Languages

Pages

Legal

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 3

1. Overview ..........................................................................................................................................3

2. Purpose of Sasria .............................................................................................................................4

3. Vision ................................................................................................................................................4

4. Mission .............................................................................................................................................4

5. Core Values ......................................................................................................................................4

6. Mandate ...........................................................................................................................................5

7. Operating Principles .......................................................................................................................5

8. Business Model ................................................................................................................................6

9. Delegation of authority ..................................................................................................................8

10. Governance Framework..................................................................................................................8

11. Organisational Structure ..............................................................................................................13

12. Financial Resources Income .........................................................................................................16

13. Risk Management .........................................................................................................................16

13.1 Enterprise Risk Management process ................................................................................................. 16

14. Analysis of Competencies & Environment ..................................................................................19

14.1 Current competencies & resources ...................................................................................................... 19

14.2 Environment within which Sasria operates ...................................................................................... 19

15. Strategic Focus Areas & Strategic Objectives .............................................................................23

15.1 Sustainable revenue growth .................................................................................................................. 24

15.2 Capital management ................................................................................................................................ 24

15.3 Innovation (products & services) .......................................................................................................... 24

15.4 Infrastructure & cost management ...................................................................................................... 24

15.5 People, capacity and capability ............................................................................................................ 25

15.6 Regulatory environment ......................................................................................................................... 25

15.7 Customer-centricity ................................................................................................................................... 25

15.8 Brand development .................................................................................................................................. 25

16. Beyond 2020 ..................................................................................................................................26

16.1 LSM/SME feasibility project .................................................................................................................... 27

16.2 Agriculture insurance administration project .................................................................................. 29

16.3 Enterprise Architecture project ............................................................................................................. 31

16.4 Incubation programme ............................................................................................................................ 34

16.5 IFRS 17 project ............................................................................................................................................. 35

17. SWOT Analysis ...............................................................................................................................36

18. Dividend Policy .............................................................................................................................37

19. Key Strategic & Financial Assumptions .......................................................................................37

20. Key Performance Indicators .........................................................................................................37

21. Alignment of Strategic Objectives to the National Development Plan ....................................45

22. Borrowing Plan ..............................................................................................................................46

23. Supporting Documents ................................................................................................................76

24. Approval ........................................................................................................................................47

ANNEXURE 1: SIGNIFICANCE & MATERIALITY FRAMEWORK .....................................................................48

ANNEXURE 2: FINANCIAL PLAN ....................................................................................................................49

ANNEXURE 3: TOP 10 RISK REGISTER ...........................................................................................................52

ANNEXURE 4: FRAUD PREVENTION PLAN ...................................................................................................66

Corporate Plan & Budget 2018 - 2019

1. OVERVIEW

Sasria SOC Limited (Sasria) is a public enterprise listed under Schedule 3B of the Public Finance Management Act No. 1 of 1999. It is a Short-Term Insurance Com-pany that provides coverage for damage caused by special risks such as politically motivated malicious acts, riots, strikes, terrorism and public disorders.

During the 1976 Soweto uprisings, the Short-Term Insurance Industry decided that it could no longer underwrite losses arising from politically motivated acts of civil disobedience and unrest of the time as the risk was too high and it was dif-fi cult, if not impossible, to purchase reinsurance cover. This resulted in the incorporation of the South African Special Risk Insurance Association (SASRIA) as a Section 21 Company under the old Companies Act (No. 61 of 1973).

The operational structure of Sasria comprised a membership network pool that included all registered Short-Term Insur-ance Companies that underwrite the fi re peril.

Section 6 of the Finance Act No. 94 of 1978 empowered the then Minister of Finance to enter into a Reinsurance Contract with Sasria as a Stop Loss Re-insurer. This Section also aff orded a monopoly to Sasria as the only Insurer with authority to underwrite political perils in the Republic of South Africa. The Reinsurance of Material Damage and Losses Act No. 56 of 1989 had the same eff ect as Section 6 of the Finance Act 94 of 1978.

In terms of Section 10 (i) (t) of the Income Tax Act No. 58 of 1962, Sasria was exempted from paying tax from the date of incorporation. This Section was however repealed, and from January 1996 Sasria became a tax paying entity.

Financially, Sasria started with a zero base. Due to lack of worldwide reinsurance coverage, it was reinsured to a limited ex-tent by the Members of Sasria. In addition, the stop loss coverage aff orded by Government gave cover in excess of Sasria’s reserves and reinsurances in an unlimited amount. Initial rates were agreed with the industry as the risks which Sasria cov-ers were actuarially considered to be uninsurable.

At the time, the mission statement was to underwrite any perils that the conventional insurance market was unwilling or unable to underwrite. Consequently, the perils of Sasria were expanded and encapsulated in the Reinsurance of Material Damage and Losses Act No. 56 of 1989 read in conjunction with the Conversion of Sasria Act No. 134 of 1998.

From the mid 1980’s to date, Sasria perils comprised of the following:i. any act (whether on behalf of any organisation, body or person, or group of persons) calculated or directed to over-

throw or infl uence any State or Government, or any provincial, local or tribal authority with force, or by means of fear, terrorism or violence

ii. any act which is calculated or directed to bring about loss or damage in order to further any political aim, objective or cause, or to bring about any social or economic change, or in protest against any State or Government, or any provin-cial, local or tribal authority, or for the purpose of inspiring fear in the public, or any section thereof

iii. any riot, strike or public disorder, or any act or activity which is calculated or directed to bring about a riot, strike or pub-lic disorder (the term “Public Disorder” shall be deemed to include civil commotion, labour disturbances or lockouts)

iv. any attempt to perform any act referred to in clause (i), (ii) or (iii) abovev. the act of any lawfully established authority in controlling, preventing, suppressing or in any other way dealing with any

occurrence referred to in clause (i), (ii), (iii) or (iv) above.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 54 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Given the monopoly, tax exempt status and low loss history over the years, Sasria accumulated substantial reserves. Ac-cordingly, in the mid 1980’s it was able to purchase reinsurance coverage in the international markets obviating the need for the insignifi cant coverage provided by its members.

In 1998, the Government together with Sasria and its Members reached consensus that the assets of Sasria should be dis-tributed for the benefi t of the people of South Africa. As a Section 21 Company, Sasria was unable to distribute any surplus-es generated. To remedy this situation, the Conversion of Sasria Act No. 134 of 1998 (the Act) was passed and it eff ectively:

• Converted Sasria to a Limited Company.• Made the State the sole shareholder of Sasria Limited.• Allowed an actuarial determination of assets surplus to the needs of Sasria.• Allowed for the payment of the determined surplus as a special dividend payable to the Shareholder to be used to

off -set interest on State debt.• Allowed for the privatisation of Sasria Limited.

The Act was eff ectively implemented and over a two-year period, Sasria was able to pay special dividends totalling approxi-mately R11 billion, to Government.

Currently Sasria functions through a network of agents, the underlying insurance companies. The agents issue the Sasria Coupons and Policies on behalf of Sasria, permit Sasria to attach to the terms and conditions of the underlying policy and are responsible for the premium collection.

During 2012, the new Companies Act (No. 71 of 2008) came into eff ect. One of the requirements was the inclusion of “SOC” in the company name for all State Owned Companies. Sasria Limited became known as Sasria SOC Limited.

2. PURPOSE OF SASRIA

The principal purpose of Sasria is to provide cover for damage caused by those risks listed in the Reinsurance of Material Damage and Losses Act No. 56 of 1989, and any other risks which may be deemed necessary or viable by management and board of directors of Sasria. In addition, it is the purpose of Sasria to research and investigate coverage for any special risk that can be considered to be of national interest.

3. VISION

The vision of Sasria is “To protect the assets of all in South Africa against special risks”.

4. MISSION

The vision will be achieved via our mission of driving a sustainable and vibrant business by:• Balancing shareholder value creation with positive social impact;• Providing excellent customer service;• Being clear and consistent in our communication to our stakeholders;• Developing the skills and capacity of our employees;• Improving our current strategic partnerships and establishing new ones; and• Providing innovative and relevant products.

5. CORE VALUES

The following values underpin Sasria’s pursuit of its stated vision and mission:

Professionalism: We will treat our stakeholders, being customers, employees and shareholder with respect and dedication while remaining accountable to them.

Integrity: We will conduct ourselves in a manner that is fair, transparent and ethical, and uphold high levels of equality and trust.

