Languages

Pages

Legal

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

1

IPO Note: Mahindra Logistics Ltd.

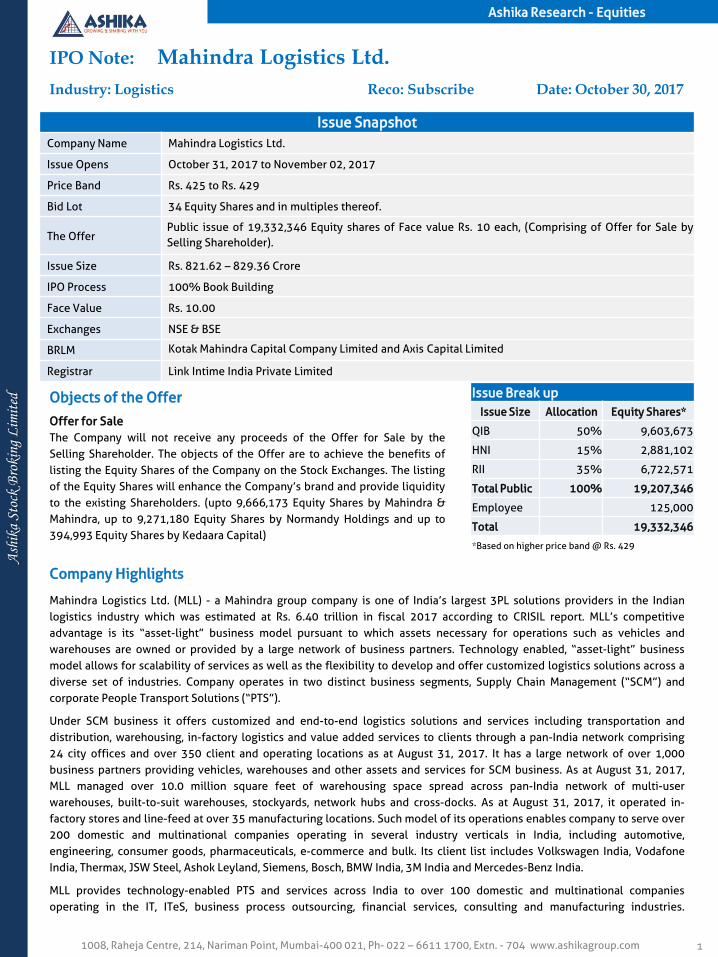

Issue Snapshot

Company Name Mahindra Logistics Ltd.

Issue Opens October 31, 2017 to November 02, 2017

Price Band Rs. 425 to Rs. 429

Bid Lot 34 Equity Shares and in multiples thereof.

The Offer Public issue of 19,332,346 Equity shares of Face value Rs. 10 each, (Comprising of Offer for Sale by

Selling Shareholder).

Issue Size Rs. 821.62 – 829.36 Crore

IPO Process 100% Book Building

Face Value Rs. 10.00

Exchanges NSE & BSE

BRLM Kotak Mahindra Capital Company Limited and Axis Capital Limited

Registrar Link Intime India Private Limited

Industry: Logistics Reco: Subscribe Date: October 30, 2017

1008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

Issue Break up

Issue Size Allocation Equity Shares*

QIB 50% 9,603,673

HNI 15% 2,881,102

RII 35% 6,722,571

Total Public 100% 19,207,346

Employee 125,000

Total 19,332,346

*Based on higher price band @ Rs. 429

Company Highlights

Mahindra Logistics Ltd. (MLL) - a Mahindra group company is one of India’s largest 3PL solutions providers in the Indian

logistics industry which was estimated at Rs. 6.40 trillion in fiscal 2017 according to CRISIL report. MLL’s competitive

advantage is its “asset-light” business model pursuant to which assets necessary for operations such as vehicles and

warehouses are owned or provided by a large network of business partners. Technology enabled, “asset-light” business

model allows for scalability of services as well as the flexibility to develop and offer customized logistics solutions across a

diverse set of industries. Company operates in two distinct business segments, Supply Chain Management (“SCM”) and

corporate People Transport Solutions (“PTS”).

