Languages

Pages

Legal

ROV Market Prospects

Andrew Reid, 6 September 2013, Aberdeen

www.dw‐1.com

LNG

offshore

onshore

downstream

power

LNG

renewables

• Established 1990• Aberdeen, Canterbury, London,

New York, Singapore & Houston

Activity & Service Lines• Business strategy & consulting• Commercial due-diligence• Market research & analysis• Published market studies

Large, Diversified Client Base• 1000 projects, 72 countries• Leading global corporates• Energy majors and their

suppliers• Investment banks & PE firms• Government agencies

Douglas-Westwood: Our Business

Macro Views

ROV Market Drivers

ROV Market Outlook

Conclusions

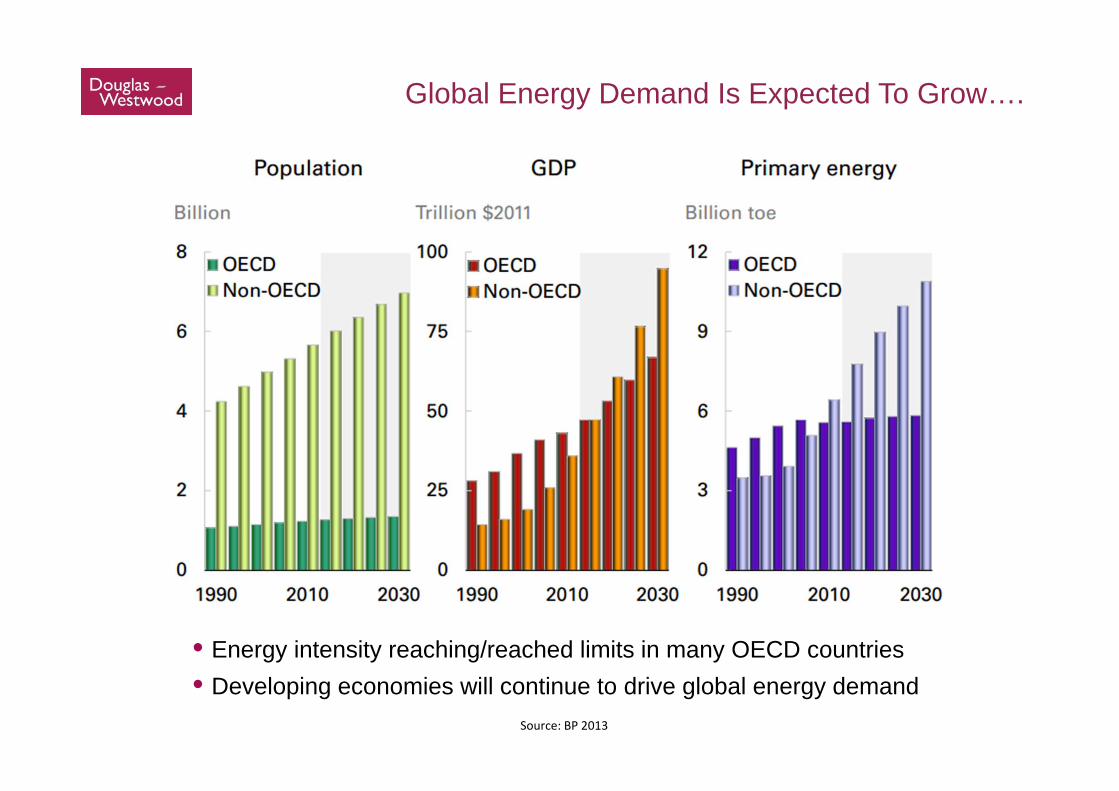

Global Energy Demand Is Expected To Grow….

