Languages

Pages

Legal

OIL PRODUCTION IN BRAZIL: CHALLENGES AND

PROSPECTS

Prof. Edmar de AlmeidaEnergy Economics Group

Institute of Economics

Federal University of Rio de Janeiro

Roundtable hosted by

Center on Global Energy Policy

Columbia University

New York, May 18, 2015

• Brazil’s oil and gas sector

• Importance of Petrobras for national and global supply

• Petrobras’ financial crisis and corruption scandal

• Consequences for Brazilian Oil and Gas Industry

• The way out of the crisis

PLAN OF THE PRESENTATION

Brazil’s oil and gas sector

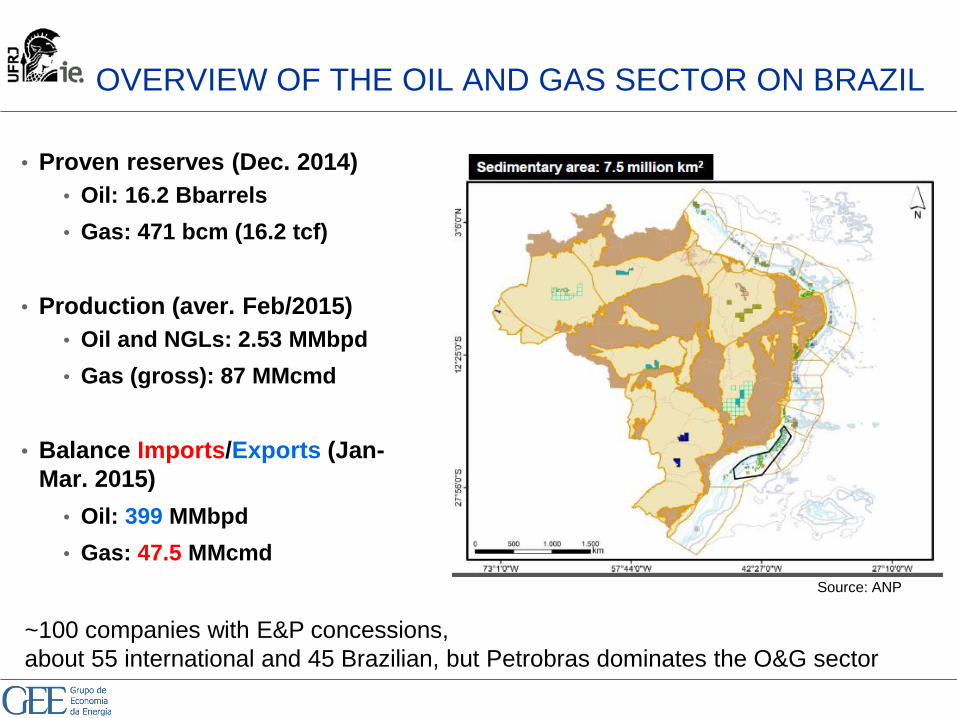

• Proven reserves (Dec. 2014)

• Oil: 16.2 Bbarrels

• Gas: 471 bcm (16.2 tcf)

• Production (aver. Feb/2015)

• Oil and NGLs: 2.53 MMbpd

• Gas (gross): 87 MMcmd

• Balance Imports/Exports (Jan-

Mar. 2015)

