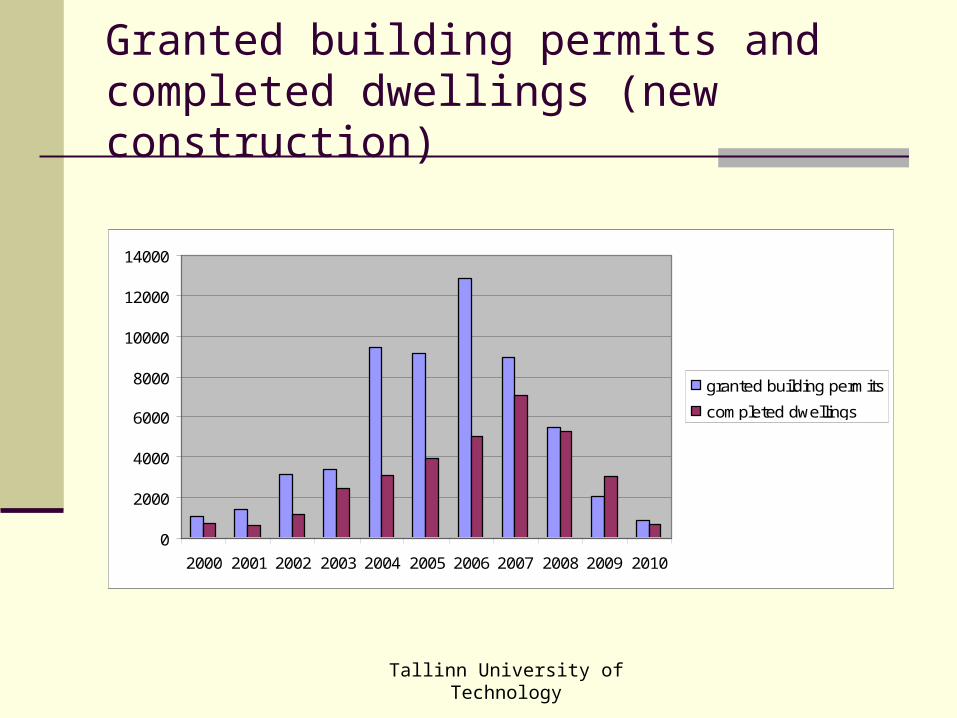

Housing supply

In 2004−2006 demand for housing was greater than supply

Since the beginning of 2007 supply started to grow rapidly

Since 2008 supply has been greater than demand

Tallinn University of Technology

Granted building permits and completed dwellings (new construction)

0

2000

4000

6000

8000

10000

12000

14000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

granted building permits

completed dwellings

Tallinn University of Technology

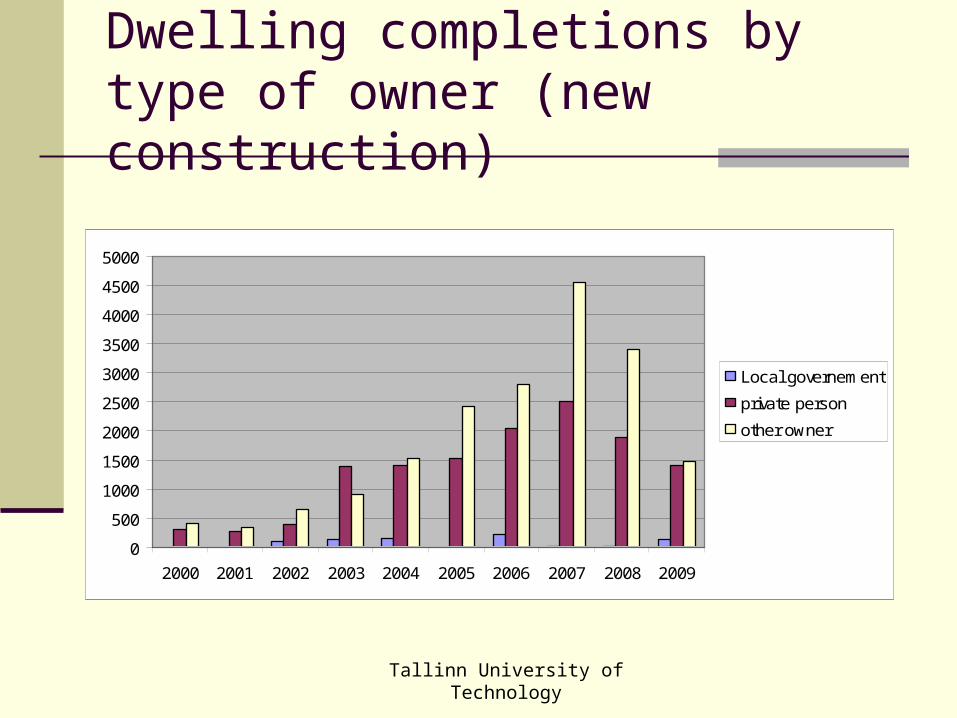

Dwelling completions by type of owner (new construction)

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Local governement

private person

other owner

Tallinn University of Technology

Conclusions (1)

Real estate prices are very cycle-sensitive It is difficult for banks to follow more prudent

policies during an economic upturn, especially in a highly competitive environment

The supervisory pressure on banks seems also to be procyclical (if real estate prices are rising, loan portfolio is rising, banks declare good earnings - it is very difficult to explain concerns with such situations)

Tallinn University of Technology

Conclusions (2)

Households budgets are tighten Borrowers have postponed their investment and

consumption decisions despite of low interest rateIf demand improves, credit growth can be expected

to pick up no sooner than in the second half of the year 2010

Loan losses have increased less than anticipated in last year forecasts

Improvement in the credit portfolio quality of banks will take time

Tallinn University of Technology

Conclusions (3)

Adoption of euro - the signals are contradictory

demand is low, but experts speak about the first signs of recovery on the real estate market (Eurozone membership will give easier access to European capital markets)

Some euro-area countries are experiencing a government debt crisis, uncertainties have arisen in the external environment

The bottom of the Estonian real estate market is approaching, although the shape of this bottom is expected to be flat, which means a long vegetating in all economy

Tallinn University of Technology

Thank you!

Tallinn University of Technology

Authors

Angelika Kallakmaa School of Economics and Business

Administration, Tallinn University of Technology e-mail: [email protected] Ene Kolbre School of Economics and Business

Administration, Tallinn University of Technology e-mail: [email protected]

Top Related