Languages

Pages

Legal

Reforming Public Internal Control: Lessons (Not) Learned

LEICE MARIA GARCIAAFC/AECI/MDS

ISSUES FOR REFLEXION

1. Challenges to the reforms of public internal control: absence of a unique prescribed path, political rush, technical insufficiency and administrative traditions.

2. Unlearned lessons: political decision precede the prescription, a modification of the norm is not a reform, precipitated juridical transplant leads to problems in the implementation, planning to guarantee resources; excessive segmentation can result in blindness in relation to systemic problems; internal control must coincide with the PFM system.

2

CONDITIONS TO SUCCESS

3

1. Top managers must be favourable to and engaged in the reform

2. Change must reach the administrative culture (management responsibility and real delegation)

3. Sufficiency of resources, including leadership over the implementation of the process

4. Integrated approach- PIC is not a technique in itself, but a part of the public Finance Management and the Public Administration

5.Permanent and sustainable formation for all

44

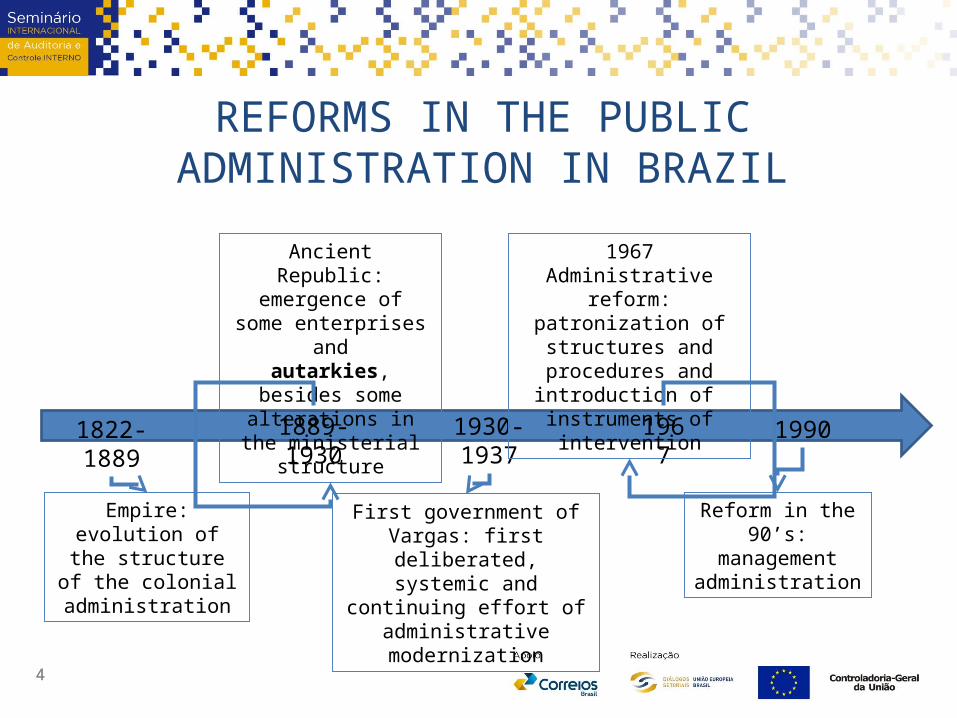

1822-1889 1930-1937 19901889-1930 1967

Empire: evolution of the structure of the

colonial administration

Ancient Republic: emergence of some

enterprises andautarkies, besides some

alterations in the ministerial structure

First government of Vargas: first deliberated, systemic and

continuing effort of administrative modernization

1967 Administrative reform: patronization of

structures and procedures and introduction of

instruments of intervention