• Oil: 399 MMbpd

• Gas: 47.5 MMcmd

OVERVIEW OF THE OIL AND GAS SECTOR ON BRAZIL

Source: ANP

~100 companies with E&P concessions,

about 55 international and 45 Brazilian, but Petrobras dominates the O&G sector

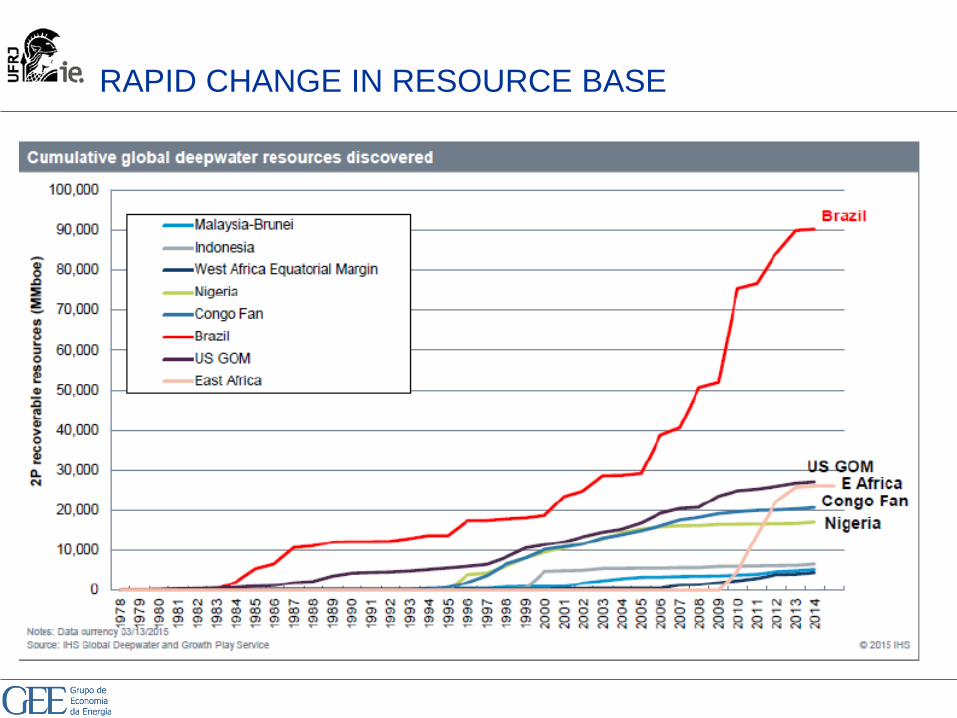

RAPID CHANGE IN RESOURCE BASE

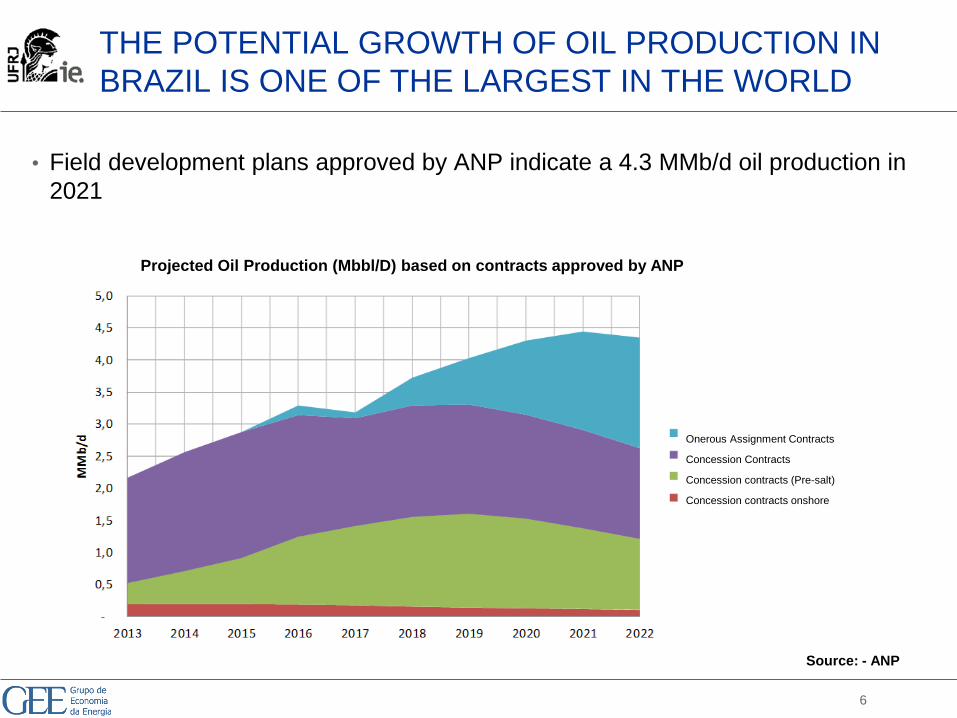

THE POTENTIAL GROWTH OF OIL PRODUCTION IN

BRAZIL IS ONE OF THE LARGEST IN THE WORLD

• Field development plans approved by ANP indicate a 4.3 MMb/d oil production in

2021

6

Onerous Assignment Contracts

Concession Contracts

Concession contracts (Pre-salt)

