Languages

Pages

Legal

1

With Gibson & Eli, Bench.co

My Money Stories:

Credit Karma

Talks Finances, Credit and Debt

Meet the Speakers…

Jennifer Micieli, CFP®Marketplace Insights ManagerCredit Karma

Maria GianottiContent MarketingKabbage

Moderator

#KabbageKam

Marketplace Insights Manager

Credit Karma

Jennifer Micieli, CFP®

Agenda

#KabbageKam

/CreditKarma

@creditkarma

Ø Quick Note on Personal vs. Small Business Money Management

Ø Snapshot of Financial Health

Ø Key Markers of Credit HealthØ How’s Your Credit Health?

Ø Check Your Credit History

Ø Know Your Credit Score

Ø Recovering From Debt

Ø Credit and Debt Pro Tips

Ø Questions

Follow us on Social:

Personal vs. Small Business

Money Management

#KabbageKam

Quick Note

#KabbageKam

We have resources available regarding business credit that you can review after the webinar:

• What is a Business Credit Score?

• How to Build a Good Business Credit Score

• Business Credit Cards

• Business Loans

Focus on Personal Money Management

• We’ll be focusing on personal money

management, however many of the tips can

apply to managing the finances of your business

as well.

• Note: The Fair Credit Reporting Act (FCRA) could

allow a lender to review personal credit for

business purposes under specific circumstances.

How’s Your Financial Health?

#KabbageKam

Snapshot

#KabbageKam

Financial Health

There are many components of financial health. The following are three areas that can give a fairly comprehensive high-level summary:

• Financial Beliefs, Goals and Habits – Expectations, Motivations and Behavioral Tendencies

• Cash Flow – Income and Expenses (Ex: Credit Card Interest)

• Net Worth – Assets and Liabilities (Ex: Auto Loan)

We’ll be spending most of our time discussing expenses and liabilities, specifically regarding credit and debt.

#KabbageKam

What’s the Difference Between Credit and Debt?

When you use credit, you borrow money to pay for something now and pay it back later.

This borrowed money becomes debt, which can accrue interest on the balance you owe.

#KabbageKam

Why Do Credit and Debt Matter?

#KabbageKam

Responsible Use of Credit

and Debt

Credit Cards with Higher Rewards,

Better Interest Rates on Loans

How do you get that?

How’s Your Credit Health?

