Languages

Pages

Legal

MEDIA MARKET IN MODERN RUSSIA

Prof. Marina Kolesnikova St.-‐Petersburg State University

HISTORICAL DATES

1992-‐1994 Market in mass-‐media started

1998 FOUNDATION of State complex VGTRK

2013 Opening of PUBLIC CHANNEL

GENERAL CHARACTERISTICS

• Annual tempos of Growth 2011-‐2016 – 11% • 7th place in EMEA region (Europe, Med.East, Africa, 2014 – 6 place • Volume by 2016 – 39 billion dollars • The highest level of consumer spending in EMEA (36%) by 2016

• INTERNET ACCESS – annually 14% • Internet adverWsing 2012-‐2016 – 29%

Structure of Russian Media Market

TV 25%

Radio 25%

Internet 10%

News agencies

9%

Newspapers 9%

Magazines 8%

Weekly ediYons 8%

Documentaries 6%

Media ConsumpYon in Russia (2012)

TV 46%

Radio 36%

Internet 8%

Newspapers 2%

Magazines 1%

Other medias 8%

ClassificaYons of Russian Media Market

Consumers Market: -‐ By gender -‐ By age

-‐ By naYonality -‐ By life style

-‐ By occupaYon and social status

Markets of Resources:

Financial Media content

Technology

Publishers

Human Resources

InformaYon

AdverYsing

Medias

Printed

Video/ Audio

Internet News Agencies

Documentaries

Environment

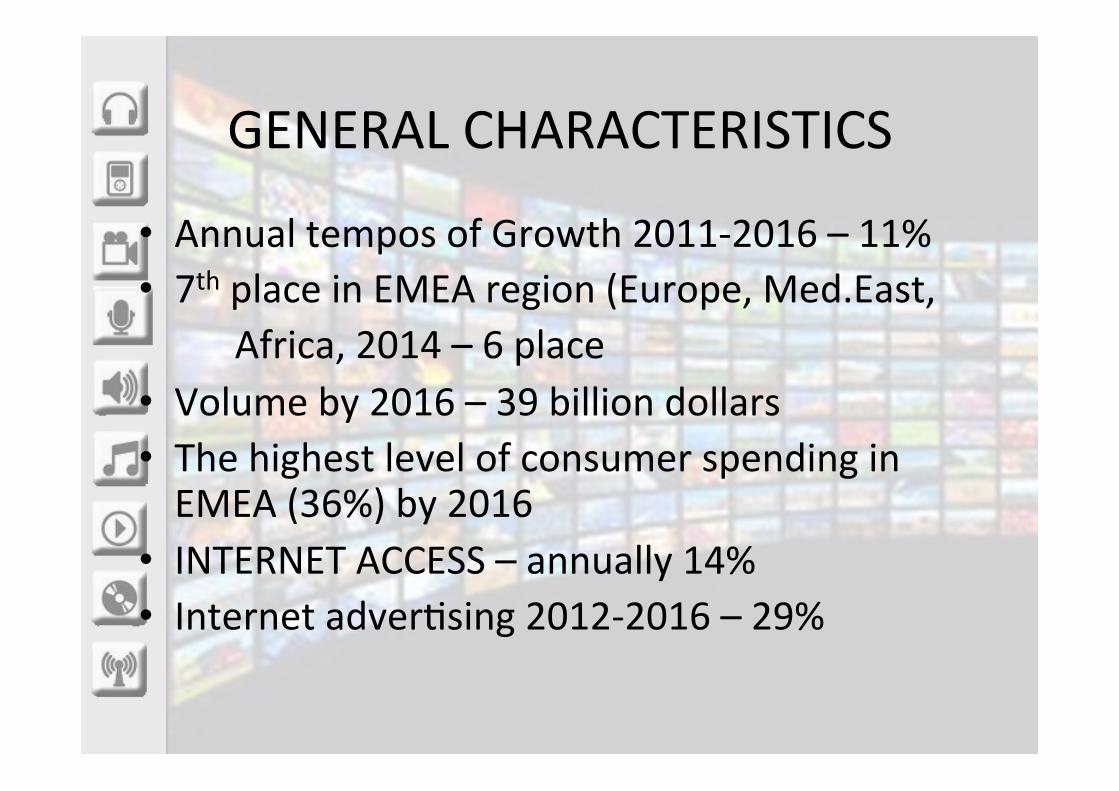

120000

80000

80000

50000

35000

Kommersant

RBC Newspaper

RBC Daily

VedomosY

Moscow Times

CirculaYon of Business Newspapers

110000

100000

100000

92000

83000

Business Magazine

Forbes

RBC Magazine

Expert

Profil

