Languages

Pages

Legal

Islamic financeFarmida BiPartnerNorton Rose Fulbright LLP28 October 2013

Islamic Finance – Overview• Importance of Islamic Finance• Features of Islamic Finance• Traditional Islamic Contracts• Governing law

Importance of Islamic Finance• Demographics• Emerging economies• Political identity

3

Incorporation of Shariah law into English law• Tax changes• Regulatory changes – CIS, deposit protection scheme, status of

SSB• AFIBs• London Stock Exchange• English law and courts

4

Islamic finance in UK

Name Date Licensed Retail Products Offered

Islamic Bank of Britain PLC

August 2004 Yes

Islamic Current Account (qard);

Home Purchase Plan; Savings Accounts; and

Personal Finance

Discretionary Portfolio Service

European Islamic Investment Bank Plc

March 2006 NoTreasury and Capital

Markets

Bank of London and the Middle East

July 2007 No

Corporate Banking, Wealth Management,

Islamic Capital Markets Products

QIB (UK) PLC January 2008 NoTreasury& Corporate

Finance/ Asset/Wealth Management

Gatehouse Bank Plc April 2008 No Treasury & Corporate

Finance

Lloyds TSB - Yes Islamic Current Account

HSBC Amarah(ceased trading in September 2012)

Yes Islamic Current Account

5

Islamic Products in UK• Islamic Funds – leveraging• UK Islamic mortgages• UK Deposit Account• UK Current Account• UK Student financing• Takaful - Cobalt• SME financing

6

Examples of Islamic financing in the UK• Shard• Battersea• Chelsea Barracks• IIT• Aston Martin

7

Features of Islamic Finance

• Riba (usury or unjust enrichment)

• Gharar (uncertainty)

• Maisir (speculation)

• Assured Profit

• Unethical Investment

Features of Islamic Finance (cont)

The Nature of Money

• Money is a means of exchange only• Money is not a commodity• Money can only be exchanged for the same par value

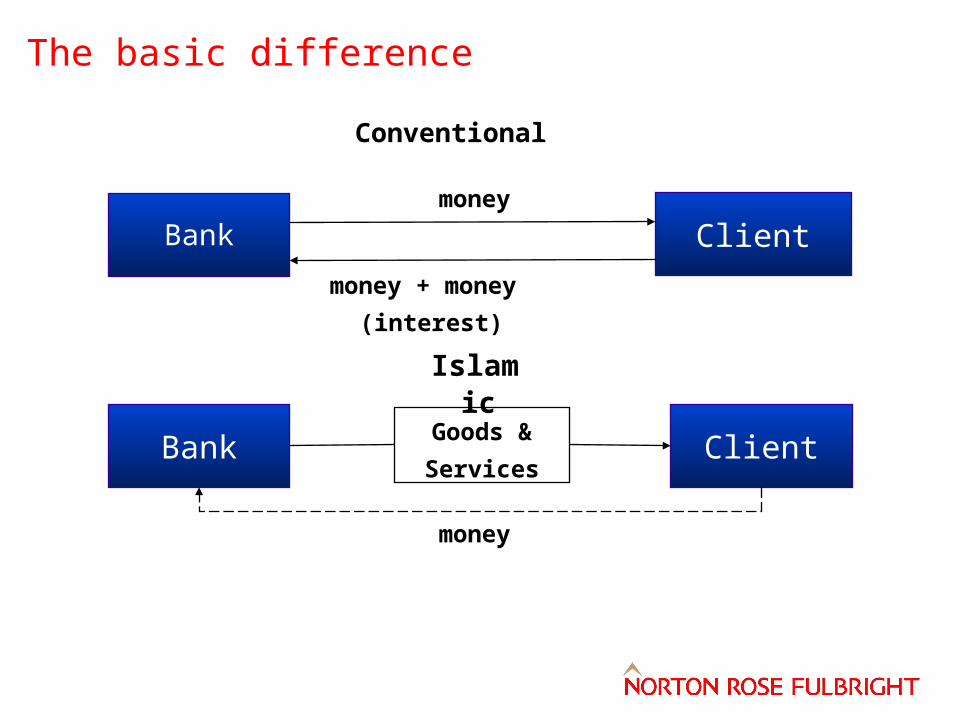

The basic difference

Bank Client

Conventional

Islamic

Bank Client

money

money

money + money (interest)

