Languages

Pages

Legal

www.osram-licht.ag

Q4 FY13 Management Presentation (preliminary figures)(preliminary figures)

Successful FY13 with a strongyear-end finishy

OSRAM Licht AGNovember 12 2013November 12, 2013

Safe Harbor StatementSafe Harbor Statement

This presentation may contain forward-looking statements that are subject to risks and uncertainties,including those pertaining to the anticipated benefits to be realized from the proposals describedherein. Forward-looking statements may include, in particular, statements about future events, futurefinancial performance plans strategies expectations prospects competitive environmentfinancial performance, plans, strategies, expectations, prospects, competitive environment,regulation and supply and demand. OSRAM Licht AG has based these forward-looking Statementson its views and assumptions with respect to future events and financial performance. Actualfinancial performance could differ materially from that projected in the forward-looking Statementsdue to the inherent uncertainty of estimates forecasts and projections and financial performancedue to the inherent uncertainty of estimates, forecasts and projections, and financial performancemay be better or worse than anticipated. Given these uncertainties, readers should not put unduereliance on any forward-looking statements. The information contained in this presentation is subjectto change without notice and OSRAM Licht AG does not undertake any duty to update the forward-looking statements and the estimates and assumptions associated with them except to the extentlooking statements, and the estimates and assumptions associated with them, except to the extentrequired by applicable laws and regulations.

Due to rounding, numbers presented throughout this and other documents may not add up preciselyto the totals provided and percentages may not precisely reflect the absolute figuresto the totals provided and percentages may not precisely reflect the absolute figures.

Management presentation Q4 FY13 (preliminary figures) | November 12, 20132© OSRAM Licht AG 2013. All rights reserved.

2

G hi hli ht FY13Group highlights FY13

Successful FY13 with a strong year-end finishMajority of announced FY12-FY14 restructuring program doneRestructuring in Luminaires and Services initiatedDuring FY13 new product pipeline filled for profitable growth in FY14During FY13 new product pipeline filled for profitable growth in FY14

Outlook FY13 guidance delivered Comparable growth: 2% Adj. EBITA margin1): 7.7% Net income: €34m FCF: €284met co e €3 C € 8

OSRAM Push execution ahead of schedule€433m cumulated PUSH gross savings reached in FY13€433m cumulated PUSH gross savings reached in FY13OSRAM Push pipeline for FY14 well filled with measures

OSRAM‘s transformation towards SSL continuedOSRAM s transformation towards SSL continued29% SSL revenue share (vs. 25% FY12) of total salesInvestments in SSL product pipeline starts to pay-off; SSL gross margins rising in all reporting segments

Management presentation Q4 FY13 (preliminary figures) | November 12, 20133© OSRAM Licht AG 2013. All rights reserved.

1) Adjusted for “Special items”

S t hi hli ht FY13Segment highlights FY13

Specialty Lighting (SP)Long-term growth above market continuedDesign win for laser light front lights; advanced development projects for OLED rear lights

Opto Semiconductors (OS)€1 bn in revenue exceeded for the first time everFlash light design wins at two leading smartphone makersFlash light design wins at two leading smartphone makers

Lamps & Components (LC)Growth in Q4 after quarters of declineGrowth in Q4 after quarters of declineIntroduction of new LEDr lamps, light engines and SSL drivers

Luminaires & Solutions (LS)Luminaires & Solutions (LS)Restructuring in Luminaires and Services initiatedSubstantial growth of professional SSL outdoor luminaires

Management presentation Q4 FY13 (preliminary figures) | November 12, 20134© OSRAM Licht AG 2013. All rights reserved.

