Languages

Pages

Legal

Capital Markets Presentation

Accelerating Growth

The long term drivers

2 October 2013

These capital markets day materials include forward-looking content with

respect to the markets in which the Group operates. Such content may be

affected by a number of risks and uncertainties that can cause results and

developments to differ materially from those currently anticipated. IMI

undertakes no obligation to update forward-looking content. Market share

information is approximate and based on certain market niches and

applications where IMI is active.

Disclaimer

2

Welcome and Introduction

Martin Lamb

Chief Executive, IMI plc

Strategic convergence

Focusing on the ‘sweetspot’

• Shared progress through

Capital Markets series

over three years

• Drive ‘sweetspot’

convergence to 75% by

2017

October 2011 – Fluid Technologies

October 2012 – Niche Leadership

Commercial Vehicle

Life Sciences Food & Beverage

Rail Sector Energy

Sector

LNG

Nuclear

Fossil

Petrochem & Refin

Iron & Steel

Hydronic Conditioning

Hydronic Balancing

TRV's

Variety, Health & Wellness

CDD Opps Efficiency

Frozen

Aftermarket Foodservice

0%

5%

10%

15%

October 2013 – Growth Drivers

• Opportunities arising from mega-

trends

• Understanding of engineering

‘need’

• Derivation of technology roadmap

Key messages

• Mega-trends will have a profound impact on our

customers and end markets

• Prime position to benefit based on market

positioning and technologies

• Technology roadmaps in place

…… and brimming!

• Pathway to higher returns clear cut

……execution is key

Welcome & Introduction Martin Lamb

Long term growth drivers Roy Twite

Mega-trend driven growth opportunities

- LNG: New growth opportunities Rob Campbell

- Petrochemical: Positive impact of shale gas Metin Gerceker

- Commercial Vehicles: Tomorrow’s truck Mark Sealy

Break for refreshments

Mega-trend driven growth opportunities

- Life Sciences: Healthcare of the future Robert Guerra

- Indoor Climate: Smart buildings Stefan Seitz

- Beverage: Restaurant of the future Mike Coombes

Sweetspot development conclusions Martin Lamb

Questions and Answers Executive Directors

Refreshments

Agenda

Long Term Growth Drivers

Roy Twite

Executive Director

Growth drivers – agenda

1. Major global trends

2. Creating engineering requirements

3. Driving IMI’s technology road map

Growth drivers – mega-trends

long term sustainable global

Climate change

Resource scarcity

Urbanisation

Ageing population

Climate change

“From 1990 to 2030 greenhouse

gases are expected to increase

by between 25% to 90%”

Source: Frost & Sullivan

Climate change

“Markets for low-carbon energy

products are likely to be worth

at least $500bn per year by 2050”

Source: Frost & Sullivan

Resource scarcity

“A 40% increase in energy

demand is forecast by 2030”

Source: Frost & Sullivan

Resource scarcity

“An additional $26trn of investment

required to support

increasing energy demands”

Source: Frost & Sullivan

+ 50 GW

Resource scarcity

“Shale gas reserves are expected

to make the US energy independent

by 2020”

Source: Frost & Sullivan

Urbanisation

“Between 2009 & 2050, urban population

will double to 6.4 billion people”

Source: Frost & Sullivan

Ageing population

“Between 2000 and 2050

the proportion of people over 60

will double from 11% to 22%”

Source: Frost & Sullivan

Ageing population

“Two-thirds of healthcare

spending goes on people

over 65 years old”

Source: Frost & Sullivan

Mega-trends to IMI technology roadmap

Understand the

mega-trends and

sub-trends they

drive

Understand the

customer‘s

engineering

requirements

Understand how

that translates into

new technology

developments

Our niches

Commercial Vehicle

Life Sciences Food &

Beverage

Rail Sector Energy

Sector

LNG

Nuclear

Fossil

Petrochem & Refin

Iron & Steel

Hydronic Conditioning

Hydronic Balancing

TRV's

Variety, Health & Wellness

CDD Opps Efficiency

Frozen

Aftermarket Foodservice

0%

5%

10%

15%

Future CAGR

Leadership Threshold

Leadership position

Niche leadership – LNG

The Niche : Severe Service application

valves & actuation into LNG plants

Growth CAGR 2012-2017

Industry growth

Source: IEA, Douglas

Westwood

6 - 8%

Niche growth 6 - 8%

Incremental revenue

growth opportunities 0 - 2%

Niche Size c.£210m

IMI Share % <10 10-20 20-30 >30

Market

Position 1

Key

Competitors

Koso, PBVS, Severn Glocon,

Vanessa (Tyco)

Key

Customers

Bechtel, Chevron, JGC,

Petronas, Shell, Woodside

Source: IMI estimates

Backing winners

KAM – Choosing winning :-

• End market drivers

• Customers

• Projects

Smart Choices……

• Dragons Den/Shark Tank

• Fit with strategy

• Value proposition

• Competitive position

Fluid Power

Dragons Den

Prioritising projects

Climate change

Climate change – implications

Climate change

Move to combined cycle

gas in powergen

Nuclear still important to

China and India

Power plant efficiency

Less flaring

Commercial Vehicle fuel

efficiency legislation

Energy efficiency in

buildings

TRENDS ENGINEERING

REQUIREMENTS

Control of huge

pressure drops

Higher temperature

materials

Safety retrofits required

Waste Heat Recovery

New refrigerants

More precise flow

control

Pressure protection

systems

Move away from harmful

refrigerants

Climate change – technology roadmap

Commercial

Vehicle valve –

Euro VI

New TRV with

Flow Control

Launched Year 1 Year 2 Year 3 +

Commercial

Vehicle – waste

heat recovery

Range of energy

efficient beverage

coolers

Nuclear steam

control valves

and actuators

Terminal unit

balancing &

control valves

Optimised

nuclear strainers

Nuclear

containment

venting systems

Analytical

chromatography

valves for gas

analysis

Valves for small

nuclear reactors

Zero leakage

seals / fugitive

emissions

monitoring

Smart Valve and

Actuator

District Energy

Products

Commercial

Vehicles - CNG

Beverage Indoor Climate Fluid Power Severe Service

2018 engine (US) 2006 engine (Eu3)

Climate change – truck engines

€50 per truck €900 per truck IMI opportunity:

Resource Scarcity

Resource scarcity – implications

Floating platforms –

FPSOs and FLNG

Fuel & energy efficiency

legislation

Peak load → cycling

Gas transportation / LNG

More extreme extraction

e.g. deep sub sea

TRENDS

Higher pressure valve

sealing

Lower power

requirements

Smaller envelope,

lighter weight

cryogenic valves

Faster response

compressor

control valves

Lower noise

requirements

Better control

Resource scarcity

Remote locations

ENGINEERING

REQUIREMENTS

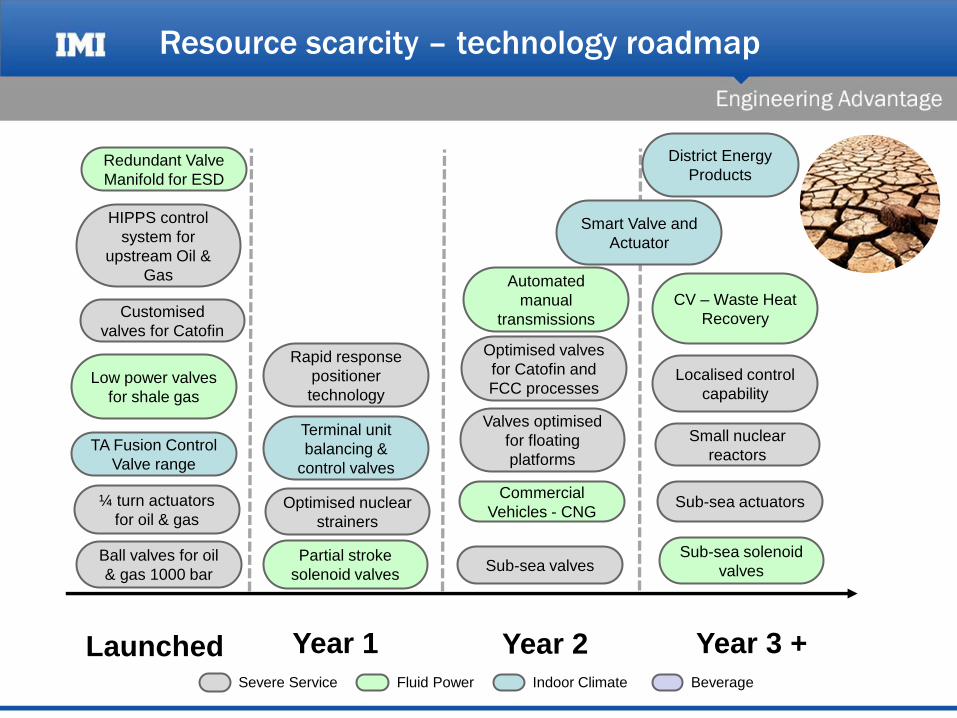

Resource scarcity – technology roadmap

Redundant Valve

Manifold for ESD

Ball valves for oil

& gas 1000 bar

Low power valves

for shale gas

Launched Year 1 Year 2 Year 3 +

Partial stroke

solenoid valves

¼ turn actuators

for oil & gas

Valves optimised

for floating

platforms

Small nuclear

reactors

CV – Waste Heat

Recovery

Commercial

Vehicles - CNG

TA Fusion Control

Valve range

Automated

manual

transmissions

Sub-sea solenoid

valves

Customised

valves for Catofin

HIPPS control

system for

upstream Oil &

Gas

Optimised nuclear

strainers

Rapid response

positioner

technology

Optimised valves

for Catofin and

FCC processes

Sub-sea valves

Localised control

capability

Sub-sea actuators

Terminal unit

balancing &

control valves

Smart Valve and

Actuator

District Energy

Products

Beverage Indoor Climate Fluid Power Severe Service

Dehydrogenation Cracking

Resource scarcity – polymers

IMI opportunity: £3m per install Up to £18m per install

Urbanisation

Urbanisation

Urbanisation – implications

Increasing consumer

demands

Increased demand for

power, energy efficient

buildings

Increasing freight

transportation

Increased pollution from

transportation

Increased demand for

materials

Pressure on space

TRENDS

More precise flow

control

Lower weights

& energy efficiency

More dispense variety

More compact solutions

Increased demand for

mass transit

EGR and SCR

Gas to chemicals

Microdosing

More reliability,

faster access

ENGINEERING

REQUIREMENTS

Urbanisation - technology roadmap

Launched Year 1 Year 2 Year 3 +

Blend in cup

smoothie

dispenser

Batch carbonator

for organic sodas

Tea dispensers

Automated

Beverage

Dispenser

Residential

carbonated water

dispenser

CV– Bus HVAC

valves

Train door control

systems

Rail air dryer

systems

CNG valves and

regulators

Emissions control

for off-highway

vehicles

Balancing &

control calve

range

New TRV with

flow control

Terminal unit

balancing &

control valves

Smart valves and

actuators

District energy

products

Batch carbonator

for organic sodas

Tea dispensers Residential

carbonated water

dispenser

Beverage Indoor Climate Fluid Power Severe Service

Urbanisation – evolving buildings

HVAC System 2005 • Balancing and differential pressure control valves

• Basic terminal valves

Smart HVAC System 2017 • Balancing & control valves

• Smart valves & actuators

• Full terminal valve offer

• Pressurisation and water quality portfolio

• Connectivity and measurement solution

£350k

£1.5m

Ageing population

Ageing population – implications

Out of hospital

treatment

More frequent and

sophisticated testing

Healthier lifestyles,

drinks

Prevention vs treatment

Increased demand for

healthcare

Ever greater regulatory

burdens

Shortages of skilled

clinical staff

TRENDS

Ease of use, robustness

Smaller, lighter

Reduce sample and reagent

size, micro dosing

Reduced testing cycle time

Increased safety &

redundancy in systems

Increased automation

Ageing population

Increasing patient

expectations

Freshness, pulp dispense

Lower Power

ENGINEERING

REQUIREMENTS

Ageing population - technology roadmap

High flow

proportional valve

Miniature inline

syringe / piston

pumps

Miniature media

separated valves

Launched Year 1 Year 2 Year 3 +

Nanoliter (nl)

dispense/dosing

technologies

Electronic

pressure & flow

Controllers

Chromatography

multiport valves &

fittings

Analytical

gas/liquid

detectors

Analytical

proportional

valves

Configurable

syringe pump

technology

DC & closed- looped

intelligent pumps

Laminated

manifold

technology

Micro

proportional

valves

Separation

technology (gas

& liquid)

Proportional

valves for liquids

Condition

monitoring &

dispense

confirmation

Disposables &

consumables

Beverage Indoor Climate Fluid Power Severe Service

2013 portable ventilator 2003 portable ventilator

Ageing population – respiratory care

IMI opportunity = £250/device

IMI opportunity = £200/device

.

Weight:

0.5KG

Weight:

6.5 KG

IMI Group technology roadmap

Launched Year 1 Year 2 Year 3 +

Commercial

Vehicle valve –

Euro VI

New TRV with

Flow Control

Commercial

Vehicle – waste

heat recovery

Range of energy

efficient beverage

coolers

Nuclear steam

control valves

and actuators

Terminal unit

balancing &

control valves

Optimised

nuclear strainers

Nuclear

containment

venting systems

Analytical

chromatography

valves for gas

analysis

Valves for small

nuclear reactors

Zero leakage

seals / fugitive

emissions

monitoring

Smart Valve and

Actuator

District Energy

Products

Commercial

Vehicles - CNG

Redundant Valve

Manifold for ESD

Ball valves for oil

& gas 1000 bar

Low power valves

for shale gas

Partial stroke

solenoid valves

¼ turn actuators

for oil & gas

Valves optimised

for floating

platforms

Small nuclear

reactors

CV – Waste Heat

Recovery

Commercial

Vehicles - CNG

TA Fusion Control

Valve range

Automated

manual

transmissions

Subsea solenoid

valves

Customised

valves for Catofin

HIPPS control

system for

upstream Oil &

Gas

Optimised nuclear

strainers

Rapid response

positioner

technology

Optimised valves

for Catofin and

FCC processes

Sub-sea valves

Localised control

capability

Sub-sea actuators

Terminal unit

balancing &

control valves

Smart Valve and

Actuator

District Energy

Products

Blend in cup

smoothie

dispenser

Batch carbonator

for organic sodas

Tea dispensers

Automated

Beverage

Dispenser

Residential

carbonated water

dispenser

CV– Bus HVAC

valves

Train door control

systems

Rail air dryer

systems

CNG valves and

regulators

Emissions control

for off-highway

vehicles

Balancing &

Control Valve

range

New TRV with

Flow Control

Terminal unit

balancing &

control valves

Smart Valves

and Actuators

District Energy

Products

Laminated

manifold

technology

High flow

proportional valve

Miniature inline

syringe / piston

pumps

Miniature media

separated valves

Nanoliter (nl)

dispense/dosing

technologies

Electronic

pressure & flow

Controllers

Chromatography

multiport valves &

fittings

Analytical

gas/liquid

detectors

Analytical

proportional

valves

Configurable

syringe pump

technology

DC & closed- looped

intelligent pumps

Laminated

manifold

technology

Micro

proportional

valves

Separation

technology (gas

& liquid)

