Languages

Pages

Legal

K+S Aktiengesellschaft

Annual General Meeting

on 13 May 2009

in Kassel

Norbert Steiner, Chairman of the Board of Executive Directors

– The spoken word is binding –

2

Experience growth.

ANNUAL GENERAL MEETING

13 May 2009, Kassel

Norbert Steiner, Chairman of the Board of Executive Directors

ANNUAL GENERAL MEETING

13 May 2009, Kassel

Norbert Steiner, Chairman of the Board of Executive Directors

Dear Shareholders,

Dear Shareholder Representatives,

Dear Guests,

Ladies and Gentlemen,

On behalf of the Board of Executive Directors of K+S Aktiengesellschaft and all our

employees, I welcome you a warmly to our Annual General Meeting. We are delighted that

so many of you have once again taken up our invitation to come to Kassel.

I would like to extend an equally warm "welcome" to all those who are following my report

online on our website as well as to the representatives of the media. We are very pleased

to see that interest in the K+S Group has risen significantly.

3

13 May 2009 K+S Group 1

Report of the Board of Executive Directors

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Annual General Meeting 2009

Ladies and Gentlemen,

I shall be informing you about the development of your Company’s business in 2008 and

will describe to you – from today's perspective – our expectations and objectives for 2009

as a whole.

In addition, I will also, however, describe to you what we have achieved over the past

years, where we stand today and what we are doing to be successful in the future too. At

the end of my presentation, I will also elaborate on the key resolutions proposed by the

Board of Executive Directors and the Supervisory Board to today’s Annual General

Meeting.

4

13 May 2009 K+S Group 2

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Firstly, let’s look at what we have achieved over the past few years and at where we stand

today.

5

13 May 2009 K+S Group 3

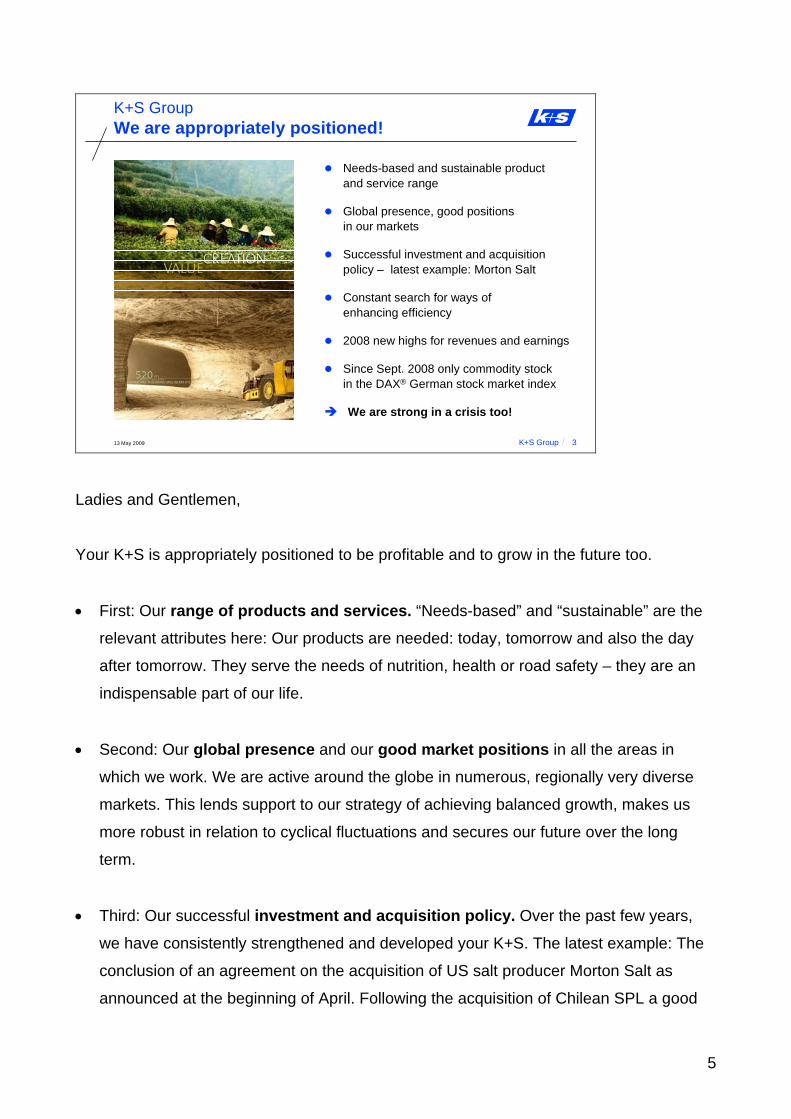

K+S GroupWe are appropriately positioned!

Needs-based and sustainable productand service range

Global presence, good positionsin our markets

Successful investment and acquisitionpolicy – latest example: Morton Salt

Constant search for ways of enhancing efficiency

2008 new highs for revenues and earnings

Since Sept. 2008 only commodity stock in the DAX® German stock market index

We are strong in a crisis too!

Ladies and Gentlemen,

Your K+S is appropriately positioned to be profitable and to grow in the future too.

• First: Our range of products and services. “Needs-based” and “sustainable” are the

relevant attributes here: Our products are needed: today, tomorrow and also the day

after tomorrow. They serve the needs of nutrition, health or road safety – they are an

indispensable part of our life.

• Second: Our global presence and our good market positions in all the areas in

which we work. We are active around the globe in numerous, regionally very diverse

markets. This lends support to our strategy of achieving balanced growth, makes us

more robust in relation to cyclical fluctuations and secures our future over the long

term.

• Third: Our successful investment and acquisition policy. Over the past few years,

we have consistently strengthened and developed your K+S. The latest example: The

conclusion of an agreement on the acquisition of US salt producer Morton Salt as

announced at the beginning of April. Following the acquisition of Chilean SPL a good

6

three years ago, which saw us successfully venture onto the American continent for the

first time, the acquisition of Morton Salt represents a further, outstanding growth

opportunity for our global salt business. I will discuss this in more detail later.

• Fourth: Our constant search for ways of enhancing efficiency. We are working

consistently on improvements along the entire value chain. We are improving

structures and processes, cutting costs, exploiting synergies and raising efficiency.

• Fifth: In financial year 2008, we achieved new highs for revenues and earnings –

and doing so in what was a more difficult market environment from the fourth quarter

onwards.

• Sixth: Since September 2008, K+S Aktiengesellschaft is the only commodity stock included in the DAX, the German stock market index comprising the 30 largest listed

companies: This promotion is, perhaps, the most conspicuous validation of our long-

term corporate policy as well as our growing importance as a fertilizer and salt

producer that operates worldwide.

Ladies and Gentlemen, all these factors taken together, make us strong, and strong too in

these times of global financial and economic crisis that we are currently experiencing.

Thus, I would like to say the following to all those who – in the light of the crisis – are

concerned about the future of the K+S Group: Your Company is well equipped to negotiate

even more difficult terrain. That is ensured by everything that makes the K+S Group what

it is today: an internationally successful company with strong regional roots – here in

Germany. More than 100 years of knowledge and experience yield dividends.

That is why we don’t want to and will not forget our roots: Today too, in the 21st century,

they are still raw materials from Germany that we process into vital fertilizers and salt

products – an activity that continues to be of great significance for the economy as a whole

and that, given appropriate conditions, has a great future too.