Teamwork: In the performance of our tasks we will be guided by the ideals of unity of purpose, cooperation and mutual respect.

Innovation: We will create opportunities for creativity and learning, and encourage the same amongst our employees.

Customer centric: We will strive at all times to meet and exceed our customer’s expectations.

6. MANDATE

Sasria is the only short-term insurer in South Africa that provides cover against special risks such as civil commotion, public disorder, strikes, riots and terrorism.

Sasria is accountable to the Minister of Finance via National Treasury. Like all the other insurance companies in South Af-rica, Sasria operates within a well-developed framework regulated by the Financial Services Board (FSB), the non-banking fi nancial services industry regulator. Sasria is a member of various industry associations.

Sasria has a dual mandate:

• Our legislative mandate as a short-term insurance company is to provide cover for special risk events in terms of the Reinsurance of Material Damages Act; and

• Our broader strategic mandate as a state-owned company is to make a positive contribution to transforming the fi nancial services industry in line with the National Development Plan (NDP), in order to create a better, sustainable economic environment for all South Africans.

Sasria delivers on this mandate in a number of ways. These range from delivering continued solid fi nancial results, which enables the company to remain self-funded as a state-owned company, whilst growing and transforming the insurance market and fi nancial sector through a number of initiatives; and Sasria’s Corporate Social Investment (CSI) spend.

7. OPERATING PRINCIPLES

Sasria conducts business in a responsible, disciplined, professional and well-governed way. As a state-owned company, Sasria plays a meaningful role in society by off ering products that will assist in the protection of assets in South Africa against potentially catastrophic special risk events. The company is proudly South African and passionately committed to accelerating its growth and business transformation goals. Sasria’s operating principles are:

• To operate with a core staff compliment.• To operate via an outsourced distribution network (agents) comprising of other short-term insurance companies.• To have suffi cient reinsurance treaties and covers in place• To strive to achieve optimal investment returns.

Sasria also:• Identifi es the insurance needs of the public through research and development.• Conducts itself in a manner that promotes co-operation, mutual understanding and fosters good relations with

relevant third parties, agent companies and intermediaries (brokers) and end-customers in the same manner.• Develops and maintains a work environment that encourages employment equity and skills development.• Establishes a co-operative relationship with employees in order to work towards common goals of profi tability and

high performance.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 76 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

8. BUSINESS MODEL

Sasria’s unique business model (Figure 1) enables the company to minimise its operating expenses, off er an extremely af-fordable product to protect the assets of the people of South Africa against special risks, and sustain its solid track record of fi nancial performance.

The company does not sell its products directly to end-customers. Instead, it enters into agreements with other short-term insurance companies and intermediaries in South Africa,who then as agents, represent and sell the special risks cover to the end-customers, be they individuals, businesses, government or corporate entities. The agents and brokers (intermedi-aries) engage with the end-customers on policy administration and collect premiums on behalf of Sasria, in exchange for a service fee.

The only contact that Sasria has with end-customers is on the settlement of claims. Customers submit claims to the inter-mediaries or insurance companies, which confi rm their validity prior to submission to Sasria. Sasria receives and verifi es all claims before payment directly to the customer.

Profi ts, after payment of all claims are invested, subject to retention of adequate liquid reserves. Sasria’s investments earn good investment returns in the form of interest and/or dividends and capital growth.

Operational costs for managing the business include reinsurance premium to reinsurers, the salary bill for employees, compensation to directors and procurement of goods and services. Sasria also pays all the relevant taxes and statutory fees to the authorities, including dividends to the shareholder from the reserves.

Agent

companies and

brokers

Reinsurers

Investments

People

Suppliers

Authorities

Shareholder

Customers

S a s r i a

Pay

clai

ms

Pay commission

Receive

premiums, claim

s

Receive return commission

and reinsurance recoveries

Pay reinsurance

premiums

Invest profit

Pay premiums Submit claims

Pay salaries, directors’ and consulting fees

Make paymentsPay taxes and fees

Pay dividendReceive interest,

dividends, capital growth

Receive servicesProcure products and

services

Figure 1: Sasria’s business model.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 98 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

9. DELEGATION OF AUTHORITY

The Board of Directors of Sasria derives its authority from the following:

• Companies Act No. 71 of 2008• Conversion of Sasria Act No. 134 of 1998• Reinsurance of Material Damages and Losses Act No. 56 of 1989• Public Finance Management Act No. 1 of 1999• Short-Term Insurance Act No. 53 of 1998• King IV Report on Governance for South Africa 2016• FSB License• FSB Regulations• National Treasury’s Signifi cance- and Materiality Frameworks.

10. GOVERNANCE FRAMEWORK

Sasria will continue its practice of applying sound governance structures, procedures and processes during the next fi nancial year. We consider these fundamental to the eff ective delivery of our dual mandate, as well as ensuring our company’s long-term sustainability.

The Board is committed to the principles of openness, transparency, integrity and accountability as advocated in the King IV Report on Corporate Governance for South Africa 2016 (King IV). This commitment to good governance is formalised in the company’s charters, policies and procedures.

The Board has fi ve committees which assist it to drive Sasria’s strategic mandate. These include the four statutory committees, namely the Audit Committee, Risk Committee, Remuneration and Nomination Committee and the Social and Ethics Commit-tee, as well as the Investment Committee (Figure 2).

Figure 2: Sasria’s corporate governance framework.

Currently, the Board of Directors comprises eight Non-Executive Directors, of whom seven are independent and one Executive Director, with the vacancy of the Finance Director position (Table 1). They meet minimum four times a year to provide strategic direction of the company.

Board members have been assigned committee responsibilities in accordance with the Public Finance Management Act No. 1 of 1999, Companies Act No. 71 of 2008, and the King IV Report on Corporate Governance.

Tabl

e 1:

Sas

ria B

oard

of D

irect

ors a

nd E

xecu

tive

Man

agem

ent (

as a

t 1 A

pril

2018

).

Init

ials

Tit

le &

su

rna

me

Fu

ll n

am

eG

en

de

r, a

ge

& r

ace

Co

mp

an

y &

tit

leT

itle

Sa

sria

Bo

ard

Oth

er

Bo

ard

pa

rtic

ipa

tio

n

Qu

ali

fi ca

tio

ns

Fie

ld o

f

ex

pe

rtis

e

Nu

mb

er

of

ye

ars

’

ex

pe

rie

nce

M.A

.M

r Sam

ieM

oham

ed

Adam

Mal

e(6

6)Co

lour

ed

Tim

esqu

are

Inve

st-

men

ts (P

ty) L

td(D

irect

or)

Non

-Exe

cutiv

e D

irect

or-C

ha

irp

ers

on

of

Sasr

ia B

oard

Me

mb

er:

-Ris

k Co

mm

ittee

-Inve

stm

ent C

omm

ittee

-Rem

uner

atio

n &

Nom

i-na

tion

Com

mitt

ee

Tim

esqu

are

Inve

stm

ents

(P

ty) L

td

Asso

ciat

e of

the

Inst

itute

of

Ris

k M

anag

emen

t SA

(IR

MSA

) 200

4Fe

llow

of t

he C

hart

ered

In

sura

nce

Inst

itute

197

8Fe

llow

of t

he In

sura

nce

Inst

itute

of S

outh

Afri

ca

1982

Insu

ranc

e, R

ein-

sura

nce,

Str

ateg

y &

Risk

Man

age-

men

t

45

S.H

.M

r Sch

oem

anSt

epha

nus

Her

man

usM

ale

(54)

Whi

te

Gua

rdris

k In

sura

nce

Gro

up(M

anag

ing

Dire

ctor

)

Non

-Exe

cutiv

e D

irect

or-C

ha

irp

ers

on

of R

isk

Com

mitt

ee-D

eput

y Ch

airp

erso

n of

Au

dit C

omm

ittee

Me

mb

er:

-Boa

rd

SAIA

, G

uard

risk

Bach

elor

of C

omm

erce

(U

nive

rsity

of P

reto

ria)

1983

Hig

her E

duca

tion

Dip

lom

a (U

nive

rsity

of

Pret

oria

) 198

4M

aste

r of B

usin

ess A

d-m

inis

trat

ion

(Uni

vers

ity

of P

reto

ria) 1

989

Insu

ranc

e, R

ein-

sura

nce,

Str

ateg

y &

Risk

Man

age-

men

t

31

R.M

r Mot

hapo

Rant

iM

ale

(36)

