Languages

Pages

Legal

1. PDS Information on your

MLC MasterKey Super & Pension Fundamentals accounts.

2. Fee Flyer Information on fees

and costs you will pay.

3. Investment Menu Information you

need to decide which investment options best suit your financial goals.

4. Investment Protection Guide

Information you need to decide if Investment Protection best suits your financial goals.

4. Super Fundamentals Application Form

Application form for MLC MasterKey Super Fundamentals.

5. Pension Fundamentals Application Form

Application form for MLC MasterKey Pension Fundamentals.

6. Application to Transfer Form

Application to move your existing account to MLC MasterKey Super Fundamentals or MLC MasterKey Pension Fundamentals.

7. Application to Transfer Pension Benefit Form

Application to transfer benefits between your existing MLC MasterKey Pension Fundamentals and MLC MasterKey Super Fundamentals accounts.

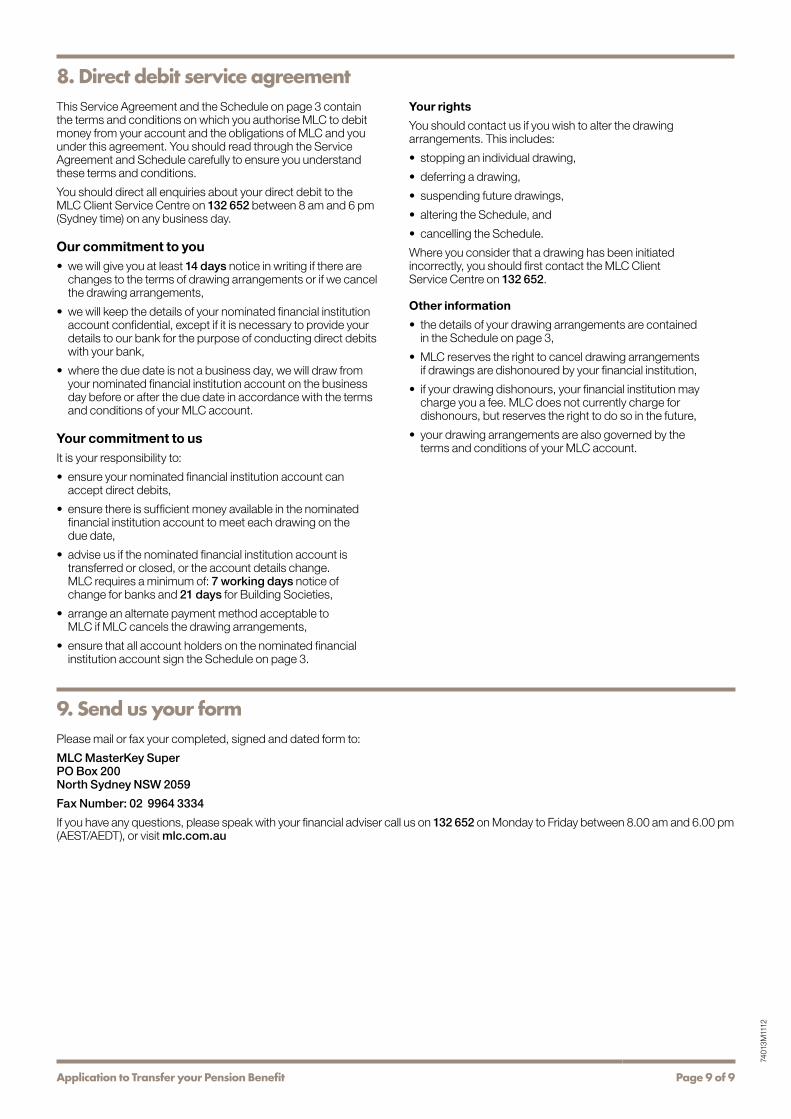

How to contact MLC

For more information, call MLC from anywhere in Australia on 132 652 or contact your adviser.

Postal address: MLC Limited, PO Box 200 North Sydney, NSW 2059

Website: mlc.com.au Fax: (02) 9964 3334

MLC MasterKey Super & Pension FundamentalsBuild your savings while you work, and look forward to a better retirement.

(Kit

9148

2)

1000

002M

0113

MLC MasterKey Super & Pension FundamentalsProduct Disclosure Statement

MLC Superannuation

Preparation date: 7 December 2012

Issued by: The Trustee, MLC Nominees Pty Limited (MLC)

ABN 93 002 814 959 AFSL 230702

The Universal Super Scheme ABN 44 928 361 101

1About MLC MasterKey Super & Pension FundamentalsWherever you are in life, MLC MasterKey Super & Pension Fundamentals can help you retire with more. It’s the one account that’s with you when you’re:

• working to save for retirement in the tax-effective environment of super

• moving towards retirement and continuing to grow your super while receiving tax-effective income from your pension, and

• enjoying retirement and can receive a lump sum when you stop working or transition easily into retirement with an account that pays you a steady income stream.

So no matter where you’re at in your working life, we can help you structure your super to build a better retirement.

With 125 years experience of looking after Australians’ needs, you know you’re with one of Australia’s most trusted and awarded wealth managers.

MLC MasterKey Super & Pension Fundamentals is part of The Universal Super Scheme.

Contents

1. About MLC MasterKey 1 Super & Pension Fundamentals

2. How super works 1

3. Benefits of investing 2 with MLC MasterKey Super & Pension Fundamentals

4. Risks of super 2

5. How we invest 3 your money

6. Fees and costs 4

7. How super is taxed 5

8. How to open 6 an account

This document is a summary of significant information and contains references to further important information in the Investment Menu, Fee Flyer, Investment Protection Guide and Application Forms.

You should consider all information before making a decision to invest in this product.

This information is general and does not take into account your personal financial situation or needs.

We recommend you obtain financial advice for your own personal circumstances.

The MLC group of companies is the wealth management division of National Australia Bank. We provide investment, super and insurance solutions and work closely with you and your adviser to help grow and protect your wealth.

2How super worksInvesting through super is a tax-effective way to save for your retirement.

The Government encourages Australians to use super to build wealth that will generate income in their retirement, and it’s compulsory for contributions to be made to super for most working Australians. Tax concessions and other Government benefits generally make it one of the best long-term investment vehicles.

Contributing to your superYou can generally choose where you want to invest your super.

Generally you, your spouse or your employer can contribute to your super and help it grow faster. You could also use strategies that include Government co-contributions or arranging with your employer to contribute some of your pre-tax salary.

Whatever strategy you choose, you can contribute via direct debit, BPAY®, credit card or cheque. You can also set up a Regular Investment Facility to make contributions from your bank account.

® Registered to BPAY Pty Ltd ABN 69 079 137 518

While you can contribute as much as you like, you will incur additional tax if contributions exceed certain limits.

The law defines your eligibility, the types of contributions you or others can make on your behalf, and the maximum amount you can contribute before you pay additional tax. It also determines whether you are eligible to access your super. To find out more go to apra.gov.au or ato.gov.au or moneysmart.gov.au

Consolidating your superKeeping your super in one place makes sense. You can transfer the money you hold in other Australian and overseas super accounts to your MLC super account.

This gives you a single view of your money, helps you keep track of your investments and means you are only paying one set of fees for your super.

We recommend that you seek financial advice before consolidating your super as your fees and benefits may be different.

Page 1 MLC MasterKey Super & Pension Fundamentals PDS

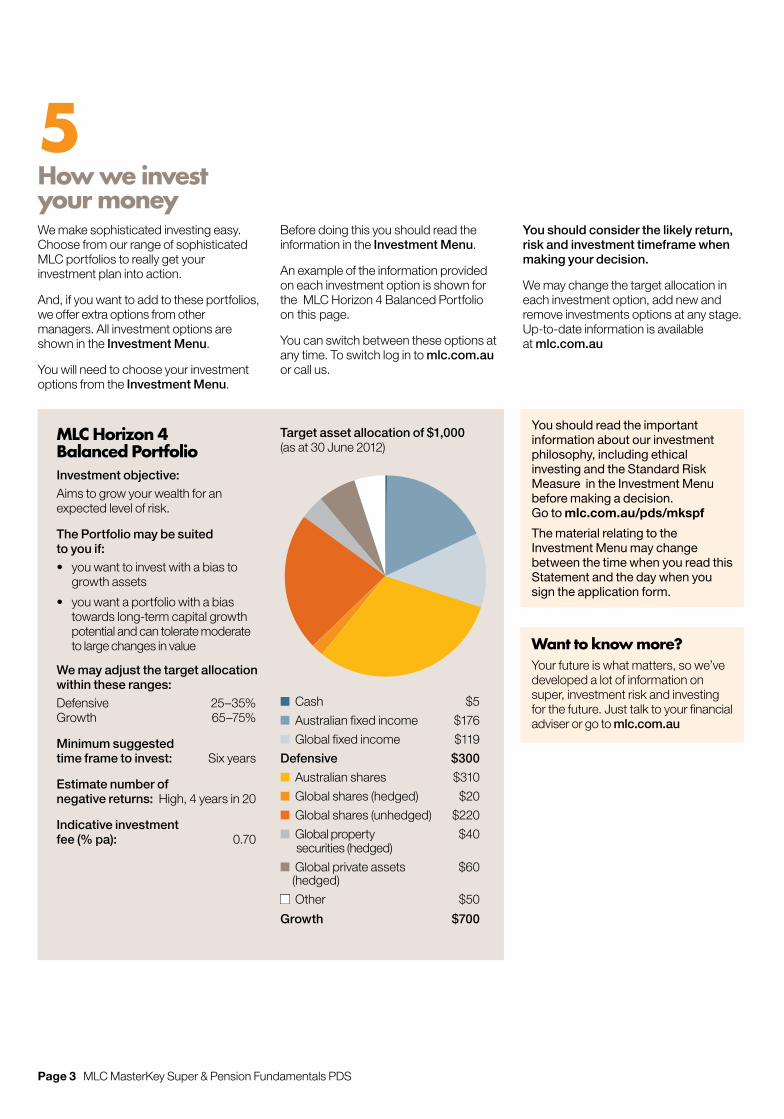

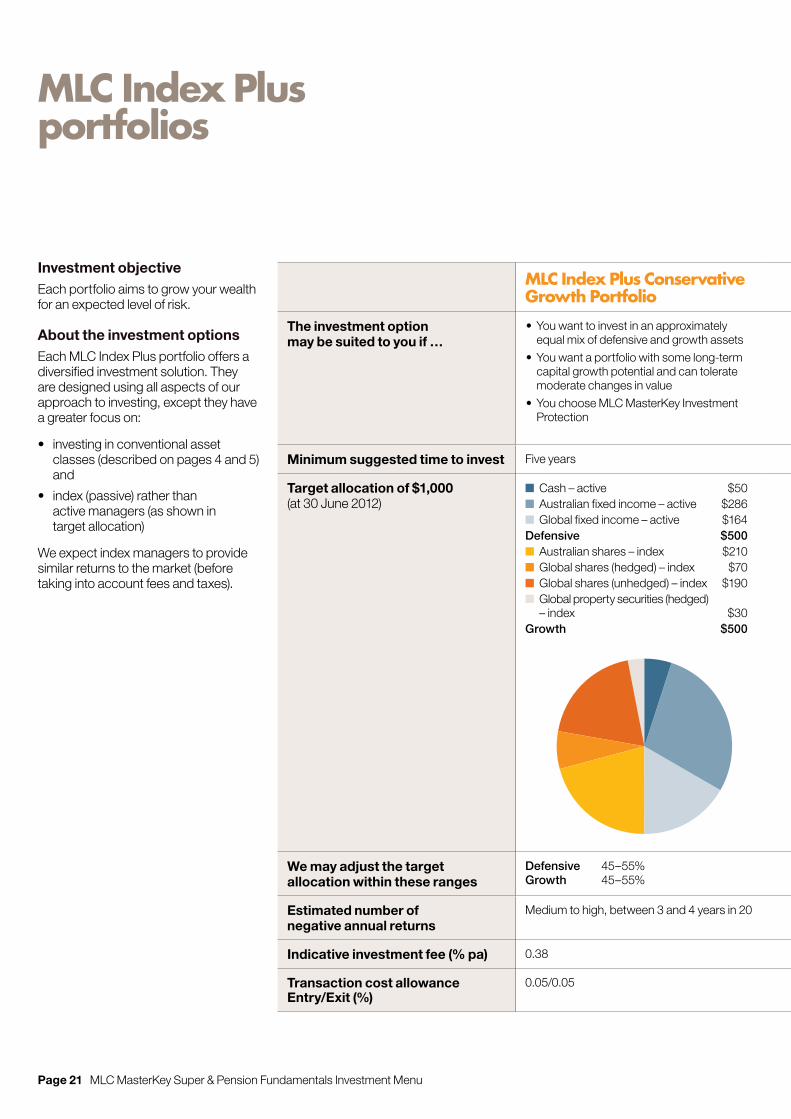

5How we invest your moneyWe make sophisticated investing easy. Choose from our range of sophisticated MLC portfolios to really get your investment plan into action.

And, if you want to add to these portfolios, we offer extra options from other managers. All investment options are shown in the Investment Menu.

You will need to choose your investment options from the Investment Menu.

Before doing this you should read the information in the Investment Menu.

An example of the information provided on each investment option is shown for the MLC Horizon 4 Balanced Portfolio on this page.

You can switch between these options at any time. To switch log in to mlc.com.au or call us.

You should consider the likely return, risk and investment timeframe when making your decision.

We may change the target allocation in each investment option, add new and remove investments options at any stage. Up-to-date information is available at mlc.com.au

MLC Horizon 4 Balanced PortfolioInvestment objective:Aims to grow your wealth for an expected level of risk.

The Portfolio may be suited to you if:• you want to invest with a bias to

growth assets

• you want a portfolio with a bias towards long-term capital growth potential and can tolerate moderate to large changes in value

We may adjust the target allocation within these ranges:Defensive 25–35% Growth 65–75%

Minimum suggested time frame to invest: Six years

Estimate number of negative returns: High, 4 years in 20

Indicative investment fee (% pa): 0.70

Target asset allocation of $1,000 (as at 30 June 2012)

n Cash $5

n Australian fixed income $176

n Global fixed income $119

Defensive $300

n Australian shares $310

n Global shares (hedged) $20

n Global shares (unhedged) $220

n Global property $40 securities (hedged)

n Global private assets $60 (hedged)

n Other $50

Growth $700

You should read the important information about our investment philosophy, including ethical investing and the Standard Risk Measure in the Investment Menu before making a decision. Go to mlc.com.au/pds/mkspf

The material relating to the Investment Menu may change between the time when you read this Statement and the day when you sign the application form.

Want to know more?Your future is what matters, so we’ve developed a lot of information on super, investment risk and investing for the future. Just talk to your financial adviser or go to mlc.com.au

Page 3 MLC MasterKey Super & Pension Fundamentals PDS

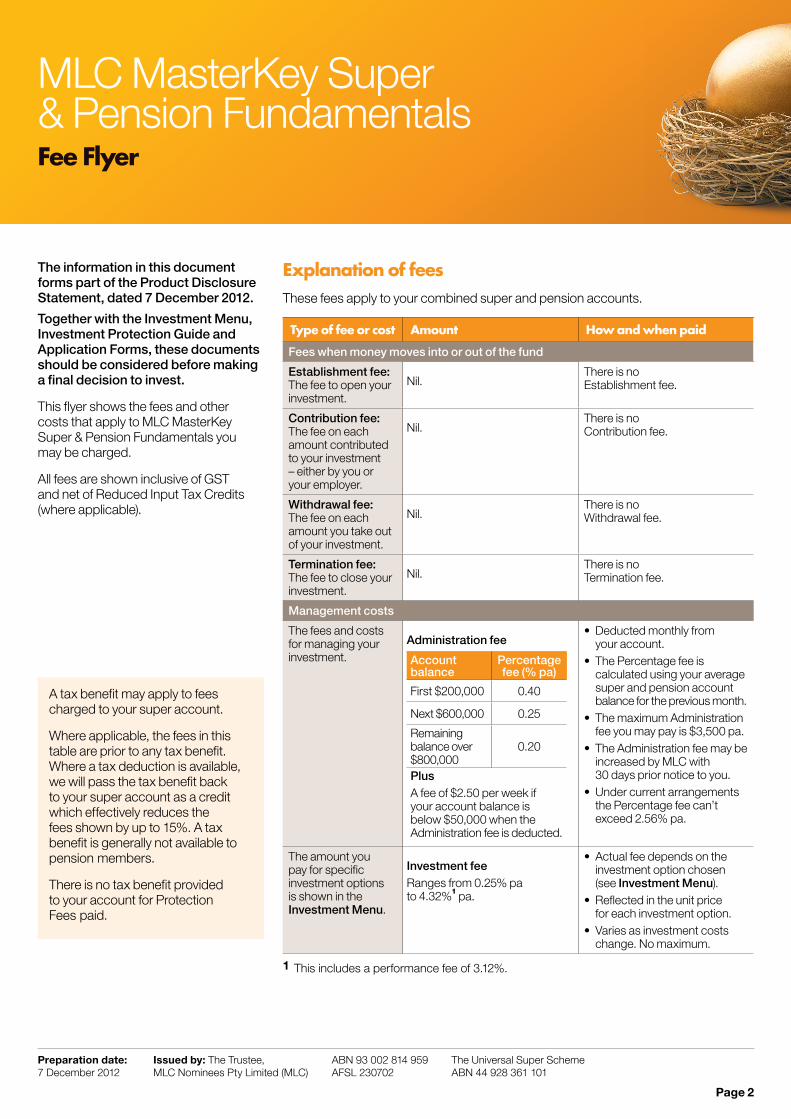

6Fees and costs

A tax benefit may apply to fees charged to your super account. All fees in the table below are before the tax benefit.

