Languages

Pages

Legal

Leverage and Capital Structure

Ross Chapter 16

Spring 2005

10.1 Leverage

Financial Leverage

Financial leverage is the use of fixed financial costs to magnify

the effect of changes in EBIT on EPS.

Fixed financial costs can be, for instance, interest payments and

dividends on preferred shares.

2

10.1 Leverage

Financial Leverage

Let T denote the tax rate, letI denote interest expense and letNS

denote the number of shares outstanding.

Then earnings per share (EPS) are given by

EPS =(1−T)(EBIT− I)

NS.

3

10.1 Leverage

Financial Leverage

At a given EBIT level, how do percentage changes in EBITtranslate into percentage changes in EPS?

∆EPSEPS

=

(1−T)(EBIT′−I)NS −

((1−T)(EBIT−I)

NS

)(1−T)(EBIT−I)

NS

=(1−T)(EBIT′−EBIT)

(1−T)(EBIT− I)

=(1−T)EBIT× EBIT′−EBIT

EBIT

(1−T)(EBIT− I)

=EBIT

EBIT− I× ∆EBIT

EBIT

4

10.1 Leverage

Financial Leverage

That is, when EBIT increases by 1%, the percentage increase in

EPS isEBIT

EBIT− I=

EBITEBIT− I

.

This thedegree of financial leverage (DFL) at base level EBIT.

5

10.2 The Firm’s Capital Structure

Types of Capital

Assets Debt & Equity

NWC

Fixed Assets

Long-TermDebt (D)

Equity (E)

6

10.2 The Firm’s Capital Structure

Capital Structure Theory

Modigliani and Miller’s propositions:

Proposition I: The market value of a firm is constant regardless

of the amount of leverage that it uses to finance its assets.

Proposition II: The expected return on a firm’s equity is an

increasing function of the firm’s leverage.

7

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I

The value of a firm is given by the present value of all the cash

flows its assets are expected to generate in the future.

The value of a firm is equal to the value of its assets.

Unlevered Firm: VU = EU

Levered Firm: VL = D + EL.

8

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I

M&M Proposition I states that

VU = VL.

Why? Consider an all-equity firm with valueVU = EU .

Suppose there existed a way to finance this firm’s assets with

debt and equity such that

VL = D + EL > VU .

9

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I

An arbitrageur could buyα shares of the above firm, place them

in a trust and sell debt and equity claims against these shares in

proportions such that

α(D+EL) > αEU ,

making then a riskless profit.

10

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I

Similarly, someone could buy all of the firm’s shares forEU and

modify the firm’s capital stucture to have

VL = D + EL > EU

and then resell the firm for a riskless profit ofVL−VU .

11

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I

In a frictionless market, this arbitrage oppotunity would lead to

an increase in the firm’s unlevered equity to the point where

VU = EU = D + EL = VL

for any level ofD andEL.

12

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I with Taxes

Consider an unlevered firm, denotedU , that expects constant

earnings before interest and taxes, denotedEBIT, forever.

Each period, if the corporate tax rate isT, shareholders receive

(1−T)EBIT

and the government receives

T×EBIT.