Blac

k

Actu

ary

and

Serv

ice

Entr

epre

neur

– M

at-

lotlo

Gro

up

Non

-Exe

cutiv

e D

irect

or-C

ha

irp

ers

on

of I

nves

t-m

ent C

omm

ittee

-Dep

uty

Chai

rper

son

of

Risk

Com

mitt

eeM

em

be

r:

-Boa

rd-R

emun

erat

ion

& N

omi-

natio

n Co

mm

ittee

Land

Ban

k In

sura

nce

Com

pany

Mor

uba

Cons

ulta

nts &

Ac

tuar

ies

Mat

lotlo

G

roup

(Pty

) Lt

d

Bach

elor

of E

cono

mic

Sc

ienc

e (U

nive

rsity

of t

he

Witw

ater

sran

d) 2

001

Bach

elor

of S

cien

ce (H

on-

ours

) (U

nive

rsity

of t

he

Witw

ater

sran

d) 2

002

Fello

w o

f the

Fac

ulty

of

Actu

arie

s 200

4Fe

llow

of t

he A

ctua

rial

Soci

ety

of S

outh

Afri

ca

2004

Actu

ary

& Q

uan-

titat

ive

Ana

lyst

; In

vest

men

t

15

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 1110 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Init

ials

Tit

le &

su

rna

me

Fu

ll n

am

eG

en

de

r, a

ge

& r

ace

Co

mp

an

y &

tit

leT

itle

Sa

sria

Bo

ard

Oth

er

Bo

ard

pa

rtic

ipa

tio

n

Qu

ali

fi ca

tio

ns

Fie

ld o

f

ex

pe

rtis

e

Nu

mb

er

of

ye

ars

’

ex

pe

rie

nce

J.M.

Mr N

air

Jaya

seel

an

Man

icku

m

Nai

r

Mal

e(5

4)In

dian

Nat

iona

l Tre

asur

y(A

ctin

g Ac

coun

tant

–

Gen

eral

)

Non

-Exe

cutiv

e D

irect

orM

em

be

r:

-Boa

rd;

-Soc

ial &

Eth

ics C

omm

it-te

e;-A

udit

Com

mitt

ee

N/a

Bach

elor

of C

omm

erce

Nat

iona

l Dip

lom

a in

G

over

nmen

t Fin

ance

Corp

orat

e G

over

-na

nce

35

B.J.

Ms M

kang

isa

Bule

lwa

Jean

ieFe

mal

e(5

9)Bl

ack

Mka

ngis

a In

vest

men

t(E

xecu

tive

Dire

ctor

)N

on-E

xecu

tive

Dire

ctor

-Ch

air

pe

rso

n o

f Soc

ial &

Et

hics

Com

mitt

ee-D

eput

y Ch

airp

erso

n of

Re

mun

erat

ion

& N

omin

a-tio

n Co

mm

ittee

Me

mb

er:

-Boa

rd

Mka

ngis

a In

vest

men

t, Bo

sasa

, Zib

ula

Expl

orat

ion

Opi

mar

t, In

yand

a En

-er

gy, K

hang

ela

Phan

da,

Nta

mba

nane

Re

sour

ces,

Mas

ter i

n Ed

ucat

ion

for

Prim

ary

Hea

lth C

are,

Dip

(H

R)

Rein

sura

nce

20

M.O

.M

s Ndl

ovu

Mar

gare

t O

ctav

iaFe

mal

e(6

6)Bl

ack

Vulis

ango

Hol

ding

s(S

hare

hold

er)

Non

-Exe

cutiv

e D

irect

or-C

ha

irp

ers

on

of

Rem

uner

atio

n &

Nom

ina-

tion

Com

mitt

ee-D

eput

y Ch

airp

erso

n of

So

cial

& E

thic

s Com

mit-

tee

Me

mb

er:

-Boa

rd-In

vest

men

t Com

mitt

ee

Sim

mer

&

Jack

Min

es

Ltd,

Vul

isan

go

Hol

ding

s, Ri

te

Futu

re C

aree

rs

CC, K

agis

o So

lutio

ns (P

ty),

Bosa

sa O

pera

-tio

ns.

Bach

elor

of S

ocia

l Sci

-en

ce (U

nive

rsity

of t

he

Nor

th) 1

977

Man

agem

ent D

iplo

ma

(Lin

coln

Uni

vers

ity) 1

992

Stud

y of

Lea

ders

hip,

Au

thor

ity &

Org

anis

atio

n (T

avis

tock

Inst

itute

of H

u-m

an R

elat

ions

, Lon

don)

19

87

Hum

an C

apita

l39

Init

ials

Tit

le &

su

rna

me

Fu

ll n

am

eG

en

de

r, a

ge

& r

ace

Co

mp

an

y &

tit

leT

itle

Sa

sria

Bo

ard

Oth

er

Bo

ard

pa

rtic

ipa

tio

n

Qu

ali

fi ca

tio

ns

Fie

ld o

f

ex

pe

rtis

e

Nu

mb

er

of

ye

ars

’

ex

pe

rie

nce

T.M

s Mba

tsha

Tand

oFe

mal

e(4

4)Bl

ack

Indy

ebo

Cons

ultin

g(A

ssoc

iate

Dire

ctor

)N

on-E

xecu

tive

Dire

ctor

Me

mb

er:

-Boa

rd-A

udit

Com

mitt

ee-In

vest

men

t Com

mitt

ee

(Dep

uty

Chai

rper

son)

-Soc

ial &

Eth

ics C

om-

mitt

ee

Nex

ia S

AB&

TBa

chel

or o

f Com

mer

ce

(Uni

vers

ity o

f For

t Har

e)

1995

Mas

ter o

f Bus

ines

s Lea

d-er

ship

(UN

ISA)

201

0

Fina

ncia

l Man

age-

men

t?

M.T

.M

s Mou

tlane

Met

ja Ts

h-w

arel

oFe

mal

e(4

3)Bl

ack

Uba

nk(H

ead

of In

tern

al

Audi

t)

Non

-Exe

cutiv

e D

irect

or-C

ha

irp

ers

on

of A

udit

Com

mitt

eeM

em

be

r:

-Boa

rd-R

isk

Com

mitt

ee

Lion

of A

frica

In

sura

nce

Bach

elor

of C

omm

erce

(In

form

atio

n Sy

stem

s)

(Uni

vers

ity o

f Sou

th

Afric

a) 1

996

Bach

elor

of A

ccou

ntin

g Sc

ienc

e (H

onou

rs) (

Uni

-ve

rsity

of S

outh

Afri

ca)

1999

Char

tere

d Ac

coun

tant

(S

A)(S

AIC

A) 2

003

Fina

ncia

l Man

age-

men

tRi

sk M

anag

emen

tAu

ditin

g

?

C.M

.M

r Mas

ondo

Cedr

ick

Mnw

abis

iM

ale

(50)

Blac

k

Sasr

ia S

OC

Lim

ited

Man

agin

g D

irect

orSo

uth

Afric

an

Actu

arie

s D

evel

opm

ent

Prog

ram

me

(Cha

irper

son)

Bach

elor

of C

omm

erce

(E

cono

mic

s) (U

nive

r-si

ty o

f Dur

ban-

Wes

tvill

e)

1991

Dip

lom

a in

Insu

ranc

e (In

sura

nce

Inst

itute

of

Sout

h Af

rica)

199

7Ad

vanc

ed D

iplo

ma

in

Insu

ranc

e (In

stitu

te o

f So

uth

Afric

a) 1

998

Adva

nced

Man

age-

men

t and

Lea

ders

hip

Prog

ram

me

(Oxf

ord

Uni

vers

ity, S

aïd

Busi

ness

Sc

hool

) 201

5

Insu

ranc

e,

Rein

sura

nce,

Ris

k M

anag

emen

t

25

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 1312 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Init

ials

Tit

le &

su

rna

me

Fu

ll n

am

eG

en

de

r, a

ge

& r

ace

Co

mp

an

y &

tit

leT

itle

Sa

sria

Bo

ard

Oth

er

Bo

ard

pa

rtic

ipa

tio

n

Qu

ali

fi ca

tio

ns

Fie

ld o

f

ex

pe

rtis

e

Nu

mb

er

of

ye

ars

’

ex

pe

rie

nce

n/a

Vaca

ntN

/aN

/aSa

sria

SO

C Li

mite

dFi

nanc

e D

irect

orN

/aN

/aN

/aN

/aS.

