Languages

Pages

Legal

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 1/60

A PROJECT REPORT

ON

SECURITIES MARKET IN INDIA

MASTER IN BUSINESS ADMINISTRATION ( FINANCE )

SUBMITTED IN PARTIAL FULFILMENT OF THE REQUIREMENT FOR

AWARD OF MASTER IN BUSINESS ADMINISTRATION OF

TILAK MAHARASHTRA UNIVERSITY, PUNE.

SUBMITTED BY

Mr. SANDEEP RAMAKANT GIRNARKAR

PRN No.07408100844

OF

PINGE’S TUTION CLASSES, DADAR , MUMBAI.

GUIDED BY PROF. R. SUBRAMANIYAN

TILAK MAHARASHTRA UNIVERSITY

GULTEKDI, PUNE 411037.

Tilak Maharashtra University, Pune 411037

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 2/60

( Deemed under section 3 of UGC Act 1956 Vide notification No. F.9 –U3 dated 24th April1987 By Government of India)

Vidyapeeth Bhavan, Gultekdi, Pune – 411037.

CERTIFICATE

This is to certify that the project titled “ SECURITIES MARKET IN INDIA”

is a bonafied work carried out by Mr. SANDEEP R. GIRNARKAR astudent of

Master of Business Administration Semester 5th, Specialization Finance,PRN No. 07408100844 under Tilak Maharashtra University, in the year 2010.

Head of the Department Examiner Examiner Internal

External

Date :

Place :

University Seal

2

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 3/60

CERTIFICATE OF INTERNAL GUIDE

This is to certify that the project titled

“SECUITIES MARKET IN INDIA “ is a bonafied work carried out

by Mr. SANDEEP R GIRNARKAR a candidate for the award of

Master of Business Administration of Tilak Maharashtra

University, Pune under my guidance and direction.

Signature of guide

Date : Name :

Place : Mumbai. Designation :

Institute :

3

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 4/60

CERTIFICATE

TO WHOMSOEVER IT MAY CONCERN

This is to certify that Mr. Sandeep R. Girnarkar MBA student of

Tilak Maharashtra University, Pune has successfully completed his

project work for the award of Master Degree in Business Administration.

He has done the project on “ SECURITIES MARKETS IN INDIA”

Company Name : Life Insurance Corporation of India

Investment Department, Mumbai

Signature : Company Seal

Designation: Dy. Secretary ( Investment)

4

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 5/60

ACKNOWLEDGEMENT

I owe a great many thanks to a great many people who helped and

supported me in successful completion of my project. I thank my friends

and colleagues for their suggestions they provided to me from time to time.

My deepest thanks to Lecturer Mr. R. Subramaniyan the guide of the

project for guiding and correcting various documents of mine with attention

and care. He has taken pain to go through the project and make

necessary corrections as and when needed.

I also wish to express sincere gratitude to all respondents of the project

without the kind co- operation of whom this work would not have been

possible.

My deep sense of gratitude to Madam Anjali N. Desai, Manager,

Investment department of Life Insurance Corporation of India. For her

support and guidance. Thanks and appreciation to the people at Life

Insurance Corporation Of India for their support.

I would also thank my Institution and my faculty members without whom

this project would have been a distant reality. I also extend my heartfelt

thanks to my family and well wishers.

5

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 6/60

INDEX

SR. NO. TOPIC PAGE NOS.

1 RATIONALE OF THE STUDY 7-8

2 OBJECTIVE OF STUDY 9

3 PROFILE OF COMPANY 10

4 HISTORY OF SECURITIES MARKET 11-17

5 THEOROTICAL PERCEPTIVE 18-32

5 MACROECONOMIC INDICATORS 33-36

6 SECURITIES MATHAMATICS 37-43

7 REGULATORS FOR THE SECURITY MARKETS 44-45

9 RESEARCH METHODOLOGY 46-4710 DATA ANALYSIS AND INTERRPRETATION 48-51

11 FINDINGS 52

12 RECOMMENDATIONS 53-54

13 LIMITATIONS 55

14 EXPECTED CONTRIBUTION FROM THE STUDY 56

APPENDIX

Copies of Questionnaire

Bibliography

RATIONALE OF THE STUDY

A robust financial system requires multiple channels of financing, wherein

Securities Markets plays a significant role. It is the largest of all the

financial markets in the world today.

6

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 7/60

Basically, Securities Markets provide a channel for allocation of savings by

an individual or an organization to those who have a productive need for

them.

India’s fixed income securities market has been evolving steadily since the

economic reforms. It has witnessed several policy initiatives, which has

refined the market micro-structure, modernized operations and broadened

investment choices for the investors. With the implementation of the

Narasimham Committee recommendations on banking sector reforms

market determined interest rates replaced administered interest rates –

with few exceptions.

Debt market analysts working in the Indian banking sector need to

understand background of banking sector, interest rate cycles, and

volatility in the interest rates that pose new challenges. It is therefore very

much required to understand the securities market in India.

The study relates to estimating the number of institutions and population of

individual investors who have invested in equity market and debt market

directly or indirectly through mutual funds.

The study also relates to improvement in the service given by Brokers/sub-

brokers, various electronic modules boosting the investor’s confidence in

the securities market.

The study gives more emphasis on Government securities market as the

people are more fascinated to equity market than Debt market. A lot of

awareness is seen these days about equity market in India as compared

to Debt market. Therefore there is need to understand debt market more

than equity market.

7

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 8/60

OBJECTIVE OF STUDY

Main Objective :

The main objective of the study is to know Government securities market

with brief study of stock market.

8

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 9/60

Some other secondary objectives are as under :

1. The major characteristics of securities are their transferability andmarketability. The objective is to understand the process of trading

and investment in them.

2. Through the study of securities market , the objective is understand

the financial systems in India.

3. Since the 1960s, there has been a surge of significant financial

innovations, many of them are in bond market. The objective of the

study is to understand these innovations.

4. To know the influencing force behind the decision making while

investing in currently available investment options.

5. To understand the various electronic modules available for

transactions in securities market.

6. To understand the impact of macroeconomic factors on securities

market.

7. To understand the issuance of securities in India.

8. Attempt to understand the concept of Yield To Maturity, Gross

Current Yield etc.

9. To draw a profile of Institutional Investors and describe their

demographic, financial and equity ownership characteristics.

COMPANY’S PROFILE

Life Insurance Corporation of India

The Life Insurance Corporation (LIC) was established about 44 years ago

with a view to provide an insurance cover against various risks in life. A

monolith then, the corporation, enjoyed a monopoly status and became

synonymous with life insurance.

9

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 10/60

Its main asset is its staff strength of 1.24 lakh employees and 2,048

branches and over six lakh agency force.

LIC has hundred divisional offices and has established extensive training

facilities at all levels. At the apex, is the Management Development

Institute, seven Zonal Training Centres and 35 Sales Training Centres.

At the industry level, along with the Government and the GIC, it has

helped establish the National Insurance Academy. It presently transacts

individual life insurance businesses, group insurance businesses, social

security schemes and pensions, grants housing loans through itssubsidiary; and markets savings and investment products through its

mutual fund. It pays off about Rs 6,000 crore annually to 5.6 million

policyholders.

Keeping in mind the primary obligation of the Corporation to its

policyholders, as enshrined in the objectives of nationalization, the funds

of the Corporation are deployed to the best advantage of the policyholders

as well as the community as a whole. While investing these monies which

are held in trust, the Corporation has to keep in view the national priorities

and obligation of reasonable returns.

