Languages

Pages

Legal

Financing Agriculture in Turkey Conference

Istanbul, Turkey

18 April, 2012

Calvin Miller

Agribusiness and Finance Group Leader

FAO, Rome, Italy

Opportunities for Financing the Agricultural Sector in

Turkey

An Evolving Agriculture

�Market integration

� Tighter supply and value chains

� Increased concentration of power of market leaders

�Open trade with intense regional and global competition

�Consumer changes

�More food processing and segmented demand

� Stringent standards, specifications and conditions

� Information and communication technology (ICT)

� access to information is easier and more important

� back-office technologies are more robust to manage data

The new context for Agriculture

Expanding high-rent markets in agriculture represent an

enormous opportunity to foster poverty reduction

Note: agro-processed goods represent an expanding market in agriculture worldwide.

Source: http://faostat.fao.org and http://comtrade.org

3

The Concept of AVCF

Where do farmers and agro-processors turn when banks or

other financial institutions are unable or unwilling to

provide them with financial services?

Exporters / Wholesalers

Processors

Local Traders & Processors

Producer Groups

Farmers

Input Suppliers

Banks

Non-bank

Financial Institutions

Private Investors

& Funds

Cooperatives /

Associations

Local MFIs /

Community Orgs

Financial Service

InstitutionsValue Chain Actors

Product Flows

Financial Flows

Technical Training

Support

Services

Business Training

Specialized

Services

Governmental

Certification/Grades

Product and Financial Flows along a VC

Financing comfort zone

Spot

market Contract

Relationship

based partnership

Capital investment

based partnershipVertical

integration

Buyer

Seller

Value Chain Relationship Structures

VC Relationships Enhance Finance

Value Chain Business Models

Business models in agriculture value chains in terms of small holders can be divided into four types:

�Producer-driven

�Buyer-driven

�Facilitator-driven

� Integrated

Financial services and the approach to their delivery

ought to be related to the VC business model?

Defining Value Chain Finance

Value chain finance – financial products and services flowing to and/or through a VC to address the needs of those involved in that chain, be it a need for finance, a need to secure sales, procure products, reduce risk and/or improve efficiency within the chain.

Objectives:

�Align and structure financial products to fit the chain

�Reduce costs and risks of finance

Approach: Why is Ag VCF Important?

1. It allows sellers of inputs to increase sales

2. It facilitates produce buyers to get what they want when they want it (quantity, quality, timing, & price of goods)

3. Financial institutions can learn from and engage more with value chain actors in order to develop new products and reach new markets

4. The Value Chain approach as a comprehensive approach to lending is useful for improving and expanding financial services, not just for enterprise development

If designed well, value chain finance interventions can increaseIf designed well, value chain finance interventions can increaseIf designed well, value chain finance interventions can increaseIf designed well, value chain finance interventions can increasethe competitiveness of small producers, as well as a range of the competitiveness of small producers, as well as a range of the competitiveness of small producers, as well as a range of the competitiveness of small producers, as well as a range of agricultural and agribusiness enterprises.agricultural and agribusiness enterprises.agricultural and agribusiness enterprises.agricultural and agribusiness enterprises.

