Languages

Pages

Legal

RCS MediaGroup

FY 2016 Results

Milan, March 24th, 2017

2

Agenda

Highlights

FY 2016 Results

Outlook 2017

Saving 2016 - 2017

New Projects

3

2016 FY Results – Highlights

EUR million

20152016

EBITDA excl. Non Recurring

100,5 M€ 71,8 M€

NFP 366,1 M€ 486,7 M€

EBITDA 89,9 M€ 16,4 M€

Net Cash Flow excl. Disposals & Acquisition

41,8 M€ -55,6 M€

Net Result 3,5 M€ -175,7 M€

Last Positive

Net Result in 2010

4

2016 FY Results – Guidance achieved

EUR million

Target2016

Net Efficiencies 71,3 M€ 40-45 M€

EBITDA % excl. Non Recurring

~10,4% ~10%

Debt Ratio ~4x3.6x

Net Cash Flow Break even>40 M€

5

Agenda

Highlights

FY 2016 Results

Outlook 2017

Saving 2016 - 2017

New Projects

6

Risultati Consolidati: KPI Dicembre 2016M€

Q4 2016 Q4 2015 ∆% 2016 2015 ∆%

Total Revenue 258,9 10 0 % 289,1 10 0 % (10 ,4%) 968,3 10 0 % 1032,2 10 0 % (6 ,2%)

Circulation 89,6 97,0 (7 ,6%) 380,4 420,9 (9 ,6%)

Advertising 133,2 148 (10,0%) 451,2 475,5 (5 ,1%)

Other 36,1 44,1 (18,1%) 136,7 135,8 0,7%

EBITDA ex NR I tems 49,5 19 ,1% 53,1 18 ,4 % (6 ,8%) 100,5 10 ,4 % 71,8 7,0 % 40,0%

Non Recurring I tems (0 ,0 ) (42 ,5 ) (10 ,6 ) (55 ,4 )

EBITDA 49,5 19 ,1% 10,6 3 ,7% 367,0% 89,9 9 ,3 % 16,4 1,6 % 448,2%

EBIT 35,8 (33,0 ) 35,0 (107,0 )

Ne t Result 21 ,0 (49,3 ) 3 ,5 (175,7 )

NFP (366,1 ) (486,7 )

7

Q416 Q415 2016 2015 ∆%

Circulation 89,6 34,6% 97,0 33,6% 380,4 39,3% 420,9 40,8% (9,6%)

Advertising 133,2 51,4% 148,0 51,2% 451,2 46,6% 475,5 46,1% (5,1%)

Other 36,1 13,9% 44,1 15,3% 136,7 14,1% 135,8 13,2% 0,7%

TOTAL REVENUE 258,9 100% 289,1 100,0% 968,3 100% 1.032,2 100,0% (6 ,2%)

Operating costs (144,3) -55,7% (169,7) -58,7% (600,8) -62,1% (679,7) -65,8% (11,6%)

Non recurring costs 0,0% 0,0% 0,0% 0,0% #DIV/0!

Labour costs (65,1) -25,1% (66,4) -23,0% (266,9) -27,6% (280,7) -27,2% (4,9%)

EBITDA ex Non Recurring It ems 49,5 19,1% 53,1 18,4% 100,5 10,4% 71,8 7,0% 40,0%

Non Recurring Items 0,0 0,0% (42,4) -14,7% (10,6) -1,1% (55,4) -5,4% (80,9%)

EBITDA 49,5 19,1% 10,6 3,7% 89,9 9,3% 16,4 1,6% 448,4%

D&A (13,2) -5,1% (15,3) -15,0% (54,2) -5,6% (59,3) -5,7%

Impairment writeoffs (0,5) -0,2% (28,2) (9,8%) (0,7) -0,1% (64,1) (6,2%)

EBIT 35,8 13,8% (33,0) (11 ,4%) 35,0 3,6% (107,0) (10 ,4%)

Net financial incomes (charges) (6,5) -2,5% (8,5) -2,9% (30,0) -3,1% (36,3) -3,5%

PRE-TAX RESULT 29,3 11,3% (41,5) (14 ,4%) 5,0 0,5% (143,3) (13 ,9%)

Taxes (8,3) -3,2% (0,3) -0,1% (9,9) -1,0% 7,9 0,8%

NET RESULT FROM CONTINUING OPERATIONS 21,0 8,1% (41,8) (14 ,5%) (4,9) (0 ,5%) (135,4) (13 ,1%)

