Languages

Pages

Legal

AllianceBernstein® and the AB AllianceBernstein logo are trademarks and service marks owned by AllianceBernstein L.P.

Merrill Lynch Banking & Financial Services Conference

November 12, 2008

David SteynExecutive Vice President

Global Head of Client Service and Marketing

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein1

Cautions regarding Forward-Looking StatementsCertain statements provided by management in this presentation are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks, uncertainties, and other factors that could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. The most significant of these factors include, but are not limited to, the following: the performance of financial markets, the investment performance of sponsored investment products and separately managed accounts, general economic conditions, future acquisitions, competitive conditions, and government regulations, including changes in tax regulations and rates and the manner in which the earnings of publicly traded partnerships are taxed. We caution readers to carefully consider such factors. Further, such forward-looking statements speak only as of the date on which such statements are made; we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements. For further information regarding these forward-looking statements and the factors that could cause actual results to differ, see “Risk Factors” in Part I, Item 1A of our Form 10-K for the year ended December 31, 2007 and Part II, Item 1A of our Form 10-Q for the quarter ended September 30, 2008. Any or all of the forward-looking statements that we make in this presentation, Form 10-K, Form 10-Q, other documents we file with or furnish to the SEC, or any other public statements we issue, may turn out to be wrong. It is important to remember that other factors besides those listed in “Risk Factors”and those listed above could also adversely affect our revenues, financial condition, results of operations, and business prospects.

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein2

We improve investor outcomes by our actions and those of our partners

We do so profitably and sustainably

”

This is a good time for rigour, to look at what you want to come out with at the other end of the tunnel. This is not a time to skimp on resources but to focus them on your best businesses: stop the weakest, invest in the strongest.

Jack WelchFinancial Times–July 26, 2008

“

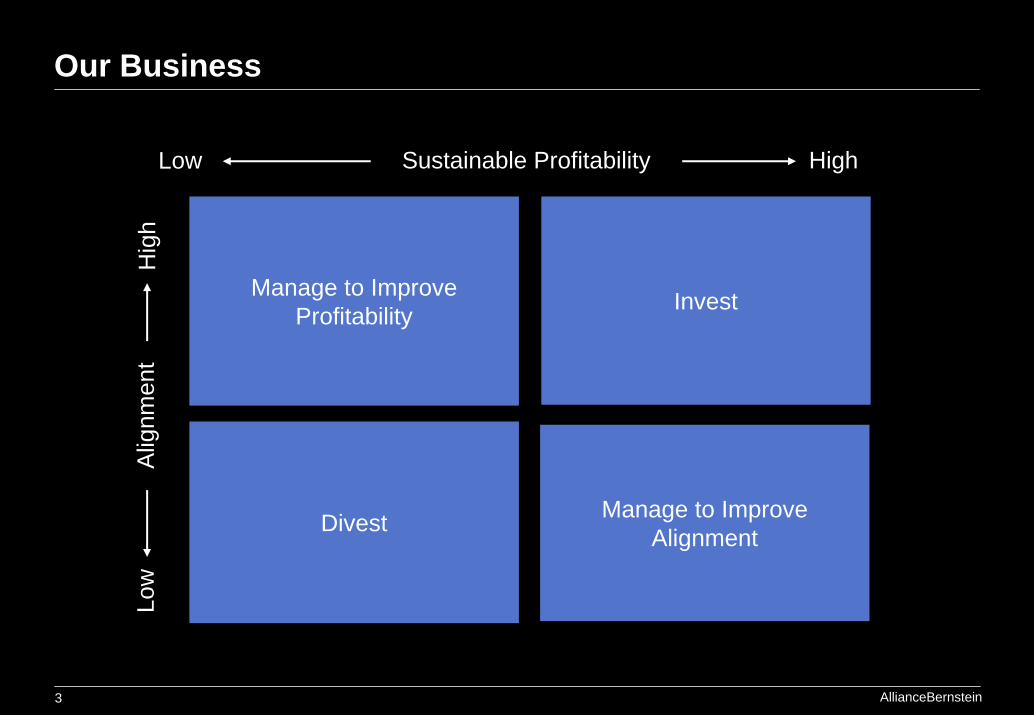

Our Best Businesses are (or will be) ones where:

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein3

Our Business

Invest

Sustainable Profitability HighLowA

lignm

ent

Hig

hLo

w

Manage to Improve Profitability

Divest Manage to Improve Alignment

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein4

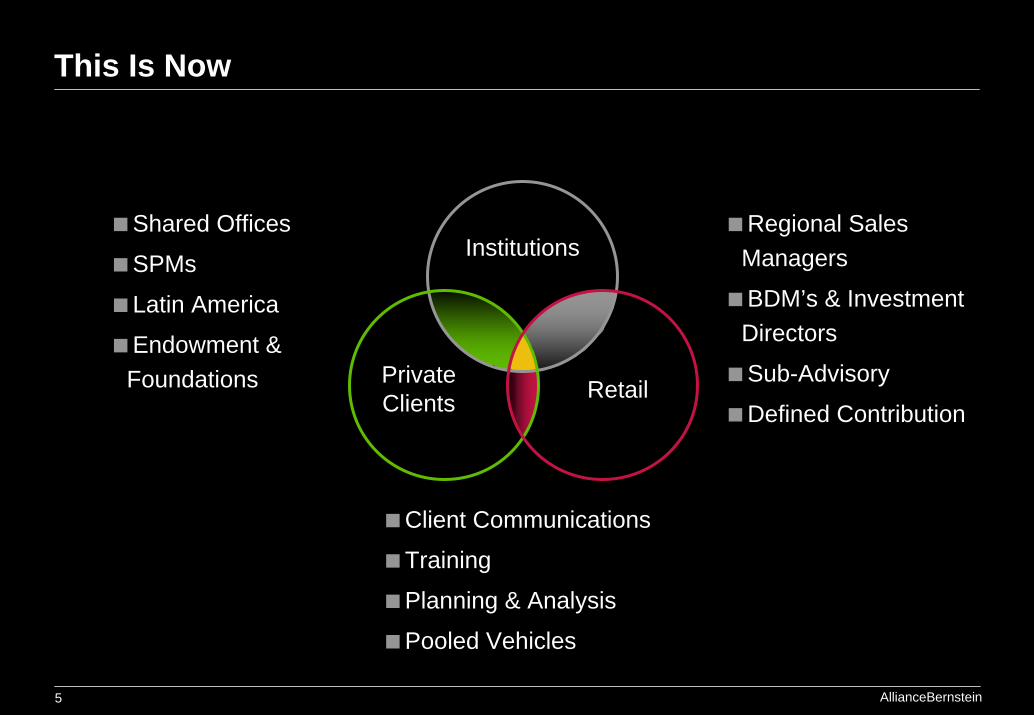

Institutions

PrivateClients Retail

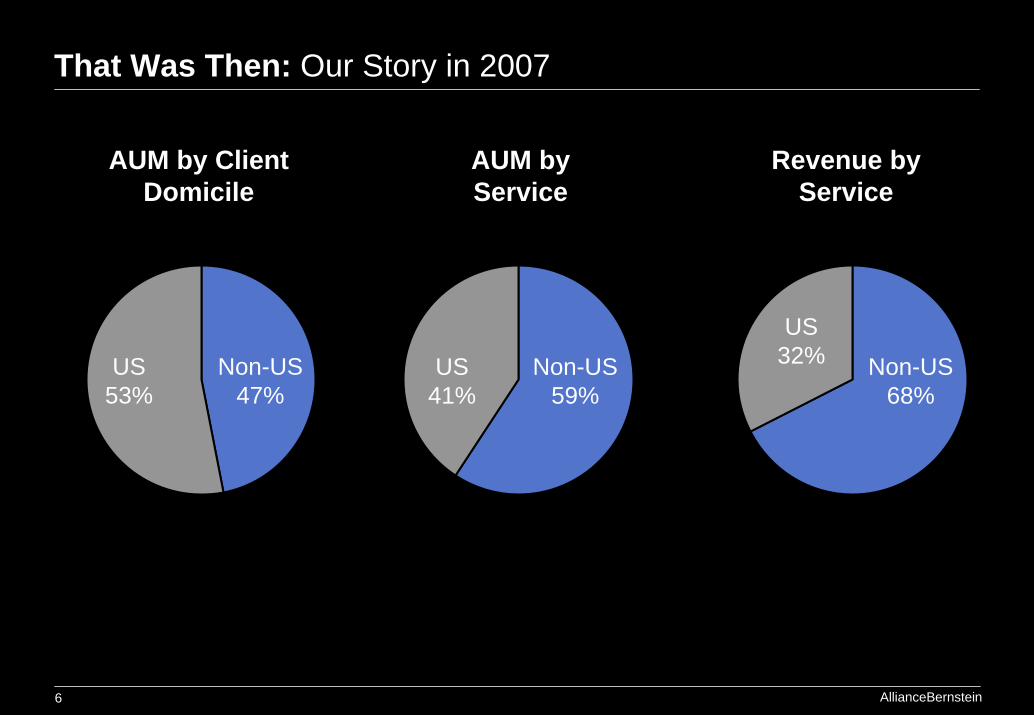

That Was Then

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein5

Shared Offices

SPMs

Latin America

Endowment & Foundations

This Is Now

Client Communications

Training

Planning & Analysis

Pooled Vehicles

Regional Sales Managers

BDM’s & Investment Directors

Sub-Advisory

Defined ContributionPrivateClients

Institutions

Retail

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein6

AUM by Service

Revenue by Service

AUM by Client Domicile

Non-US47%

US53%

That Was Then: Our Story in 2007

Non-US59%

US41%

Non-US68%

US32%

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein7

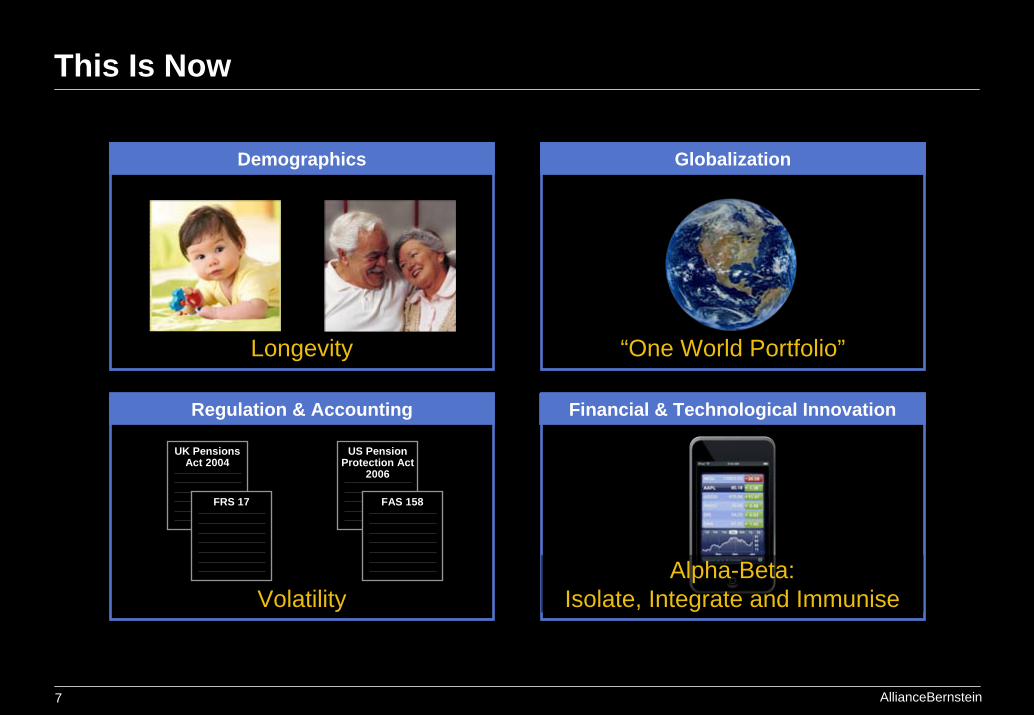

This Is Now

Demographics Globalization

US Pension Protection Act

2006

FAS 158

UK Pensions Act 2004

FRS 17

Regulation & Accounting Financial & Technological Innovation

“One World Portfolio”