We charge the fees and then pass the tax benefit back to your super account as a credit, which effectively reduces the fees shown below by 15%.

The information in this table can be used to compare fees and costs between different superannuation products.

These fees and costs may be deducted from your account, from the returns on your investment or from fund assets as a whole.

To find out moreIf you would like to find out more, or see the impact of fees for your own circumstances, the Australian Securities and Investments Commission (ASIC) website (moneysmart.gov.au) has a Superannuation calculator to help you check out different fee options.

These fees apply to your combined super and pension accounts.

Type of fee or cost Amount

Fees when you move your money in or out of the fund

Establishment fee Nil.

Contribution fee Nil.

Withdrawal fee Nil.

Termination fee Nil.

Management costs

The fees and costs for managing your investment.

Administration fee

Account balance Percentage fee (% pa)

First $200,000 0.40

Next $600,000 0.25

Remaining balance over $800,000 0.20

Plus A fee of $2.50 per week if your account balance is below $50,000 when the Administration fee is deducted.

1 Includes a performance fee. For more information refer to the Investment Menu.

Example of annual fees and costsThis table is an example of how the fees and costs in a balanced option for this product can affect your investment over a one year period. You should use this table to compare this product with other super products.

Example: MLC Horizon 4 Balanced Portfolio

Balance of $50,000 with total contributions of $5,000 during the year

Contribution fees

0% For every $5,000 you put in, you’ll be charged $0.

Plus Management costs:

Administration fee

0.40% x $50,000

$200 And, for every $50,000 you have in the fund you will be charged $550 each year.

Investment fee

0.70%1 x $50,000

$350

Equals Cost of fund If you put in $5,000 during a year and your balance was $50,000, then for that year you will be charged fees of:

$5502

What it costs you will depend on the investment option you choose and the fees you negotiate with your fund or financial adviser.

1 The Indicative investment fee for MLC Horizon 4 Balanced Portfolio is 0.70%.2 Additional fees may apply: Establishment fee – $0. And, if you leave the fund early, you may be charged Withdrawal fees of 0% of your total account balance. A Termination fee of $0 is deducted from the amount paid when you make a full withdrawal. This example assumes no investment gains or losses during the year and the contribution was made on the last day of the year.

Page 4 MLC MasterKey Super & Pension Fundamentals PDS

Administration fee

Account balance Percentage fee (% pa)

First $200,000 0.40

Next $600,000 0.25

Remaining balance over $800,000 0.20

Plus A fee of $2.50 per week if your account balance is below $50,000 when the Administration fee is deducted.

Investment fee Ranges from 0.25% pa to 4.32%1 pa.

Did you know?Small differences in both investment performance and fees and costs can have a substantial impact on your long-term returns.

For example, total annual fees and costs of 2% of your fund balance rather than 1% could reduce your final return by up to 20% over a 30 year period (for example, reduce it from $100,000 to $80,000).

You should consider whether features such as superior investment performance or the provision of better member services justify higher fees and costs.

You may be able to negotiate to pay a lower contribution fee and management costs where applicable. Ask us or your financial adviser.

Adviser service feeIf you wish, you can have amounts deducted from your account to pay fees to your financial adviser.

This fee will be in addition to the other fees described in the Fee Flyer.

Any arrangement you have should be detailed in the Statement of Advice provided by your financial adviser.

Varying of feesWe may vary our fees, costs or fee discounts but we’ll give you 30 days’ notice of any increase. The only exception is for investment fees, which vary daily with investment costs and Government taxes and charges.

You should read the important information about the fees, costs and investment options in the Fee Flyer and Investment Menu before making a decision. Go to mlc.com.au/pds/mkspf

The material relating to the fees, costs and investment options in the Fee Flyer and Investment Menu may change between the time when you read this Statement and the day when you sign the application form.

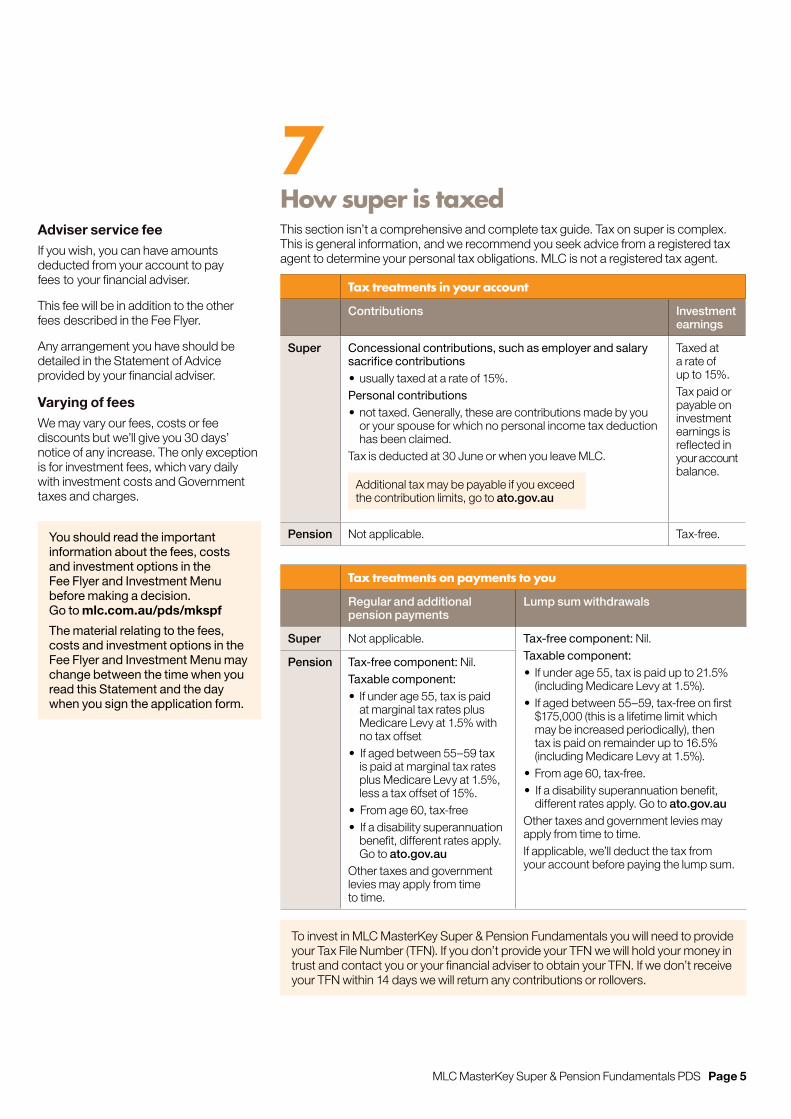

7How super is taxedThis section isn’t a comprehensive and complete tax guide. Tax on super is complex. This is general information, and we recommend you seek advice from a registered tax agent to determine your personal tax obligations. MLC is not a registered tax agent.

Tax treatments in your account

Contributions Investment earnings

Super Concessional contributions, such as employer and salary sacrifice contributions•usually taxed at a rate of 15%.Personal contributions •not taxed. Generally, these are contributions made by you

or your spouse for which no personal income tax deduction has been claimed.

Tax is deducted at 30 June or when you leave MLC.

Additional tax may be payable if you exceed the contribution limits, go to ato.gov.au

Taxed at a rate of up to 15%.Tax paid or payable on investment earnings is reflected in your account balance.

Pension Not applicable. Tax-free.

Tax treatments on payments to you

Regular and additional pension payments

Lump sum withdrawals

Super Not applicable. Tax-free component: Nil.Taxable component:• If under age 55, tax is paid up to 21.5%

(including Medicare Levy at 1.5%).• If aged between 55–59, tax-free on first

$175,000 (this is a lifetime limit which may be increased periodically), then tax is paid on remainder up to 16.5% (including Medicare Levy at 1.5%).

•From age 60, tax-free.• If a disability superannuation benefit,

different rates apply. Go to ato.gov.auOther taxes and government levies may apply from time to time.If applicable, we’ll deduct the tax from your account before paying the lump sum.

Pension Tax-free component: Nil.Taxable component: • If under age 55, tax is paid

at marginal tax rates plus Medicare Levy at 1.5% with no tax offset

• If aged between 55–59 tax is paid at marginal tax rates plus Medicare Levy at 1.5%, less a tax offset of 15%.

• From age 60, tax-free• If a disability superannuation

benefit, different rates apply. Go to ato.gov.au

Other taxes and government levies may apply from time to time.

To invest in MLC MasterKey Super & Pension Fundamentals you will need to provide your Tax File Number (TFN). If you don’t provide your TFN we will hold your money in trust and contact you or your financial adviser to obtain your TFN. If we don’t receive your TFN within 14 days we will return any contributions or rollovers.

MLC MasterKey Super & Pension Fundamentals PDS Page 5

8How to open an accountTo open your super account you may apply online through your financial adviser or fill in an Application Form and send to us. We may need to confirm your identity when we process your application.

Once you have access to your super money you can start a pension. This may be from an existing MLC account, other super accounts or both. Just apply online through your financial adviser or fill in an Application Form and send to us. We may need to confirm your identity when we process your application.

Product and investment option changesChanges will be made from time to time. Changes that are not materially adverse will be made available on mlc.com.au or you can obtain a paper copy of the changes on request free of charge.

Want to change your mind?

You can mail, fax or email us to close your account within 14 days of opening it. We’re restricted by law on the amount that may be paid. To find out more go to apra.gov.au or ato.gov.au. Your account balance will be adjusted for any:

• increase or decrease in the value of your investment

• pension payments made to you

• any insurance premium paid

• tax payable, and

• administration costs incurred in establishing or closing your account.

This cooling-off period doesn’t apply if you transact on your account within 14 days.

For more information For more information please go to the online copy of this document on mlc.com.au/pds/mkspf or contact us or your financial adviser.

MLC MasterKey Super & Pension Fundamentals PDS Page 6

Resolving complaintsWe can usually resolve complaints over the phone. If we can’t, or you’re not satisfied with the outcome, please write to us. We’ll work to resolve your complaint as soon as possible.

If you’re not satisfied with our decision you can get further advice from the Superannuation Complaints Tribunal by calling 1300 884 114, or emailing [email protected]

More information is available on sct.gov.au

3Benefits of investing with MLC MasterKey Super & Pension FundamentalsMLC MasterKey Super & Pension Fundamentals is a great way to access sophisticated investment solutions designed to help you grow and protect your super. We offer a range of features to help you get your money working for you, the way you want.

Investments As Australia’s largest and most experienced multi-manger, we research hundreds of investment managers from around the world to select some of the best ones for our investment portfolios.

This means our portfolios are expertly designed so you can use them as a total investment solution.

And, because world markets change, we manage and evolve our portfolios by actively researching these markets, and seeking new opportunities to increase returns or reduce risk.

We recognise some investors want extra options when it comes to managing their money. To help you do this, we offer options from other managers that don’t use MLC’s approach to investing, for you and your financial adviser to choose from.

Investment ProtectionIf you want to take advantage of market growth and protect your savings, then investment protection may be right for you.

With MLC MasterKey Investment Protection you can invest with greater certainty and protect your super or pension.

For information on protection options that meet your needs, please contact your financial adviser.

ReportingWe also keep you updated with regular reports and online access to your account, so you can see exactly how your investments are performing.

Insurance you can depend onWith MLC, you get cover you can trust from a multi-award winning provider of personal insurance to more Australians than any other company.

If you’re under 65, you can apply for our life and disability insurance and pay the premiums from your account.

For more information on insurance options that meet your needs, please contact your financial adviser or go to mlc.com.au

In the event of your deathYour account balance can be paid to your beneficiaries or your estate in the event of your death. Please let us know who you want to receive your account balance, otherwise the Trustee will decide.

MLC MasterKey Super & Pension Fundamentals PDS Page 2

4Risks of superBefore you do any investing in super, there are some things you need to consider including the level of risk you are prepared to accept. Factors that will affect your decision include:

• your investment goals

• the savings you’ll need to reach your goals

• how many years you have to invest

• the return you may expect from your investments, including investments outside of super, and

• how comfortable you are with investment risk.

Investment riskEven the simplest of investments come with a level of risk and different investments have different levels of risk.

While the idea of investment risk can be confronting, it’s a normal part of investing. Without it you may not get the returns you need to reach your financial goals. This is known as the risk/return trade-off.

When considering your investment, it’s important to understand that:

• its value will vary over time

• investments with higher return potential, usually have higher levels of risk

• returns aren’t guaranteed, and you may lose some of your money

• previous returns shouldn’t be used to predict future returns, and

• your final super balance may not provide for an adequate retirement.

Accessing the money you put into superBecause super is for your retirement the law is strict about how and when you can access your money. To find out more go to moneysmart.gov.au

Legislative changeJust as the Government makes rules, it can also change them. Your financial adviser can help you respond to any changes to laws on super, tax, social security and other retirement issues.

You should read the important information about our protection options in the Investment Protection Guide before making a decision. Go to mlc.com.au/pds/mkspfThe material relating to the Investment Protection Guide may change between the time when you read this Statement and the day when you sign the application form.

For more information call MLC from anywhere in Australia on 132 652 or contact your adviser.

Postal address: PO Box 200 North Sydney NSW 2059

Registered office: Ground Floor, MLC Building 105–153 Miller Street North Sydney NSW 2060

mlc.com.au 68455M1112

MLC Superannuation

Page 2

The information in this document forms part of the Product Disclosure Statement, dated 7 December 2012.

Together with the Investment Menu, Investment Protection Guide and Application Forms, these documents should be considered before making a final decision to invest.

This flyer shows the fees and other costs that apply to MLC MasterKey Super & Pension Fundamentals you may be charged.

All fees are shown inclusive of GST and net of Reduced Input Tax Credits (where applicable).

MLC MasterKey Super & Pension FundamentalsFee Flyer

A tax benefit may apply to fees charged to your super account.

Where applicable, the fees in this table are prior to any tax benefit. Where a tax deduction is available, we will pass the tax benefit back to your super account as a credit which effectively reduces the fees shown by up to 15%. A tax benefit is generally not available to pension members.

There is no tax benefit provided to your account for Protection Fees paid.

Type of fee or cost Amount How and when paid

Fees when money moves into or out of the fund

Establishment fee: The fee to open your investment.

Nil.There is no Establishment fee.

Contribution fee: The fee on each amount contributed to your investment – either by you or your employer.

Nil.There is no Contribution fee.

Withdrawal fee: The fee on each amount you take out of your investment.

Nil.There is no Withdrawal fee.

Termination fee: The fee to close your investment.

Nil.There is no Termination fee.

Management costs

The fees and costs for managing your investment.