CirculaYon Business Magazines

The Most Popular Business Newspapers in Russia

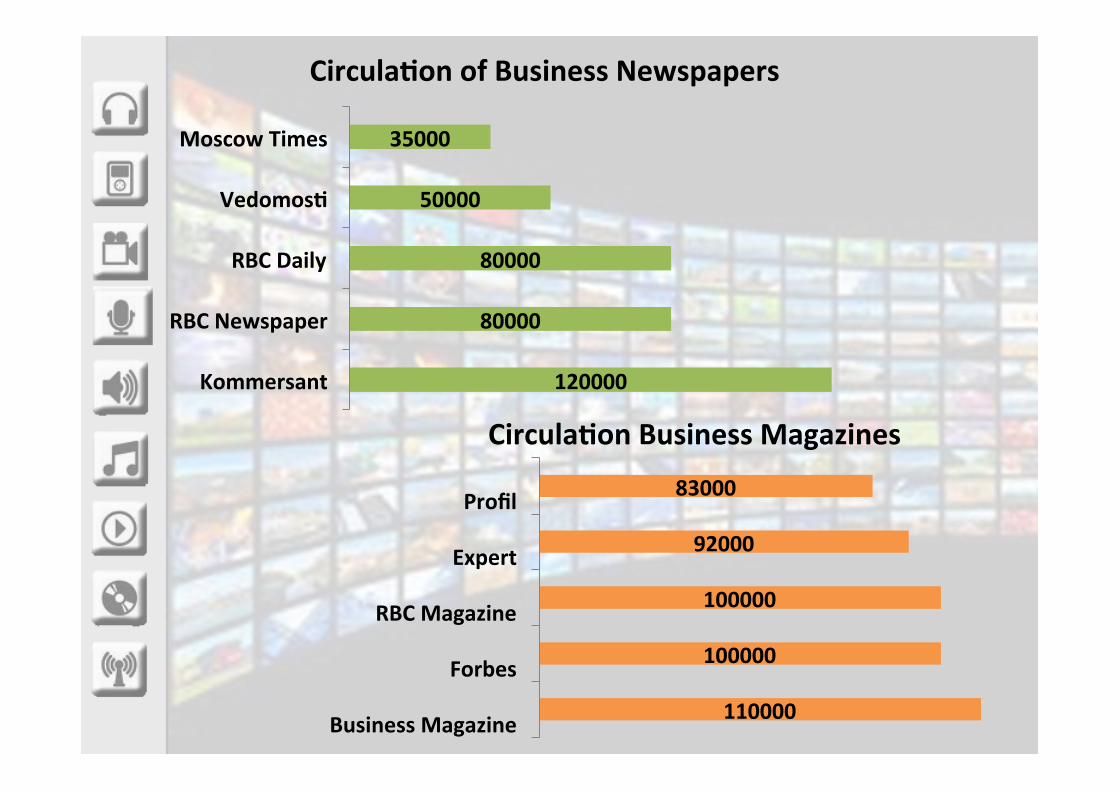

The Most Popular Business Magazines in Russia

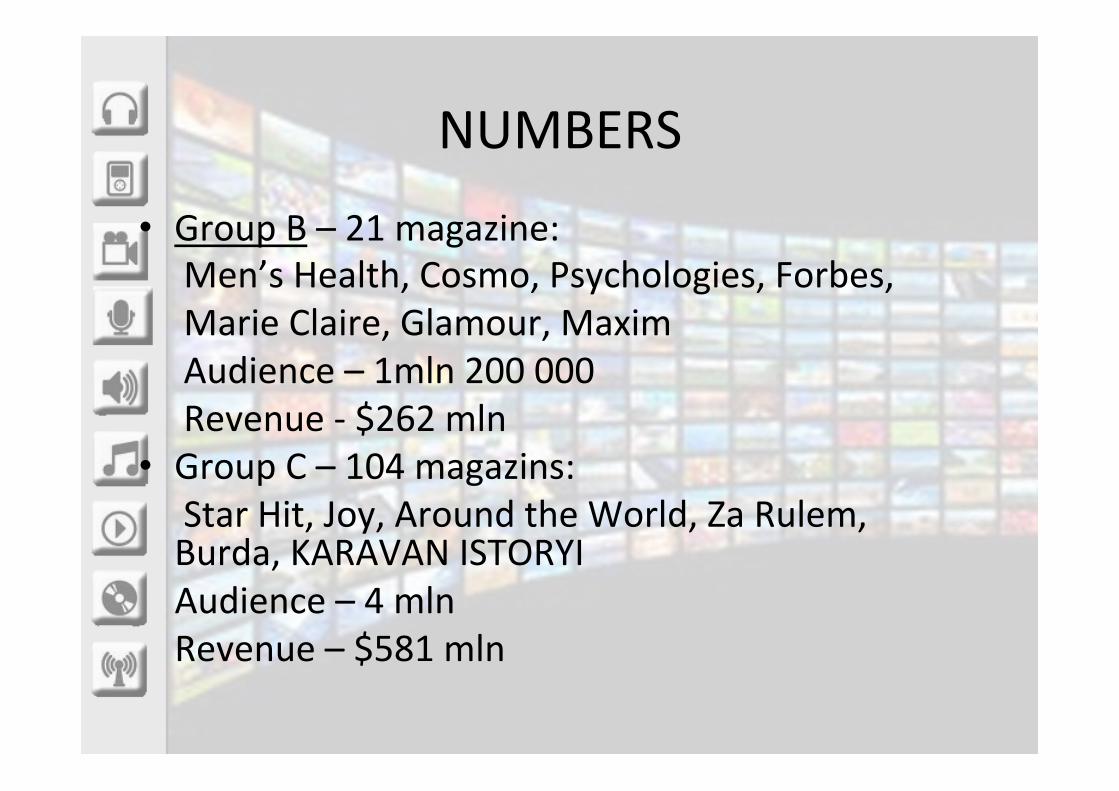

NUMBERS

• REGISTERED -‐24 500 Wtles of magazins • 242 – the most demanded • Readers – 15 mln people • 92% -‐ printed in Moscow • The most expensive ediWons: 11 (group A) VOGUE,GRACIA, GQ, ELLE, HARPER’S BAZAAR, L’Officiel -‐ audience 199 000 readers Revenue -‐ $232 mln

NUMBERS • Group B – 21 magazine: Men’s Health, Cosmo, Psychologies, Forbes, Marie Claire, Glamour, Maxim Audience – 1mln 200 000 Revenue -‐ $262 mln • Group C – 104 magazins: Star Hit, Joy, Around the World, Za Rulem, Burda, KARAVAN ISTORYI