Alpha-Beta:Isolate, Integrate and ImmuniseVolatility

Longevity

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein8

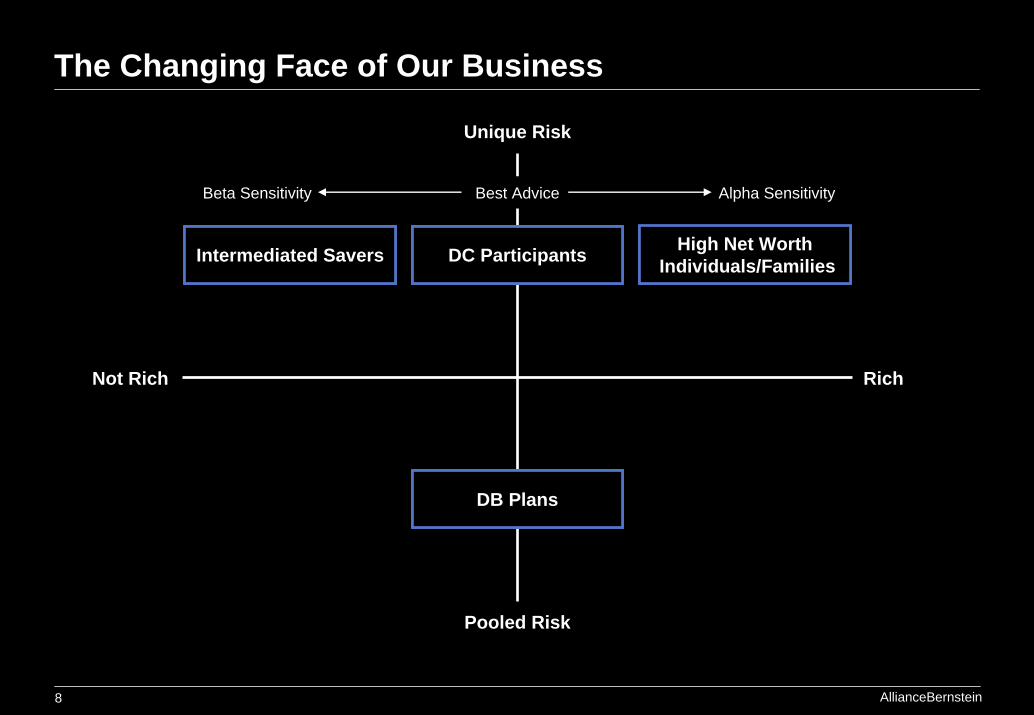

The Changing Face of Our Business

Unique Risk

Pooled Risk

Not Rich Rich

High Net WorthIndividuals/FamiliesIntermediated Savers DC Participants

DB Plans

Beta Sensitivity Alpha SensitivityBest Advice

High Net WorthIndividuals/FamiliesIntermediated Savers DC Participants

DB Plans

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein9

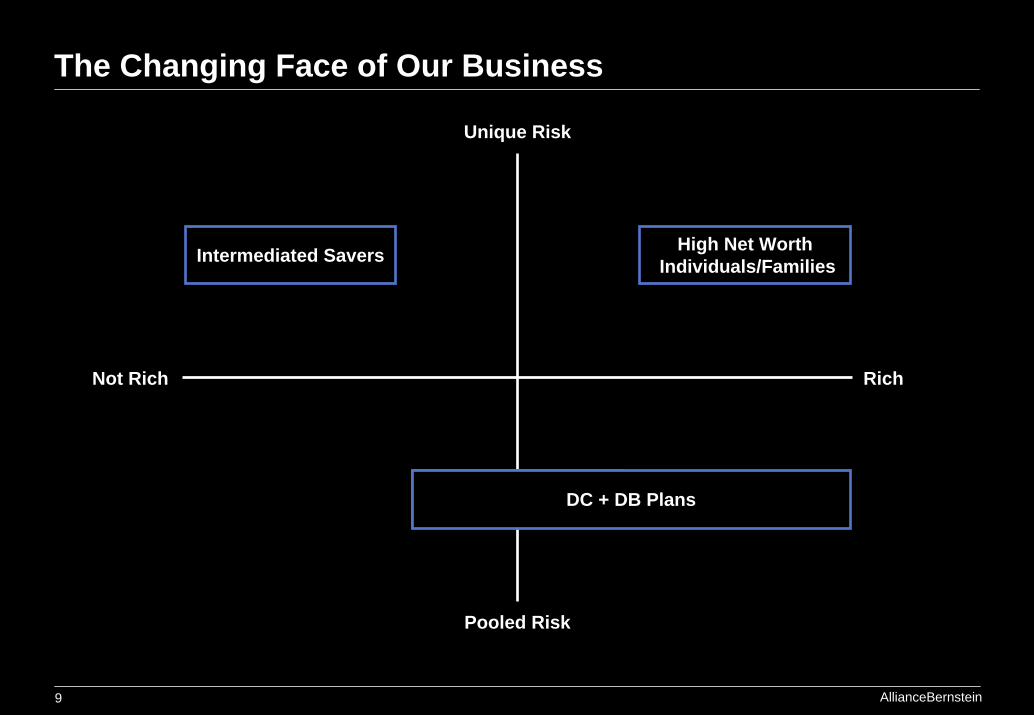

Not Rich

Unique Risk

Pooled Risk

Rich

High Net WorthIndividuals/Families

The Changing Face of Our Business

Intermediated Savers

DB Plans DC + DB Plans

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein10

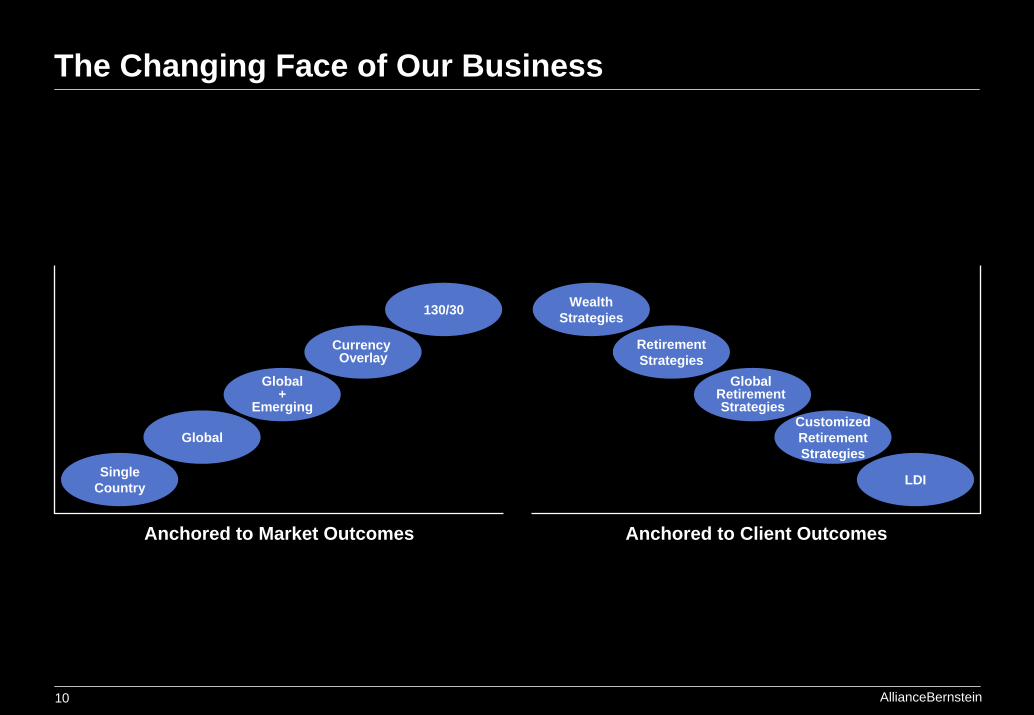

The Changing Face of Our Business

Source Alpha Platforms Assembled Advice Platforms

Anchored to Market Outcomes

Global

SingleCountry

Global+

Emerging

130/30

Currency Overlay

Anchored to Client Outcomes

CustomizedRetirementStrategies

LDI

RetirementStrategies

WealthStrategies

Global Retirement Strategies

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein11

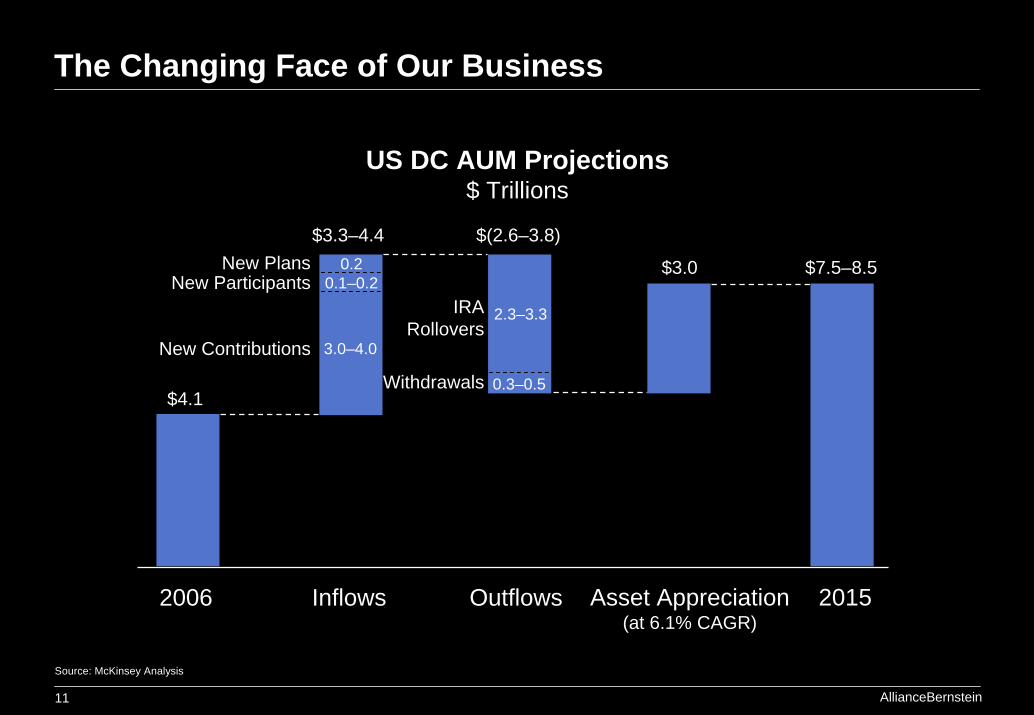

Source: McKinsey Analysis

US DC AUM Projections$ Trillions

2006

$4.1

Asset Appreciation (at 6.1% CAGR)