Administration fee

Account balance

Percentage fee (% pa)

First $200,000 0.40

Next $600,000 0.25

Remaining balance over $800,000

0.20

PlusA fee of $2.50 per week if your account balance is below $50,000 when the Administration fee is deducted.

•Deducted monthly from your account.

• The Percentage fee is calculated using your average super and pension account balance for the previous month.

• The maximum Administration fee you may pay is $3,500 pa.

• The Administration fee may be increased by MLC with 30 days prior notice to you.

•Under current arrangements the Percentage fee can’t exceed 2.56% pa.

The amount you pay for specific investment options is shown in the Investment Menu.

Investment feeRanges from 0.25% pa to 4.32%1 pa.

•Actual fee depends on the investment option chosen (see Investment Menu).

•Reflected in the unit price for each investment option.

•Varies as investment costs change. No maximum.

1 This includes a performance fee of 3.12%.

Explanation of feesThese fees apply to your combined super and pension accounts.

Preparation date: 7 December 2012

Issued by: The Trustee, MLC Nominees Pty Limited (MLC)

ABN 93 002 814 959 AFSL 230702

The Universal Super Scheme ABN 44 928 361 101

Page 3

Type of fee or cost Amount How and when paid

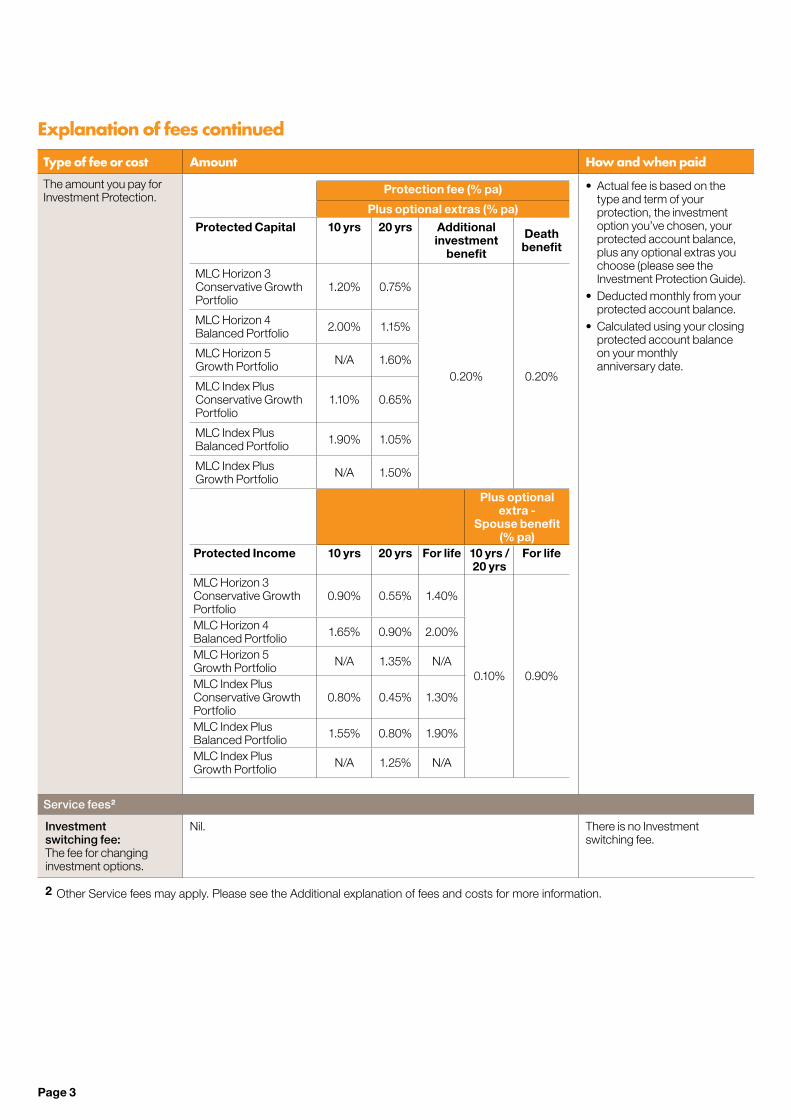

The amount you pay for Investment Protection.

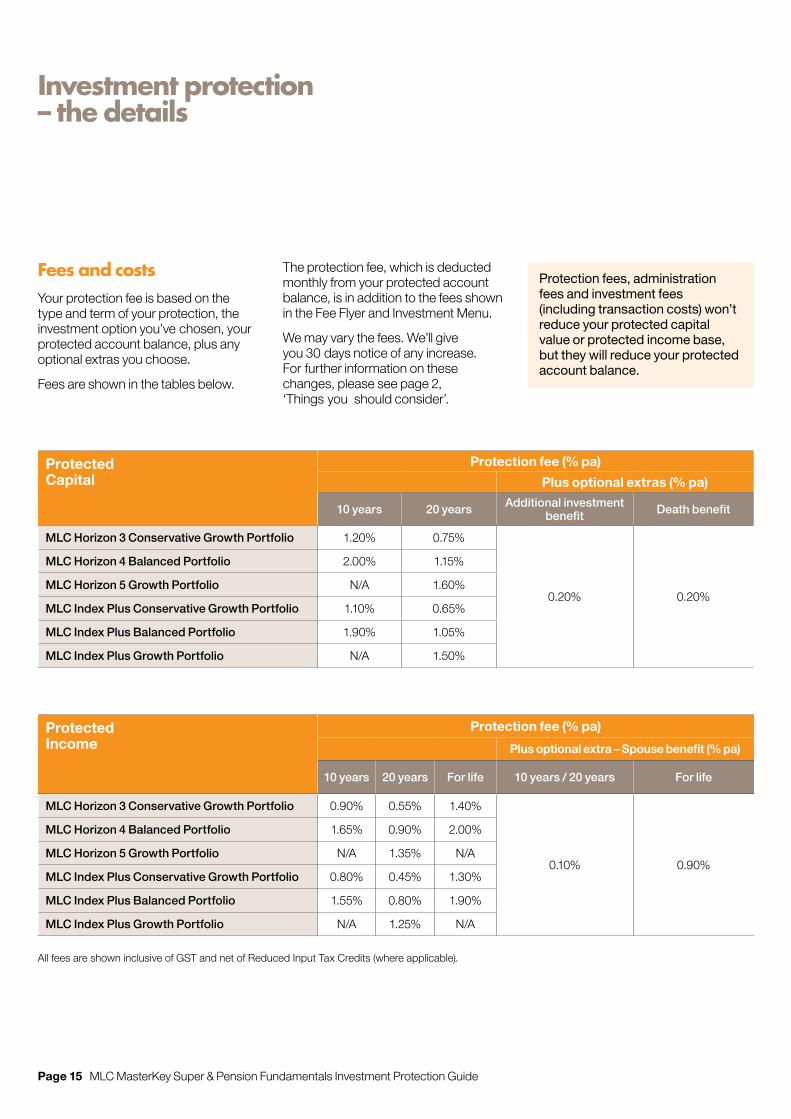

Protection fee (% pa)

Plus optional extras (% pa)

Protected Capital 10 yrs 20 yrs Additional investment

benefit

Death benefit

MLC Horizon 3 Conservative Growth Portfolio

1.20% 0.75%

0.20% 0.20%

MLC Horizon 4 Balanced Portfolio 2.00% 1.15%

MLC Horizon 5 Growth Portfolio N/A 1.60%

MLC Index Plus Conservative Growth Portfolio

1.10% 0.65%

MLC Index Plus Balanced Portfolio 1.90% 1.05%

MLC Index Plus Growth Portfolio N/A 1.50%

Plus optional extra -

Spouse benefit (% pa)

Protected Income 10 yrs 20 yrs For life 10 yrs / 20 yrs

For life

MLC Horizon 3 Conservative Growth Portfolio

0.90% 0.55% 1.40%

0.10% 0.90%

MLC Horizon 4 Balanced Portfolio 1.65% 0.90% 2.00%

MLC Horizon 5 Growth Portfolio N/A 1.35% N/A

MLC Index Plus Conservative Growth Portfolio

0.80% 0.45% 1.30%

MLC Index Plus Balanced Portfolio 1.55% 0.80% 1.90%

MLC Index Plus Growth Portfolio N/A 1.25% N/A

•Actual fee is based on the type and term of your protection, the investment option you’ve chosen, your protected account balance, plus any optional extras you choose (please see the Investment Protection Guide).

•Deducted monthly from your protected account balance.

•Calculated using your closing protected account balance on your monthly anniversary date.

Service fees2

Investment switching fee: The fee for changing investment options.

Nil. There is no Investment switching fee.

2 Other Service fees may apply. Please see the Additional explanation of fees and costs for more information.

Explanation of fees continued

Page 4

Additional explanation of fees and costsInvestment manager fee rebateSome investment managers provide a rebate on their investment management fee, which we pass entirely back to your account.

The investment fees in the Investment Menu are shown after allowing for this rebate.

Transaction cost allowanceWhen calculating unit prices, MLC may make an allowance for the costs of buying and selling assets. These costs include brokerage and stamp duty.

When you transact on your account you may pay a small proportion of your transaction towards meeting these costs. These may vary in future without prior notice to you.

Performance feeAn investment manager may charge a performance fee when its investment returns exceed a specified level. Where applicable, an estimate of this fee is included in the investment fees shown in the Investment Menu.

The actual performance fee charged in future periods may differ from that disclosed in the Investment Menu.

You can get more information on how performance fees are calculated by going to the investment managers’ Product Disclosure Statements available on mlc.com.au

Family Law feeThe Family Law Act enables investments to be divided between parties in the event of a breakdown of a marriage or de facto relationship.

We may be legally compelled to provide information to other parties in accordance with this legislation.

We may charge a fee for this service.

Adviser service feeIf you wish you can have amounts deducted from your account to pay fees to your financial adviser.

This fee will be in addition to the other fees described in this Fee Flyer. Any arrangement you have with your financial adviser should be detailed in the Statement of Advice provided by them.

Adviser remuneration

MLC does not pay commission to financial advisers for this product.

Advisers may receive alternative forms of remuneration, such as the costs of maintaining their professional development qualifications. This is paid from the Administration fee and is not an additional cost to you. Actual payments are recorded in registers which you can view on request.

Fees paid to NAB group companiesMLC may use the services of NAB owned companies where it makes good business sense to do so and will benefit our customers.

Amounts paid for these services are always negotiated on an arms length basis and are included in all the fees detailed on these pages.

Each financial year, MLC pays NAB a fee of up to 0.1% of contributions made to MLC MasterKey Super & Pension Fundamentals by customers introduced by NAB. This is included in the fees and costs already shown in this flyer.

Fee rebates for small super account balancesThe law limits the amount of fees we can deduct from your account if the value of your account is less than $1,000 and it includes or has included Superannuation Guarantee or award contributions made by your employer.

Other fees we may chargeFees may be charged if you request a service not currently offered.

We may charge members, or the fund generally, with actual or estimated costs of running the fund. These may include costs resulting from government legislation or fees that are charged by third parties.

Varying your feesWe may vary our fees, costs or fee discounts but we’ll give you 30 days notice of any increase. The only exceptions are for investment fees which vary daily with investment costs and Government taxes and charges.

84499M1112

For more information please go to mlc.com.au or call us on 132 652 or from outside Australia on +61 3 8634 4721 or speak with your adviser.

Postal address: PO Box 200 North Sydney NSW 2059

Registered office: Ground Floor, MLC Building 105–153 Miller Street North Sydney NSW 2060

MLC MasterKey Super & Pension FundamentalsInvestment Menu

MLC Superannuation

Preparation date: 7 December 2012

Issued by: The Trustee, MLC Nominees Pty Limited (MLC)

ABN 93 002 814 959 AFSL 230702

The Universal Super Scheme ABN 44 928 361 101

For more information please contact us, your financial adviser or go to the online copy of this document on mlc.com.au/pds/mkspf

References to websites in this document direct you to additional information.

This menu gives you information about the investments available through MLC MasterKey Super & Pension Fundamentals.

ContentsWhat this menu covers

MLC. With you 1Who you go through life with makes all the difference.

Things to consider 2 before you invest Before you do any investing, we want you to know about both the benefits and potential risks involved.

MLC’s approach 8 to investingWe design investment solutions to help investors achieve their goals while managing risk.

Investing with MLC 9Our portfolios make sophisticated investing straightforward.

Investment options 26 not managed by MLCThese are single asset class investment options from other managers.

The information in this document forms part of the Product Disclosure Statement, dated 7 December 2012. Together with the Fee Flyer, Investment Protection Guide and Application Forms, these documents should be considered before making a final decision to invest.

Page 1 MLC MasterKey Super & Pension Fundamentals Investment Menu

Who you go through life with makes all the difference.

At MLC, we’ve been looking after Australians’ investment and insurance needs for over 125 years.

This experience has taught us the right solution is as unique as each investor.

That’s why we specialise in creating a diverse range of super, investment and insurance solutions.

We do this so you and your financial adviser can grow and protect your wealth the way you want to.

And, as your needs will change with time, we’ll continually enhance our products and services so you can get the best out of your experience with us.

The Fund Profile ToolThis easy to use, interactive tool will give you greater insight into how your money is managed including where your money is invested and how your investments are performing. For the latest information on the MLC portfolios go to mlc.com.au

Investing with usOur portfolios make sophisticated investing straightforward.

We’re experts in putting together portfolios for people.

With our leading-edge design process, we structure our portfolios to deliver more reliable returns in many potential market environments.

And, as our view of world markets changes, we evolve our portfolios to manage new risks and capture new opportunities.

We have both internal investment management expertise, and the experience and resources to find some of the world’s best investment managers.

Importantly, we stay true to the objectives of our portfolios, so you can keep on track to meeting your goals.

MLC.With you

The MLC group of companies looks after more than $123.5 billion (as at 31 March 2012) on behalf of individual and corporate investors in Australia and is the wealth management division of the National Australia Bank.

We provide investment, super and insurance solutions and work closely with you and your financial adviser to help grow and protect your wealth.

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 2

Things to considerbefore you invest

Before you do any investing, we want you to know about both the benefits and potential risks involved.

Even the simplest of investments come with a level of risk.

While the idea of investment risk can be confronting, it’s a normal part of investing. Without it you may not get the returns you need to reach your financial goals.

This is known as the risk/return trade-off.

The value of an investment with a higher level of risk will tend to rise and fall more often and by greater amounts.

In other words, it is likely to be more volatile than those with less risk.

Many factors influence an investment’s value. These include, but aren’t limited to:

•market sentiment

•growth and contraction in the Australian and overseas economies

• legislative changes

•changes in interest rates

•defaults on loans

•company specific issues

• liquidity (the ability to buy or sell investments when you want to), and

•changes in the value of the Australian dollar.

Page 3 MLC MasterKey Super & Pension Fundamentals Investment Menu

Things to considerbefore you invest

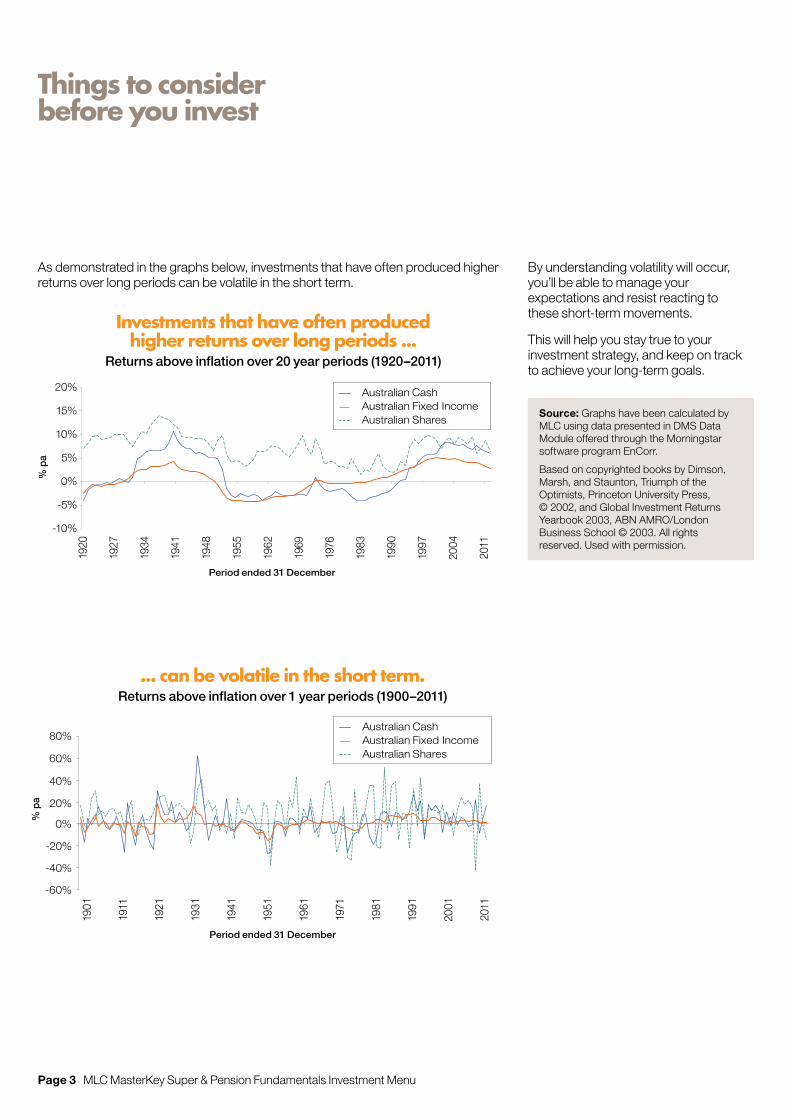

As demonstrated in the graphs below, investments that have often produced higher returns over long periods can be volatile in the short term.