Ms H

arro

p-A

llin

Suza

nne

Fem

ale

(39)

Whi

te

Sasr

ia S

OC

Lim

ited

Chie

f Ris

k O

ffi ce

rN

/aCh

arte

red

Acco

unta

nt

(SA)

(SA

ICA)

200

5Ba

chel

or o

f Com

mer

ce

Hon

ours

(Acc

ount

ing)

- (

Uni

vers

ity o

f Joh

anne

s-bu

rg) 2

002

Insu

ranc

e,

Fina

nce,

Ris

k an

d Ca

pita

l Man

age-

men

t

13

M.S

.M

r Mav

uso

Mzi

wox

olo

Succ

ess

Mal

e(4

6)Bl

ack

Sasr

ia S

OC

Lim

ited

Exec

utiv

e M

anag

er: G

ov-

erna

nce

& Se

cret

aria

tM

biza

na L

ocal

M

unic

ipal

-ity

(Aud

it Co

mm

ittee

m

embe

r)

Bach

elor

of P

rocu

ratio

nis

(Uni

vers

ity o

f For

t Har

e)

1993

Bach

elor

of L

aws (

Uni

ver-

sity

of F

ort H

are)

199

5G

ener

al M

anag

emen

t Pr

ogra

m (G

ordo

n In

sti-

tute

of B

usin

ess S

tudi

es)

2013

Gov

erna

nce,

Le

gal,

Com

-pa

ny S

ecre

taria

l, Co

mpl

ianc

e, R

isk

Man

agem

ent

22

N/a

Vaca

ntN

/aN

/aN

/aEx

ecut

ive

Man

ager

: Hu-

man

Cap

ital &

Fac

ilitie

sN

/aN

/aN

/aN

/a

F.M

s Ben

jam

inFa

reed

ahFe

mal

e(4

5)Co

lour

ed

Sasr

ia S

OC

Lim

ited

Exec

utiv

e M

anag

er:

Insu

ranc

e O

pera

tions

&

Stak

ehol

der M

anag

e-m

ent

N/a

N/a

Insu

ranc

e op

era-

tions

A.S

.M

r Nko

siA

phol

o Sa

mso

nM

ale

(49)

Blac

k

Sasr

ia S

OC

Lim

ited

Exec

utiv

e M

anag

er: B

usi-

ness

Ope

ratio

ns &

ITRi

sk &

Com

pli-

ance

Com

mit-

tee

mem

ber

at H

olla

rd

Insu

ranc

e

Mas

ter o

f Sci

ence

in

Info

rmat

ion

Syst

ems

(Lee

ds B

ecke

tt U

nive

r-si

ty) 2

001

Hig

her D

iplo

ma

in B

usi-

ness

Stu

dies

(Ins

titut

e of

Bu

sine

ss M

anag

emen

t)

2000

IT M

anag

ers C

ertifi

ca-

tion

(Brit

ish

Com

pute

r So

ciet

y) 2

006

Oxf

ord

CIO

Aca

dem

y (O

xfor

d U

nive

rsity

, Saï

d Bu

sine

ss S

choo

l) 20

15

IT m

anag

emen

t13

11. ORGANISATIONAL STRUCTURE

The company has an envisaged staff complement of 103 permanent positions (Figure 3) in six divisions (Table 2) for 2018-2019. Interns and temporary positions are not refl ected.

The Executive Management comprises the following:• Managing Director• Finance Director• Chief Risk Offi cer• Executive Manager: Governance & Company Secretariat• Executive Manager: Insurance Operations & Stakeholder Management• Executive Manager: Business Operations & IT• Executive Manager: Human Capital & Facilities

Table 2: Sasria’s business and functional structure for 2018-2019.

DIVISIONS DEPARTMENTS

Insurance Opera-tions

Underwriting Claims Reinsurance Marketing & Communi-cations

Customer Relationship Management

Finance Finance Investment Procurement

Governance & Company Secre-tariat

Compliance Legal Company Secretariat

Control Functions Internal Audit Risk Management Actuarial Services Quality Assurance

Human Capital Human Capital Facilities Corporate Social Investment

Business Opera-tions & IT

Project Manage-ment

Process Manage-ment

Information Tech-nology

The Underwriting, Claims, Customer Relationship Management and Actuarial Services departments represent the core functions of Sasria.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 1514 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Figu

re 3

: Sas

ria’s

orga

nisa

tiona

l str

uctu

re fo

r 201

8-20

19.

Figu

re 4

dep

icts

the

num

ber o

f sta

ff (c

apac

ity) p

er c

apab

ility

gro

upin

g in

the

2017

-201

8 fi n

anci

al y

ear a

s w

ell a

s th

e 20

18-2

019

fi nan

cial

yea

r. Th

e m

ajor

ity o

f the

incr

ease

in

capa

city

wer

e in

the

Clai

ms-

and

IT fu

nctio

ns.

Figu

re 4

: Sas

ria’s

capa

bilit

ies/

capa

city

cata

logu

e

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 1716 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

12. FINANCIAL RESOURCES INCOME

Sasria holds a legislative monopoly on the sale of its current product and its assured source of revenue is through insurance premiums payable by policyholders. Sasria cover is not compulsory, the policyholder has to elect to include our product.

The other source of income is investment income. Asset allocation and benchmarking according to the company’s risk profi le is determined by the company’s Investment Committee, Risk Committee and the Board, which as a targeted return requires investment performance returns equal to Consumer Price Index, plus an allocated percentage of 2% over a three-year rolling period.

13. RISK MANAGEMENT

The Risk Appetite Policy and Risk Strategy was fi rst developed and approved by the Board in 2012. The policy was reviewed in March 2017 in accordance with the FSB Solvency Assessment and Measurement (SAM) regime, and the nature of Sasria’s business. The Risk Appetite Framework (Framework) document provides details for development and application of the risk appetite as referred to in the Enterprise Risk Management Policy.

Enterprise Risk Management (ERM) enables management to eff ectively deal with uncertainty and associated risk and op-portunity, enhancing the capacity to build value.

Eff ective risk management is crucial to the company’s continued growth and success and this can only be achieved if all three elements of risks – namely threat, uncertainty and opportunity – are recognised and managed accordingly.

Through executing its business strategy, Sasria is exposed to a range of risks which need to be managed within its risk ap-petite and tolerances. This assists the Board and Management in achieving its business goals and objectives.

Sasria aims to align strategy, processes, people and technology for the purpose of evaluating and managing the uncertain-ties that are faced by the company.

Value is maximized when management sets strategy and objectives to strike an optimal balance between growth and return goals, and related risks, and effi ciently and eff ectively deploys resources in pursuit of the entity’s objectives.

ERM policies and processes are updated on a yearly basis to include new legislation and regulatory requirements (espe-cially regarding SAM). The policies form part of Sasria’s governance framework.

13.1 Enterprise Risk Management process

Processes are implemented to ensure all aspects and categories of risks are identifi ed, assessed and monitored and that risks are managed within the risk appetite.

Risk identifi cation, risk assessment and management are fundamental components of the business, in planning the com-pany’s future and executing its strategy. Internal fi nancial and other controls ensure a focus on critical risk areas, which are closely monitored and are subject to management oversight and internal audit reviews.

In ensuring that the risk universe is complete as much as possible, the risk management value chain is used across all divi-sions within Sasria.

The following are the elements of the risk management value chain:

13.1.1 Identifi cation

Risk workshops are facilitated by the risk function annually for the identifi cation of risks, risk drivers and the taxonomy. The sources of risks are obtained from strategic objectives, process fl ows, internal and external loss data, policies and processes, previous internal and external audit reports, previous risk registers (Risk and Control Self-Assessment results) and regula-tory reports.

13.1.2 Assessment

Once the risks are identifi ed, they are assessed in accordance with the company’s Risk Assessment matrix which articulates the likelihood and severity impact. The impact assessment defi nes impact into four categories namely- fi nancial, reputa-tional, stakeholder and customer. The impact is rated on a scale of 1 to 5, with 1 being insignifi cant and 5 being signifi cant. Whereas the likelihood of the event occurring is rated on a scale of 1 to 5, with 1 being unlikely and 5 almost certain.

