Languages

Pages

Legal

12/05/2017

1

Lithium ion battery supply chain in an energy storage revolution

University of Oxford, UK Guest Lecture, 11 May 2017

Simon Moores | Managing Director Benchmark Mineral Intelligence, UK

o www.benchmarkminerals.como @sdmoores o [email protected]

GuestLecture|11May2017|UniversityofOxford 1

What is Benchmark?

Subscriptions

Events

Lithium Graphite

Cobalt

GuestLecture|11May2017|UniversityofOxford 2

Nickel

12/05/2017

2

Where do we operate in the supply chain?

GuestLecture|11May2017|UniversityofOxford 3

Upstream Downstream

RawMaterials Semiprocessed

products

Batteries Battery

Packs

Mobile/

EV/Utility

LithiumGraphiteCobalt

AnodeCathodeSeparators

CellsVariousformfactors(18650)

4-7Wh7-10kWh40-85kWh>500kWh

SmartphoneHomeEVsCommercial

How do we do this?

GuestLecture|11May2017|UniversityofOxford 4

• Firsthanddatacollection…PaloAlto,California,USHeilongjiang,NorthernChina Hirschau,Germany

12/05/2017

3

Convergence of three multi billion dollar industries: Auto, Tech, Energy

GuestLecture|11May2017|UniversityofOxford 5

Batteries

2017: The Era of the Semi Mass Market EV begins…

GuestLecture|11May2017|UniversityofOxford 6

Bolt(60kWhlithiumion)Model3(60-65kWhlithiumion)

LEAF2017(60kWhlithiumion)

12/05/2017

4

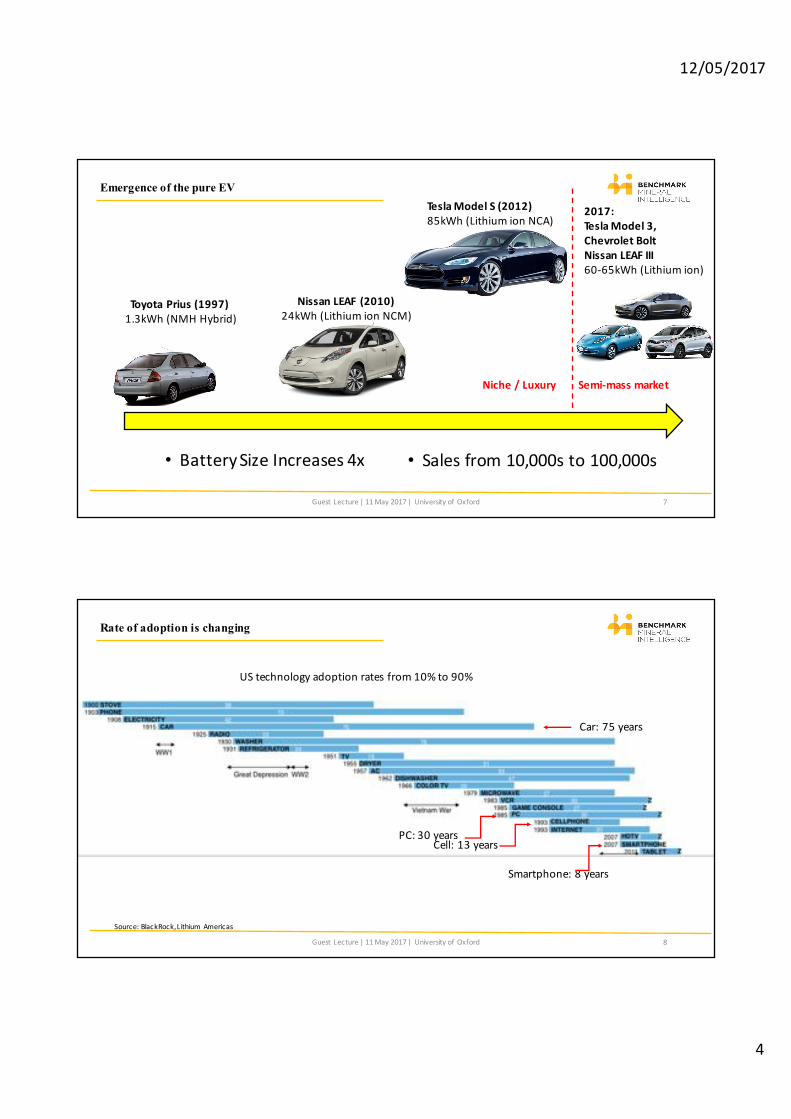

Emergence of the pure EV

GuestLecture|11May2017|UniversityofOxford 7

• BatterySizeIncreases4x • Salesfrom10,000sto100,000s

ToyotaPrius(1997)