Under SCM business it offers customized and end-to-end logistics solutions and services including transportation and

distribution, warehousing, in-factory logistics and value added services to clients through a pan-India network comprising

24 city offices and over 350 client and operating locations as at August 31, 2017. It has a large network of over 1,000

business partners providing vehicles, warehouses and other assets and services for SCM business. As at August 31, 2017,

MLL managed over 10.0 million square feet of warehousing space spread across pan-India network of multi-user

warehouses, built-to-suit warehouses, stockyards, network hubs and cross-docks. As at August 31, 2017, it operated in-

factory stores and line-feed at over 35 manufacturing locations. Such model of its operations enables company to serve over

200 domestic and multinational companies operating in several industry verticals in India, including automotive,

engineering, consumer goods, pharmaceuticals, e-commerce and bulk. Its client list includes Volkswagen India, Vodafone

India, Thermax, JSW Steel, Ashok Leyland, Siemens, Bosch, BMW India, 3M India and Mercedes-Benz India.

MLL provides technology-enabled PTS and services across India to over 100 domestic and multinational companies

operating in the IT, ITeS, business process outsourcing, financial services, consulting and manufacturing industries.

Objects of the Offer

Offer for Sale

The Company will not receive any proceeds of the Offer for Sale by the

Selling Shareholder. The objects of the Offer are to achieve the benefits of

listing the Equity Shares of the Company on the Stock Exchanges. The listing

of the Equity Shares will enhance the Company’s brand and provide liquidity

to the existing Shareholders. (upto 9,666,173 Equity Shares by Mahindra &

Mahindra, up to 9,271,180 Equity Shares by Normandy Holdings and up to

394,993 Equity Shares by Kedaara Capital)

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

21008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

As at August 31, 2017, it operated PTS business in 12 cities and over 120 client and operating locations across India.

Certain key clients in India for PTS business include Tech Mahindra, AXISCADES Engineering and ANZ Support Services.

Company’s subsidiary, 2X2 Logistics, provides logistics and transportation services to OEMs to carry finished automobiles

from the manufacturing locations to stockyards or directly to the distributors through specially designed vehicles. MLL’s

other subsidiary, Lords, provides international freight forwarding services for exports and imports, customs brokerage

operations, project cargo services and charters.

An “asset-light” business model helps MLL to reduce capital expenditure requirements, mitigate the effects of operational

risks relating to direct fuel costs, maintenance costs and depreciation in addition to reducing the effect of any risks

emanating from changes in laws and regulations. This also enables it to deploy and utilize capital more efficiently, as

reflected in company’s adjusted ROE which is at 33.77% in FY17. Revenue from the SCM division, which contributed ~89%

to total revenue in FY17, has grown at a CAGR of 17% over FY13-17 to ~Rs24bn with the larger share coming from Non-

Mahindra group. The revenue from operations of SCM business, attributable to Non-Mahindra group clients, has increased

at a CAGR of ~65% over FY15-17 to Rs9.5bn, reducing its dependence on the Mahindra group. The PTS business,

comprising 10% of total revenue, has also seen a steady growth of 5% CAGR over FY13-17 to Rs2.9bn.

View

Mahindra Logistic ltd. (MLL), a part of Mahindra & Mahindra group, is one of the largest 3rd party logistic (3PL) solution

providers in Indian logistic industry. MLL is an asset light, integrated, end to end and technology driven 3PL company with

presence in two distinct business segments including Supply chain management (SCM) and Corporate people transport

solutions (PTS). In SCM segment, it offers customized and end to end logistics solution & services, including transportation,

distribution, warehousing, in-factory logistics and value-added services to various clients. In PTS business, MLL provides

technology-enabled people transportation solutions & services across India to over 120 domestic as well as MNCs

operating in IT, ITeS, BPO, Financial Services, Consulting and Manufacturing industries. Company’s SCM division contributes

~89% of the total revenue, while PTS division contributes rest of the revenue. During FY13-17, revenue from SCM segment

has increased at a CAGR of 17%, with larger share contributed by non-Mahindra GROUP. Revenue from Non-Mahindra

group has increased at a CAGR of ~65% over FY15-17, thus gradually reducing its dependence on the Mahindra Group. In

SCM segment, company offers services to various industries across India including automotive, engineering, consumer

goods, pharmaceuticals, e-commerce and bulk. The company has a pan India network comprising 24 city offices and a large

network of over 1,000 business partners, providing assets such as vehicles, warehouses and other services to ~350 clients.