Goods &

Services

Use of funds by Islamic financial institutions

DEBT BASED EQUITY BASED

The main contracts used in Islamic

financing activities

Murabaha /

Tawarruq

Istisna’a

Mudaraba

Musharaka

Ijarah

Wa’ad

Wakala

Traditional Islamic Contracts: Murabaha

Market

Bank(Financier)

Counterparty (Borrower)

Market

1. $100 Cost Price

(spot)

2. Assets (spot)

3. Assets (spot)

4. $110 Sale Price (deferred payment)

5. Assets (spot)

6. $100 Cost Price (spot)

Traditional Islamic Contracts: Murabaha (cont)

Cost-plus financing:

• terms are fixed from the outset of the agreement (in particular quantum of payment)

• in the event of early termination, no discount applied for early settlement

• rebate on the deferred sale price permitted, but at the discretion of the financier

Traditional Islamic Contracts: Wa’ad

Market

Bank(Financier)

Counterparty (Borrower)

Market

2. $100 Cost Price

(spot)

3. Assets (spot)

4. Assets (spot)

5. Sale Price calculated pursuant to formula (deferred

payment)6. Assets

(spot)

7. $100 Cost Price (spot)

1. Undertaking to purchase Assets in the future for a Sale Price calculated pursuant

to a formula

Traditional Islamic Contracts: Wa’ad (cont)

Wa’ad (unilateral promise):

• allows for flexibility in future cashflows• due to the unilateral nature of the promise, only the

issuer of the undertaking is bound to perform• consideration from the recipient of the promise is

generally not permitted

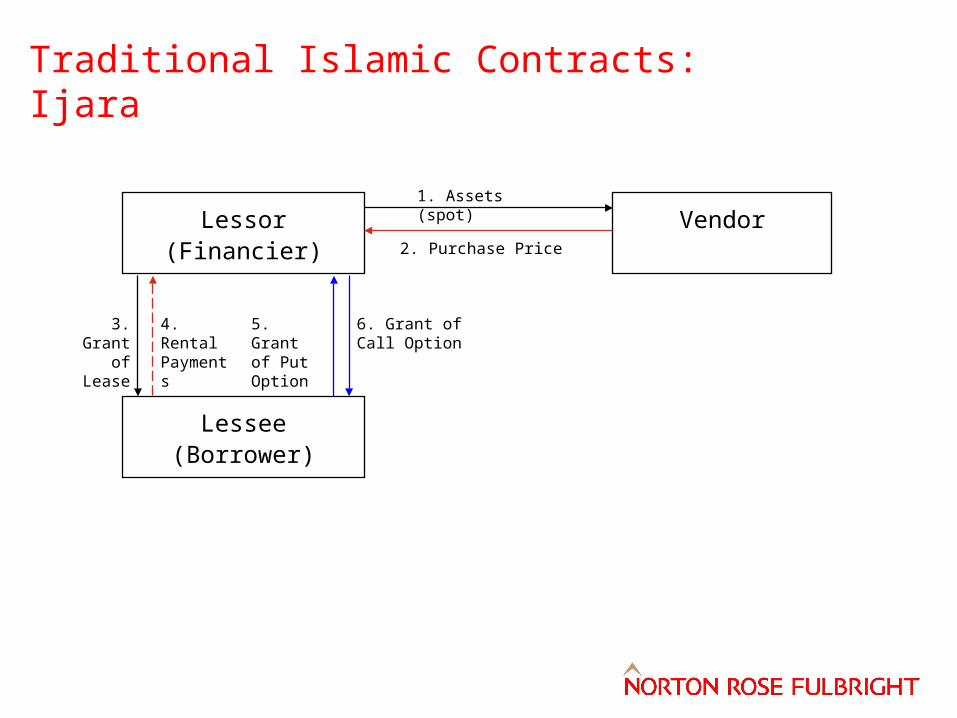

Traditional Islamic Contracts: Ijara

Lessee(Borrower)

Lessor(Financier)

Vendor

3. Grant of Lease

4. Rental Payments

1. Assets (spot)

2. Purchase Price

5. Grant of Put Option

6. Grant of Call Option

Traditional Islamic Contracts: Ijara (cont)

Ijara (leasing):

• allows for flexibility in future cashflows through the mechanism to calculate rent on a periodic basis

• Financier holds a proprietary interest in the asset during the term of the financing. Financier takes on risk that may not exist in a conventional transaction