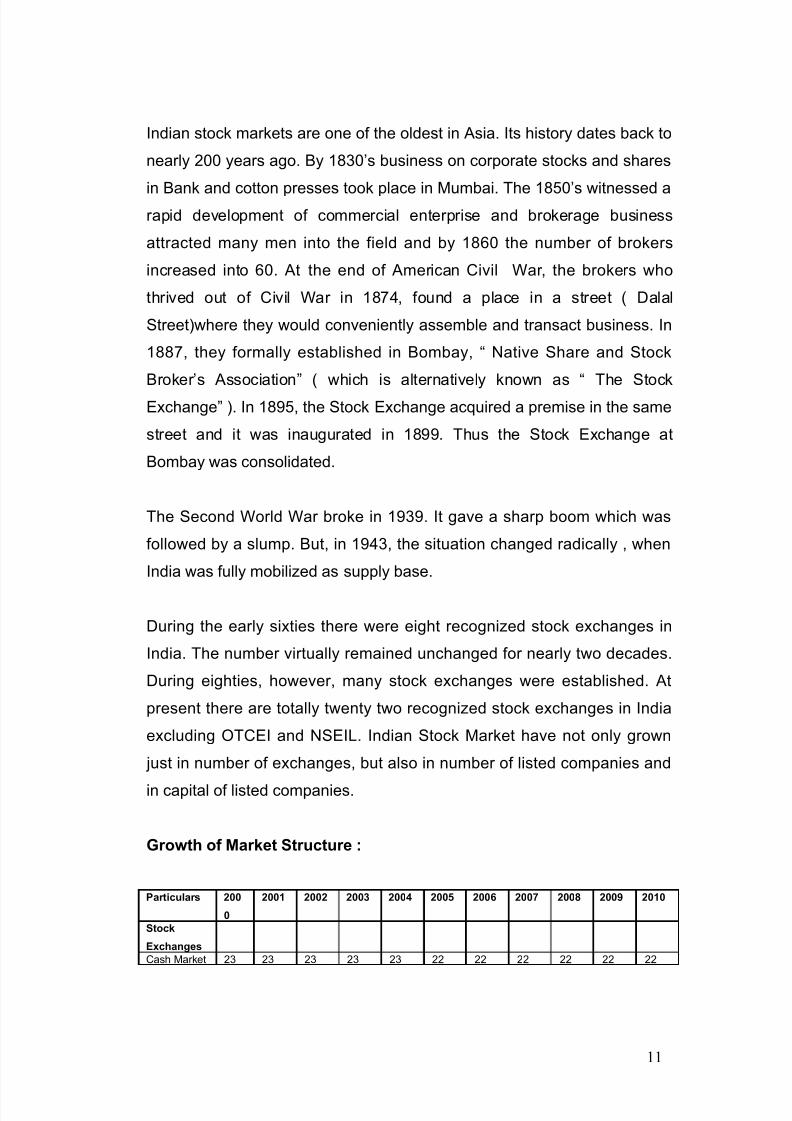

HISTORY OF SECURITIES MARKET

Evolution of Stock market & Govt. securities market in

India :

Stock Market :

10

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 11/60

Indian stock markets are one of the oldest in Asia. Its history dates back to

nearly 200 years ago. By 1830’s business on corporate stocks and shares

in Bank and cotton presses took place in Mumbai. The 1850’s witnessed arapid development of commercial enterprise and brokerage business

attracted many men into the field and by 1860 the number of brokers

increased into 60. At the end of American Civil War, the brokers who

thrived out of Civil War in 1874, found a place in a street ( Dalal

Street)where they would conveniently assemble and transact business. In

1887, they formally established in Bombay, “ Native Share and Stock

Broker’s Association” ( which is alternatively known as “ The Stock

Exchange” ). In 1895, the Stock Exchange acquired a premise in the same

street and it was inaugurated in 1899. Thus the Stock Exchange at

Bombay was consolidated.

The Second World War broke in 1939. It gave a sharp boom which was

followed by a slump. But, in 1943, the situation changed radically , when

India was fully mobilized as supply base.

During the early sixties there were eight recognized stock exchanges in

India. The number virtually remained unchanged for nearly two decades.

During eighties, however, many stock exchanges were established. At

present there are totally twenty two recognized stock exchanges in India

excluding OTCEI and NSEIL. Indian Stock Market have not only grown

just in number of exchanges, but also in number of listed companies and

in capital of listed companies.

Growth of Market Structure :

Particulars 200

0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Stock

Exchanges

Cash Market 23 23 23 23 23 22 22 22 22 22 22

11

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 12/60

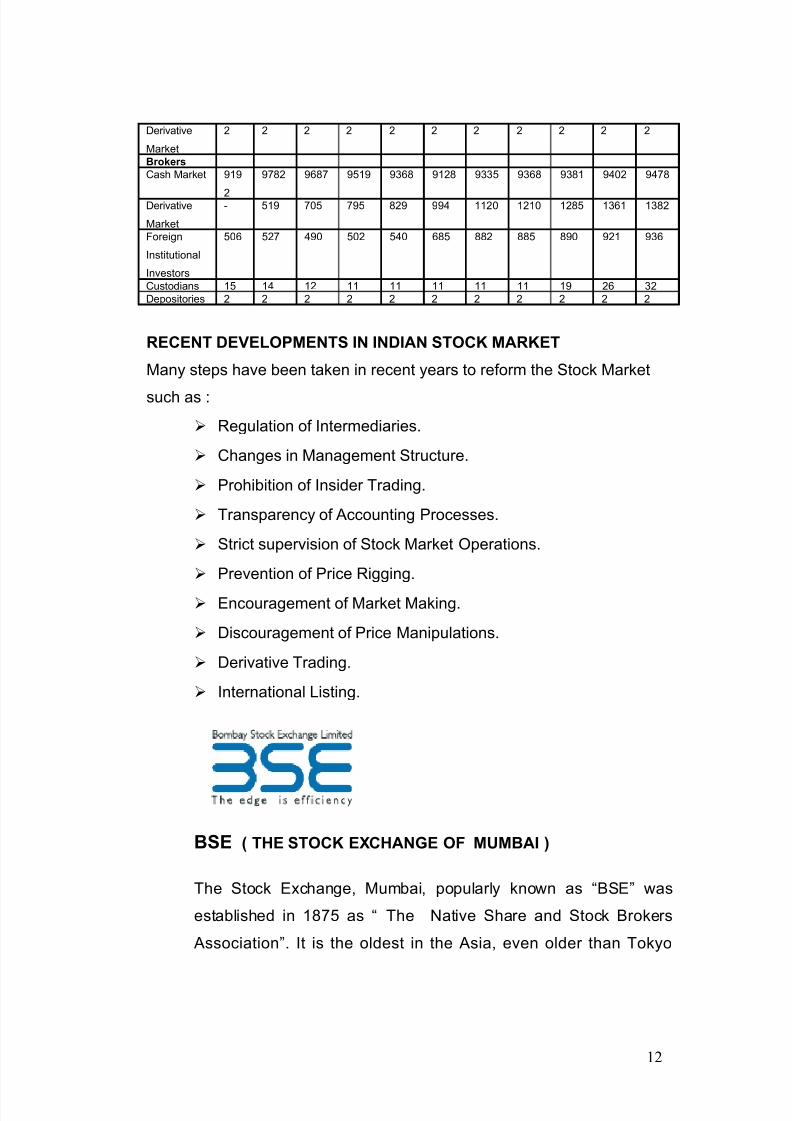

Derivative

Market

2 2 2 2 2 2 2 2 2 2 2

Brokers

Cash Market 919

2

9782 9687 9519 9368 9128 9335 9368 9381 9402 9478

Derivative

Market

- 519 705 795 829 994 1120 1210 1285 1361 1382

Foreign

Institutional

Investors

506 527 490 502 540 685 882 885 890 921 936

Custodians 15 14 12 11 11 11 11 11 19 26 32

Depositories 2 2 2 2 2 2 2 2 2 2 2

RECENT DEVELOPMENTS IN INDIAN STOCK MARKET

Many steps have been taken in recent years to reform the Stock Market

such as :

Regulation of Intermediaries.

Changes in Management Structure.

Prohibition of Insider Trading.

Transparency of Accounting Processes.

Strict supervision of Stock Market Operations.

Prevention of Price Rigging.

Encouragement of Market Making.

Discouragement of Price Manipulations.

Derivative Trading.

International Listing.

BSE ( THE STOCK EXCHANGE OF MUMBAI )

The Stock Exchange, Mumbai, popularly known as “BSE” was

established in 1875 as “ The Native Share and Stock Brokers

Association”. It is the oldest in the Asia, even older than Tokyo

12

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 13/60

Stock Exchange. It is voluntary non-profit making Association of

Persons and is currently engaged in the process of converting itself

into demutualised and corporate entity. It has evolved over theyears into its present status as the premier Stock Exchange in the

country. It is the first Stock Exchange in the country to have

obtained permanent recognition in 1956 from Govt. of India under

the Securities Contracts (Regulation) Act,1956.

The Exchange, while providing an efficient and transparent market

for trading in Securities, debt and derivatives upholds the interest of

the investors and ensures redressal of their grievances whether

against the companies or its own member brokers. It also strives to

educate and enlighten the investors by conducting investor

education program and making available to them necessary

informative inputs.

