Languages

Pages

Legal

LEVEL 3 COMMUNICATIONSJULY 2016

Level 3 CommunicationsMarch 2017

2

Modified Adjustment and Cautionary Statement

In this presentation, Modified prior period results exclude the company’s Venezuelan subsidiary’s operations, which were deconsolidated as of September 30, 2015, and reflect changes made to customer assignments between the wholesale and enterprise channels at the beginning of 2016. Consistent with the SEC’s Compliance and Disclosure Interpretations relating to non-GAAP metrics, we have made changes to some of our earnings materials. See slide 17 for Non-GAAP Reconciliations.

Some statements made in this presentation are forward-looking in nature and are based on management's current expectations or beliefs. These forward-looking statements are not a guarantee of performance and are subject to a number of uncertainties and other factors, many of which are outside Level 3's control, which could cause actual events to differ materially from those expressed or implied by the statements. Important factors that could prevent Level 3 from achieving its stated goals include, but are not limited to, the company's ability to: increase revenue from its services to realize its targets for financial and operating performance; develop and maintain effective business support systems; manage system and network failures or disruptions; avert the breach of its network and computer system security measures; develop new services that meet customer demands and generate acceptable margins; manage the future expansion or adaptation of its network to remain competitive; defend intellectual property and proprietary rights; manage risks associated with continued uncertainty in the global economy; manage continued or accelerated decreases in market pricing for communications services; obtain capacity for its network from other providers and interconnect its network with other networks on favorable terms; successfully integrate future acquisitions; effectively manage political, legal, regulatory, foreign currency and other risks it is exposed to due to its substantial international operations; mitigate its exposure to contingent liabilities; and meet all of the terms and conditions of its debt obligations. Additional information concerning these and other important factors can be found within Level 3's filings with the Securities and Exchange Commission. Statements in this presentation should be evaluated in light of these important factors. Level 3 is under no obligation to, and expressly disclaims any such obligation to, update or alter its forward-looking statements, whether as a result of new information, future events, or otherwise.

3

Modified Adjustment and Cautionary StatementForward-Looking Statements

Except for the historical and factual information contained herein, the matters set forth in this communication, including statements regarding the expected timing and benefits of the proposed transaction, such as efficiencies, cost savings, enhanced revenues, growth potential, market profile and financial strength, and the competitive ability and position of the combined company, and other statements identified by words such as “will,” “estimates,” “anticipates,” “believes,” “expects,” “projects,” “plans,” “intends,” “may,” “should,” “could,” “seeks” and similar expressions, are forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, many of which are beyond our control. These forward-looking statements, and the assumptions upon which they are based, (i) are not guarantees of future results, (ii) are inherently speculative and (iii) are subject to a number of risks and uncertainties. Actual events and results may differ materially from those anticipated, estimated, projected or implied in those statements if one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect. Factors that could affect actual results include but are not limited to: the ability of the parties to timely and successfully receive the required approvals for the combination from regulatory agencies free of conditions materially adverse to the parties and from their respective shareholders; the possibility that the anticipated benefits from the proposed transaction cannot be fully realized or may take longer to realize than expected; the possibility that costs, difficulties or disruptions related to the integration of Level 3’s operations with those of CenturyLink will be greater than expected; the ability of the combined company to retain and hire key personnel; the effects of competition from a wide variety of competitive providers, including lower demand for CenturyLink’s legacy offerings; the effects of new, emerging or competing technologies, including those that could make the combined company’s products less desirable or obsolete; the effects of ongoing changes in the regulation of the communications industry, including the outcome of regulatory or judicial proceedings relating to intercarrier compensation, interconnection obligations, access charges, universal service, broadband deployment, data protection and net neutrality; adverse changes in CenturyLink’s or the combined company’s access to credit markets on favorable terms, whether caused by changes in its financial position, lower debt credit ratings, unstable markets or otherwise; the combined company’s ability to effectively adjust to changes in the communications industry, and changes in the composition of its markets and product mix; possible changes in the demand for, or pricing of, the combined company’s products and services, including the combined company’s ability to effectively respond to increased demand for high-speed broadband service; changes in the operating plans, capital allocation plans or corporate strategies of the combined company, whether based on changes in market conditions, changes in the cash flows or financial position of the combined company, or otherwise; the combined company’s ability to successfully maintain the quality and profitability of its existing product and service offerings and to introduce new offerings on a timely and cost-effective basis; the adverse impact on the combined company’s business and network from possible equipment failures, service outages, security breaches or similar events impacting its network; the combined company’s ability to maintain favorable relations with key business partners, suppliers, vendors, landlords and financial institutions; the ability of the combined company to utilize net operating losses in amounts projected; changes in the future cash requirements of the combined company; and other risk factors and cautionary statements as detailed from time to time in each of CenturyLink’s and Level 3’s reports filed with the U.S. Securities and Exchange Commission (the “SEC”). Due to these risks and uncertainties, there can be no assurance that the proposed combination or any other transaction described above will in fact be completed in the manner described or at all. You should be aware that new factors may emerge from time to time and it is not possible for us to identify all such factors nor can we predict the impact of each such factor on the proposed combination or the combined company. You should not place undue reliance on these forward-looking statements, which speak only as of the date of this communication. Unless legally required, CenturyLink and Level 3 undertake no obligation and each expressly disclaim any such obligation, to update publicly any forward-looking statements, whether as a result of new information, future events, changed events or otherwise.

