Languages

Pages

Legal

RUPEE-DENOMINATED

EXTERNAL COMMERCIAL BORROWINGS

February 3, 2016

Mr. Rajesh Agarwal

Senior Vice President

SBI Capital Markets Limited (Complete Solutions in Investment Banking)

5

4

3

2

AGENDA

RBI Revised Framework on ECBs

Rupee Denominated ECBs

Impact & Potential

Issues & Challenges

1 Introduction

2

INTRODUCTION 1

4

Incorporated in 1986; 100% subsidiary of SBI - India’s largest commercial bank

Pioneer in Indian Project Finance Market

Many ‘firsts’ to its credit:

Privatisation in the Country

Securitisation in Power Sector

Reserve Based Lending

Only Indian Investment Bank to act as Arranger for Foreign Currency Bond Issuance

Strong relationship with Central/State Government(s) with involvement in several strategic sale & other advisory transactions, including:

Auction of Coal Mines

Auction of 6 Mineral Blocks in India

Auction of RLNG for Stranded Gas Based

Power Plants

Financial Structuring of State Distribution

Utilities

SBICAP - INDIA’S PREMIER INVESTMENT BANK & PREFERRED GROWTH PARTNER…

SBICAP UK

SBICAP Singapore

Mumbai

Guwahati

Kolkata Ahmedabad

New Delhi

Pune Hyderabad

Chennai

SBICAP’s Network of Offices

Strictly Private & Confidential

5

.

Securities Research

International Offerings

Private Placements

Sales & Distribution

Project Finance Advisory

Brokerage Services

Mergers & Acquisitions

Corporate Advisory

Capital Markets

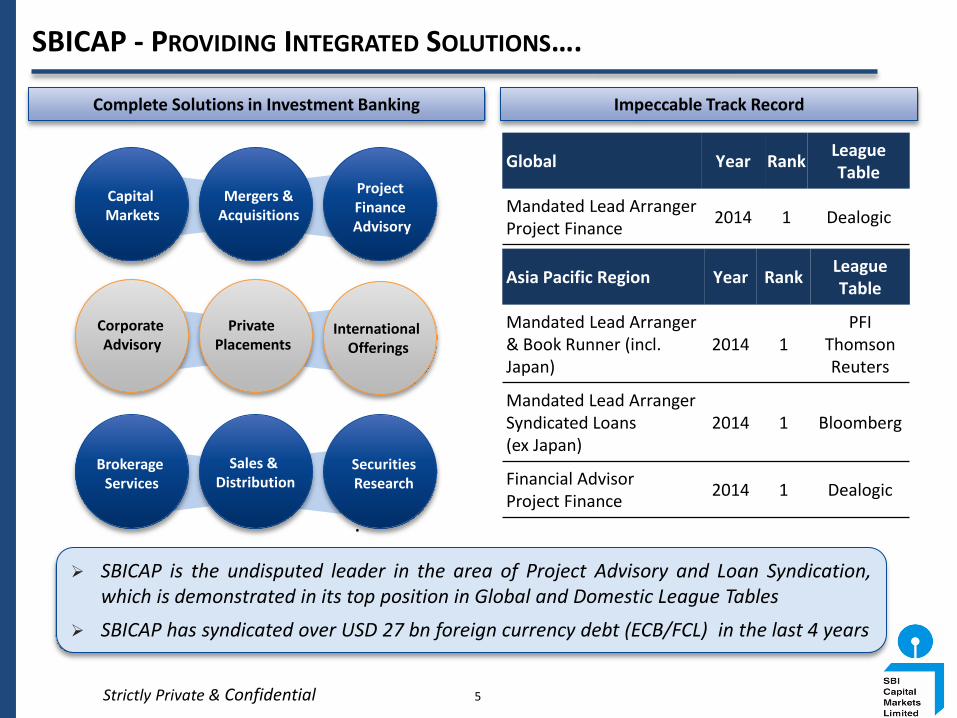

Complete Solutions in Investment Banking

SBICAP - PROVIDING INTEGRATED SOLUTIONS….