• Energy intensity reaching/reached limits in many OECD countries• Developing economies will continue to drive global energy demand

Global Oil Consumption (BP)

Source: BP 2013

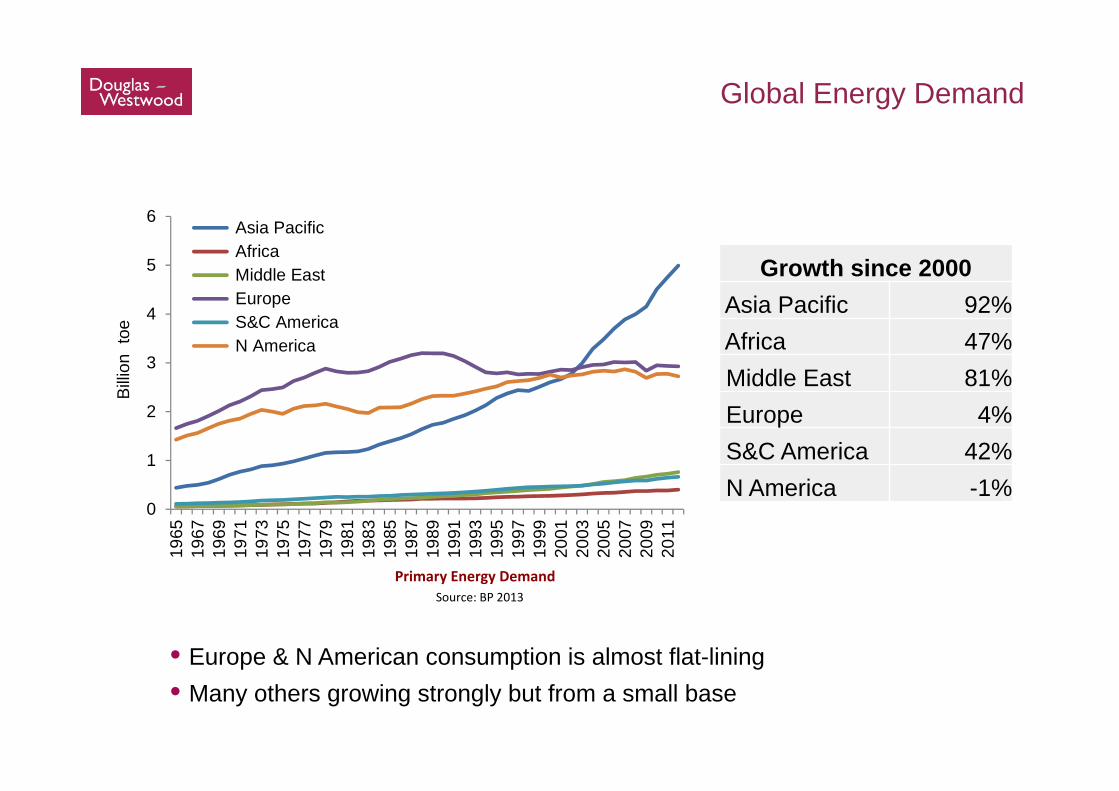

Global Energy Demand

Primary Energy Demand

0

1

2

3

4

5

6

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

Billio

n to

e

Asia Pacific Africa Middle East Europe S&C America N America

Growth since 2000 Asia Pacific 92%Africa 47%Middle East 81%Europe 4%S&C America 42%N America -1%

• Europe & N American consumption is almost flat-lining• Many others growing strongly but from a small base