Net Result from Discontinuing and Discontinued Op. 0,0 0,0% (5,1) -1,8% 8,4 0,9% (38,8) -3,8%

Minorities 0,0 0,0% (2,4) -0,8% 0,0 0,0% (1,5) -0,1%

NET RESULT 21,0 8,1% (49,3) (17 ,1%) 3,5 0,4% (175,7) (17 ,0%)

Q4 & FY 2016 ResultsEUR million

Last Positive Net Result in 2010

8

Balance Sheet

EUR million

Net fixed assets 695,2 149,0% 745,0 125,9%

Tangible & Intangible fixed assets 502,9 107,8% 539,9 91,2%

Financial fixed assets 192,3 41,2% 205,1 34,7%

Net working capital (73,6) (15,8%) (64,2) (10,8%)

Reserve for risk and charges (114,9) (24,6%) (115,7) (19,5%)

Employee termination indemnity (40,2) (8,6%) (40,1) (6,8%)

Net invested capital: assets held for sale 66,8 11,3%

CAPITAL EMPLOYED 466,5 100,0% 591,9 100,0%

Net financial debt (cash) total 366,1 78,5% 486,7 82,2%

Net financial debt (cash) related to continuing operations 530,9 89,7%

Net financial debt (cash) of assets held for sale (44,2) (7,5%)

Equity 100,4 21,5% 105,2 17,8%

EQUITY & NFP 466,5 100,0% 591,9 100,0%

31/12/2016 31/12/2015

9

-486,7

-366,1

-23,9-39,7

NFP31/12/2016

+120,6

Operating Cash Flow (3)

+105,4

CAPEXOthers (2)Disposals, Acquisition (1)

NFP31/12/2015

+78,8

2016 Cash Flow

Cash flow representation as of management reporting

EUR million

(1) Including Books NFP deconsolidation(2) Non recurring items and other minor (3) Including dividends

-7VS PY

+90VS PY

+16VS PY

-7VS PY

+16VS PY

+99VS PY

10

Agenda

Highlights

FY 2016 Results

Outlook 2017

Saving 2016 - 2017

New Projects

11

2017E

RevenuesSlight increase net

of third parties publishers

EBITDA 140 M€

EBITDA % ~15%

Net Result Increasing Positive

Outlook 2017

Net Cash Flow Improving Positive

12

Outlook 2017

936

Target 2017

32Third party

RCS

2016

940-950

Excluding advertising

revenues coming from ceased

third party publishers with

little marginality, expected

revenues for 2017 are

exceeding the 2016 result.

13

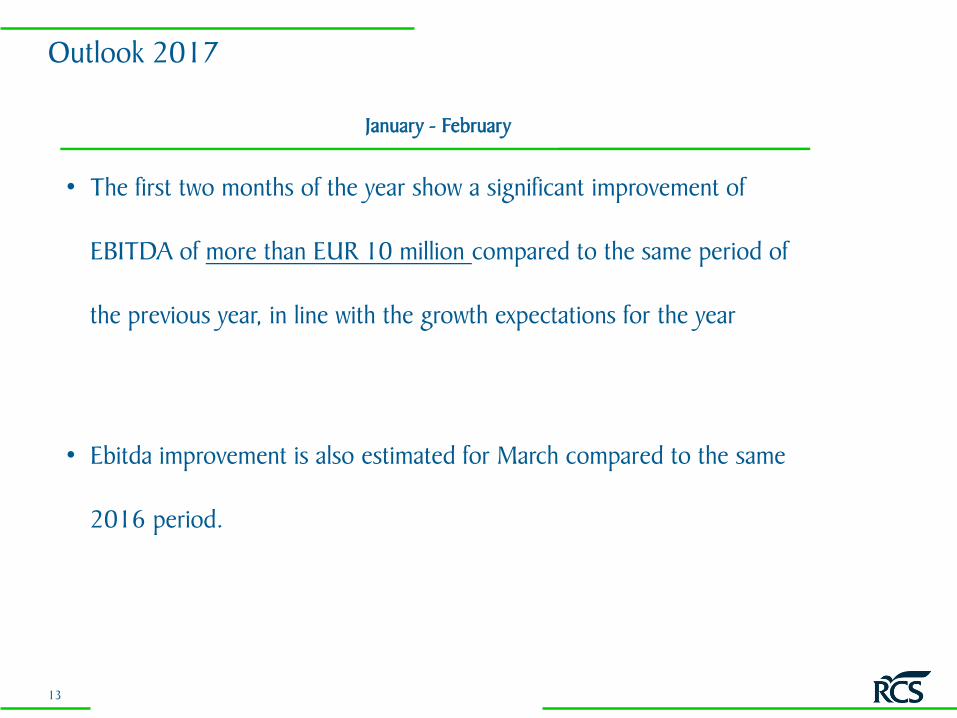

Outlook 2017

• The first two months of the year show a significant improvement of

EBITDA of more than EUR 10 million compared to the same period of

the previous year, in line with the growth expectations for the year

• Ebitda improvement is also estimated for March compared to the same

2016 period.