Concession contracts onshore

Source: - ANP

Projected Oil Production (Mbbl/D) based on contracts approved by ANP

FUTURE DEMAND AND PRODUCTION FOR BRAZIL ON

THE NEW POLICIES SCENARIO

Source: IEA

EXPECTED OIL PRODUCTION GROWTH IN BRAZIL

HAS A GLOBAL IMPACT

Source: IEA

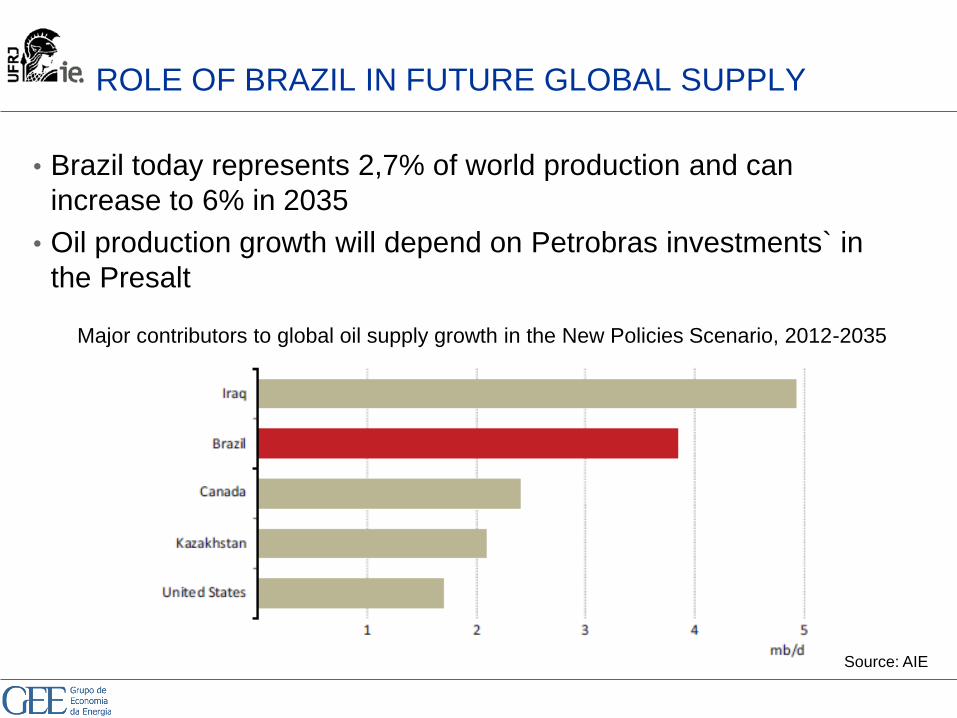

• Brazil potential increase in oil production represents 51% of the

expected demand increase until 2035

• Brazil today represents 2,7% of world production and can

increase to 6% in 2035

• Oil production growth will depend on Petrobras investments` in

the Presalt

ROLE OF BRAZIL IN FUTURE GLOBAL SUPPLY

Major contributors to global oil supply growth in the New Policies Scenario, 2012-2035

Source: AIE

RESOURCE BOUNTY NURTURED ENERGY

NATIONALISM

•New oil laws of 2010

• Petrobras as a sole operator in the Presalt

• Exclusive rights for Petrobras:• Onerous Assignment contracts (5 billion barrels +)

• Production Sharing contracts (~10 billion barrels in Presalt)

• Petrobras resource portfolio is very large as compared to its investment

capacity – need to divest?

•Five years without E&P bidding rounds have deeply

affected the industry

•Strong emphasis on local content

10

Importance of Petrobras for

national and global supply

DIVERSIFICATION OF UPSTREAM INVESTMENT

• Today there are about 100 companies, aside from Petrobras,

active in E&P in Brazil

• About 55 international companies (majors and independents)• Responsible for most of non-Petrobras investment in Brazil

• About 45 Brazilian companies• Mostly newly-created companies

• Diversity of size and business models

• Important for onshore exploration

• However, Petrobras is still responsible for about 70% of all

investments in the Brazilian upstream

12

TOTAL INVESTMENT IN BRAZIL E&P (1998-2013)

Source: Statoil

Petrobras + partners

Petrobras financial crisis and

corruption scandal

TO ACHIEVE EXPECTED PRODUCTION, PETROBRAS

MUST KEEP ITS INVEST AT HIGH LEVEL

• The investment increased by more than 4 times on 10-year time

• Reduction on 2014

Source: Petrobras.