#KabbageKam

Credit Reports & Credit Scores

#KabbageKam

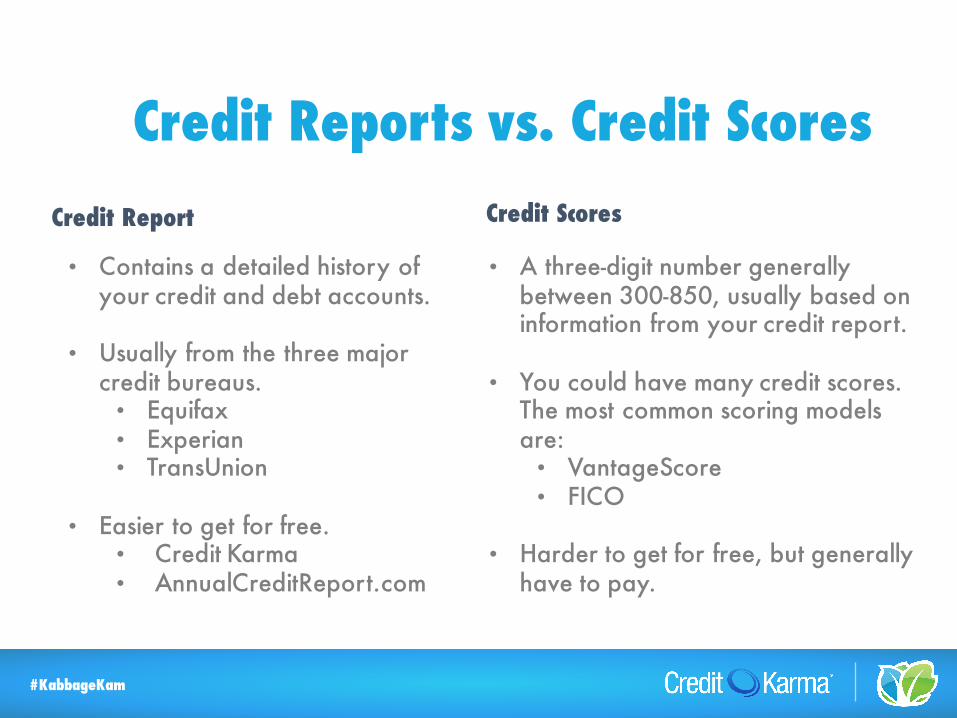

Credit Reports vs. Credit Scores

• Contains a detailed history of your credit and debt accounts.

• Usually from the three major credit bureaus.• Equifax• Experian• TransUnion

• Easier to get for free.• Credit Karma• AnnualCreditReport.com

#KabbageKam

• A three-digit number generally between 300-850, usually based on information from your credit report.

• You could have many credit scores. The most common scoring models are:• VantageScore• FICO

• Harder to get for free, but generally have to pay.

Credit Report Credit Scores

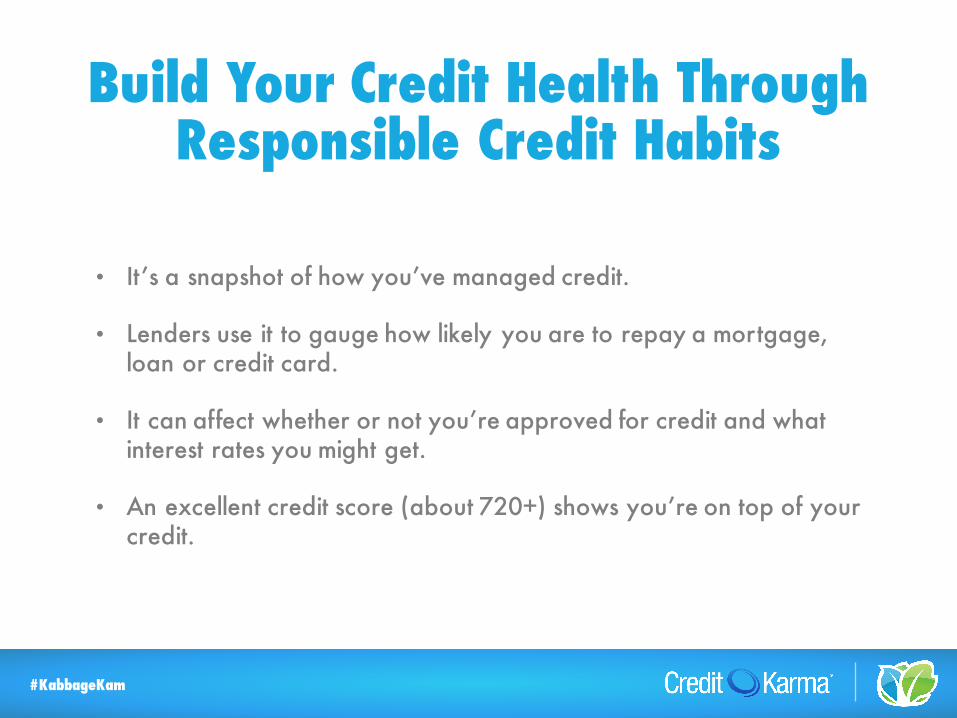

Build Your Credit Health Through Responsible Credit Habits

• It’s a snapshot of how you’ve managed credit.

• Lenders use it to gauge how likely you are to repay a mortgage, loan or credit card.

• It can affect whether or not you’re approved for credit and what interest rates you might get.

• An excellent credit score (about 720+) shows you’re on top of your credit.

#KabbageKam

Check Your Credit History

#KabbageKam

Credit Reports

#KabbageKam

My Money Story

#KabbageKam

Hear from others about their financial experiences and challenges. Visit our YouTube channel for more videos and credit tips.