7

13 May 2009 K+S Group 4

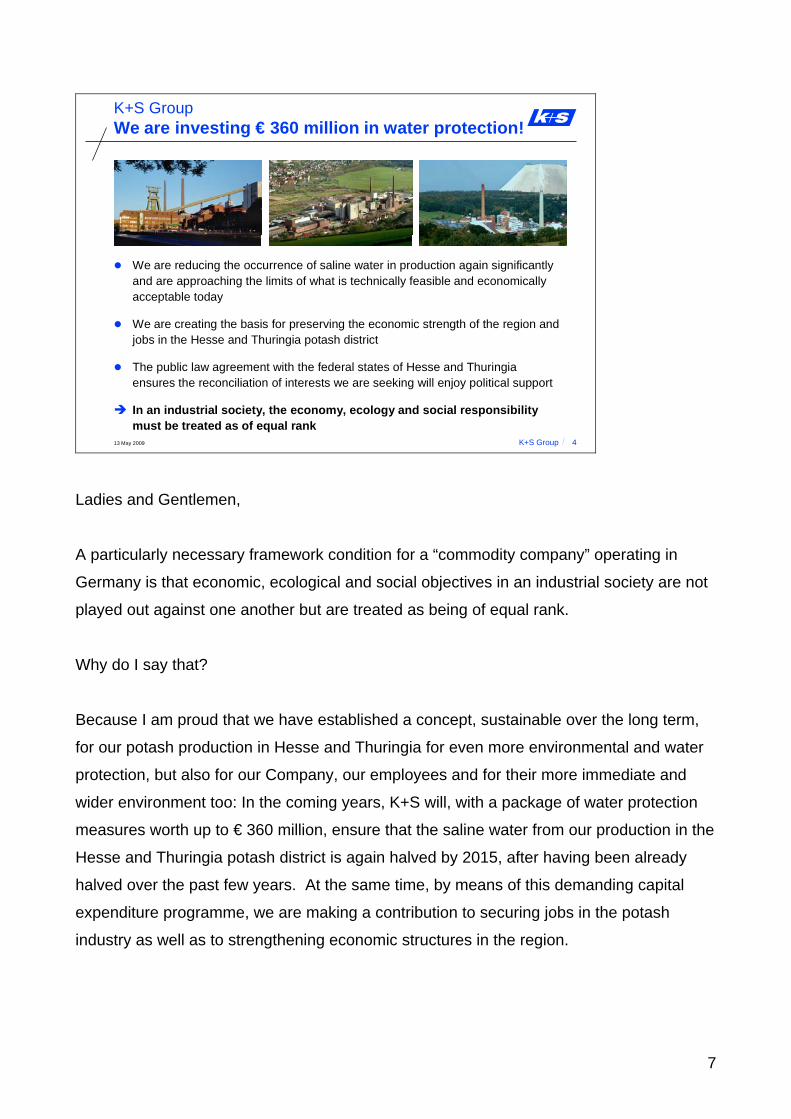

We are reducing the occurrence of saline water in production again significantlyand are approaching the limits of what is technically feasible and economically acceptable today

We are creating the basis for preserving the economic strength of the region andjobs in the Hesse and Thuringia potash district

The public law agreement with the federal states of Hesse and Thuringiaensures the reconciliation of interests we are seeking will enjoy political support

In an industrial society, the economy, ecology and social responsibilitymust be treated as of equal rank

K+S GroupWe are investing € 360 million in water protection!

Ladies and Gentlemen,

A particularly necessary framework condition for a “commodity company” operating in

Germany is that economic, ecological and social objectives in an industrial society are not

played out against one another but are treated as being of equal rank.

Why do I say that?

Because I am proud that we have established a concept, sustainable over the long term,

for our potash production in Hesse and Thuringia for even more environmental and water

protection, but also for our Company, our employees and for their more immediate and

wider environment too: In the coming years, K+S will, with a package of water protection

measures worth up to € 360 million, ensure that the saline water from our production in the

Hesse and Thuringia potash district is again halved by 2015, after having been already

halved over the past few years. At the same time, by means of this demanding capital

expenditure programme, we are making a contribution to securing jobs in the potash

industry as well as to strengthening economic structures in the region.

8

The public law agreement with the federal states of Hesse and Thuringia, signed at the

beginning of February, recognizes this proactive stance of K+S and ensures that the

reconciliation of interests we are seeking will essentially enjoy political support over the

next 30 years. This is sustainability in its best form, from both an entrepreneurial and a

political angle, and I would like to expressly thank the state governments of Hesse and of

Thuringia for this common-sense solution.

Ladies and Gentlemen,

By the end of this month, we will present an overall strategy that will end the underground

injection of liquid residues in Hesse and further reduce saline water discharges into the

Werra. We will coordinate this strategy with the relevant ministries in Hesse and Thuringia

by the end of July. Then, by the end of October, we will develop a concept providing for

measures that will build on this.

We have to devote considerable energy to developing and implementing such concepts;

the K+S package of measures alone that was presented in the autumn constituted an

unprecedented challenge for our technicians and engineers, because it all has to be taken

care of alongside the "normal business". Despite the workload, we want to continue to

participate intensively in the “Water Protection Werra/Weser and Potash Production”

Round Table. This body has already achieved great things; it has made a considerable

contribution to ensuring objective debate and, with great expertise, formulated numerous

alternative solutions meriting discussion.

We are also pleased that the Round Table has welcomed the package of measures and

finds its ideas incorporated into the public law agreement – and I would like to see the

Round Table also accompany the implementation in a constructive manner. From our

perspective, we are, with our package of measures, approaching the limits of what is today

technically feasible and economically acceptable. As an industrial company, we are unable

to fulfil every wish, but, in keeping with our sense of corporate responsibility, keep sight of

the “magic triangle” which consists in a balance between economic, ecological and social

aspects. The constant appearance of new environmental requirements from outside –

requirements that are, in part, neither technically, economically nor ecologically sensible or

9

reasonable – serves no one: Those, who demand more than is realisable are more likely

to place everything at risk.

That is why, against this background, we are unable to understand the rationale behind the

counter-motion, announced by the Dachverband der Kritischen Aktionärinnen und

Aktionäre in connection with Item 3 of the agenda of our Annual General Meeting,

opposing the discharge from liability of the Board of Executive Directors.

Ladies and Gentlemen,

I would like to emphasize once again that for us at K+S, responsible economic behaviour,

the conservation of natural resources and social responsibility are inextricably linked

together. Our package of measures will yield substantial benefits for the flora and fauna of

the Werra and Weser as well as for the people of the region – that is also confirmed by

independent expert studies. I would ask you to take this into consideration when voting on

Item 3.

10

13 May 2009 K+S Group 5

K+S GroupWe are a strong team!

About 12,400 employees use their knowledge and experience to contribute

to the success of your K+S Group –day in, day out.

In the past year too, the K+S team displayed high personal commitment and

demonstrated its determination and flexibility once again.

We thank ouremployees!

Ladies and Gentlemen,

Our committed employees are a particular success factor in dealing with the tasks that lie

ahead of us. Without them, we would not be anywhere close to where we are today.

Ladies and gentlemen, I think I will also be speaking on your behalf in now warmly

thanking the approximately 12,400 people we employ in the meantime, for their high level

of personal commitment below and above ground, their determination and, above all, for

the high degree of flexibility that they have demonstrated once again. Over the past year,

this made a substantial contribution to be so successful once again.

Of course, our thanks are also extended to our trainees, on whom the future success of

our Company will be based. At the end of 2008, the K+S Group employed a total of 615

trainees, of whom 610 were based in Germany. At 6.1%, we have attained an above-

average trainee ratio once again. Ladies and gentlemen, I would like to warmly thank our

trainees once again for their determination and commitment in the past year!

11

13 May 2009 K+S Group 6

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Dear Shareholders,

I would now like to take a look at the development of business in 2008.

12

13 May 2009 K+S Group 7

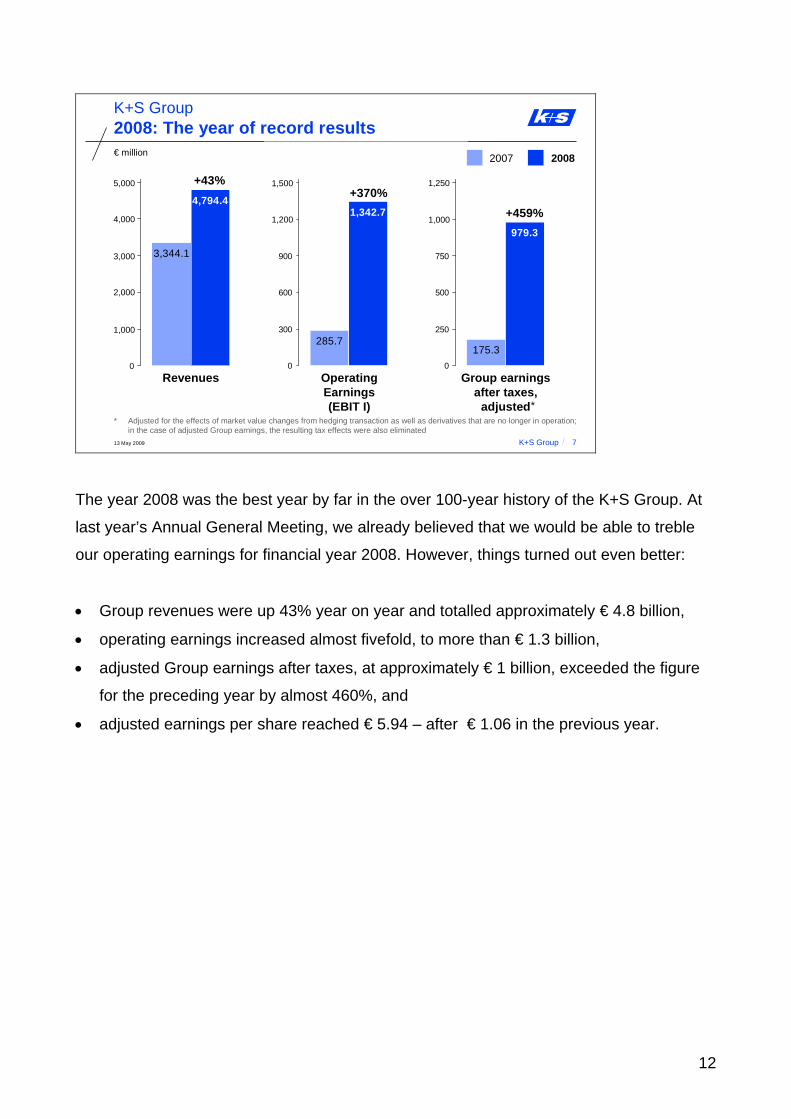

3,344.1

4,794.4

0

1.000

2.000

3.000

4.000

5.000

285.7

1,342.7

0

300

600

900

1.200

1.500

175.3

979.3

0

250

500

750

1.000

1.250

K+S Group

OperatingEarnings(EBIT I)