A Governing Board having 20 directors is the apex body, which

decides the policies and regulates the affairs of the Exchange. The

Governing Board consists of 9 elected directors, who are from the

broking community, 3 SEBI nominees, 6 public representatives and

an Executive Director & Chief Executive Officer and a Chief

Operating Officer.

NSE ( NATIONAL STOCK EXCHANGE)

NSE was incorporated in 1992 and was given recognition as a

stock exchange in April 1993. It started operations in June 1994,

with trading on Wholesale Debt Market Segment. Subsequently it

launched the Capital Market Segment in November 1994 as a

13

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 14/60

trading platform for equities and Futures and Options Segment in

June 2000 for various derivatives instruments.

NSE has been able to take the stock market to the doorsteps of the

investors. The technology has been harnessed to deliver the

service to the investors across the country at the cheapest possible

cost. It provides a nation-wide, screen-based, automated trading

system, with high degree of transparency and equal access to

investors irrespective of geographical location. The high level of

information dissemination through on-line system has helped in

integrating retail investors on a nation-wide basis. The standards

set by the exchange in terms of market practices, products,

technology and service standards have become industry

benchmarks and are being replicated by other market participants.

Within a very short span of time, NSE has been able to achieve all

the objectives for which it was set up. It has been playing a leading

role as a change agent in transforming the Indian Capital Markets to

its present form. The India Capital Markets are a far cry from what

they used to be a decade ago in terms of market practices,

infrastructure, technology, risk management, clearing and

settlement and investor service.

NCDEX ( NATIONAL COMMODITIES AND DERIVATIVES EXCHANGE)

NCDEX started working on 15th December, 2003. This exchange provides

facilities to their trading and clearing member at different 130 centres for

contract. In commodity market the main participants are speculators,

hedgers and arbitrageurs.

14

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 15/60

Promoters of NCDEX are

• National Stock Exchange (NSE)

• ICICI Bank

• Life Insurance Corporation of India (LIC)

• NABARD

• IFFICO

• Punjab National Bank (PNB)

• CRISIL

GOVT. SECURITIES / DEBT MARKET :

The government spends more than its income by borrowing from

various sources to meet growing needs of defence, social services and

planned development. Since 1951, the importance of public borrowing

as a source of financing government expenditure has increased

enormously and public debt began to grow by leaps and bound due to

the increasing planned expenditure under various five year plans.

In terms of provisions of the Public Debt Act, 1944, the administration

of public debt of Centre and States is entrusted to the RBI. Public Debt

management is concerned with the raising of finance for government

through market loans, treasury bills and other methods. The requiredfinance in any year is governed by the budgetary considerations of

their revenue and expenditure. The amount of finance to be raised, the

time, the rate of interest and terms of loan are all decided by the

Ministry of Finance in consultation with RBI. The RBI acts as an

underwriter for government debt , particularly of the Central

Government. In respect of State Government loans, RBI uses its moral

15

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 16/60

influence on the market to see that full subscription takes place for the

loans floated.

The role of RBI in debt management is

To keep the cost of financing to the minimum.

To maintain the market stable and smooth.

To meet the portfolio requirements of all investors to the extent

possible.

To maintain a minimum level of activity in the market with a

view to providing liquidity to the securities in the market for purpose of developing the market.

In most of the countries, the debt market is more popular than the

equity market. This is due to sophisticated bond instruments that have

return – reaping assets as their underlying. However, in India, equity

markets are more popular than debt markets due to dominance of

government securities in debt markets. Moreover, the government is

borrowing at a pre-announced coupon rate targeting a captive group of

investors such as Banks, Financial Institutions, Insurance Companies

etc. This coupled with automatic monetization of fiscal deficit,

prevented the emergence of a deep and vibrant government securities

market.

The bond markets exhibit a much lower volatility than equities, and all

bonds are priced based on same macroeconomic information. The

bond market liquidity is normally much higher than the stock market

liquidity in most of the countries. The performance of the market for

debt is directly related to the interest rate movement as it is reflected in

16

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 17/60

the yields of government bonds, corporate debentures, MIBOR-related

commercial papers and non-convertible debentures.

The Indian debt market is composed of government bonds and

corporate bonds. However, the Central Government bonds are

predominant and they form most liquid component of bond market. In

2003, the National Stock Exchange (NSE) introduced Interest Rate

Derivatives. The trading platforms for government securities are

“Negotiated Dealing System” (NDS) and “Wholesale Debt Market”

(WDM) segment of NSE and BSE. In negotiated market, the trades

are normally decided by the seller and the buyer, and are reported to

the exchange through the broker, whereas the WDM trading system,

know as NEAT, is fully automated screen based trading system, which

enables members across the country to trade simultaneously with

enormous ease and efficiency.

THEORETICAL PERCEPTIVE

TRADING PATTERN OF THE INDIAN STOCK MARKET

17

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 18/60

Trading in Indian stock exchanges are limited to listed securities of public

limited companies. They are broadly divided into two categories namely,

specified securities (forward list) and non-specified securities (cash list).Equity shares of dividend paying, growth oriented companies with a paid

up capital of at least Rs. 50 million and a market capitalization of at least

Rs.100 million and having more than 20,000 shareholders are, normally,

put in the specified group and balance in non specified group.

Two types of transactions can be carried out on the Indian stock

exchanges : (a) spot delivery transactions “ for delivery and payment

within the time or on the date stipulated when entering into the contract

which shall not be more than 14 days following the date of contract” and

(b) forward transactions “ delivery and payment can be extended by further

period of 14 days each so that the overall period does not exceed 90 days

from date of contract”. The latter is permitted only in case of specified

shares.

A member broker in an Indian stock exchange can act as an agent, buy

and sell securities for his clients on a commission basis and also can act

as a trader or dealer as a principal, buy and sell securities on his own

account and risk, in contrast with practice prevailing on New York and

London Stock Exchanges, where a member can act as a jobber or broker

only.

The nature of trading on Indian Stock Exchanges are that of age old

conventional style of face-to-face trading with bids and offers being made

by open outcry. However, there is a great amount of effort to modernize

the Indian Stock Exchanges in the very recent times.

18

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 19/60

To provide improved service to investors, the country’s first ring less, scrip

less, electronic stock exchange – OTCEI was created in 1992. Trading at

OTCEI is done over the centres spread across the country. Securitiestraded on OTCEI are classified into :

o Listed securities – The shares and debentures of the companies

listed on the OTC can be bought or sold at any OTC counter all

over the country and they should not be listed anywhere else.

o Permitted securities – Certain shares and debentures listed on

other exchange and units of mutual funds are allowed to be traded.

o Initiated debentures – Any equity holding at least one lakh

debentures of a particular scrip can offer tem for trading on OTC.

OTC has unique feature of trading compared to other traditional

exchanges. That is, certificate of listed securities and initiated

debentures are not traded at OTC. The original certificate will be safely

with custodian. But, a counter receipt is generated out at the counter

which substitutes the share certificate and is used for all transactions.

In case of permitted securities, the system is similar to a traditional

stock exchange. The difference is that the delivery and payment

procedure will be completed within 14 days.

Trading at NSE can be classified under two broad categories :

(a) Wholesale Debt Market

(b) Capital Market.

19

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 20/60

Wholesale Debt Market operations are similar to money market

operations – institutions and corporate bodies enter into high value

transactions in financial instruments such as government securities,treasury bills, public sector unit bonds, commercial paper, certificate of

deposit etc.

There are two kinds of players in NSE, trading members and

participants. Recognized members of NSE are called trading members

who trade on behalf of themselves and their clients. Participants

include trading members and large players like banks who takes direct

settlement responsibility.

Trading at NSE takes place through fully automated screen-based

trading mechanism which adopts the principle of an order driven

market. Trading members can stay at their offices and execute the

trading, since they are linked through a communication network. The

prices at which buyers and sellers are willing to transact will appear on

the screen. When prices match the transaction will be completed and

confirmation slip will be printed at the office of the trading member.

INDIAN FIXED INCOME SECURITIES MARKET

20

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 21/60

Government Securities

Government securities(G-secs) are sovereign securities which are issued

by the Reserve Bank of India on behalf of Government of India, in lieu of

the Central Government's market borrowing programme.