#KabbageKam

#MyMoneyStory

#KabbageKam#KabbageKam

My $42 Gas Bill Went to Collections

His credit has bounced back since then.

Michael

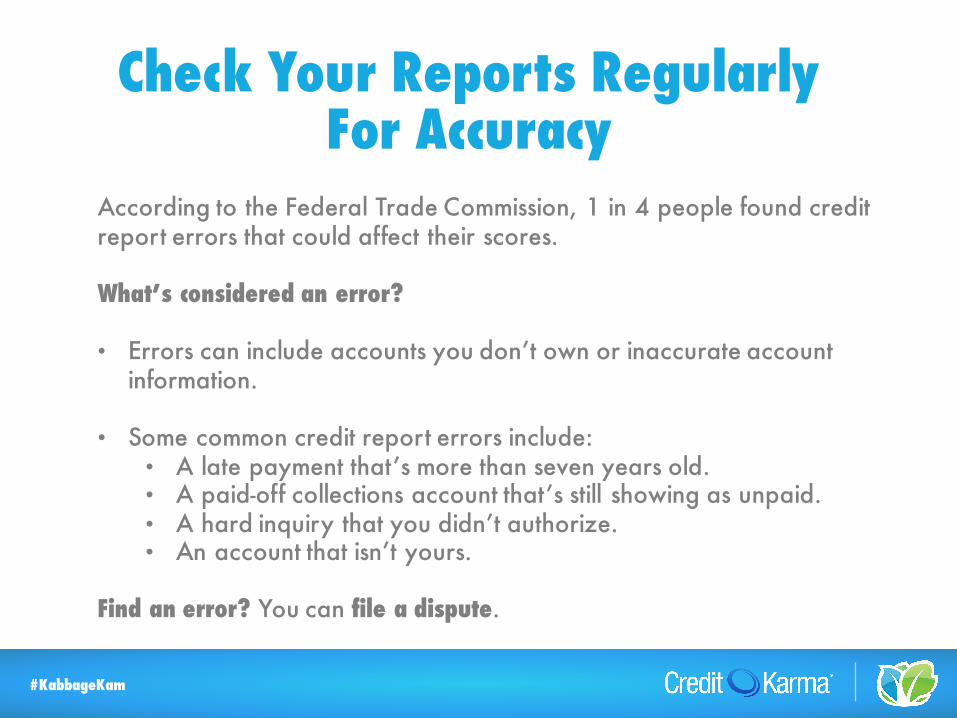

Check Your Reports Regularly For Accuracy

According to the Federal Trade Commission, 1 in 4 people found credit report errors that could affect their scores.

What’s considered an error?

• Errors can include accounts you don’t own or inaccurate account information.

• Some common credit report errors include:• A late payment that’s more than seven years old.• A paid-off collections account that’s still showing as unpaid.• A hard inquiry that you didn’t authorize.• An account that isn’t yours.

Find an error? You can file a dispute.