As per the management, in SCM segment, transportation : warehousing mix is at 86%:14% vs industry average at

89%:11%. MLL intends to take warehousing share higher in bid to get GST related benefits. Further, as per business

segment wise warehousing commands higher margins vs transportation. In SCM segment, MLL has 180 non M&M

customers, with top 25 clients contributing 70% of non M&M business. Currently, MLL is managing over 10mn sqft of

warehousing space spread across India under various heads such as multi-user warehouses, built-to-suit warehouses,

stockyards, network hubs and cross-docks. Currently, MLL operated in-factory stores and line-feed at over 35

manufacturing locations across the country. Further, MLL has recently set up a warehouse in Gurugram with an aggregate

space of 191,000 sqft, which is well connected to several manufacturing and consumption clusters in India. It is also in the

process of setting up additional large format and multi-user warehouses in certain strategic locations on a long-term lease

basis. Company has two subsidiary named “2X2 logistics”, which provides logistics and transportation services to OEMs

and “Lords”, which provides international freight forwarding services for exports and imports.

On financial front, MLL registered a revenue growth of 15% CAGR over FY13-17, while EBITDA grew at a CAGR of 20%

during the same period. Net profitability growth during FY13-17, grew at a pace of 17% CAGR. At net level, company

earned lower margin of 1.7% which is a drag on its financial performance. The issue is comprised of offer for sale from

promoters and other strategic investors. India has high logistic cost as compared to developed and other emerging

countries. Thus, there is immense potential in Indian logistic space given its long term growth opportunity. MLL is well

positioned to gain an uptick in the logistic sector on the back of its strong parentage, asset light business model and large

network of business partners. Further, logistic sector would be benefited most from the rollout of GST. On valuation front,

at upper price band the issue is valued at P/E multiple 66x on FY17 EPS. Due to its asset light model, there is no exact

comparable peer. Given its strong parentage, asset light model, attractiveness of GST in logistic sector and steady

financials, we recommend “SUBSCRIBE” on the issue from long term investment perspective.

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

31008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

(In Rs. Cr) FY13 FY14 FY15 FY16 FY17 Q1FY18

Cash flow from Operations Activities 48.4 48.7 26.8 (47.9) (29.3) (7.5)

Cash flow from Investing Activities (1.8) (3.9) (164.8) 1.0 53.4 (0.4)

Cash flow from Financing Activities (6.4) 1.7 102.9 18.4 2.4 3.7

Net increase/(decrease) in cash and cash equivalents 40.3 46.5 (35.1) (28.5) 26.5 (4.2)

Cash and cash equivalents at the beginning of the year 0.4 40.7 87.2 52.1 23.6 50.2

Cash and cash equivalents at the end of the year 40.7 87.2 52.1 23.6 50.2 45.9

Source: RHP

Comparison with listed industry peers

Financial Statement

Cash Flow Statement

(In Rs. Cr) FY13 FY14 FY15 FY16 FY17 Q1FY18

Share Capital 57.7 59.1 59.8 59.8 68.0 68.0

Net Worth 85.9 124.3 268.2 304.7 352.4 368.7

Long Term Borrowings 0.0 0.0 0.1 20.1 19.8 24.1

Other Long Term Liabilities 7.2 8.2 11.1 14.0 13.1 14.0

Short-term borrowings 0.0 0.0 3.9 3.5 8.2 7.5

Other Current Liabilities 168.1 202.5 235.6 249.1 423.2 473.5

Fixed Assets 10.5 15.8 26.0 52.4 62.2 71.6

Non Current Assets 35.2 31.9 27.7 56.6 80.9 96.3

Current Assets 215.6 287.4 465.2 482.5 673.6 720.0

Total Assets 261.2 335.0 518.8 591.5 816.7 888.0

Revenue from Operations 1532.1 1750.7 1930.9 2063.9 2666.6 852.5

Revenue Growth (%) 14.3 10.3 6.9 29.2

EBITDA 36.5 51.3 57.0 52.3 76.2 26.5

EBITDA Margin (%) 2.4 2.9 3.0 2.5 2.9 3.1

Net Profit 24.4 36.6 38.5 36.0 46.1 15.1

Net Profit Margin (%) 1.6 2.1 2.0 1.7 1.7 1.8

Earnings Per Share (Rs.) 4.2 6.3 6.6 5.4 6.7 2.2

Return on Networth (%) 28.4 29.5 14.8 12.1 13.1 4.1

Net Asset Value per Share (Rs.) 14.9 21.1 44.2 50.5 51.1 53.4

Source: RHP, Ashika Research

Company believes that none of the listed companies in India have a business model and asset structure similar to the

Company.