Revenues Group earningsafter taxes,

adjusted

+459%

€ million

+370%

2008

*

2007

+43%

2,000

3,000

4,000

5,000

1,000

1,200

1,500

1,000

1,250

2008: The year of record results

* Adjusted for the effects of market value changes from hedging transaction as well as derivatives that are no longer in operation; in the case of adjusted Group earnings, the resulting tax effects were also eliminated

The year 2008 was the best year by far in the over 100-year history of the K+S Group. At

last year’s Annual General Meeting, we already believed that we would be able to treble

our operating earnings for financial year 2008. However, things turned out even better:

• Group revenues were up 43% year on year and totalled approximately € 4.8 billion,

• operating earnings increased almost fivefold, to more than € 1.3 billion,

• adjusted Group earnings after taxes, at approximately € 1 billion, exceeded the figure

for the preceding year by almost 460%, and

• adjusted earnings per share reached € 5.94 – after € 1.06 in the previous year.

13

13 May 2009 K+S Group 8

K+S Aktiengesellschaft

(proposed)

Dividend(€ per share)

Totaldividend payment(€ million)

On the basis of the year-end closing priceof € 39.97, the dividend proposal for 2008 gives a dividend yield of 6.0%.

0.500.500.450.33

2.40

2004 2005 2006 2007 2008

55.474.3 82.5

396.0

82.5

Dividend almost quintupled

We would again like to involve you, dear shareholders, in this very positive course of

business, in keeping with the earnings-based dividend policy that we have pursued for a

long time. Thus, under Item 2 of the agenda, the Board of Executive Directors and the

Supervisory Board propose to the Annual General Meeting the payment of a dividend of € 2.40 per share. In accordance with the earnings increases achieved last year, this

represents an almost five-fold rise on the previous dividend payout. This is also an

expression not only of our financial solidity, but also of our medium- and long-term

confidence.

With currently 165 million shares titled to dividend, our proposal will result in a dividend

payout of € 396.0 million. With a dividend payout ratio of a good 40%, this lies within our

payment corridor of 40% to 50% of the adjusted Group earnings of the K+S Group that we

are seeking to achieve. Based on a closing share price of € 39.97 at the end of the year,

our dividend proposal will lead to a dividend yield of 6.0%.

Given the economic and political environment, it was not easy for the Board of Executive

Directors and the Supervisory Board to reach this decision and numerous aspects were

taken into consideration. Nevertheless, we arrived at this proposal with conviction.

14

13 May 2009 K+S Group 9

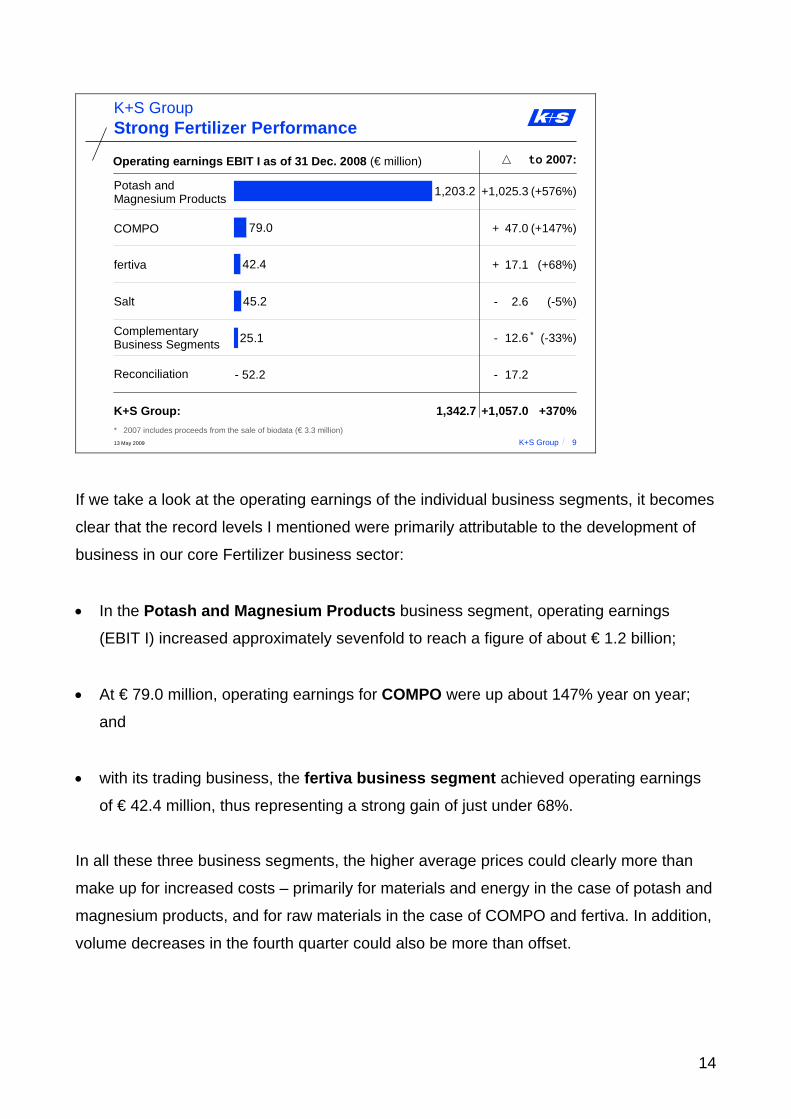

K+S Group

25.1

45.2

42.4

79.0

1,203.2Potash andMagnesium Products

COMPO

ComplementaryBusiness Segments

fertiva

Reconciliation

K+S Group: +370%1,342.7 +1,057.0

- 52.2

to 2007:

Salt

* 2007 includes proceeds from the sale of biodata (€ 3.3 million)

*

Operating earnings EBIT I as of 31 Dec. 2008 (€ million)

Strong Fertilizer Performance

(+576%)+1,025.3

(+147%)+ 47.0

(+68%)+ 17.1

(-5%)- 2.6

(-33%)- 12.6

- 17.2

If we take a look at the operating earnings of the individual business segments, it becomes

clear that the record levels I mentioned were primarily attributable to the development of

business in our core Fertilizer business sector:

• In the Potash and Magnesium Products business segment, operating earnings

(EBIT I) increased approximately sevenfold to reach a figure of about € 1.2 billion;

• At € 79.0 million, operating earnings for COMPO were up about 147% year on year;

and

• with its trading business, the fertiva business segment achieved operating earnings

of € 42.4 million, thus representing a strong gain of just under 68%.

In all these three business segments, the higher average prices could clearly more than

make up for increased costs – primarily for materials and energy in the case of potash and

magnesium products, and for raw materials in the case of COMPO and fertiva. In addition,

volume decreases in the fourth quarter could also be more than offset.

15

However, in the past year, the salt business was fair to middling: Despite a revenue

increase of just under 14% due to volume and price factors, operating earnings reached

€ 45.2 million and were down about 5% on the figure for the preceding year as a result of

higher costs, particularly for energy and freight, and of a lower foreign currency result.

Operating earnings of the Complementary Business segments too could not quite reach

the figure for the preceding year which benefited, however, from the gain of a good

€ 3 million attained on the sale of biodata ANALYTIK GmbH.

13 May 2009 K+S Group 10

K+S GroupExcellent fertilizer business in Q1 – Q3/2008

Attractive framework conditions foragriculture

Strong global demand for fertilizersresulted in scarce availability withprices rising significantly

Enormous demand could onlybe met with the greatest ofproduction efforts

Ladies and Gentlemen,

What were the reasons behind the ability of our Fertilizer business sector to achieve such

high average prices in 2008?

Above all, a key factor in this success was the heavy demand for potash fertilizers in the

first three quarters, a demand that could only be met with the greatest of production

efforts: As fertilizer producers had been already been operating at close to their technical

capacity for years, the increase in demand in the past year led to availability bottlenecks at

16

all suppliers. This tight demand-to-supply ratio as well as the sharp rise in agricultural

prices that could be observed worldwide until the middle of the year made it possible to

raise potash fertilizer prices significantly.

However, not only potash but also nitrogen fertilizer markets developed splendidly during

the first three quarters.

