Languages

Pages

Legal

Opportunities and Challenges at the Interface between Petrochemistry and Refinery DGMK/SCI-Conference October 10-12, 2007, Hamburg, Germany

Light Olefins – Challenges from new Production Routes ? H. Zimmermann Linde Engineering, Pullach, Germany

Abstract Light Olefins are the building blocks for many modern plastic products and are produced in large quantities. Driven by high crude oil prices, production is shifted to regions with low cost raw materials. Alternatives to the traditional production from Naphta, AGO and other crude products are becoming attractive. This paper evaluates several methods Ethylene and Pro-pylene production economically and also the regional advantageous routes. The analysis includes Steamcracking, dehydrogenation, dehydration of Ethanol, Methanol based routes and olefin conversion by Metathesis.

Introduction Almost 200 million t/a of light olefins are produced and processed to a variety of products. The production of the bulk products Ethylene and Propylene is traditionally based on Steam-cracking and separation of off-gases from refinery processes. However, today, with the dramatic change of raw material costs due to crude oil price development, a number of new processes are being utilized for the production of light olefins.

1. Light Olefin Production Routes The petrochemical production routes for light olefins are Steamcracking of hydrocarbons from Ethane to Naphta, AGO and even Hydrocracker bottoms, dehydrogenation of hydro-carbons, dehydration of alcohol, Methanol based routes and Metathesis. Economic comparison of the different routes is complex, since some routes (Naphtacracking) produce many valuable by-products. A first comparison can be made on the basis of selec-tivity of the routes as shown in Fig. 1. Due to the low conversion per pass, the Dehydrogenation of Ethane can be excluded for commercial production, as this route is not competitive to cracking of Ethane. The other processes have to be evaluated in detail in order to see the commercial competitiveness.

2. Steamcracking of Hydrocarbons Steamcracking of hydrocarbons is the most important method of producing Ethylene and Propylene today. Ethylene production is almost exclusively utilizing this route, whereas 70 % of the Propylene is produced via Steamcracking today. Steamcracking technology has been used for more than 50 years and can be summarized as shown below in Fig. 2.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 75

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

6 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Light Olefins – Production Routes

Selectivity % Conversion %

Cracking of Ethane 82-84 64-75

Dehydro of Ethane 80 15-20

Dehydration of EtOH 97 -99 70-100

MTO 70 (E+P) 100

MTP 70 (P) 100

Metathesis 90

Dehydro of Propane 85-90 35-50

Fig. 1: Light Olefin Production Routes

Linde Engineering

7 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Steamcracking

Feed C2 H 4 , C 3 H 6 , C 6 H 12 , C H 4 + PyGas (C5-C10) +PFO(C10+ )

820 -860 °C

0,2-0,5 sec

Feed Steam / Feed (Typical)

Ethane 0, 3 ( wt/wt)