4

Modified Adjustment and Cautionary Statement

Additional InformationIn connection with the proposed combination, CenturyLink filed a registration statement on Form S-4 with the SEC (Registration Statement No. 333-215121), which was declared effective by the SEC on February 13, 2017. CenturyLink and Level 3 have filed a joint proxy statement/prospectus and will file other relevant documents concerning the proposed transaction with the SEC. CenturyLink and Level 3 began mailing the definitive joint proxy statement/prospectus to their respective security holders on or about February 13, 2017. The definitive joint proxy statement/prospectus, dated as of February 13, 2017, contains important information about CenturyLink, Level 3, the proposed combination and related matters. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN CONNECTION WITH THE PROPOSED COMBINATION OR INCORPORATED BY REFERENCE IN THE DEFINITIVE JOINT PROXY STATEMENT/PROSPECTUS CAREFULLY BECAUSE THEY CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain the definitive joint proxy statement/prospectus and the filings that are incorporated by reference in the definitive joint proxy statement/prospectus, as well as other filings containing information about CenturyLink and Level 3, free of charge, at the website maintained by the SEC at www.sec.gov. Investors and security holders may also obtain these documents free of charge by directing a request to CenturyLink, 100 CenturyLink Drive, Monroe, Louisiana 71203, Attention: Corporate Secretary, or to Level 3, 1025 Eldorado Boulevard, Broomfield, Colorado 80021, Attention: Investor Relations..

