Languages

Pages

Legal

The global body for professional accountants 2

ISA and ISQC1 – Challenges and Tips for

SME audits.

The global body for professional accountants 3

AGENDA

• ACCA audit monitoring feedback

• Clarity ISA implementation

• Materiality (ISA 320 and ISA 450)

• Documentation in smaller audits

• ISQC1

• Questions

The global body for professional accountants 4

• 426,000 students

• 162,000 members

• 173 countries

• ACCA ‘Quality Checked’

• Quality monitoring in 15

countries

• 89 offices

The global body for professional accountants 5

2012 monitoring: global

The global body for professional accountants 6

2012 Quality Checked outcomes: UK and Ireland

The global body for professional accountants 7

2012 audit visit outcomes: UK and Ireland

“How Practice Monitoring assesses compliance with ISAs” http://www.accaglobal.com/en/member/professional-standards/monitoring/auditing/assess-compliance.html

The global body for professional accountants 8

2012 audit visit outcomes: UK and Ireland

The global body for professional accountants 9

“the overall objectives of the auditor are…to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error” ISA 200.11

The global body for professional accountants 10

Why do files ‘fail’?

substantive

evidence

audit

report ISA

compliance

going

concern

‘key’ areas

planning

performance

recording

risk identification material misstatement?

The global body for professional accountants 11 11

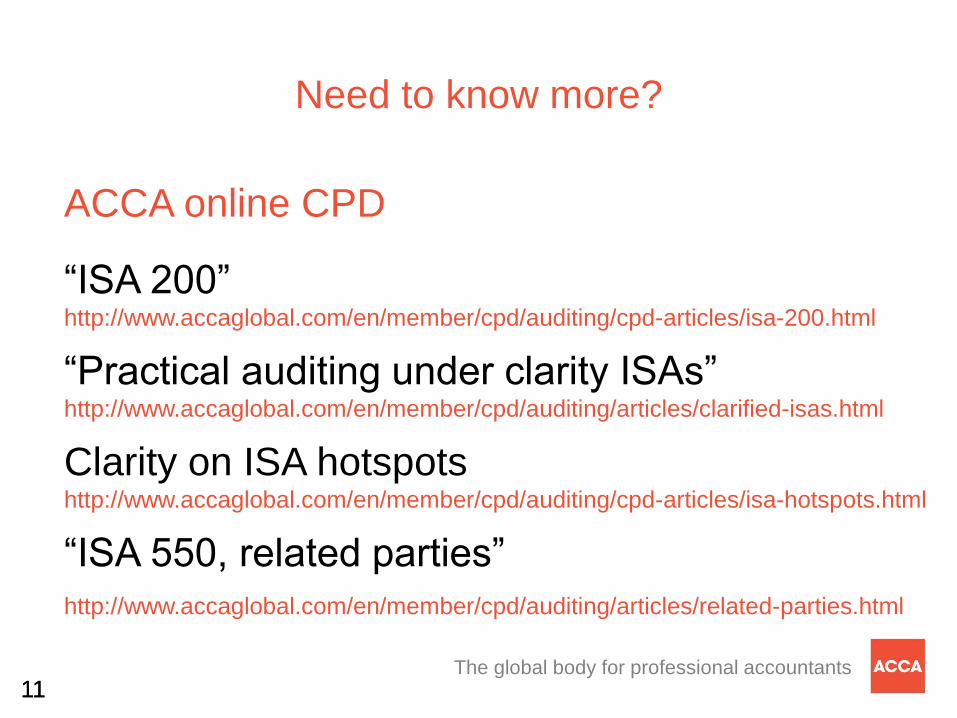

Need to know more?

ACCA online CPD

“ISA 200” http://www.accaglobal.com/en/member/cpd/auditing/cpd-articles/isa-200.html

“Practical auditing under clarity ISAs” http://www.accaglobal.com/en/member/cpd/auditing/articles/clarified-isas.html

Clarity on ISA hotspots http://www.accaglobal.com/en/member/cpd/auditing/cpd-articles/isa-hotspots.html

“ISA 550, related parties”

http://www.accaglobal.com/en/member/cpd/auditing/articles/related-parties.html

The global body for professional accountants 12

Audit materiality.