OSRAM Push – Execution ahead of scheduleNew OSRAM Push targets

OSRAM Push: Overall, comprehensive, sustainable performance improvement program

New OSRAM Push targets

>8%1)

OSRAM Push execution track record “old”

>80%

As of Q3 FY13

As of Q4 FY13 Progress Target

Transformation costs (€m)(FY12 – 14)

388 498 ≤ 600

Structure Growth

63%83%

64%

(FY12 14)

Plant reductions(FY12 – 14) 5 7 11

Headcount reduction (‘000)(FY12 – 14)

5.2 6.6 2) c.8.0

OSRAM Push gross

Operation CultureEBITA Margin: 8% 43%

OSRAM Push gross savings, cum. (€m)(FY13 – 15)

316 433 c.1,000

OSRAM Push execution track record “new”As of Q3 As of Q4

New OSRAM Push targets:

>8% as average over the cycle

64%

>80%

FY13 FY13 Progress Target Transformation costs (€m)(FY12 – 14)

388 498 ≤ 600

Plant reductions(FY12 – 14) 5 7 11

New OSRAM Push targets: Cum. gross savings raised to €1.2bn by FY15

Headcount reduction increased to 8,700 by FY14

Reduction of manufacturing sites unchanged

36%

76%Headcount reduction (‘000)(FY12 – 14)

5.2 6.6 2) c.8.7

OSRAM Push gross savings, cum. (€m)(FY13 – 15)

316 433 c.1,200

g g

OPEX targets unchanged:

SG&A1): Reduce by ~8-10% by FY14 vs. FY12

R&D: Keep absolute terms flat until FY14 vs. FY121) w/o logistics costs

Management presentation Q4 FY13 (preliminary figures) | November 12, 20135© OSRAM Licht AG 2013. All rights reserved.

2) Including impact of Tangerang (closure of production)Cumulated, as of Q3 FY13 Cumulated, as of Q4 FY13

1) w/o logistics costs

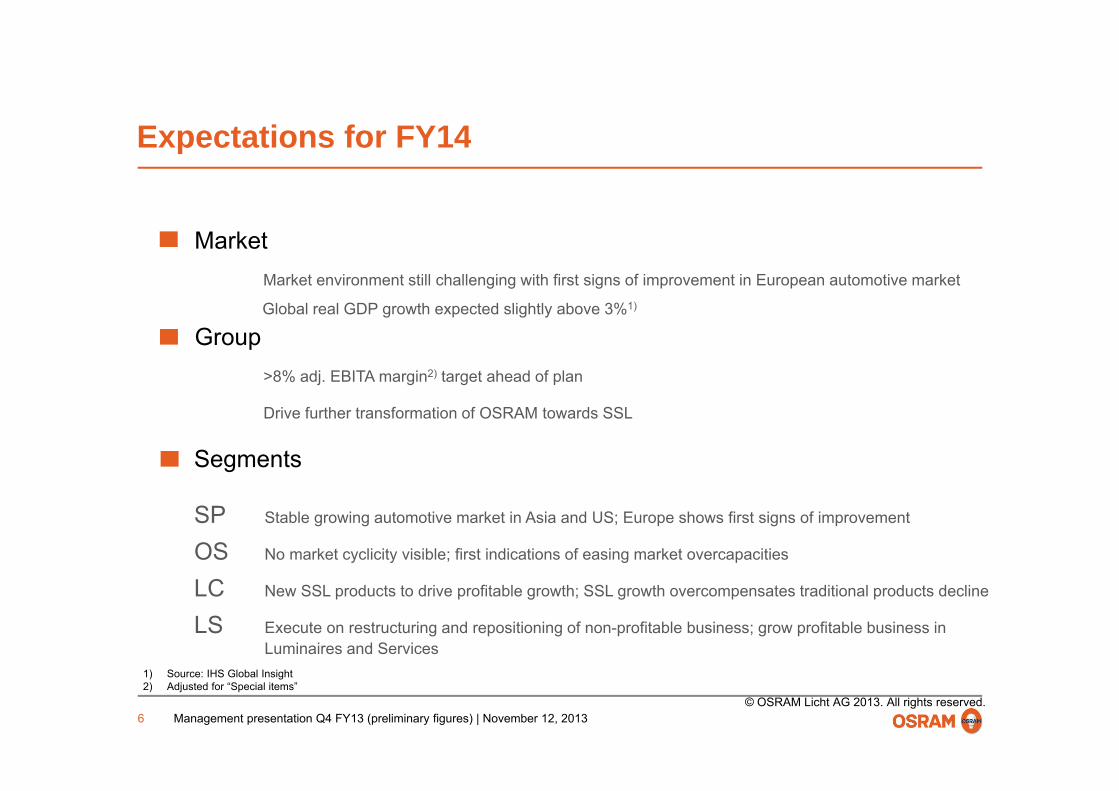

E t ti f FY14Expectations for FY14

MarketSMarket environment still challenging with first signs of improvement in European automotive market