1.3kWh(NMHHybrid)NissanLEAF (2010)

24kWh(LithiumionNCM)

TeslaModelS(2012)

85kWh(LithiumionNCA)2017:

TeslaModel3,

ChevroletBolt

NissanLEAFIII

60-65kWh(Lithiumion)

Niche/Luxury Semi-massmarket

Rate of adoption is changing

GuestLecture|11May2017|UniversityofOxford 8

Source:BlackRock,LithiumAmericas

UStechnologyadoptionratesfrom10%to90%

Car:75years

PC:30yearsCell:13years

Smartphone:8years

12/05/2017

5

Rate of adoption is changing: Smartphone

GuestLecture|11May2017|UniversityofOxford 9

Source:Nokia,Apple, BenchmarkMineral Intelligence

0 50 100 150 200 250 300 350 400

2005:NokiaN70

2007:AppleiPhone

2014:AppleiPhone 6

Daysto1mhandset sales

1year

72Days

7.2hours

180,000

8,000

300

0 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000 200,000

2016:Model3

2015:ModelX

2012:ModelS

Teslareservationsinfirst24hours

$68,000to$94,000

$110,000to$144,000*$35,000

Rate of adoption is changing: Tesla EVs

GuestLecture|11May2017|UniversityofOxford 10

Source:BenchmarkMineral Intelligence,*pricenotdisclosed onfirstdayof reservations

12/05/2017

6

WhichbatterytypeswillwintheEVrace?

GuestLecture|11May2017|UniversityofOxford 11

GuestLecture|11May2017|UniversityofOxford 12

Source:BenchmarkMineral Intelligence

1969 Late-1990s 200620072010

Watches

CarsCellphones

Powertools

Personalmusic

Smartphones

Tablets

Laptops

Hybridcars

FullElectricvehicles

Utility/Stationary

storage

Lithium-ion/NiMH Lithium-ion

I II III IV

NiMH/Lithium-ionMercuryLeadacid

Today: Fourth phase of battery commercialisation…

12/05/2017

7

GuestLecture|11May2017|UniversityofOxford 13

There is more than one type of lithium ion battery…

Lithium Cobalt Oxide (LCO)

Nickel Cobalt Manganese (NCM)

Nickel Cobalt Aluminium (NCA)

Lithium Iron Phosphate (LFP)

Lithium Manganese Oxide (LMO)

GuestLecture|11May2017|UniversityofOxford 14

Battery technology: where are we going?

Source:Panasonic, reproducedbyBenchmarkMineral Intelligence

12/05/2017

8

GuestLecture|11May2017|UniversityofOxford 15

Manufacturing cost profile of a lithium ion battery and pack

Source:BenchmarkMineral Intelligence

BillofMaterials,60%

Labour,Manufacturing,

Energy,Other

Margin

LITHIUMIONCELL

CellCost,40%

EnergyManagement

System

Other(incllabour)

Margin

BATTERYPACK

Whatbatterydemandcanweexpect?

GuestLecture|11May2017|UniversityofOxford 16

12/05/2017

9

0 100 200 300 400 500 600

2016

70-75%EVs

GuestLecture|11May2017|UniversityofOxford 17

Lithium ion battery demand expectations by 2025 (GWh)