The global body for professional accountants 13 13

Original ISA 320

Revised and Clarified ISAs: materiality

ISA 320 Plan ISA 450

Evaluate

ISA 700 Report

New

Revised Revised

• placed where makes most sense

• promote greater consistency in

judgments

• Reflect the 3 different audit stages

The global body for professional accountants 14

ISA 320: determining materiality

The auditor shall determine:

• materiality for the financial statements

as a whole

• (possibly) materiality for particular

classes of transactions, account

balances or disclosures (influence on

users’ economic decisions?)

• performance materiality

The global body for professional accountants 15

ISA 320: calculating materiality

Professional judgment

Benchmark Percentage x

• elements of the financial statements

• items focused on by users

• nature of the entity/industry/economic

environment

• structure of the entity

relationship

The global body for professional accountants 16

ISA 320: What is performance materiality?

Used for:

• assessing the risks of material

misstatement

• determining the nature, timing and

extent of further audit procedures

The global body for professional accountants 17

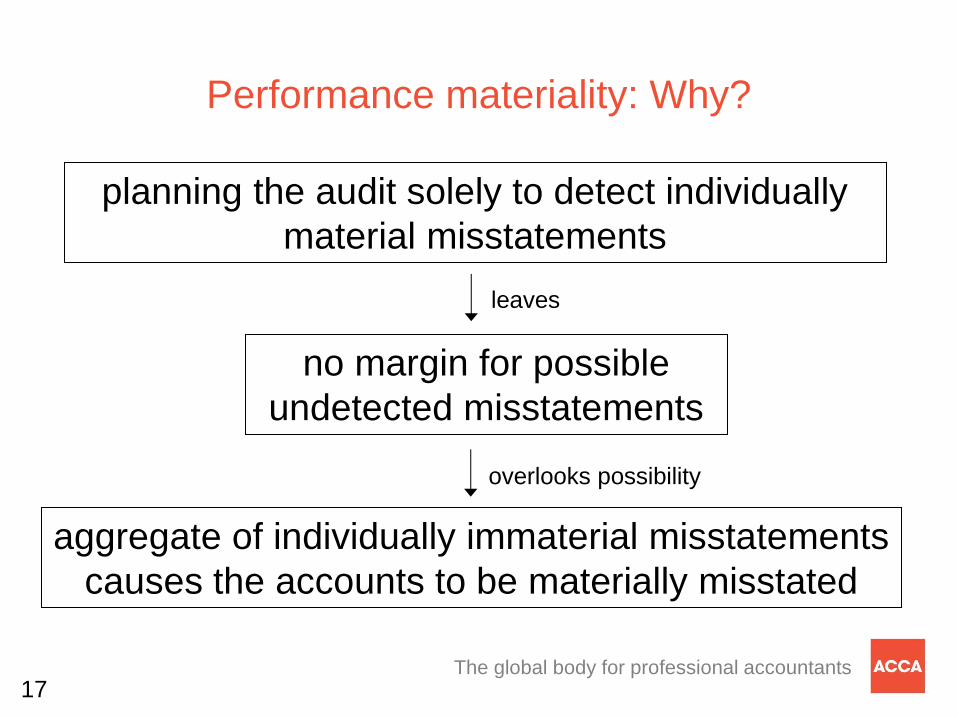

Performance materiality: Why?

planning the audit solely to detect individually

material misstatements

aggregate of individually immaterial misstatements

causes the accounts to be materially misstated

no margin for possible

undetected misstatements

leaves

overlooks possibility

The global body for professional accountants 18

The purpose of performance materiality

Designed to ensure that at the end of the

assignment:

Detected Undetected +

Aggregate

misstatements

<

Materiality for the accounts as a whole

The global body for professional accountants 19

• must be lower than materiality for the

accounts as a whole

• may use

- one PM for all items

- different PM for different items

• if different materiality determined for

each balance, class of transaction,

disclosure etc….must determine PM

for each balance, etc

Determining performance materiality (PM)

The global body for professional accountants 20

Take into account:

• nature of the entity

• misstatements identified in previous

audits

• expectation of misstatements in the

current audit

Determining performance materiality (PM)