January - February

14

Agenda

Highlights

FY 2016 Results

Outlook 2017

Saving 2016 - 2017

New Projects

15

Saving 2016 - 2017EUR million

71,30

42-46

Achieved 2016

Target 2017

113-117 M€

16

Print cost ~15,0

Paper cost ~4,0

Set up sport events ~1,0

Publishing collaboration ~7,0

It ~6,0

Playout Digicast ~0,5

Saving 2016-2017: Italy + SpainEUR million

Distribution & transports ~7.5

Travel expenses ~3,5

Rental costs ~5,2

Consultancy, profess. serv. ~3,0

Facility management/Utilities ~3,0

Others * ~10,0

*Insurance, car fleet, canteen, taxi, newspapers & books, switchboard, ect

,0

17

Agenda

Highlights

FY 2016 Results

Outlook 2017

Saving 2016 - 2017

New Projects

18

• From October 2016: thorough review, enthusiastic readers and

advertising market reaction

Magazines

18

• From August 2016: most popular topics, new graphic, +37% in copies

(Yoy Jan-Feb 2017)

• From March 2016: L’economia, the new Monday economic attachement

characterised by innovative updated graphics and exclusive contents to offer

continuous, accurate and fast economic and financial information

19

Magazines

RCS - OGGI

Newsstand sales

First 10 issues

1.520.000

1.125.000

1.409.0001.481.000

20162014 2015 2017

20

Corriere della Sera

• Lo dico al Corriere: a new page by Aldo Cazzullo where the readers of

Corriere della Sera can share experiences and reflections.

• The newspaper also features the new column Il Caffè written by Massimo

Gramellini.

• From April 2017: every Thursday at the newsstands with a new editor,

Beppe Severgnini.

21

The week of Corriere della Sera

MON TUE WED THU FRI SAT SUN

ECONOMIA

• Free

• 48/56 pg

• National

LIVING

STYLE

• +0,50€

• National

• Monthly

VIVIMILANO

• Free

• 72 pag

• Local

IO DONNA

• +0,50€

• National

LA LETTURA

• +0,50€

• Optional

• National

SETTE

• +0,50€

• 116 pag

• National

22

«Grande» Gazzetta dello Sport

• 10 special issues during 2017 (one per month from

February) giving wide space to relevant national and

international sport events

• Increased print run

• Large foliation

• Wide Cover

• Supporting advertising campaign

• Additional advertising spaces to sell

23

Gazzetta dello Sport

• Geolocalization contents in order to maintain the circulation market share in

specific areas following customer needs:

• ATALANTA

• BOLOGNA/TORINO

• FIORENTINA/UDINESE

• HELLAS VERONA

• CAGLIARI

• BRESCIA/VARESE

• BARI

• PALERMO

• Add value through local edition with first page dedicated to each specific team

24

Spain

24

• Commercial Agreement including the creation of Marca Claro,

the Worldwide alliance for multimedia sports information in

South America

• Launch of a new magazine before summer 2017

• Major changes also for Marca and Radio Marca, with

completely renewed style and contents.

25

Disclaimer

Statements contained in this document, particularly the ones regarding any RCS MediaGroup possible or assumed future performance, are or may be forward looking statements and in this respect they involve some risks and uncertainties.

RCS MediaGroup actual results and developments may differ materially from the ones expressed or implied by the following statements depending on a variety of factors.Any reference to past performance of RCS MediaGroup shall not be taken as an indication of future performance.

This communication does not constitute an offer or solicitation for the sale, purchase or acquisition of securities of any of the companies mentioned in any jurisdiction and is directed to professionals of the financial community.

Riccardo Taranto, the Manager responsible for drawing up the company’s accounting statements, hereby declares, pursuant to article 154-bis, paragraph 2 of the “Testo Unico della Finanza” (Legislative Decree n. 58/1998), that the information contained in this presentation corresponds to those one contained in the group’s documents and books accounting records.

Investor Relations Department

Forward-looking Statements

+39 02 2584 [email protected]

Paolo Gatti

Top Related