#KabbageKam

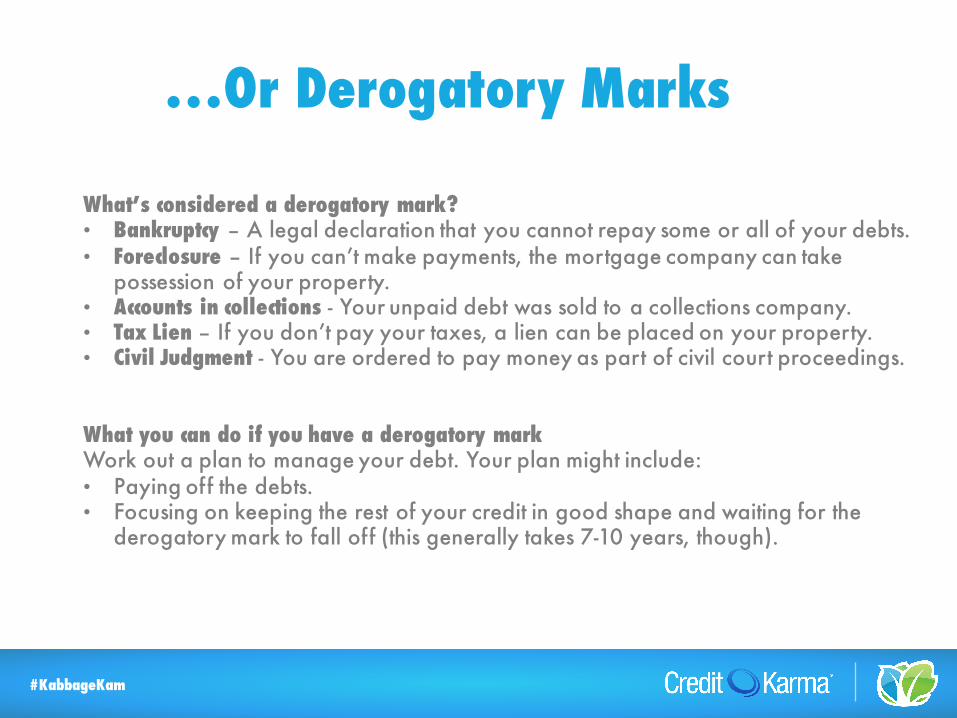

…Or Derogatory Marks

What’s considered a derogatory mark?• Bankruptcy – A legal declaration that you cannot repay some or all of your debts. • Foreclosure – If you can’t make payments, the mortgage company can take

possession of your property. • Accounts in collections - Your unpaid debt was sold to a collections company.• Tax Lien – If you don’t pay your taxes, a lien can be placed on your property. • Civil Judgment - You are ordered to pay money as part of civil court proceedings.

What you can do if you have a derogatory markWork out a plan to manage your debt. Your plan might include:• Paying off the debts.• Focusing on keeping the rest of your credit in good shape and waiting for the

derogatory mark to fall off (this generally takes 7-10 years, though).