5

Level 3 Overview

6

Company Overview

Over $8B FY 2016 Total Revenue

Approx. 360 Colocation and Data Center facilities

200,000+ Route Miles of Fiber Globally

Ou

r C

om

pan

y

Approx. $2.9B FY 2016 Adjusted EBITDA

~12,600 Employees

Connecting 60+ Countries and Counting

7

Global ReachOur expansive global network provides a competitive advantage

8

Level 3 Delivers Adaptive Networking

Enabling the journey

to the hybrid cloudConnecting sites, people and

machines in the digital

organization

Cloud Ecosystem Real-Time

Communications

Hybrid Connectivity Security

Protecting and defending

public/private networks

and cloud connections

Providing a reliable and

secure, common

workforce experience

anytime, anywhere

9

Level 3 Strategy

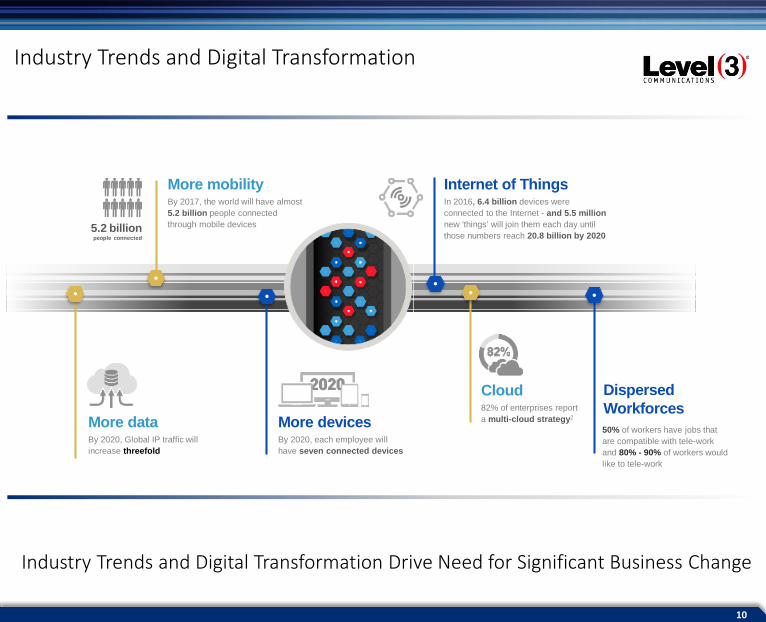

10

5.2 billionpeople connected

By 2017, the world will have almost

5.2 billion people connected

through mobile devices

More mobility

By 2020, each employee will

have seven connected devices

More devices

In 2016, 6.4 billion devices were

connected to the Internet - and 5.5 million

new 'things' will join them each day until

those numbers reach 20.8 billion by 2020

Internet of Things

82% of enterprises report

a multi-cloud strategy2

Cloud

By 2020, Global IP traffic will

increase threefold

More data50% of workers have jobs that

are compatible with tele-work

and 80% - 90% of workers would

like to tele-work

Dispersed

Workforces

Industry Trends and Digital Transformation Drive Need for Significant Business Change

Industry Trends and Digital Transformation

11

Digital Transformation Creates More and More Connections

IT to become more agile to keep up with the pace of change in the constantly changing environment for connections

IT continues to evolve from a back-office necessity to a critical business driver continues to provide opportunities for our business

12

CIO Challenges have Anchored the Level 3 Value Proposition

GROWTH EFFICIENCY SECURITY

Traffic growing

~23%/year• Mobile traffic growing ~57%/year

• ~10B new connected devices

by 2019

IT spend down 1.3% in 2015

DDoS attacks

up 117%

in the past year

13

Sweet Spot for Level 3

Strategic Enterprise

Tier 1

4,000 – 30,000 employees

Tier 2

500-4,000 employees

Tier 3

15-500 employees

30,000+ employees and/or 800 sites

High bandwidth or On-net

Diverse Customer Base

14

Level 3 Strategy

1 2 3 4

FOCUS ON ENTERPRISE CUSTOMERS

EXPAND OUR

NETWORK

DELIVER A SUPERIOR

CUSTOMER EXPERIENCE

EVOLVE OUR PRODUCT

PORTFOLIO

Continue to capture share of

the global communications

market

Invest in our product portfolio

to solve customers’

complex needs

Build directly to our customers to

provide better network

performance

Invest in operational excellence

Strategy to position the company to become the premier provider of global communications services

15

Level 3 Financial Overview

16

$(106)$(165)

$(47)

$251

$626

$1,009

2011 2012 2013 2014 2015 2016

Historical Financial Performance

Note: For definitions and reconciliation of non-GAAP results to GAAP measures used in this presentation can be found at investors.level3.com

Total Revenue($ in millions)

Adj. EBITDA and Adj. EBITDA Margin($ in millions)

Free Cash Flow($ in millions)

5.8x

5.1x4.8x

4.4x

3.8x

3.2x

2011 2012 2013 2014 2015 2016

Leverage Ratio

$4,333

$6,376 $6,313 $6,777

$8,229 $8,172

2011 2012 2013 2014 2015 2016

$958

$1,459 $1,624

$1,895

$2,638

$2,850

22.1%22.9%

25.7%

28.0%

32.1%

34.9%

2011 2012 2013 2014 2015 2016

17

74%

26%

66% 34%

Level 3’s Business is Enterprise Driven

Level 3 continues to be successful in delivering targeted solutions to meet the needs of enterprise customers

1Q14 4Q16

WholesaleEnterprise

1Q11

CNS Revenue $729 M CNS Revenue $1,457 M CNS Revenue $1,934 M

48%

52%

18

Credit Profile Overview

➢ Level 3 continues to focus on prudent balance sheet management

➢ Rating agencies have acknowledged Level 3’s balance sheet improvement, upgrading credit ratings several notches in the past several years

Caa1/B- B3/B- B3/B- B3/B B2/BB- Ba3/BB-

Note: Ratings denote Moody’s and Standard & Poor’s ratings.2016 Pro forma reflects the refinancing of Term Loans completed on February 21, 2017