13.1.3 Mitigation

Controls for each of the risks are identifi ed. Where controls are found to be inadequate and/or ineff ective, actions to im-prove controls are identifi ed to further strengthen them and reduce residual risks to an acceptable level. The controls are assessed for adequacy and eff ectiveness, considering the design of the control in question and whilst determining how well the control should function in practice when applied and implemented consistently across the division. Control eff ec-tiveness refers to the operating effi ciency of the control in question and is assessed by determining whether the control is operating as intended, and has been in place at all times, and whether it has been applied consistently across the division or the company.

13.1.4 Monitoring

The risks are monitored monthly by the risk function with the risk champions in the diff erent divisions, and on a quarterly basis by the Chief Risk Offi cer and the Executive Manager of each division.

13.1.5 Reporting

The risk function reports on the risk activities to the Risk Committee on a quarterly basis.The Internal Auditors annually perform risk-based audits throughout the organisation and give assurance on the overall eff ectiveness of controls.

13.1.6 Risk strategy

Sasria’s Board of Directors and Management are aware of the implications that strategic decisions have on the risk and overall capital needs of Sasria, and encourage careful consideration of whether such strategic decisions are desirable and aff ordable.

13.1.7 Risk appetite

Sasria’s risk appetite is the amount of risk that Sasria is willing to accept in pursuit of shareholder value and the attain-ment of strategic objectives. The risk appetite framework is embedded in key decision-making processes and supports the implementation of the company’s strategy. This is used to maximise returns without exposing the company to risk levels above its appetite. The risk appetite framework assists in protecting Sasria’s fi nancial performance, improves management responsiveness and debate regarding the risk profi le, assists executive management in improving the control and coordi-nation of risk-taking across business divisions, and identifi es available risk capacity in pursuit of profi table opportunities.

Measure 1: Capital at Risk

Sasria will at all times hold suffi cient eligible fi nancial resources to ensure it meets the relevant statutory solvency capital requirement, as well as its internal (economic) assessment of the capital required to deliver on its business plans, reason-able policyholder expectations and claim payments as they fall due.

The minimum capital requirement will be the greater of the Economic Capital at Risk (ECR) and the Solvency Capital Re-quirement (SCR) limits.

Appetite SCR % ECR %

Target 230% 230%

Threshold 150% 150%

Limit 130% 130%

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 1918 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Sasria developed an economic capital model for the calculation of the Economic Capital at Risk. The model simulates attri-tional, large and catastrophic losses separately. The model is currently only used for internal reporting purposes on the risk appetite measure (capital at risk) and has been used for Sasria’s Own Risk and Solvency Assessment (ORSA).

Measure 2: Earnings at risk

Sasria defi nes Earnings at Risk (EaR) as the diff erence in actual EBITDA compared to the budgeted EBITDA:

Appetite % of EBITDA

Target 5%

Threshold 10%

Limit 15%

Measure 3: Operational risk

Sasria operates at a high standard regarding the management, prevention and mitigation of losses caused by operational risk events. It has a low tolerance for operational risk but recognises it represents a cost of doing business.

Appetite Million

Target R 0

Threshold R 2

Limit R 10

13.1.8 Key risk indicators & triggers

We aim to manage our risk profi le in a proactive way. To support this, key risk indicators (KRI) and triggers have been es-tablished during the year. The KRI were developed to act as early warning signals in the event that one of the scenarios or stress situations may materialise. The indicators and triggers are monitored routinely and considered by the Risk Commit-tee with any breaches in the limits communicated to the Board.