THE COMPANY HAS LOST REVENUES BY SELLING PRODUCTS

BELOW THE INTERNATIONAL MARKET PRICE

16

Source: PETROBRAS

Average realization prices in Brazil vs. the US Gulf prices

ESTIMATED ACCUMULATED LOSS OF REVENUE BY

PETROBRAS DUE TO PRICE CONTROLS

17

Source: Own Elaboration

Estimated accumulated revenue losses by Petrobras for selling

gasoline, diesel and LPG below the international benchmark prices

IN THE LAST FOUR YEARS PETROBRAS HAD TO

RELY ON CREDIT

Debt Index for Petrobras

(Net debt / EBITDA)

• Even without this scandal scenario, Petrobras crisis would come anyway: it's

overinvestment and consequent high debt were a large problem itself

Source: Petrobras.

PETROBRAS’ DEBT IS NOW A CONCERN

•About 45% of the

debt must be

renewed by the

end of 2018

•Only 20% of the

debt is based in

domestic currency

19

Source: Petrobras

Evolution of Petrobras’ Debt

• Sales Revenue growth: 11%

• Growth in total oil and natural gas production: 5% (2,669

thousand boe/day)

• Net loss: (-) R$ 26.1 bi (US$ 7.5 bi)

• This negative result has been fuelled by different factors:

• Impairment (Refining, E&P and Petrochemical) = R$ 44.6 bi (US$

16,8)

• Write-off of overpayment incorrectly capitalized (Car Wash

Operation) = R$ 6.2 bi (US$ 2.5)

• Cancellation of projects

• Provision for losses in the electric sector

HIGHLIGHTS OF PETROBRAS 2014 RESULTS

2014 RESULTS: IMPAIRMENT TESTS

•Refining: postponement

of projects/assets

•E&P: decline in oil

prices

•Petrochemical:

Reduction in demand

and margins

Source: Petrobras.

2014 RESULTS: WRITE-OFF OF OVERPAYMENT

INCORRECTLY CAPITALIZED

•Amount of 3% over

contracts with 27

companies members of

the cartel between 2004

and 2012

•For companies outside

the cartel, specific

values mentioned in the

depositions

Source: Petrobras.

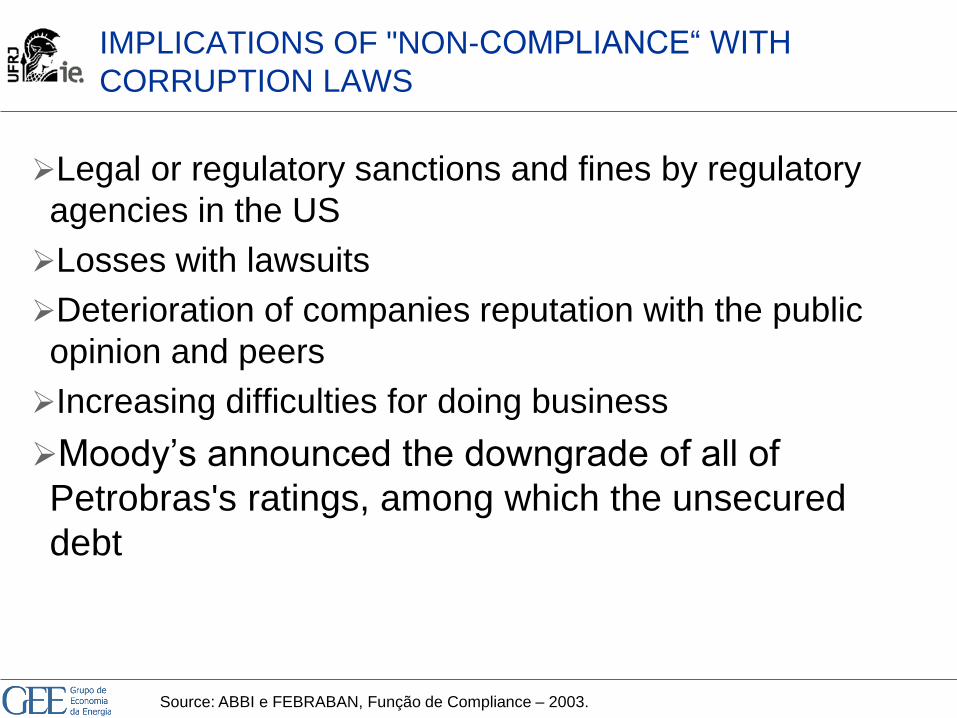

IMPLICATIONS OF "NON-COMPLIANCE“ WITH

CORRUPTION LAWS

Legal or regulatory sanctions and fines by regulatory

agencies in the US

Losses with lawsuits

Deterioration of companies reputation with the public

opinion and peers

Increasing difficulties for doing business

Moody’s announced the downgrade of all of

Petrobras's ratings, among which the unsecured

debt

Source: ABBI e FEBRABAN, Função de Compliance – 2003.