$3.0

2015

$7.5–8.5

Inflows

$3.3–4.4

3.0–4.0

0.20.1–0.2

New PlansNew Participants

New Contributions

Outflows

$(2.6–3.8)

0.3–0.5

2.3–3.3IRA Rollovers

Withdrawals

The Changing Face of Our Business

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein12

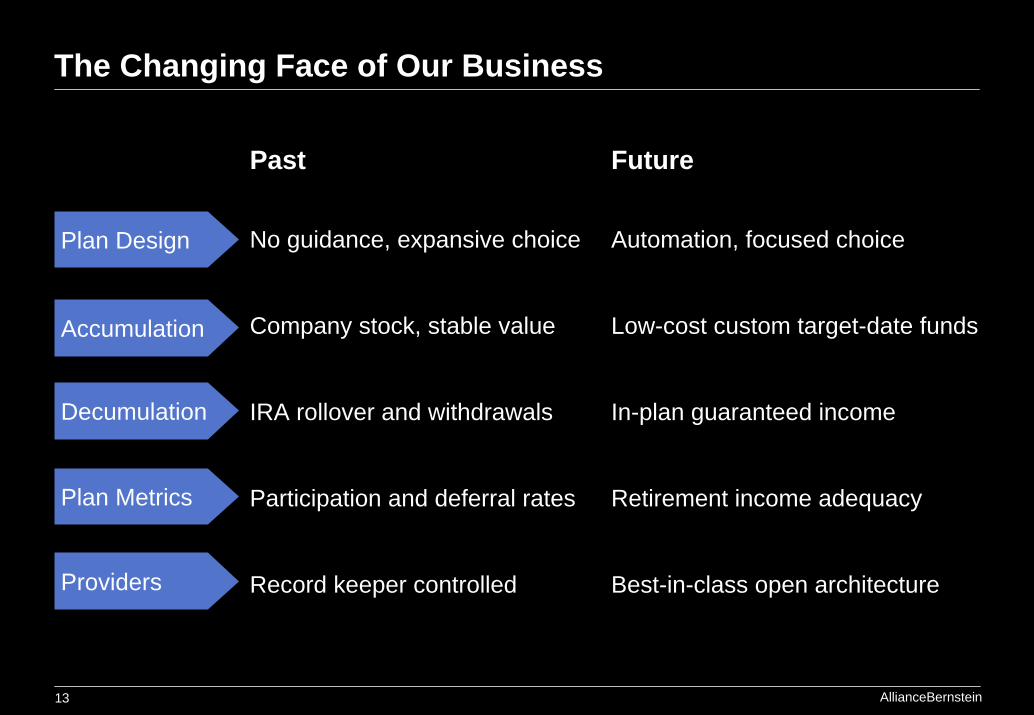

The Changing Face of Our Business

Past

Simple Technology

Hard to use

Expensive

Future

Complex Technology

Easy to use

Inexpensive

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein13

No guidance, expansive choice

Company stock, stable value

IRA rollover and withdrawals

Participation and deferral rates

Record keeper controlled

Past

Automation, focused choice

Low-cost custom target-date funds

In-plan guaranteed income

Retirement income adequacy

Best-in-class open architecture

Future

Plan Design

Accumulation

Decumulation

Plan Metrics

Providers

The Changing Face of Our Business

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein14