Propane 0,4

Naphta 0,5

AGO 0,6

HVGO 0,8

Steam

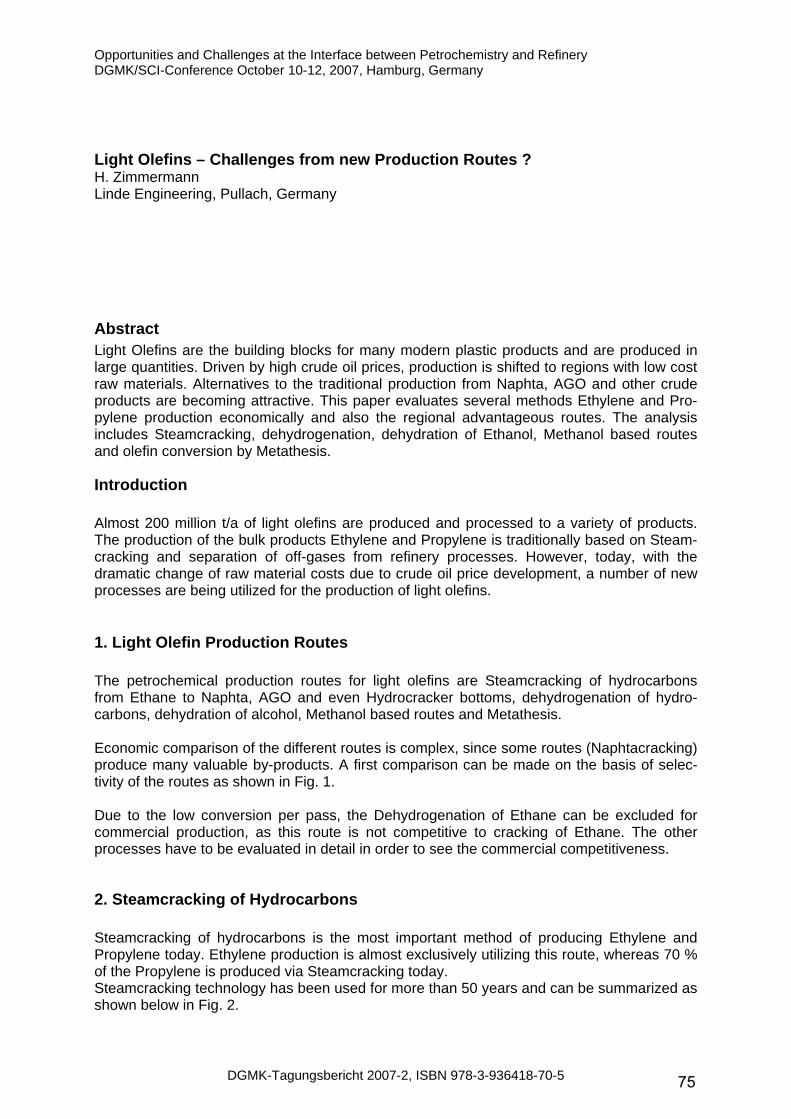

Fig. 2: Steamcracking of Hydrocarbons The cracking reaction is carried out in cracking furnaces as shown in Fig. 3.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 76

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

9 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Steamcracking Furnace

Fig. 3: Cracking Furnace Modern Steamcracking Plants have capacities of up to 1.5 million t/a Ethylene and a total olefin production (Ethylene + Propylene) up to 1.8 million t/a. Investment costs for such plants are in the range of 1 billion Euros. A typical view of a cracker is shown in Fig. 4.

Linde Engineering

10 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

3D Model View of a Steamcracker

260 m260 m

230 m230 m

Fig. 4: 3D View of a Steamcracker

Typical cracking yields for the different feedstocks are shown in Fig. 5.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 77

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

15 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Steam Cracking Yields ( wt % ex Furnace)

HCR

0.68

9.38

0.43

29.64

2.77

16.83

0.37

11.17

17.73

10.98

0.80

177%

Feedstock

H2 + CO

CH4

C2H2

C2H4

C2H6

C3H6 + C3H4

C3H8

C4

Pyrolyis Gasoline

Pyrolysis Fuel Oil

Dilution Steam / HC

Total HC Load

Ethane

4.06

3.67

0.50

52,45

34.76

1.15

0.12

2.24

0.87

0.16

0.30

100%

Propane

1.70

23.37

0.67

39.65

4.57

13.28

7.42

4.03

4.27

1.11

0.35

132%

FR Naphtha

1.03

15.35

0.69

31.02

3.42

16.21

0.38

9.54

19.33

3.01

0.50

169%

AGO

0.71

10.69

0.34

24.85

2.75

14.28

0.31

9.61

20.6

15.78

0.80

211%

Fig. 5: Cracking Yields

As can be seen from the Fig. 5 Ethane can be cracked very selectively compared to Ethyl-ene, whereas all other feedstocks produce significant quantities of by-products such as Methane, Propylene, C4- cut, Benzene, Pygas (Pyrolysis Gasoline) and Pyrolysis Fuel Oil (PFO). The attractiveness of Ethane cracking can be explained by the selectivity but also the regionally advantaged Ethane price contributes to the outstanding economics of Ethane cracking. Costs of 0,75 to 1,6 USD per MM BTU equivalent to 40 to 85 USD /t are typical for Middle East locations and countries like Venezuela, where several cracker projects are in the planning phase. Low cost Ethane cracking has an advantage of 300 to 400 USD per t of Ethylene in produc-tion costs compared to Naphta cracking at market price. The huge difference is the driver for all new investments in areas with advantaged feedstock costs as shown in Fig. 6.

Linde Engineering

21 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Market - Feedstocks

China

South EastAsia

Middle Eastcountries Iran,

Iraq, Qatar,UAE

WestAfrica

AlgeriaEgypt

Caspian

Norway

Gulfof Mexico

Peru,Colombia,

Ecuador andVenezuela

Key Areas of Oil & Gas ExplorationKey Areas of Oil & Gas Exploration

Fig. 6: Key Areas with advantaged feedstock costs

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 78

Opportunities and Challenges at the Interface between Petrochemistry and Refinery The detailed comparison of Ethylene production costs by cracking of Ethane and Naphta is shown in Fig. 7 on the basis of a 1 million t/a cracker including raw materials, capital costs, operation costs as well as overhead and maintenance costs.