IMPORTANT IMPACT IS ON TRUST

• Petrobras had a 220 billions dollars investment plan for the next 5

years

• The company relationship with its suppliers deteriorated

• Nearly two dozen companies banned from doing business with Petrobras

• Some of these companies (Engevix, OAS, UTC and Mendes Júnior) are

responsible for the construction of the FPSO and drilling rigs for the pre-salt

projects

• The companies are companies are facing credit access difficulties, which will

delay the construction projects

• Lack of trust for doing business results in higher costs

Consequences for Brazilian Oil

and Gas Industry

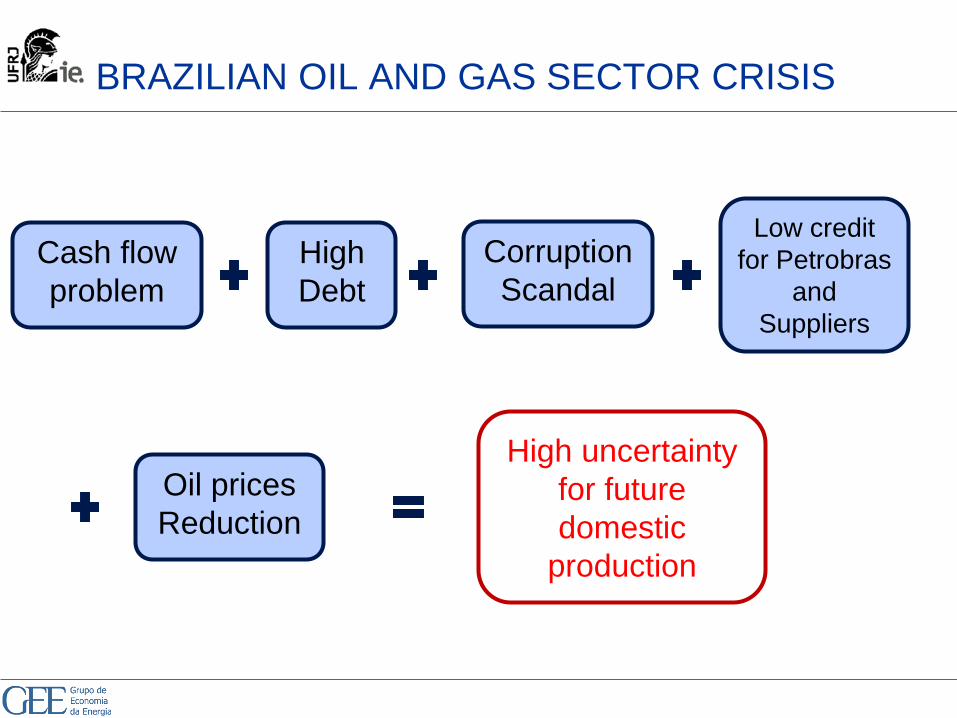

BRAZILIAN OIL AND GAS SECTOR CRISIS

Cash flow

problem

High

Debt

Corruption

Scandal

Oil prices

Reduction

Low credit

for Petrobras

and

Suppliers

High uncertainty

for future

domestic

production

LACK OF FINANCING IS AFFECTING THE ABILITY OF

BRAZILIAN INDEPENDENTS TO INVEST

27

Source: ANP

Evolution of the Number of Wells Drilled in Brazil

BRAZIL: SHARP REDUCTION IN EXPLORATORY