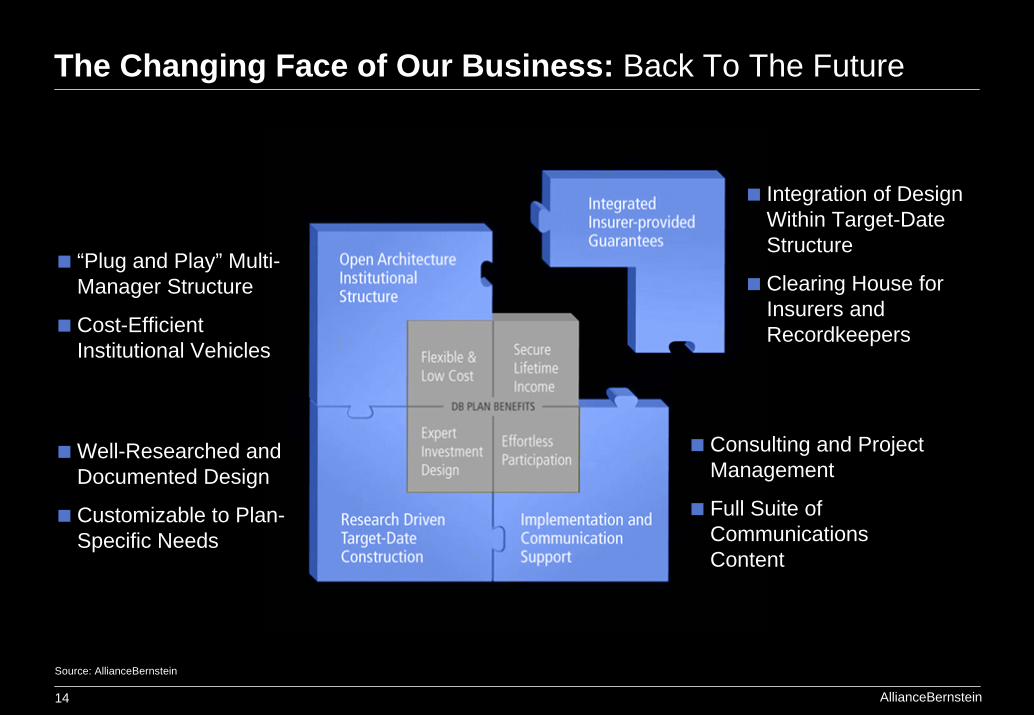

The Changing Face of Our Business: Back To The Future

Source: AllianceBernstein

SimpleParticipation

Low Cost

SecureLifetimeIncome

1

2 3

4

“Plug and Play” Multi-Manager Structure

Cost-Efficient Institutional Vehicles

Well-Researched and Documented Design

Customizable to Plan-Specific Needs

Consulting and Project Management

Full Suite of Communications Content

Integration of Design Within Target-Date Structure

Clearing House for Insurers and Recordkeepers

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein15

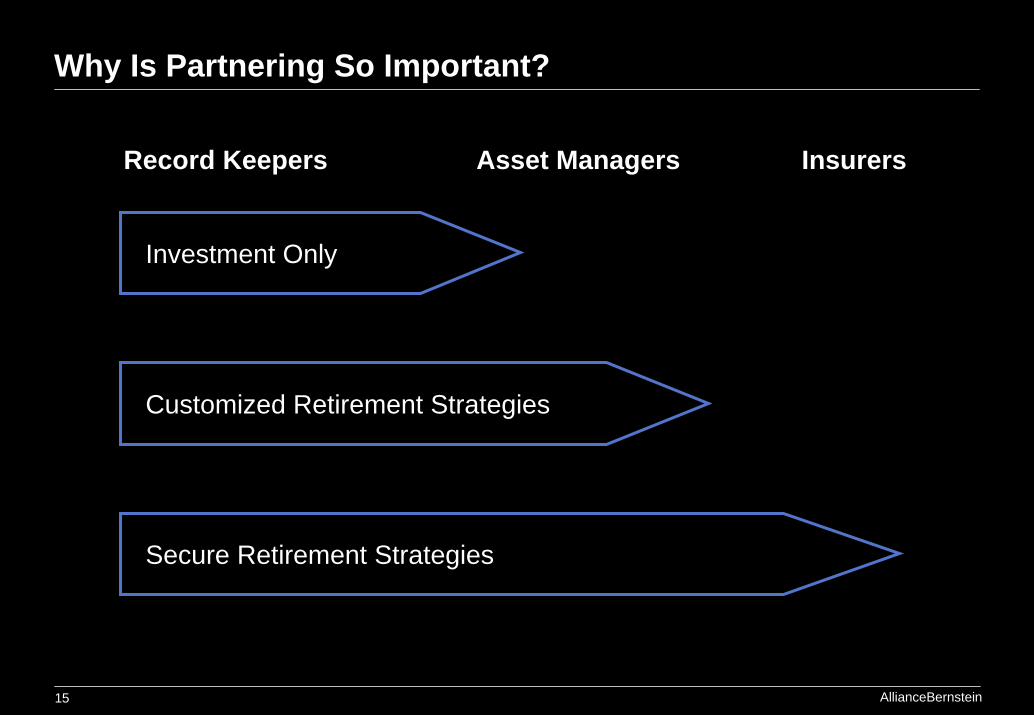

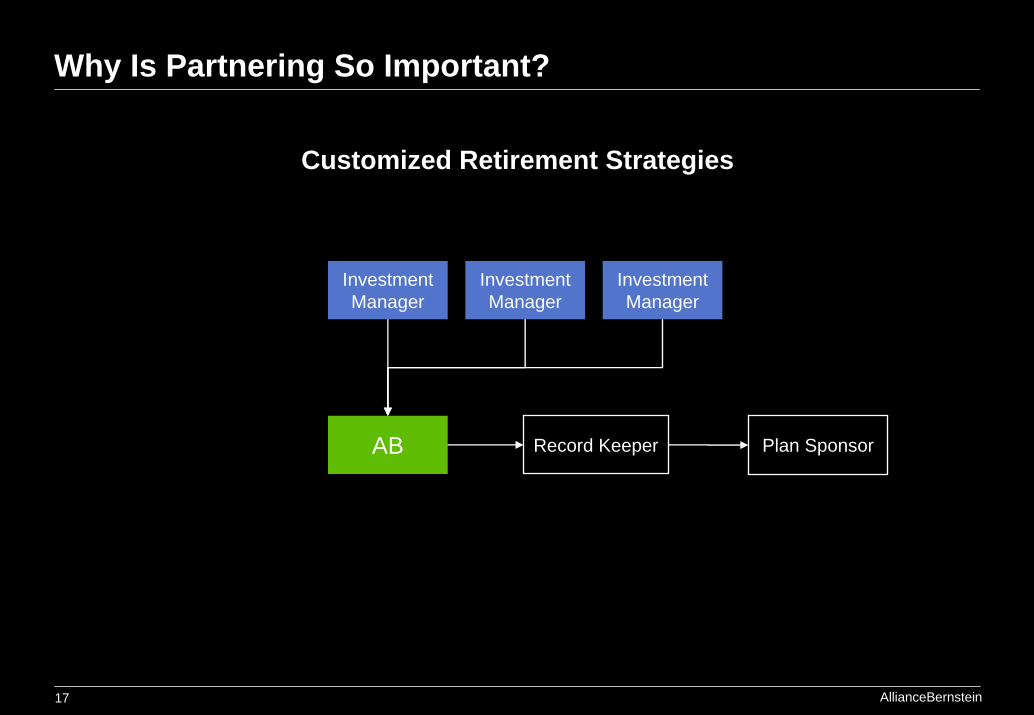

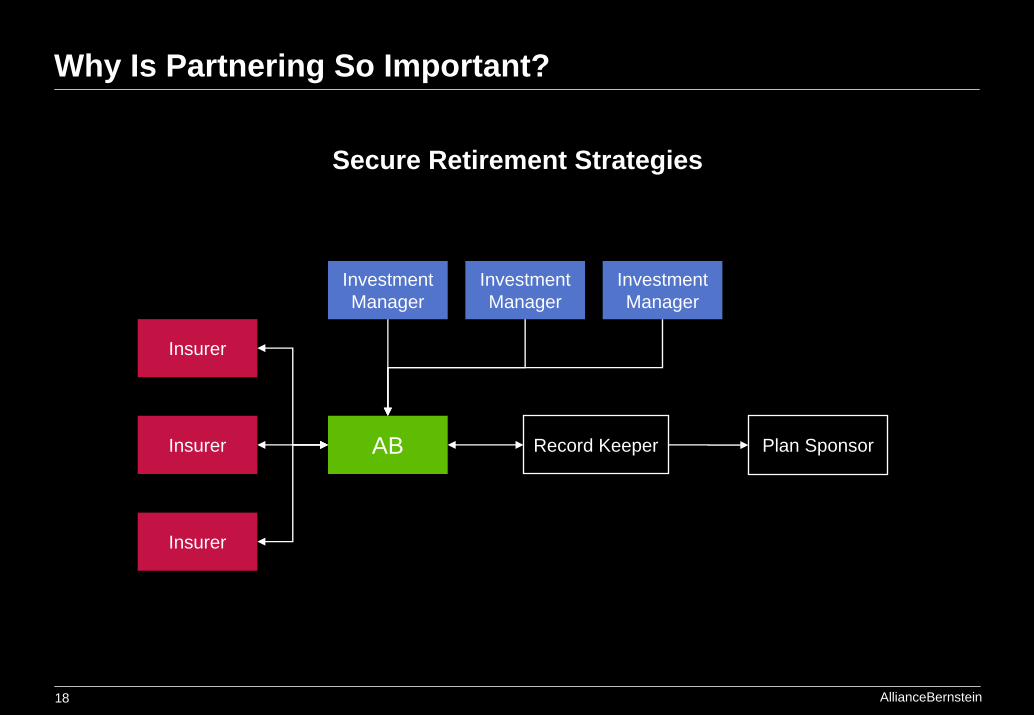

Why Is Partnering So Important?

Record Keepers Asset Managers Insurers

Investment Only

Customized Retirement Strategies

Secure Retirement Strategies

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein16

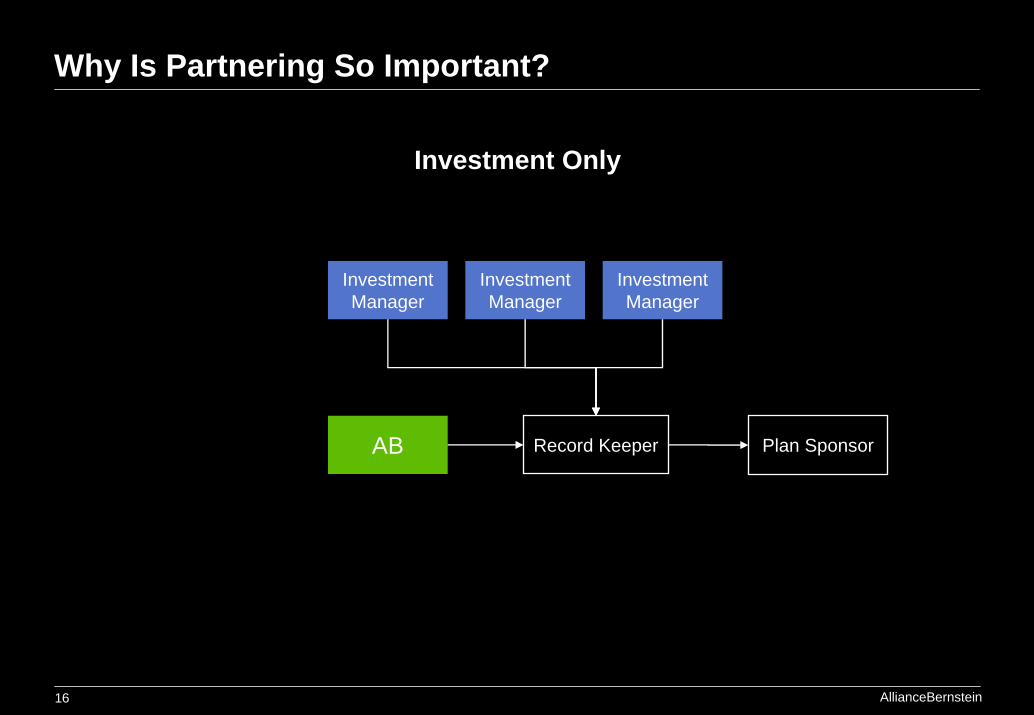

Why Is Partnering So Important?