13

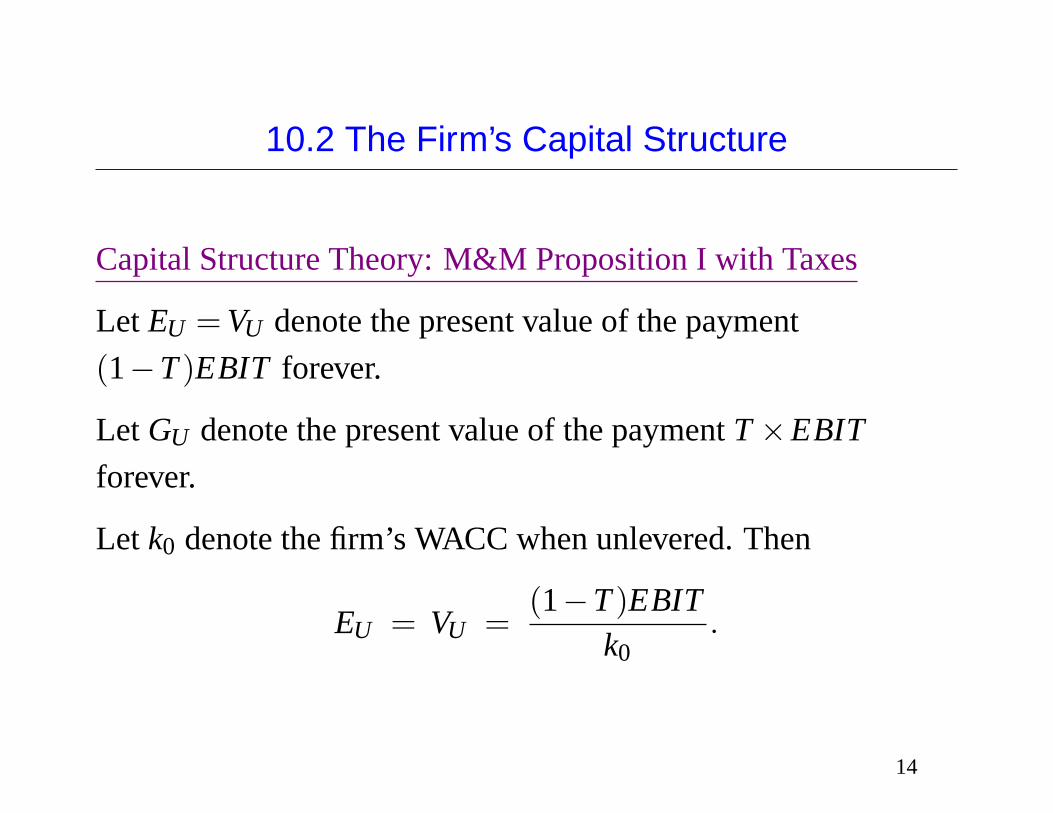

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I with Taxes

Let EU = VU denote the present value of the payment

(1−T)EBIT forever.

Let GU denote the present value of the paymentT×EBIT

forever.

Let k0 denote the firm’s WACC when unlevered. Then

EU = VU =(1−T)EBIT

k0.

14

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I with Taxes

Consider a levered firm, FirmL, with the sameEBIT asU , but

with a perpetual debt issueD with coupon ratei.

Interest payments are tax exempt.

Shareholders receive(1−T)(EBIT− iD) each period forever,

bondholders receiveiD each period forever, and

the government receivesT(EBIT− iD) each period forever.

15

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I with Taxes

Each period, the total cash flow to shareholders and bondholders

of Firm L is

(1−T)(EBIT− iD) + iD = (1−T)EBIT + TiD.

The value of the levered firm is then the sum of two perpetuities,

i.e. (1−T)EBIT forever andTiD forever.

16

10.2 The Firm’s Capital Structure

Capital Structure Theory: M&M Proposition I with Taxes

As before, the present value of(1−T)EBIT forever isVU .

Discounting the tax shield cash flowsTiD at the bonds’ coupon

ratei, their present value is

TiDi

= TD,

and thus the value of the levered firm is

VL = VU + TD.

17

10.2 The Firm’s Capital Structure

Capital Structure Theory: Financial Distress

In a world with uncertainty, however, increasingD also increases

the risk of bankruptcy. Financial distress creates some costs.

Business risk is not affected by the level of debt but has an

impact on the firm’s capability to meet in financial obligations.

Financial risk is directly affected by the firm’s level of debt.