#KabbageKam

Know Your Credit Score

#KabbageKam

A Measure of Credit Health

#KabbageKam

#MyMoneyStory

#KabbageKam#KabbageKam

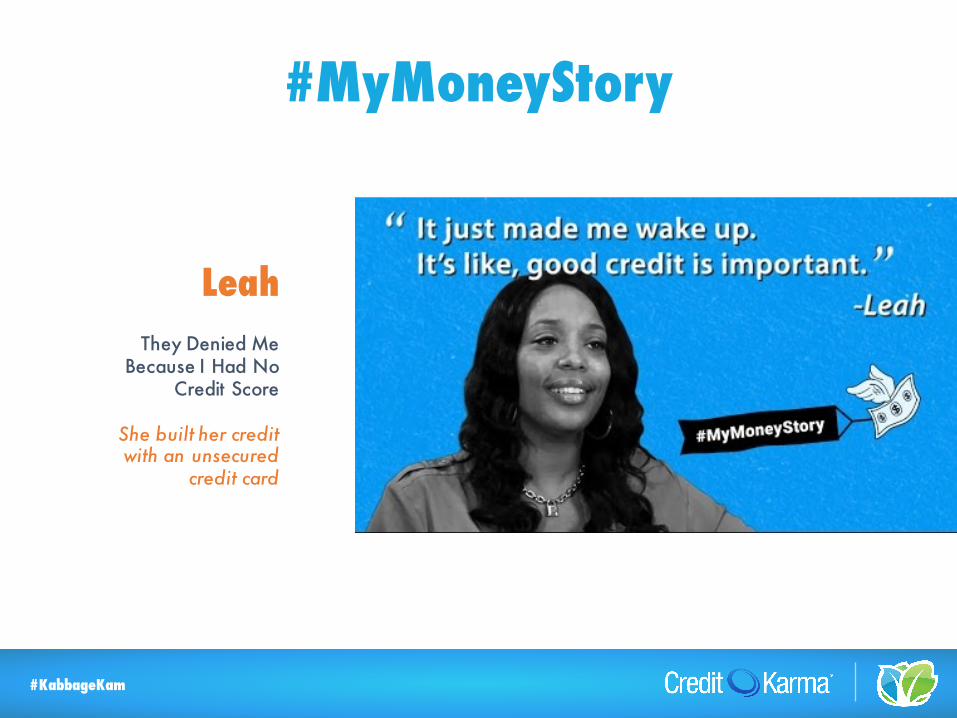

They Denied Me Because I Had No

Credit Score

She built her credit with an unsecured

credit card

Leah

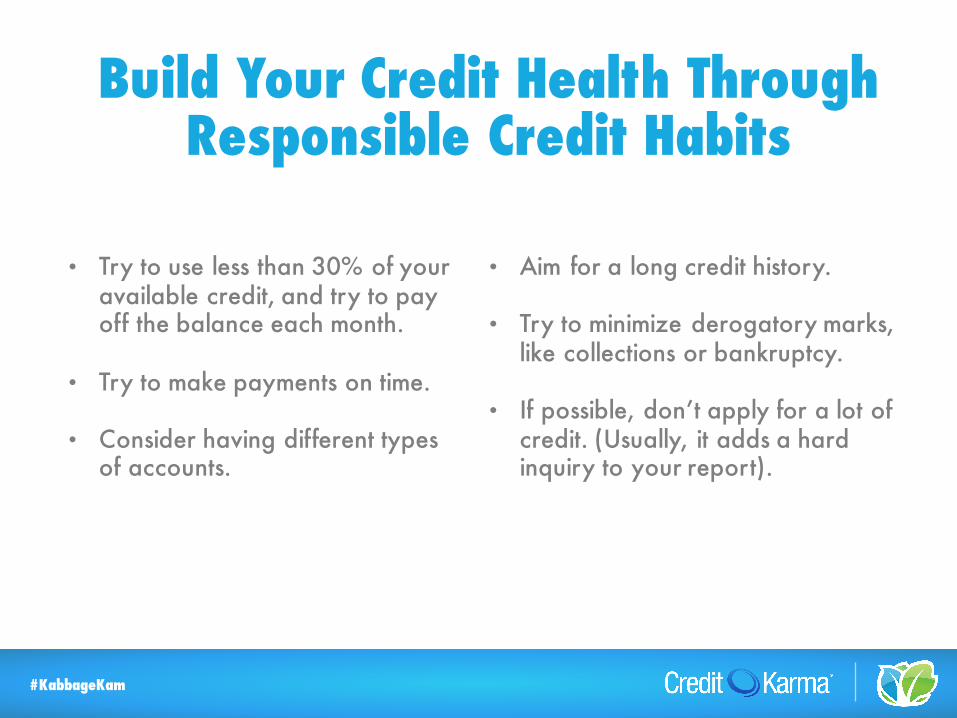

Build Your Credit Health Through Responsible Credit Habits

• Try to use less than 30% of your available credit, and try to pay off the balance each month.

• Try to make payments on time.

• Consider having different types of accounts.

#KabbageKam

• Aim for a long credit history.

• Try to minimize derogatory marks, like collections or bankruptcy.

• If possible, don’t apply for a lot of credit. (Usually, it adds a hard inquiry to your report).