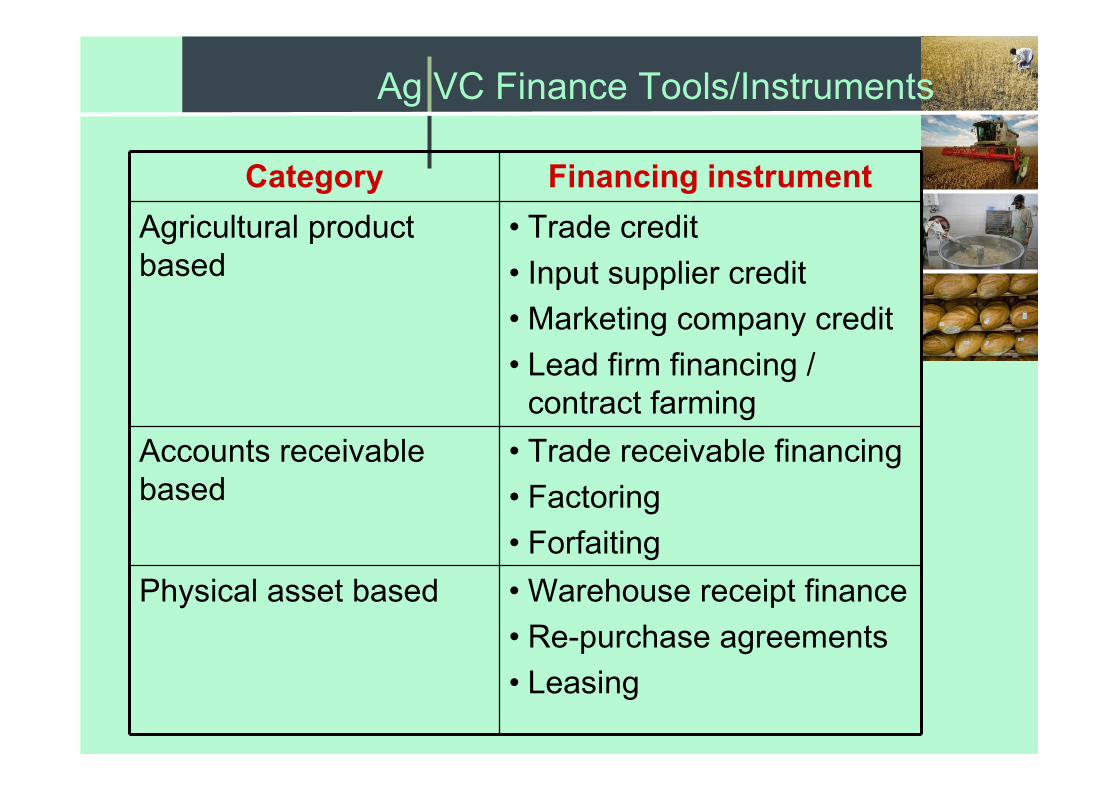

Category Financing instrument

Agricultural product based

• Trade credit

• Input supplier credit

• Marketing company credit

• Lead firm financing / contract farming

Accounts receivable based

• Trade receivable financing

• Factoring

• Forfaiting

Physical asset based • Warehouse receipt finance

• Re-purchase agreements

• Leasing

Ag VC Finance Tools/Instruments

11

Type of product Financial instrument

Risk mitigation • Insurance

• Forward contracts

• Futures

Financial enhancements • Securitization

• Loan Guarantees

• Joint ventures

The instruments of agricultural value chain financing

channels are many and can be used in conjunction with

one another.

Ag VC Finance Tools/Instruments

Purchase Order Model - “Palmito” VC

Sale of Product

Loan repayment

K + i

Fund transfer agreement

IndividualCredit

$US 2.000

FABOPAL / INDATROP /BOLHISPANIA

Importer

Buyer Order(Contract)

Producer

ProcessorsProcessors

FIE Bank

12

43

5

6

7

Local merchant

Micro-credit

Lead Firm Contract Financing

Integrated Ag VCF Model

LAFISE

Trade

Network of offices in 10 countries

Identify marketsAnd buyers

Place Products

5

Collection and

payment to producer

6

Identify organizedproducers

1

Technical AssistanceQuality Certification

Productor

cosecha

3

Insurance - transport,life, fire, etc.

Financing:

* Asset management.* Warehouse receipts

2

4

Consolidation Processing

Added ValueProduct in

storage

Certification of Deposit and Warrants

Islamic FinanceIslamic Finance

Agriculture value chain finance conforms to and has many Agriculture value chain finance conforms to and has many Agriculture value chain finance conforms to and has many Agriculture value chain finance conforms to and has many

similarities to Islamic finance tools in that risk sharing and similarities to Islamic finance tools in that risk sharing and similarities to Islamic finance tools in that risk sharing and similarities to Islamic finance tools in that risk sharing and

mutual interest is part of the business modelmutual interest is part of the business modelmutual interest is part of the business modelmutual interest is part of the business model....

VC FinanceVC Finance

Al Murabaha (Markup Sale)

Selling Price = Cost + Profit (Both costs and profits have to be fixed and declared)

Product Finance (Provided the bank’s profit is fixed before hand)

Bie Al-Salam (Advance Contracting)

Price is paid upfront whereas the delivery is differed.

Contract Farming (Provided the bank allows for reconsideration of price in case of significant rise of market price)

Al – Musharakah (Partnership)A contract between two parties where in the profits are shared

Financial Lease ( Provided both the parties split profits in agreed proportion until the borrower buys back the bank share)

Al – Mudarabah (Speculation)

Partnership between provider of capital (Bank) and provider of experience and labor(Farmer)

Joint venture/Partnership

(Provided the bank’s finance is not considered as debt owed by the farmer)

Ag VCA and Islamic Finance

Producing Storing

Production

Price

Operational

Financing

Institutional

Infrastructure

Quality control

Technology

Logistics

Seasonal glut

Processing Marketing

Infrastructure

Storage

Price

Product loss

Govt. policy

Technology

Product supply

Human resource

Product quality

Govt. policy

Input

Supply

Quality

Availability

Infrastructure

Knowledge

Financing

Addressing Risks along the VC

From supplyFrom supplyFrom supplyFrom supply----driven driven driven driven ““““how we lendhow we lendhow we lendhow we lend”””” to to to to

client driven client driven client driven client driven ““““how can we structure finance how can we structure finance how can we structure finance how can we structure finance

to address client needs and risksto address client needs and risksto address client needs and risksto address client needs and risks””””