Audience – 4 mln Revenue – $581 mln

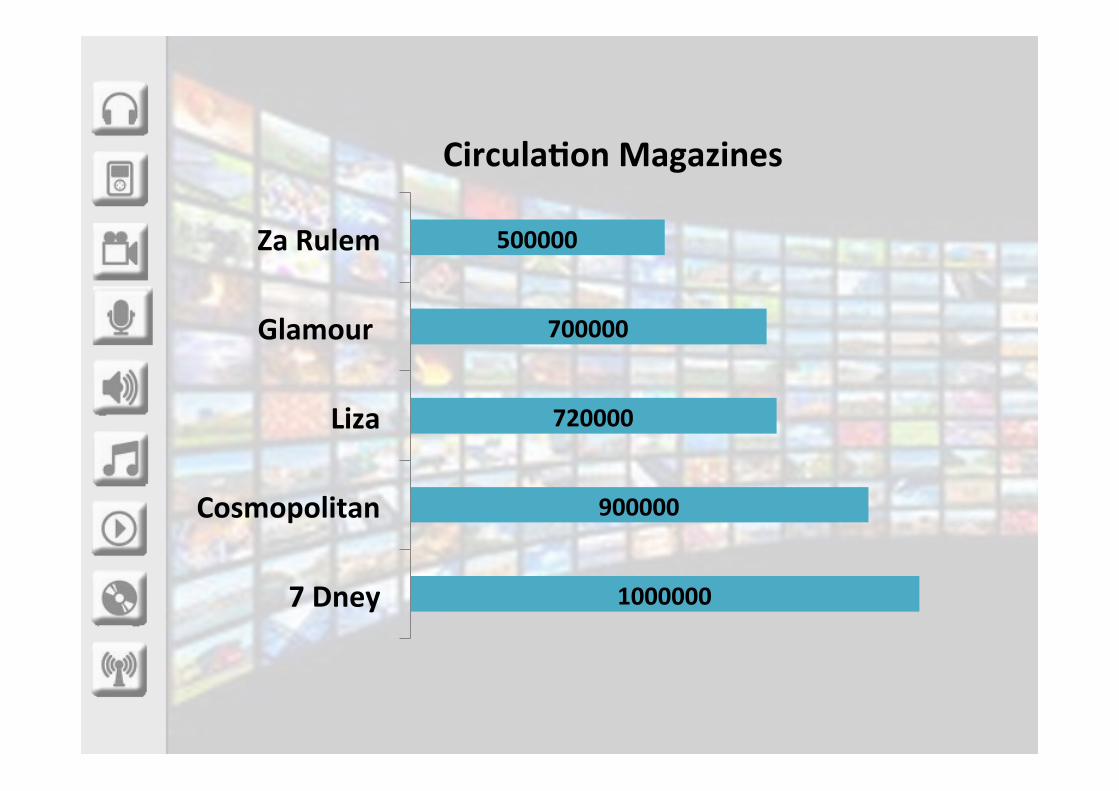

1000000

900000

720000

700000

500000

7 Dney

Cosmopolitan

Liza

Glamour

Za Rulem

CirculaYon Magazines

The Most Popular Magazines in Russia (Women) Foreign Russian

Foreign Russian

The Most Popular Magazines in Russia (Men)