Proportional

valves for liquids

Condition

monitoring &

dispense

confirmation

Disposables &

consumables

Beverage Indoor Climate Fluid Power Severe Service

Filling the technology gaps

• Some technology needs will be met via:

• Acquisition, licencing, joint ventures

• Potential adjacent markets include:

- Sub-sea valves and actuation

- Complex controls and electronics

- Sensors

- Specialist filtration

LNG

Nuclear

Fossil

Petrochem

Iron & Steel

Commercial Vehicle

Life Sciences

Food & Beverage

Rail

Energy

Hydronic Balancing

Hydronic Conditioning

TRVs

Variety, Engagement,Health & WellnessOperator Efficiency

Frozen

Aftermarket Parts

Group technology roadmap impact

Adjacencies

2012

17 Niches

2017

c.20 Niches

• Underlying growth in niche

markets 5-7%

• c.£400m of revenue coming

from new products in 2017

• Incremental growth from

new products 2-3%

• Opportunities to develop

leadership positions in

adjacent niches through

acquisition

Mega-trend driven growth opportunities

• LNG

New growth opportunities

• Petrochemical

Positive impact of shale gas

• Commercial Vehicles

Tomorrow’s truck

Mark Sealy

Metin

Gerceker

Rob Campbell

• Life Sciences

Healthcare of the future

• Indoor Climate

Smart buildings

• Beverage

Restaurant of the future

Mike Coombes

Robert Guerra

Stefan Seitz

Mega-trend driven growth opportunities

LNG

New growth opportunities Rob Campbell

Sales Director, Northern Europe

Niche leadership – LNG

The Niche : Severe Service application

valves & actuation into LNG plants

Growth CAGR 2012-2017

Industry growth

Source: IEA, Douglas

Westwood

6 - 8%

Niche growth 6 - 8%

Incremental revenue

growth opportunities 0 - 2%

Niche Size c.£210m

IMI Share % <10 10-20 20-30 >30

Market

Position 1

Key

Competitors

Koso, PBVS, Severn Glocon,

Vanessa (Tyco)

Key

Customers

Bechtel, Chevron, JGC,

Petronas, Shell, Woodside

Source: IMI estimates

Ageing population

Urbanisation

Climate change

Resource scarcity

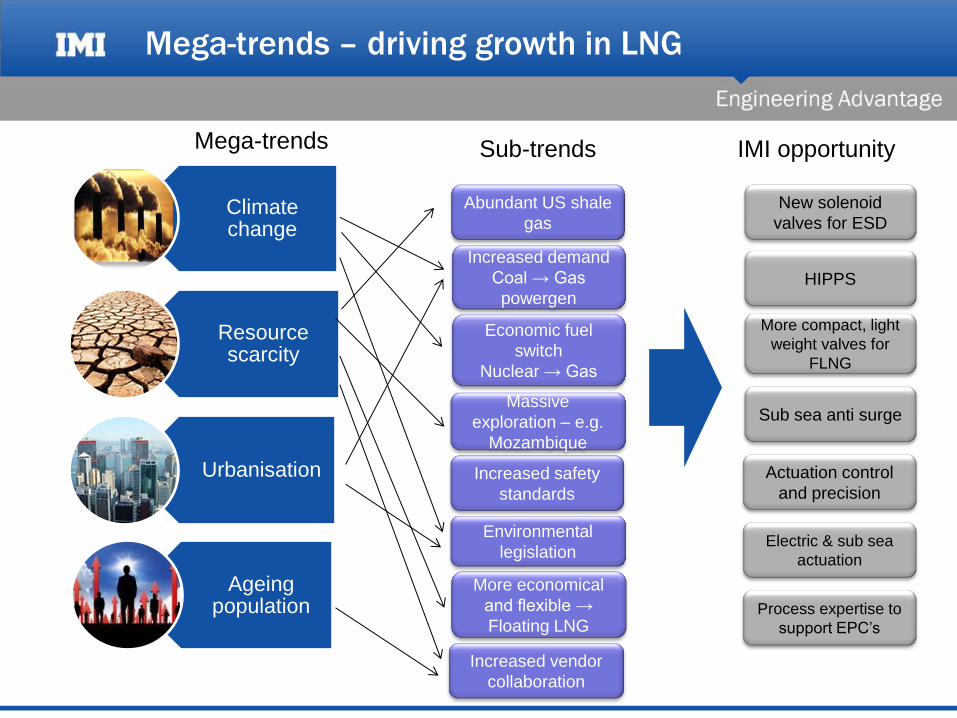

Mega-trends – driving growth in LNG

Massive

exploration – e.g.

Mozambique

Increased safety

standards

More economical

and flexible →

Floating LNG

Abundant US shale

gas

Economic fuel

switch

Nuclear → Gas

New solenoid

valves for ESD

Electric & sub sea

actuation

More compact, light

weight valves for

FLNG

Sub sea anti surge

Actuation control

and precision

HIPPS

Process expertise to

support EPC’s

Mega-trends IMI opportunity Sub-trends

Environmental

legislation

Increased demand

Coal → Gas

powergen

Increased vendor

collaboration

Ball valves for oil

& gas <1000bar

Launched Year 1 Year 2 Year 3 +

Partial stroke

solenoid valves

¼ turn actuators

for oil & gas Floating LNG

valves

Commercial

Vehicles - CNG

Harnessing the growth opportunity

Fast Trak / Quick

Trak

Redundant Valve

Manifold for ESD

Safety Integrity

Level 2 & 3

LNG valves for

marine engines

Fugitive

emissions

monitoring

Optimised valves

for Catofin & FCC

Subsea LNG

valves

Optimised valves

for Floating

Platforms

Support global

engineering for

O&G Majors

Recent successes in LNG

Recent LNG projects awarded:

Australia Pacific LNG 9mtpa

Gladstone LNG 3.5mtpa

Ichthys LNG 10mtpa

Sabine Pass 1 & 2 LNG 10mtpa

Prelude (Shell) FLNG 3.6mtpa

PNG Papua New Guinea 6.9mtpa

Approx. £85m in value

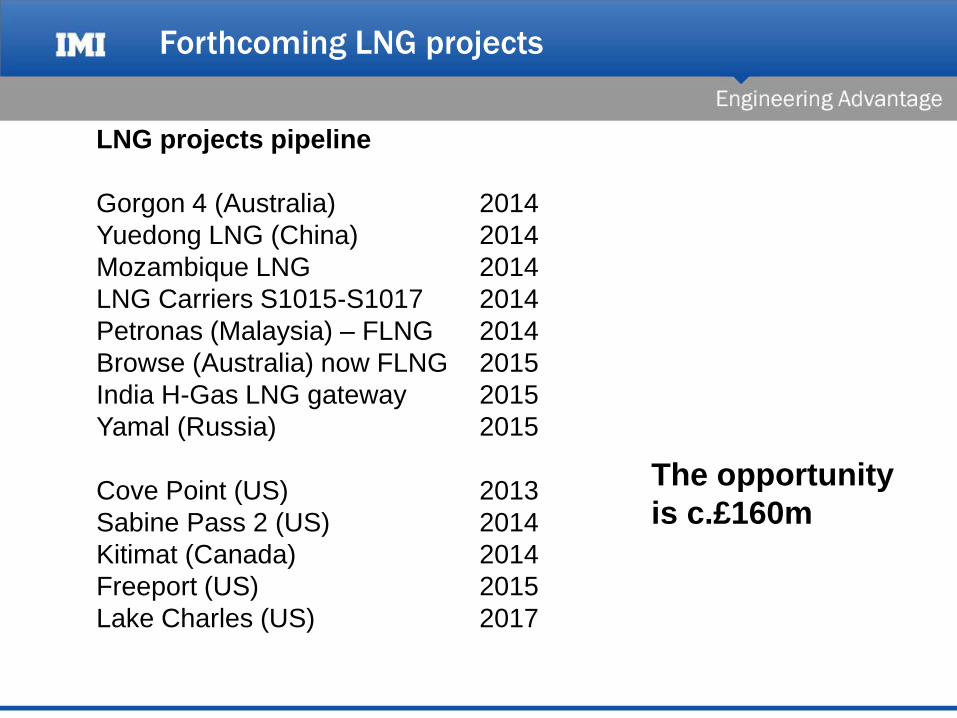

Forthcoming LNG projects

LNG projects pipeline

Gorgon 4 (Australia) 2014

Yuedong LNG (China) 2014

Mozambique LNG 2014

LNG Carriers S1015-S1017 2014

Petronas (Malaysia) – FLNG 2014

Browse (Australia) now FLNG 2015

India H-Gas LNG gateway 2015

Yamal (Russia) 2015

Cove Point (US) 2013

Sabine Pass 2 (US) 2014

Kitimat (Canada) 2014

Freeport (US) 2015

Lake Charles (US) 2017

The opportunity

is c.£160m

Floating LNG

Why Floating LNG?