Reform in the 90’s: management

administration

REFORMS IN THE PUBLIC ADMINISTRATION IN BRAZIL

55

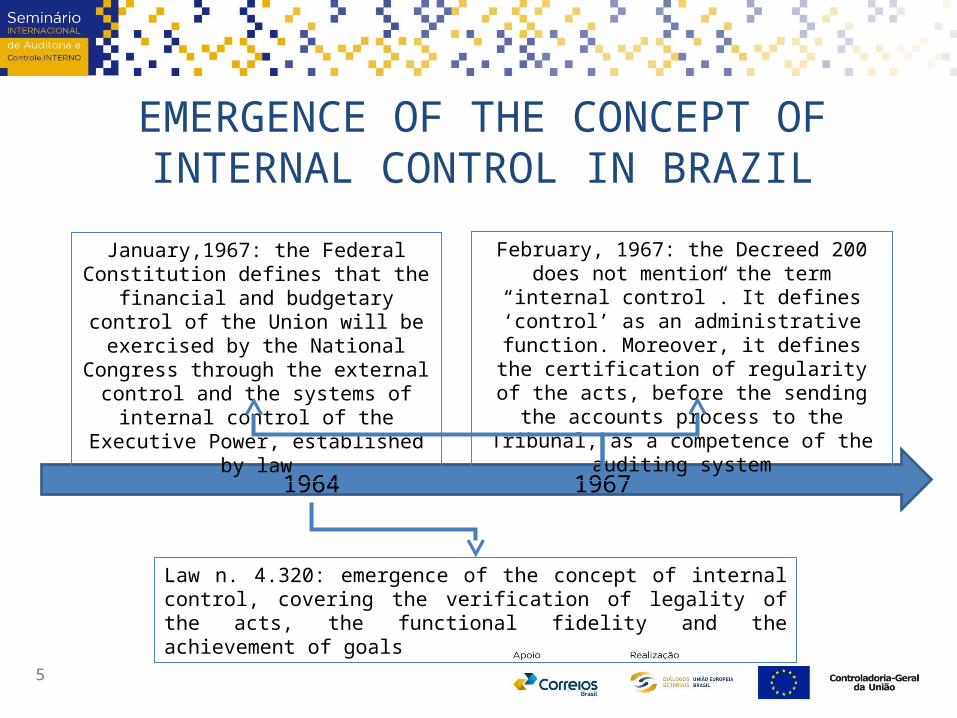

1964 1967

Law n. 4.320: emergence of the concept of internal control, covering the verification of legality of the acts, the functional fidelity and the achievement of goals

January,1967: the Federal Constitution defines that the financial and budgetary

control of the Union will be exercised by the National Congress through the external control and the systems of internal control of the Executive Power, established by law

February, 1967: the Decreed 200 does not mention the term “internal control”. It defines

‘control’ as an administrative function. Moreover, it defines the certification of regularity of the acts,

before the sending the accounts process to the Tribunal, as a competence of the auditing system

EMERGENCE OF THE CONCEPT OF INTERNAL CONTROL IN BRAZIL

6

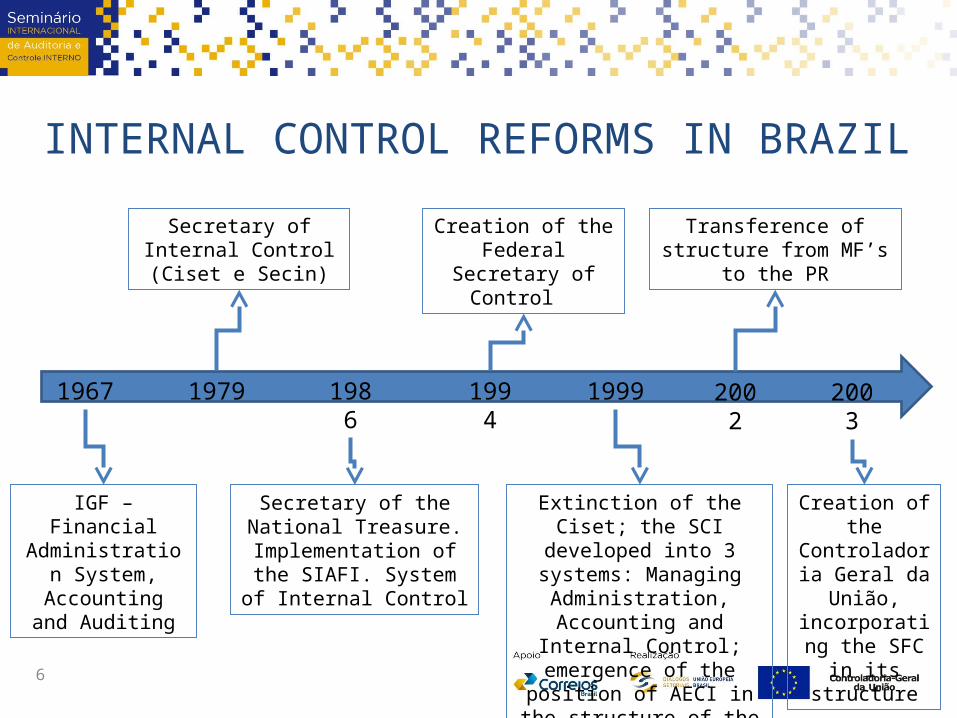

20021967 1986 1999 20031979 1994

IGF – Financial Administration

System, Accounting and Auditing

Secretary of Internal Control (Ciset e Secin)

Secretary of the National Treasure. Implementation of

the SIAFI. System of Internal Control

Creation of the Federal Secretary of

Control

Extinction of the Ciset; the SCI developed into 3 systems:

Managing Administration, Accounting and Internal

Control; emergence of the position of AECI in the

structure of the Ministries

Transference of structure from MF’s to the PR

Creation of the Controladoria

Geral da União, incorporating the SFC in its

structure

INTERNAL CONTROL REFORMS IN BRAZIL

Top Related