13 May 2009 K+S Group 11

50

100

150

200

250

300

350

400

450

500

July 2008(as of 8 May 2009)

Consumption

Production

Stocks-to-use ratio

Cereal production / consumption worldwide(million tonnes)

Price changes sincebeginning of July 2008:• Wheat: - 33%• Soybeans: - 32%• Palm oil: - 27%• Corn: - 45%

Wheat price (indexed)

K+S GroupDeclining demand for fertilizers from Q4/2008

1.500

1.600

1.700

1.800

1.900

2.000

2.100

2.200

2.300

2.400

2.500

87/88 90/91 93/94 96/97 99/00 02/03 05/06 08/09

2,300

2,200

2,100

2,000

1,900

1,800

1,700

1,600

1,500

2005

Distortions from financial andeconomic crisis

In the 2nd half of 2008, strong price corrections for agricultural products

Uncertainty among farmers over

• future earnings situation and

• possibilities for borrowing

Worldwide production cutbacksfor fertilizers, at K+S too

Then, however – and this is also part and parcel of the year 2008 – the first signs of the

financial and economic crisis also impacted the real economy, which also adversely affect

our business in the fourth quarter:

After grain prices fell sharply from the middle of the year onwards in the wake of the

financial crisis, our customers in agriculture ordered much less fertilizer on account of the

uncertainty they felt over their future earnings situation. European farmers above all feared

substantial decreases in earnings, although the fundamentals of agriculture were (and are)

intact:

17

• Prices for agricultural products remained on a comparatively high level and were still

higher than in 2007 (which is still the case today) and

• The global stocks-to-use ratio – as you can see in the bottom left-hand corner of the

slide – continued to be tight, despite last year’s record harvests, which should give a

further boost to the price level for agricultural products over the medium term.

Nevertheless, there was uncertainty among farmers.

Similarly, restrictive lending to farmers for the purpose of financing inputs as a result of the

financial crisis, especially in South America, also depressed fertilizer demand. In the last

few months of the past year, there was no stimulation of demand from the trade sector too,

because it had heavily built up stocks until the autumn in view of rising fertilizer prices and

was more interested in reducing rather than increasing stocks, which tie up capital.

The decline in demand had consequences for the production volume of international

fertilizer producers: Not only did numerous producers of nitrogenous fertilizers significantly

cut back their output worldwide, but potash producers too responded to the decrease in

demand by scaling back output substantially: Overall, last year saw global potash

production declining by about 1.9 million tonnes year on year.

We too responded to the sharp fall in demand and rising stocks with the most immediate

business measure available: In the last months of the previous year, we produced about

400,000 tonnes less of potassium chloride than in 2007.

18

13 May 2009 K+S Group 12

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Ladies and Gentlemen,

There has been no fundamental change in the fertilizer business environment in the first

quarter of 2009 too.

19

13 May 2009 K+S Group 13

Q1 Q2 Q3

Continued weak fertilizer sales,but strong winter service business in Q1/2009

K+S Group

Q4

Despite a restabilisation of prices foragricultural products, still no fundamental change of mood in agriculture

Slow fertilizer demand with stocksremaining high

Some overseas markets stronger again

Continued output adjustmentsin the fertilizer industry• K+S also affected, prompting temporary

short-time working at some sites

Strong de-icing salt demand inWestern Europe and North America due to weather factors

The first few months of the current year were marked by still very low demand for fertilizers

on almost all markets:

At first, the winter in the northern hemisphere was relatively long. But there were still no

signs of a fundamental change of mood in agriculture; demand remained muted for potash

and nitrogen fertilizers although prices for agricultural products continued to stabilise

again. In addition, stocks at the trade sector level were still largely high and the financial

crisis restricted room for manoeuvre with regard to financing for the entire distribution

chain.

In the light of falling acquisition costs and rising stocks, suppliers of nitrogen and

phosphate responded to the slowdown in demand by reducing output and cutting prices.

However, as a result of hoped-for further declines in prices, the hesitant reaction of the

agricultural sector then grew even stronger, so that the increase in demand aimed for with

the price cuts has not materialised so far.

Conditions on the potash fertilizer markets were also far from normal. Like our competitors,

we also scaled back our potash output considerably. Unfortunately, we had to and have to

introduce short-time working at several sites on a temporary basis, and I wish to assure

20

you that this is a matter that pleases no one. Nevertheless, we are pleased that we are

able to retain our employees in this way because we will need them in the future; in many

other countries, personnel is currently being made redundant on a large scale. At the

same time, short-time working offers the possibility in the first half of 2009 of producing up

to 2.0 million tonnes less of potassium and magnesium products.

On the basis of reduced output, the international potash markets are seeing the

emergence of a price level comparable to that in the third quarter of 2008 since the

beginning of March – and since the end of April in Europe. In view of their high fixed cost

burden in connection with crude salt extraction and production, potash producers require a

high price level.

We expect that the stocks of fertilizers that are still available at the trade sector level will

decline to such an extent by the middle of the year that it should be possible to assume

that fertilizer demand will slowly begin to normalise again in the second half of the year.

Demand has already picked up again in Brazil and Southeast Asia. That is because

farmers there know, with their soil in mind, that any reduction in the application of fertilizers

would inevitably be associated with lower crop yield. In addition, continue restraint with

regard to the use of fertilizers would further exacerbate the already scarce availability of

grain, corn and soy beans worldwide. Balanced, sustainable fertilizer use will thus also

remain a key factor in the future for countering the decline in the land available for

cultivation as a result of urbanisation, erosion and flooding by means of more intensive

farming.

By contrast, the situation looks particularly bright for our Salt business segment: The de-

icing salt business in the first quarter was very good both in Western Europe as well as on

the North American east cost in view of the above-average severity and prolonged

duration of the winter. On some markets, there were even supply bottlenecks, which the

K+S Group was able to exploit for itself thanks to available capacity and its customary,

great production flexibility.

21

13 May 2009 K+S Group 14

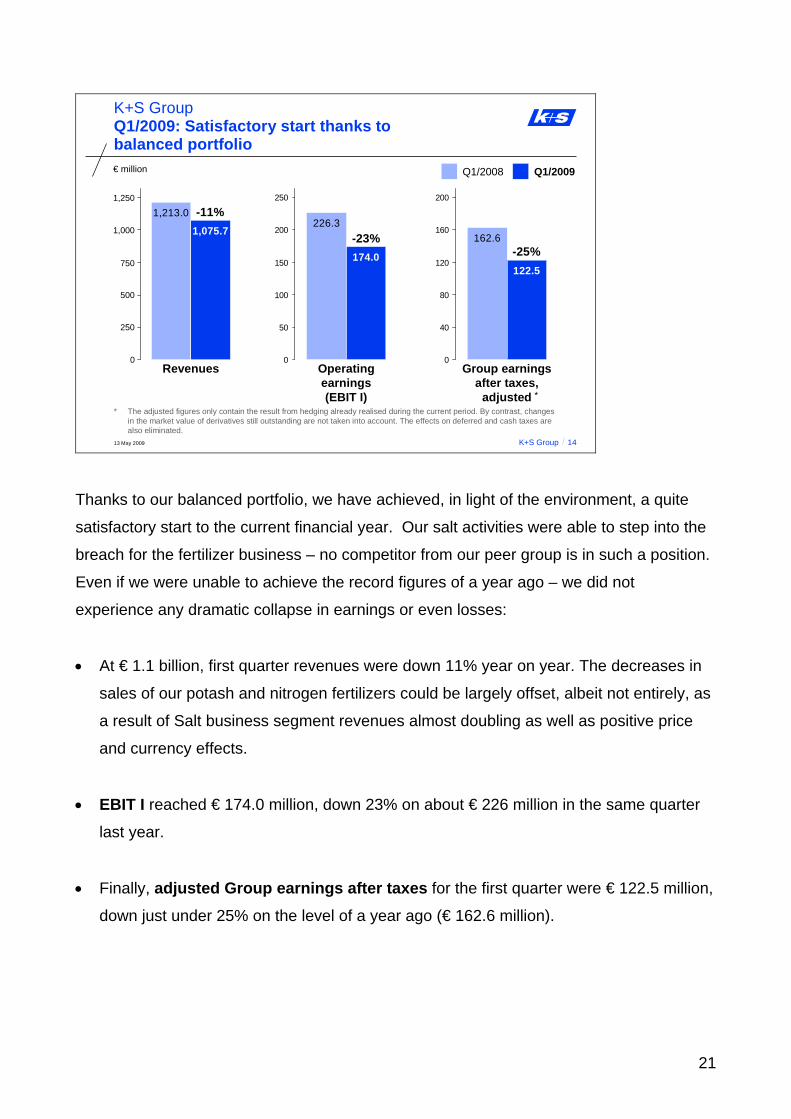

1,213.0

1,075.7

0

250

500

750

1.000

1.250

1.500

226.3

174.0

0

50

100

150

200

250

300

162.6

122.5

0

40

80

120

160

200

240

* The adjusted figures only contain the result from hedging already realised during the current period. By contrast, changesin the market value of derivatives still outstanding are not taken into account. The effects on deferred and cash taxes are also eliminated.