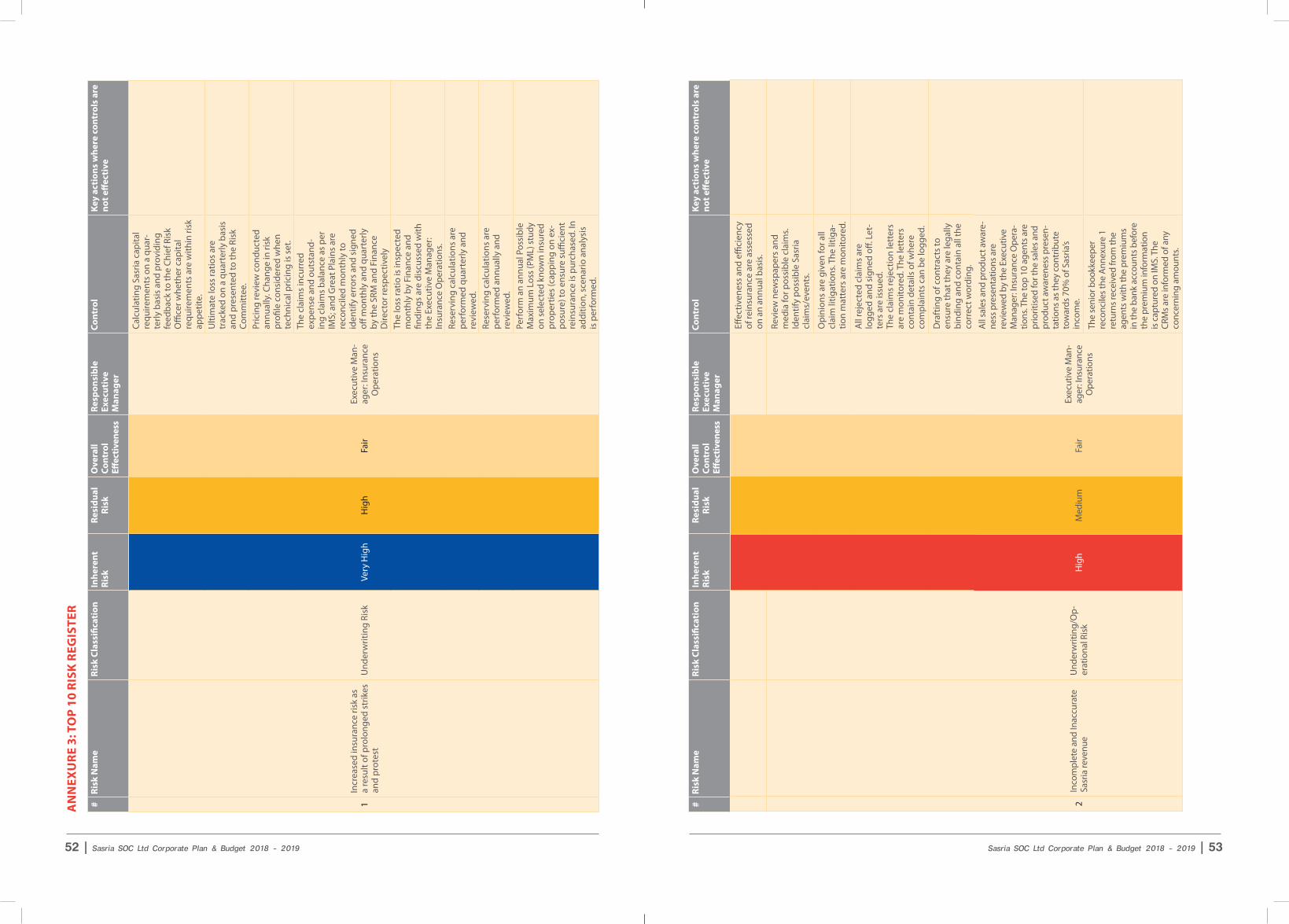

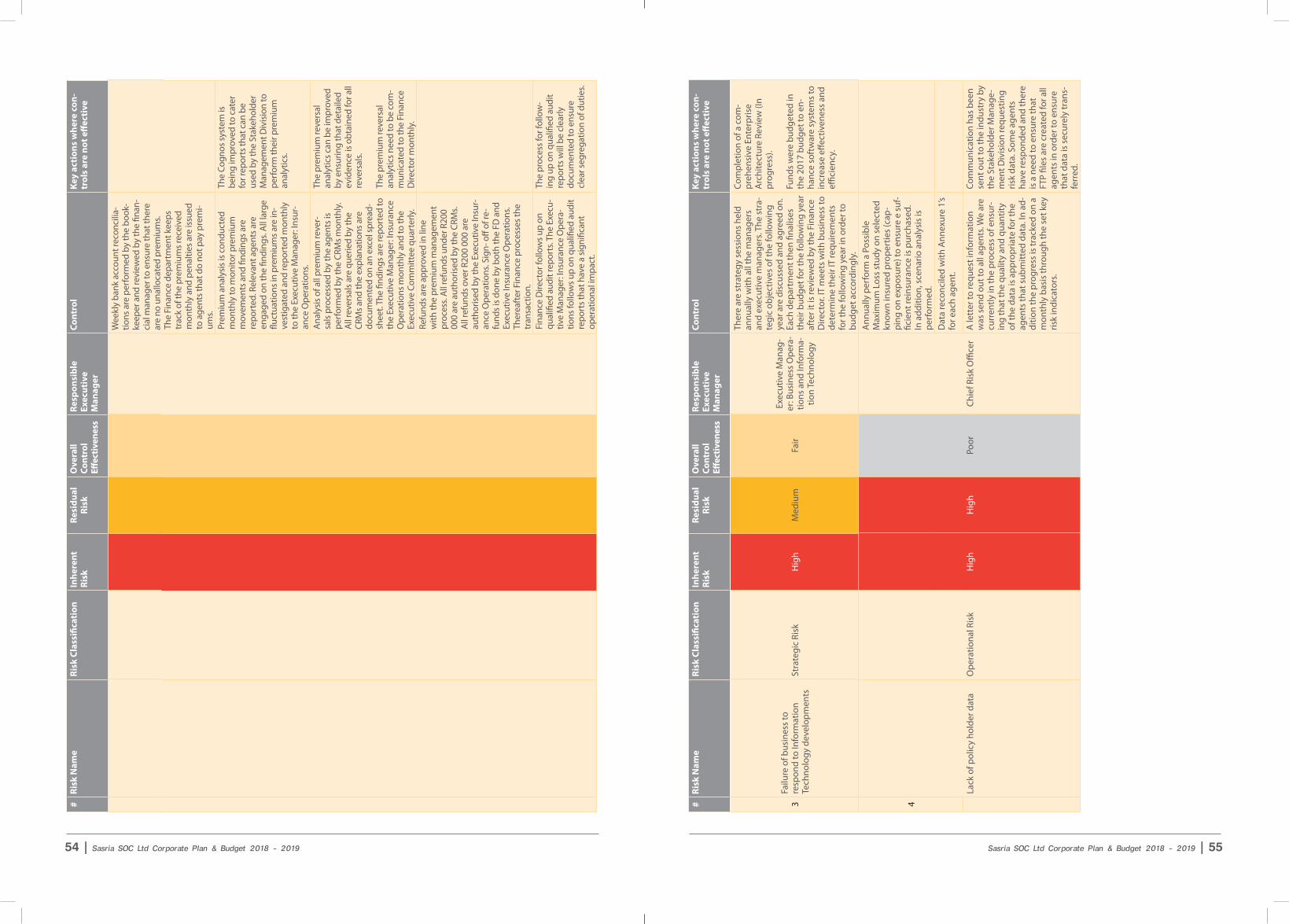

13.1.9 Top risks

The table of the top 10 key risks is attached in Annexure 3. The Chief Risk Offi cer and Risk Manager meet with the risk champions from each business division on a monthly basis. Quarterly meetings are held with the Executive Managers of all divisions. The following issues are discussed and reviewed during the monthly and quarterly meetings:

• The division’s risks• Assessment of risks based on likelihood and impact• Eff ectiveness of the controls• Movement in risks, changes made to risks and new risks• Actions required to be addressed per risk• Changes in the industry and business division• New contracts entered into by the division• Review of risk ratings• Discussions on monitoring and review of risks• Emerging risks in the department, division or companyDiscussion regarding the achievement of strategic objectives.

13.1.10 Own Risk and Solvency Assessment

The Own Risk and Solvency Assessment (ORSA) as defi ned by the FSB, is the entirety of processes and procedures em-ployed to identify, assess, monitor, manage, and report the short and long term risks an insurance undertaking faces or may face. It also defi nes the process to determine the own funds necessary to ensure that insurers’ overall solvency needs are met at all times and are suffi cient to achieve its business objectives.

The regulatory balance sheet is currently projected once a year as part of the ORSA stress testing and risk budgeting process. Projected regulatory capital requirements are considered together with the risk appetite, to ensure that Sasria’s business is managed within the risk appetite on an ongoing basis.

A key part of Sasria’s ORSA process is to evaluate the potential adverse impact to the current and future fi nancial condition of the company resulting from changes to key risk factors from unexpected events.

Sasria submitted its second ORSA report during September 2017 to the FSB. Sasria is currently in the process of further embedding the ORSA process into the business for the next business cycle, and preliminary ORSA results which are based on the fi nancial budget for the business planning period were submitted to the Risk Committee during November 2017.

14. ANALYSIS OF COMPETENCIES & ENVIRONMENT

14.1 Current competencies & resources

Sasria’s current competencies and resources comprise the following:

• A core staff with specifi c and intricate knowledge and experience in the structure of provision and administration of special risk insurance as defi ned in the Reinsurance of Material Damage and Losses Act.

14.2 Environment within which Sasria operates

14.2.1 Regulatory

• Sasria SOC Limited is established in terms of section 3 of the Conversion of Sasria Act No. 134 of 1998. It is also a National Government Business Enterprise listed in Schedule 3B of the Public Finance Management Act No. 1 of 1999, and a registered Short-Term Insurance company operating in the fi nancial services sector overseen by the FSB.

• Sasria operates under a legislated monopoly aff orded by the Reinsurance of Material Damages and Losses Act No. 56 of 1989, read in conjunction with the Conversion of Sasria Act.

• As a state owned company, Sasria is also governed by the Companies Act No. 71 of 2008 and the Public Finance Management Act No. 1 of 1999.

• Like other insurance companies Sasria will be aff ected by a number of new laws that have already commenced or will potentially commence in 2017/2018. These include Protection of Personal Information Act (PoPI), the Financial Sector Regulation Act (Twin Peaks), new King IV Code and others. All these are aimed at enhancing governance and to protect customers. While these regulatory developments are welcome they will also bring about certain fi nancial and risk implications for the organisation that will require strengthening of the governance and compliance re-sponse functions.

• Financial Sector Regulation (FSR) Act – In terms of this Act Sasria will: - Have to apply for a new license in terms of this Act. - Be reporting to two regulators, namely Prudential Authority (under South African Reserve Bank) and Financial

Sector Conduct Authority. - Be obliged not to provide fi nancial product or fi nancial service except in accordance with a licence in terms of

a specifi c fi nancial sector law. Finance sector law includes the Short Term Insurance Act and Financial Advisory and Intermediary Services Act, which requires one to be duly licensed in order to conduct insurance/fi nancial services business.

- Have an obligation to fi nancial institutions to report on contraventions with any fi nancial sector, law, directive, enforcement undertaking, court order, etc.

- Have to note that the responsible authority is empowered to suspend a license if there is contravention with licensing conditions or fi nancial sector laws.

- Have to note that the licence may be revoked if it will be in the best interest of fi nancial customers or would frustrate the object of fi nancial sector laws.

- Have to disclose that it holds a license in all business documentation. - Have to ensure compliance as non-compliance with the Bill is a fi ne not exceeding R15 000 000 or imprisonment

for a period not exceeding 10 years.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 2120 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

• King IV – In terms of King IV Sasria:

- Will include references to King IV in the Shareholder Compact. - Will review the letter of appointment of Managing Director to check if it is in line with the recommendations of

King IV. - Will have to ensure ongoing engagement with National Treasury on Treasury’s needs and expectations as a

shareholder. - Will ensure that all shareholder resolutions are done in line with the King IV Code. - Will ensure that its governing body (board) adheres to the recommendations of King IV. In this regard all Board

and Board Committee charters have been reviewed against King IV requirements and updated where required. - Will ensure that the ethical tone is set at the top and the board should ensure that they conduct themselves in

an ethical manner both in their personal and collective capacity. - Ensure that King IV principles of technology governance and reporting is adhered to.

14.2.2 Economic

• As a consequence of its exclusivity, Sasria has no direct competitors in South Africa. The BMI South Africa Insurance Report (Q4/2017) forecasts that the South African non-life segment will grow its gross written insurance premium y-o-y by 5.5% in 2017, 6% in 2018 and 6% in 2019. The non-life market in South Africa is expected to record steady growth over the forecast period through to 2021, though the sector will continue to lag in annual % growth terms. In infl ation adjusted terms, growth in the short term sector will be close to zero for at least the next year or so, in the context where key segments of this sector are sensitive to economic cycles and Gross Domestic Product (GDP) growth will remain very sluggish.