Ash

ika

Stoc

k B

roki

ng L

imit

edAshika Research - Equities

41008, Raheja Centre, 214, Nariman Point, Mumbai-400 021, Ph- 022 – 6611 1700, Extn. - 704 www.ashikagroup.com

Ashika Stock Broking Limited (“ASBL”) or Research Entity has started its journey in the year 1994 and is engaged in the business of broking services,

depository services, distributor of financial products (Mutual fund, IPO & Bonds). This research report has been prepared and distributed by ASBL in the

sole capacity of a Research Analyst (Reg No. INH000000206) of SEBI (Research Analyst) Regulations 2014. ASBL is a wholly owned subsidiary of Ashika

Global Securities (P) Ltd., a RBI registered non-deposit taking NBFC Company. Ashika group (details is enumerated on our website

www.ashikagroup.com) is an integrated financial service provider inter alia engaged in the business of Investment Banking, Corporate Lending,

Commodity Broking, Debt Syndication & Other Advisory Services.

There were no significant and material disciplinary actions against ASBL taken by any regulatory authority during last three years.

Disclosure

ASBL or its associates, its Research Analysts (including their relatives) may have financial interest in the subject company(ies). However, the said

financial interest is not limited to having an open stock market position in /acting as advisor to /having a loan transaction with the subject company(ies)

apart from registration as clients.

1) ASBL or its Research Analysts (including their relatives) do not have any actual / beneficial ownership of 1% or more of securities of the subject

company(ies) at the end of the month immediately preceding the date of publication of this report or date of the public appearance. However

ASBL's associates may have actual / beneficial ownership of 1% or more of securities of the subject company(ies).

2) ASBL or their Research Analysts (including their relatives) do not have any other material conflict of interest at the time of publication of this

research report or date of the public appearance. However ASBL's associates might have an actual / potential conflict of interest (other than

ownership).

3) ASBL or its associates may have received compensation for investment banking, merchant banking, and brokerage services and for other products

and services from the subject companies during the preceding 12 months. However, ASBL or its associates or its Research analysts (forming part

of Research Desk) have not received any compensation or other benefits from the subject companies or third parties in connection with the

research report. Moreover, Research Analysts have not received any compensation from the companies mentioned herein in the past twelve

months.

4) ASBL or their Research Analysts have not managed or co–managed public offering of securities for the subject company(ies) in the past twelve

months. However ASBL's associates may have managed or co–managed public offering of securities for the subject company(ies) in the past

twelve months.

5) Research Analysts have not served as an officer, director or employee of the companies mentioned in the report.

6) Neither ASBL nor its Research Analysts have been engaged in market making activity for the companies mentioned in the report.

Disclaimer

The research recommendation and information herein are solely for the personal information of the authorized recipient and does not construe to be

an offer documents or any investment, legal or taxation advice or solicitation of any action based upon it. This report is not for public distribution or use

by any person or entity, where such distribution, publication, availability or use would be contrary to law, regulation or subject to any registration or

licensing requirement. We will not treat recipients as customer by virtue of their receiving this report. The report is based upon the information

obtained from public sources that we consider reliable, but we do not guarantee its accuracy or completeness. ASBL shall not be in anyways responsible

for any loss or damage that may arise to any such person from any inadvertent error in the information contained in this report. The recipients of this

report should rely on their own investigations.

Name Designation Email ID Contact No.

Paras Bothra President Equity Research [email protected] +91 22 6611 1704

Krishna Kumar Agarwal Equity Research Analyst [email protected] +91 33 4036 0646

Partha Mazumder Equity Research Analyst [email protected] +91 33 4036 0647

Arijit Malakar Equity Research Analyst [email protected] +91 33 4036 0644

Kapil Jagasia Equity Research Analyst [email protected] +91 22 6611 1715

Tirthankar Das Technical & Derivative Analyst [email protected] +91 33 4036 0645

Research Team

Top Related