Linde Engineering

24 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Comparison Ethane / Naphtacracker (Basis 1MM MTA)Production Costs 2007

0,00

100,00

200,00

300,00

400,00

500,00

600,00

700,00

800,00

900,00

Ethan Naphta Naphta / Europe fully depreciated

Plant

USD /t Ethylene

Raw MaterialDepreciation

Operation

Overhead

Fig. 7: Comparison of Ethane and Naphta cracking Fig. 7 also indicates that a fully depreciated cracker in Europe has excellent economics but cannot reach the production cost of an Ethane cracker. However, Ethane availability is limited in the Middle East and other raw materials have to be utilized. Fig. 8 shows a comparison between new Saudi Cracker economics and an existing European cracker and one can see that due to a discount of 30% for some feedstocks, cracking in this area is advantaged. Without the discount, the situation would be different and the European cracker would be quite competitive.

Linde Engineering

25 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Saudi Crackers (new) compared with European (existing)Discount of 30% on Propane and Butane

0

100

200

300

400

500

600

700

800

900

Ethan E/P 50/50 Butan E/B 50/50 Naphta / Europe

USD / ton of Ethylene

Fig. 8: Comparison of Crackers based on different feedstocks

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 79

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

3. Alternative Processes for Ethylene Production An alternative route for production of Ethylene is the dehydration of Ethanol, which has a very high selectivity. A summary of the production costs by Ethanol dehydration are shown in Fig. 9.

Linde Engineering

26 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Dehydration of EthanolC2H5OH ------- C2H4 + H2O ( Cat , 300°C)

Production: 500 000 MTA Ethylene Per ton C2H4

S: ,097

Weight Yield : 60,86 %

Raw Material: 846 966 MTA @ 300 USD (400) 508 USD (677)

Investment 500 MM USD @20% 200 USD

Operation 20 USD

Overhead & Maintenance @ 5% of Invest 50 USD

Sum production Cost 778 USD (947)

Fig. 9: Summary of Ethylene production costs via Ethanol dehydration Methanol-based Ethylene production via MTO is one of the routes which creates a lot of interest. A process is offered by UOP / Hydro based on a special zeolithe catalyst. The process flow diagram is shown in Fig. 10.

Linde Engineering

11 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

UOP /Hydro MTO process

RegenRegen GasGas

AirAir

MethanolMethanol

DMERecovery

WaterWater

ReactorReactor RegeneratorRegeneratorQuenchQuenchTowerTower

RegenRegen GasGas

AirAir

MethanolMethanol

DMERecovery

WaterWater

ReactorReactor RegeneratorRegeneratorQuenchQuenchTowerTower

Mixed CMixed C44

PropanePropane

EthaneEthane

Tail GasTail Gas

EthyleneEthylene

PropylenePropylene

CC55++

DryerDryer

CC22HH22ReactorReactor

Caustic Caustic WashWash DeDe--CC2 2 DeDe--CC11

CC22SplitterSplitter

CC33SplitterSplitterDeDe--CC33 DeDe--CC44

Mixed CMixed C44

PropanePropane

EthaneEthane

Tail GasTail Gas

EthyleneEthylene

PropylenePropylene

CC55++

DryerDryer

CC22HH22ReactorReactor

Caustic Caustic WashWash DeDe--CC2 2 DeDe--CC11

CC22SplitterSplitter

CC33SplitterSplitterDeDe--CC33 DeDe--CC44

Source : UOP

Fig. 10: UOP / Hydro MTO process

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 80

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

The economics for Ethylene production via MTO are shown in detail in Fig. 11.

Linde Engineering

27 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

MTO Economics for Ethylene

750 000 MTA Ethylene

750 000 Propylene Per ton Ethylene

Raw Material 3 428 571 MeOH @ 200 USD (250) 1306 (1632)

Byproduct Credit - 1040

Net Raw Material 266 (592)

Investment 2 500 MM USD @20 % 666

Operation 13

Maintenance & Overhead @ 5 % of Invest 166

Production Cost 1112(1439)

Fig. 11: MTO economics for Ethylene production

A comparison of production economics for all Ethylene routes is shown in Fig. 12.