Source: Graphs have been calculated by MLC using data presented in DMS Data Module offered through the Morningstar software program EnCorr.

Based on copyrighted books by Dimson, Marsh, and Staunton, Triumph of the Optimists, Princeton University Press, © 2002, and Global Investment Returns Yearbook 2003, ABN AMRO/London Business School © 2003. All rights reserved. Used with permission.

By understanding volatility will occur, you’ll be able to manage your expectations and resist reacting to these short-term movements.

This will help you stay true to your investment strategy, and keep on track to achieve your long-term goals.

... can be volatile in the short term.Returns above inflation over 1 year periods (1900–2011)

Investments that have often produced higher returns over long periods ...

Returns above inflation over 20 year periods (1920–2011)

Period ended 31 December

1920

1934

1927

1941

1948

1955

1962

1969

1976

1983

1990

1997

2004

2011

20%

15%

10%

5%

0%

-5%

-10%

% p

a

Australian Cash Australian Fixed Income Australian Shares

Period ended 31 December

1901

1911

1921

1931

1941

1951

1961

1971

1981

1991

2001

2011

% p

a

Australian Cash Australian Fixed Income Australian Shares

Period ended 31 December

1920

1934

1927

1941

1948

1955

1962

1969

1976

1983

1990

1997

2004

2011

20%

15%

10%

5%

0%

-5%

-10%

% p

a

Australian Cash Australian Fixed Income Australian Shares

Period ended 31 December

1901

1911

1921

1931

1941

1951

1961

1971

1981

1991

2001

2011

% p

a

Australian Cash Australian Fixed Income Australian Shares

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 4

Diversify to reduce volatility and other risksDiversification is a sound way to reduce short-term volatility. It also helps you manage the risk of not being able to buy or sell assets when you want to.

The more you diversify the less impact any one investment can have on your portfolio.

One of the most effective ways of reducing volatility is to diversify across a range of asset classes.

Asset classes are groups of similar types of investments.

Each class has its risks and benefits, and goes through its own market cycle. A market cycle can take a couple of years or many years; it’s different each time.

In the description of the investment options (from page 10), we include a minimum time to invest. Investing for the minimum time or longer improves your chances of achieving the return you expect. However, returns can’t be guaranteed.

You need to be prepared for all sorts of return outcomes when investing.

The main asset class risks and benefits are:

CashCash tends to be included in a portfolio to meet liquidity needs.

Things to consider:

•Cash is usually the least volatile type of investment. It also tends to have the lowest return over a market cycle.

•The return is typically all income and is referred to as interest or yield.

•The market value tends not to change. However, when you invest in cash, you’re effectively lending money to businesses or governments that could default on the loans. A default could result in a loss on your investment.

•Many cash funds invest in fixed income securities that have a very short term until maturity.

•Cash is generally a low risk investment.

Fixed incomeWhen investing in fixed income securities, you’re effectively lending money to businesses or governments.

Returns typically comprise interest and changes in the market value of the security.

Things to consider:

•There are different types of fixed income securities and these will have different returns and volatility.

•Fixed income securities denominated in foreign currencies will be exposed to exchange rate variations.

•The market value of a fixed income security may fall due to factors such as an increase to interest rates or concern about defaults on loans. This may result in a loss on your investment.

•The interest rate on a term deposit is fixed for its specified term. That means the return won’t be affected by a change in interest rates for the term of the deposit.

•Fixed income securities are usually included in a portfolio for their defensive characteristics.

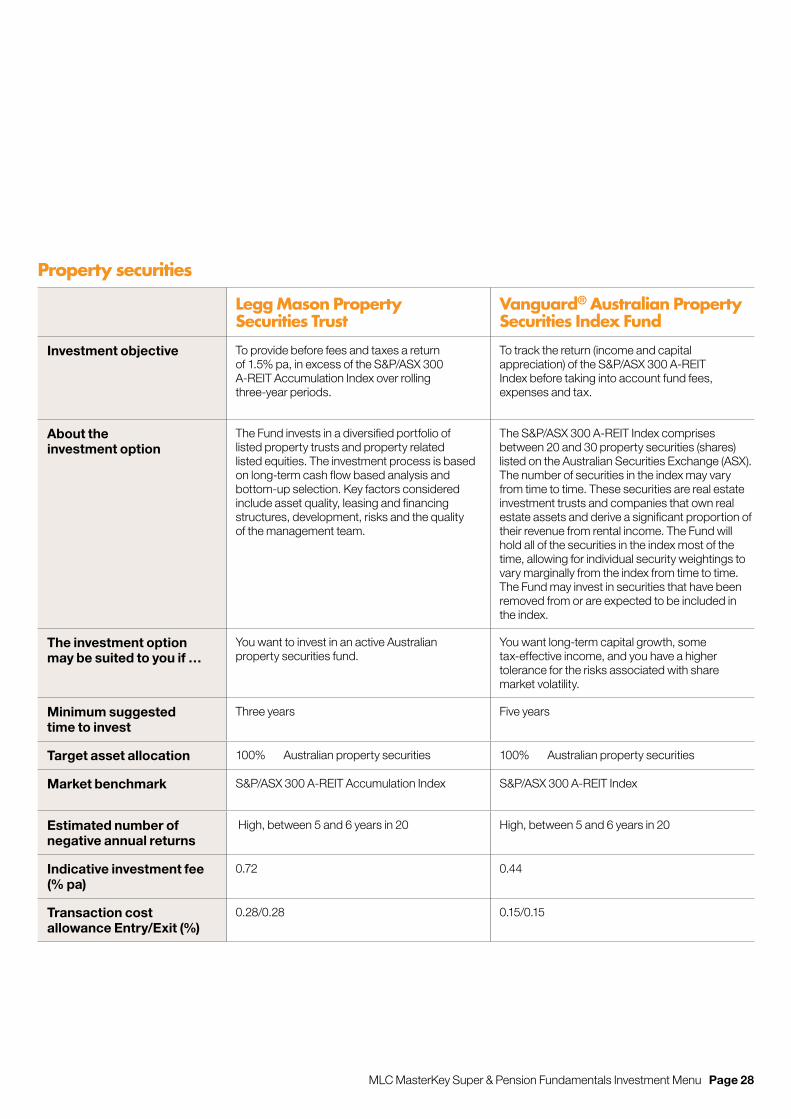

Property securitiesInvesting in property securities will give your portfolio exposure to listed property securities in Australia and around the world. These are referred to as Real Estate Investment Trusts (REITs).

Things to consider:

•Returns are driven by many factors including the economic environment in various countries.

•Australian property securities are dominated by only a few REITs and provide limited diversification.

• Investing outside Australia means you’re exposed to exchange rate variations.

• Property securities may be volatile and are usually included in a portfolio for their income and growth characteristics.

A financial adviser can create a financial plan to help you manage risk and consider issues such as:

•how many years you have to invest

•the savings you’ll need to reach your goals

•the return you may expect from your investments, and

•how comfortable you are with volatility.

Page 5 MLC MasterKey Super & Pension Fundamentals Investment Menu

Things to considerbefore you invest

Australian sharesThis asset class consists of investments in companies listed on the Australian Securities Exchange (and other regulated exchanges). Shares are also known as equities.

Things to consider:

•The Australian share market has recently been dominated by a few industries such as Financials and Resources.

•Australian shares can be volatile and are usually included in a portfolio for their growth characteristics.

• Australian shares may provide dividend income and tax advantages through imputation (franking) credits.

Global sharesGlobal shares consist of investments in companies listed on securities exchanges around the world.

Things to consider:

•The number of potential investments is far greater than in Australian shares.

•Returns are driven by many factors including the economic environment in various countries.

•When you invest globally, you’re less exposed to the risks associated with investing in just one economy.

• Investing outside Australia means you’re exposed to exchange rate variations.

•Global shares can be volatile and are usually included in a portfolio for their growth characteristics.

Private assetsThese are investments in assets that aren’t traded on listed exchanges. An example of this is an investment in a privately owned business.

Things to consider:

•Private assets are illiquid which makes them difficult to buy or sell.

•To access private assets you generally need to do so via a managed fund.

•Because private assets aren’t listed on an exchange, determining their value is difficult and may involve a considerable time lag. This means you need to be careful in interpreting the unit price of any fund with a substantial holding of private assets.

•Returns are driven by many factors including the economic environment in various countries.

•You may be exposed to exchange rate variations.

•Private assets can be volatile and are usually included in a portfolio for their growth characteristics.

Investment techniquesInvestment managers, including MLC, use different investment techniques that can change the value of an investment.

Derivatives are an investment technique generally used in all the investment options.

DerivativesDerivatives are a common tool used to enhance returns or manage risk.

They are contracts that have a value derived from an external reference (eg the level of a share price index).

There are many types of derivatives and they can be an invaluable tool for an investment manager.

However, they can incur significant losses.

MLC’s Derivative Policy, which outlines how we manage derivatives, is available on mlc.com.au

How the other managers invest in derivatives is included in their Product Disclosure Statement available on mlc.com.au

And there are additional investment techniques used in some investment options. Where these techniques are used extensively, we’ve made a note of it from page 10 (under the relevant investment options).

Diversification across asset classes is just one way of managing risk. At MLC, we can diversify across asset classes and investment managers.

Please read more about our investment approach on page 8.

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 6

These include:

Currency managementCurrency management is a form of hedging. If an investment manager invests in assets in other countries, the value will be affected by the exchange rate.

Returns from global investments reflect movements in currency exchange rates (gains and losses), as well as movements in the value of the underlying securities.

Where desired, this can largely be managed through hedging the currency exposure back to Australian dollars.

GearingGearing an investment through borrowing, or leverage by using derivatives, magnifies your exposure to the potential gains and losses and risks of an investment. As a result, you can expect larger fluctuations (both up and down) in the value of your investment (ie increased volatility), compared to the same investment which is not geared. And the less diversified the investment is across asset classes, investment managers and securities, the greater this potential volatility.

When asset values are rising by more than the costs of gearing, a geared investment will generally have a higher return than if it wasn’t geared. In rising markets it can be easy to lose sight of the risk of a fall. Falling values are inevitable from time to time and in a geared investment they are accentuated because exposure to the assets is higher. If the fall is dramatic there can be even more implications for geared investments.

For example, the lender requires the gearing level be maintained below a predetermined limit. If asset values fall dramatically, the gearing level may rise above the limit forcing assets to be sold when values may be continuing to fall.

In turn this could lead to more assets having to be sold and more losses realised. Withdrawals (and applications) may be suspended in such circumstances, preventing you from accessing your investments at a time when values continue to fall.

Although this is an extreme example, significant market falls have occurred in the past. Recovering from such falls can take many years and the geared investment’s unit price may not return to its previous high.

Other circumstances (such as the lender requiring the loan to be repaid for other reasons) may also prevent a geared investment from being managed as planned, leading to losses.

You need to be prepared for all types of environments and understand their impact on your geared investment.

Short-sellingShort-selling is used by an investment manager when it has a view that an asset’s price will fall. The manager borrows the asset and sells it with the intention of buying it back at a lower price. If all goes to plan, a profit is made. However, if the price of the asset increases, then the loss could be significant.

Ethical investingInvestment managers may take into account labour standards, environmental, social or ethical considerations when making decisions to buy or sell investments. At MLC, we expect our active investment managers to consider any material effect these factors may have on the returns from their investments, however we don’t require them to.

How much consideration the other managers give to these factors is included in their Product Disclosure Statement available on mlc.com.au

Want to know more?We’ve developed a lot of information on how we can help you grow and protect your wealth. Just talk to your financial adviser or visit mlc.com.au

Page 7 MLC MasterKey Super & Pension Fundamentals Investment Menu

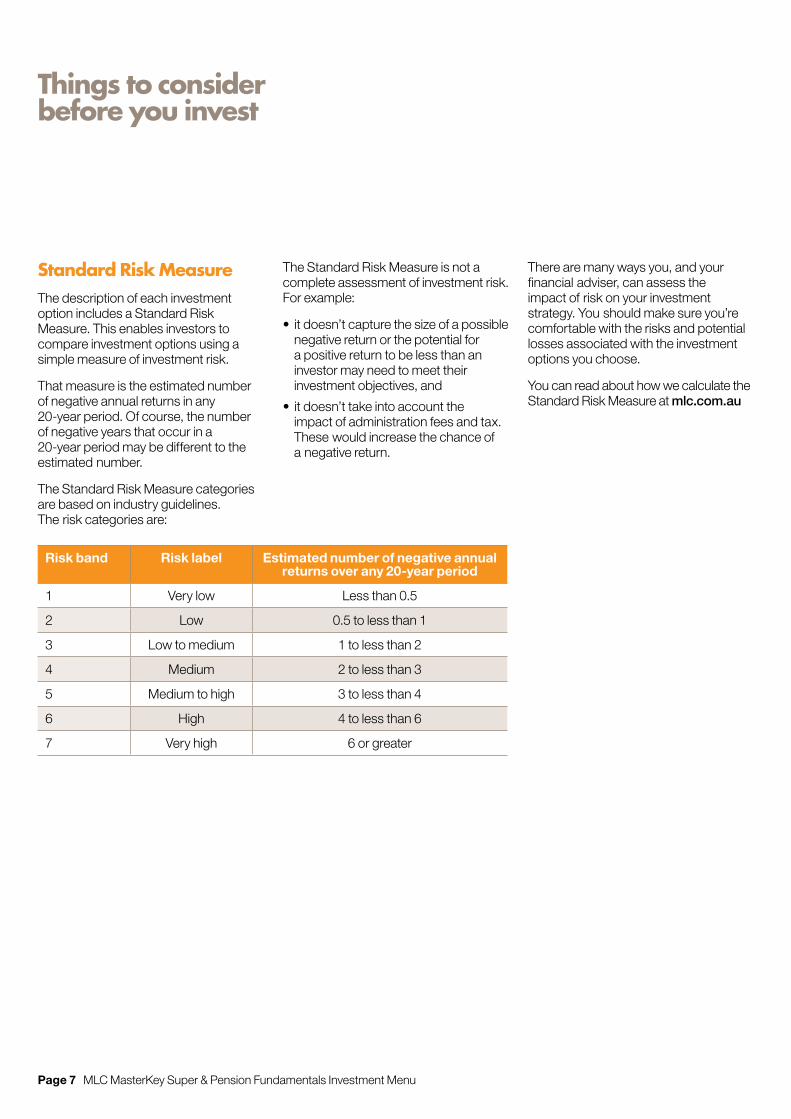

Standard Risk MeasureThe description of each investment option includes a Standard Risk Measure. This enables investors to compare investment options using a simple measure of investment risk.

That measure is the estimated number of negative annual returns in any 20-year period. Of course, the number of negative years that occur in a 20-year period may be different to the estimated number.