Benchmark’s 2025 lithium demand based on battery forecasts

0 100,000 200,000 300,000 400,000 500,000

2016 2020

Tonnes

GuestLecture|11May2017|UniversityofOxford 18

12/05/2017

10

0 100000 200000 300000 400000 500000 600000 700000

Benchmark’s 2025 graphite demand based on battery forecasts

2016 2020

TonnesGuestLecture|11May2017|UniversityofOxford 19

0 50000 100000 150000 200000

Benchmark’s 2025 cobalt demand based on battery forecasts

2016 2020

TonnesGuestLecture|11May2017|UniversityofOxford 20

12/05/2017

11

Riseofthelithiumionbatterymegafactory

GuestLecture|11May2017|UniversityofOxford 21

Rise of the lithium ion megafactories continues…

0

20000

40000

60000

80000

100000

120000

Annual Cap 2016 (MWh) Expanded Capacity (MWh) 100GWh

35GWh

20GWh

GuestLecture|11May2017|UniversityofOxford 22

12/05/2017

12

0% 10% 20% 30% 40% 50% 60% 70%

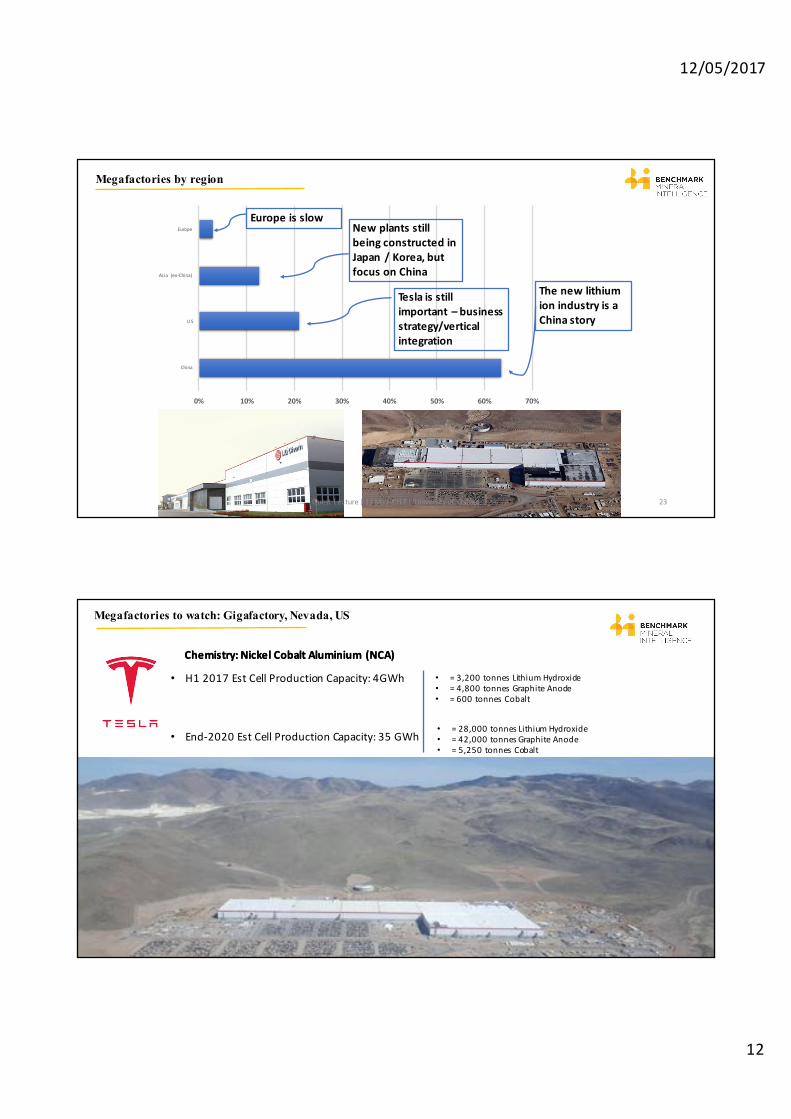

China

US

As ia (ex-China)

Europe

Thenewlithium

ionindustryisa

Chinastory

Teslaisstill

important– business

strategy/vertical

integration

Newplantsstill

beingconstructedin

Japan/Korea,but

focusonChina

Europeisslow

Megafactories by region

GuestLecture|11May2017|UniversityofOxford 23

Megafactories to watch: Gigafactory, Nevada, US

• H12017EstCellProductionCapacity:4GWh

• End-2020EstCellProductionCapacity:35GWh

• =3,200tonnesLithiumHydroxide• =4,800tonnesGraphiteAnode• =600tonnesCobalt

• =28,000tonnesLithiumHydroxide• =42,000tonnesGraphiteAnode• =5,250tonnesCobalt

Chemistry:NickelCobaltAluminium(NCA)Chemistry:NickelCobaltAluminium(NCA)

GuestLecture|11May2017|UniversityofOxford 24

12/05/2017

13

Megafactories to watch: Dalian, China

• H12017EstCellProductionCapacity:3GWh

• End-2020EstCellProductionCapacity:9GWh

• =2,400tonnesLithiumHydroxide• =3,600tonnesGraphiteAnode• =450tonnesCobalt

• =7,200tonnesLithiumHydroxide• =10,800tonnesGraphiteAnode• =1,350tonnesCobalt

Chemistry:NickelCobaltAluminium(NCA)