The global body for professional accountants 21

ISA 450

The global body for professional accountants 22

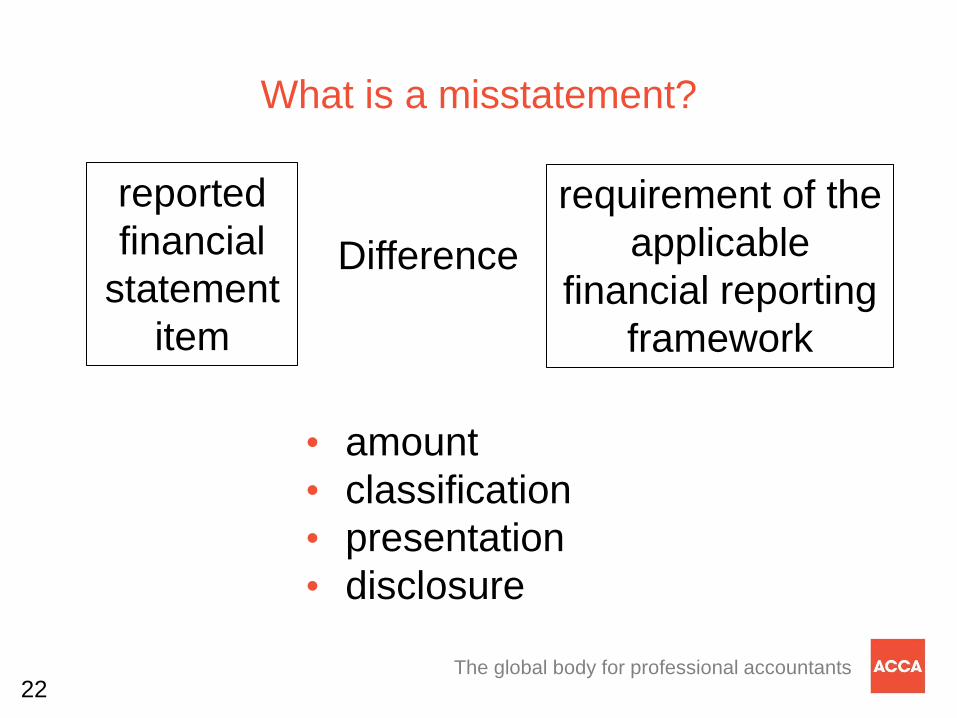

What is a misstatement?

reported

financial

statement

item

requirement of the

applicable

financial reporting

framework

Difference

• amount

• classification

• presentation

• disclosure

The global body for professional accountants 23

• accumulate identified misstatements

(other than “clearly trivial”)

• consider need to revise overall audit

strategy and plan

• communicate misstatements to

management and request correction

• evaluate effect of uncorrected

misstatements

• written representations

• documentation

ISA 450: what does this mean?

The global body for professional accountants 24

Documentation in smaller audits.

The global body for professional accountants 25

ISA 230.2: Purposes of Audit Documentation

• evidence of the auditor’s basis for a

conclusion about the achievement of

the overall objectives of the auditor

(ISA 200.11)

• (“A sufficient and appropriate record of

the basis for the auditor’s report” – ISA

230.5)