ACTIVITY IN THE LAST 3 YEARS

28

Source: Backer

Hughes Rig Count

Evolution of the number of Drilling Rigs in Operation in Brazil

THE SLOWDOWN IN BRAZIL WAS THE LARGEST IN THE WORLD

IN THE H1-2014; ARGENTINA IS GAINING GROUND

29

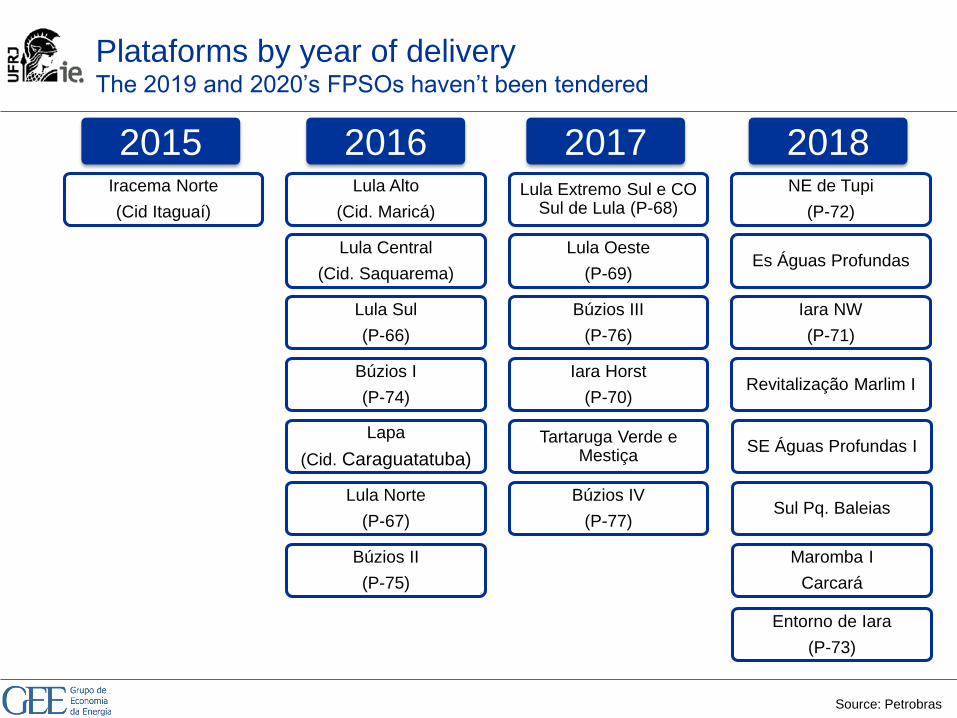

Petrobras business plan was to double production until

2020, reaching 4.2 kbpd

Source: Petrobras

Petrobras planned to construct:

• 22 new FPSOs on 2015-2020 period

• 28 rigs from Sete Brasil

Plataforms by year of deliveryThe 2019 and 2020’s FPSOs haven’t been tendered

2015Iracema Norte

(Cid Itaguaí)

2016Lula Alto

(Cid. Maricá)

Lula Central

(Cid. Saquarema)

Lula Sul

(P-66)

Búzios I

(P-74)

Lapa

(Cid. Caraguatatuba)

Lula Norte

(P-67)

Búzios II

(P-75)

2017Lula Extremo Sul e CO

Sul de Lula (P-68)

Lula Oeste

(P-69)

Búzios III

(P-76)

Iara Horst

(P-70)

Tartaruga Verde e Mestiça

Búzios IV

(P-77)

2018NE de Tupi

(P-72)

Es Águas Profundas

Iara NW

(P-71)

Revitalização Marlim I

SE Águas Profundas I

Sul Pq. Baleias

Maromba I

Carcará

Entorno de Iara

(P-73)