Ba3/BB

4.0

5.0

5.7 5.6 5.66.0

6.7

8.1 8.07.5

6.8

5.9

4.84.4

7.0x

5.8x

5.1x4.8x

4.4x

3.8x

3.2x

2010 2011 2012 2013 2014 2015 2016 PF

Weighted Avg Maturity (Years) Weighted Avg Cost of Debt (%) Leverage

19

Summary of Financial Data

December 31,

2016

December 31,

2015(1)

December 31,

2016

December 31,

2015(1)

December 31, 2015

Modified (1)(2)

Core Network Services 1,934$ 1,943$ 7,767$ 7,757$ 7,685$

Wholesale Voice Services 98 110 405 472 472

Total Revenue 2,032$ 2,053$ 8,172$ 8,229$ 8,157$

Adjusted EBITDA 709$ 681$ 2,850$ 2,638$ 2,592$

Capital Expenditures (306)$ (330)$ (1,334)$ (1,229)$ (1,219)$

Unlevered Cash Flow 386$ 399$ 1,513$ 1,293$ 1,262$

Free Cash Flow 251$ 226$ 1,009$ 626$ 595$

Network Access Margin 66.5 % 65.5 % 66.7 % 65.6 % 65.4 %

Adjusted EBITDA Margin 34.9 % 33.2 % 34.9 % 32.1 % 31.8 %

Net Income 250$ 3,323$ 677$ 3,433$

Basic Earnings Per Share 0.70$ 9.33$ 1.89$ 9.71$

Weighted-Average Shares

Outstanding (in thousands)359,937 356,274 358,559 353,385

Diluted Earnings Per Share 0.69$ 9.24$ 1.87$ 9.58$

Weighted-Average Shares

Outstanding (in thousands)363,250 359,712 361,472 358,593

Three Months Ended Year Ended

Level 3 Communications Consolidated($ in millions)

(1) The 2015 results have been adjusted to reflect changes made to customer assignments between the wholesale and enterprise channels as of the beginning of 2016.(2) Represents the consolidated results modified to exclude the Company's Venezuelan subsidiary's operations that was deconsolidated as of September 30, 2015, except for Net Income and Basic

and Diluted Earnings per Share.

20

CenturyLink to acquire Level 3

21

Advancing Shared Visions and Strategies

Improve the Lives of Our

Customers by Connecting

them to the Digital World

The Trusted Connection to

the Networked World

• Provide our customers leading

products and services enabled by

the fastest, most reliable

broadband network

• Customer-centric focus delivered

by committed employees

• Build scalable and efficient

network-based services to deliver

industry-leading value

• Operational excellence is our core

value discipline

22

Transaction Overview

Leading Facilities-

Based Enterprise

Communications

Provider

Strong Financial

Profile

Multiple

Opportunities for

Growth

Proven Ability to

Integrate and Meet

/ Exceed Synergy

Targets

● $19bn in pro forma business revenue represents ~76% of total consolidated revenue (1)(2)

● Increases network by 200,000 route miles of fiber, including 64,000 route miles in more than

350 metropolitan areas and 33,000 subsea fiber route miles connecting multiple continents

● On-net buildings expected to increase by nearly 75% to approximately 75,000, including 10,000

buildings in EMEA and Latin America

● Pro forma revenue of $26bn and adjusted EBITDA of $11bn (including synergies) (2)(3)

o Pro forma business revenue of $19bn and $13bn in business strategic revenue (1)(2)

● Accretive to free cash flow in first year following close and significantly accretive on annual run-rate

basis thereafter

● Acceleration of nearly $10bn Level 3 NOLs drives robust free cash flow and significantly lowered

dividend payout ratio

● Pro forma net leverage of less than 3.7x at close (including run-rate synergies) (3)

● Accretive to CenturyLink’s existing growth profile with additional upside opportunities:

o Deploy product portfolio across combined customer bases

o Increased scale of network with dense local metropolitan areas and global reach

● Expected to achieve $975mm in annual run-rate cash synergies

o $850mm opex and $125mm capex synergies targeted

● Track record of strong execution and meeting or exceeding synergy targets

o CenturyLink: Qwest, Embarq; Level 3: tw telecom, Global Crossing

.

(1) Excludes CenturyLink Other Revenues.