• evidence that the audit was planned

and performed in accordance with

ISAs

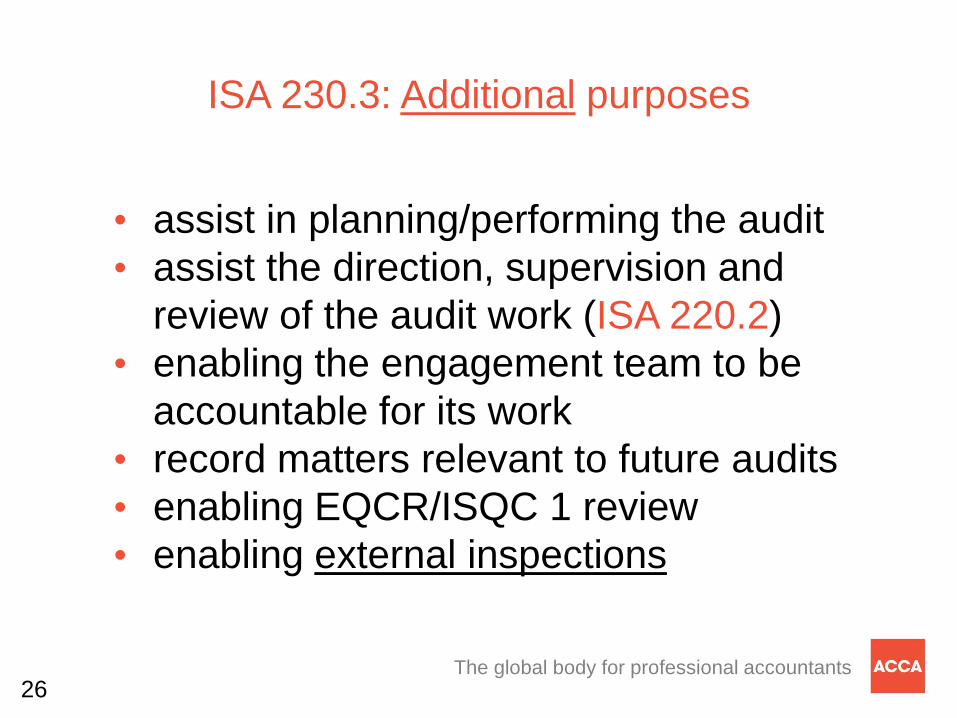

The global body for professional accountants 26

ISA 230.3: Additional purposes

• assist in planning/performing the audit

• assist the direction, supervision and

review of the audit work (ISA 220.2)

• enabling the engagement team to be

accountable for its work

• record matters relevant to future audits

• enabling EQCR/ISQC 1 review

• enabling external inspections

The global body for professional accountants 27

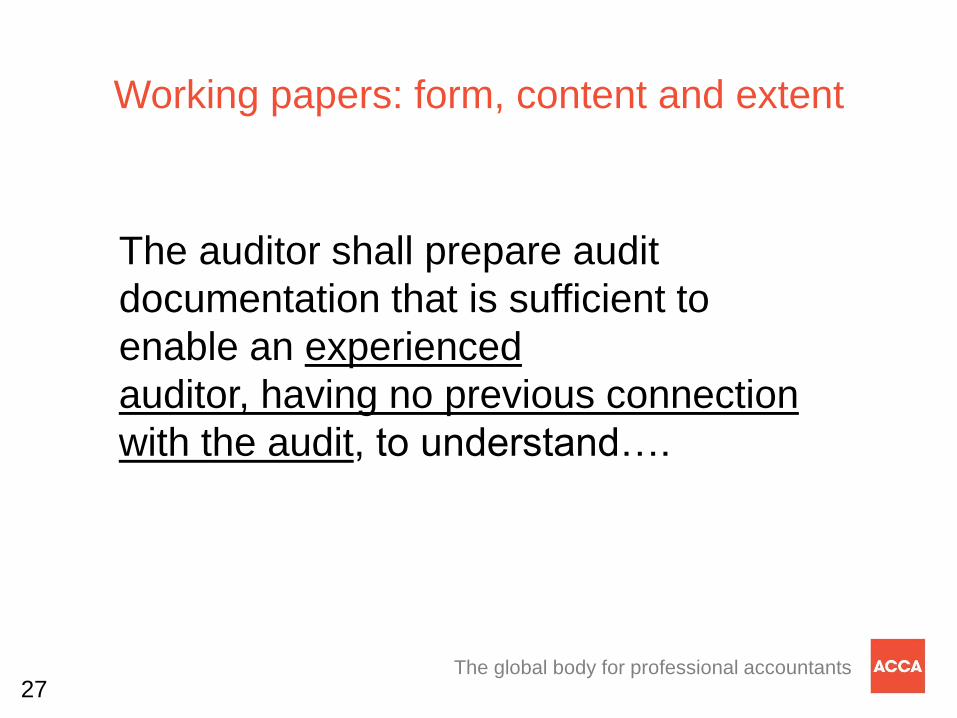

Working papers: form, content and extent

The auditor shall prepare audit

documentation that is sufficient to

enable an experienced

auditor, having no previous connection

with the audit, to understand….