Linde Engineering

28 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Ethylene Production Cost Comparison

0

200

400

600

800

1000

1200

Ethan E/P 50/50 Butan E/B 50/50 Naphta EtOH MTO

USD / ton Ethylene

Fig. 12: Production Costs for Ethylene for different routes Fig. 12 shows that the alternative routes to Ethylene cannot compete with steamcracking today, but e.g. Ethanol dehydration can be attractive if low cost Ethanol is made available. Today's Ethanol production based on sugar cane is most efficient. However, once new methods of biomass fermentation are developed, this route can be very attractive for Ethylene production. Of course, Ethanol is also used as a gasoline component and this application will be competing with the use as olefin feedstock. MTO economics is suffering from the high investment costs for this process and does not look competitive today.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 81

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

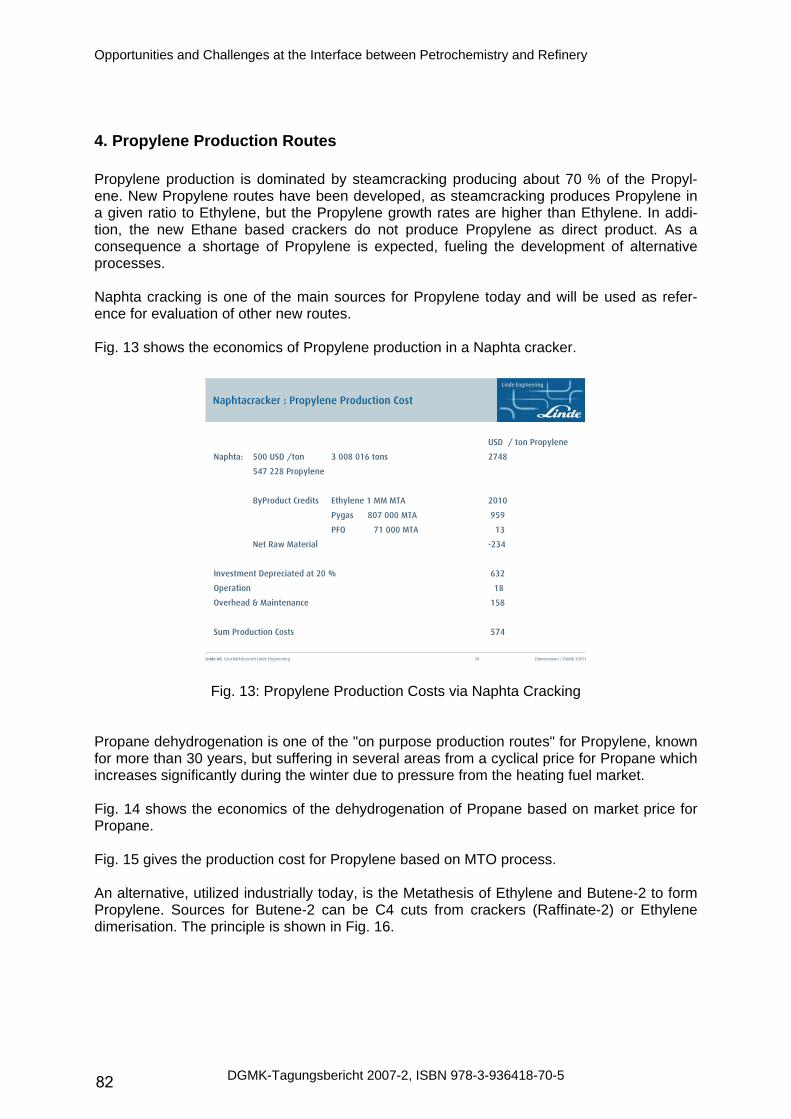

4. Propylene Production Routes Propylene production is dominated by steamcracking producing about 70 % of the Propyl-ene. New Propylene routes have been developed, as steamcracking produces Propylene in a given ratio to Ethylene, but the Propylene growth rates are higher than Ethylene. In addi-tion, the new Ethane based crackers do not produce Propylene as direct product. As a consequence a shortage of Propylene is expected, fueling the development of alternative processes. Naphta cracking is one of the main sources for Propylene today and will be used as refer-ence for evaluation of other new routes. Fig. 13 shows the economics of Propylene production in a Naphta cracker.