• Addresses environmental

constraints

• More economical

• Can be relocated

• More suitable for small gas

fields

Floating LNG Projects

• Shell Prelude

• Browse, Australia

• Petronas (Malaysia)

New FLNG designs – meeting needs

Design for

• lightweight

• streamlined castings

• DRAG for low noise characteristic

Designs validated by our Valve Doctors and flow capacity and stress analysis

using CFD and FEA

Original design New design CFD studies

Floating example – Prelude

Prelude – world’s first FLNG

• Many valve packages (to date, design not

finalised)

• Need to be approved/certified by Shell &

Technip

• IMI has won 75% of all packages for ball and

butterfly isolations valves

GAS TREATMENT

(Sweetening; De-Watering

etc.)

Tri Eccentric Butterfly

Trunnion Mounted Ball

Valves

LIQUEFACTION

(Cryogenic Process)

Tri Eccentric Butterfly

Trunnion Mounted Ball

Anti surge compressor valves COOLING SYSTEM

Butterfly

FIRE FIGHTING

Butterfly UL 1091

PROCESS VALVE

Top Entry Ball Valve

STEAM PACKAGE

Unique to FLNG

Other growth opportunities in LNG

• Noise – manned floating platforms

• Lightweight but maintain CV (capacity)

• Fast response, precise control

Summary

• The mega-trends are driving growth in LNG of 6-8%

• Sub-trend towards Floating

• Terminal process reversal in US

• Niche leadership in Severe Service valves in LNG is captured through

• Valve Doctor & engineering expertise

• Design Partnership – Key LNG & EPC players

• Surge protection

• Delivered by developing technology

• Actuation – speed of response, precise control

• Noise attenuation

• Lightweight maintaining capacity

LNG Opportunity

Petrochemical

Positive impact of shale gas Metin Gerceker

Managing Director, Zimmermann & Jansen

Niche Leadership – Petrochemical

The Niche: Severe service in several key applications;

Delayed Coking (DC), Fluid Catalytic Cracking (FCC),

Ethylene/Propylene (Catofin) and Purified Terephthalic Acid

(PTA)

Niche Size c.£180m

IMI Share % <10 10-

20 20-30 >30

Market Position 1

Key

Competitors

Delta Valve (both Curtiss

Wright), Poyam,

Tapco/Enpro

Key Customers

ExxonMobil, Lukoil,

Petrobras, Sinopec,

Statoil, UOP

Growth CAGR 2012-2017

Industry growth

Source; Global Data

12, Oil & Gas

Journal

2 - 4%

Niche growth 2 - 4%

Incremental revenue

growth opportunities 3 - 5%

Source: IMI estimates

Ageing population

Urbanisation

Climate change

Resource scarcity

Mega-trends – driving growth in Petrochemical

OPEC countries

– aim to add

more value to

resources

Shale & LNG

demand reduced

gas costs

Requirement for

new catofin

plants

High temperatures

FCC

Duplicated safety

valve systems

Fracking -

injection

New generation

plants in ME

Highly corrosive

materials

DC

Mega-trends IMI opportunity Sub-trends

Increased

demand for

plastics

US investing in

new petrochem

plant

Increased vendor

collaboration

Launched Year 1 Year 2 Year 3 +

Slide gate valves

Harnessing the growth opportunity

Butterfly valves

Goggle valves

Through conduit

valves

Double disc

through conduit

Variable orifice

valves

Hydraulic control

for DC valves

Hydraulic

actuation for

Catofin valves

Combined

control/isolation

valves for FCC

New ball valves

for processes

Partial stroking

solenoid valves

Fugitive

emissions

monitoring

Support global

engineering for

O&G majors

Every product is

engineered to order

Recent successes in Petrochemical

Recent Petrochemical projects awarded:

Enterprise Catofin® (US)

Reliance PTA (India)

PDVSA (Venezuela)

TANEKO (Russia)

Wood River (US)

TongYi (China)

Hengli Petrochemical (Dalian, China – PTA)

Project value

c.£55m

Forthcoming Petrochemical projects

Selected Petrochem projects pipeline

Catofin® is the process license owned by Lumus (CB&I)

Atyrau Kazakhstan Refinery PetroPeru Talara Coking

EIL – BPCL Kochi Refinery, India FCC & Coker

SK Gas S. Korea Catofin®

KPI Kazakhstan Catofin®

GS Trakreer Refinery, India FCC

Petrologistics/JGC Catofin®

Shangdong II China Catofin®

PDVSA Venezuela FCC

Project value c.£90m

Winning in Petrochemical

Catofin dehydrogenation

• Converts feedstock (propane) into plastic

(propylene) for commercial use

• Severe service valves:

− Air inlet and outlet

− Steam purge

− Hydrocarbon inlet/outlet

− Evacuating

• Up to £18m per plant

Delayed Coker Units

• Thermal cracking to produce hydrocarbon coke

• Severe service valves:

− Butterfly isolation

− Slide valves for unheading

− Goggle valves

• Up to £5m per plant

Winning in Petrochemical

Fluid Catalytic Cracking

• Converts heavy gas oil into gasoline and

diesel

• Severe service valves:

− Sliding gate valves around the

fractionator (c50-60 tonnes)

− Goggle valves around precipitator

− Turbo expander butterfly valves

• Up to £3.5m per plant

Meeting the Severe Service valve needs

Unique needs of FCC & Delayed Coker

• Very high temperature – 750 to 1,650°C

• Extremely corrosive environment

• Maximum reliability – install for 25 year life

Delayed Coker – Severe Service

GDP growth leads to demand – e.g. Rosneft, Russia

Typical Coking plant

Double Disc Through Conduit

slide gate valves

& goggle valves

Catofin plant – Severe Service

• Air inlet & outlet valves

• Hydrocarbon inlet & outlet

valves

• Hydraulic actuators, control

system

Summary

• The mega-trends and sub-trends are driving growth in

Petrochemical of 2 – 4%%

• Niche leadership in Severe Service valves in

Petrochemical are captured through:

• Engineering know-how & expertise

• Bespoke solutions

• Proven track record of reliability over a large install

base

• Delivered by developing technology

• Optimised slide valves

• Design to feedstock requirements

Petrochemical Opportunity

Commercial Vehicles

Tomorrow’s truck

Mark Sealy

Global Technical Director CV Sector

Niche Leadership – Commercial Vehicle

The Niche; robust, precise pneumatic and fluids

control for heavy duty commercial vehicles –

engine valve control, transmission automation

and chassis cab applications

Niche Size c.£580m

IMI Share % <10 10-20 20-30 >30

Market Position 1 or 2

Key

Competitors

Bendix, Bosch, Pierburg,

Wabco

Key Customers

Scania, Volvo, ZF, MAN,

Cummins, Paccar, Daimler,

Ford, Eaton, Caterpillar

Growth CAGR 2012-2017

Industry growth

Source: LMC, Stark,

ATC

3 - 5%

Niche growth 4 - 6%

Incremental revenue

growth opportunities 1 - 2%

Source: IMI estimates

Ageing population

Urbanisation

Climate change

Resource scarcity

Mega-trends – driving growth in Commercial Vehicles

Freight efficiency

Abundant cheap

shale gas

Hybrid drives

Increased

mobility

Emissions

control legislation

Environmental

control <CO2

Improved fuel

consumption

Clean engine

development

Reduce rolling

resistance

CNG engines

Waste Heat

Recovery

Secondary

braking

After treatment

Battery cooling

Mega-trends IMI opportunity Sub-trends

Harnessing the growth opportunity

Effort / risk

Str

ate

gic

va

lue

Growth

Sustain

Amplify

Evaluate

New throttle

ISIS UTHV 2

Asia Trans

CNG/LNG

Water valves

Electric AIT

ZF, Eaton

Tyre inflate

Wastegate

Digital pair

Seat FormFit

Manifolds

ERHC

Prop

pneumatic

Axle mgmt Cab switches

Fuel

Mechanical

pneumatic

Air prep

Waste Heat

Recent successes

Norgren emissions technologies to address pollution and climate change

Electric

Throttle

Wastegate

Proportional

pneumatic

Purge air

Urea tank

heating

Increasing vehicle sophistication = more potential

74

2018 engine 2006 engine

Extending our technology into emerging markets

75

e.g. Level 4 emissions & secondary braking legislation in BRIC

Wastegate

control

Retarder & shift

assist

Gearbox

Interlock EGR control

The road to 2020 – CO2 reduction imperative

• US 2012 legislation requires 17% less CO2 for Class 8

trucks (for a freight-ton-mile) by 2018

• Europe to reduce greenhouse gases from the transport

sector by 20% between 2008 and 2030

Typical CO2 output

s

CO2 reduction – every aspect of fuel usage is examined

Every facet will

be improved

Exhaust

22%

Over 50% of the fuel is

wasted directly as heat

CO2 reduction – what it means by 2020

• 10 - 30% of commercial vehicles will have converted to natural gas

• Rankine cycle waste heat recovery will be deployed

• Advanced & active aerodynamics will be common

• Super single tyres will pervade with inflation management

• Auxiliary Power Units will be utilised to avoid idle time

• Automated Manual Transmissions with retarders will be prevalent

• Most city trucks will have some level of hybrid drive

• Fully electric vehicles will continue to slowly penetrate

• Fuel cells will remain a niche

Conversion from diesel to natural gas is accelerating

Natural gas presents several fluid control opportunities

Typical operating conditions • 350Kw engine > 100Kw waste heat > 30Kw can be recovered > 5% real life fuel saving

• 200g/sec flow rate, -40ºC to 300°C, 30 Bar Ethanol (vacuum sealed for life)

Waste Heat Recovery – a strategic new opportunity

We have made good progress in 12 months

• Market potential for valves in Europe and US > £100M

• 100% sweet spot convergence

• 4 OEM customer programmes > strategic co-developments

• 4 differentiated valve solutions > 3 significant patents

• Deep collaboration between Fluid Power & Severe Service

• Presently leading the valve field

Ethanol turbine by-pass

with de-superheating

Summary

• The mega-trends will continue to drive growth in the CV niche by 4 to 6%

• Niche leadership in CV is captured through

• Proven range of products that operate in extreme environments

(temperature & vibration, long life expectancy)

• Proven track record creating solutions for new applications

• Extension of products within global OEMs

• Technology development includes

• Electric inlet throttles

• Next generation digital pneumatics

• Natural gas

• Waste heat recovery

Commercial Vehicle opportunity

Life Sciences

Healthcare of the Future

Robert Guerra

President, Norgren Americas

Niche Leadership – Life Sciences

The Niche: providing application specific

solutions for the most critical precision fluidic

applications in medical devices, diagnostics

and analytical equipment.

Niche Size c.£520m

IMI Share % <10 10-20 20-30 >30

Market

Position 2-3 (market dependant)

Key

Competitors

Bürkert, Hamilton, Parker

Idex, Tecan

Key

Customers

GE Healthcare, Philips,

Abbott, Danaher, Illumina,

Mindray, Waters

Growth CAGR 2012-2017

Industry growth

Source: AMR

International

4 - 6%

Niche growth 4 - 6%

Incremental revenue

growth opportunities 2 - 4%

Source: IMI estimates

Mega-trends – driving growth in Life Sciences

Ageing population

Urbanisation

Climate change

Resource scarcity

Personalised

medicine

Prevention &

detection vs.

treatment

Rising costs of

healthcare

Point of care /

fast results

Food / drug /

environmental

concerns

Sub-trends Mega-trends

High flow

proportional

valves

Laminated

manifold

technology

Chromatography

multiport valves

Configurable

syringe pump

technology

Inline syringe

pumps

Electronic

pressure & flow

control

Gas & liquid

detectors

IMI opportunity

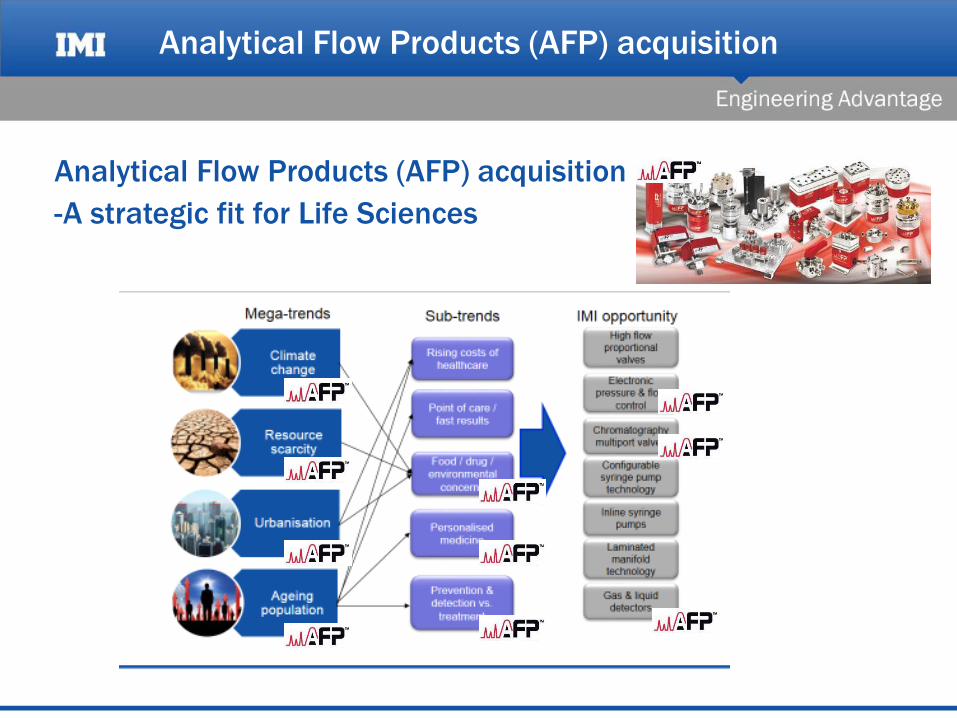

Analytical Flow Products (AFP) acquisition

Analytical Flow Products (AFP) acquisition

-A strategic fit for Life Sciences

Life Sciences technology roadmap

High flow

proportional valve

Miniature inline

syringe / piston

pumps

Miniature media

separated valves

Launched Year 1 Year 2 Year 3 +

Nanoliter (nl)