S Global real GDP gro th e pected slightl abo e 3%1)

GroupS>8% adj. EBITA margin2) target ahead of plan

S Global real GDP growth expected slightly above 3%1)

SDrive further transformation of OSRAM towards SSL

Segments

SP Stable growing automotive market in Asia and US; Europe shows first signs of improvement

OS No market cyclicity visible; first indications of easing market overcapacities

LC New SSL products to drive profitable growth; SSL growth overcompensates traditional products decline

LS Execute on restructuring and repositioning of non-profitable business; grow profitable business in Luminaires and Services

Management presentation Q4 FY13 (preliminary figures) | November 12, 20136© OSRAM Licht AG 2013. All rights reserved.

1) Source: IHS Global Insight2) Adjusted for “Special items”

Broad based growthBroad-based growth

Comments Q4 y-o-yRevenue developmentGroup (€m)

Comments Q4 y-o-yRevenue development

Quarterly revenue Strong year-end finish: Revenue +4% (comp.) backed by all segments and regions

SSL revenue growth +19% (comp.)5,2895,400

Comp. th (%)

Revenue(in €m)

g ( p )

SSL share at 31%, up from 27% y-o-y

EMEA: comp. growth driven especially by OS and SP

APAC comp gro th backed b SP

1,3321,2781,3221,3571,371

( ) 0 2 41 2

growth (%)

Growth (%) (1)3 (3) (2)(3) 7(2)

APAC: comp. growth backed by SP

Americas: comp. growth turned positive including strong OS sales and recovering lamps business

FY13FY12Q4FY13

Q3FY13

Q2FY13

Q1FY13

Q4FY12

(3) (1) 0 1

Revenue by Region1) Q4Revenue by Segment1) Q4

Americas34% EMEA42%nom (3%)

Opto Semiconductors19%

Lamps & Components

nom. 10%comp. 13% 34%

APAC

23%

EMEA42% nom. 2%comp. 4%

nom. (3%)comp. 5%

nom. (10%)5%

Specialty Lighting26%

Luminaires & Solutions11%

Lamps & Components44%nom. (8%)comp. 2%

nom. 2%comp. 8% nom. 1%

comp 4%

Management presentation Q4 FY13 (preliminary figures) | November 12, 20137© OSRAM Licht AG 2013. All rights reserved.

1) Based on sum of Segments´ revenue, w/o considering corp. items & consolidation; nom. (nominal growth) / comp. (comparable growth, adjusted for FX and portfolio effects)

comp. 5%comp. 4%

OSRAM Push translates into bottom line performanceOSRAM Push translates into bottom-line performance

EBITA development Comments Q4 y o y

Group (€m)

EBITA development Comments Q4 y-o-y

7.47.9 8.1

5.8

7.5 7.77.4 Transformation progress impacted reported EBITA

heavily with €133m Special items

Profitability before Special items continued to

EBITAMargin (%) (1 8)

0.90.5 0.1

1.91.71.0

Adj. EBITAMargin1) (%)

y pincrease to 8.1% (+710bps) with OSRAM Push measures materializing

Strong EBITA contributions from SP and OS; improving results of LC and LS before Special items

2012 2013Q4 FY Q1 Q2 Q3 Q4 FY

Margin (%)

Special items2)

(1.8) FY13 Net income at €34m

99100

incl. (133)Special items Q4 FY Q1 Q2 Q3 Q4 FY

EBITA reported 7 51 100 1 222 (24) 99

therein:

OSRAM Push transformation costsincl. personnel restructuring (15) (199) (36) (90) (64) (110) (300)

p

EBITA(€ )

51

22

17

Special items

Spin-off/stand alone-related costs 12 (31) 29) (8) (9) (22) (10)

Substantial legal and regulatory matters (FY12: trademark & license case)

(4) (34) –) –) – – –

Total Special items (7) (264) (7) (98) (72) (133) (310)

(€m)

-24

Q4FY13

Q3FY13

Q2FY13

Q1FY13

Q4FY12

FY13FY12

Management presentation Q4 FY13 (preliminary figures) | November 12, 20138© OSRAM Licht AG 2013. All rights reserved.

Total Special items (7) (264) (7) (98) (72) (133) (310)

1) Adjusted for “Special items” 2) "Special items” in this context include certain items, e.g. (personnel) restructuring costs, that will also occur in future periods

FY13FY13FY13FY13FY12

FY13 and FY12 burdened by Special Items, adjusted EBITA with strong contribution from OSRAM Push

€433m

Margin 7.7%

Margin5.8% Margin

1.9%Margin

0.9%

1) EBITA adjusted for Special Items. The definition of Special Item is company specific and includes also topics which could occur in following periods, especially (personnel) restructuring costs

EBITA FY13 as reported

EBITA FY13 adjusted1)

Cost Reduction Measures

(OSRAM Push)

Volume / Degression / Product

Mix / Others

InflationCustomer Price Change

EBITA FY12 adjusted1)

EBITA FY12 as reported

Management presentation Q4 FY13 (preliminary figures) | November 12, 20139© OSRAM Licht AG 2013. All rights reserved.