Investment Only

Record Keeper

Investment Manager

Investment Manager

Plan Sponsor

Investment Manager

AB

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein17

Why Is Partnering So Important?

Customized Retirement Strategies

Record Keeper

Investment Manager

Investment Manager

Plan Sponsor

Investment Manager

AB

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein18

Why Is Partnering So Important?

Secure Retirement Strategies

Record Keeper

Investment Manager

Investment Manager

Plan Sponsor

Investment Manager

AB

Insurer

Insurer

Insurer

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein19

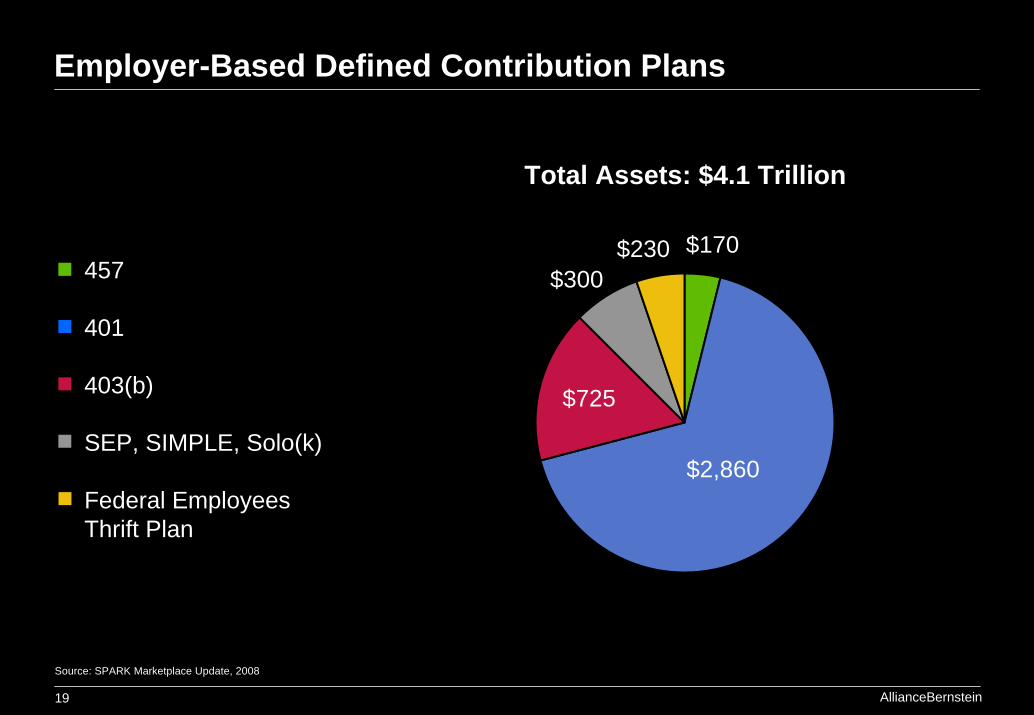

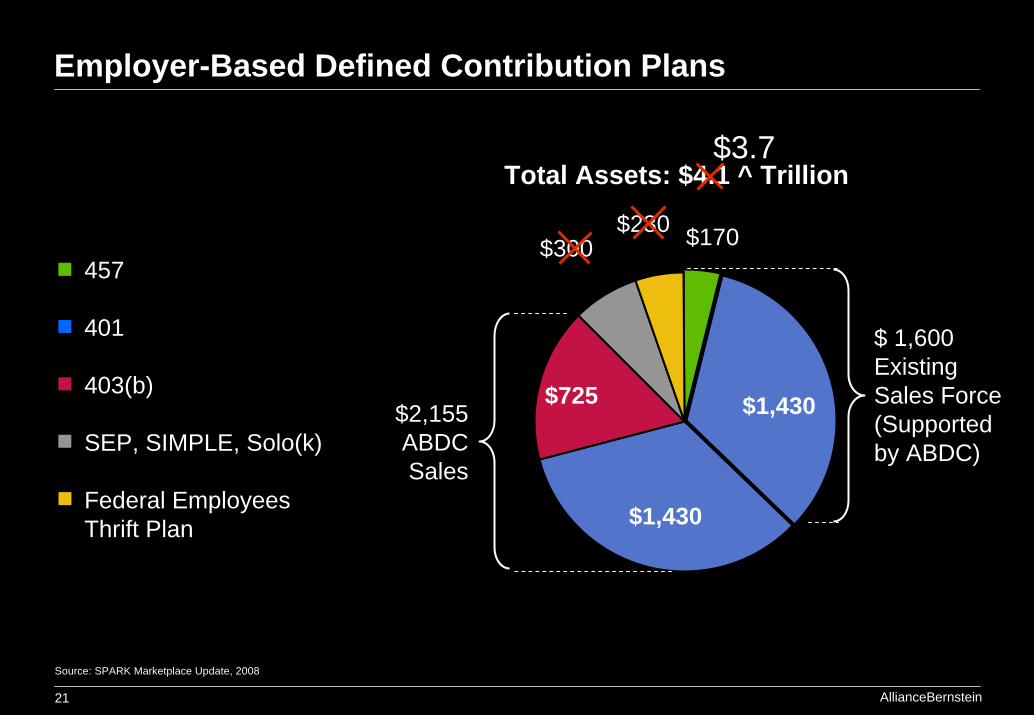

Employer-Based Defined Contribution Plans

Source: SPARK Marketplace Update, 2008

$725

$300$230 $170

$2,860

Total Assets: $4.1 Trillion

457

401

403(b)

SEP, SIMPLE, Solo(k)

Federal Employees Thrift Plan

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein20

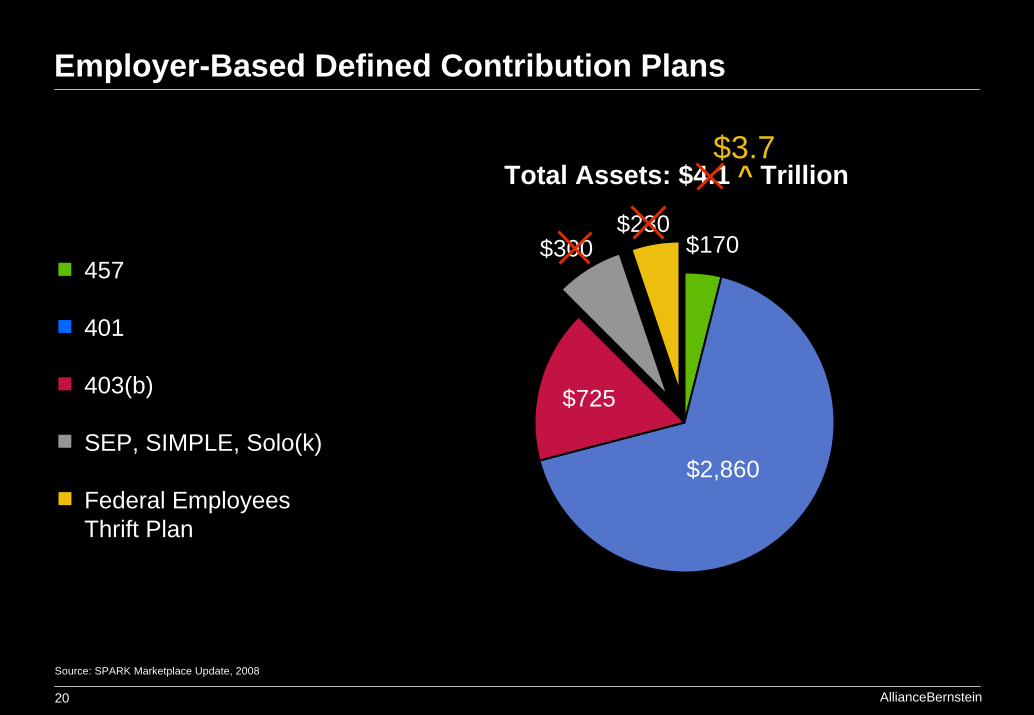

Employer-Based Defined Contribution Plans

Source: SPARK Marketplace Update, 2008

$300$230

$2,860

$170

$725

Total Assets: $4.1 ^ Trillion$3.7

457

401

403(b)