Global Year Rank League Table

Mandated Lead Arranger Project Finance

2014 1 Dealogic

Asia Pacific Region Year Rank League Table

Mandated Lead Arranger & Book Runner (incl. Japan)

2014 1 PFI

Thomson Reuters

Mandated Lead Arranger Syndicated Loans (ex Japan)

2014 1 Bloomberg

Financial Advisor Project Finance

2014 1 Dealogic

Strictly Private & Confidential

SBICAP is the undisputed leader in the area of Project Advisory and Loan Syndication, which is demonstrated in its top position in Global and Domestic League Tables

SBICAP has syndicated over USD 27 bn foreign currency debt (ECB/FCL) in the last 4 years

Impeccable Track Record

RBI REVISED FRAMEWORK ON ECBs 2

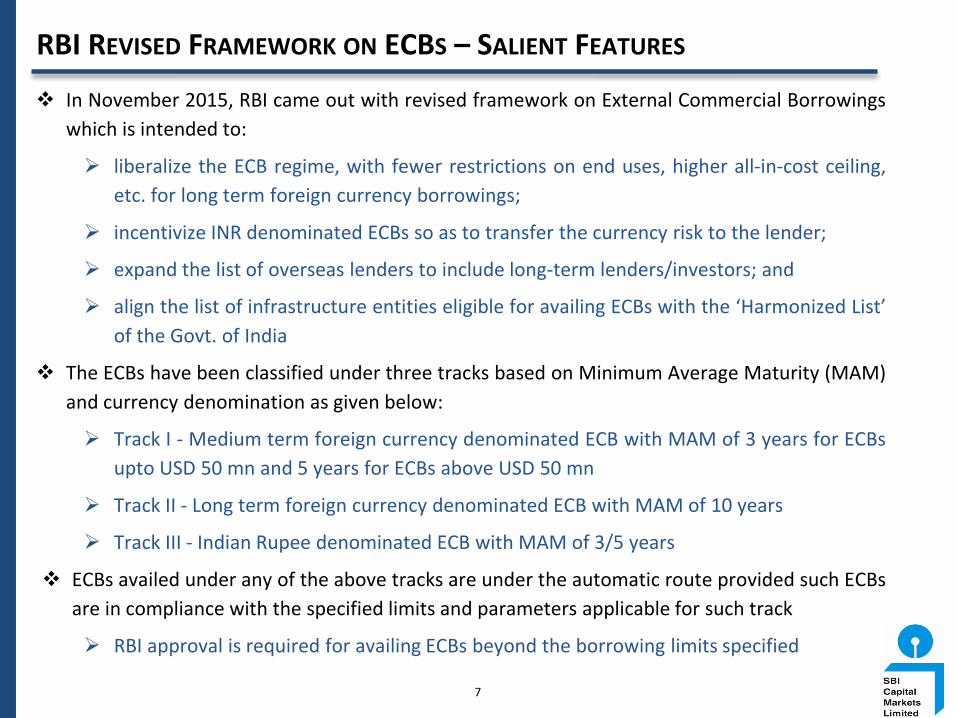

RBI REVISED FRAMEWORK ON ECBS – SALIENT FEATURES

7

In November 2015, RBI came out with revised framework on External Commercial Borrowings

which is intended to:

liberalize the ECB regime, with fewer restrictions on end uses, higher all-in-cost ceiling,

etc. for long term foreign currency borrowings;

incentivize INR denominated ECBs so as to transfer the currency risk to the lender;

expand the list of overseas lenders to include long-term lenders/investors; and

align the list of infrastructure entities eligible for availing ECBs with the ‘Harmonized List’

of the Govt. of India

The ECBs have been classified under three tracks based on Minimum Average Maturity (MAM)

and currency denomination as given below:

Track I - Medium term foreign currency denominated ECB with MAM of 3 years for ECBs

upto USD 50 mn and 5 years for ECBs above USD 50 mn

Track II - Long term foreign currency denominated ECB with MAM of 10 years

Track III - Indian Rupee denominated ECB with MAM of 3/5 years

ECBs availed under any of the above tracks are under the automatic route provided such ECBs

are in compliance with the specified limits and parameters applicable for such track