Customized Products to VC Stakeholders

Contract Seed Growers

Dealer

Seed Company

Distributor

Farmer

Contractual agreement

Credit sales

Preferred distributors

Lending against offtake contract

SEEDS

Lending against stop sales agreement

Term lending/ WC

Short term lending against liquid collateral

Crop loans

Credit

Credit/ forward contract

Farmer

Wholesaler

Village level CA

Mandi/ Warehouse

Miller

Warehouse Receipt

Warehouse Receipt

Spot market price

EDIBLE OIL

Vendor bill discounting

WR finance

Crop loan

Agri-trade, finance & risk management ecosystem

Ruttan 2010

Risk Management

in agriculture

value chain

Agri-business segmentation

Social vs. commercial insurance

Traditional farming sector

Emerging farming sector

Commercial farming sector

Agricultural risk assessment

Risk identification

Risk quantification

Probabilistic agricultural risk model

Agricultural risk financing

Risk layering

Insurance index

Insurance pool

Insurance and rural finance

Institutional capacity building

Data management

Regulatory/supervisory framework

Information and education

Technical expertise

Programme administration and

monitoring

Agricultural risk management

Why an Agribusiness Investment Fund?E

con

om

y, M

ark

et

Co

nd

itio

ns,

Sh

ock

s

Clim

ate

Co

mp

eti

tio

n,

stra

teg

yRISK FACTORS

Space for subsidized lending &grants

Low profits, high risk, but viable esp.

with support for productivity

enhancement

raw materialsIncome +

technology or

credit supportSpace for SEAF-like investment funds

Reasonable and consistent returns

(less exposed to market factors than

other sectors), but not extremely

high returns.

Kn

ow

-ho

w

� Agribusiness fund focusing on businesses that link farmers to global buyers

can complete a farm-level development strategy for emerging markets.

Space for SEAF-like investment funds

and private sector

Opportunities for high returns, based

on business strategy and ability to

beat competition.

FARMERS, PRIMARY PRODUCERS

PROCESSORS, AGGREGATORS, EXPORTERS

LOCAL & INT’L BUYERS/RETAILERS

processed goods

VALUE CHAIN PLAYERS OPPORTUNITIES

Source: (SEAF), 2009

Diversification of agricultural investment risk

ICT applications (e.g. improved MIS systems, mobile phones,

internet price & trade information) can reduce information and

transaction costs to service rural areas.

0

10

20

30

40

50

60

70

80

Africa Asia Latin America

2003

2008

Subscriptions per 100 million persons

ICT Innovation for Improved Competitiveness

Innovative Aggregator Models for Agriculture

Farmers

Aggregator at Village and Higher

Levels

ISB (Knowledge partner)

Forward contract

Input credit

Knowledg

e

sharing

Regional Call Centres (RCC)

Bank

Fund

transfer

WR financing

NBHC

MCX

NSEL

Market players

Some risk management tools are more practical for agroSome risk management tools are more practical for agroSome risk management tools are more practical for agroSome risk management tools are more practical for agro----industries and wholesalers, industries and wholesalers, industries and wholesalers, industries and wholesalers,

but can stabilize prices and reduce risks for all producers and but can stabilize prices and reduce risks for all producers and but can stabilize prices and reduce risks for all producers and but can stabilize prices and reduce risks for all producers and bankers.bankers.bankers.bankers.

• Character

• Capacity

_______________

• Capital

• Collateral

• Conditions

• Management &

technical ability

• Human labor

• Loan terms

• Production cycle

• Markets

Good Client Analysis Remains Fundamental

Five Five Five Five ““““CCCC’’’’ssss”””” for loan analysis are still important ,with a change in emphasfor loan analysis are still important ,with a change in emphasfor loan analysis are still important ,with a change in emphasfor loan analysis are still important ,with a change in emphasisisisis

• Integrity &

responsibility

Need for Good Governmental Policies and Support

� Business capacity building and market integration

� Contract farming and out-grower schemes

� Technical capacity in market norms and standards

� Commodity exchanges and active futures markets

� Insurance innovation, data collection and initiation

� Market information and access

� Infrastructural investment

� Product and service innovation and diversity

� Technology adaptation and access

Contract Farming Contract Farming www.fao.org/ag/ags/contract-farming/en

FAOFAO

www.fao.org/ag/ags

Rural Finance Learning CentreRural Finance Learning Centrewww.ruralfinance.org

Useful Websites

Thank You

Top Related