especially (personnel) restructuring costs

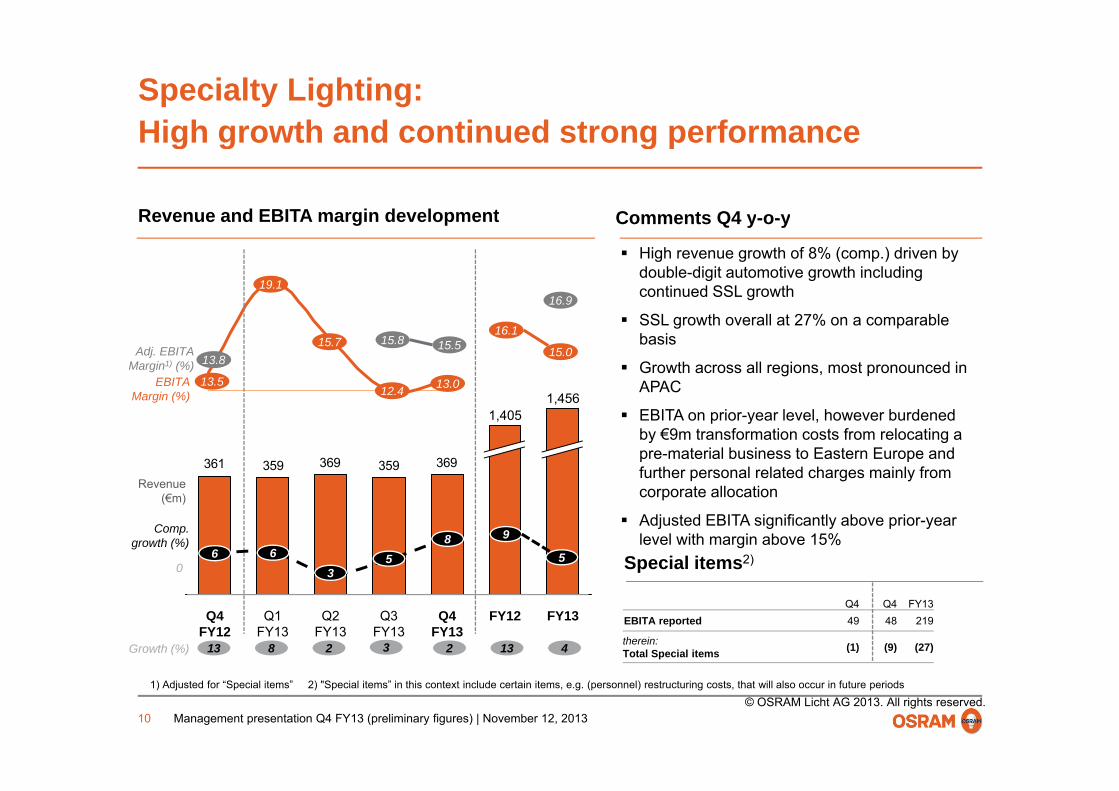

Specialty Lighting: High growth and continued strong performanceHigh growth and continued strong performance

Revenue and EBITA margin development Comments Q4 y o yRevenue and EBITA margin development

High revenue growth of 8% (comp.) driven by double-digit automotive growth including continued SSL growth

Comments Q4 y-o-y

16.919.1

16.1 SSL growth overall at 27% on a comparable

basis

Growth across all regions, most pronounced in APACEBITA

Margin (%)

Adj. EBITAMargin1) (%)

13.512.4

15.013.8

1 456

15.8 15.515.7

13.0

EBITA on prior-year level, however burdened by €9m transformation costs from relocating a pre-material business to Eastern Europe and further personal related charges mainly from

Margin (%)

369359369359361

1,4561,405

Revenue

Special items2)

corporate allocation

Adjusted EBITA significantly above prior-year level with margin above 15%

0

Revenue(€m)

Comp. growth (%)

663

8 9

55

Growth (%) 813 2 42 133

Q4 Q4 FY13EBITA reported 49 48 219

therein:Total Special items (1) (9) (27)

Q1FY13

Q4FY12

FY13FY12Q4FY13

Q3FY13

Q2FY13

3

Management presentation Q4 FY13 (preliminary figures) | November 12, 201310© OSRAM Licht AG 2013. All rights reserved.

1) Adjusted for “Special items” 2) "Special items” in this context include certain items, e.g. (personnel) restructuring costs, that will also occur in future periods

Opto Semiconductors: Double digit top line growth and high profitabilityDouble-digit top-line growth and high profitability

Revenue and EBITA margin development Comments Q4 y-o-y

Revenue growth of 13% (comp.), again double-digit the fourth consecutive quarter

14 6

EBITAMargin (%)

12.2

8.5

Growth across all regions, most pronounced in EMEA and Americas, fueled by infrared business and components for general lighting

Strong EBITA margin benefited from favorable 1,0189.8

14.6

10.2

13.5

8.3Margin (%)product mix as well as OSRAM Push productivity

268279241230244

899

Revenue(€m)

241230244

Comp. growth (%)

0

10714 13

1

1418

Growth (%) 1214 14 1310 517

Q3FY13

Q2FY13

Q1FY13

Q4FY12

FY12Q4FY13

FY13

Management presentation Q4 FY13 (preliminary figures) | November 12, 201311© OSRAM Licht AG 2013. All rights reserved.

Lamps & Components: Growth after quarters of declineGrowth after quarters of decline

R d EBITA i d l t C t Q4Revenue and EBITA margin development Comments Q4 y-o-y

Strong finish results in modest revenue growth of 2% (comp.) across all regions driven by SSL business increasing by 38%

4.9

2 8

4.8

EBITAMargin (%)

Adj. EBITAMargin1) (%)

Strong traditional revenues, nearly flat Y-o-Y

EBITA substantially improved benefiting from OSRAM Push measures; however, held back by higher transformation costs as well as 2 786

0.2

(4.8)(2.7)

(2.0)(2.4)(1.3)

(5.9)(4.4)

2.8

Margin (%)

Revenue(€m)

y gunfavorable product mix

604668695686

633

2,786

2,600

( )

Special items2)Comp.

growth (%)

02 (1)(2) (1)(3)--3) --3)

Q4 Q4 FY13EBITA reported (41) (30) (53)

therein:Total Special items (10) (48) (179)

Q2FY13

Q1FY13

Q4FY12

Q3FY13

Q4FY13

FY13FY12

growth (%)

Growth (%) (7)(8) --3)(7)(7)(5)--3)

Management presentation Q4 FY13 (preliminary figures) | November 12, 201312© OSRAM Licht AG 2013. All rights reserved.