Source: BP 2013

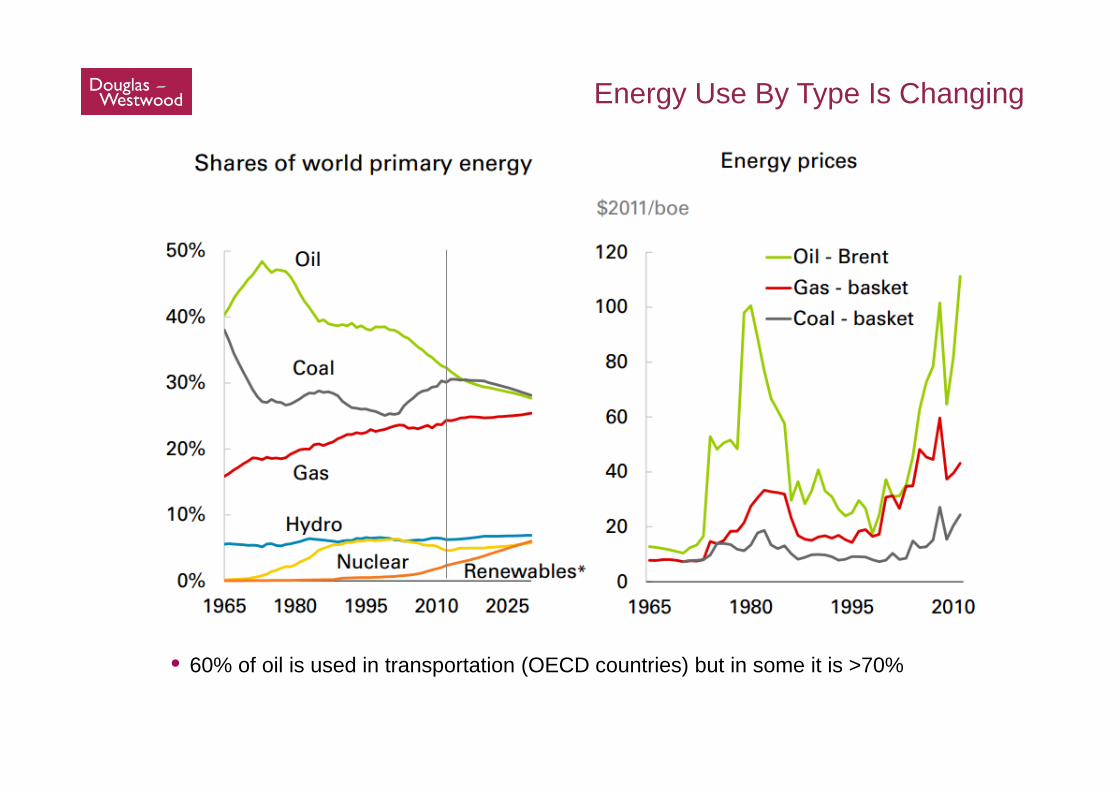

Energy Use By Type Is Changing

• 60% of oil is used in transportation (OECD countries) but in some it is >70%

Macro Views

ROV Market Drivers

ROV Market Outlook

Conclusions

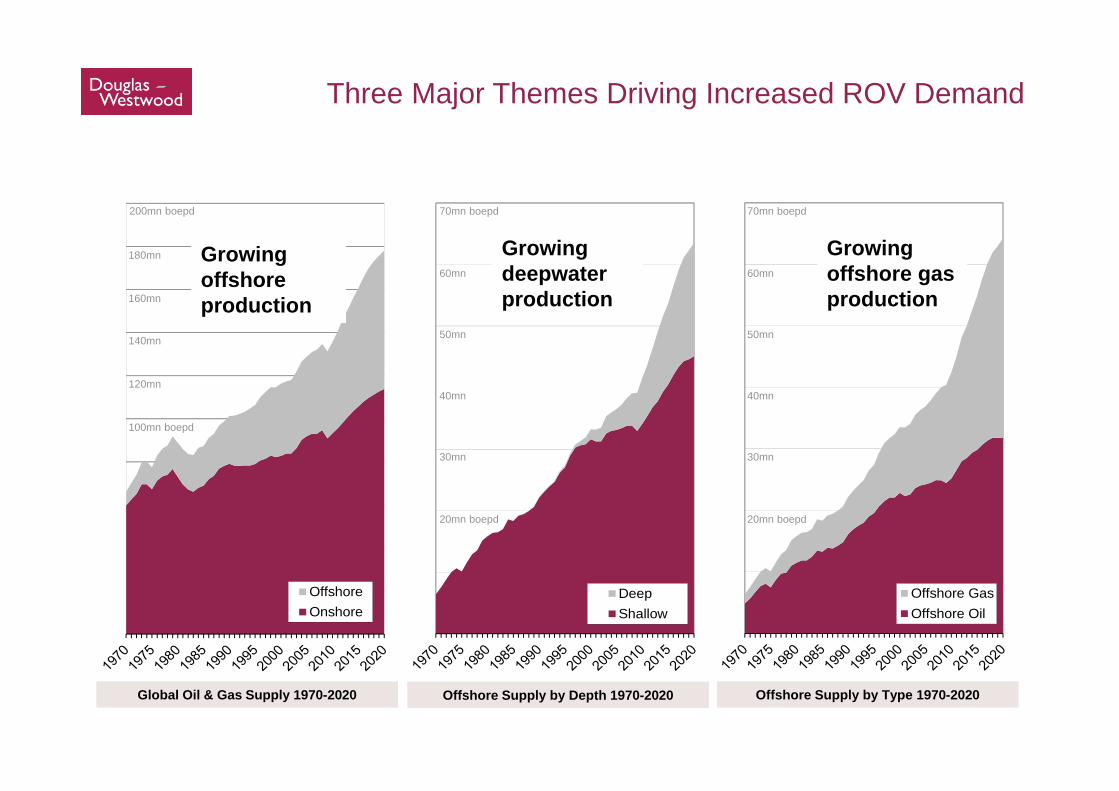

Three Major Themes Driving Increased ROV Demand

Offshore Supply by Type 1970-2020

Offshore GasOffshore Oil

20mn boepd

30mn

40mn

50mn

60mn

70mn boepd

Global Oil & Gas Supply 1970-2020

100mn boepd

120mn

140mn

160mn

180mn

200mn boepd

OffshoreOnshore

Offshore Supply by Depth 1970-2020