dispense/dosing

technologies

Electronic

pressure & flow

Controllers

Chromatography

multiport valves &

fittings

Analytical

gas/liquid

detectors

Analytical

proportional

valves

Configurable

syringe pump

technology

DC & closed-

looped intelligent

pumps

Laminated

manifold

technology

Micro 6mm

solenoid valves

Analytical technologies’ impact on healthcare

Analytical technologies will impact the future of healthcare

• Drug discovery

• Pre-Symptomatic diagnostics

• Personalised therapy

• Pharmacogenomics

• Personalised medicine

Norgren opportunity

• Genomics-Microarray equipment

• Genomics-DNA amplification equipment

• Genomics-DNA sequencing equipment

• Chromatography

• Mass spectrometry

• Automated sample preparation

Life Sciences technology roadmap

High flow

proportional valve

Miniature inline

syringe / piston

pumps

Miniature media

separated valves

Launched Year 1 Year 2 Year 3 +

Nanoliter (nl)

dispense/dosing

technologies

Electronic

pressure & flow

Controllers

Chromatography

multiport valves &

fittings

Analytical

gas/liquid

detectors

Analytical

proportional

valves

Configurable

syringe pump

technology

DC & closed-

looped intelligent

pumps

Laminated

manifold

technology

Micro 6mm

solenoid valves

Analytical technologies’ impact on healthcare

Norgren LMT for Genomic OEMs

Laminated Manifold Technology

(LMT) enables Genomic OEMs

the ability to accurately move

small samples and multiple

reagents at high speeds.

Benefits

• Ability to create complex fluid paths reduces

overall footprint/size

• Fewer leak paths increase reliability

• Fully assembled/tested sub assembly from

a single supplier mitigates OEM’s risk

Genomics /

Microarray

Ageing population

Laminated

Manifold

Technology

Life Sciences technology roadmap

High flow

proportional valve

Miniature inline

syringe / piston

pumps

Miniature media

separated valves

Launched Year 1 Year 2 Year 3 +

Nanoliter (nl)

dispense/dosing

technologies

Electronic

pressure & flow

Controllers

Chromatography

multiport valves &

fittings

Analytical

gas/liquid

detectors

Analytical

proportional

valves

Configurable

syringe pump

technology

DC & closed-

looped intelligent

pumps

Laminated

manifold

technology

Micro 6mm

solenoid valves

Analytical technologies’ impact on healthcare

Norgren FAS solenoid valve technology for Genomic OEMs

Miniature Media Separated Solenoid

Valves. FAS solenoid valves help the

OEM reduce the overall footprint of their

instrument, use less reagents, and

improve the reliability and repeatability of

their analysis.

Benefits:

• Cartridge & manifold-mount valve designs

reduces the overall footprint

• Low power consumption reduces heat so

the components can be mounted close

together

• Highly repeatable valve performance is

required to control low flow liquids & gasses

Genomics /

Microarray

Ageing population

Miniature media

separated

valves

Case study – single cell genomics

Customer: » Leading single cell genomics manufacturer Trend: » Prevention vs. treatment, personalised medicine Opportunity: » Precision fluidic assembly for single cell genomics Competition: » SMC, Burkert, Idex Solution: » Multi-module pneumatic assembly to include multi-

layered manifold, ultra high accuracy electronic pressure controls, valves, actuators & FRLs

Advantage: » Core competency of delivering integrated and tested

solutions with pneumatic, design, engineering expertise

Key: » Product mix/speed of integration/co-collaborate on

solution/international product/KAM support

Genomics /

Microarray

Ageing population

Laminated

Manifold

Technology

Miniature Media

Separated

Valves

Case study – digital Polymerase Chain Reaction

Customer: » Leading digital Polymerase Chain Reaction manufacturer Trend: » Prevention vs. treatment, personalised medicine Opportunity: » Air-over liquid Multilayered manifold for Digital

Polymerase Chain Reaction (dPCR) Competition: » Parker, LEE, SMC Solution: » 5-layer acrylic manifold with 11-FAS Chipsol valves, 1

FAS MS valve, 1 FAS Flatprop and an array of sensors Advantage: » Core competency of delivering integrated and tested

solutions with precision valves and layered plastic manifolds

Key: » Large percentage of the bill of material, manifold

capabilities, assembly and testing capabilities

Genomics /

Microarray

Ageing population

Laminated

Manifold

Technology

Miniature Media

Separated

Valves

Summary

• The mega & sub-trends are driving growth in Life Sciences

of 4 - 6%

• Niche leadership in Life Sciences is captured through

• Providing application-specific solutions for the most

critical precision fluidic applications in medical,

analytical, and diagnostic markets

• Delivered by developing technology

• For precisely filtering, regulating, sensing, pumping

and controlling gasses and fluids

Life Sciences opportunity

Smart Buildings

Stefan Seitz

VP Business Development, TA Hydronics

Niche Leadership – Indoor Climate

European Balancing c.£170m

IMI Share % <10 10-20 20-30 >30

Market Position 1

Key Competitors Danfoss, Oventrop,

Key Customers

Ahlsell, Arup, Cordes &

Graefe, GDF Suez, Saint

Gobain, Skanska

GLOBAL CAGR 2012-2017

Industry growth Source: Comparable Heating &

Cooling Equipment,

Freedonia World HVAC

Equipment Study

2 – 4%

Niche growth 4 – 5%

Incremental

revenue growth

opportunities

5 – 6%

Hydronics

Hydronic Balancing, Hydronic Conditioning & Thermostatic Control

• Critical to the overall performance and energy consumption of HVAC system

• We are unique in our combined offer

Source: IMI estimates

Building’s evolution

Building

envelope

Building

controls

Building

performance

Smarter Building,

Eco-District

1st/2nd oil crisis, 1st Gulf War:

•Investment in Insulation

•Investment in nuclear Power Plants

1980 1990 2000 2010 2020

2nd Gulf War:

•Improvement of component efficiencies

•Efficient system management with BMS

End of Asia crisis => strong econ. growth

•Improvement of system efficiencies with integrated components

•Performance based Facility management

•Performance contracting

•Life cycle costs

“final” Oil crisis???

•Sustainable buildings and eco-cities

•De-central, regenerative energy generation

•“Plus” energy, 0 CO2 emission buildings

• all E-supply, E-storage, E-distribution and dissipation systems communicate via “smart grid”

Ageing population

Urbanisation

Climate change

Resource scarcity

Mega-trends – driving growth in Hydronics

From eco-efficient

buildings to eco-

districts

Flexible Buildings

District Energy to

grow 25%+

Comfort &

productivity

Focus shift to

“greening” existing

buildings

Emerging Markets

North America

HVAC System

communication

De-centralised

apartment sub-

systems

Hydronic conditioning

Measurement &

Diagnostics

Mega-trends IMI opportunity Sub-trends

“Smart Grids”

”Smart Buildings”

Flexibility in home

energy usage

(matching lifestyle)

Water Quality &

Saving

Home Automation

Potable Water

Pre Fab Systems

Speedier & easier

system install

“Fit & Forget” products

Indoor Climate technology roadmap

TA FUS1ON

Balancing &

Control Valve

range

Launched Year 1 Year 2 Year 3 +

District Energy

Portfolio

Next Generation

Braincube for

Pressurisation

(water quality)

USA Potable

Water Valve

Next Gen Air &

Dirt Separator

(Water Quality)

EcoEfficient De-

Gassing Unit

(water quality)

Equalizer Control

Valve (USA)

Terminal Unit

Balancing &

Control Valve

(heating &

cooling/emerging)

Potable Water

Portfolio

Water Quality

Portfolio

Home Automation

Next Generation

Thermostatic

Radiator Valve

Smart Valve &

Actuator

Apartment

prefab stations

(Heating &

Cooling)

TA SCOPE

upgrade

(measuring

device) Terminal Unit valve for

Emerging markets

“Fit & Forget”

TRV with Flow

Control

At the heart of what we do

When comparing a non balanced with a balanced system,

electrical pumping and energy costs can be significantly

reduced whilst enhancing comfort:

Indoor Climate projects proven energy savings:

• Hammarplast Consumer factory, Sweden (61%)

• Tianjin Saixiang Hotel, China (31%)

• Pfizer, France (31%)

• Citate Administrativa, Brazil (21%)

Energy Insights

At the heart of what we do

• In heating systems, the room temperature being

1°C too high costs 6% to 11% of the annual plant

energy consumption

• ICG Renovation Project: MOL, Hungary (27%

Energy saving)

• In cooling systems, the room temperature being

1°C too low costs 12% to 18% of the annual

cooling plant energy consumption

Energy Insights

Driving energy efficiency in buildings

• Small things can make a BIG difference

The use of accurate thermostatic radiator valves can provide energy savings of up to 28% compared to the use of

manual valves*

• Consideration of a single Thermostatic control valve (vs manual valve)

• Saving on consumption – oil (gas) 70 litres (m³) /yr

• Cost reduction 53 EUR /yr

• Payback 1 year

• CO2 reduction 168 kg /yr

(*) Source: University of Dresden Independent Study

Driving energy efficiency in buildings

• There are an estimated 600 million manual valves still used in Europe today.