1) Adjusted for “Special Items” 2) "Special items” in this context include certain items, e.g. (personnel) restructuring costs, that will also occur in future periods3) Growth rates FY12 not available (due to change in segment structure as of FY13)

Luminaires & Solutions: Restructuring initiated in Luminaires and ServicesRestructuring initiated in Luminaires and Services

Revenue and EBITA margin development

0

Comments Q4 y-o-y

Continued comp. growth of the luminairesbusiness with double-digit contribution to the

(8 9) (6 7)0

EBITAMargin (%)

(11.4)Adj. EBITA

Margin1) (%)current quarter; again based on strong SSL outdoor demand for new products

Growth across all regions, however, held back in Americas by declining services business

(11.5)(13.5)(18.2)

(22.9)

(11.5)(18.0)

(8.9) (6.7)

(15.1)

EBITA heavily burdened by transformation costs related to the restructuring of the luminaires and services businesses

Profitability expected to benefit when t t i t t t t i li h

602

561

(41.7)

Revenue(€m)

Special items2)

restructuring starts to materialize; however, burden on revenue anticipated in the next quarters

155131128

148154

0 --3)

( )(6)4

Q4 Q4 FY13EBITA reported (17) (65) (128)

therein:Total Special items (4) (54) (64)

FY12 FY13Q4FY13

Q3FY13

Q2FY13

Q1FY13

Q4FY12

Comp.growth (%)

0 (6)

Growth (%) (7)1 --3)(7)(8)(12)--3)

--3)(14)

(8) (6)

Management presentation Q4 FY13 (preliminary figures) | November 12, 201313© OSRAM Licht AG 2013. All rights reserved.

1) Adjusted for “Special Items” 2) "Special items” in this context include certain items, e.g. (personnel) restructuring costs, that will also occur in future periods3) Growth rates FY12 not available (due to change in segment structure as of FY13)

Growth (%) (7)1 -- )(7)(8)(12))

St FCF d l tStrong FCF development

Group (€m)

Net Debt bridgeCapital Expenditure+30%

901869SP 38

18743

+11%

20715162

-23-35

3720

Q4 13

3 4

2718

Q4 12

3 6

2417

L&COS

OtherL&S

59 87

63

FY 12

8 14

6243

FY 13

9 10

55

Δ Non curr.

ΔNWC

EBITDANet Liquidity

108

Other income /

Mainly taxes

-90

CAPEX

-22

Other invest./

172

Net Liquidity

FCF 85

Capex as% of revenue 6.7% 3.9%

Working Capital

assets &liab.

Q3 FY 2013

expense paid financing activities

Q4 FY 2013

Free Cash Flow ROCEGroup WC

284277 2)

968

1,145

-113-126

Trade receivables

Inventories

853

1,258

823

1,044

1,384

851

1,118 1.9%

WACC 8.5%

Turns1)4.3

FY 13FY 12

-223-677Trade payables

FY13FY12

-609

FY11

-586

3.6 4.6FY 13FY 12

-11.3%

Management presentation Q4 FY13 (preliminary figures) | November 12, 201314© OSRAM Licht AG 2013. All rights reserved.