DeepShallow

20mn boepd

30mn

40mn

50mn

60mn

70mn boepd

Growing offshore production

Growing deepwater production

Growing offshore gasproduction

2007 2009 2011 2013 2015 2017

Deepwater Drilling (Indexed to 2007)Shallow Water Drilling (Indexed to 2007)

Drilling To Increase In Deepwater

1

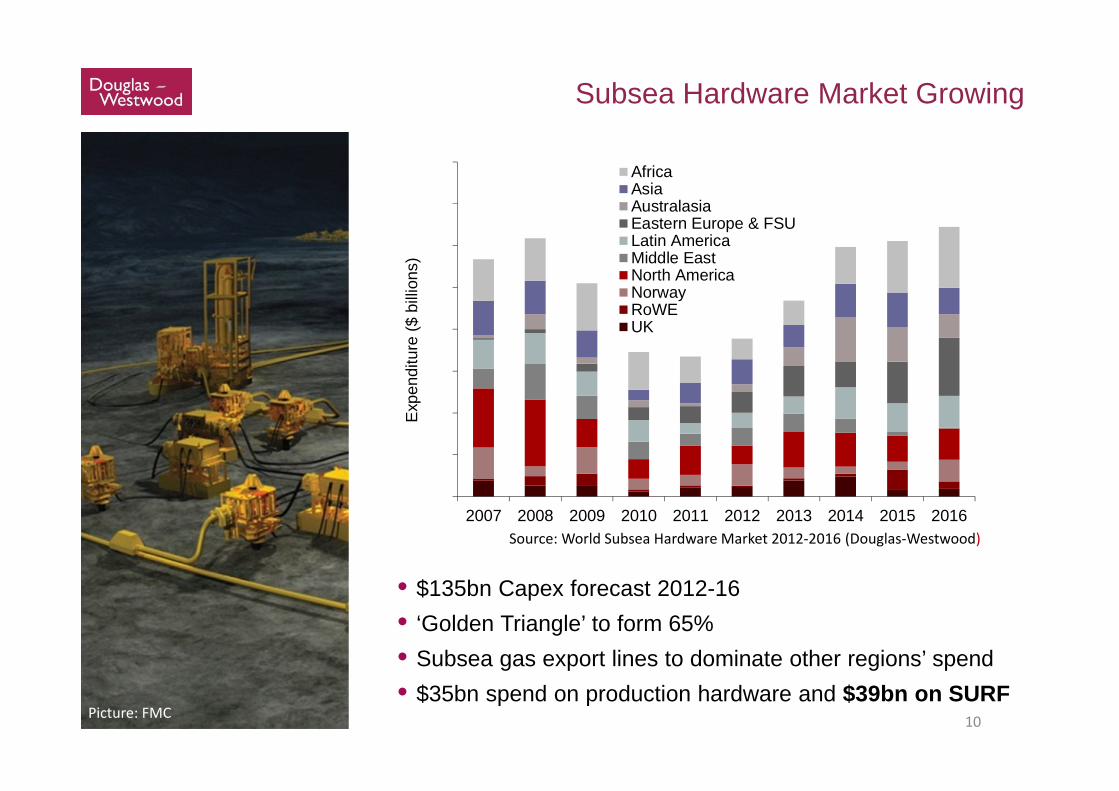

Subsea Hardware Market Growing

• $135bn Capex forecast 2012-16• ‘Golden Triangle’ to form 65%• Subsea gas export lines to dominate other regions’ spend• $35bn spend on production hardware and $39bn on SURF