SEP, SIMPLE, Solo(k)

Federal Employees Thrift Plan

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein21

Employer-Based Defined Contribution Plans

Source: SPARK Marketplace Update, 2008

$1,430

$170

$725

$1,430

$ 1,600Existing Sales Force (Supported by ABDC)

$300$230

Total Assets: $4.1 ^ Trillion$3.7

$2,155 ABDC Sales

457

401

403(b)

SEP, SIMPLE, Solo(k)

Federal Employees Thrift Plan

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein22

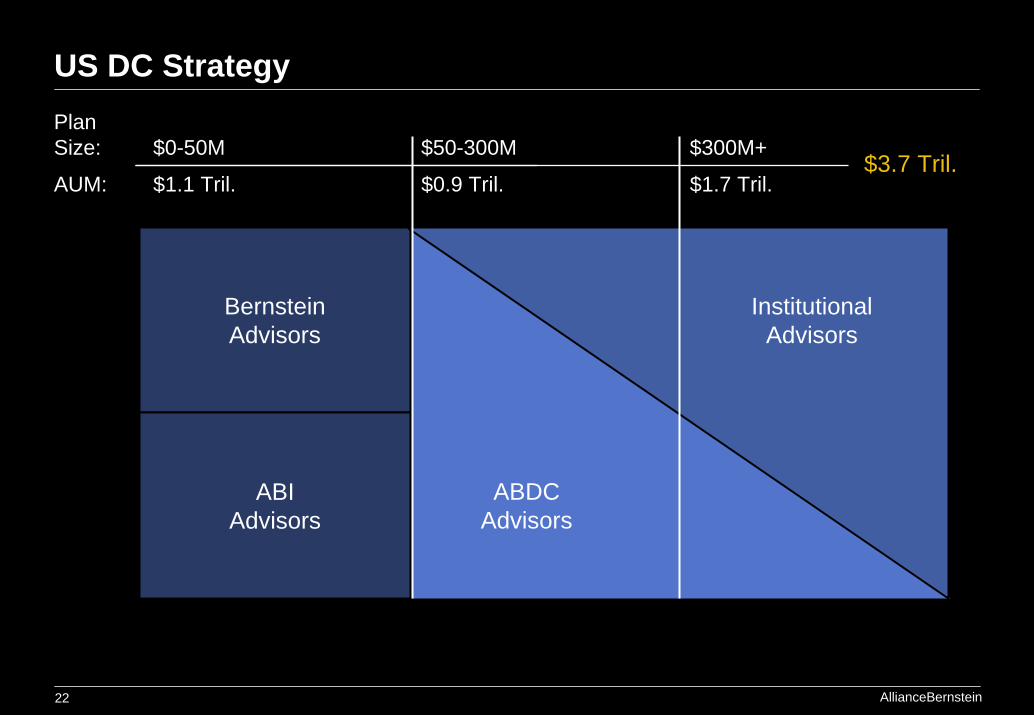

BernsteinAdvisors

ABIAdvisors

US DC StrategyPlan Size: $0-50M $50-300M $300M+

AUM: $1.1 Tril. $0.9 Tril. $1.7 Tril.

ABDCAdvisors

$3.7 Tril.

InstitutionalAdvisors

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein23

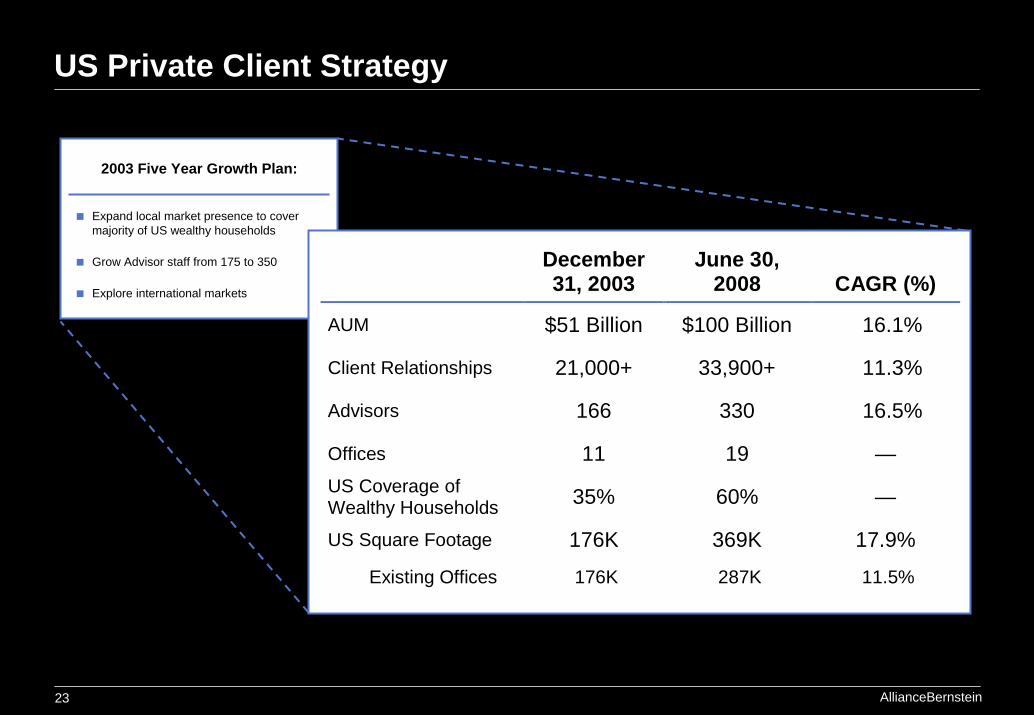

US Private Client Strategy

2003 Five Year Growth Plan:

Expand local market presence to covermajority of US wealthy households

Grow Advisor staff from 175 to 350

Explore international markets December 31, 2003

June 30, 2008 CAGR (%)