RBI approval is required for availing ECBs beyond the borrowing limits specified

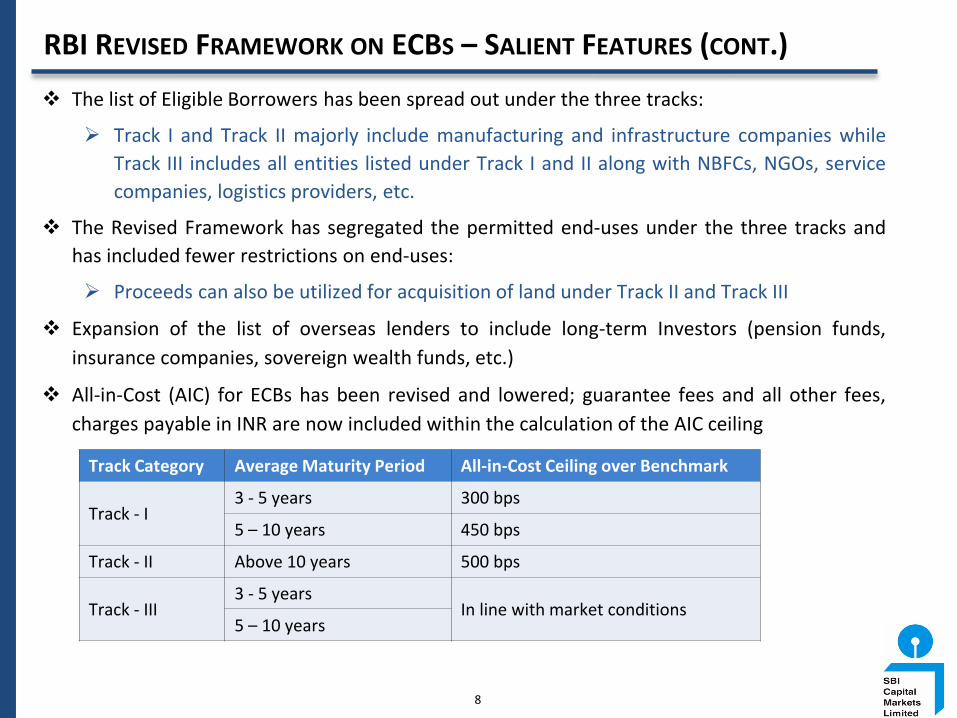

RBI REVISED FRAMEWORK ON ECBS – SALIENT FEATURES (CONT.)

8

The list of Eligible Borrowers has been spread out under the three tracks:

Track I and Track II majorly include manufacturing and infrastructure companies while

Track III includes all entities listed under Track I and II along with NBFCs, NGOs, service

companies, logistics providers, etc.

The Revised Framework has segregated the permitted end-uses under the three tracks and

has included fewer restrictions on end-uses:

Proceeds can also be utilized for acquisition of land under Track II and Track III

Expansion of the list of overseas lenders to include long-term Investors (pension funds,

insurance companies, sovereign wealth funds, etc.)

All-in-Cost (AIC) for ECBs has been revised and lowered; guarantee fees and all other fees,

charges payable in INR are now included within the calculation of the AIC ceiling