The Standard Risk Measure categories are based on industry guidelines. The risk categories are:

The Standard Risk Measure is not a complete assessment of investment risk. For example:

• it doesn’t capture the size of a possible negative return or the potential for a positive return to be less than an investor may need to meet their investment objectives, and

• it doesn’t take into account the impact of administration fees and tax. These would increase the chance of a negative return.

There are many ways you, and your financial adviser, can assess the impact of risk on your investment strategy. You should make sure you’re comfortable with the risks and potential losses associated with the investment options you choose.

You can read about how we calculate the Standard Risk Measure at mlc.com.au

Risk band Risk label Estimated number of negative annual returns over any 20-year period

1 Very low Less than 0.5

2 Low 0.5 to less than 1

3 Low to medium 1 to less than 2

4 Medium 2 to less than 3

5 Medium to high 3 to less than 4

6 High 4 to less than 6

7 Very high 6 or greater

Things to considerbefore you invest

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 8

MLC’s approachto investing

We design investment solutions to deliver more reliable returns to investors.

For over 25 years, we’ve been designing portfolios to help investors achieve their goals.

The four key aspects of our unique investment approach are:

1 Portfolio designOur portfolios focus on what affects investor outcomes the most: asset allocation.

We allocate money between asset classes based on the following beliefs:

Diversification matters Asset classes perform differently in different circumstances, so we invest in many asset classes.

This helps us smooth the overall portfolio returns as we can offset the ups and downs of each asset class.

Risk can’t be avoided, but can be managedEach asset class has its own return and risk characteristics.

This becomes more obvious when you look at performance over a long period of time.

We consider potential market scenarios—both good and bad—to work out what combination of investments is likely to be rewarded.

The process also reveals how risk can change in different market environments.

This helps us prepare our portfolios for future market ups and downs.

Risks and returns vary through time

We have the flexibility to adjust our portfolios to exploit changes in risk and return potential. We base these adjustments on our three to seven-year assessment of the market environment.

2 Managing the portfolio Our portfolios have different investment objectives. That’s why each has a different mix of assets and managers.

Our managers may be specialist in-house managers, external investment managers or a blend.

We research hundreds of investment managers from around the world and select some of the best for our portfolios.

We then combine them in our portfolios so they complement each other.

You can find out about our current investment managers at mlc.com.au

3 Ongoing reviewTo make sure our portfolios are working hard for our investors, we continuously review and actively manage them.

We may adjust the asset allocation, investment strategies and managers.

This may be because our view of the future market environment has altered or because we have found new ways to balance risk and return in the portfolios.

4 Portfolio implementation We deliver better returns by avoiding unnecessary costs. We do this by carefully managing cash flows and changes in our portfolios.

Our knowledge of local tax requirements means our portfolios are sensitive to the needs of Australian investors.

The MLC differenceOur leading-edge approach to portfolio design recognises we live in a complex, changing world.

We constantly explore the many ways events could unfold in markets worldwide and their potential impact on our portfolios.

Through this careful analysis, our experts discover changing risks and opportunities. We can then adjust our portfolios to manage the risks and capture the potential returns.

This means our portfolios are better positioned to deliver more reliable long-term returns to investors.

Page 9 MLC MasterKey Super & Pension Fundamentals Investment Menu

Investingwith MLC

Our portfolios make sophisticated investing straightforward.

We base our portfolios on the fundamental needs of our investors; to grow wealth for the long term.

MLC portfoliosWhen you’re invested in an MLC portfolio, your money is with Australia’s largest and most experienced multi-manager.

Each portfolio uses the MLC approach to investing and benefits from our leading-edge portfolio design process, our manager research capability, and our experience and knowledge of investing.

MLC Horizon Series of portfolios

We designed the MLC Horizon Series of portfolios so you can select an expected risk and return profile to meet your needs.

This comprehensive series of portfolios means, wherever you are in life, you can choose an investment solution to suit you.

Each MLC Horizon portfolio brings together a specific combination of assets and managers and is an easy way to gain access to sophisticated investments. This way you can implement your financial plan with confidence.

MLC asset class portfoliosYou may decide to implement your investment strategy using our asset class portfolios.

These portfolios invest in one asset class and cater for people looking for a complete asset class solution, or a particular investment style.

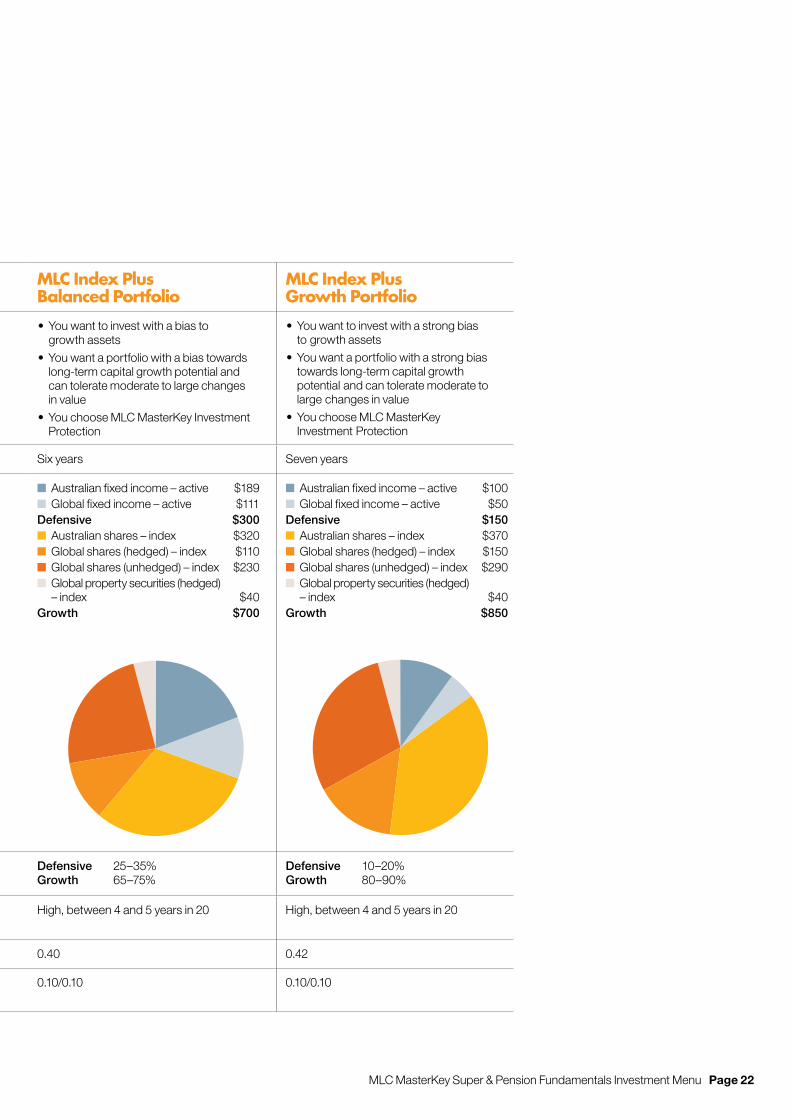

MLC Index Plus portfoliosWe combine our innovative approach to asset allocation with a smaller set of managers in our Index Plus portfolios. These portfolios mainly consist of index managers that aim to provide similar returns to the market.

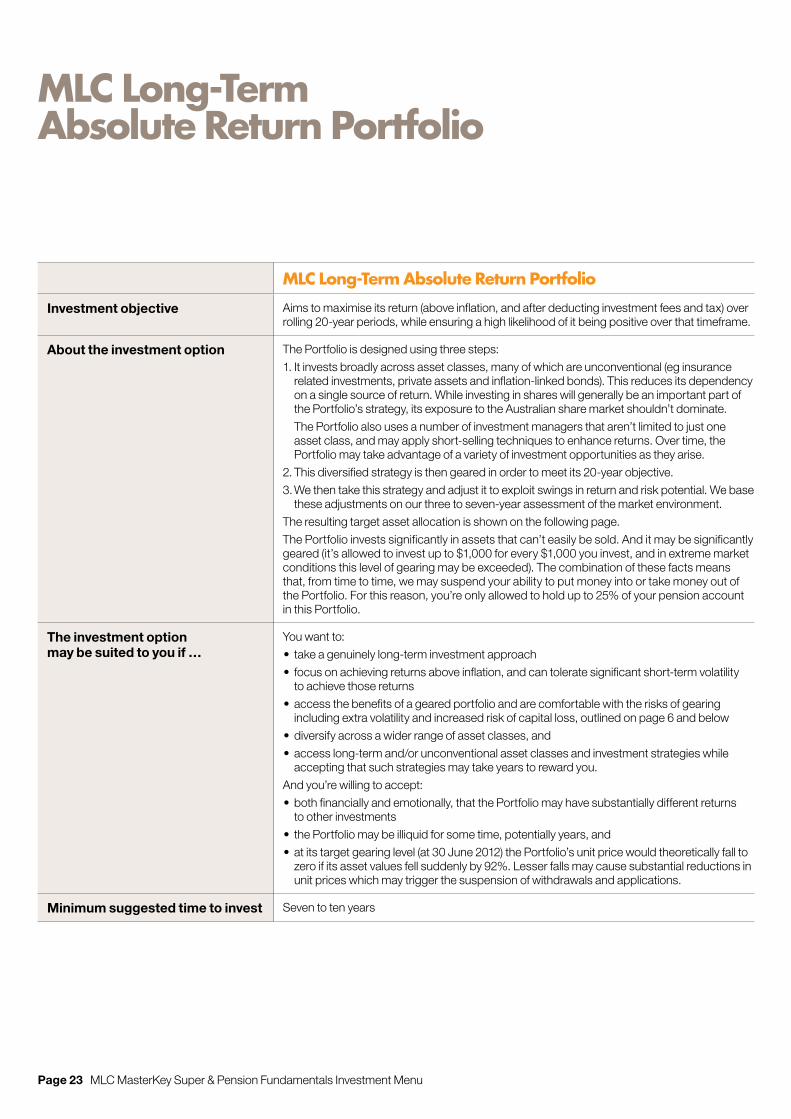

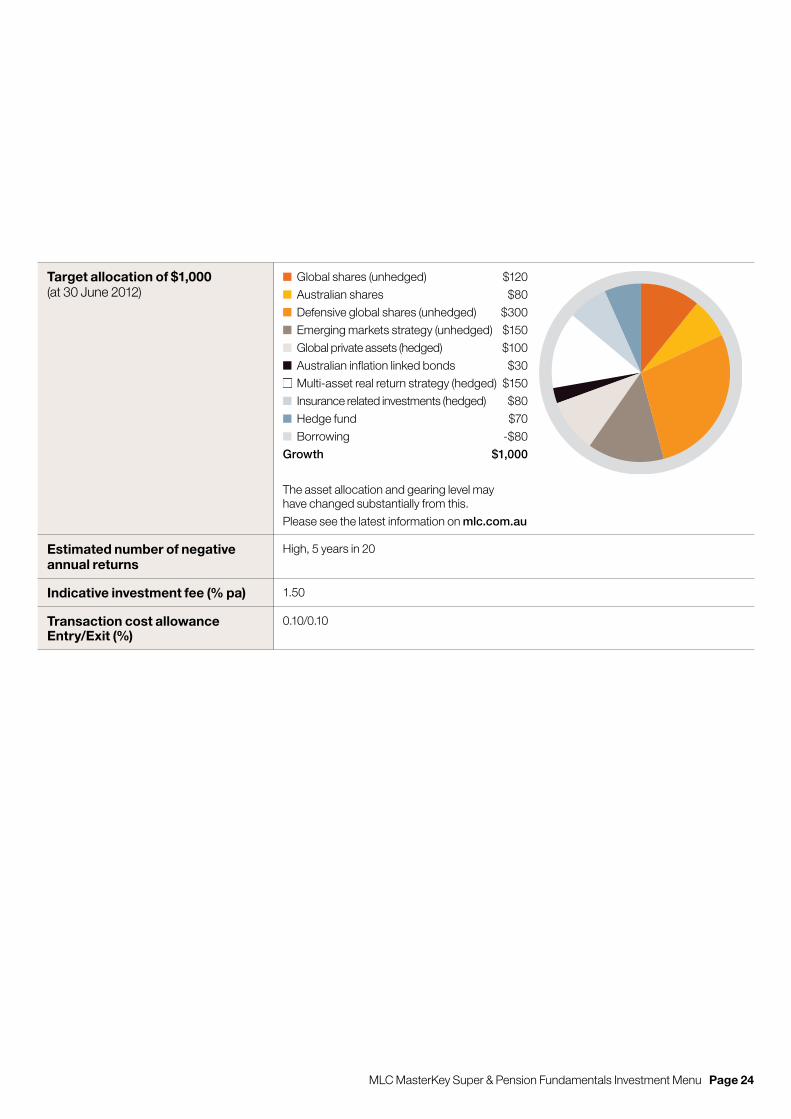

MLC Long-Term Absolute Return Portfolio This portfolio goes beyond conventional investing.

It accesses more sources of return and an even broader range of assets and strategies than the MLC Horizon Series of portfolios.

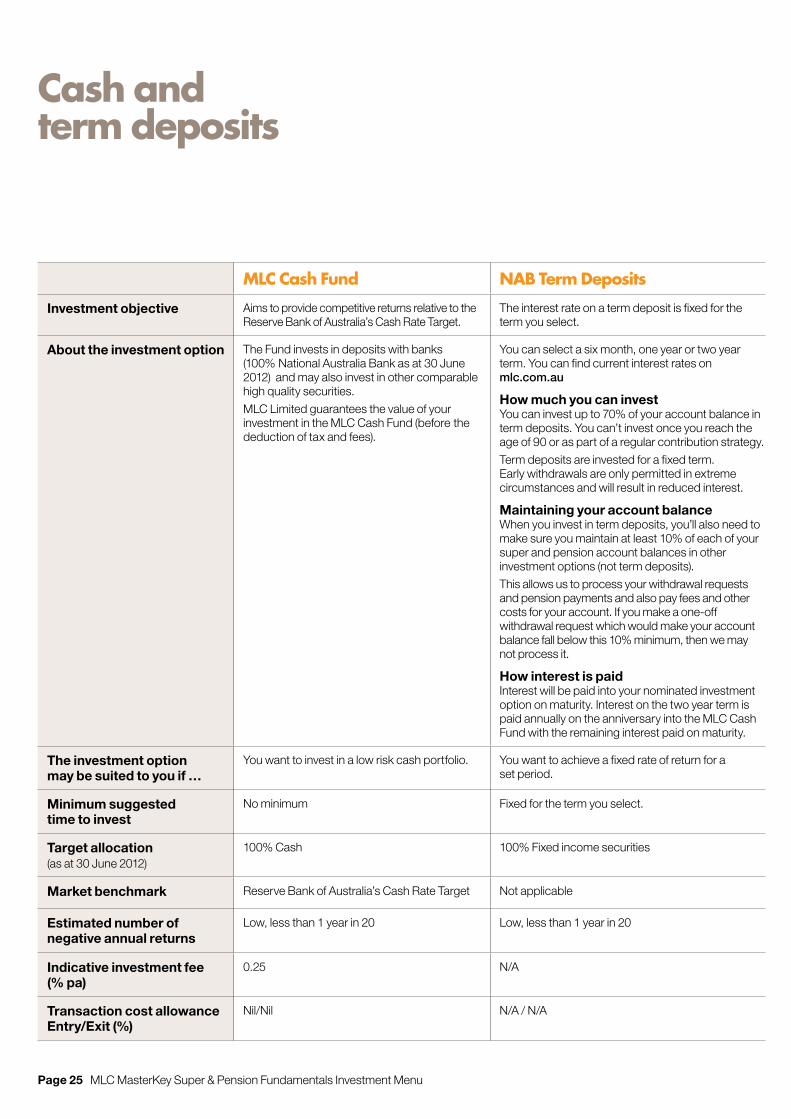

Cash and term depositsWe also offer a range of term deposits and the MLC Cash Fund as a cash option.