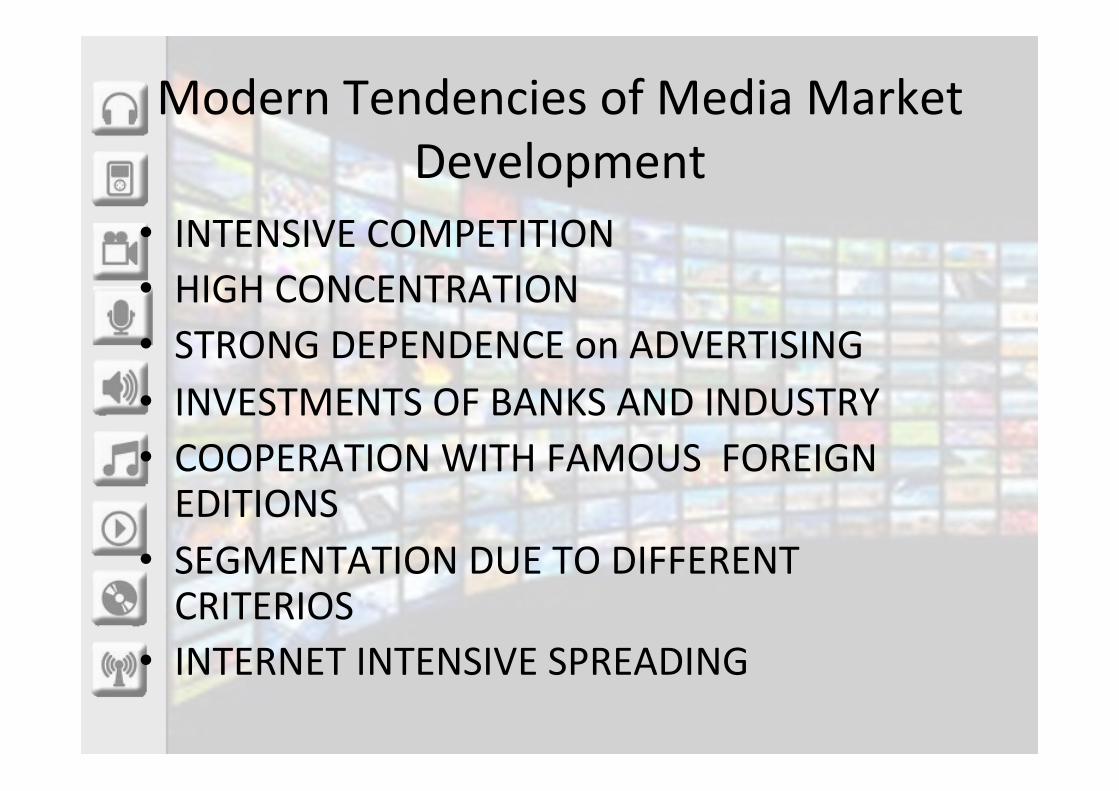

Modern Tendencies of Media Market Development

• INTENSIVE COMPETITION • HIGH CONCENTRATION • STRONG DEPENDENCE on ADVERTISING • INVESTMENTS OF BANKS AND INDUSTRY • COOPERATION WITH FAMOUS FOREIGN EDITIONS