• Growth in South Africa’s non-life sector is heavily dependent upon the growth trajectory of the South African economy. South Africa’s real GDP growth will accelerate gradually in the years ahead, weighed down by structural headwinds from a challenging operating environment and low commodity prices. Elevated unemployment and a pullback in government spending on subsidies, transfers and wage hikes will tamper the pace of private consump-tion growth in the years ahead. Private consumption is expected to account for 60.9% of GDP by 2026, up from 59.5% in 2016.

• Government spending will grow as a share of overall GDP in the years ahead, as government struggles to sharply pare back spending, South Africa’s fi xed investment will remain relatively subdued in the coming years in the face of tepid foreign and domestic investor sentiment. Sporadic industrial actions, the recent investor unfriendly policy proposal and high operating costs will tamper fi rms’ enthusiasm for operating in the country in the coming quarters.

• BMI Research has revised real GDP growth forecast for 2017, from 1.0% to 0.7%1.• Sasria is subject to the vagaries in the international reinsurance markets as it has to purchase adequate reinsurance

cover. Recent natural disasters and acts of terrorism across the globe are key drivers of catastrophe reinsurance rates. Currently, global reinsurance capacity is in over supply and Sasria is expected to benefi t from this oversup-ply. Sasria will use this oversupply to adequately protect itself against volatility without having to incur a signifi cant increase in reinsurance costs.

• With more than 90% of all debt issued in rand, a downgrade to South Africa’s local currency debt rating would have signifi cant knock-on eff ects on the country. It could prompt a sharp currency sell-off , prompt further rand weakness, and weigh on business confi dence and ramp up government and private fi rms’ borrowing costs2.

• The country is further impacted by global volatility, a slump in commodity prices and weak business and consumer confi dence. Consumer price infl ation is within the Reserve Bank’s target range of 3% to 6% in 2017. This is mainly at-tributable to expected rainfall forecasts, which has driven food prices to stabilise to a moderate level in comparison to 2016 where the economy was impacted by severe drought conditions and the increase in energy tariff s. SARB has noted the medium term infl ation outlook has improved to 5.3% in 2017, 4.9% in 2018 and 5.2% in 2019 in consid-eration of the recent exchange rate appreciation, normalisation of weather patterns, which will aff ect the agricul-ture sector positively, and the interest rate cycle that will stimulate economic growth. A low infl ation rate forecast supports economic growth as it helps to reduce interest rates over time, which creates growth, sustains jobs and encourages long term investing.

• South Africa’s growth expectations have been materially marked down induced by deep-rooted structural prob-lems, political uncertainty and a high unemployment rate. SARB in its economic growth forecasts expects SA’s economy to accelerate by 0.5% in 2017, 1.2% in 2018 and 1.5% in 2019. SARB has raised its concerns over consumer and business confi dence with the latter falling to its worst level since the 2009 recession. Domestic growth pros-

1 BMI South Africa Country Risk Report Q4 20172 BMI South Africa Country Risk Report Q4 2017

pects have deteriorated, as the impact of the ratings downgrades is expected to weigh on domestic investment and consumer sentiment.

• To generate infl ation beating returns over the long term, Sasria must take a balanced approach to risk. Being too conservative is detrimental to long-term wealth creation due to the eff ect of infl ation eroding the real value of capi-tal. Sasria’s current asset allocation includes exposure to growth assets being equities, which have proven to yield higher returns over the long term.

• Following a pessimistic approach (worst-case scenario), a CPI growth of -0.4% is expected, based on the South Africa’s low growth environment and the country offi cially entering into a technical recession. The possibility of a local currency downgrade by rating agencies looms heavily over the economy with concerns raised over weak growth prospects, trade defi cit and the institutional frameworks, which have become less transparent with policymakers’ previous commitments becoming less certain.

• South African markets, like most other emerging markets, are driven by excess liquidity and to some extend inves-tor sentiment. Local markets are extremely vulnerable to a decrease in liquidity. Signifi cant downside risk exist in the South African markets. Sasria’s strategic asset allocation is designed cognisant of these risks. The allocation relies heavily on short-dated cash and near-cash instruments. The strategy is very defensive but will ensure that capital is preserved in real and nominal terms.

14.2.3 Socio-economic

Terrorism

• The Institute for Security Studies has identifi ed South Africa as a high-priority target for terrorist networks across the continent. SA has also been dubbed a ‘top 10 target’ following a spate of terrorist incidents in the last decade that have claimed victims from our country. At least 50 South Africans have been killed, kidnapped or injured by terrorist groups operating in Mali, Yemen, Somalia, Nigeria, Syria and Iraq since 20103.

Unemployment

• South Africa’s unemployment in the third quarter of 2017 increased by 1.2 of a percentage point to 27.7% - the high-est fi gure since September 20034.

• We expect the income gap to widen between the poor and the rich, and political risk will remain elevated, resulting in frequent protests. The gap between the unemployment rate envisaged in the National Development Plan (14% by 2020) and the current rate is also widening.

Service delivery protests

• A record peak in the second quarter of 2017 may mean that 2017 will eclipse other years’ records for service delivery protests, although a downward trend since May could keep it under 2014’s current record. As at the end of Septem-ber 2017, service delivery protests accounted for 11% of service delivery protests recorded since 20045 (Figure 5).

• Gauteng has been the most prominent site for service delivery protests this year; accounting for more than one out of every three protests.

• Other protest-affl icted provinces for the year include the Eastern Cape, KwaZulu-Natal and the North West. Together the four provinces account for three-quarter of protests recorded in 2017 (Figure 6).

3 The Municipal IQ. Published 2017-07-28. https://www.thesouthafrican.com/south-africa-has-become-a-top-10-target-for-terrorist-groups-iss/4 Daily Maverick. Published 2017-06-01. https://www.dailymaverick.co.za/article/2017-06-01-sa-unemployment-rate-rises-to-14-year-high/#.

WhKeh2YUmWs5 Municipal IQ. 2017 service delivery protests in a high range, but downward trend from May peak – for immediate release. Press release 24

October 2017.

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 2322 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

Figure 5: Major service delivery protests, by year (2004 – YTD 30th September 2017).

Figure 6: Service delivery protests by province 2017 (as of 30th September 2017).

• Service delivery protests will continue to be a main driver of Sasria claims in 2018-2019. Violent protest activity remains a concern for many South African communities given its adverse impact on schooling, work opportunities and community safety. It is of further concern that policing of protests appears to add another layer of violence, further destabilising the already vulnerable relationship between communities and authority fi gures.

Student protests

• #FeesMustFall at Wits was at the centre of the whole movement and in 2015 major gains were achieved, with the highlight being the 0% fee increase. The movement also brought to the table the debate around free higher educa-tion. The 2016 movement at Wits, although not as successful as it was in 2015, was more about challenging the status quo and was centred around the decolonisation of the university rather than on fees. The decolonisation proj-ect that the movement has started at Wits is an important one, as it seeks to highlight some of the structural issues at the university, most notably the marginalisation of black and African experiences in the curriculum and in how things are done at the university. Black students are forced to assimilate rather than being included in the university.

Decolonisation will not be realised in a day but the fact that it is back on the table has ushered in a new era in terms of how the university does things. Changing the demographics of the student body alone does not mean that the university is decolonised. More needs to be done to ensure that black students and staff feel that they are a part of the university6.

• As universities prepare to announce fee increases for 2018‚ a swirl of unrest is engulfi ng some campuses as students speak out against the proposed increments7.

• Student protests are the cause of a signifi cant rise in Sasria claims and this trend is set to continue in the next fi nan-cial year.

14.2.4 Technological

• In the past Sasria was a “late adopter” on the technology adoption curve. Sasria will close the technological gap over the next three to fi ve years.

• With the desire to be more effi cient and reach a wider market as well as the unreached market, Sasria will use tech-nology as a strategic enabler.

15. STRATEGIC FOCUS AREAS & STRATEGIC OBJECTIVES

Sasria’s goal in the next three years is to ensure that it: remains a professional and effi cient company; establishes itself as a thought leader in the special risk space; is innovative in terms of its product off ering to achieve National Treasury’s and the Financial Services Board’s objectives of fi nancial product inclusivity; while remaining sustainable.

To achieve the above, the strategic direction (purpose) Sasria has chosen for the next year is focused on Sustainable growth, Effi ciency, Customer centricity and Social impact (Figure 7).

Figure 7: Sasria’s strategic direction.