Recovering From Debt

#KabbageKam

Debt Management

#KabbageKam

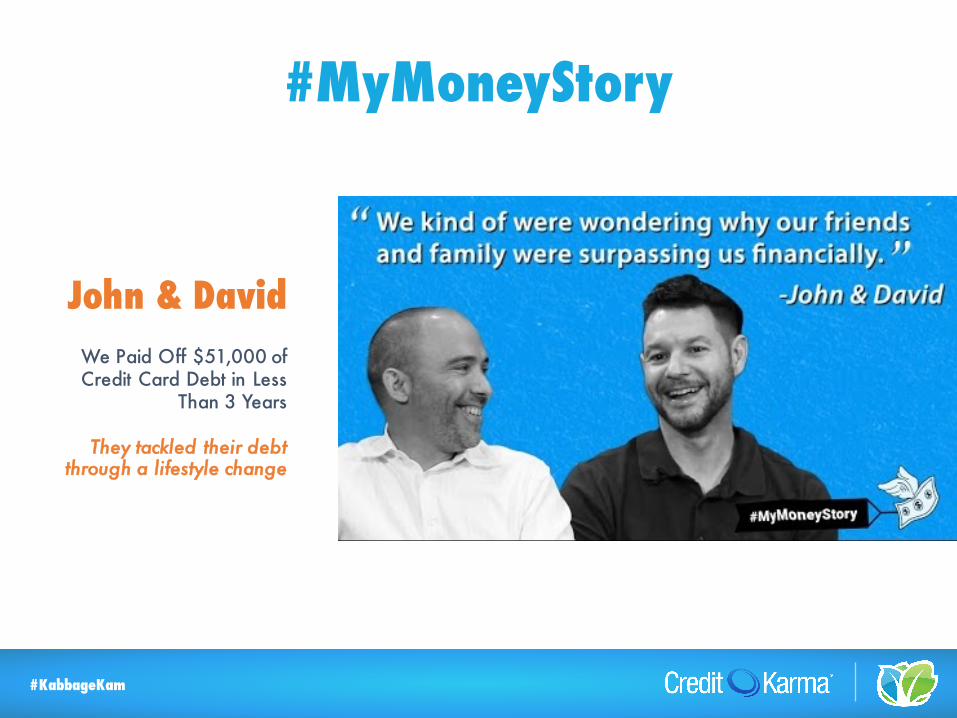

#MyMoneyStory

#KabbageKam#KabbageKam

We Paid Off $51,000 of Credit Card Debt in Less

Than 3 Years

They tackled their debt through a lifestyle change

John & David

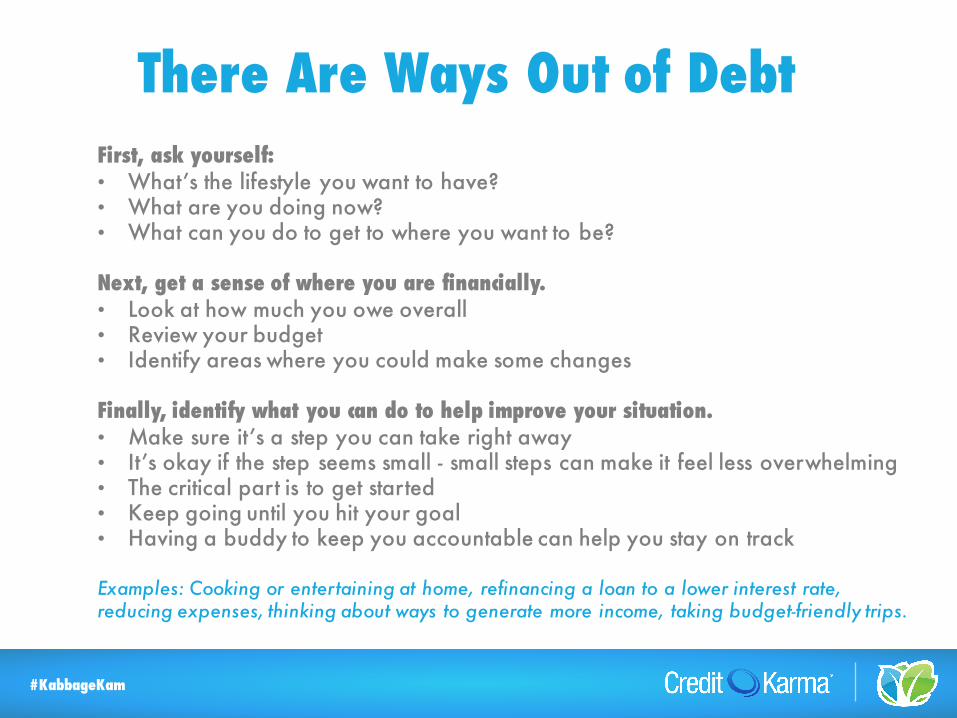

There Are Ways Out of DebtFirst, ask yourself:• What’s the lifestyle you want to have?• What are you doing now?• What can you do to get to where you want to be?