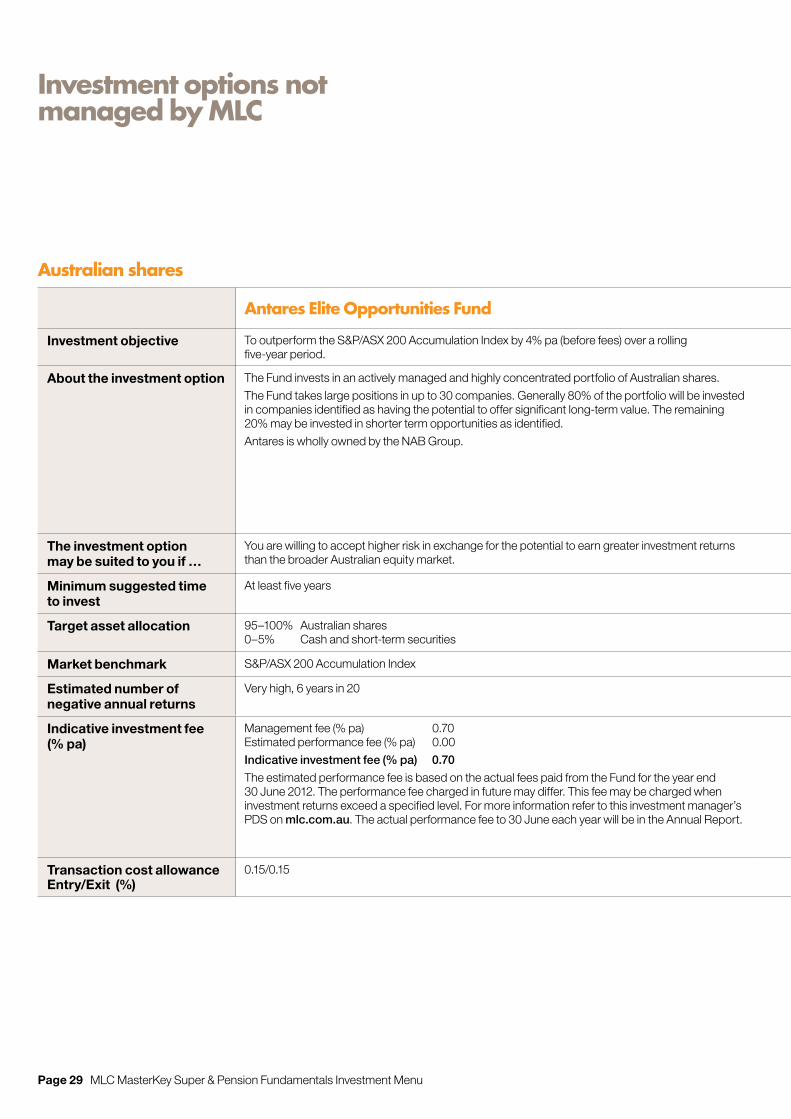

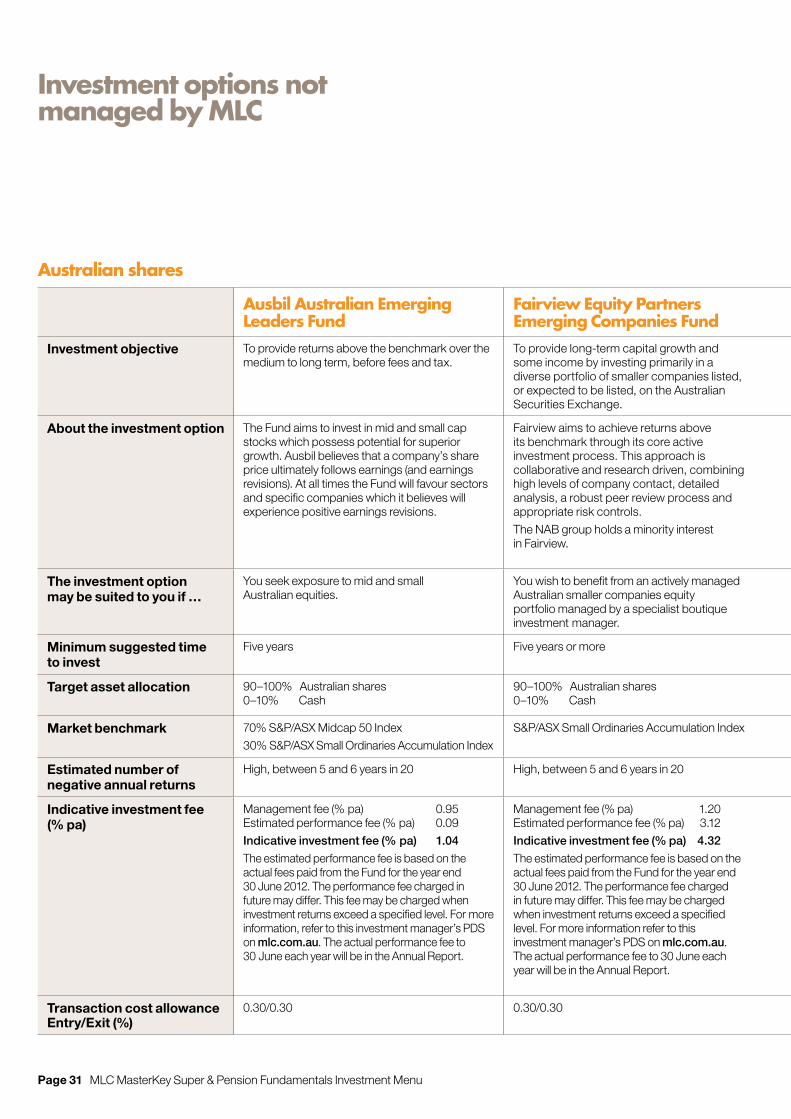

Investment options not managed by MLCWe recognise some investors want extra options when it comes to managing their money.

To help give you this choice, we also offer investment options not managed by MLC.

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 10

MLC Horizon Seriesof portfolios

Investment objectiveEach portfolio aims to grow your wealth for an expected level of risk.

About the investment optionsWhere you are in life, and what your investment goals are, will influence the kind of investment you choose.

We designed the MLC Horizon Series of portfolios with this in mind as each portfolio offers a different risk and return expectation. So whatever your circumstances are now, and as they change over time, you can choose the portfolio to suit your specific needs.

At the lower end of the risk and return potential is MLC Horizon 1. This invests in defensive assets such as fixed income and cash. At the higher end of the risk and return potential is MLC Horizon 7 which gears its investment into growth assets such as shares.

The portfolios use all aspects of our approach to investing described on page 8. They’re actively managed and broadly diversified within asset classes, across asset classes and across investment managers. These managers invest in many companies and securities around the world.

The main asset classes are described on pages 4 and 5.

Page 11 MLC MasterKey Super & Pension Fundamentals Investment Menu

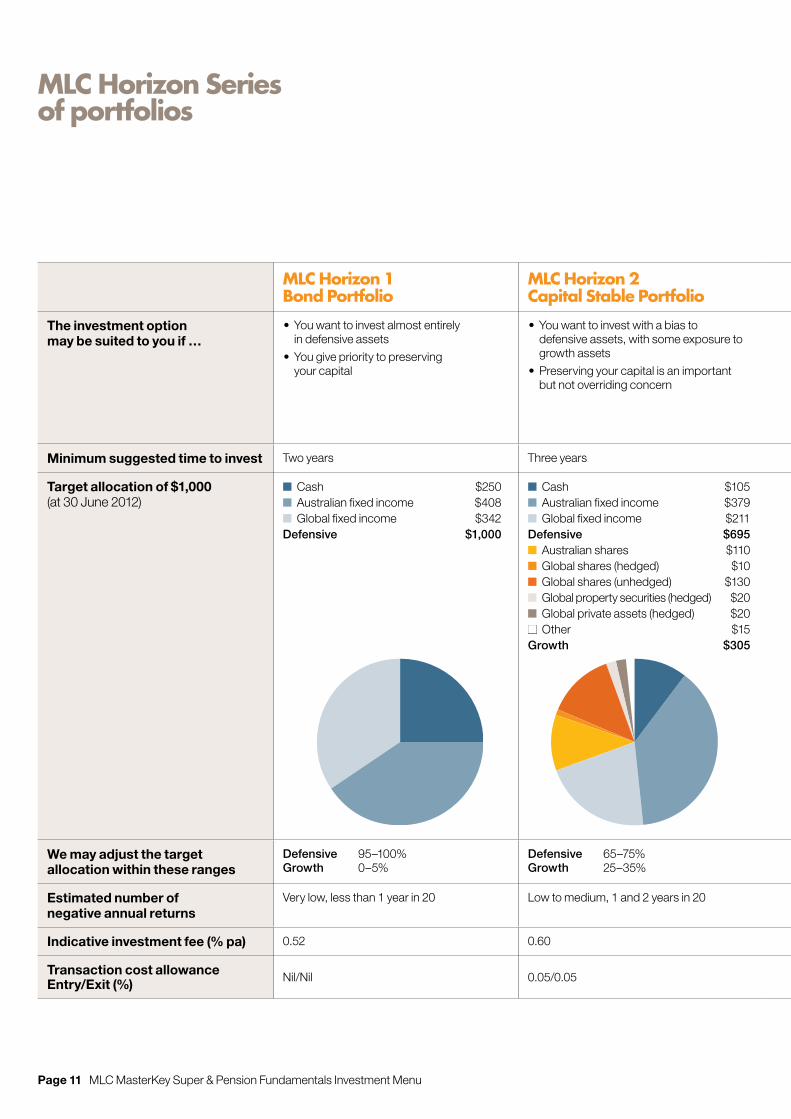

MLC Horizon 1 Bond Portfolio

MLC Horizon 2 Capital Stable Portfolio

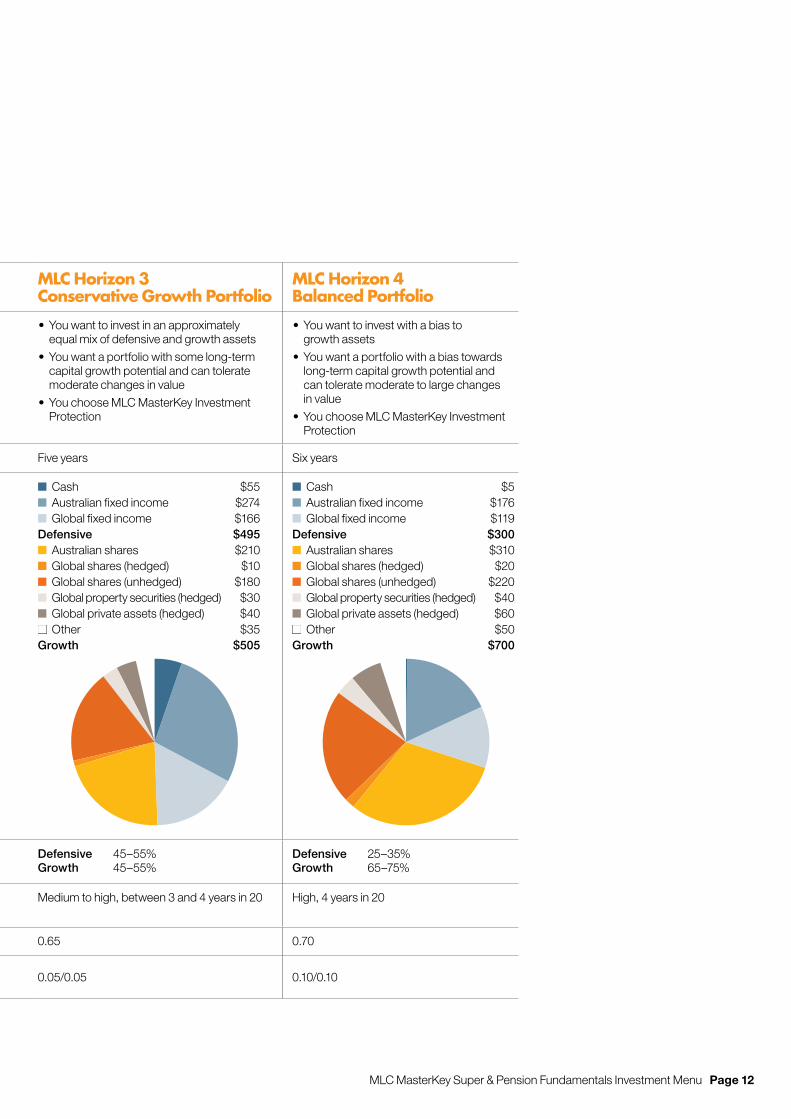

MLC Horizon 3 Conservative Growth Portfolio

MLC Horizon 4 Balanced Portfolio

The investment option may be suited to you if …

•You want to invest almost entirely in defensive assets

•You give priority to preserving your capital

•You want to invest with a bias to defensive assets, with some exposure to growth assets

•Preserving your capital is an important but not overriding concern

•You want to invest in an approximately equal mix of defensive and growth assets

•You want a portfolio with some long-term capital growth potential and can tolerate moderate changes in value

•You choose MLC MasterKey Investment Protection

•You want to invest with a bias to growth assets

•You want a portfolio with a bias towards long-term capital growth potential and can tolerate moderate to large changes in value

•You choose MLC MasterKey Investment Protection

Minimum suggested time to invest Two years Three years Five years Six years

Target allocation of $1,000 (at 30 June 2012)

n Cash $250 n Australian fixed income $408n Global fixed income $342Defensive $1, 000

n Cash $105 n Australian fixed income $379n Global fixed income $211Defensive $695n Australian shares $110n Global shares (hedged) $10n Global shares (unhedged) $130n Global property securities (hedged) $20n Global private assets (hedged) $20n Other $15Growth $305

n Cash $55 n Australian fixed income $274 n Global fixed income $166Defensive $495n Australian shares $210n Global shares (hedged) $10n Global shares (unhedged) $180n Global property securities (hedged) $30n Global private assets (hedged) $40n Other $35Growth $505

n Cash $5 n Australian fixed income $176 n Global fixed income $119Defensive $300n Australian shares $310n Global shares (hedged) $20n Global shares (unhedged) $220n Global property securities (hedged) $40n Global private assets (hedged) $60n Other $50Growth $700

We may adjust the target allocation within these ranges

Defensive 95–100% Growth 0–5%

Defensive 65–75% Growth 25–35%

Defensive 45–55% Growth 45–55%

Defensive 25–35% Growth 65–75%

Estimated number of negative annual returns

Very low, less than 1 year in 20 Low to medium, 1 and 2 years in 20 Medium to high, between 3 and 4 years in 20 High, 4 years in 20

Indicative investment fee (% pa) 0.52 0.60 0.65 0.70

Transaction cost allowance Entry/Exit (%) Nil/Nil 0.05/0.05 0.05/0.05 0.10/0.10

MLC Horizon Seriesof portfolios

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 12

MLC Horizon 1 Bond Portfolio

MLC Horizon 2 Capital Stable Portfolio

MLC Horizon 3 Conservative Growth Portfolio

MLC Horizon 4 Balanced Portfolio

The investment option may be suited to you if …

•You want to invest almost entirely in defensive assets

•You give priority to preserving your capital

•You want to invest with a bias to defensive assets, with some exposure to growth assets

•Preserving your capital is an important but not overriding concern

•You want to invest in an approximately equal mix of defensive and growth assets

•You want a portfolio with some long-term capital growth potential and can tolerate moderate changes in value

•You choose MLC MasterKey Investment Protection

•You want to invest with a bias to growth assets

•You want a portfolio with a bias towards long-term capital growth potential and can tolerate moderate to large changes in value

•You choose MLC MasterKey Investment Protection

Minimum suggested time to invest Two years Three years Five years Six years

Target allocation of $1,000 (at 30 June 2012)

n Cash $250 n Australian fixed income $408n Global fixed income $342Defensive $1, 000

n Cash $105 n Australian fixed income $379n Global fixed income $211Defensive $695n Australian shares $110n Global shares (hedged) $10n Global shares (unhedged) $130n Global property securities (hedged) $20n Global private assets (hedged) $20n Other $15Growth $305

n Cash $55 n Australian fixed income $274 n Global fixed income $166Defensive $495n Australian shares $210n Global shares (hedged) $10n Global shares (unhedged) $180n Global property securities (hedged) $30n Global private assets (hedged) $40n Other $35Growth $505

n Cash $5 n Australian fixed income $176 n Global fixed income $119Defensive $300n Australian shares $310n Global shares (hedged) $20n Global shares (unhedged) $220n Global property securities (hedged) $40n Global private assets (hedged) $60n Other $50Growth $700