The term Government Securities includes:

• Central Government Securities

• State Government Securities

• Treasury bills

The Central Government borrows funds to finance its 'fiscal deficit'. The

market borrowing of the Central Government is raised through the issue of

dated securities and 364 days treasury bills either by auction or by

floatation of loans.

In addition to the above, treasury bills of 91 days are issued for managing

the temporary cash mismatches of the Government. These do not formpart of the borrowing programme of the Central Government.

Types of Government Securities

Government Securities are of the following types:-

Dated Securities : are generally fixed maturity and fixed coupon

securities usually carrying semi-annual coupon. These are called dated

securities because these are identified by their date of maturity and the

coupon, e.g., 11.03% GOI 2012 is a Central Government security maturing

in 2012, which carries a coupon of 11.03% payable half yearly.

The key features of these securities are:

21

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 22/60

They are issued at face value.

Coupon or interest rate is fixed at the time of issuance, and remains

constant till redemption of the security. The tenor of the security is also fixed.

Interest /Coupon payment is made on a half yearly basis on its face

value.

The security is redeemed at par (face value) on its maturity date.

Zero Coupon bonds : are bonds issued at discount to face value and

redeemed at par. These were issued first on January 19, 1994 and were

followed by two subsequent issues in 1994-95 and 1995-96 respectively.

The key features of these securities are:

They are issued at a discount to the face value.

The tenor of the security is fixed.

The securities do not carry any coupon or interest rate. The

difference between the issue price (discounted price) and face

value is the return on this security.

Partly Paid Stock : is stock where payment of principal amount is made in

installments over a given time frame. It meets the needs of investors with

regular flow of funds and the need of Government when it does not need

funds immediately. The first issue of such stock of eight year maturity was

made on November 15, 1994 for Rs. 2000 crore. Such stocks have been

issued a few more times thereafter.

The key features of these securities are:

They are issued at face value, but this amount is paid in

installments over a specified period.

22

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 23/60

Coupon or interest rate is fixed at the time of issuance, and remains

constant till redemption of the security.

The tenor of the security is also fixed.

Interest /Coupon payment is made on a half yearly basis on its face

value.

The security is redeemed at par (face value) on its maturity date.

Floating Rate Bonds : are bonds with variable interest rate with a fixed

percentage over a benchmark rate. There may be a cap and a floor rate

attached thereby fixing a maximum and minimum interest rate payable on

it. Floating rate bonds of four year maturity were first issued on September

29, 1995, followed by another issue on December 5, 1995. Recently RBI

issued a floating rate bond, the coupon of which is benchmarked against

average yield on 364 Days Treasury Bills for last six months. The coupon

is reset every six months .

The key features of these securities are:

They are issued at face value.

Coupon or interest rate is fixed as a percentage over a predefined

benchmark rate at the time of issuance. The benchmark rate may

be Treasury bill rate, bank rate etc.

Though the benchmark does not change, the rate of interest may

vary according to the change in the benchmark rate till redemption.

The tenor of the security is also fixed.

Interest /Coupon payment is made on a half yearly basis on its face

value.

The security is redeemed at par (face value) on its maturity date.

23

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 24/60

Bonds with Call/Put Option: First time in the history of Government

Securities market RBI issued a bond with call and put option this year.

This bond is due for redemption in 2012 and carries a coupon of 6.72%.However the bond has call and put option after five years i.e. in year 2007.

In other words it means that holder of bond can sell back (put option) bond

to Government in 2007 or Government can buy back (call option) bond

from holder in 2007. This bond has been priced in line with 5 year bonds.

Capital indexed Bonds: are bonds where interest rate is a fixed

percentage over the wholesale price index. These provide investors with

an effective hedge against inflation. These bonds were floated on

December 29, 1997 on tap basis. They were of five year maturity with a

coupon rate of 6 per cent over the wholesale price index. The principal

redemption is linked to the Wholesale Price Index.

The key features of these securities are:

They are issued at face value.

Coupon or interest rate is fixed as a percentage over the wholesale

price index at the time of issuance. Therefore the actual amount of

interest paid varies according to the change in the Wholesale Price

Index.

The tenor of the security is fixed.

Interest /Coupon payment is made on a half yearly basis on its face

value.

The principal redemption is linked to the Wholesale Price Index.

24

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 25/60

Features of Government Securities

Nomenclature

The coupon rate and year of maturity identifies the government security.

Example: 12.25% GOI 2008 indicates the following:

12.25% is the coupon rate, GOI denotes Government of India, which is the

borrower, 2008 is the year of maturity.

Eligibility

All entities registered in India like banks, financial institutions, Primary

Dealers, firms, companies, corporate bodies, partnership firms,

institutions, mutual funds, Foreign Institutional Investors, State

Governments, Provident Funds, trusts, research organisations and even

individuals are eligible to purchase Government Securities.

Availability

Government securities are highly liquid instruments available both in the

primary and secondary market. They can be purchased from Primary

Dealers. PNB Gilts Ltd., is a leading Primary Dealer in the government

securities market, and is actively involved in the trading of government

securities.

Forms of Issuance of Government Securities

Banks, Primary Dealers and Financial Institutions have been allowed to

hold these securities with the Public Debt Office of Reserve Bank of Indiain dematerialized form in accounts known as Subsidiary General Ledger

(SGL) Accounts.

Entities having a Gilt Account with Banks or Primary Dealers can hold

these securities with them in dematerialized form.

25

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 26/60

In addition government securities can also be held in dematerialized form

in demat accounts maintained with the Depository Participants of NSDL.

Minimum Amount

In terms of RBI regulations, government dated securities can be

purchased for a minimum amount of Rs. 10,000/-only.Treasury bills can be

purchased for a minimum amount of Rs 25000/- only and in multiples

thereof. State Government Securities can be purchased for a minimum

amount of Rs 1,000/- only.

Repayment

Government securities are repaid at par on the expiry of their tenor.

The different repayment methods are as follows :

For SGL account holders, the maturity proceeds would be credited to their

current accounts with the Reserve Bank of India.

For Gilt Account Holders, the Bank/Primary Dealers, would receive the

maturity proceeds and they would pay the Gilt Account Holders.

For entities having a demat account with NSDL, the maturity proceeds

would be collected by their DP's and they in turn would pay the demat

Account Holders

26

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 27/60

Day Count

For government dated securities and state government securities the day

count is taken as 360 days for a year and 30 days for every completed

month. However for Treasury bills it is 365 days for a year.

Example : A client purchases 7.40% GOI 2012 for face value of Rs. 10

lacs.@ Rs.101.80, i.e. the client pays Rs.101.80 for every unit of

government security having a face value of Rs. 100/- The settlement is

due on October 3, 2002. What is the amount to be paid by the client?

The security is 7.40% GOI 2012 for which the interest payment dates are

3rd May, and 3 rd November every year.

The last interest payment date for the current year is 3 rd May 2002. The

calculation would be made as follows:

Face value of Rs. 10 lacs.@ Rs.101.80%.

Therefore the principal amount payable is Rs.10 lacs X 101.80%

=10,18,000

Last interest payment date was May 3, 2002 and settlement date is

October 3, 2002. Therefore the interest has to be paid for 150 days

(including 3 rd May, and excluding October 3, 2002)

(28 days of May, including 3 rd May, up to 30 th May + 30 days of June,

July, August and September + 2 days of October). Since the settlement is

on October 3, 2002, that date is excluded.

Interest payable = 10 lacs X 7.40% X 150 / 360 X 100 = Rs. 30833.33.

Total amount payable by client = 10,18,000+30833.33 = Rs. 10,48,833.33

27

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 28/60

Benefits of Investing in Government Securities

No tax deducted at source

Additional Income Tax benefit u/s 80L of the Income Tax Act for

Individuals

Qualifies for SLR purpose

Zero default risk being sovereign paper

Highly liquid.

Transparency in transactions and simplified settlement procedures

through CSGL/NSDL.

Methods of Issuance of Government Securities

Government securities are issued by various methods, which are as

follows:

Auctions:

Auctions for government securities are either yield based or price based.

The basic features of the auctions are given below:

In an yield based auction, the Reserve Bank of India announces the issue

size(or notified amount) and the tenor of the paper to be auctioned. The

bidders submit bids in terms of the yield at which they are ready to buy the

security.

In a price based auction, the Reserve Bank of India announces the issue

size(or notified amount), the tenor of the paper to be auctioned, as well as

the coupon rate. The bidders submit bids in terms of the price. This

method of auction is normally used in case of reissue of existing

government securities.