Governing Law

• Shariah law

– non-national system of law– applies to all aspects of life and behaviour– Different schools of thought as to how principles

should be interpreted or applied

• English law

– has a well-known and developed jurisprudence – not open to doubt on basis of religious or

philosophical principles

Governing law: Shamil Bank v Beximco• Leading case in the United Kingdom

– High Court & Court of Appeal judgements

• Background

– Shamil operated in accordance with the principles of Shariah law

– Shamil’s commercial activities supervised by its Religious Supervisory Board and audited each year

Governing law: Shamil Bank v Beximco (cont)

• Court of Appeal, Lord Justice Potter’s leading judgement in January 2004 concluded:

– when interpreting governing law clauses court should lean against a construction that would defeat the commercial purpose of the agreements

– there could not be two governing laws– although possible to incorporate provisions of Shariah law

the general reference to Shariah law here did not identify any specific aspects which the parties intended to incorporate

Governing law: Best practice

• Non binding statement in recitals

• Representation from each party as to Shariah compliance

• Covenant / undertaking that it will raise no objection as to matters of Shariah compliance

• Submission to single governing law

• Fatwa from Shariah Supervisory Board

The Scholars• Limited number• Different jurisdictions• SSB• Annual audit• Fatwa

22

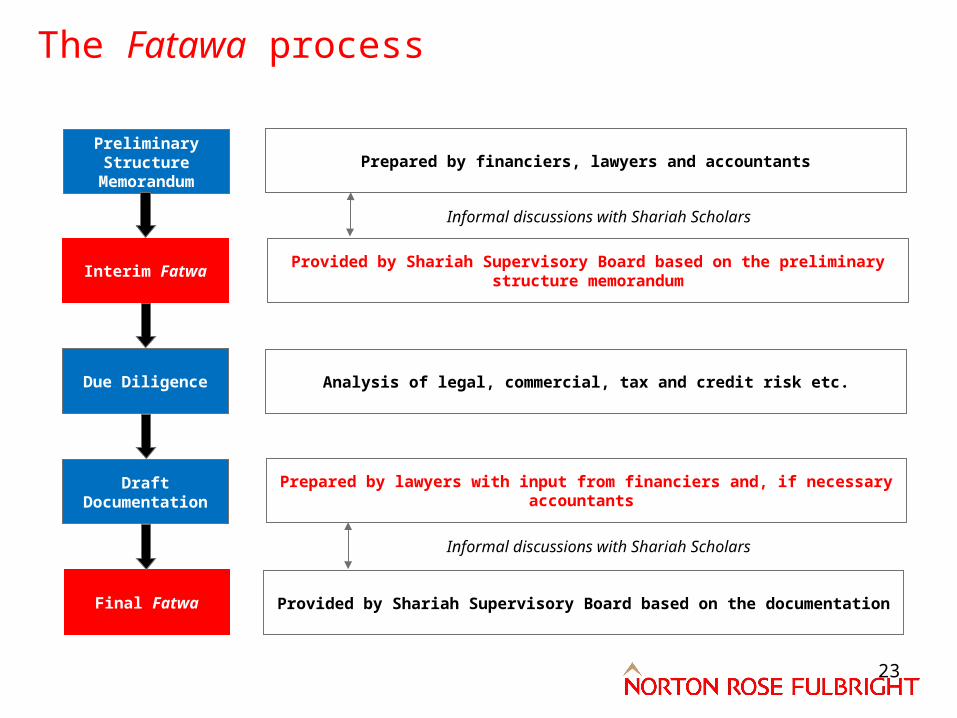

Preliminary Structure Memorandum

Interim Fatwa

Due Diligence

Draft Documentation

Final Fatwa

Prepared by financiers, lawyers and accountants

Provided by Shariah Supervisory Board based on the preliminary structure memorandum

Analysis of legal, commercial, tax and credit risk etc.

Prepared by lawyers with input from financiers and, if necessary accountants

Provided by Shariah Supervisory Board based on the documentation

Informal discussions with Shariah Scholars

Informal discussions with Shariah Scholars

The Fatawa process

23

The future of Islamic finance

24

• 9th WIEF: 29-31/10/13• UK government Sukuk• Changes in global economy – move east/developing markets• Legislation normally needed to accommodate Islamic finance• Demographic and political factors• Equity investment• Infrastructure funding

BD#19060212-3

Top Related