We may adjust the target allocation within these ranges

Defensive 95–100% Growth 0–5%

Defensive 65–75% Growth 25–35%

Defensive 45–55% Growth 45–55%

Defensive 25–35% Growth 65–75%

Estimated number of negative annual returns

Very low, less than 1 year in 20 Low to medium, 1 and 2 years in 20 Medium to high, between 3 and 4 years in 20 High, 4 years in 20

Indicative investment fee (% pa) 0.52 0.60 0.65 0.70

Transaction cost allowance Entry/Exit (%) Nil/Nil 0.05/0.05 0.05/0.05 0.10/0.10

Page 13 MLC MasterKey Super & Pension Fundamentals Investment Menu

MLC Horizon Seriesof portfolios

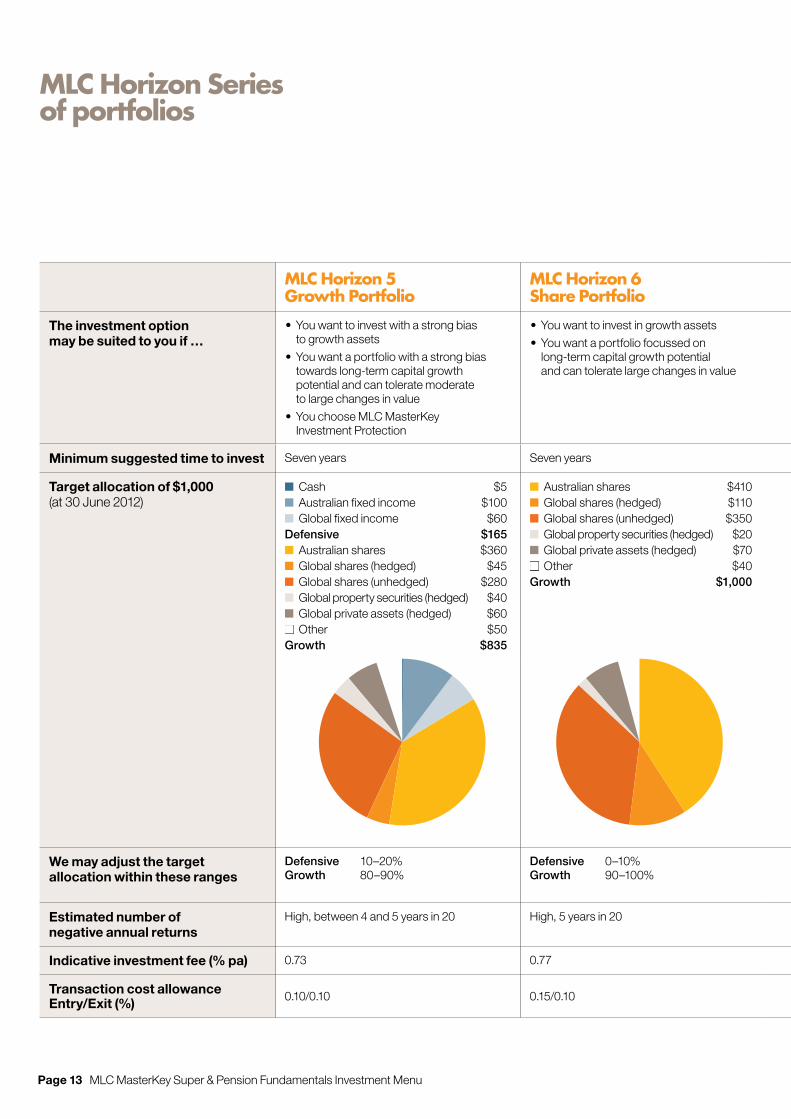

MLC Horizon 5 Growth Portfolio

MLC Horizon 6 Share Portfolio

MLC Horizon 7 Accelerated Growth Portfolio

The investment option may be suited to you if …

•You want to invest with a strong bias to growth assets

•You want a portfolio with a strong bias towards long-term capital growth potential and can tolerate moderate to large changes in value

•You choose MLC MasterKey Investment Protection

•You want to invest in growth assets

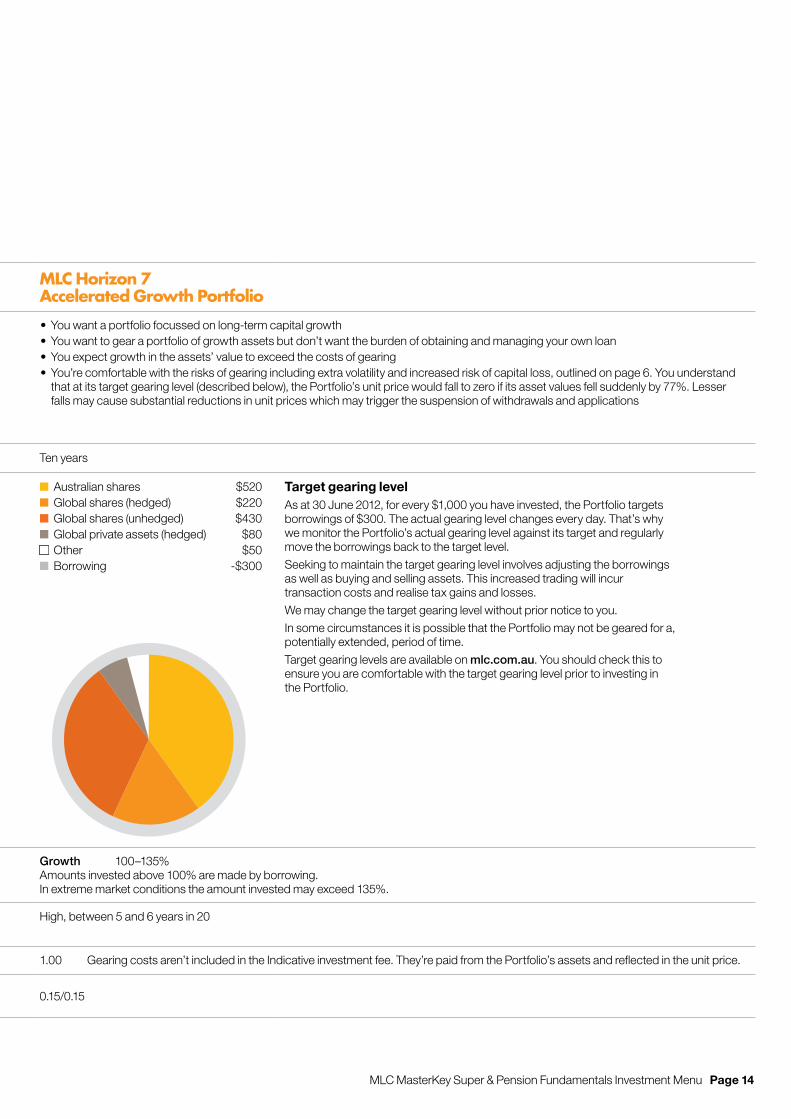

•You want a portfolio focussed on long-term capital growth potential and can tolerate large changes in value

•You want a portfolio focussed on long-term capital growth•You want to gear a portfolio of growth assets but don’t want the burden of obtaining and managing your own loan•You expect growth in the assets’ value to exceed the costs of gearing•You’re comfortable with the risks of gearing including extra volatility and increased risk of capital loss, outlined on page 6. You understand

that at its target gearing level (described below), the Portfolio’s unit price would fall to zero if its asset values fell suddenly by 77%. Lesser falls may cause substantial reductions in unit prices which may trigger the suspension of withdrawals and applications

Minimum suggested time to invest Seven years Seven years Ten years

Target allocation of $1,000 (at 30 June 2012)

n Cash $5 n Australian fixed income $100n Global fixed income $60Defensive $165n Australian shares $360n Global shares (hedged) $45n Global shares (unhedged) $280n Global property securities (hedged) $40n Global private assets (hedged) $60n Other $50Growth $835

n Australian shares $410n Global shares (hedged) $110n Global shares (unhedged) $350n Global property securities (hedged) $20n Global private assets (hedged) $70n Other $40Growth $1,000

n Australian shares $520n Global shares (hedged) $220n Global shares (unhedged) $430n Global private assets (hedged) $80n Other $50n Borrowing -$300

Target gearing levelAs at 30 June 2012, for every $1,000 you have invested, the Portfolio targets borrowings of $300. The actual gearing level changes every day. That’s why we monitor the Portfolio’s actual gearing level against its target and regularly move the borrowings back to the target level.

Seeking to maintain the target gearing level involves adjusting the borrowings as well as buying and selling assets. This increased trading will incur transaction costs and realise tax gains and losses.

We may change the target gearing level without prior notice to you.

In some circumstances it is possible that the Portfolio may not be geared for a, potentially extended, period of time.

Target gearing levels are available on mlc.com.au. You should check this to ensure you are comfortable with the target gearing level prior to investing in the Portfolio.

We may adjust the target allocation within these ranges

Defensive 10–20% Growth 80–90%

Defensive 0–10% Growth 90–100%

Growth 100–135% Amounts invested above 100% are made by borrowing. In extreme market conditions the amount invested may exceed 135%.

Estimated number of negative annual returns

High, between 4 and 5 years in 20 High, 5 years in 20 High, between 5 and 6 years in 20

Indicative investment fee (% pa) 0.73 0.77 1.00 Gearing costs aren’t included in the Indicative investment fee. They’re paid from the Portfolio’s assets and reflected in the unit price.

Transaction cost allowance Entry/Exit (%) 0.10/0.10 0.15/0.10 0.15/0.15

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 14

MLC Horizon 5 Growth Portfolio

MLC Horizon 6 Share Portfolio

MLC Horizon 7 Accelerated Growth Portfolio

The investment option may be suited to you if …

•You want to invest with a strong bias to growth assets

•You want a portfolio with a strong bias towards long-term capital growth potential and can tolerate moderate to large changes in value

•You choose MLC MasterKey Investment Protection

•You want to invest in growth assets

•You want a portfolio focussed on long-term capital growth potential and can tolerate large changes in value

•You want a portfolio focussed on long-term capital growth•You want to gear a portfolio of growth assets but don’t want the burden of obtaining and managing your own loan•You expect growth in the assets’ value to exceed the costs of gearing•You’re comfortable with the risks of gearing including extra volatility and increased risk of capital loss, outlined on page 6. You understand

that at its target gearing level (described below), the Portfolio’s unit price would fall to zero if its asset values fell suddenly by 77%. Lesser falls may cause substantial reductions in unit prices which may trigger the suspension of withdrawals and applications

Minimum suggested time to invest Seven years Seven years Ten years

Target allocation of $1,000 (at 30 June 2012)

n Cash $5 n Australian fixed income $100n Global fixed income $60Defensive $165n Australian shares $360n Global shares (hedged) $45n Global shares (unhedged) $280n Global property securities (hedged) $40n Global private assets (hedged) $60n Other $50Growth $835

n Australian shares $410n Global shares (hedged) $110n Global shares (unhedged) $350n Global property securities (hedged) $20n Global private assets (hedged) $70n Other $40Growth $1,000

n Australian shares $520n Global shares (hedged) $220n Global shares (unhedged) $430n Global private assets (hedged) $80n Other $50n Borrowing -$300

Target gearing levelAs at 30 June 2012, for every $1,000 you have invested, the Portfolio targets borrowings of $300. The actual gearing level changes every day. That’s why we monitor the Portfolio’s actual gearing level against its target and regularly move the borrowings back to the target level.

Seeking to maintain the target gearing level involves adjusting the borrowings as well as buying and selling assets. This increased trading will incur transaction costs and realise tax gains and losses.

We may change the target gearing level without prior notice to you.

In some circumstances it is possible that the Portfolio may not be geared for a, potentially extended, period of time.

Target gearing levels are available on mlc.com.au. You should check this to ensure you are comfortable with the target gearing level prior to investing in the Portfolio.

We may adjust the target allocation within these ranges

Defensive 10–20% Growth 80–90%

Defensive 0–10% Growth 90–100%

Growth 100–135% Amounts invested above 100% are made by borrowing. In extreme market conditions the amount invested may exceed 135%.

Estimated number of negative annual returns

High, between 4 and 5 years in 20 High, 5 years in 20 High, between 5 and 6 years in 20

Indicative investment fee (% pa) 0.73 0.77 1.00 Gearing costs aren’t included in the Indicative investment fee. They’re paid from the Portfolio’s assets and reflected in the unit price.