Source: World Subsea Hardware Market 2012‐2016 (Douglas‐Westwood)

10

0

5

10

15

20

25

30

35

40

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Exp

endi

ture

($ b

illio

ns)

AfricaAsiaAustralasiaEastern Europe & FSULatin AmericaMiddle EastNorth AmericaNorwayRoWEUK

Picture: FMC

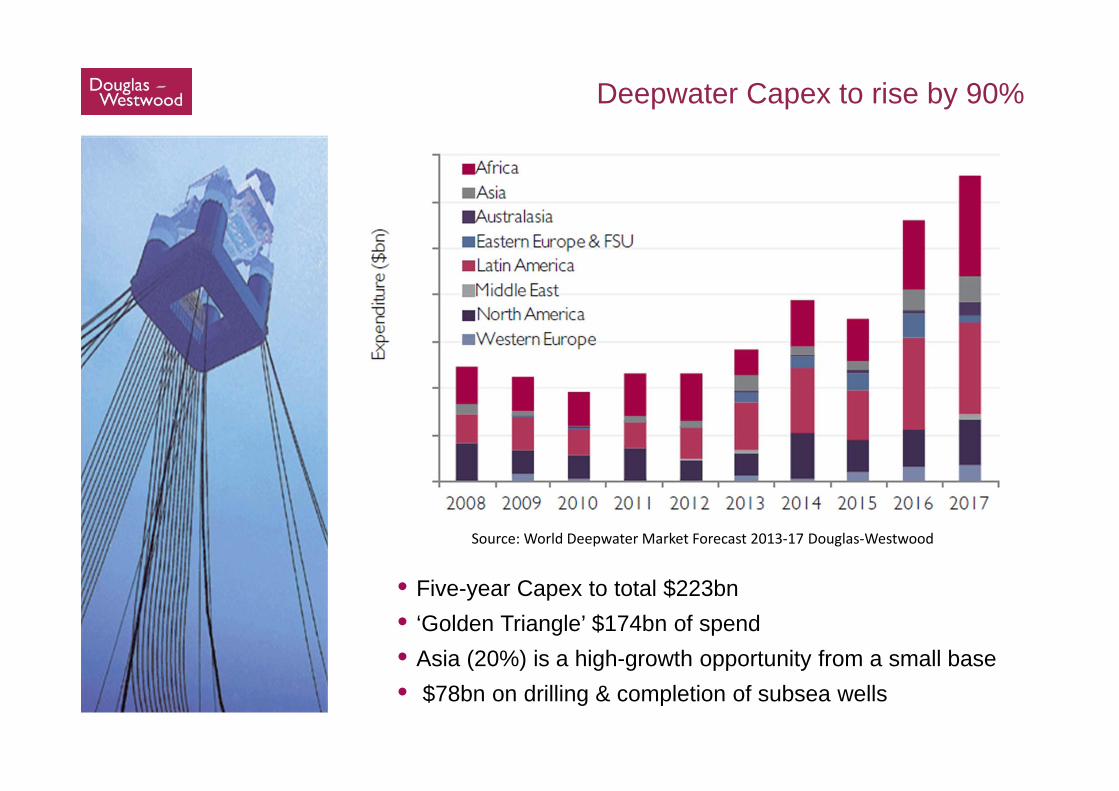

Deepwater Capex to rise by 90%

• Five-year Capex to total $223bn• ‘Golden Triangle’ $174bn of spend• Asia (20%) is a high-growth opportunity from a small base • $78bn on drilling & completion of subsea wells

Source: World Deepwater Market Forecast 2013‐17 Douglas‐Westwood

Major Cost And Margin Challenges For IOCs

Structural costs:• geology (HPHT deep &

complex)• remote locations• extreme conditions (deepwater,

arctic)• marginal fieldsDurable costs:• forex rates (e.g. Aus)Transient costs:• manufacturing bottlenecks• certain labour shortages• elevated drillship dayrates

Combined data for BG, BP, COP, CVX, ENI, OXY, PBR, RDS, STO, TOT, XOMSource: Bloomberg via Phibro Trading LLC