28

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 29/60

Method of auction: There are two methods of auction which are followed-

Uniform price Based or Dutch Auction procedure is used in auctions of

dated government securities. The bids are accepted at the same prices as

decided in cut off.

Multiple/variable Price Based or French Auction procedure is used in

auctions of Government dated securities and treasury bills. Bids are

accepted at different prices / yields quoted in the individual bids.

Bids: Bids are to be submitted in terms of yields to maturity/prices as

announced at the time of auction.

Cut off yield: is the rate at which bids are accepted. Bids at yields higher

than the cut-off yield is rejected and those lower than the cut-off are

accepted.

Cut-off yield is set as the coupon rate for the security. Bidders who have

bid at lower than the cut-off yield pay a premium on the security, since the

auction is a multiple price auction.

Cut off price: It is the minimum price accepted for the security. Bids at

prices lower than the cut-off are rejected and at higher than the cut-off are

accepted. Coupon rate for the security remains unchanged. Bidders who

have bid at higher than the cut-off price pay a premium on the security,thereby getting a lower yield. Price based auctions lead to finer price

discovery than yield based auctions.

Notified amount: The amount of security to be issued is ‘notified' prior to

the auction date, for information of the public.

29

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 30/60

The Reserve Bank of India (RBI) may participate as a non-competitor in

the auctions. The unsubscribed portion devolves on RBI or on the Primary

Dealers if the auction has been underwritten by PDs. The devolvement isat the cut-off price/yield.

Underwriting in Auctions

For the purpose of auctions, bids are invited from the Primary Dealers one

day before the auction wherein they indicate the amount to be

underwritten by them and the underwriting fee expected by them.

The auction committee of Reserve Bank of India examines the bids and

based on the market conditions, takes a decision in respect of the amount

to be underwritten and the fee to be paid to the underwriters.

Underwriting fee is paid at the rates bid by PDs , for the underwriting which

has been accepted.

In case of the auction being fully subscribed, the underwriters do not haveto subscribe to the issue necessarily unless they have bid for it.

If there is a devolvement, the successful bids put in by the Primary Dealers

are set-off against the amount underwritten by them while deciding the

amount of devolvement.

On-tap issue

This is a reissue of existing Government securities having pre-determined

yields/prices by Reserve Bank of India. After the initial primary auction of a

security, the issue remains open to further subscription by the investors as

and when considered appropriate by RBI. The period for which the issue is

kept open may be time specific or volume specific. The coupon rate, the

interest dates and the date of maturity remain the same as determined in

30

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 31/60

the initial primary auction. Reserve Bank of India may sell government

securities through on tap issue at lower or higher prices than the prevailing

market prices. Such an action on the part of the Reserve Bank of Indialeads to a realignment of the market prices of government securities. Tap

stock provides an opportunity to unsuccessful bidders in auctions to

acquire the security at the market determined rate.

Fixed coupon issue

Government Securities may also be issued for a notified amount at a fixed

coupon. Most State Development Loans or State Government Securitiesare issued on this basis.

Private Placement

The Central Government may also privately place government securities

with Reserve Bank of India. This is usually done when the Ways and

Means Advance (WMA) is near the sanctioned limit and the market

conditions are not conducive to an issue. The issue is priced at market

related yields. Reserve Bank of India may later offload these securities to

the market through Open Market Operations (OMO).

After having auctioned a loan whereby the coupon rate has been arrived at

and if still the government feels the need for funds for similar tenure, it may

privately place an amount with the Reserve Bank of India. RBI in turn may

decide upon further selling of the security so purchased under the Open

Market Operations window albeit at a different yield.

Open Market Operations (OMO)

Government securities that are privately placed with the Reserve Bank of

India are sold in the market through open market operations of the

Reserve Bank of India. The yield at which these securities are sold may

31

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 32/60

differ from the yield at which they were privately placed with Reserve Bank

of India. Open market operations are used by the Reserve Bank of India to

infuse or suck liquidity from the system. Whenever the Reserve Bank of India wishes to infuse the liquidity in the system, it purchases government

securities from the market, and whenever it wishes to suck out the liquidity

from the system, it sells government securities in the market.

State Government Securities

State Government Securities are securities/loans issued by the Reserve

Bank of India on behalf of various state governments for financing their

developmental needs. These securities are auctioned by the Reserve

Bank of India from time to time. These auctions are of fixed coupon, with

pre announced notified amounts for different states.

Approved Securities

Approved securities are the securities, which are eligible for SLR purposes

under Section 24 of the Banking Regulation Act.

32

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 33/60

MACROECONOMIC INDICATORS

Securities markets are affected by many factors, mainly

macroeconomic indicators.

Growth Indicators :

The most important growth indicators are Gross Domestic Product

(GDP), Gross Domestic Savings (GDS) and Gross Domestic

Capital Formation (GDCF).

Economic growth is the single – most important macroeconomic

variable. It can be defined as the rate at which the real national

product of a country’s economy has grown during a specific time

period.

Gross Domestic Product ( GDP)

The Gross Domestic Product represents the money value of all final

goods and services produced in the country during the given time

period, generally during one year.

Index of Industrial Production ( IIP)

Broadly, an economy can be classified into three sectors,

Agriculture, Industry and Services. Over a period of time each

sector contributes to the GDP growth in the economy. The growth in

the industrial activity of an economy is measured by Index of

Industrial Production (IIP) with reference to base year.

33

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 34/60

Interest Rates

This is defined as the cost of money, which is determined by thedemand and supply of money. Demand is generally related to

industries and investment and supply pertain to savings. There are

two aspects of interest rates – nominal interest rates and real

interest rates. The real interest rate is obtained by subtracting the

expected inflation from the nominal interest rate. Interest rates play

a role in deciding the level of investment activity in the country.

Liquidity Factors

These are the factors which affect the liquidity in cash markets.

Debt security trading is done in cash markets and are cash settled.

Cash Reserve Ratio (CRR)

This represents a bank’s percentage of the net demand and time

liabilities that it has to maintain as a balance with RBI current

account. An increase in the CRR means that more reserves have to

be maintained with RBI, hence leading to tight money conditions.

Statutory Liquidity Reserve (SLR)

Banks are required to maintain daily 25% of their net demand and

time liabilities (NDT) in RBI designated securities. CRR and SLR

serve as monetary policy tools used to signal interest rates and

affect debt markets sentiment from policy point of view.

34

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 35/60

Bank Rate

This is the rate at which RBI rediscounts the securities held by

commercial banks to finance their liquidity needs. The RBI uses

the rate as an interest rate policy signal, and it lays down the basic

interest rate structure.

RBI Reverse Repo Rate

This is the rate at which the RBI borrows the excess liquidity from the

banking system. A lowered rate indicates excess liquidity and that the RBI

is willing to lower the interest rates it will borrow from the inter-bank

market, thereby signaling easy liquidity.

RBI Repo Rate

This is the rate at which the RBI lends the money to the banking system.

Lowered rates indicate the RBI’s preference for lower short-term rates

thereby indicating a lower lifeline.

MONETARY INDICATORS

There are different measures of money supply, which are defined

as M1 , M2 , M3 and M4. Of these, in India M3 is widely used for

indicating the true form of money supply.

The four money supply measures can be defined as follows :

35

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 36/60

M1 = Currency with public + demand deposits + other deposits with RBI

M2 = M1 + Post office Savings Bank Deposits.

M3 = M2 + Time Deposits with Banks.

M4 = M3 + Total Post office Deposits.

Domestic Currency is issued by the central bank to fund investment

activities. A higher than required money supply may lead to inflation as

more money chases fewer goods. The money issued by central bank is

known as reserve money. The banking system, through lending and re-

lending, multiplies the reserve money, and we therefore have

Money Supply = ( Real GDP x Income elasticity of money ) +

( Inflation x price elasticity of money).

INFLATION

Inflation refers to the sustained rise in the general price level over a

given period. In India, the most important measure of inflation is the

Wholesale Price Index ( WPI).

Government normally conduct some periodic surveys to estimate

the proportion of income spent on major goods and services during

the surveyed period. Such commodities will then be given weights

in proportion to the money spent on them based on sample

population expenditure. The initial year’s value of the index of prices

of a select basket of commodities is equated to 100.