18

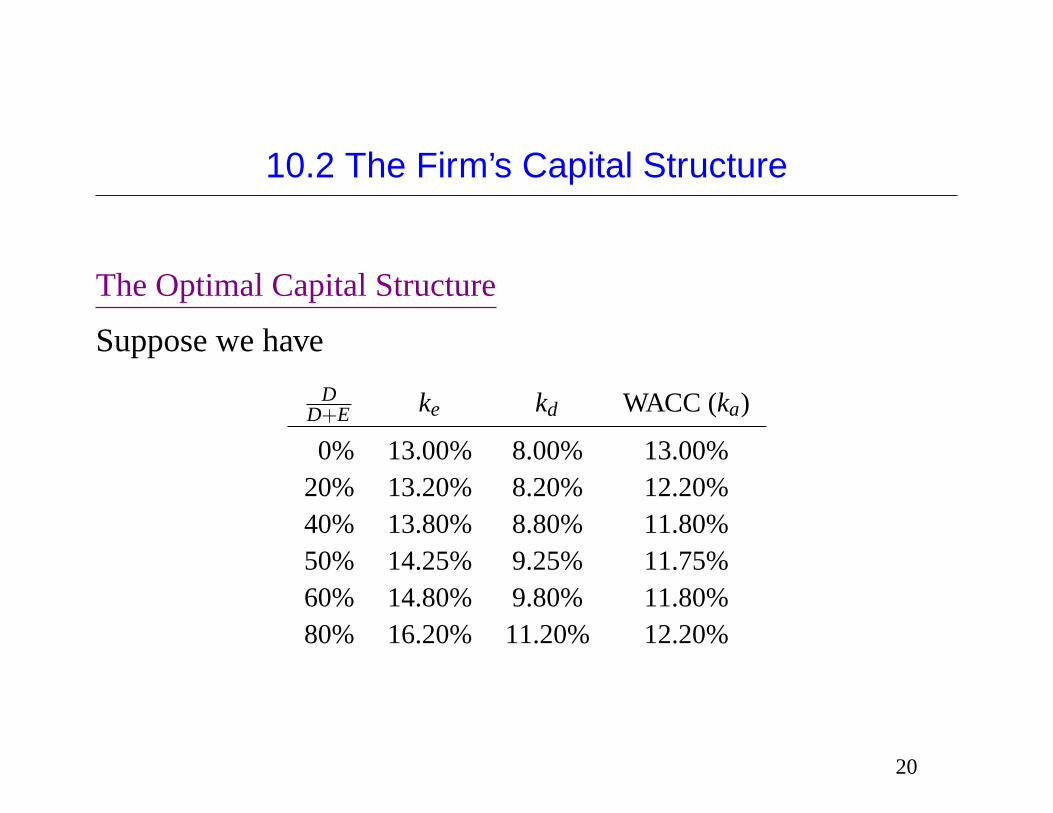

10.2 The Firm’s Capital Structure

The Optimal Capital Structure

The value of the levered firm can also be obtained using

V =(1−T)EBIT

ka,

whereka is the firm’s cost of capital.

19

10.2 The Firm’s Capital Structure

The Optimal Capital Structure

Suppose we have

DD+E ke kd WACC (ka)

0% 13.00% 8.00% 13.00%20% 13.20% 8.20% 12.20%40% 13.80% 8.80% 11.80%50% 14.25% 9.25% 11.75%60% 14.80% 9.80% 11.80%80% 16.20% 11.20% 12.20%

20

10.2 The Firm’s Capital Structure

The Optimal Capital Structure

Then the value of the firmV = (1−T)EBITka

, is maximized when

ka is minimized.

21

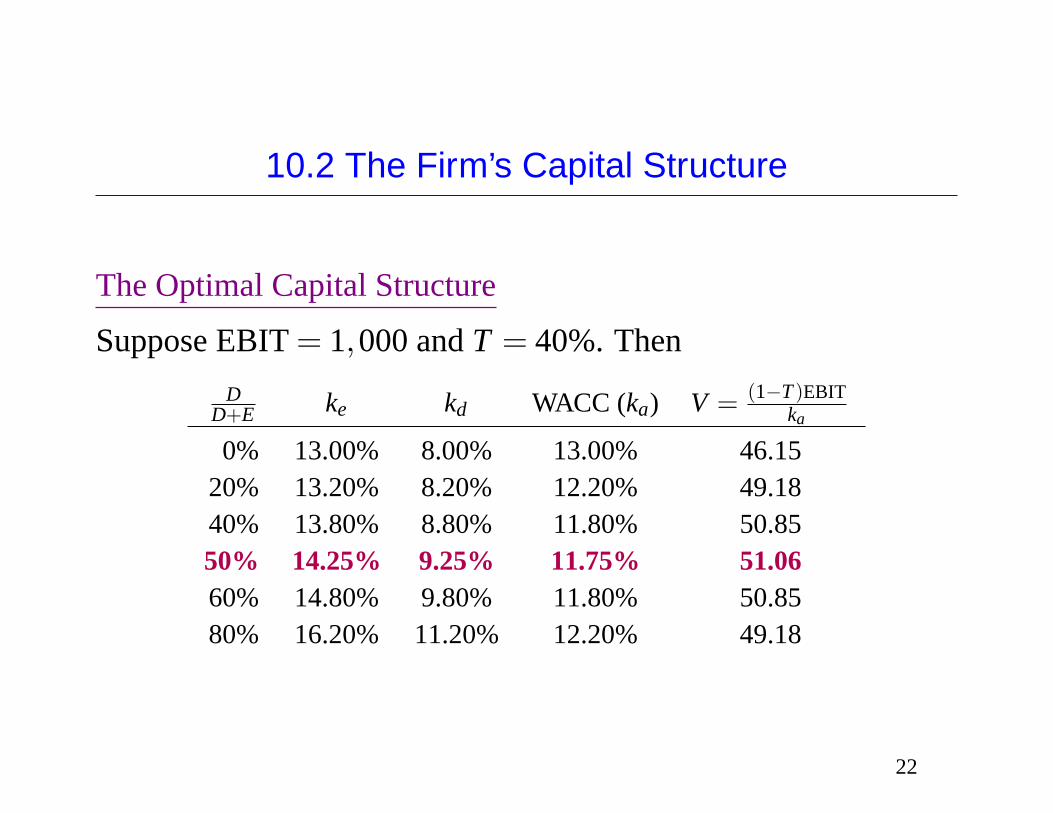

10.2 The Firm’s Capital Structure

The Optimal Capital Structure

Suppose EBIT= 1,000 andT = 40%. Then

DD+E ke kd WACC (ka) V = (1−T)EBIT

ka

0% 13.00% 8.00% 13.00% 46.1520% 13.20% 8.20% 12.20% 49.1840% 13.80% 8.80% 11.80% 50.8550% 14.25% 9.25% 11.75% 51.0660% 14.80% 9.80% 11.80% 50.8580% 16.20% 11.20% 12.20% 49.18

22

Top Related