The global body for professional accountants 28

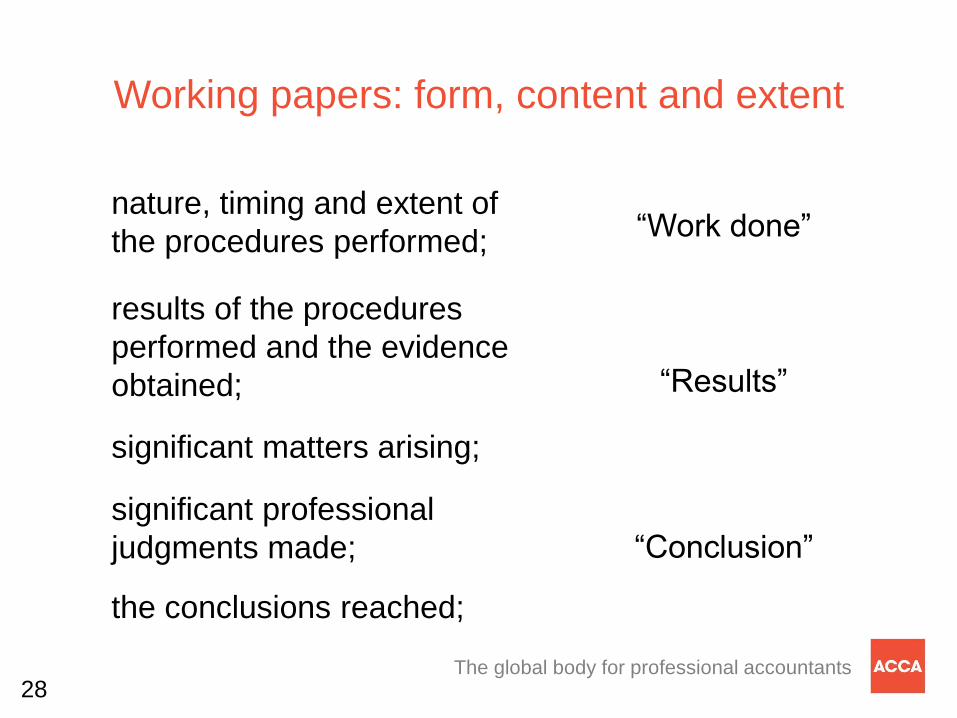

Working papers: form, content and extent

nature, timing and extent of

the procedures performed;

results of the procedures

performed and the evidence

obtained;

significant matters arising;

significant professional

judgments made;

the conclusions reached;

“Work done”

“Results”

“Conclusion”

The global body for professional accountants 29

Identifying characteristics of the specific

items tested

dates and unique PO

numbers;

scope of the procedure and

identify the population

source, starting point and

the sampling interval

Purchase orders

All items over a

specific amount

from a given

population

Systematic

sampling from a

population of

documents

The global body for professional accountants 30

‘Sufficient’ audit documentation

“Oral explanations by the auditor, on

their own, do not represent adequate

support for the work the auditor

performed or conclusions the auditor

reached, but may be used to explain

or clarify information contained in the

audit documentation” ISA 230.A5

If it’s not documented…. it wasn’t done!

The global body for professional accountants 31

D-I-Y

ISAs: what are my options?

Software provider

Professional body?

• read ISAs

• CPD/workshop?

• design from

scratch

• CPD/workshop?

• buy in

programmes

• assistance

• practical guide

• small & medium

firms

• examples

• Free?

Your programme Tailor it Follow it

The global body for professional accountants 32

UK PN26 Characteristics of the smaller entity audit

• concentration of ownership and

management

• uncomplicated operations

• simple accounting systems and few,

informal controls

• small audit team

• proprietary audit system

http://www.frc.org.uk/Our-Work/Publications/APB/PN-26-(Revised)-

Guidance-on-Smaller-Entity-Audit-D.aspx

The global body for professional accountants 33

Examples

• Appendix B of PN 26

• particularly Example 11

• other examples provide excellent

guidance

• if followed, would result in a significant

increase in the number of satisfactory

files

The global body for professional accountants 34

International Standard on Quality Control 1.

The global body for professional accountants 35

Policies and procedures

ISQC 1: the requirements

Documented

Communicate Apply

Monitor

The global body for professional accountants 36

• engagements performed in

accordance with requirements

• reports issued are appropriate to

circumstances

ISQC 1: why my firm?

Quality

controls Consistency

The global body for professional accountants 37

• Documentation of policies

• Ethics

• dependence on fees from one

source

• loan to client (overdue fees or

otherwise)

• long association

• employment/business relationship

Monitoring: the most common issues

The global body for professional accountants 38

D-I-Y

ISQC 1: what are my options?

Training Co Professional Body?

• read ISQC 1

• CPD/workshop?

• design from

scratch

• CPD/workshop?

• buy in manual

• assistance

• practical guide

• small & medium

firms

• examples

• Free?

• Self-diagnostic

checklist

Your policies

and procedures Tailor it Follow it

The global body for professional accountants 39

Questions?

Top Related