Linde Engineering

30 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Naphtacracker : Propylene Production Cost

USD / ton Propylene

Naphta: 500 USD /ton 3 008 016 tons 2748

547 228 Propylene

ByProduct Credits Ethylene 1 MM MTA 2010

Pygas 807 000 MTA 959

PFO 71 000 MTA 13

Net Raw Material -234

Investment Depreciated at 20 % 632

Operation 18

Overhead & Maintenance 158

Sum Production Costs 574

Fig. 13: Propylene Production Costs via Naphta Cracking

Propane dehydrogenation is one of the "on purpose production routes" for Propylene, known for more than 30 years, but suffering in several areas from a cyclical price for Propane which increases significantly during the winter due to pressure from the heating fuel market. Fig. 14 shows the economics of the dehydrogenation of Propane based on market price for Propane. Fig. 15 gives the production cost for Propylene based on MTO process. An alternative, utilized industrially today, is the Metathesis of Ethylene and Butene-2 to form Propylene. Sources for Butene-2 can be C4 cuts from crackers (Raffinate-2) or Ethylene dimerisation. The principle is shown in Fig. 16.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 82

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

29 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Propane Dehydrogenation

Cost of Production: USD Per ton of Propylene

Propane : 500 USD per ton 581

Selectivity 0,86

Investment 400 MM USD for 450 000 KTA 177

(20 % Depreciated)

Operation 10

Overhead 5 % of Invest 44

Total 817

Fig. 14: Economics of Propane Dehydrogenation

Linde Engineering

31 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

MTO Economics for Propylene

750 000 MTA Ethylene

750 000 MTA Propylene Per ton Propylene

Raw Material 3 428 571 MeOH @ 200 USD (250) 1306 (1632)

Byproduct Credit - 1100

Net Raw Material 206 ( 532)

Investment 2 500 MM USD @20 % 666

Operation 13

Maintenance & Overhead @ 5 % of Invest 166

Production Cost 1052 (1379)

Fig. 15: Economics for MTO based Propylene Production

The economics of a Metathesis with Butene-2 from Raffinate are shown in Fig. 17 and with Dimerisation in Fig. 18.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 83

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

32 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Metathesis to Propylene

Ethylene

H2C == CH2

CH3- HC == CH- CH3

2 CH3 - CH ==CH2

Butene 2

Propylene

Cat / 300 C

Fig. 16: Metathesis to Propylene

Linde Engineering

34 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Metathesis for 800 000 MTA Propylene / Europewith Raffinate 2 Import

Raw Materials: 33.33 % Ethylene 66,66 % Butene 2

Selectivity 0,9 Per ton C3H6

Ethylene: 296 266 MTA @ 1100 USD 407 USD

Butene 2 592 533 MTA @ 600 USD 444 USD

Investment 300 MM USD @20 % 75 USD

Operation 3 USD

Maintenance & Overhead 19 USD

Sum Production Costs 948 USD

Fig. 17: Economics of Metathesis from Raffinates

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 84

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

Linde Engineering

33 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Metathesis for 800 000 MTA Propylene / Middle Eastwith Ethylene Dimerisation

Raw Materials: 33.33 % Ethylene 66,66 % Butene 2

Selectivity 0,9 Per ton C3H6

Ethylene: 296 266 MTA @ 500 USD 185 USD

Butene 2 592 533 MTA @ 600 USD 444 USD

Investment 300 MM USD @20 % 75 USD

Operation 3 USD

Maintenance & Overhead 19 USD

Sum Production Costs 726 USD

Fig. 18: Metathesis with Ethylene dimerisation

A comparison of the economics for the different approaches to Propylene is shown in Fig. 19.

Linde Engineering

35 Zimmermann / DGMK 2007tLinde AG Geschäftsbereich Linde Engineering

Production Costs for Propylene

0

200

400

600

800

1000

1200

PDH MTO MTP Metathesis- ME MetathesisEurope

Naphta

Cracking

Fig. 19: Summary of Propylene production costs

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 85

Opportunities and Challenges at the Interface between Petrochemistry and Refinery

4. Summary Summarizing the evaluation of various petrochemical production routes to Ethylene and Propylene, one can state that Steamcracking is still an attractive route and will continue to dominate the production in the future. However, production will be shifted to areas with advantaged feedstocks. Naphta cracking in Europe will remain competitive if the feedstock prices remain within the current range, but economic pressure from low cost regions will increase. At present MTO cannot be seen as competitive on a global basis. There might be locations where economics are better, e.g. MTO based on coal in China. Bioethanol could be an alternative especially if new fermentation processes are developed. However, competition is fierce for ethanol as a gasoline additive, which creates very high ethanol market prices. For Propylene production only Propane dehydrogenation with discounted feedstock costs can compete with Steamcracker economics. Metathesis based on low cost Ethylene dimerisation is quite attractive, whereas Metathesis based on Raffinate 2 is similar to Propane dehydrogenation. Under current market conditions MTO and MTP are not competitive for Propylene produc-tion. There are several challenges to the traditional production schemes for light olefins, but Steamcracking will remain the main source for these products, with some alternatives being attractive in certain situations.

DGMK-Tagungsbericht 2007-2, ISBN 978-3-936418-70-5 86

Top Related