Next, get a sense of where you are financially. • Look at how much you owe overall• Review your budget• Identify areas where you could make some changes

Finally, identify what you can do to help improve your situation. • Make sure it’s a step you can take right away• It’s okay if the step seems small - small steps can make it feel less overwhelming• The critical part is to get started• Keep going until you hit your goal• Having a buddy to keep you accountable can help you stay on track

Examples: Cooking or entertaining at home, refinancing a loan to a lower interest rate, reducing expenses, thinking about ways to generate more income, taking budget-friendly trips.

#KabbageKam

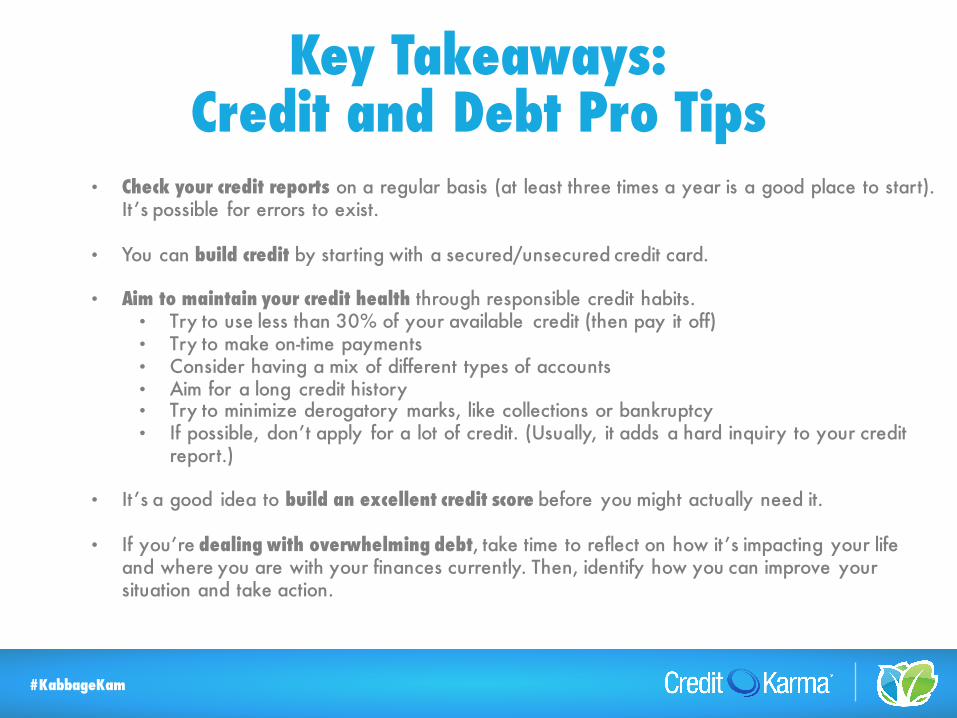

Key Takeaways: Credit and Debt Pro Tips

• Check your credit reports on a regular basis (at least three times a year is a good place to start). It’s possible for errors to exist.

• You can build credit by starting with a secured/unsecured credit card.

• Aim to maintain your credit health through responsible credit habits. • Try to use less than 30% of your available credit (then pay it off)• Try to make on-time payments• Consider having a mix of different types of accounts• Aim for a long credit history• Try to minimize derogatory marks, like collections or bankruptcy• If possible, don’t apply for a lot of credit. (Usually, it adds a hard inquiry to your credit

report.)

• It’s a good idea to build an excellent credit score before you might actually need it.

• If you’re dealing with overwhelming debt, take time to reflect on how it’s impacting your life and where you are with your finances currently. Then, identify how you can improve your situation and take action.

#KabbageKam

Get Small Business Content

Download Kabbage’s Free Comparison Hot Sheet:Small Business Loans 101

Visit this page to download: http://kabb.ag/kabbage101

Contact Information

#KabbageKam

Jennifer Micieli, CFP®

Marketplace Insights Manager

CreditKarma

28

Thank you!From us @KabbageInc

Top Related