GuestLecture|11May2017|UniversityofOxford 25

Megafactories to watch: NingDe, China

• H12017EstCellProductionCapacity:5GWh

• End-2020EstCellProductionCapacity:100GWh

• =~3,500tonnesLithiumCarbonate• =~6,000tonnesGraphiteAnode• =~1,700tonnesCobalt

• =~75,000tonnesLithiumCarbonate• =~120,000tonnesGraphiteAnode• =~11,000tonnesCobalt

Chemistry:NickelCobaltManganese(NCM)

GuestLecture|11May2017|UniversityofOxford 26

12/05/2017

14

GuestLecture|11May2017|UniversityofOxford 27

0

500

1000

1500

2000

2500

3000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020High Low

Lithiumioncellcosts($/perkWh)

2016-2020:15-20%ayear

2000to2015:12-14%ayear

The result? Battery cell costs continue decline…

Isthereenoughlithium?

GuestLecture|11May2017|UniversityofOxford 28

12/05/2017

15

GuestLecture|11May2017|UniversityofOxford 29

Battery raw materials have hit the headlines

$12,313/tonne (March 2017) $17,000/tonne (March 2017)

LithiumHydroxideLithiumCarbonate

GuestLecture|11May2017|UniversityofOxford 30

Why has lithium hit the headlines?

12/05/2017

16

-40%

-20%

0%

20%

40%

60%

80%

100%

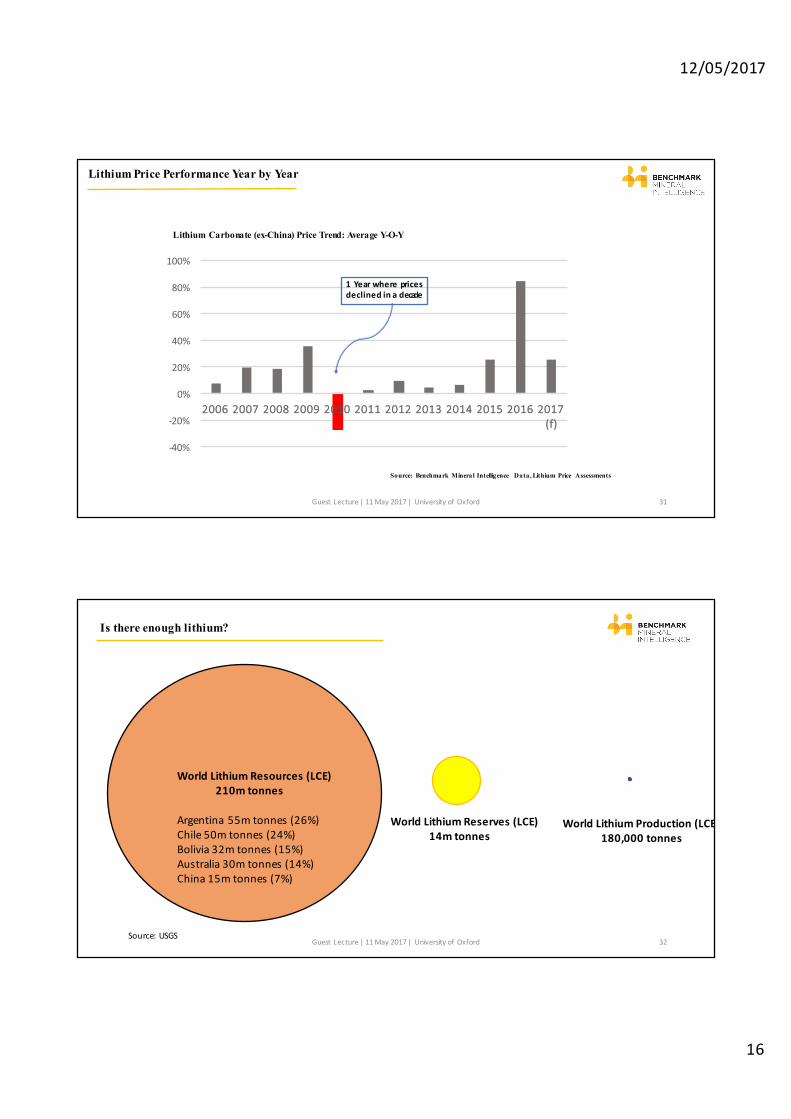

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017(f)

Lithium Carbonate (ex-China) Price Trend: Average Y-O-Y

1Yearwherepricesdeclinedinadecade

Source: Benchmark Mineral Intelligence Data, Lithium Price Assessments

Lithium Price Performance Year by Year

GuestLecture|11May2017|UniversityofOxford 31

GuestLecture|11May2017|UniversityofOxford 32

Is there enough lithium?