-11%

-23%-25%

Q1/2009 Q1/2008

K+S GroupQ1/2009: Satisfactory start thanks tobalanced portfolio€ million

Operatingearnings(EBIT I)

Revenues Group earningsafter taxes,

adjusted *

1,250

1,000

750

500

250

0

Thanks to our balanced portfolio, we have achieved, in light of the environment, a quite

satisfactory start to the current financial year. Our salt activities were able to step into the

breach for the fertilizer business – no competitor from our peer group is in such a position.

Even if we were unable to achieve the record figures of a year ago – we did not

experience any dramatic collapse in earnings or even losses:

• At € 1.1 billion, first quarter revenues were down 11% year on year. The decreases in

sales of our potash and nitrogen fertilizers could be largely offset, albeit not entirely, as

a result of Salt business segment revenues almost doubling as well as positive price

and currency effects.

• EBIT I reached € 174.0 million, down 23% on about € 226 million in the same quarter

last year.

• Finally, adjusted Group earnings after taxes for the first quarter were € 122.5 million,

down just under 25% on the level of a year ago (€ 162.6 million).

22

13 May 2009 K+S Group 15

€ million

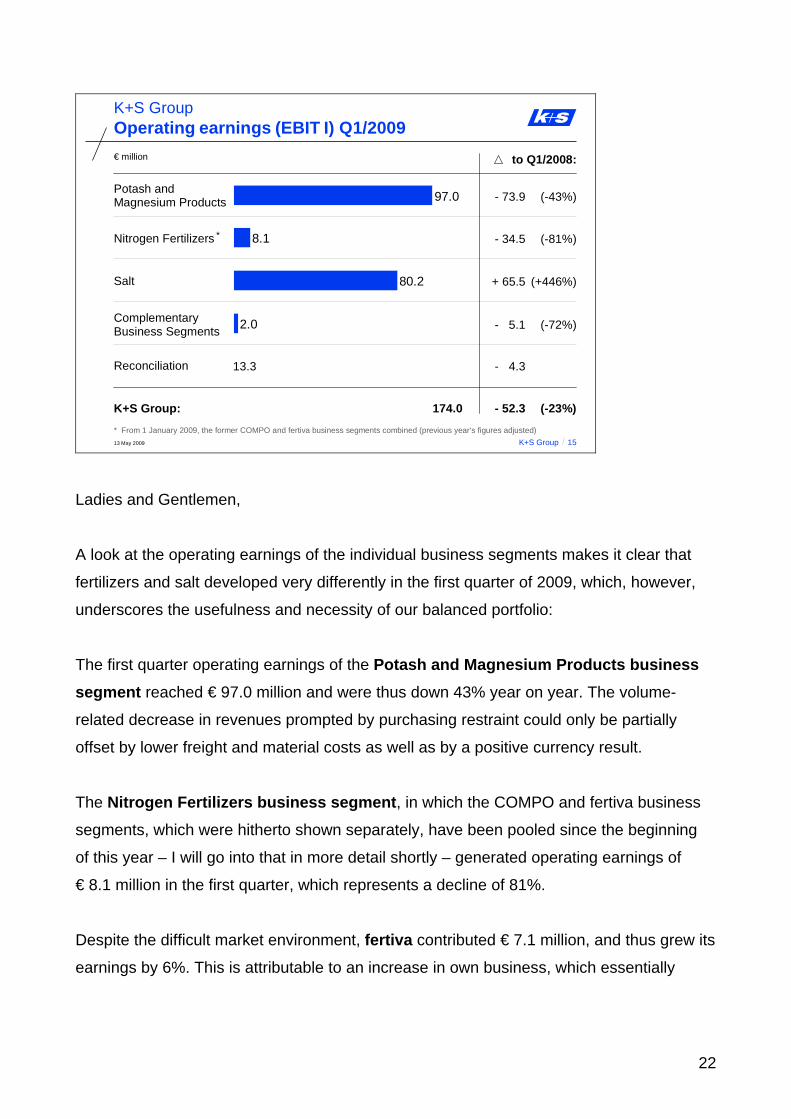

K+S GroupOperating earnings (EBIT I) Q1/2009

2.0

80.2

8.1

97.0Potash andMagnesium Products

Nitrogen Fertilizers

ComplementaryBusiness Segments

Reconciliation

(-23%)

(-43%)- 73.9

(-81%)- 34.5

(+446%)+ 65.5

(-72%)- 5.1

to Q1/2008:

Salt

- 4.3

* From 1 January 2009, the former COMPO and fertiva business segments combined (previous year‘s figures adjusted)

13.3

*

K+S Group: 174.0 - 52.3

Ladies and Gentlemen,

A look at the operating earnings of the individual business segments makes it clear that

fertilizers and salt developed very differently in the first quarter of 2009, which, however,

underscores the usefulness and necessity of our balanced portfolio:

The first quarter operating earnings of the Potash and Magnesium Products business segment reached € 97.0 million and were thus down 43% year on year. The volume-

related decrease in revenues prompted by purchasing restraint could only be partially

offset by lower freight and material costs as well as by a positive currency result.

The Nitrogen Fertilizers business segment, in which the COMPO and fertiva business

segments, which were hitherto shown separately, have been pooled since the beginning

of this year – I will go into that in more detail shortly – generated operating earnings of

€ 8.1 million in the first quarter, which represents a decline of 81%.

Despite the difficult market environment, fertiva contributed € 7.1 million, and thus grew its

earnings by 6%. This is attributable to an increase in own business, which essentially

23

involves Granammon® brand ammonium sulphate; these earnings contributions are not

shared between K+S and BASF.

However, first quarter operating earnings of COMPO amounted to € 1.0 million, down just

under € 35 million year on year. This is mainly attributable to lower demand in the

professional business and one-off expenditures connected with restructuring measures.

By contrast, the Salt business segment – prompted by the strong de-icing salt business

in Europe and North America – managed to achieve an almost five-fold increase in

earnings to more than € 80 million.

Complementary business segments’ operating earnings for the first quarter reached

€ 2.0 million, compared with € 7.1 million a year ago. This decrease is largely due to

changes in internal group billing procedures, lower average prices for Waste Management

and Recycling as well as volume decreases in logistics.

13 May 2009 K+S Group 16

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. The start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

24

Ladies and Gentlemen,

As you can see, our start to 2009 has been not quite bad, and, most importantly, the

fundamental business prospects for the coming years essentially remain positive. Also and

precisely in times such as these, the Company needs to be made fit for the future. That is

why, over the past months, we have initiated or already implemented a series of measures

with which we want to make your K+S even stronger, more competitive and, thus, more

resistant to crises.

13 May 2009 K+S Group 17

Reorganisation of the nitrogenousfertilizer business

K+S Group

Combining of nitrogen fertilizersdistributed by fertiva with ENTEC /Nitrophoska products from theCOMPO professional business in one company ("K+S nitrogen")

More efficient distribution structuresand greater concentration on majorconsumers

Stronger positioning of theK+S Group in the fertilizer sector

First of all, let us regard the reorganisation of our nitrogen fertilizer business I have already

referred to:

On the one hand, the realignment envisages that the nitrogenous fertilizers distributed by

fertiva and the ENTEC products as well as the sulphur-containing Nitrophoska products

hitherto distributed by COMPO will be grouped together in a new company, K+S Nitrogen GmbH, from 1 July 2009.

25

With efficient distribution structures, K+S Nitrogen will be able to concentrate more on

major consumers in agriculture and special crops such as fruit, vegetables and grapes.

Here we see for us considerable growth potential.

13 May 2009 K+S Group 18

Reorganisation of COMPOK+S Group

Future portfolio will concentrate on slow-release and coated fertilizers, NPK specialities, nutrient salts as well as consumer products

Headcount adjustment

In Germany, reduction of about80 full-time positions

Personnel concepts for foreigncompanies are currently beingimplemented

More effective in working the market

Significant improvement in earningscapacity envisaged

On the other hand, COMPO should also be better equipped for the future: Slow-release

fertilizers, coated fertilizers, NPK specialities as well as nutrient salts in the professional

sector along with consumer products will continue to be sold under the traditional primrose

logo. As a result of this concentration, COMPO has good prospects of being able to work

successfully in the future too.

The new COMPO will continue to offer a broad product range to customers from

commercial horticulture, public green areas and nurseries with its proven competence. The

new COMPO will continue its business in the professional and consumer segments with

much leaner structures and higher efficiency, and it should be able to work the market

more effectively. In addition, new growth areas of the market should be tapped into for

COMPO. Overall, the measures should result in a considerable improvement in earnings

power, even though the costs of restructuring and the market conditions obscure that at

the present time.

26

An adjustment of the headcount is, however, also necessary. At German sites, about

80 jobs are affected. Operations-related redundancies could in large measure be avoided

by, for example, providing further employment within the Group. Jobs will also be shed in

the foreign companies belonging to the COMPO group. The necessary measures are

being currently implemented in Belgium and France.