Source: Petrobras

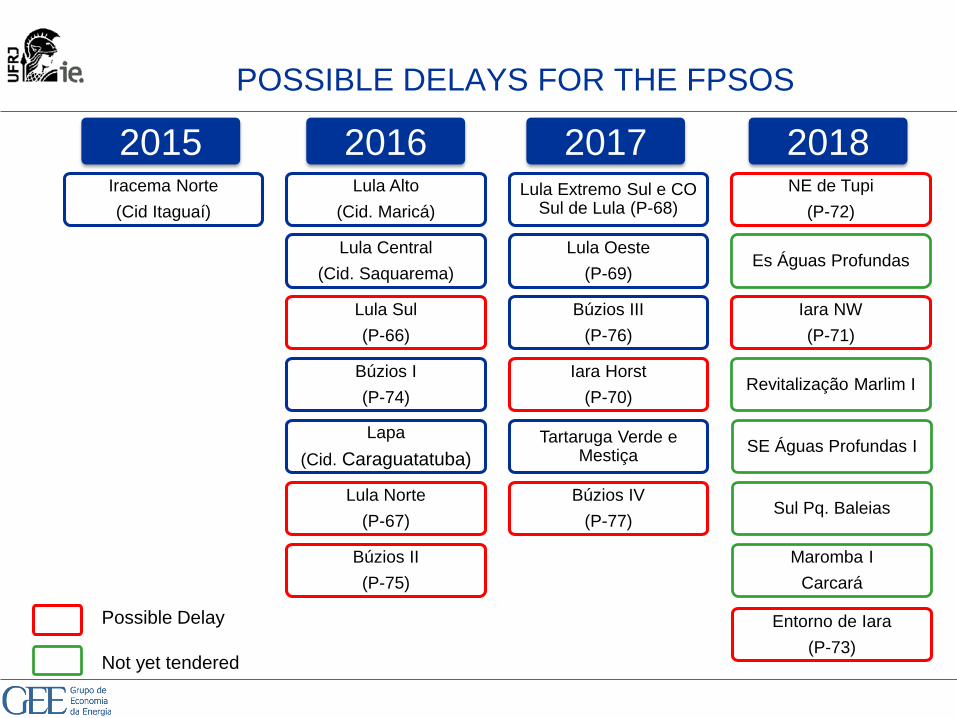

POSSIBLE DELAYS FOR THE FPSOS

2015Iracema Norte

(Cid Itaguaí)

2016Lula Alto

(Cid. Maricá)

Lula Central

(Cid. Saquarema)

Lula Sul

(P-66)

Búzios I

(P-74)

Lapa

(Cid. Caraguatatuba)

Lula Norte

(P-67)

Búzios II

(P-75)

2017Lula Extremo Sul e CO

Sul de Lula (P-68)

Lula Oeste

(P-69)

Búzios III

(P-76)

Iara Horst

(P-70)

Tartaruga Verde e Mestiça

Búzios IV

(P-77)

2018NE de Tupi

(P-72)

Es Águas Profundas

Iara NW

(P-71)

Revitalização Marlim I

SE Águas Profundas I

Sul Pq. Baleias

Maromba I

Carcará

Entorno de Iara

(P-73)

Possible Delay

Not yet tendered

The way out of the crisis

• The company is trying to improve the credibility by changing the

CEO and executives

• As a state-run company, the president choose the executives of Petrobras

• On February, the CEO and five executives resigned

• Announcement of a two-years (2015/2016) disinvestment plan

on March, 2 2015

• Divestitures total US$ 13.7 billion, and include Exploration & Production

assets in Brazil and abroad (30%), as well as assets in the Downstream

(30%) and Gas & Energy (40%) segments

• The company wants to focus on priority investments, mainly oil and gas

production in Brazil in areas of high productivity and return

HOW PETROBRAS IS TRYING TO SOLVE THE

PROBLEMS

• Oil and Natural Gas Production (Brazil and abroad): 2,886

kboed (+/- 2%)

• Divestments: US$ 10 billion

• Investments:

• Approximately US$ 25 billion (82% in E&P)

• 37% below 2016 CAPEX (US$ 39.5 billion), in the 2014-2018 Business

Plan

• New FPSOs:

• Cidade de Itaguaí (4Q15)

• Cidade de Maricá (1Q16)

• Cidade de Saquarema (2Q16)

• Cidade de Caraguatatuba (3Q16)

• Extended Well Test - Libra (4Q16)

PETROBRAS PLANNING ASSUMPTIONS FOR 2016

• The government announced on May 4th a new bidding round

this year, on October

• The 13th Bidding Round will offer 269 exploratory blocks, no

offer on the pre-salt area

• The offered areas are distributed at 10 basins: Amazonas,

Parnaíba, Potiguar (onshore), Recôncavo, Sergipe-Alagoas

(offshore), Jacuípe, Camamu Almada, Campos, Espírito Santo

(offshore) and Pelotas.

• The bidding round for the pre-salt area will probably be

postponed to 2017

THE NEW BIDDING ROUND IS A GOOD SIGN

AREAS TO BE OFFERED IN THE13TH BIDDING

ROUND

Grupo de Economia da Energia

www.gee.ie.ufrj.br

Thank you

Top Related