WorldLithiumResources(LCE)

210mtonnes

WorldLithiumReserves(LCE)

14mtonnes

Argentina55mtonnes(26%)Chile50mtonnes(24%)Bolivia32mtonnes(15%)Australia30mtonnes(14%)China15mtonnes(7%)

Source:USGS

WorldLithiumProduction(LCE)

180,000tonnes

12/05/2017

17

GuestLecture|11May2017|UniversityofOxford 33

Is there enough lithium?

94,976,569

CarsandCommercialVehiclessoldin2016

22,871,134Commercialvehicles

72,105,435

Cars

3,430GWh(150kWhav)

5,047GWh(70kWhav)

2.74mtonnesLCE

4mtonnesLCE

6.74m

tonnesLCE

Source:OICA Source:OICA Source:BenchmarkMineral Intelligence

Lithiumion

battery

production

>12,000%

Lithium

production

up3,735%

=50%globalreserves

=3%globalresources

GuestLecture|11May2017|UniversityofOxford 34

How much investment is needed?

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2005200620072008200920102011201220132014201520162017

Lithium Carbonate Low Lithium Carbonate High Lithium Hydroxide Low Lithium Hydroxide High

$1bnraised

$520mraised

$/tonne

• =20,000tonnesLCE• Shouldhave=50,000tpa• 1expensivebankruptcy• 2failedchemicalplants• 40%misallocatedcapital

• =25,000tonnes• Moretocome• Investorsmorecautiousbut

furtherdowneducationpath

12/05/2017

18

GuestLecture|11May2017|UniversityofOxford 35

What investment is needed?

Source:HouseMountainPartners,BenchmarkMineralIntelligence

~$500m~$400m

BrineMine

25,000tpa

BatteryGradeLithiumPlant

HardRockMine

Concentrator=

25,000tpaoffeedstock thatneedschemicalconversion

GuestLecture|11May2017|UniversityofOxford 36

What investment is needed?

2020 = 100,000tonnesLCE=

2025=150,000tonnesLCE=

IncrementalLithiumNeeded

$2.5bn0%allocatedbyend2017

$1.7bn50%allocatedbyend2017

Source:HouseMountainPartners,BenchmarkMineralIntelligence

12/05/2017

19

Where will the most profitable sit?

GuestLecture|11May2017|UniversityofOxford 37

Upstream Downstream

RawMaterials BatteryGrade

Materials

Batteries Battery

Packs

Mobile/

EV/Utility

LithiumGraphiteCobalt

AnodeCathodeSeparators

CellsVariousformfactors(18650)

4-7Wh7-10kWh40-85kWh>500kWh

SmartphoneHomeEVsCommercial

GuestLecture|11May2017|UniversityofOxford 39

Othertrendstowatch

12/05/2017

20

GuestLecture|11May2017|UniversityofOxford 39

Othertrendstowatch

Corporate Social Responsibility

GuestLecture|11May2017|UniversityofOxford 39

GuestLecture|11May2017|UniversityofOxford 39

Othertrendstowatch

Corporate Social Responsibility

GuestLecture|11May2017|UniversityofOxford 40

12/05/2017

21

GuestLecture|11May2017|UniversityofOxford 39

Othertrendstowatch

Recycling

• Tesla seeking torecycleitsbatteriespost2020• Gigafactorycellswillnothavesecondlifeinutilitystoragepost80%capacity• Nomajorplansinplaceyet, justaninitiativeforspentbatteries

GuestLecture|11May2017|UniversityofOxford 41

GuestLecture|11May2017|UniversityofOxford 39

Othertrendstowatch

Recycling

• Recyclingabout responsiblydisposingofbatteries• Extractinghazardouswaste• Forcingcompaniestothinkaboutmanufacturing

• Notlikelytobeaboutrawmaterialsupply• Cobaltopportunity• Nickelopportunity• Lithium&Graphiteunlikelybefore2023(economics)

Credit:Bloomberg

GuestLecture|11May2017|UniversityofOxford 42

12/05/2017

22

GuestLecture|11May2017|UniversityofOxford 43

“Changeoccurswhenpeoplearebusydiscussingwhetherchangewilloccur.”