13 May 2009 K+S Group 19

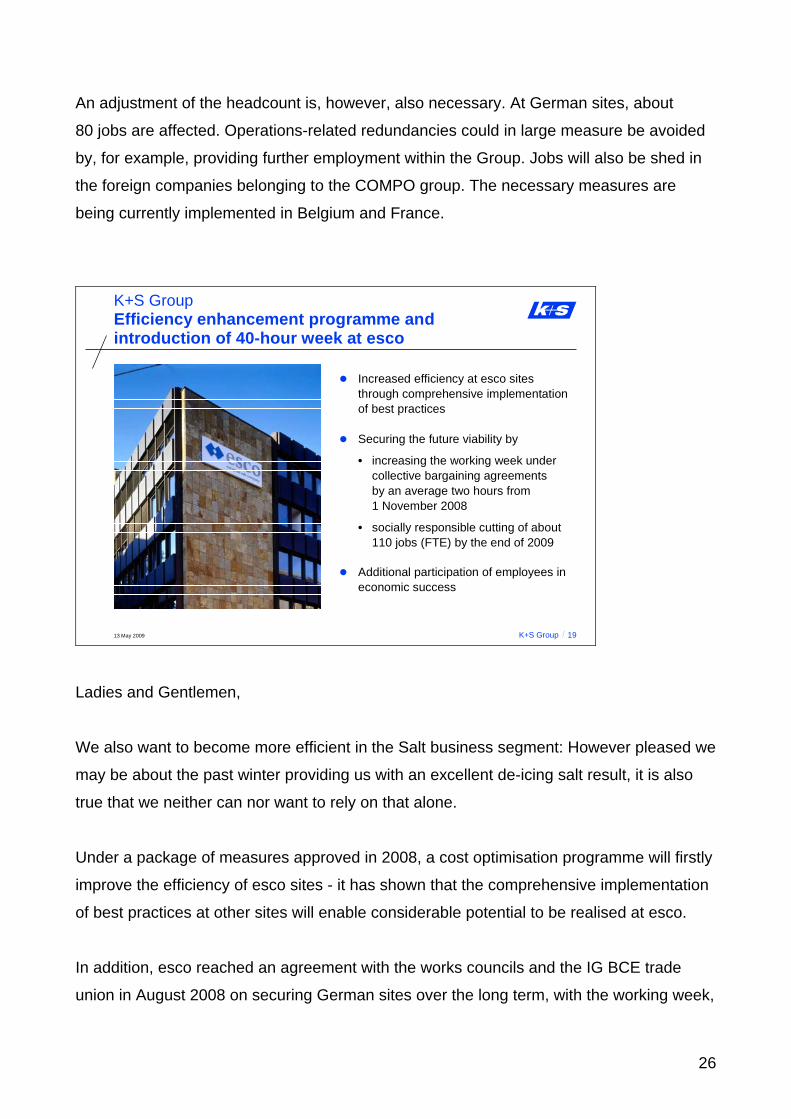

Efficiency enhancement programme andintroduction of 40-hour week at esco

K+S Group

Increased efficiency at esco sitesthrough comprehensive implementationof best practices

Securing the future viability by

• increasing the working week undercollective bargaining agreementsby an average two hours from1 November 2008

• socially responsible cutting of about110 jobs (FTE) by the end of 2009

Additional participation of employees ineconomic success

Ladies and Gentlemen,

We also want to become more efficient in the Salt business segment: However pleased we

may be about the past winter providing us with an excellent de-icing salt result, it is also

true that we neither can nor want to rely on that alone.

Under a package of measures approved in 2008, a cost optimisation programme will firstly

improve the efficiency of esco sites - it has shown that the comprehensive implementation

of best practices at other sites will enable considerable potential to be realised at esco.

In addition, esco reached an agreement with the works councils and the IG BCE trade

union in August 2008 on securing German sites over the long term, with the working week,

27

as established under collective bargaining agreements, being increased by an average of

two hours per week without direct wage-based compensation but with the opportunity of

additional profit participation.

Altogether, about 110 jobs across Europe will be affected by these measures. In this case

too, operations-related redundancies should be prevented wherever possible by also

providing further employment within the Group.

13 May 2009 K+S Group 20

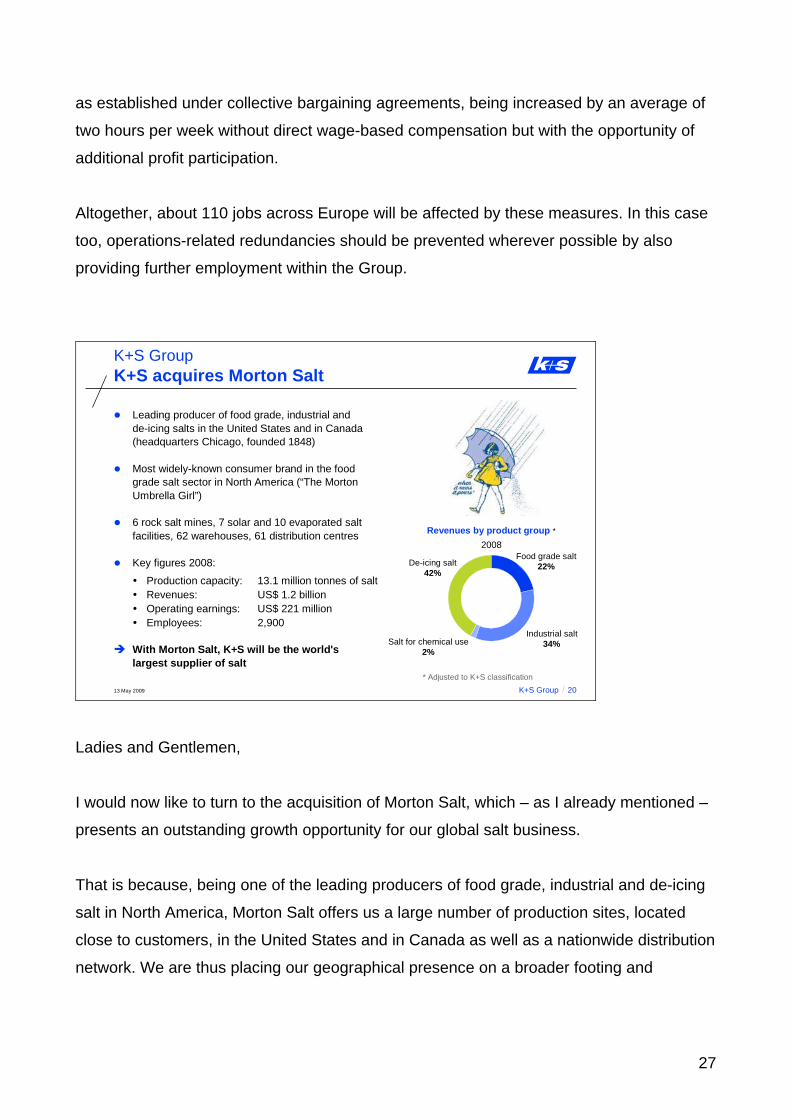

K+S acquires Morton Salt

Leading producer of food grade, industrial andde-icing salts in the United States and in Canada (headquarters Chicago, founded 1848)

Most widely-known consumer brand in the food grade salt sector in North America (“The Morton Umbrella Girl”)

6 rock salt mines, 7 solar and 10 evaporated saltfacilities, 62 warehouses, 61 distribution centres

Key figures 2008:

Production capacity: 13.1 million tonnes of saltRevenues: US$ 1.2 billionOperating earnings: US$ 221 millionEmployees: 2,900

With Morton Salt, K+S will be the world's largest supplier of salt

* Adjusted to K+S classification

Revenues by product group *2008

De-icing salt42%

Food grade salt22%

Industrial salt34%Salt for chemical use

2%

K+S Group

Ladies and Gentlemen,

I would now like to turn to the acquisition of Morton Salt, which – as I already mentioned –

presents an outstanding growth opportunity for our global salt business.

That is because, being one of the leading producers of food grade, industrial and de-icing

salt in North America, Morton Salt offers us a large number of production sites, located

close to customers, in the United States and in Canada as well as a nationwide distribution

network. We are thus placing our geographical presence on a broader footing and

28

improving our market position in both the North American industrial salt as well as

consumer business.

Morton Salt is a highly profitable company that achieves high cash flows and also makes

operating synergies available to us: in logistics and technology but also at the product

level. Thus, we will, for example, in future also be able to use the most widely known brand

on the North American food grade salt market – the Morton “Umbrella Girl” – for the

products from our hitherto salt activities.

Our operating businesses complement each other ideally, and our understanding of what

we do is the same. This will make it easier to integrate our new subsidiary smoothly and

will be of direct benefit to our employees and customers – but also to you, dear

shareholders.

That is why we are very pleased to be able to work together with a first-class team and to

jointly realise the growth opportunities that lie ahead of us. And they are – that is already

clear – enormous: Measured in terms of production capacity, which, with Morton Salt, will

rise by 13 million tonnes to just under 30 million tonnes per year, K+S will become the

largest producer of salt in the world. We are already the number one in Europe and South

America, and we will become the number one in North America and the world in the near

future.