1) Defined as revenue (last twelve months) divided by working capital 2) Excl. 500 pension funding in FY 2012

Solid balance sheetSolid balance sheetGroup (€m)

Adjusted N t D bt

Equity 1,946 2,113

+1671,096

2,169

Net Debt

PensionPlans1)

596-163

-3372)

,

490

595Credit

guarantees

FinancialNet Debt

11 95

490

11

187

0

359Capital strengtheningof ~500 by Siemens

Adj N t D bt /

Pro-forma FY123)

Capital strengtheningby Siemens

(Oct. 31 2012)

Compensation for losses by

Siemens(Nov. 2012)

FY 12 (Sep. 30)

FY 13 (Sep. 30) 3)

-1720

Adj. Net Debt / equity ratio 56% 28% 9%

Equity ratio 38% 42% 49%

1) Pension plans and commitments similar to pensions2) As of September 30, 2012, compensation for loss (337) reflected in position "Receivables from Siemens Group" but not in position "Financial receivables from Siemens Group";

f f ( ) f S

Management presentation Q4 FY13 (preliminary figures) | November 12, 201315© OSRAM Licht AG 2013. All rights reserved.

therefore reflected in equity but not in net debt (cash) as of September 30, 20123) Based on IAS 19R

Key financial metricsKey financial metricsGroup (€m)

Q4 FY12 Q4 FY13 Change ( )

FY12 FY13 Change (y-o-y) (y-o-y)

Revenue 1,371 1,332 Nom: (3)%Comp: 4%

5,400 5,289 Nom: (2)%Comp: 2%

Gross Margin 24.4% 27.2% 280bps 25.9% 28.2% 230bpsR&D (93) (86) 7 (340) (341) (1)R&D (93) (86) 7 (340) (341) (1)SG&A (301) (315) (14) (1,056) (1,103) (47)EBITA 7 (24) (31) 51 99 48EBITA Margin 0.5% (1.8%) (230)bps 0.9% 1.9% 100bps

Adj. EBITA 13 108 95 314 410 9695 3 0 96Adj. EBITA Margin 1.0% 8.1% 710bps 5.8% 7.7% 190bps

Financial result(incl. at-equity results) (14) (10) 4 (105) (22) 83

Income before Taxes (197) (44) 153 (367) 50 417Taxes 78 16 (62) (24) (1 )Taxes 78 16 (62) (24) (17) 7Net Income (119) (29) 90 (391) 34 425

Basic EPS (in €) (1.14)1) (0.28)1) 0.86 (3.75)1) 0.26 4.01

Free Cash Flow 93 85 (8) (223) 284 507Free Cash Flow 93 85 (8) (223) 284 507CAPEX (69) (90) (21) (187) (207) (20)Net Debt / Net Liquidity (595) 172 767 (595) 172 767ROCE (17.3)% (3.8)% 1350bps (11.3)% 1.9% 1320bpsEmployees 39 2 35.1 (4 1) 39 2 35 1 (4 1)

Management presentation Q4 FY13 (preliminary figures) | November 12, 201316© OSRAM Licht AG 2013. All rights reserved.

Employees 39.2 35.1 (4.1) 39.2 35.1 (4.1)1) Pro forma

Outlook

Comp. revenue growth FY14 expected to exceed global real GDP growth,

Outlook

Comp. revenue growth FY14 expected to exceed global real GDP growth, currently estimated at approximately 3% for 20141)

Despite the initiated restructuring within LS

We expect an adjusted2) EBITA margin of more than 8% in FY142

1

We expect an adjusted2) EBITA margin of more than 8% in FY14

Cumulated gross cost savings of ~€1.2bn until FY15 OPEX targets remain unchanged3

2

OPEX targets remain unchangedTransformation costs for FY14 expected to approach €100m

Net income for FY14 expected to rise sharply

3

4

ROCE for FY14 expected to exceed cost of capital of 8.5%

F C h Fl f FY14 t d t i ith iti

5

Free Cash Flow for FY14 expected to come in with a positivetriple-digit €m amount, however below the high FY13 levelHigher cash-out for transformation costs and CAPEX

6

Management presentation Q4 FY13 (preliminary figures) | November 12, 201317© OSRAM Licht AG 2013. All rights reserved.