(2) Combined balances and metrics represent pro forma results of CenturyLink and Level 3 as of LTM ended June 30, 2016.

(3) Includes expected run-rate cost synergies of $850mm.

23

Compelling for CenturyLink and Level 3 Shareholders

Consideration

and Transaction

Structure

● CenturyLink to acquire Level 3 for $66.50 per share

o 60% stock consideration at $40.00 per share

– Fixed exchange ratio of 1.4286x based on CenturyLink $28.00 per share reference price

o 40% cash consideration at $26.50 per share

Transaction

Value

● Transaction valued at $34bn, including assumption of debt (1)

o Represents a premium of approximately 42% based on Level 3’s unaffected share price (2)

Pro Forma

Ownership

● 51% CenturyLink shareholders

● 49% Level 3 shareholders

Dividend ● Expect to maintain CenturyLink annual dividend of $2.16 per share

Financing ● Financing commitment currently in place

● ~$10.2bn acquisition financing, including $2.0bn undrawn revolver at close

Board /

Leadership

● After the close of the transaction, Glen Post will continue to serve as Chief Executive Officer and

President and Sunit Patel, Executive Vice President and Chief Financial Officer of Level 3, will serve as

Chief Financial Officer of the combined company

● The Chairman of CenturyLink’s Board at the time of the closing of the transaction will continue to serve

as Chairman of the combined company. CenturyLink has agreed to appoint four Level 3 Board members

at closing, one of whom will be a representative of STT Crossing Ltd., a wholly owned subsidiary of

Singapore Technologies Telemedia Pte Ltd (“ST Telemedia”)

Closing ● Both CenturyLink and Level 3 shareholders will have the opportunity to vote on the transaction

o Voting agreement in place with STT Crossing (currently holds approximately 18% of Level 3

outstanding common stock)

● Closing expected by the end of third quarter 2017____________________

Source: Company filings.

(1) Based on $66.50 / Level 3 share; balance sheet data as of June 30, 2016.

(2) Level 3’s unaffected share price of $46.92 as of October 26, 2016.

24

Expansive Domestic and Global Network

8J6H: 851698_1.worInternational Presence

Legend

Level 3 On-net Area with Metro Network

Level 3 On-net Metropolitan Area

Level 3 Owned & Leased Network

CenturyLink Core Fiber

CenturyLink Local Territory

Pro Forma Network Map

Metropolitan

Areas with

Metro Fiber

350

On-Net

Buildings75,000

London

ParisFrankfurt

Dublin

Edinburgh

Madrid

Amsterdam

ZurichMilan

Europe

Hong Kong

Singapore

SeoulTokyo

SydneyPerth

Asia

Johannesburg

Capetown

Nairobi

Dubai

Africa

Rio de JaneiroSão Paulo

Lima

Santiago

Buenos Aires

CaracasBogotá

Latin America

25

Combining Diversified and Complementary Businesses

LTM 2Q’16A Revenue Mix

____________________

Source: Company filings.

(1) Total Revenue excludes CenturyLink Other Revenues.

(2) Total Core Revenue excludes CenturyLink data integration and Other Revenues; treats Level 3’s WVS revenue as Legacy revenue.

26

Combination will provide leading Business Focus and Scale

76%

17%

13% 13%

6%

(3)(2) (4)(1)

$32.5

$18.8

$17.3

$10.6

$8.2

$4.9 $4.7

(2) (4)(3) (5)

Business Focus

Enterprise / SME / Wholesale Revenue as % of Total Revenue (2015A)

Leading Domestic Communications Provider Serving Global Enterprise Customers

Enterprise / SME / Wholesale Revenue ($bn, 2015A)

____________________

Source: Company filings.

(1) Excludes CenturyLink Other Revenues.

(2) Pro forma for TWX acquisition.

(3) Pro forma for the sale of wireline assets to Frontier Communications and Yahoo acquisition.

(4) Pro forma for TWC and Bright House acquisitions.

(5) Excludes other operating revenues.