This will be achieved by:• Conducting a feasibility study into additional distribution channels, to reach previously unreached markets to en-

sure fi nancial inclusion of all South Africans.• Leading from the abovementioned, to develop tailor-made LSM & SME products.• Partnering with other companies already active in the LSM & SME space.

6 #Hashtag: An analysis of the #FeesMustFall Movement at South African Universities. Africa Portal. https://www.africaportal.org 7 Times Live. Is this the start of Fees Must Fall protests? Published 25 October 2017. https://www.timeslive.co.za/news/south-africa/2017-10-25-is-

this-the-start-of-fees-must-fall-protests/

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 2524 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

• Remaining customer focussed in all business operations, by ensuring that service delivery is enhanced through more eff ective processes.

• Increasing Sasria’s brand and product awareness within the distribution channels as well as end-customers.• Attracting and developing the talent required to execute our strategy.• Ensure alignment of the organisation to its future expansion strategy through the Enterprise Architecture Frame-

work and IT Strategy.

15.1 Sustainable revenue growth

Sustainable revenue growth will be achieved through the following strategic objectives: - To consistently outperform the industry average in premium growth; and - To improve our current strategic partnerships and establish new ones.

These two strategic objectives will be achieved through embedding a strategic stakeholder management approach that is focused on the high income generating distribution channel and high income generating customers. This will be done through brand and product awareness to the target audience, technical support and product training to the distribution channel. Furthermore focus will be given to maximise the current product off ering to existing customers as well as taking the current product off ering to new markets.

The focus on the distribution channel will enable eff ective selling of our product by the distribution channel on our behalf as well as eff ective advice giving and engagements with end customers during underwriting. The focus on end customers is to empower them with the knowledge on special risks in order to create demand for our product.

15.2 Capital management

The following strategic objectives will support the capital management strategic focus area: - To ensure compliance with statutory capital requirements and the calculation of an economic risk basis for capi-

tal value; and - To target a return on equity greater than the government bond yield.

During the 2018-2019 year Sasria will continue to implement the FSB SAM requirements to ensure compliance with statu-tory capital requirements, with the continued focus on the embedding of the ORSA methodology and processes, the paral-lel runs (of the economic capital models and the Solvency Capital requirements. It will further continue to improve on its calculation of an economic risk basis for capital value.

Sasria aims to optimise its return on capital by growing its insurance premium income, managing expenses, yielding a return of CPI + 2% on investments over a three year rolling basis and buying suffi cient reinsurance cover to supplement its current capital, to cover potential maximum losses as per the annual probable maximum loss (PML) study conducted.

15.3 Innovation (products & services)

Sasria will support sustainable business growth through the following strategic objectives: - To become a centre of innovation in special risk insurance;

- Research, benchmarking and best practice. - To conduct feasibility studies for new products; and - To establish new business distribution channels.

Refer to the section “Beyond 2020” for more detailed explanation on the initiatives to be undertaken.

15.4 Infrastructure & cost management

The following strategic objective will supports the strategic focus area: - To optimally enable business while satisfying regulatory requirements.

- Systems/processes/procedures/productivity/knowledge management.

Sasria’s cost management is tightly controlled and all infrastructure spent is governed by Board oversight. Over the me-dium term operational and capital expenditure is expected to increase above CPI in order to deliver on its fi ve year strategy plan as well as the Government’s broader expectations of Sasria.

Sasria is embarking on an IT digital strategy and Enterprise Architecture (EA) Framework to ensure that it is aligned with the company’s future strategy. The EA review will deliver an Architecture Vision (defi ning the future vision and buy-in), Business Architecture (understanding the business; defi ning future business), Information Systems Architecture (defi ning applica-tion and data requirements), as well as a Technology Architecture (defi ning requirements in terms of platforms, software, security and tools).

15.5 People, capacity and capability

The following strategic objectives will support the strategic focus area: - To attract, retain and develop skills that support our aspirations; and - To maintain a high-performance culture.

- Skills development/ incentivisation/ talent management/ professionalism/terms & conditions of employ-ment/ performance management/ employer value proposition.

In 2018-2019, the Human Capital department will facilitate recruitment for all vacant positions, ensure suffi cient staff devel-opment plans are in place, facilitate the implementation of identifi ed initiatives for key talent, and drive succession plan-ning, while it continues to drive performance-based outcomes within the organisation.

Sasria also realises that it needs to help build capacity outside the organisation and in support of the NDP. Sasria supports education of the youth by contributing to school infrastructure projects, sponsoring bursaries and intervention programs.

15.6 Regulatory environment

The following strategic objective will support the strategic focus area: - To proactively manage compliance.

- Compliance management/legal services/risk management.

The implementation of SAM policies and processes will continue in the 2018-2019 in anticipation of the regime’s imple-mentation date of July 2018, to accommodate the legislative timeline for the Insurance Bill enactment. The Financial Sector Regulation Act No. 9 of 2017 (FSR Act) was processed by Parliament ahead of the Insurance Bill. This enables the Insurance Bill to build on the regulatory framework created through the FSR Act. The Insurance Bill, tabled in Parliament in January 2016, is currently being considered in Parliament and is expected to be processed during the second half of 2017 and pos-sibly also the fi rst half of 20188.

15.7 Customer-centricity

The following strategic objectives will support the strategic focus area: - To provide relevant and appropriate products; and - To provide superior service.

Claims settlement turn-around time and communication is central to the customer centricity theme. The Claims Depart-ment aims to settle 90% of all fast-track claims within 30 days in the 2018-2019 year. The department aims to accept liabil-ity on 70% large losses within 60 days (from the date of submission).

15.8 Brand development

The following strategic objective will support the strategic focus area:

- To create a trusted brand that resonates with all our customers. - Loyalty/recognition/association/visibility/advocacy – fi rst commercial & corporate, then the end-consumer.

8 Solvency Assessment and Management (SAM). September 2017 Update. Published 1 September 2017. https://www.fsb.co.za/Departments/insur-ance/Documents/SAM%202017%20Update.pdf

Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019 | 2726 | Sasria SOC Ltd Corporate Plan & Budget 2018 - 2019

The elevation of the Sasria brand will continue to be focused on the big income generating agents and brokers, corporate and commercial customers, as well as creating internal brand appreciation. Further brand building to the end consumer will be enhanced via consumer education and awareness initiatives.

This will be achieved through the following:• Keeping abreast with market trends as well as developments within the environment in which we operate• Collaborative and relationship marketing with all strategic stakeholders• Elevation of the brand and product awareness to the end-customer• Developing sustainable relations with media partners• Eff ective communication with all stakeholders and• Elevate brand and product awareness.

An integrated marketing and communications approach will be utilised to achieve the above via an “always on” media approach. This, together with a clearly defi ned brand positioning, will enable the Sasria brand to move from an indiff erent brand to become a top-of-mind brand within the stakeholders segments.

16. BEYOND 2020

Sasria has started its journey to identify areas of focus for the strategy beyond 2020. These areas of focus provide opportu-nities to various stakeholders and specifi cally address the risks that the government, insurers and Sasria face.

Our process in identifying the areas of focus or opportunities was based on the risks that are currently faced by the organ-isation, risks which the industry is facing and risks that the government is facing.

In the world where climate change and its impact is a reality, the frequency and severity of disaster is increasing. Special risks, if not adequately addressed, pose a major risk to the economy of the country and also to the attainment of the NDP goals. The impact of special risk is not just economic and social but these risks further pose signifi cant food security risks to the country. They also pose an escalating threat to the three main problems facing South Africa, namely poverty, inequality and unemployment.

Government is the reinsurer of last resort; its citizens expect the Government to intervene and help the citizens in the event of a disaster. Public-private partnerships are crucial in making sure that the country builds fi nancial resilience to withstand any special risk disaster.

Based on the above it can be concluded that the government is currently facing various challenges, which include:• Special risks (as indicated above)• Poverty and inequality• Limited skills capacity and capability• Lack of transformation and inclusive growth

Sasria has started the journey to address these challenges and achieve specifi c objectives which include:• Stimulation of inclusive economic growth• Building of skills and capacity• Protecting South Africans against all types of Special risks• Support of the NDP

The focus areas and opportunities which we have identifi ed to achieve these objective and mitigate the risks are the fol-lowing:• LSM/SME feasibility project• Agriculture insurance administration project• Enterprise Architecture project• Transformation projects:

- Incubation programme - IFRS17 project

16.1 LSM/SME feasibility project