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

$

mn

b/d

110

60

160

210

260

10

16.5

15.5

15.0

14.5

14.0

13.5

13.0

12.5

16.0

Liquids Production - RHS

CAPEX ($ billion) - LHS

Brent ($/bbl) - LHS

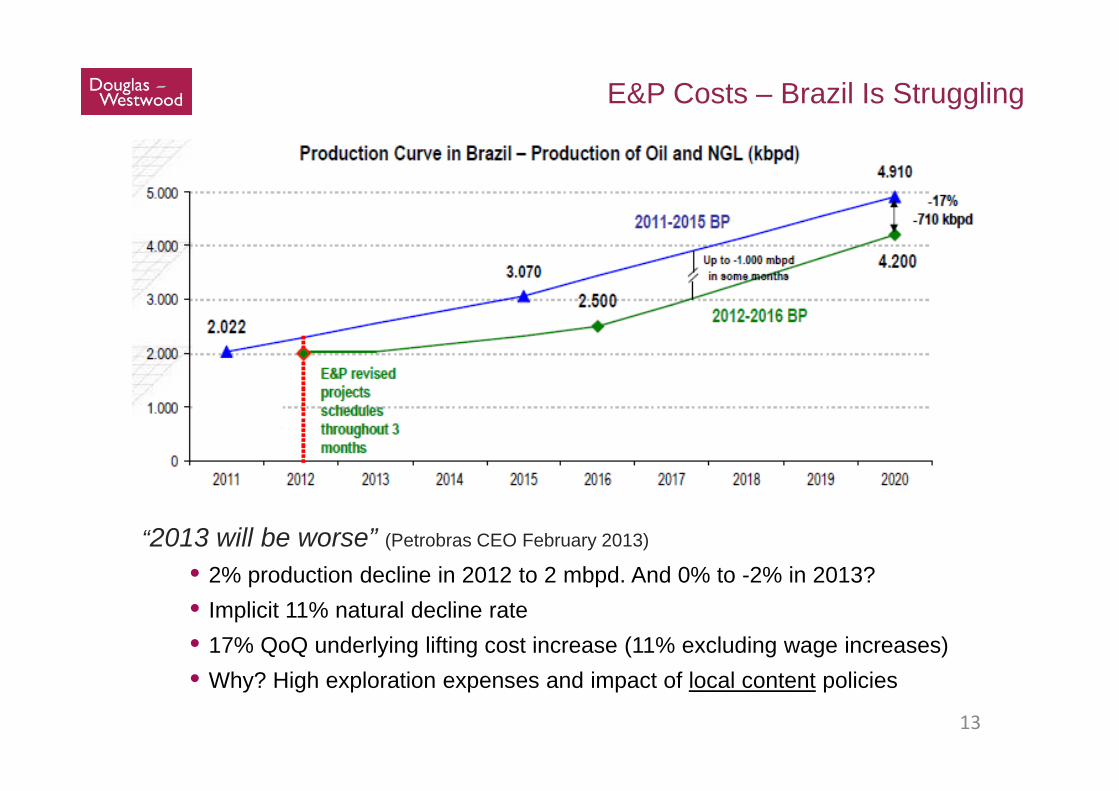

E&P Costs – Brazil Is Struggling

“2013 will be worse” (Petrobras CEO February 2013)

• 2% production decline in 2012 to 2 mbpd. And 0% to -2% in 2013?• Implicit 11% natural decline rate• 17% QoQ underlying lifting cost increase (11% excluding wage increases)• Why? High exploration expenses and impact of local content policies