Track Category Average Maturity Period All-in-Cost Ceiling over Benchmark

Track - I 3 - 5 years 300 bps

5 – 10 years 450 bps

Track - II Above 10 years 500 bps

Track - III 3 - 5 years

In line with market conditions 5 – 10 years

RUPEE DENOMINATED ECBs 3

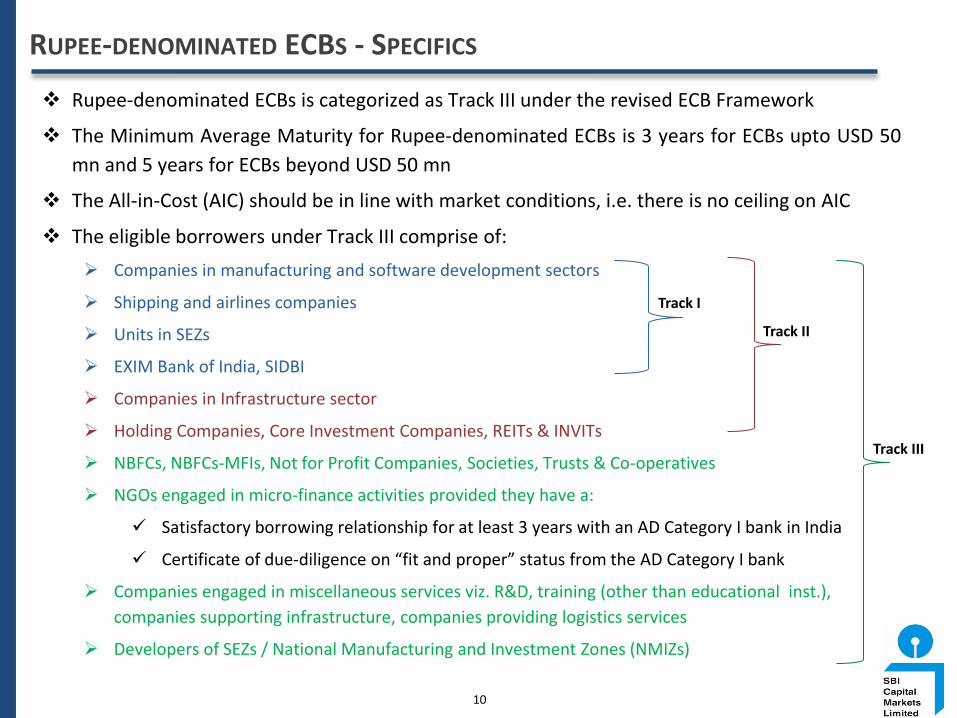

RUPEE-DENOMINATED ECBS - SPECIFICS

10

Rupee-denominated ECBs is categorized as Track III under the revised ECB Framework

The Minimum Average Maturity for Rupee-denominated ECBs is 3 years for ECBs upto USD 50

mn and 5 years for ECBs beyond USD 50 mn

The All-in-Cost (AIC) should be in line with market conditions, i.e. there is no ceiling on AIC

The eligible borrowers under Track III comprise of:

Companies in manufacturing and software development sectors

Shipping and airlines companies

Units in SEZs

EXIM Bank of India, SIDBI

Companies in Infrastructure sector

Holding Companies, Core Investment Companies, REITs & INVITs

NBFCs, NBFCs-MFIs, Not for Profit Companies, Societies, Trusts & Co-operatives

NGOs engaged in micro-finance activities provided they have a:

Satisfactory borrowing relationship for at least 3 years with an AD Category I bank in India

Certificate of due-diligence on “fit and proper” status from the AD Category I bank

Companies engaged in miscellaneous services viz. R&D, training (other than educational inst.),

companies supporting infrastructure, companies providing logistics services

Developers of SEZs / National Manufacturing and Investment Zones (NMIZs)