36

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 37/60

SECURITIES MATHAMATICS

Time value of Money

The concept of and measurement of the time value of money is

crucial to corporate finance and investment analysis. It helps us to

compare the value of the rupee at different points in time.

Present Value

The present value of single or bullet cash flow is the amount that

must be invested today to get a given amount at a future date.

Present Value = C t / ( 1 + r ) t

C t = Cash flow at time t , r = rate per period , t = number of

Periods.

The present value of multiple cash flows is the sum of the present

values of individual cash flows as shown below :

Present Value = ∑ C t / ( 1 + r ) t

Discount Rate

The money that is invested can earn a return known as the

discount rate. If the investment is made on guaranteed return

instruments, the discount rate is equal to risk free government

securities yield, which is certain and fixed.

37

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 38/60

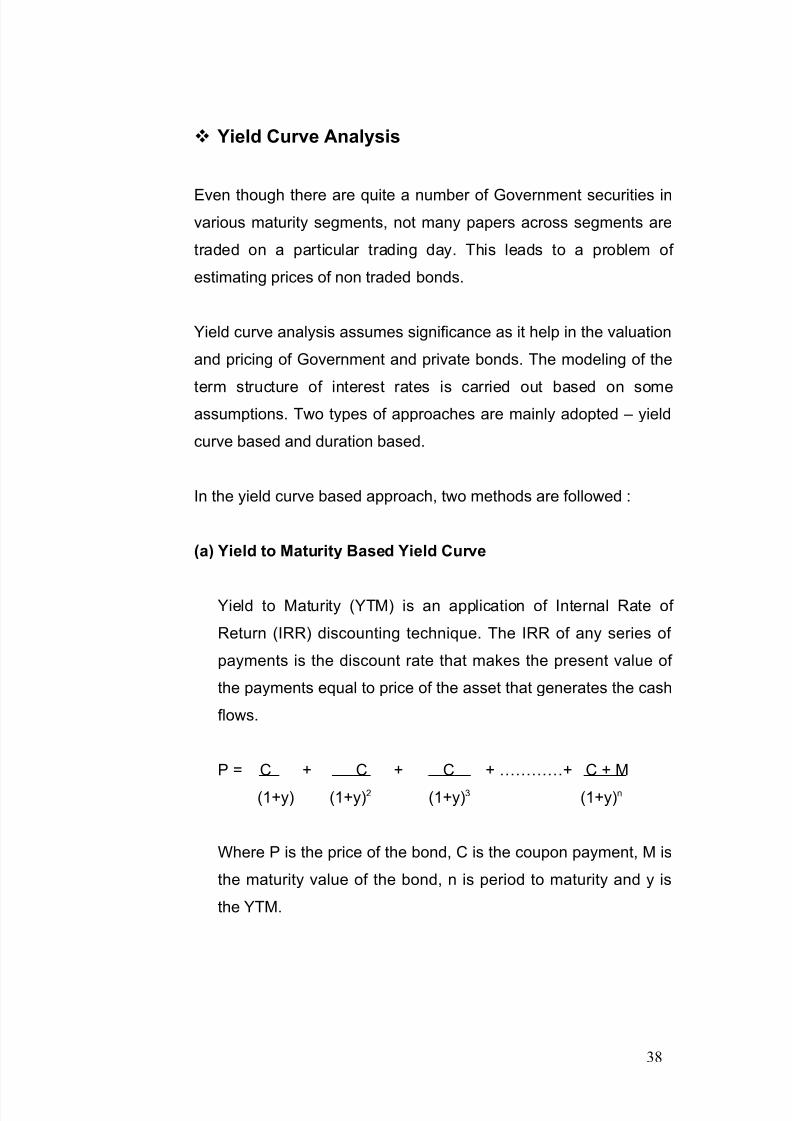

Yield Curve Analysis

Even though there are quite a number of Government securities in

various maturity segments, not many papers across segments are

traded on a particular trading day. This leads to a problem of

estimating prices of non traded bonds.

Yield curve analysis assumes significance as it help in the valuation

and pricing of Government and private bonds. The modeling of the

term structure of interest rates is carried out based on someassumptions. Two types of approaches are mainly adopted – yield

curve based and duration based.

In the yield curve based approach, two methods are followed :

(a) Yield to Maturity Based Yield Curve

Yield to Maturity (YTM) is an application of Internal Rate of

Return (IRR) discounting technique. The IRR of any series of

payments is the discount rate that makes the present value of

the payments equal to price of the asset that generates the cash

flows.

P = C + C + C + …………+ C + M

(1+y) (1+y)2 (1+y)3 (1+y)n

Where P is the price of the bond, C is the coupon payment, M is

the maturity value of the bond, n is period to maturity and y is

the YTM.

38

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 39/60

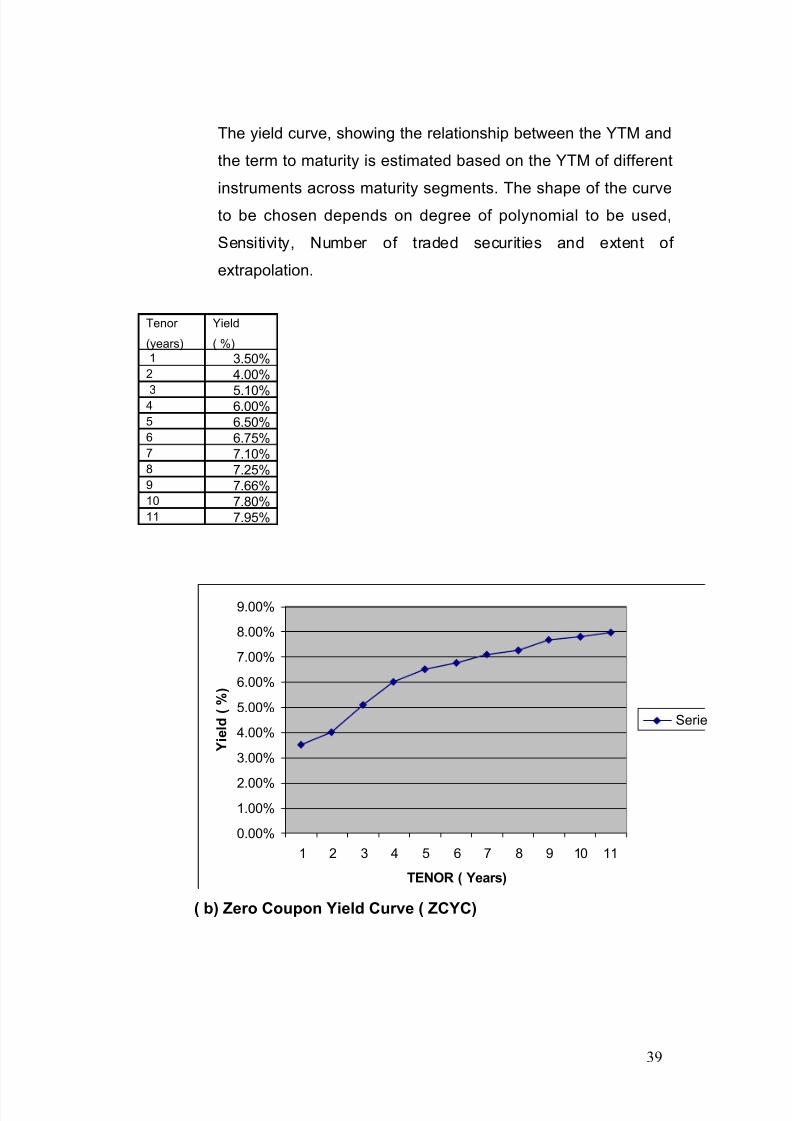

The yield curve, showing the relationship between the YTM and

the term to maturity is estimated based on the YTM of different

instruments across maturity segments. The shape of the curveto be chosen depends on degree of polynomial to be used,

Sensitivity, Number of traded securities and extent of

extrapolation.