29

13 May 2009 K+S Group 21

Strengthening of salt business: Balanced growthand higher value added

K+S and Morton Salt(Pro forma revenues 2008)

K+S Group

K+S Salt business segment(Revenues 2008)

Salt for chemical use11%

Food grade salt16%

De-icing salt35%

Industrial salt27%

Other 11%

Salt for chemical use6%

Food grade salt19%

De-icing salt39%

Industrial salt31%

Other 5%

€ 0.6billion

€ 1.4billion *

* Exchange rate 1.47 USD/EUR

Strengthening of the food grade, industrial and de-icing salt areas Creates important regional balance in de-icing salt areaIncreases the less cyclical salt business component

This comparison makes it clear that with the acquisition of Morton Salt, the K+S salt

business will grow considerably: On a pro forma basis and based on the actual figures for

2008, the acquisition means that revenues of the Salt business segment will grow by about

€ 800 million. In other words, in relation to our stand-alone business, which amounted to

about € 620 million last year, revenues would have more than doubled.

Moreover, the comparison shows that Morton Salt will first and foremost strengthen the

food grade, industrial and de-icing salt areas, that is, the component of the salt business

which is less dependent on economic conditions when compared with salt for chemical

use. This too can only benefit us in what has become a more difficult economic

environment overall.

In addition, in the case of de-icing salt, we will now gain access to new and less volatile

de-icing salt regions, that are, as far as anyone can judge, relatively “winter-stable”. This

creates a better regional balance, not only within North American but also between Europe

and the United States.

30

13 May 2009 K+S Group 22

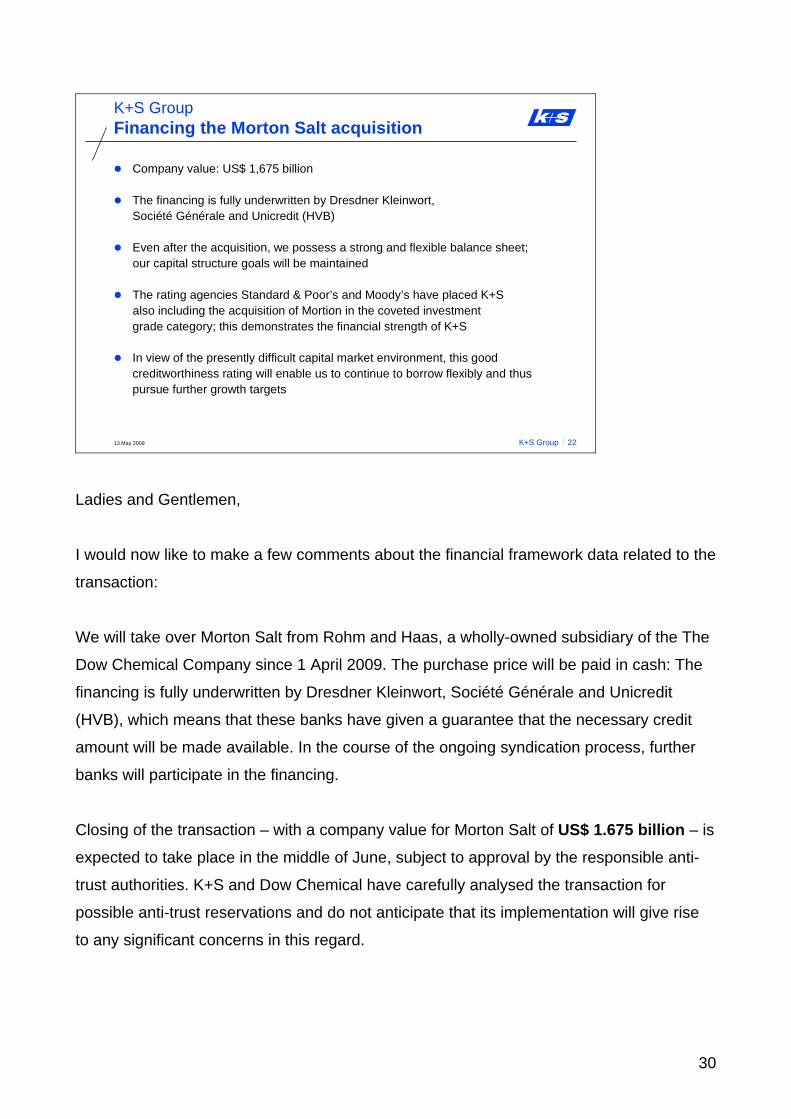

Financing the Morton Salt acquisition

Company value: US$ 1,675 billion

The financing is fully underwritten by Dresdner Kleinwort,Société Générale and Unicredit (HVB)

Even after the acquisition, we possess a strong and flexible balance sheet;our capital structure goals will be maintained

The rating agencies Standard & Poor’s and Moody’s have placed K+S also including the acquisition of Mortion in the coveted investmentgrade category; this demonstrates the financial strength of K+S

In view of the presently difficult capital market environment, this goodcreditworthiness rating will enable us to continue to borrow flexibly and thuspursue further growth targets

K+S Group

Ladies and Gentlemen,

I would now like to make a few comments about the financial framework data related to the

transaction:

We will take over Morton Salt from Rohm and Haas, a wholly-owned subsidiary of the The

Dow Chemical Company since 1 April 2009. The purchase price will be paid in cash: The

financing is fully underwritten by Dresdner Kleinwort, Société Générale and Unicredit

(HVB), which means that these banks have given a guarantee that the necessary credit

amount will be made available. In the course of the ongoing syndication process, further

banks will participate in the financing.

Closing of the transaction – with a company value for Morton Salt of US$ 1.675 billion – is

expected to take place in the middle of June, subject to approval by the responsible anti-

trust authorities. K+S and Dow Chemical have carefully analysed the transaction for

possible anti-trust reservations and do not anticipate that its implementation will give rise

to any significant concerns in this regard.

31

Following the acquisition of Morton Salt we will still possess a strong and flexible balance

sheet. Even after this important growth step, we will still maintain our goals for capital

structure, especially with regard to equity capitalisation and level of indebtedness.

In connection with the upcoming financing of our growth projects, we decided to undergo

an external rating process for the first time. The rating agencies Standard & Poor’s as well

as Moody’s have placed us – after taking into account the purchase of Morton Salt too – in

the coveted investment grade sector. Both agencies’ outlook is “stable.” This demonstrates

the financial strength of K+S and enables us, in the light of the current, difficult capital

market environment, to remain flexible on borrowing and to thus pursue further growth

targets.

13 May 2009 K+S Group 23

Originally, European salt business strongly gearedtowards de-icing and industrial salt

Complemented by salt for chemical use through acquisition of Frisia Zout (NL)

Leading European saltproducer through theacquisition of the Solvaysalt business

1

2

Acquisition of Morton Salt,one of the leading saltproducers in North America

5

K+S

Morton Salt

SPL 3

Implementation of our salt strategyK+S Group

Takeover of SPL, the largest salt producerin South America- market entry in the USA

and in Latin America - potential for expansion

into Asia

4

Ladies and gentlemen, before I go into further growth targets in more detail – let me briefly

summarize how the purchase of Morton Salt ties in with our strategy for the Salt business

segment.

Our European salt business was mainly geared towards de-icing salt and industrial salt

until the end of the 1990’s, but with the takeover of Dutch Frisia Zout in 2000, it was

32

strengthened by the inclusion of a site for salt for chemical use providing products for the

chemical industry.

Just one and a half years later, at the beginning of 2002, we further expanded our salt

activities, through the formation of the joint venture “esco – european salt company”, in

which Belgian Solvay initially participated and which was completely take over by us in

2004. esco was the leading producer in Europe from the beginning.

This was followed by the purchase of South America’s largest salt producer, Chilean

Sociedad Punta de Lobos or SPL in short, in 2006. This meant that we were active as a

producer outside Europe for the first time. It also meant the entry of our salt business into

the Latin American and US markets. Proceeding from Chilean activities, we are also

looking at Asia.

The acquisition of Morton Salt follows on from this: It represents an important step in

growing the K+S salt business in a controlled and profitable fashion – and that this is our

strategy is something that one can read again and again for years in our publications, such

as, for example, the corporate and financial reports.

13 May 2009 K+S Group 24

Bolstering of our two-pillar strategyK+S Group

For years now, our strategy has been to grow in our established business sectors – fertilizersand salt – externally too.

Acquisition of Morton Salt

Strengthens the K+S salt business

Creates greater balance between the corebusiness sectors

Yields higher operating earnings potential

Strengthening of the entire K+S Group inEurope and overseas

Strengthened K+S Group is the basis for ourgrowth strategy also as regards fertilizers

Around the globe, we are reviewing possibilitiesfor acquiring additional capacities

Core BusinessFertilizers

Core BusinessSalt

K+S Group

33

However, this is not – and this is import for me – about strengthening the salt business for

its own sake. It concerns the further development of the entire K+S Group.