• Example Europe: converting all manual to thermostatic control valves • Saving on consumption – oil (gas) 42 billion litres (m³) /yr

• Cost reduction 32 billion EUR /yr

• Payback 1 year

• CO2 reduction 100 million tons /yr

• This is an equivalent of 50 million cars with an annual mileage of 15,000 km with CO2 emissions in average of 133 g/km.

Winning in the Niche

• Occupancy from Sept 2013 (multi phase development)

• 6000 employees

• 7 buildings (inc a 22 storey tower)

• £1m opportunity for ICG

• Energy saving target of 30%

• LEED accreditation sought

• Proven results

BBVA HQ

Summary

• The Mega Trends are driving growth in Hydronics with the sub

trends creating specific opportunities

• Niche leadership in Hydronics is captured through

• Translating trends into customer value

• Global infrastructure

• Our Technology development delivers:

• Energy efficiency

• Comfort & reliability

• Building value

Hydronics Opportunity

Beverage Dispense

Restaurant of the Future

Mike Coombes

Commercial Director, North West Europe

IMI Cornelius

Niche leadership – Beverage

The Niche:

Foodservice operators are investing in new BEVERAGE dispensers that

will drive both incremental sales through variety; better for you choices

and increase profitability from store efficiencies

Niche V,E, H&W Opp Eff

Growth CAGR 2012-2017

Industry growth

1 - 3%

Niche growth 5 - 7% 9-11%

Incremental revenue growth opportunities

1 - 3% 4-6%

Niche V,E, H&W Op Eff

Niche Size c.£130m c.£40m

IMI Share % <10 10-20 20-30 >30

Market

Position 1

Key

Competitors Manitowoc, Lancer, Bunn

Key

Customers

McDonalds, YUM!,

Starbucks, Subway,

Coca-Cola, Pepsi,

Brita Vivreau, Grohe Source: IMI estimates

Ageing

population

Urbanisation

Climate change

Resource scarcity

Sub-trends

Life style Variety & Choices

Right sized Equipment

Energy Efficiency

Labour Savings

Wage increases

expected in emerging

markets by end of 2013

10.5%

$1,500 Annual cost of one square foot

of retail real estate in major

urban markets

$2bn Annual Energy bill for

McDonald's Restaurants globally

170,000 Ways to create the perfect

Starbucks drink

Impact Mega-trends

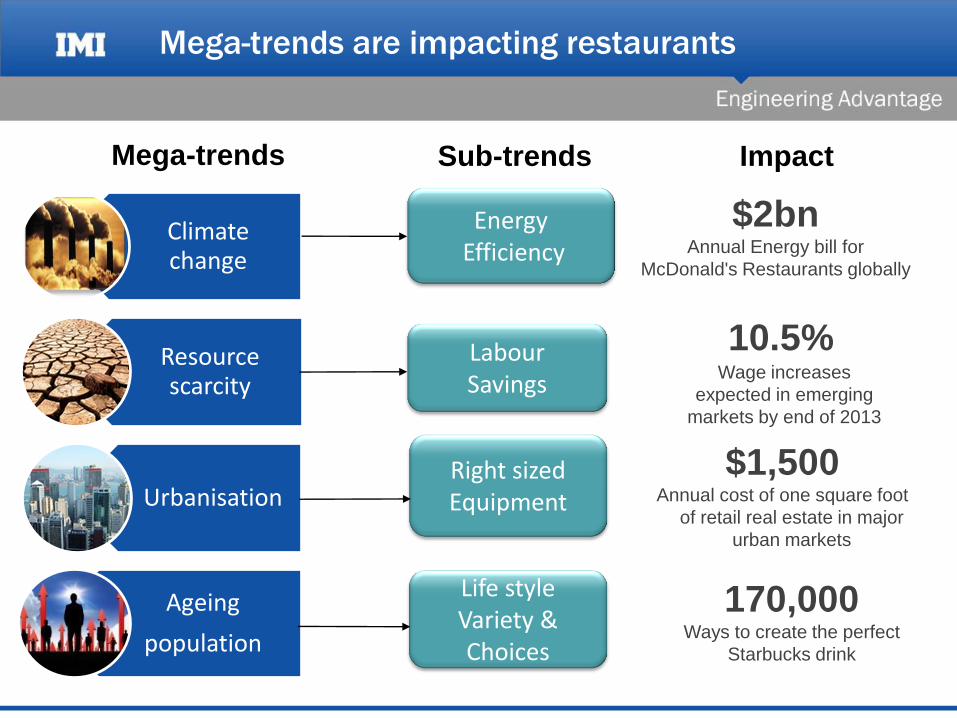

Mega-trends are impacting restaurants

Global restaurant market

Global restaurant industry will generate

$1.8 trillion revenue by end of 2015

Source: Euromonitor International

‒ Fast-food sector $240b in 2014, a 19% increase during

last 5 years

‒ QSR’s represent largest segment, with 71% of global

market value

‒ Competing for consumer footfall and up selling

opportunities

‒ QSR’s are creating a ‘destination’ for beverage

‒ McDonald’s beverage sales 22% of revenue

‒ Beverage represents a significant revenue and profit

opportunity

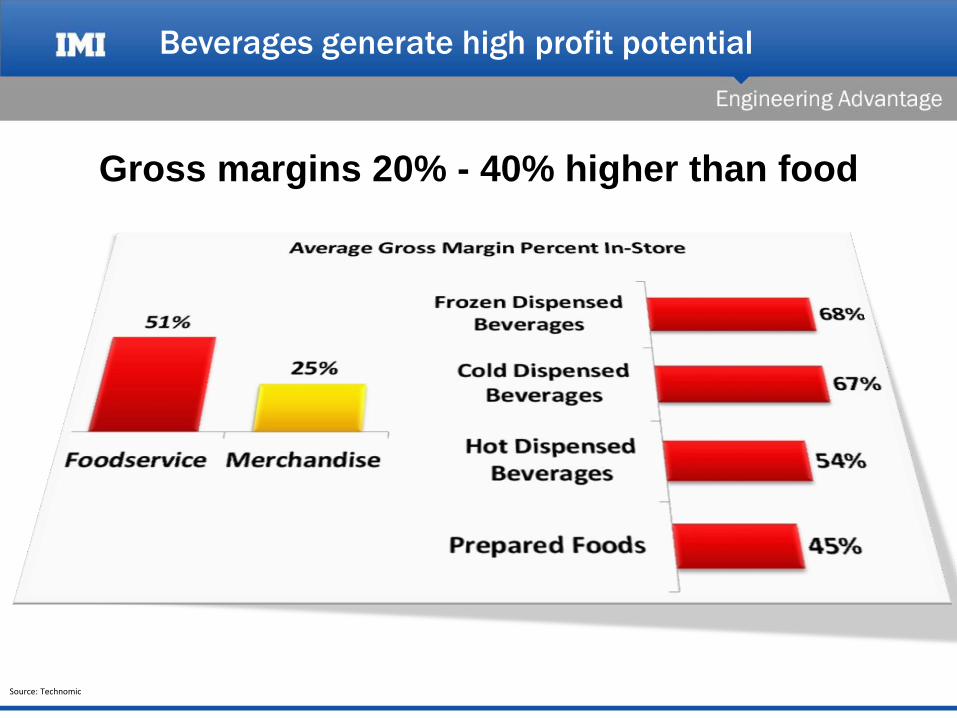

Beverages generate high profit potential

Source: Technomic

Gross margins 20% - 40% higher than food

Source: Euromonitor International

Beverages are central to

successful strategy

Beverages drive consumer

traffic throughout the day

Specialty beverages provide

incremental day part

opportunities

Variety above all

Refreshing over sweet driven by

healthier beverage choices

Tea is the next wave

hot and cold

0

50

100

150

200

250

300

350

400

450

500

Bre

akfa

st

Mo

rnin

g S

na

ck

Lun

ch

Afte

rnoo

n S

nack

Din

ner

Even

ing

Late

Nig

ht S

na

ck

Beverage day part growth opportunity

Global foodservice market trends for Beverage

Opportunities for IMI to grow in the Beverage niche

Mega-trends IMI opportunities Sub-trends

HFC-free gases

Health & Wellness

Miniaturisation

Emerging Markets

Fit for purpose

Automation

Social Media

Hot & cold combinations

Indulgence

Frozen

Variety

Fresh

Hand-crafted

Life style Variety &

Choice

Right sized Equipment

Energy Efficiency

Labour Savings

Ageing population

Urbanisation

Climate change

Resource scarcity

HFC free gases

Health & Wellness

Miniaturization

Emerging Markets

Fit for purpose

Automation

Social Media

Hot & cold combinations

Indulgence

Frozen

Variety

Fresh

Hand-crafted

Carbonating Variable

Carbonating In-Line

Merchandising LED

Merchandising Touch Screen

Cooling HFC-free

Cooling Remote Cooling Cooling

Rack Refrigeration

Valves Multi-flavor Valves

Valves Self Cleaning

Valves Miniature

Valves Microdosing

Merchandising Modular

Launched Year 1 Year 2 Year 3 +

Carbonating Batch Carbonation

Driving IMI’s beverage technology development

IMI opportunities Technology roadmap

Blending Ice Drink Blending

Creating new product development opportunities

Product roadmap

Launched Year 1 Year 2 Year 3 +

Blend in Cup smoothie dispenser

Batch Carbonator for organic sodas

Coffee Dispensers

High Density Tower Dispenser