• SEGMENTATION DUE TO DIFFERENT CRITERIOS

• INTERNET INTENSIVE SPREADING

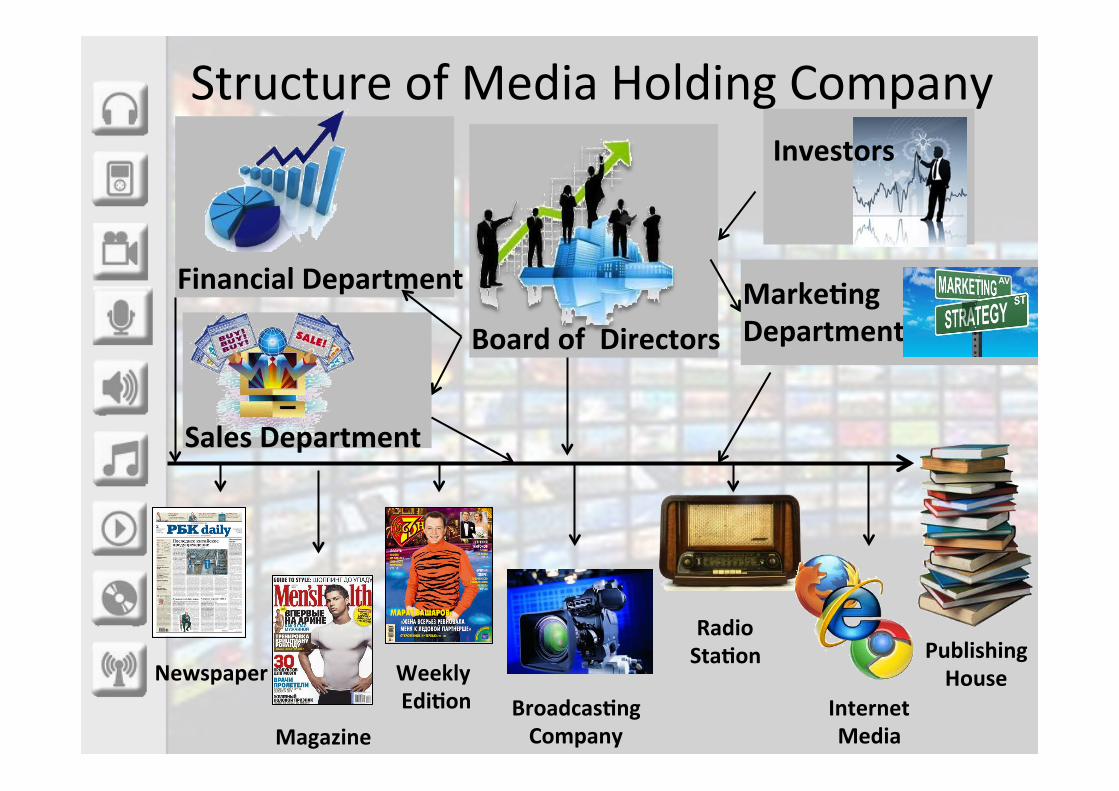

Structure of Media Holding Company

Weekly EdiYon

Newspaper

Magazine BroadcasYng Company

Publishing House

Radio StaYon

Internet Media

Investors

Board of Directors

Financial Department MarkeYng Department

Sales Department

TYPICAL CLUSTERS IN MASS-‐Media

TECHNOLOGY of PRODUCTION + DISTRIBUTION OF MEDIA PRODUCT

CLUSTERS in the INDUSTRY of CONTENT

• Newspapers and magazines • Book printing

• TV industry

• Broadcasting

• Video production

• Film-production

• Recording

• On-line information

• Production of Computer games • Data Basis

“UMBRELLA COMPETITION”

HORIZONTAL INTEGRATION

• NEWSPAPER + SPECIALISED ATTACHMENTS • NEW GEOGRAPHICAL ENTRIES • NEWSPAPER CHAINS

VERTICAL INTEGRATION

• NEWSPAPER + PUBLISHING HOUSE • NEWSPAPER + DISTRIBUTION CHANNELS • CABEL TV + ENTERTAINMENT PROGRAM PACKAGE

Foreign Investment in Russian Media Market

RESULTS OF SURVEY “CONSUMER DEMAND FOR TV PROGRAMS”

• Specialized CHANNELS -‐ 21% • AMUSEMENT for children – 28% • EducaWonal channel – 16% • InformaWon and News – 13% • Russian and World classics – 12% • “Useful” channel – 11% • Amusement programs – 10% • Military and patrioWc – 9% • Culture and art – 7% • Religion – 4% • Fashion and style – 4% • Programs about products and services – 3%

Online News Media Ranking

25%

20%

19%

17%

15%

13%

12%

9%

0% 5% 10% 15% 20% 25% 30%

I Don't read news online

RBC.ru

Lenta.ru

rian.tu

others

gazeta.ru

kommersant.tu

aif.ru

Online News Media Ranking

0% 5% 10% 15% 20% 25% 30%

I Don't read news online

RBC.ru

Lenta.ru

rian.tu

others

gazeta.ru

kommersant.tu

aif.ru

all

female

male

DistribuYon of Online News Readers by Age

0%

5%

10%

15%

20%

25%

30%

35%

40%

I Don't read news online

RBC.ru Lenta.ru rian.tu others gazeta.ru kommersant.tu aif.ru

All

<19

19-‐29

30-‐39

40-‐49

50<

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

I Don't read news online

RBC.ru Lenta.ru rian.tu others gazeta.ru kommersant.tu aif.ru

All

<250

250-‐450

450-‐750

750-‐1000

1000<

Monthly Income of Online News Readers (Euro)

PenetraWon of Internet in Russia (Different Age Groups)

0%

10%

20%

30%

40%

50%

60%

70%

80%

2003 2004 2005 2006 2007 2008 2009 2010

18-‐24

25-‐34

35-‐44

45-‐54

55<

ADVERTISING: GENERAL DATA

• 5th place aler Germany, GB, France, Italy • Volume – 9 billion dollars • 4th place by the year 2016 • Internet adverWsing segment growth by 56% in 2011 • Prognoses for 2016 – TV ads in Russia will be ahead of TV ads in other European countries

AdverWsing Market in Russia

TV 42%

Radio 4%

Printed Media 14%

Outdoor adverYsing

10%

Internet 8%

Other Medias 1%

MarkeYng Servicies 21%

AdverWsing Revenues (%)

CONCLUSIONS • The MARKET IS DEVELOPING • COMING TO MORE CIVILISED WAY OF FUNCTIONING • QUALITY is becoming very important • LEGAL BASIS is becoming stronger • HUGE MEDIA HOLDINGS are in power • PRESS is in the most criWcal situaWon • INTERNET is the serious compeWtor • NEW TECHNICAL POSSIBILITIES are coming into use • Appearance of the unanimous informaWon field • ContradicWon between the growing freedom of distribuWon the

informaWon through social nets and the legal regulaWon of property rights and state regulaWon of Media

Top Related