AUM $51 Billion $100 Billion 16.1%

Client Relationships 21,000+ 33,900+ 11.3%

Advisors 166 330 16.5%

Offices 11 19 — US Coverage of Wealthy Households 35% 60% —

US Square Footage 176K 369K 17.9%

Existing Offices 176K 287K 11.5%

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein24

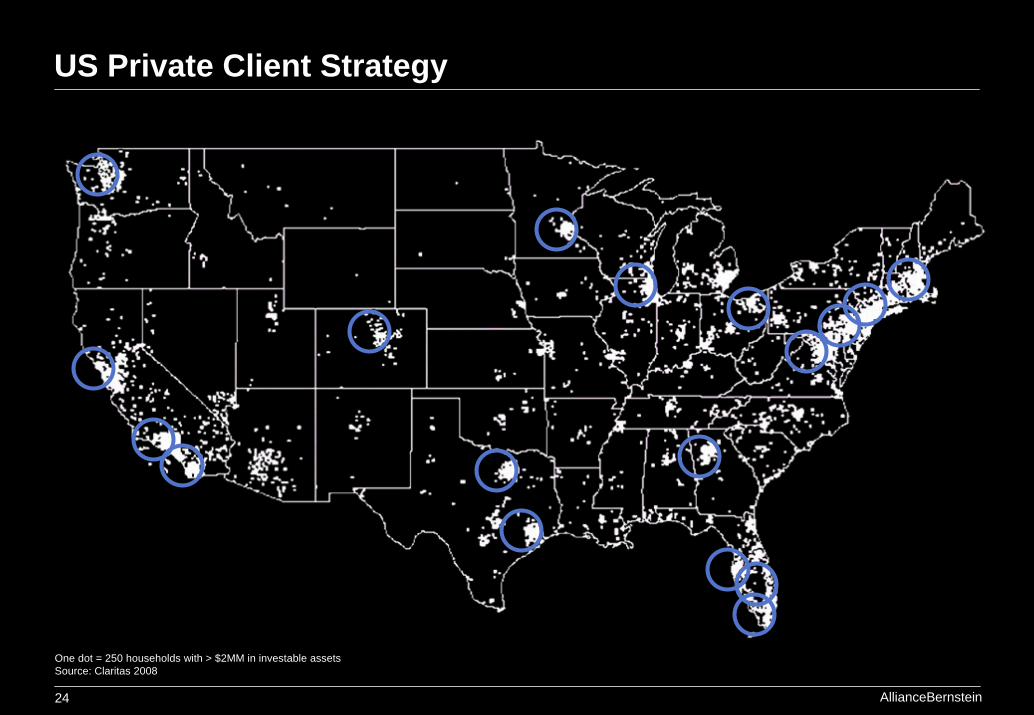

US Private Client Strategy

One dot = 250 households with > $2MM in investable assetsSource: Claritas 2008

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein25

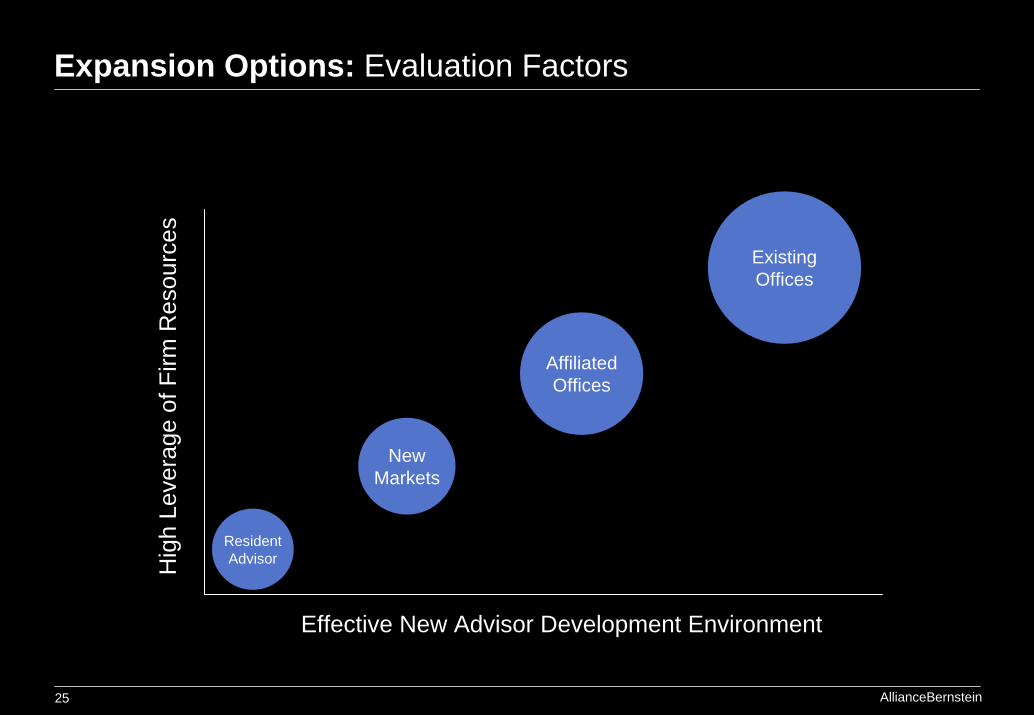

Expansion Options: Evaluation Factors

Hig

h Le

vera

ge o

f Firm

Res

ourc

es

Effective New Advisor Development Environment

Existing Offices

AffiliatedOffices

New Markets

ResidentAdvisor

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein26

US Private Client StrategyM

argi

n

Merrill Lynch Banking & Financial Services ConferenceAllianceBernstein27

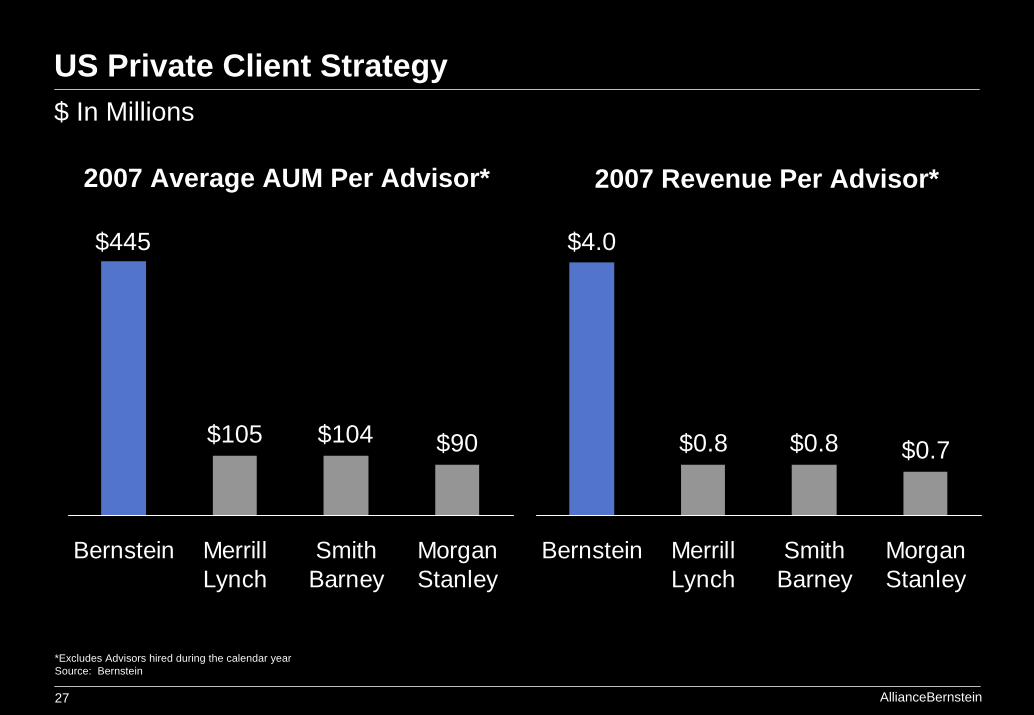

US Private Client Strategy

2007 Revenue Per Advisor*2007 Average AUM Per Advisor*

$ In Millions

*Excludes Advisors hired during the calendar yearSource: Bernstein

$445

$105 $104 $90

Bernstein MerrillLynch

SmithBarney

MorganStanley

$4.0

$0.8 $0.8 $0.7

Bernstein MerrillLynch

SmithBarney

MorganStanley

AllianceBernstein® and the AB AllianceBernstein logo are trademarks and service marks owned by AllianceBernstein L.P.

Merrill Lynch Banking & Financial Services Conference

November 12, 2008

David SteynExecutive Vice President

Global Head of Client Service and Marketing

Top Related