Automated Beverage System Residential carbonated

water dispenser

Range of energy efficient beverage HFC

free coolers

Fountain Touch Screen

Digital Display Towers

Hot/Cold Tea Dispensers

Emerging Markets all in one Systems

Enhanced Water Dispensing

Multiple Beverage Fountain Dispense

Station

Self Serve Towers – Consumer Engagement

Key projects

Opportunity | A fully automated blend-in-cup blended ice drinks system for QSR

Technology Result Sub Trends to Customer Value

Rat io & b lending

t echno logy

Opt im ized va lves , pumps

and ac tua to rs f o r d i spense

accuracy

Rea l t ime, PC Con t ro l

sys tem

HFC- f ree re f r igera t ion

Clean- in -p lace [C IP ]

Helix blended ice drinks system

Right-sized equipment

~10% sma l le r i n f oo tp r in t

~50% more i ce capac i t y

Energy saving

~15% less energy consumpt ion ~20% reduct ion in p roduct was te ~50% reduct ion in r i nse wa te r

Labor savings

Crew touch sc reen ope ra t ion Speed o f se rv i ce – 3 d r inks pe r m inu te Clean- in -P lace sys tem f o r i ce maker

Life-style choice

Up to 14 con f igurab le i ced f ru i t & yogu r t smooth ies and f rappe ’s

Operator Value

Sign i f i cant p ro f i t oppor tun i t y – l ess than 1 yea r payback

Right-sized equipment

Dr ive th ru and f ron t coun te r

I nc reased b rand cho ice

Labor savings

I n tegra t ion wi th POS sys tem

6sec p rocess pe r d r ink

12 d r inks a t any one t ime

Labor sav ing o f $15 ,000 p rov ides po ten t ia l one yea r pay back

Operator Value

Sa les Up l i f t – f ewer ‘d r i ve o f f s ’

I nc reased va r ie ty and cho ice

Technology Result

Automated Cup F i l l

Pat te rn Recogn i t ion & Vis ion Sys tem

Sp lash P roo f S ink Des ign wi th mo t ion /Ac tuat ion mechan isms and p ro tec t ion

Automated Beverage System (ABS)

Sub Trends to Customer Value

Opportunity |Next generation fully automated beverage delivery system that can specifically for drive through QSR’s... in US markets drive through sales account for up to 70% of revenue

Right-sized equipment

Com pac t and l i g h t -we igh t

Eq u ipment des ig n c om p l imen ta ry t o c us t omer ope r a t i ng env i r onmen t

Labor savings

Con t ro l l ed ba t c h c a r bona t i on one d r i nk a t a t im e – c us t om ised

Easy access and c l ean

Life Style Choices

Un iq ue Beve r age m enu w i t h ab i l i t y t o c us tom ize t o c ons umer c ho i c e

T hea t re o f d i s pens e t o add c ons umer eng agement

Operator Value

Cr ea tes h i g he r va lue & h ig he r p r i c e po in t s

S ig n i f i c an t p r o f i t oppo r tun i t y – l e s s t han 1 yea r paybac k

Opportunity | To enable an operator to uniquely hand-craft and batch carbonate a variety of soda’s on a

compact footprint

Technology Result

Batch Carbonat ion

Paten ted ag i ta t ion

ca rbonat ion

techno logy

Ant i - f oaming

s i l i cone sea l /gaske t

des ign

Fas t p rocess ing

cyc les

– Ba t c h c a r bona ted

w i t h i n 36s ec s

Batch carbonator for hand-crafted sodas

Sub Trends to Customer Value

Summary

• The mega trends are driving growth in Beverage Dispense of

5% - 7%

• Sub trends creating specific growth opportunities with global

chains as well as with beverage brand owners.

• Niche leadership in Beverage Dispense is captured through

• Customer intimacy with beverage brand owners & key retailers

• Market leading position & extensive knowledge base

• Global and local presence support network

• Technology development includes

• Energy efficient equipment – HFC free

• Next generation valve technology – multi flavour

• Dispense solutions to enable beverage menu extension

Beverage Opportunity

Summary and

Conclusions

Martin Lamb

Driving sweetspot convergence

Disposal of Merchandising

2013 H1 sweetspot

Illustrative 2017 sweetspot

Supported by favourable mega-trends and

strong emerging markets growth

EM sales to increase from 24% to 35%

M&A • Strengthening of existing positions • Adoption of new adjacencies

60%

+3%

+4%

+4%

+4%

75%

Higher underlying market growth

sweetspot niches

Growth and market share gains

from new product development

Directed by technology roadmaps Supported by strong balance sheet On track

Directed by detailed technology roadmaps Supported by accelerated investment in new product development % NPD sales less than 3 years old to increase from 15% to 20%

Organic revenue growth 2 x GDP

Operating margins 20%

Post tax ROIC 20%

Key messages

• Mega-trends will have a profound impact on our

customers and end markets

• Prime position to benefit based on market

positioning and technologies

• Technology roadmaps in place

…… and brimming!

• Pathway to higher returns clear cut

……execution is key

Questions and Answers

Executive Directors

Top Related