Ladies and gentlemen, you know that the core of our business rests on two pillars:

fertilizers and salt. And for years now, our strategy in both core business sectors has been

to grow externally too, in order to maintain our current market positions in the future too

and – if possible – to expand them.

It is true that the acquisition of Morton Salt will strengthen the salt business initially and

that is a good thing. However, the higher value added that we will be able to realise in the

future with the acquisition will strengthen the entire Group – and that is much better. This

is because the European sites will profit from the higher value added just as much as

those overseas. At the same time, the acquisition will spread our business risk, in that the

relationship between the two core business sectors of fertilizers and salt will be more

balanced now. This too will benefit the K+S Group overall.

The increase in operating earnings potential that will come from Morton Salt will also

provide a good basis for further acquisitions and cooperation undertakings, in the fertilizer

field, for example:

Especially in our Potash and Magnesium Products business segment, which operates at

full capacity in normal years, we are continuing to review all opportunities for acquiring

additional capacity around the globe. That is because worldwide megatrends, such as the

increasing world population, changes in dietary patterns in the emerging markets and a

growing demand for biofuels will cause fertilizer demand to rise further over the medium

term – and we want to participate in this market growth.

34

13 May 2009 K+S Group 25

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Ladies and Gentlemen,

How do we assess the business development of the K+S Group for 2009 as a whole?

13 May 2009 K+S Group 26

K+S GroupRevenues and earnings expectations in 2009

Revenues expected to decline appreciably in 2009:

• Though appreciably higher average price level, nevertheless significantlylower sales of potash and magnesium products expected (effects shouldapproximately balance each other out)

• Marked decline in revenues in Nitrogen Fertilizers business segment expected mainly on account of substantial price decreases

• Good start for de-icing salt business should allow Salt business segment revenues to rise significantly

Significantly lower operating earnings expected compared to last year's record results:

• Stronger US dollar exchange rate and higher salt earnings will not be ableto make up for sales decreases in the Potash and Magnesium Products business segment

35

In view of the continuing global financial and economic crisis, we expect that the hitherto

positive performance of the K+S Group will suffer a temporary setback this year.

Initially, we assume, against the background of the price level for potash and magnesium

products evident in the first quarter, tangibly higher average prices for 2009 as a whole

compared with the previous year. However, we expect significantly lower sales, which will

roughly offset the aforementioned price effect in the case of revenues. While the revenues

of the Nitrogen Fertilizers business segment should be down significantly, mainly in view of

substantial price decreases, we expect significantly higher revenues for the Salt business

sector because of the good start for the de-icing salt business.

Overall, revenues of the K+S Group in the financial year 2009 should be down markedly

on the previous year.

For the financial year 2009, we forecast significantly lower operating earnings EBIT I in

comparison to the record figure achieved last year. This is primarily due to the already

described decreasing sales volume in the Potash and Magnesium Products business

segment. Even an estimated stronger US dollar exchange rate against last year and

higher earnings from salt cannot change anything about this forecast.

As we essentially pursue an earnings-based dividend policy, the earnings decrease

anticipated for 2009 will have a corresponding impact on future dividends.

Our outlook for 2009 is based on a series of premises, e.g.:

• the normalisation once more of demand for potash fertilizers worldwide starting from

the second half of 2009,

• average de-icing salt business in the fourth quarter in Europe and North America, as

well as

• a US dollar exchange rate of about 1.30 USD/EUR in 2009.

The effects of the intended acquisition of Morton Salt have not been taken into account in

this forecast for 2009.

36

13 May 2009 K+S Group 27

Report of the Board of Executive DirectorsAnnual General Meeting 2009

I. What we have achieved and where we stand

II. Review of financial year 2008

III. Start of financial year 2009 (Q1)

IV. What we are doing to be successful in the future too

V. Outlook for financial year 2009 as a whole

VI. Comments on proposed resolutions

Ladies and Gentlemen,

Allow me to now make a few comments about the key resolutions proposed on today’s

agenda. I have already discussed Item 2 of the agenda, our dividend proposal, and I will

limit myself here to Items 6 to 8.

37

13 May 2009 K+S Group 28

Item 6:

Issue convertible bonds and bonds withwarrants and creation of conditional capital

Deletion of the AGM resolution of 10 May 2006

Item 7:

Purchase and use of own shares

Item 8:

Revision of Article 12 of the Articles of Association (Supervisory Board remuneration)

K+S AktiengesellschaftAnnual General Meeting 2009

At the Annual General Meeting held on 10 May 2006, you, our esteemed shareholders,

approved the creation of conditional capital and authorised the Board of Executive

Directors to issue convertible bonds and bonds with warrants. However, this resolution

was successfully challenged on formal grounds.

In view of the uncertain outcome of an appeal and the lengthy period of time that would

elapse before the Federal Court of Justice could be expected to issue a decision, the

Board of Executive Directors and the Supervisory Board decided not to launch an appeal,

but decided to propose the Annual General Meeting on 14 May 2008, taking into account

the concerns raised by the plaintiffs, that it adopt a resolution granting new authorisation to

issue convertible bonds and bonds with warrants alongside the simultaneous creation of

conditional capital. The proposed resolution did not, however, receive the requisite three-

quarters majority.

Today, esteemed shareholders, under Item 6 of the agenda, we are presenting you with a

new, modified authorisation resolution once again. In the view of the Board of Executive

Directors and the Supervisory Board, the ability to issue convertible bonds or bonds with

warrants will improve the financing basis of the K+S Group.

38

Let me elaborate on this: The issuing of convertible bonds or bonds with warrants makes it

possible to raise capital on attractive terms. Depending on the form that such financing

instrument takes, it is possible to borrow capital at attractive rates of interest or to

implement a capital increase. The possibility that is envisaged of establishing conversion

obligations alongside the granting of conversion and/or warrant rights, increases the room

for manoeuvre with regard to the form that any such financing instrument should take.

The issuing of shares on the basis of conversion and warrant rights or warrant obligations

should be restricted to no more than ten percent of the share capital of the Company.

This is significantly less than in the case of the resolutions proposed previously – we have

gone for the lower limit.

Essentially, shareholders are to be granted subscription rights in respect of convertible

bonds or bonds with warrants too. However, the Board of Executive Directors, with the

approval of the Supervisory Board, shall be authorised to exclude the subscription rights of

shareholders if bonds are issued. This will enable the Company to respond to favourable

stock exchange situations rapidly and to place a bond on the market quickly and flexibly.

The interests of shareholders are safeguarded if subscription rights are excluded in that

the bonds will be issued at a price not significantly below market value. And there are

ways to prevent the dilution of existing shares to a large extent or even completely – for

instance, through the formulation of the conversion terms and conditions or through the

use of own shares that have been bought back.

To avoid misunderstandings, the Board of Executive Directors, on 21 April 2008, resolved

the following with regard to the use of the authorisation at a later date:

• The Company will not make use of the conditional capital if conversion takes place on

the basis of bonds that were previously issued against in-kind contributions.

• In addition, the Board of Executive Directors is of the opinion that Section 194,

Paragraph 1, Sentence 1 of the German Stock Corporate Act prohibits such use of

conditional capital irrespective of the resolution referred to immediately above.

39

I would now like to turn to Item 7 of the agenda – Acquisition of own shares:

Ladies and gentlemen, this item has been regularly appearing on the agenda for years – it

is a standard issue for German stock corporations. As you know, this stems from the fact

the law only permits such authorisation to be granted for a period of 18 months and is, in

our case, therefore limited until October 2009. It is thus proposed that the authorisation –

now limited until October 2010 – be renewed. This would enable the Company, beyond the

timeframe of the current authorisation, to continue to use the instrument of the acquisition

of own share to realise the associated advantages in the interest of the Company and its

shareholders. We have not made use of the existing authorisation, but you no doubt recall

that we have already employed the instrument on three occasions.

Regarding Item 8, Dr Bethke, the Chairman of the Supervisory Board, has already

mentioned everything of importance.

We would like to ask you to approve all the resolution items that have been proposed.

Experience growth.

40

Ladies and Gentlemen,

I would now like to close my presentation. I have commented on the corporate figures and

their background. I hope you will agree with me when I say that, all things considered,

they are impressive. However, what I wanted to make clear to you above all is what we are

doing to lead your K+S into a successful future.

I mean that we are appropriately positioned in order to be able to grow “strongly” in the

future too. This is true of the entire K+S Group, but is particularly true of our two Fertilizers

and Salt core business sectors, which – and shortly in the United States too – extract

natural raw materials deep underground and bring them to the surface. That is why “Deep-

rooted strength” is the motto that appears on the title page of our current financial report

and which you can see on the screen behind me. That is because we produce high-quality

fertilizers as well as high-quality industrial and salt products, and thus offer our customers

a needs-based product range that provides the cornerstones of “strong” growth in almost

all areas of daily life – and that means:

the strength to achieve greater health,

the strength to achieve more quality of life, and naturally

the strength to achieve higher crop yields.

Thank you.

Top Related