27

Transaction Synergies

~$685mm

(one-time)

Operating Cost

Savings

Capex

Synergies

Integration

Costs

• Corporate

• Network and Operational Efficiencies

• IT Support

• Purchasing Synergies

• Advertising / Marketing

• Purchasing Synergies

• Realization of Synergies

• Network Integration

~$850mm

annually

~$125mm

annually

Description Amount

CenturyLink and Level 3 have a proven ability to integrate and

meet or exceed synergy targets

Incur majority

by 2019

80% of run-rate within

36 months

100% of run-rate within

36 months

Timing

$975mm Annually in Clear, Achievable Synergies

28

Pro Forma Capital Structure and Financial Policy

Net Debt $19.7 $9.7

2Q'16A LTM Adj. EBITDA (Pre-SBC) 7.0 2.7

Net Leverage 2.8x 3.5x 3.7x

____________________

Source: Company filings.

Note: Dollars in billions.

(1) Excludes Qwest 2056 Notes issued in August 2016.

(2) LTM EBITDA modified to exclude Level 3’s Venezuelan subsidiary's operations that were deconsolidated as of September 30, 2015 .

Pro Forma Capitalization (2Q’16A)

● Combined company’s capital structure benefits from:

o Strong liquidity profile, including $2bn unfunded revolver

o Free cash flow accretion and focus on sustainable free cash flow growth

o Significantly lowered dividend payout ratio

● Long-term leverage target at ~3.0x

● CenturyLink’s strategic review of its data center and colocation business continues, and if completed, cash

proceeds can be used to delever

(1)

29

Pro Forma Financing Structure Overview

Level 3 Financing, Inc.

TLB: $4.6bn

HY Notes: $5.3bn

Qwest Comm. Int. (QCII)

Qwest Capital Funding Inc.

(QCF) HY Notes: $1.0bn

Qwest Corp. (QC) (1)

IG Notes: $7.3bn

Qwest Services Corp

(QSC)

Level 3 Communications, LLC

CenturyLink, Inc.

HY Notes: $8.1bn;

$10.2bn of New Acquisition Debt ($8.2bn funded)

Various CenturyLink

Subs / Others / Capital

Leases: $0.4bn

Embarq Corp. (EQ)

HY Notes/Other: $1.8bnNew Level 3 HoldCo

Level 3 Communications, Inc.

HY Notes: $0.6bn

• Stays in place• No new debt

New Debt

• New acquisition debt expected to receive guarantees from material non-regulated CenturyLink subs

(including Embarq parent) and new Level 3 HoldCo

• Expected pledge of stock from QC and Level 3 Communications Inc.

● Level 3 will not incur or guarantee any acquisition debt

● Based on expected ratings, Change of Control puts will not be triggered

● No consents are required from Lenders or Noteholders for closing the acquisition

____________________

Source: Company filings.

(1) QC is a regulated sub and is a non-guarantor. Includes QC Preferred Notes of $4.4bn. Pro forma for $285mm QC Notes due 2033 called in Q3-2016.

30

Roadmap to Completion

• Key conditions

o Regulatory approvals and customary closing conditions

– HSR Clearance

– FCC Review

– National Security Approvals

– Certain State Regulatory Approvals

– International Filings

o Approval by CenturyLink and Level 3 shareholders

– Voting agreement in place with STT Crossing, a wholly owned subsidiary of ST

Telemedia (currently holds 18% of Level 3)

– Both companies’ stockholders approved the merger on March 16, 2017

• Expected closing by the end of third quarter 2017

31

CenturyLink + Level 3: Transaction to Benefit All Stakeholders

Customers

● Combined presence in over 60 countries, network and fiber capabilities over an owned network that

connects more than 350 metropolitan areas

● Increased bandwidth capacity and additional managed services

● Ability to invest in and further improve its broadband infrastructure, enhancing broadband deployment

speeds for both business and consumer customers

● Ability to offer CenturyLink’s larger enterprise customer base the benefits of Level 3’s global footprint

● Complementary portfolios will allow combined company to offer an even broader range of services and

solutions to meet the demand for more bandwidth and new applications in an increasingly complex

operating environment

Employees

● Opportunity to work for a leading global fiber infrastructure company

● Combining two highly customer-focused organizations to place an even greater emphasis on customer

service

● Provides employees growth and advancement opportunities companies could not offer separately

● Values and unifying principles align and will drive an employee-centric culture

Shareholders

● CenturyLink and Level 3 shareholders to benefit from significant upside potential of combination