Track I

Track II

Track III

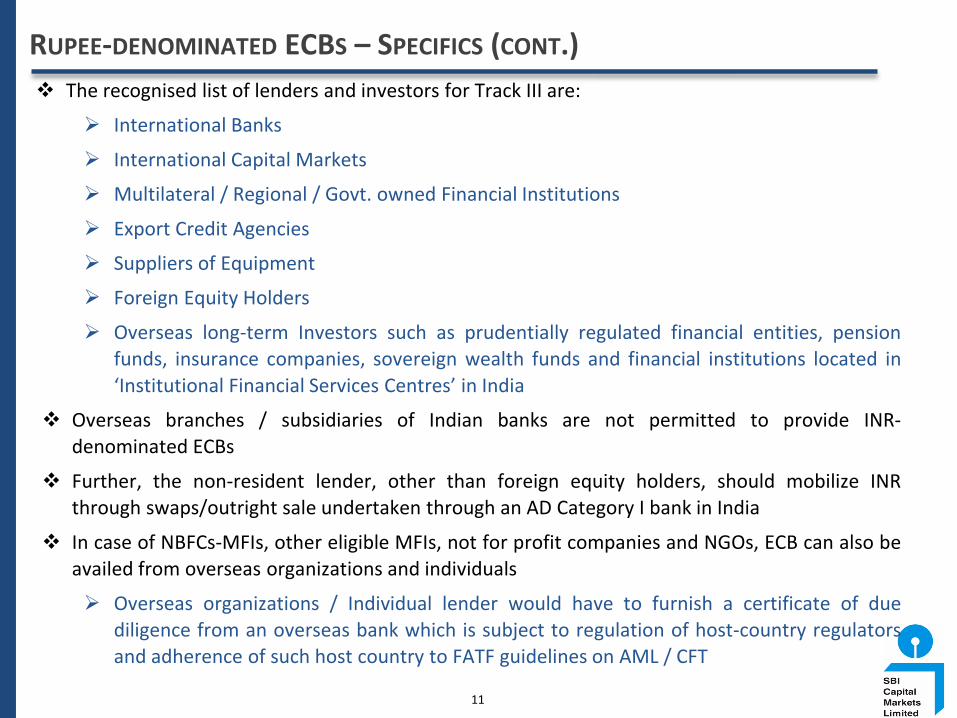

RUPEE-DENOMINATED ECBS – SPECIFICS (CONT.)

11

The recognised list of lenders and investors for Track III are:

International Banks

International Capital Markets

Multilateral / Regional / Govt. owned Financial Institutions

Export Credit Agencies

Suppliers of Equipment

Foreign Equity Holders

Overseas long-term Investors such as prudentially regulated financial entities, pension funds, insurance companies, sovereign wealth funds and financial institutions located in

‘Institutional Financial Services Centres’ in India

Overseas branches / subsidiaries of Indian banks are not permitted to provide INR-denominated ECBs

Further, the non-resident lender, other than foreign equity holders, should mobilize INR through swaps/outright sale undertaken through an AD Category I bank in India

In case of NBFCs-MFIs, other eligible MFIs, not for profit companies and NGOs, ECB can also be availed from overseas organizations and individuals

Overseas organizations / Individual lender would have to furnish a certificate of due diligence from an overseas bank which is subject to regulation of host-country regulators and adherence of such host country to FATF guidelines on AML / CFT

RUPEE-DENOMINATED ECBS – SPECIFICS (CONT.)