1) Based on IHS Global Insight 2) Excl. impact from transformation costs, spin-off- / stand alone-related costs and substantial legal and regulatory matters

CEO i iti f th t 12 thCEO priorities for the next 12 months

2

1 Drive the strategic repositioning of OSRAM towards SSL

Expand OSRAM Push for organic growth

3

2 Expand OSRAM Push for organic growth

Make the past acquisitions work3

4

Make the past acquisitions work

Reach “all in” EBITA margin target >8% by FY15 as average over the cycle 4 g g y g y

5 Identify white spot areas in regions, products and value chain

Confidence that continuous improvement becomes part of OSRAM’s DNA

Management presentation Q4 FY13 (preliminary figures) | November 12, 201318© OSRAM Licht AG 2013. All rights reserved.

OSRAM’s transformation pathOSRAM’s transformation path

>8% EBITA as Ø over the cycle

Deliver

2014

2015

F /

Transform / Execute

Transform / Execute

Continuous improvement process is

Structure /People / Processes

Focus / Prioritize

2012

2013

Q1: Equipment roll in at Wuxi plant (OS backend facility) Q2: New SSL products driving top line growth Q3: Repositioning of LS shows first effects

Continuous improvement process is part of OSRAM’s DNA

2011 Q1: Q2: Top-line bottomed out Q3: Back to profitable growth Q4: Majority of restructuring done

p g Q4: Transformation becomes part of operational business (“all in”)

Apr: New board members Jul: Start of restructuring

Jul: Restructuring progress, further consolidation of manufacturing footprint and “OPEX” program started

Management presentation Q4 FY13 (preliminary figures) | November 12, 201319© OSRAM Licht AG 2013. All rights reserved.

Jul: Start of restructuring

Financial Calendar and Investor contactsFinancial Calendar and Investor contacts

Upcoming events

November 12-15, 2013 January 29, 2014Q4 Roadshow

December 5, 2013Annual Report (online)

Preliminary first-quarter figures

February 27, 2014Annual General Meeting

Investor Relations contact

M B i T + 49 89 6213 4686Mr. Boris Tramm + 49 89 6213 4686

Munich Office + 49 89 6213 4875

Internet http://www.osram.com/ir

Email: [email protected]

Management presentation Q4 FY13 (preliminary figures) | November 12, 201320© OSRAM Licht AG 2013. All rights reserved.

DisclaimerDisclaimer

This presentation contains certain non-IFRS measures. FCF, EBITDA, EBITA, EBIT, EBITA margin, capital expenditures, capitalexpenditures as percentage of revenues and other operating income, net financial debt, net working capital and certain other itemsincluded herein are not recognized measures in accordance with IFRS and should not be considered as an alternative to theapplicable IFRS measures. We have provided these measures and other information in this presentation because we believe they

id i t ith dditi l i f ti t f O f th t FCF EBITDA EBITA EBITprovide investors with additional information to measure our performance. Our use of the terms FCF, EBITDA, EBITA, EBIT,EBITA margin, capital expenditures, capital expenditures as percentage of revenues and other operating income, net financialdebt, net working capital varies from others in our industry and should not be considered as an alternative to net income (loss),cash flows from operating activities, revenues or any other performance measures derived in accordance with IFRS as measuresof operating performance or to cash flows as measures of liquidity. FCF, EBITDA, EBITA, EBIT, EBITA margin, capitalexpenditures capital expenditures as percentage of revenues and other operating income net financial debt and net workingexpenditures, capital expenditures as percentage of revenues and other operating income, net financial debt and net workingcapital have important limitations as analytical tools and should not be considered in isolation or as substitutes for analysis of ourresults as reported under IFRS.

Certain numerical data, financial information and market data (including percentages) in this presentation have been roundedaccording to established commercial standards. As a result, the aggregate amounts (sum totals or interim totals or differences or ifnumbers are put in relation) in this presentation may not correspond in all cases to the amounts contained in the underlying(unrounded) figures appearing in the consolidated financial statements. Furthermore, in tables and charts, these rounded figuresmay not add up exactly to the totals contained in the respective tables and charts.

Management presentation Q4 FY13 (preliminary figures) | November 12, 201321© OSRAM Licht AG 2013. All rights reserved.

Top Related