● Improved free cash flow will enhance the combined company’s financial flexibility and significantly lower

its payout ratio

● Accretive to free cash flow in first year following close and significantly accretive including run-rate

synergies

● Expected to generate $975mm of annual run-rate synergies

32

Level 3 Fourth Quarter and Full Year Results

33

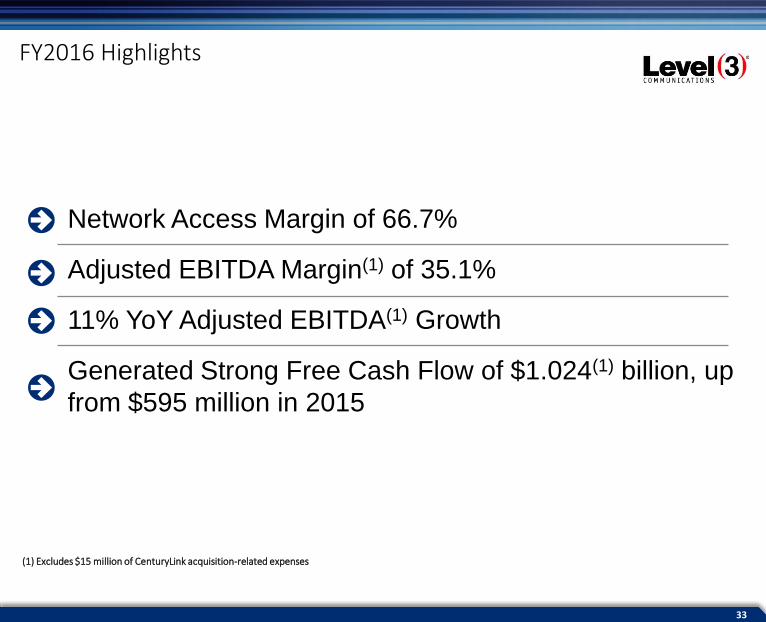

FY2016 Highlights

Network Access Margin of 66.7%

Adjusted EBITDA Margin(1) of 35.1%

11% YoY Adjusted EBITDA(1) Growth

Generated Strong Free Cash Flow of $1.024(1) billion, up

from $595 million in 2015

(1) Excludes $15 million of CenturyLink acquisition-related expenses

34

CNS Revenue

(1) Level 3 measures revenue churn as disconnects of Core Network Services (CNS) monthly recurring revenue as a percentage of CNS revenue. This calculation excludes churn from customers who disconnected existing service in a particular location but replaced it with new services in the same location. The calculation also excludes usage.

CNS Revenue($ in millions)

4Q16 CNS Revenue Performance

Revenue Constant Currency

YoY%YoY%

Total CNS 0.2% (0.5%)

Enterprise 2.9% 2.3%

Enterprise(ex UK Gov’t) 3.4% 3.1%

Wholesale (6.9%) (7.6%)

North America 0.8% 0.8%

Enterprise 3.2% 3.2%

Wholesale (5.8%) (5.8%)

EMEA (7.3%) (15%)

Enterprise (1.9%) (9.4%)

Wholesale (9.4%) (15%)

UK Government (25%) (41%)

Latin America 3.8% 6.9%

Enterprise 10% 14%

Wholesale (16%) (15%)

4Q16 CNS Revenue Churn(1)1.1%

$1,943 $1,934

4Q15 4Q16

35

4Q16 CNS Services Revenue

CNS Revenue by Service Type CNS Revenue by Service Type

1.7%

1.1%

Constant Currency

(1.6%)

(2.0%)

0.3%

(1.0%)

(2.3%)

(2.7%)

As Reported

Constant Currency

As Reported

Constant Currency

As Reported

Constant Currency

As Reported$146M

Colocation &Data Center

Voice Services

$295M

Transport & Fiber

$577M

$916M

IP & Data Services

47%

30%15%

8%

IP & Data

Transport & Fiber

Colocation & Data Center

Voice Services

Note: Growth rates are on a Year-over-Year basis.