Tenor

(years)

Yield

( %)

1 3.50%2 4.00%

3 5.10%4 6.00%5 6.50%6 6.75%7 7.10%8 7.25%9 7.66%10 7.80%11 7.95%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

1 2 3 4 5 6 7 8 9 10 11

TENOR ( Years)

Y i e l d ( % )

Serie

( b) Zero Coupon Yield Curve ( ZCYC)

39

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 40/60

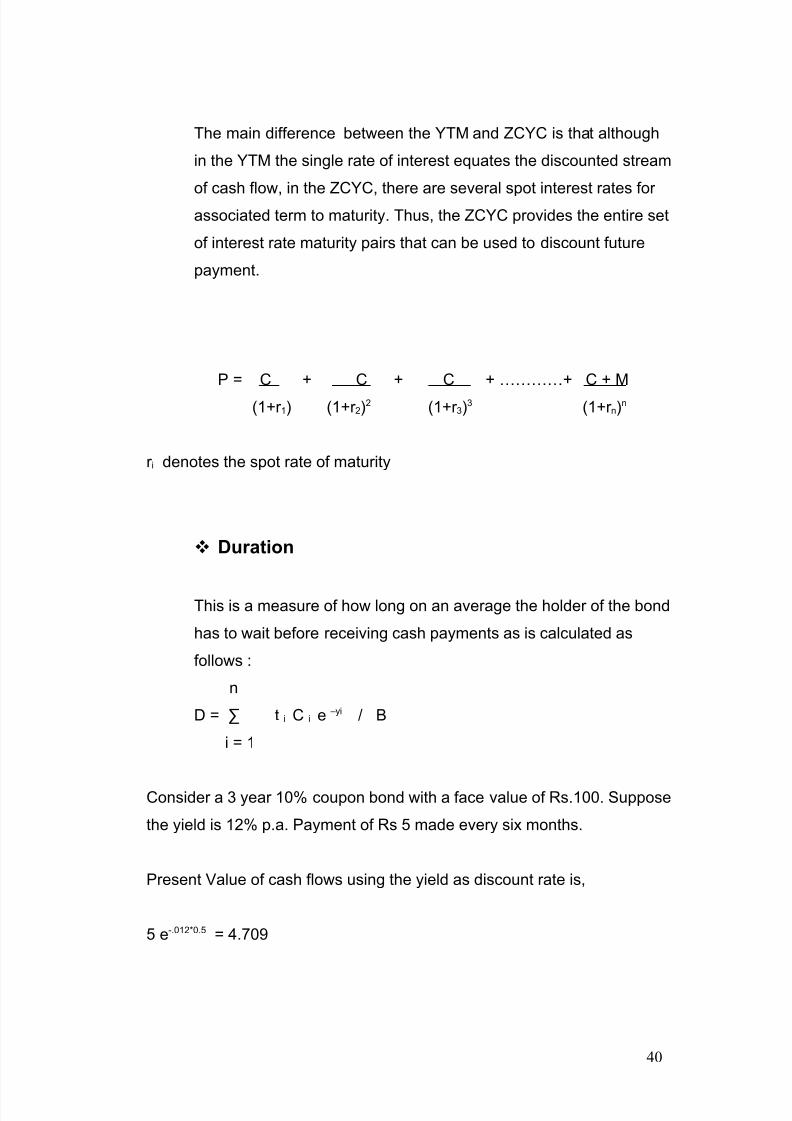

The main difference between the YTM and ZCYC is that although

in the YTM the single rate of interest equates the discounted stream

of cash flow, in the ZCYC, there are several spot interest rates for associated term to maturity. Thus, the ZCYC provides the entire set

of interest rate maturity pairs that can be used to discount future

payment.

P = C + C + C + …………+ C + M

(1+r 1) (1+r 2)2 (1+r 3)

3 (1+r n)n

r i denotes the spot rate of maturity

Duration

This is a measure of how long on an average the holder of the bond

has to wait before receiving cash payments as is calculated as

follows :

n

D = ∑ t i C i e –yi / B

i = 1

Consider a 3 year 10% coupon bond with a face value of Rs.100. Suppose

the yield is 12% p.a. Payment of Rs 5 made every six months.

Present Value of cash flows using the yield as discount rate is,

5 e-.012*0.5 = 4.709

40

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 41/60

Time Cash Flow PV

a

Weight

a/94.213

Time * Weight

0.05 5 4.709 0.050 0.025

1.0 5 4.435 0.047 0.0471.5 5 4.176 0.044 0.066

2.0 5 3.933 0.042 .083

2.5 5 3.704 0.039 0.098

3.0 105 73.256 0.778 2.333

Total 130 94.213 1.00 2.652

Thus duration of security is 2.652 years.

Macaulay Duration

The weighted average time to maturity of a bond is known as the

Macaulay Duration. The weights are the present value of the cash flows.

Larger cash flows get more weight than smaller cash flows. The Macaulay

Duration is defined for a bond with annual cash flow C t , yield to maturity y

and a maturity T as follows :

D mac = { ∑ t * PV ( C t ) } / { ∑ PV ( Ct ) }

Modified Duration

Macaulay’s Duration can be modified slightly to give better risk

measure known as Modified Duration.

Modified Duration = D mac / ( 1 + y/k ) * k

Where k is frequency of compounding and y is yield to maturity.

Modified Duration directly gives the percentage change in price with

a unit change in yield and also be explained as follows :

41

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 42/60

If one holds a bond and the interest rate moves up, the following

two effects can occur :

• The price of the bond goes down

• The reinvestment income of the coupon goes up.

Similarly, vice versa when interest rate moves down.

If this is plotted on a graph in which the x axis shows the time and y axis

shows interest rates, different cash flows occur. The graph will be plotted

for the changes in price and reinvestment income at various interest rates.

Thus the Modified Duration denotes the point where both meet on the x

axis.

Modified Duration as Interest Rate Sensitivity

For a bond, the basic pricing equation is as follows :

P = ∑ C t / ( 1 + y ) t

Differentiating price with respect to yield y,

dP / dy = - ∑ C t * t / ( 1 + y) ( t + 1)

Using the formula for duration,

dP / dy = - (MD) * P

MD = - ( dP /P) / dy

42

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 43/60

Thus Modified Duration is equal to the negative value of the

percentage change in price for a unit change in the yield. Hence,

MD can be used as an interest rate risk measure for bonds.

Convexity

Duration is accurate measure only for small yield changes,

whereas convexity is a measure that ( combined with duration )

allows us to do a better approximation of the price than using just

duration alone. Convexity measures how duration changes withinterest rates and is second derivative of price with respect to yield.

C = 1 d2P

P dy2

REGULATORS FOR THE SECURITY MARKETS

SECURITIES EXCHANGE BOARD OF INDIA ( SEBI)

43

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 44/60

The rise in number of investors was leading to an increase in malpractices

on part of the companies, brokers, merchant bankers, investmentconsultants and various other agencies involved in new issues. This led to

erosion of investor confidence in equity market. The Government and the

stock exchanges were helpless as the existing legal framework was just

not enough. Realizing this, Securities Exchange Board of India (SEBI) was

constituted by the Government of India in April 1988.

The major functions of SEBI are :

1. To promote fair dealings by the issuers of securities and ensure a

market place where funds can be raised at relatively low costs.

2. To provide protection to the investors and safeguard their rights and

interests such that there is steady flow of savings into the market.

3. To regulate and develop a code of conduct and fair practices by the

intermediaries involved in the stock market.

The regulator for the Indian corporate debt market is also Securities and

Exchange Board of India (SEBI). SEBI controls bond market in cases

where entities especially Corporates raise money from public through

public issues.

It regulates the manner in which money is raised and to ensure a fair play

for the retail investor. It forces the issuer to make the retail investor aware

of the risks inherent in the investment and its disclosure norms. SEBI is

also a regulator for the mutual funds and regulates the entry of new mutual

44

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 45/60

funds in the industry. It also regulates the instruments in which these

mutual funds can invest. SEBI also regulates the investments of FIIs.

RESERVE BANK OF INDIA (RBI) :

The Reserve Bank of India is the main regulator for the money market. It

controls and regulates the G-Secs market. Apart from its role as a

regulator, it has to simultaneously fulfill several other important objectives,

such as managing the borrowing programme for the Government of India,

controlling inflation, ensuring adequate credit at reasonable costs to

various sectors of the economy, managing the foreign exchange reserves

of the country and ensuring a stable currency environment.

The RBI controls the issuance of new banking licenses to banks. It

controls the manner in which various scheduled banks raise money from

depositors. Further, it controls the deployment of money through its

policies on CRR, SLR, priority sector lending, export refinancing,

guidelines on investment assets, etc.

The RBI also administers the interest rate policy. Earlier, it used to strictly

control interest rates through a directed system of interest rates. Each type

of lending activity was supposed to be carried out at a pre-specified

interest rate. Over the years, the RBI has moved slowly towards a regime

of market-determined controls.