12

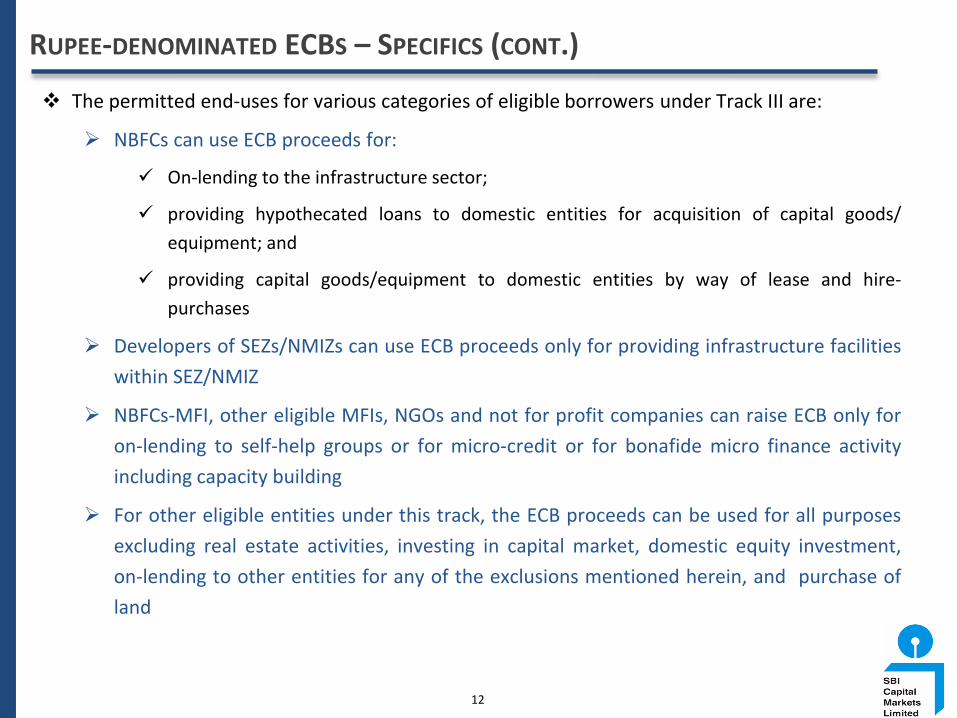

The permitted end-uses for various categories of eligible borrowers under Track III are:

NBFCs can use ECB proceeds for:

On-lending to the infrastructure sector;

providing hypothecated loans to domestic entities for acquisition of capital goods/

equipment; and

providing capital goods/equipment to domestic entities by way of lease and hire-

purchases

Developers of SEZs/NMIZs can use ECB proceeds only for providing infrastructure facilities

within SEZ/NMIZ

NBFCs-MFI, other eligible MFIs, NGOs and not for profit companies can raise ECB only for

on-lending to self-help groups or for micro-credit or for bonafide micro finance activity

including capacity building

For other eligible entities under this track, the ECB proceeds can be used for all purposes

excluding real estate activities, investing in capital market, domestic equity investment,

on-lending to other entities for any of the exclusions mentioned herein, and purchase of

land

IMPACT & POTENTIAL 4

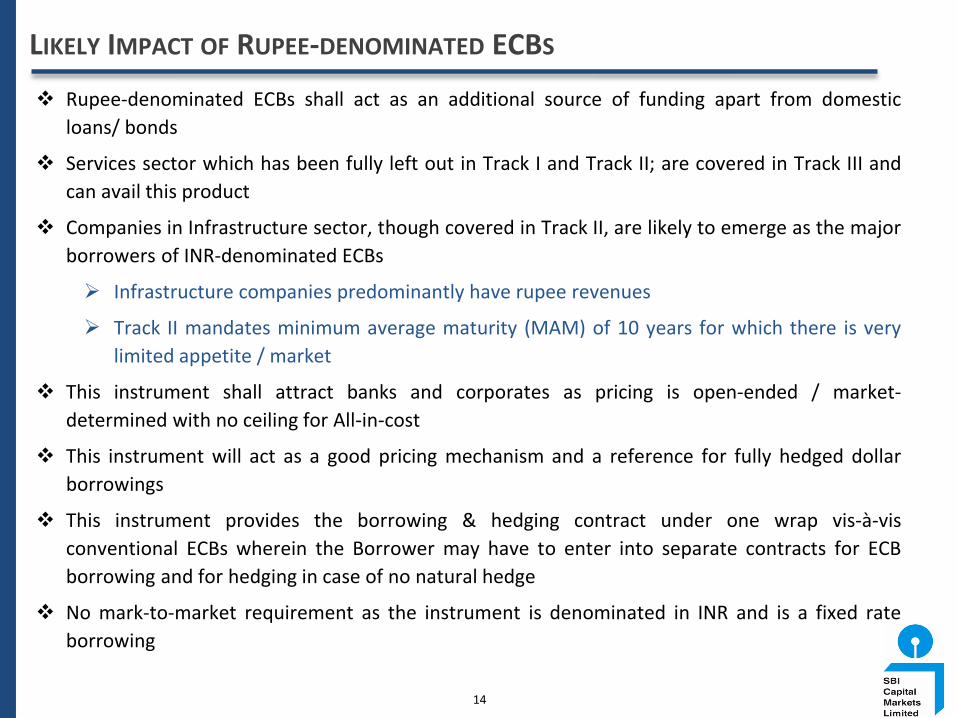

LIKELY IMPACT OF RUPEE-DENOMINATED ECBS

14

Rupee-denominated ECBs shall act as an additional source of funding apart from domestic