4Q16 CNS Services Revenue

36

95%

5%

4Q16 Revenue Mix

CNS Revenue by Region CNS Revenue by Customer Type

82%

9%

9%

North America EMEA Latin America

74%

26%

Enterprise Wholesale

Total Revenue by Currency Total Revenue Mix

USD

GBP

EURBRLOther

CNS

WVS

90%4%2%2%2%

4Q16 Revenue Mix

37

$338 $327

$326 $316

32.3%31.6%

4Q15 4Q16

NRE SG&A NRE and SG&A Expenses % Total Revenue

$643$664$708

$680

65.5%

66.5%

4Q15 4Q16

Network Access Costs Network Access Margin

Network Access Costs & Operating Expenses

Network Access Costs & Margin($ in millions)

Network Related Expenses(NRE) and SG&A(1)

($ in millions)

(1) Excludes non-cash compensation expense of $6 million and $5 million in NRE and $43 million and $30 million in SG&A for 4Q15 and 4Q16, respectively.

Network Access Costs and Operating Expenses

38

$2,592

$2,865

31.8%

35.1%

FY15 FY16

Adjusted EBITDA Adjusted EBITDA Margin

$681

$724

33.2%

35.6%

4Q15 4Q16

Adjusted EBITDA Adjusted EBITDA Margin

Adjusted EBITDA

Fourth Quarter Adjusted EBITDA

($ in millions)

Net Debt to Adjusted EBITDA Leverage Ratio 3.2x

Full Year Adjusted EBITDA

($ in millions)

(3)(2) (2)

(1) Includes $4 million of tw telecom integration-related expenses(2) Excludes $15 million of CenturyLink acquisition-related expenses(3) Modified to exclude the company’s Venezuelan subsidiary’s operations, which were deconsolidated as of September 30, 2015 and includes $32 million of tw telecom integration-related expenses

(1)

Adjusted EBITDA

39

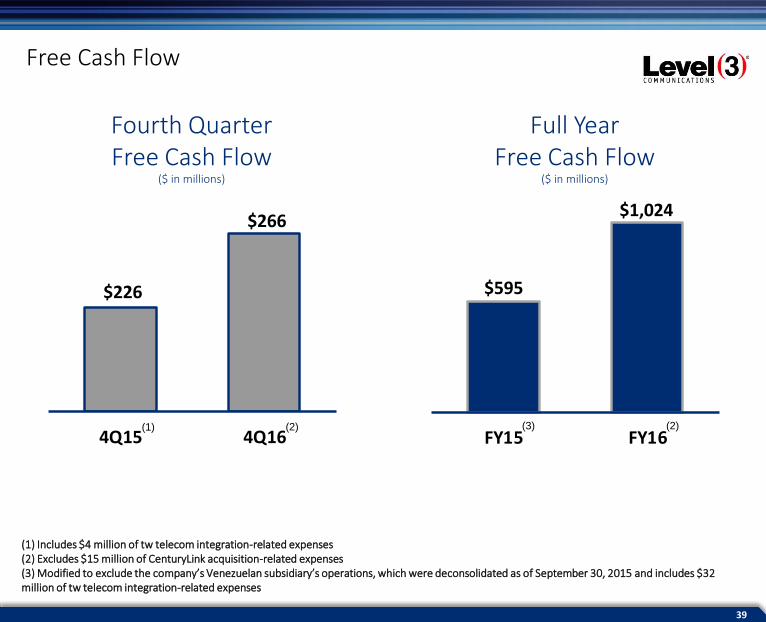

$595

$1,024

FY15 FY16

$226

$266

4Q15 4Q16

Full YearFree Cash Flow

($ in millions)

(3)

Fourth QuarterFree Cash Flow

($ in millions)

Free Cash Flow

(2) (2)(1)

(1) Includes $4 million of tw telecom integration-related expenses(2) Excludes $15 million of CenturyLink acquisition-related expenses(3) Modified to exclude the company’s Venezuelan subsidiary’s operations, which were deconsolidated as of September 30, 2015 and includes $32 million of tw telecom integration-related expenses

Free Cash Flow

40

2017 Business Outlook

Adjusted EBITDA

Free Cash Flow

GAAP Interest Expense

Cash Interest Expense

Capital Expenditures

Depreciation & Amortization

Non-Cash Compensation

Cash Income Tax

$2.94 to $3.00 billion

$1.10 to $1.16 billion

$570 million

$520 million

16% of Total Revenue

$1.35 billion

$170 million

$40 million

Outlook Metric

Full Year Income Tax Rate Approximately 38%

2017 Business Outlook

41

Level 3 Welcomes Your Feedback

Level 3 Communications 1025 Eldorado Boulevard

Broomfield, CO 80021

720-888-2518investors.level3.com

To be the trusted connection to the networked world

Top Related