RESEARCH METHODOLOGY

Research Design : Exploratory

45

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 46/60

Research Approach : Online Training

Research Instrument : Questionnaire

Information Need : Primary / Secondary Data

Area of Survey : Mumbai

Sample Size : 10 Dealers in Equity &Debt

Sampling unit : Individual

Interview method : Personal Interview

Research Design :

The research design used for the study was exploratory in

nature. So as to identify and explore the participation in security

market in India.

Coverage :

Mainly Life Insurance Corporation of India’s equity and Debt

dealing room was covered apart from few visits to Primary

Dealer ISEC’s dealing room.

Data Collection Methods / Sources :

Sources of Data : Data collected for this project study isinclusive of both primary as well as secondary data.

Primary Data : The primary data for this project has been

gathered first hand with the help of a well structured

questionnaire and also with the help of personal interview.

46

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 47/60

Secondary Data : Secondary data information is taken from

websites, books, journals, magazines and newspapers etc.

Sampling Design :

Sample Size :

The sample size is selected 25 respondents.

Sampling Units :

People working in equity dealing room, Debt dealing room ,

Back office and Mid Office.

Data Analysis and Interpretation

47

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 48/60

• Almost entire team of Equity dealing room and Debt dealing room of

two organizations were interviewed through pre tested

questionnaire.

• Debt dealing was observed on line. Strategies adopted during

different situations were studied.

• Use of technical analysis for taking decisions of buy or sell were

studied.

• Use various packages like Newswire 18, Reuters were handled for

various news related to Debt Market and Equity Market.

• Impact of release of economic data on market was studied in detail.

• Various segments of Government securities like short term, medium

term and long term were studied to understand yield movement.

• FIMMDA valuation of securities was studied to understand yield

curve of illiquid securities.

• Use of FIMMDA spread for pricing non SLR securities was

understood for different ratings like AAA, AA+, BBB etc.

48

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 49/60

• Mark to Market valuation of Govt. Securities, State Govt. Securities

and Approved securities was learned practically on Excel Sheet.

• Analysis of Duration, Modified Duration and Convexity for small

portfolio was studied to take strategic decisions.

• Use of Reuters package for plotting yield curve of various securities

with historic data was learned and analysis technique for future

yield projection was done.

• Impact of macroeconomic indicators on security market was

analyzed.

• Electronic bidding system for auction of Central / State Govt.

securities was understood.

• Strategy of switching short term securities with long term securities

adopted mostly by Insurance Companies and its impact on market

was studied.

• Attempt was made to understand the concept of When Issued

Market and Short Selling.

• Participants in Government security market and their responses to

price fluctuations were studied .

• Role of Brokers in Equity as well as Government security market

was understood.

49

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 50/60

• Year wise volume of Government securities was studied and plotted

on graph as shown below.

Year Net Traded

Value Rs. In

Crore

2005 887293

2006 475523

2007 219106

2008 282317

2009 335951

2010 563815

• Investment pattern of Insurance Companies was understood and

their preferences for various class of investments was studied.

50

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 51/60

• Attempt was made to understand Asset – Liability matching

process .

• Monetary Policy and its impact on market was studied.

FINDINGS

OBSERVATIONS :

51

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 52/60

Insurance companies invest chunk of their surplus in Central /

State Government securities as compared to their investment in

equity markets.

Government Securities market is much interesting than equity

market though retail participation is very less.

Technology has changed the market remarkably and helped in

increased participation.

Money Markets also has impact to great extent on security markets.

Security market in short term segment is mostly run by traders than

investors.

There are good opportunities in Government securities market for

profit making by creating trading portfolio.

Reserve Bank of India has good control over security market. It

discourage any off market deal.

Non SLR market is not yet developed as SLR.

RECOMMENDATIONS :

52

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 53/60

Investors should undertake an analysis before investing into the

stock market, as most of the investors do not undertake any

systematic study before entering into any stock.

Individual investors have very less knowledge of capital market.

Their knowledge can be improved by conducting seminars,

workshops on capital market, mainly Government securities

market.

There should be stability in securities market and the factors

which influence the securities market should be properly

analyzed and controlled, volatility should be reduced and risk

factors should be taken care of.

Decisions based on only technical analysis should be avoided

and fundamental analysis has to be done for proper decision

making.

The regulatory authority should keep a check on market

mechanism and bring about a stable guaranteed return to the

retail investor. The investment should be protected. Investor

should shift their focus from fixed income securities to capital

market securities.

Advance technology should be used more and more vigorously

to avoid frauds.

Recommendations by Respondents

• Only genuine company should be allowed to raise capital.

53

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 54/60

• Risk Management has to be given more importance.

• Investor should be taught about when to enter the market

and when to exit.

• No hidden cost of brokerage.

• Arbitrage opportunities for FII should not prevail in the

market.

• More transparency is required.

• Fair valuation of IPOs.

• Role of Regulator to avoid circular trading.

• Arrange investors meetings for guidance and knowledge

sharing.

LIMITATIONS

The survey was limited to only two organization in Mumbai.3

54

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 55/60

Unwillingness of respondents to reveal the information due to data

security purposes.

Conclusions were based on small amount of data.

The secondary data collected is restricted to certain contents.

Recommendations and findings are purely based on primary data.

Practical knowledge is more required to understand many concepts

and procedures in securities market.

Hands on training not possible due to severity of mistake if any in

Government securities market.

Much awareness is not there in respect of SLR market.

EXPECTED CONTRIBUTION FROM THE STUDY

55

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 56/60

A overall understanding of Equity Market and Debt Market.

Investment preferences of Institutional Investors depending onmarket conditions.

Understanding volatility in the security market.

Price Yield relationship.

Management of Risk in equity as well as debt market.

Understanding Bond Mathematics.

Strategies to be adopted in different market situations.

Use of Duration, Modified Duration and Convexity as tools of

portfolio management.

Impact of macroeconomic factors on security markets.

Efforts to be taken by regulators to increase retail participation in

debt market.

Understanding role of regulators to control the market.

ANNEXURE

56

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 57/60

QUESTIONNAIRE

EQUITY MARKET :

1. Name of the Dealer : __________________________________

2. No of years of experience in equity dealing ________ years.

3. Which exchange do you prefer to trade

BOTHס BSEס NSEס

4. How release of economic data impact the market.

5. Which industry is preferred for investment.

6. How decisions of investment in different sectors is taken.

DEBT MARKET :

1. Name of the Dealer : __________________________________

2. No of years of experience in equity dealing ________ years.

3. How mandate for purchases is obtained.?

4. Whether trading portfolio is maintained ?

5. How decisions of investment in various segments is taken?

57

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 58/60

7. What percentage of surplus is invested in debt market?

8. How bids / offers are put in NDS / NDS OM system ?

9. Whether NDS or NDS OM system is preferred ?

10. What percentage of deals are done through brokers?

11.Whether deals are done only through empanelled brokers?

12.What is structure of brokerage to be paid?

13. How decisions about entry and exit from the market are taken ?

14. How frequently RBI conducts Central / State Govt. security

auctions?.

15.How auction bids are put in the system.

16.What are the possible actions in response to auctions results?

17.How many participants are there in government securities market?

18.Is the role of brokers in government security market significant?

19.How frequently switch deals are executed ?

20.What is the methodology used in case of switch deals.?

21. How release of economic data impact the security market ?

58

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 59/60

22. What actions are taken before and after the release of economic

data ?

23.How risk management is used in securities market ?

24.What is role of Back Office in securities market ?

25.What role is played by Mid Office in securities market ?

26. What are the market timings ?

27.Impact of decisions taken in Monetary Policy or Review of Monetary

Policy on securities market?

28.How regulators play their role in securities markets?

29.How settlement of deals take place ?

30.Whether concept of margin money is applicable for settlement of

deals in securities market ?

31.What are the various systems / packages used in dealing room?

BIBLIOGRAPHY

59

8/6/2019 Mba Project Mod

http://slidepdf.com/reader/full/mba-project-mod 60/60

WEBSITES :

www.moneycontrol.com

www.fimmda.org.in

www.nseindia.com

www.bseindia.com

www.rbi.org.in

www.sebi.gov.in

www.capitalmarket.com

www.ccil.co.in

NEWSPAPERS

Economic Times

DNA Money

Business Standard

Mint

Top Related