Transaction cost allowance Entry/Exit (%) 0.10/0.10 0.15/0.10 0.15/0.15

Page 15 MLC MasterKey Super & Pension Fundamentals Investment Menu

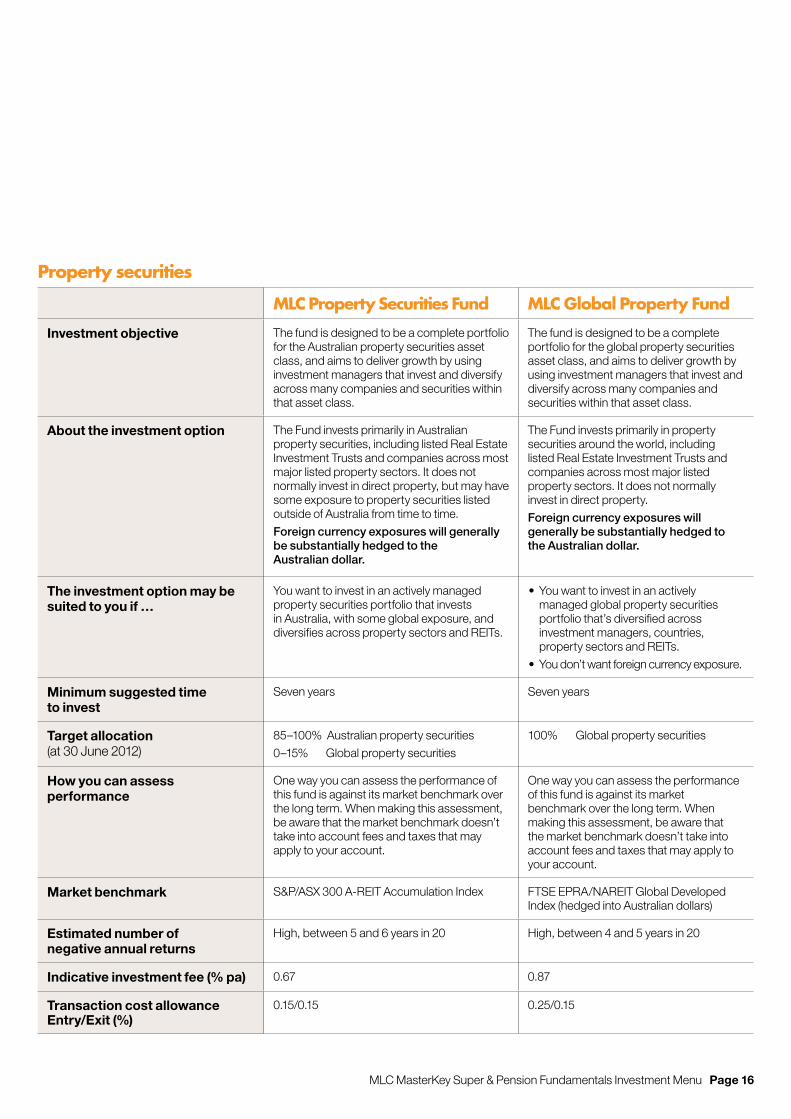

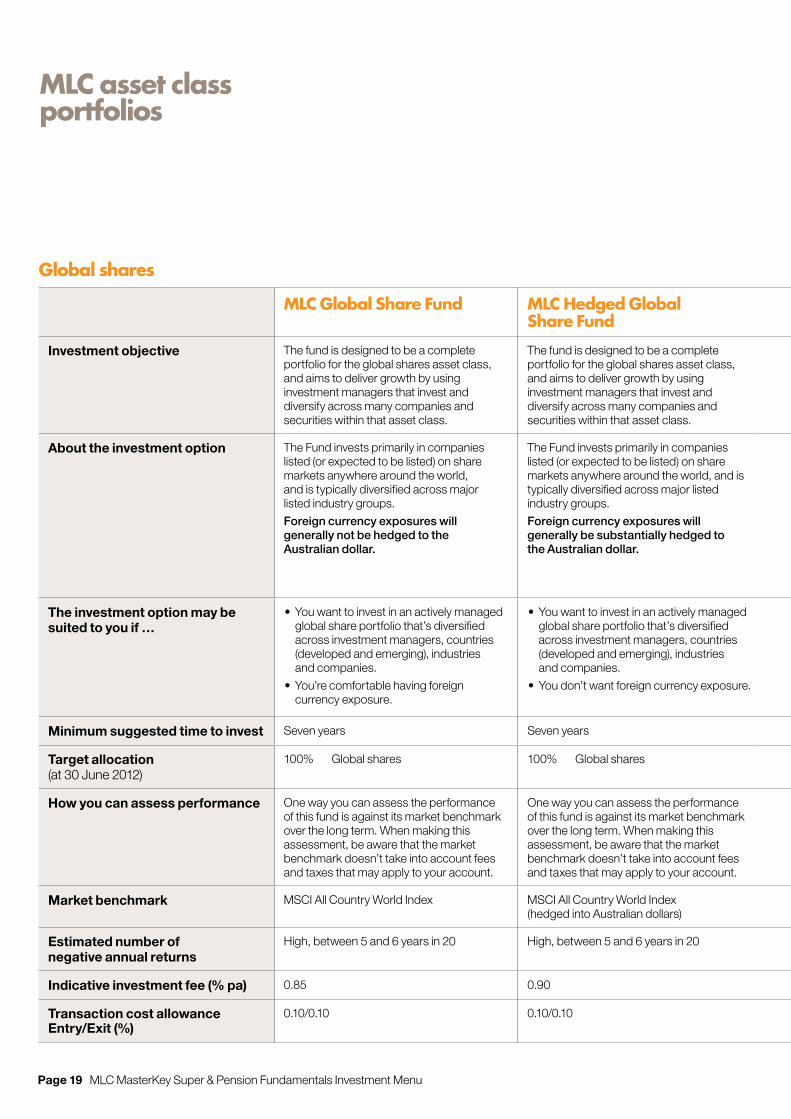

MLC asset class portfolios

Fixed income Property securities

MLC Diversified Debt Fund MLC Property Securities Fund MLC Global Property Fund

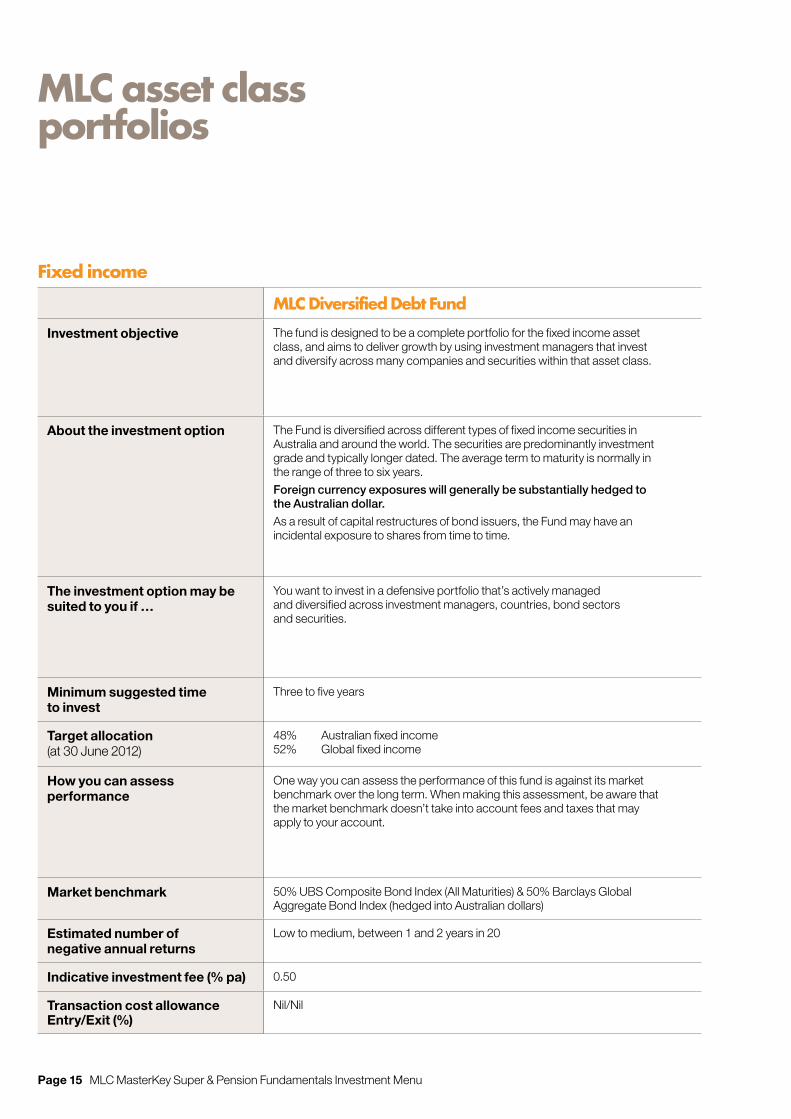

Investment objective The fund is designed to be a complete portfolio for the fixed income asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

Investment objective The fund is designed to be a complete portfolio for the Australian property securities asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

The fund is designed to be a complete portfolio for the global property securities asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

About the investment option The Fund is diversified across different types of fixed income securities in Australia and around the world. The securities are predominantly investment grade and typically longer dated. The average term to maturity is normally in the range of three to six years.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

As a result of capital restructures of bond issuers, the Fund may have an incidental exposure to shares from time to time.

About the investment option The Fund invests primarily in Australian property securities, including listed Real Estate Investment Trusts and companies across most major listed property sectors. It does not normally invest in direct property, but may have some exposure to property securities listed outside of Australia from time to time.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

The Fund invests primarily in property securities around the world, including listed Real Estate Investment Trusts and companies across most major listed property sectors. It does not normally invest in direct property.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

The investment option may be suited to you if …

You want to invest in a defensive portfolio that’s actively managed and diversified across investment managers, countries, bond sectors and securities.

The investment option may be suited to you if …

You want to invest in an actively managed property securities portfolio that invests in Australia, with some global exposure, and diversifies across property sectors and REITs.

•You want to invest in an actively managed global property securities portfolio that’s diversified across investment managers, countries, property sectors and REITs.

•You don’t want foreign currency exposure.

Minimum suggested time to invest

Three to five years Minimum suggested time to invest

Seven years Seven years

Target allocation (at 30 June 2012)

48% Australian fixed income52% Global fixed income

Target allocation (at 30 June 2012)

85–100% Australian property securities

0–15% Global property securities

100% Global property securities

How you can assess performance

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

How you can assess performance

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

Market benchmark 50% UBS Composite Bond Index (All Maturities) & 50% Barclays Global Aggregate Bond Index (hedged into Australian dollars)

Market benchmark S&P/ASX 300 A-REIT Accumulation Index FTSE EPRA/NAREIT Global Developed Index (hedged into Australian dollars)

Estimated number of negative annual returns

Low to medium, between 1 and 2 years in 20 Estimated number of negative annual returns

High, between 5 and 6 years in 20 High, between 4 and 5 years in 20

Indicative investment fee (% pa) 0.50 Indicative investment fee (% pa) 0.67 0.87

Transaction cost allowance Entry/Exit (%)

Nil/Nil Transaction cost allowance Entry/Exit (%)

0.15/0.15 0.25/0.15

MLC MasterKey Super & Pension Fundamentals Investment Menu Page 16

Fixed income Property securities

MLC Diversified Debt Fund MLC Property Securities Fund MLC Global Property Fund

Investment objective The fund is designed to be a complete portfolio for the fixed income asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

Investment objective The fund is designed to be a complete portfolio for the Australian property securities asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

The fund is designed to be a complete portfolio for the global property securities asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.

About the investment option The Fund is diversified across different types of fixed income securities in Australia and around the world. The securities are predominantly investment grade and typically longer dated. The average term to maturity is normally in the range of three to six years.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

As a result of capital restructures of bond issuers, the Fund may have an incidental exposure to shares from time to time.

About the investment option The Fund invests primarily in Australian property securities, including listed Real Estate Investment Trusts and companies across most major listed property sectors. It does not normally invest in direct property, but may have some exposure to property securities listed outside of Australia from time to time.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

The Fund invests primarily in property securities around the world, including listed Real Estate Investment Trusts and companies across most major listed property sectors. It does not normally invest in direct property.

Foreign currency exposures will generally be substantially hedged to the Australian dollar.

The investment option may be suited to you if …

You want to invest in a defensive portfolio that’s actively managed and diversified across investment managers, countries, bond sectors and securities.

The investment option may be suited to you if …

You want to invest in an actively managed property securities portfolio that invests in Australia, with some global exposure, and diversifies across property sectors and REITs.

•You want to invest in an actively managed global property securities portfolio that’s diversified across investment managers, countries, property sectors and REITs.

•You don’t want foreign currency exposure.

Minimum suggested time to invest

Three to five years Minimum suggested time to invest

Seven years Seven years

Target allocation (at 30 June 2012)

48% Australian fixed income52% Global fixed income

Target allocation (at 30 June 2012)

85–100% Australian property securities

0–15% Global property securities

100% Global property securities

How you can assess performance

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

How you can assess performance

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

One way you can assess the performance of this fund is against its market benchmark over the long term. When making this assessment, be aware that the market benchmark doesn’t take into account fees and taxes that may apply to your account.

Market benchmark 50% UBS Composite Bond Index (All Maturities) & 50% Barclays Global Aggregate Bond Index (hedged into Australian dollars)

Market benchmark S&P/ASX 300 A-REIT Accumulation Index FTSE EPRA/NAREIT Global Developed Index (hedged into Australian dollars)

Estimated number of negative annual returns

Low to medium, between 1 and 2 years in 20 Estimated number of negative annual returns

High, between 5 and 6 years in 20 High, between 4 and 5 years in 20

Indicative investment fee (% pa) 0.50 Indicative investment fee (% pa) 0.67 0.87

Transaction cost allowance Entry/Exit (%)

Nil/Nil Transaction cost allowance Entry/Exit (%)

0.15/0.15 0.25/0.15

Page 17 MLC MasterKey Super & Pension Fundamentals Investment Menu

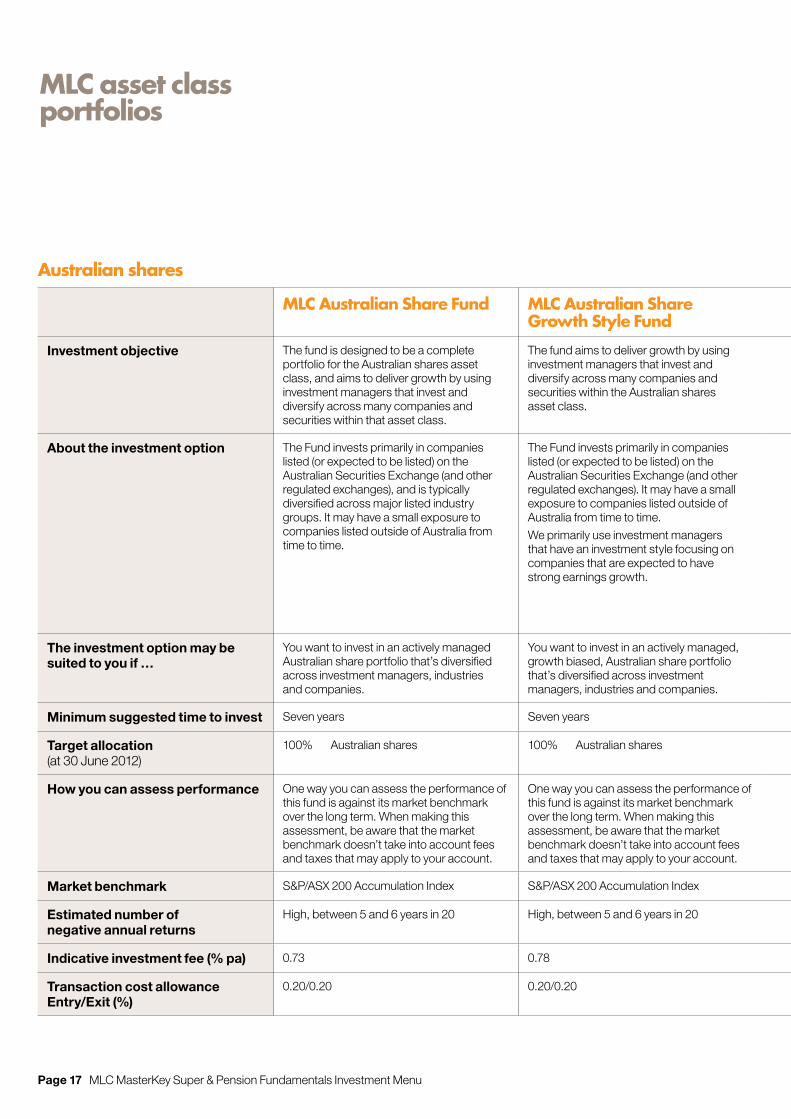

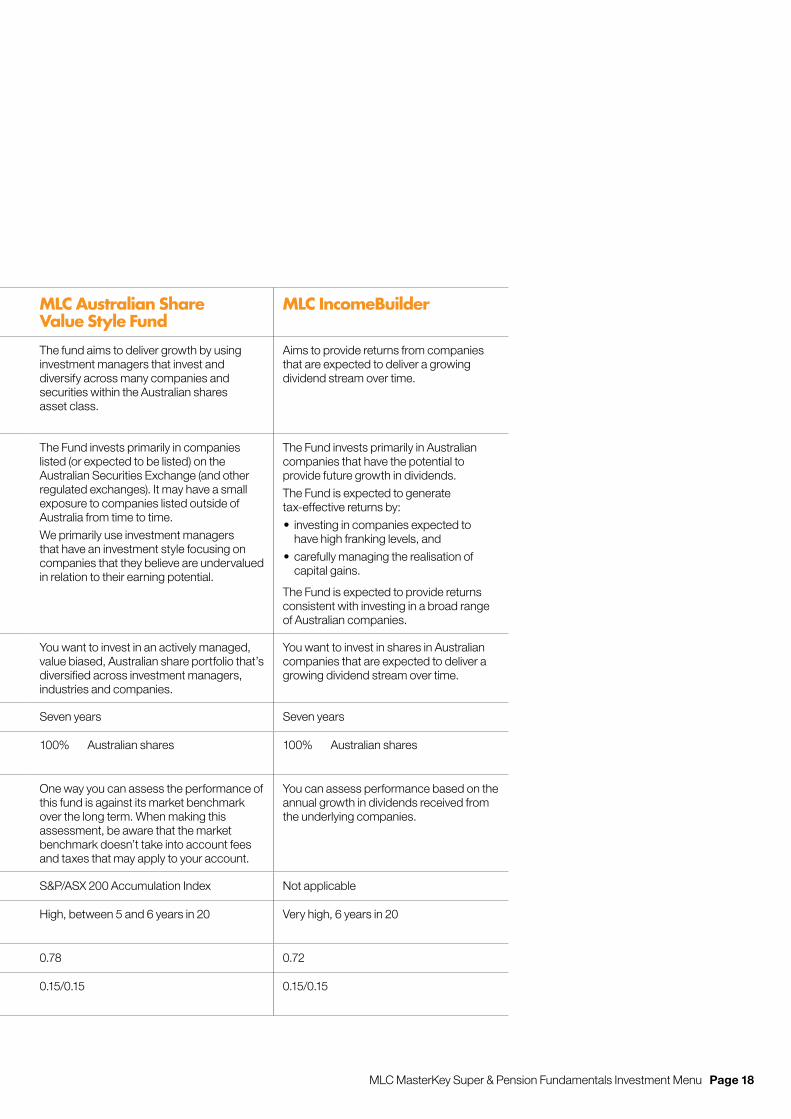

Australian shares

MLC Australian Share Fund MLC Australian Share Growth Style Fund

MLC Australian Share Value Style Fund

MLC IncomeBuilder

Investment objective The fund is designed to be a complete portfolio for the Australian shares asset class, and aims to deliver growth by using investment managers that invest and diversify across many companies and securities within that asset class.