loans/ bonds

Services sector which has been fully left out in Track I and Track II; are covered in Track III and

can avail this product

Companies in Infrastructure sector, though covered in Track II, are likely to emerge as the major

borrowers of INR-denominated ECBs

Infrastructure companies predominantly have rupee revenues

Track II mandates minimum average maturity (MAM) of 10 years for which there is very

limited appetite / market

This instrument shall attract banks and corporates as pricing is open-ended / market-

determined with no ceiling for All-in-cost

This instrument will act as a good pricing mechanism and a reference for fully hedged dollar

borrowings

This instrument provides the borrowing & hedging contract under one wrap vis-à-vis

conventional ECBs wherein the Borrower may have to enter into separate contracts for ECB

borrowing and for hedging in case of no natural hedge

No mark-to-market requirement as the instrument is denominated in INR and is a fixed rate

borrowing

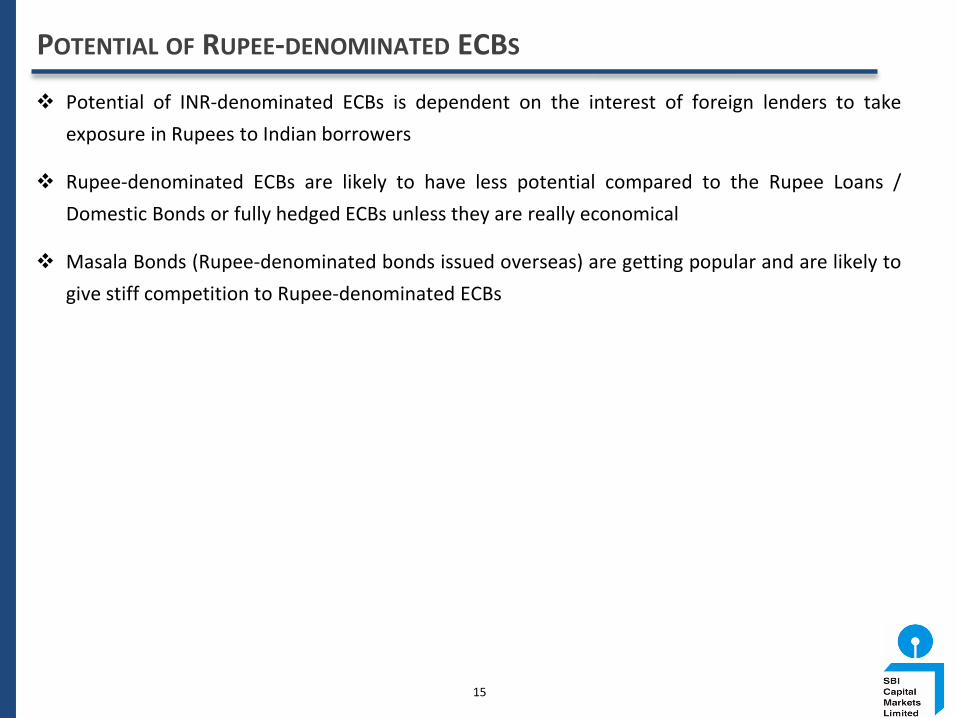

POTENTIAL OF RUPEE-DENOMINATED ECBS

Potential of INR-denominated ECBs is dependent on the interest of foreign lenders to take

exposure in Rupees to Indian borrowers

Rupee-denominated ECBs are likely to have less potential compared to the Rupee Loans /