13

Macro Views

ROV Market Drivers

ROV Market Outlook

Conclusions

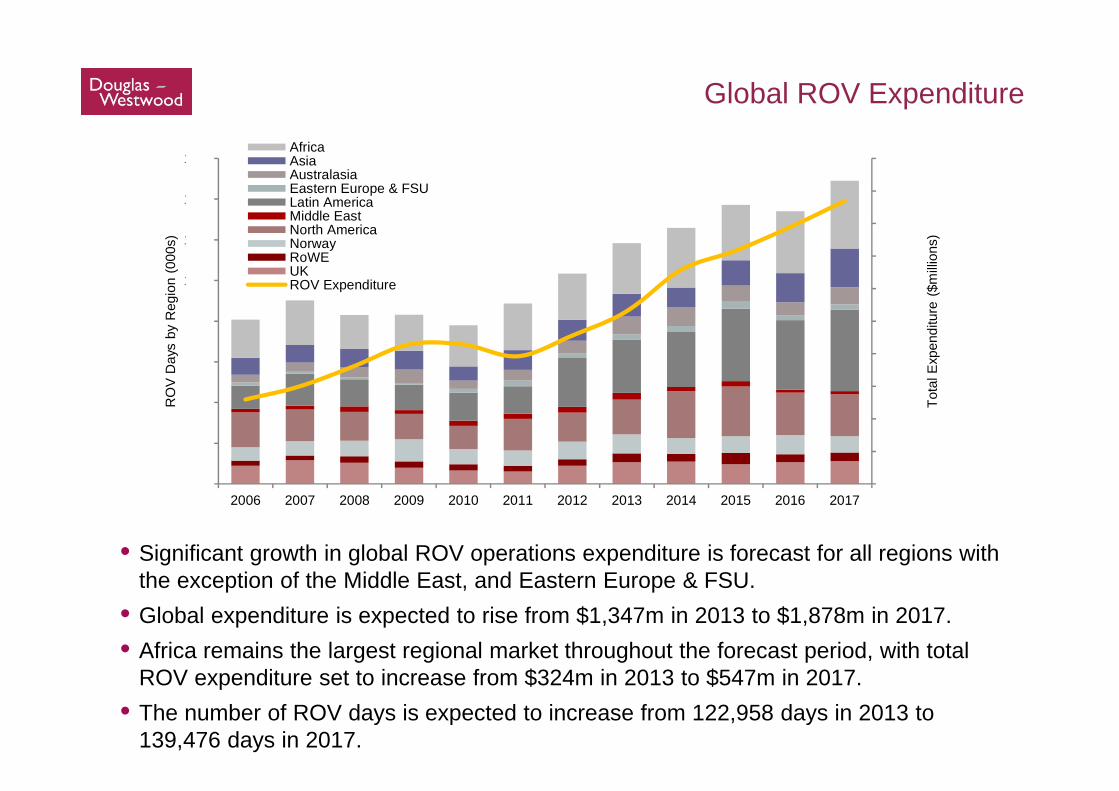

Global ROV Expenditure

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Tota

l Exp

endi

ture

($m

illion

s)

RO

V D

ays

by R

egio

n (0

00s)

AfricaAsiaAustralasiaEastern Europe & FSULatin AmericaMiddle EastNorth AmericaNorwayRoWEUKROV Expenditure

• Significant growth in global ROV operations expenditure is forecast for all regions with the exception of the Middle East, and Eastern Europe & FSU.

• Global expenditure is expected to rise from $1,347m in 2013 to $1,878m in 2017. • Africa remains the largest regional market throughout the forecast period, with total

ROV expenditure set to increase from $324m in 2013 to $547m in 2017.• The number of ROV days is expected to increase from 122,958 days in 2013 to

139,476 days in 2017.

ROV Days by Driver

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Tota

l Exp

endi

ture

($m

illio

ns)

RO

V D

ays

by H

ardw

are

(000

s)

RM - Repair & MaintainenceDS - Subsea DV WellsDS - E&A WellsCS - Trunkline InstallationCS - FPSO Mooring & RisersCS - Subsea ProcessingCS - TMFJCS - Umbilicals & FlowlinesCS - Subsea TreesROV Expenditure

• This is driven primarily by E&A and development well drilling support requirements• E&A drilling support contributes the largest proportion of future work for ROVs,

making up almost 41% of demand days over 2013-2017.• Trunkline installation days remain steady during the forecast period, as large

projects in Asia, the Americas and Europe can take years to complete.

Macro Views

ROV Market Drivers

ROV Market Outlook

Conclusions

Conclusions

18

•Macro fundamentals are strong and support continued investment in the energy sector

• Increased investment in offshore and deepwater oil and gas production will support continued ROV demand

• Increasing costs are not sustainable and further delays and potential cancellation of projects are expected

Thank You

Top Related