Domestic Bonds or fully hedged ECBs unless they are really economical

Masala Bonds (Rupee-denominated bonds issued overseas) are getting popular and are likely to

give stiff competition to Rupee-denominated ECBs

15

ISSUES AND CHALLENGES 6

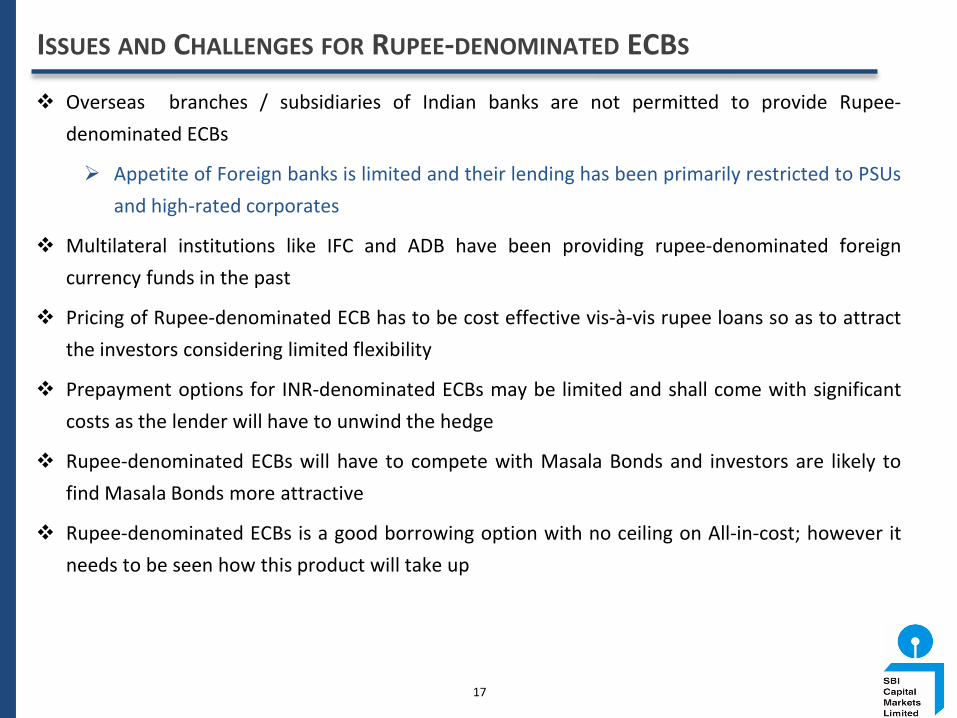

ISSUES AND CHALLENGES FOR RUPEE-DENOMINATED ECBS

17

Overseas branches / subsidiaries of Indian banks are not permitted to provide Rupee-

denominated ECBs

Appetite of Foreign banks is limited and their lending has been primarily restricted to PSUs

and high-rated corporates

Multilateral institutions like IFC and ADB have been providing rupee-denominated foreign

currency funds in the past

Pricing of Rupee-denominated ECB has to be cost effective vis-à-vis rupee loans so as to attract

the investors considering limited flexibility

Prepayment options for INR-denominated ECBs may be limited and shall come with significant

costs as the lender will have to unwind the hedge

Rupee-denominated ECBs will have to compete with Masala Bonds and investors are likely to

find Masala Bonds more attractive

Rupee-denominated ECBs is a good borrowing option with no ceiling on All-in-cost; however it

needs to be seen how this product will take up

KEY OBSERVATIONS ON THE REVISED FRAMEWORK

18

Alignment of the list of infrastructure entities eligible for ECB borrowing with the ‘Harmonized

List’ of the Govt. of India has resulted in leaving out certain sectors like Exploration &

Production, Mining, etc. which were earlier eligible to raise ECB and largely relied on ECBs for

their capital expenditure requirements

Track II ECB stipulates minimum average maturity requirement of 10 years for which there is no

market as Indian banks are not permitted to participate in Track II and foreign banks are

generally more inclined for lending in the 3-5 year maturity

Overseas branches / subsidiaries of Indian banks are not permitted to participate in refinancing

of existing ECBs

Refinancing mostly happens when the initial project risk (often financed by Indian banks) is

over; thereby depriving Indian banks of excellent business opportunities even after

carrying significant risks at various stages of the project/business life cycle and causing

huge business loss

Participation of Indian banks in refinance doesn’t increase the risk and will ensure real

benefits to Indian corporates and a fair opportunity to Indian banks

Top Related